Europe Biocomposites Market Size, Share, Trends & Growth Forecast Report, Segmented By Fiber, Polymer, End-User, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Biocomposites Market Size

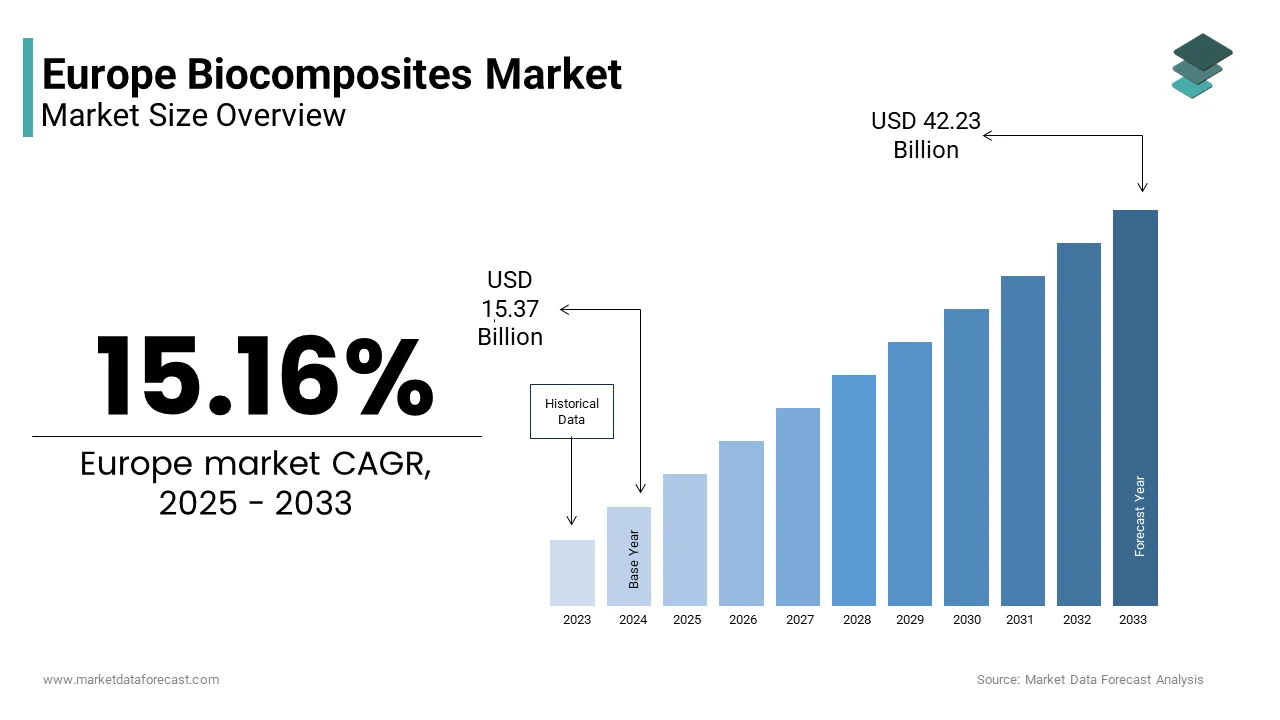

The Europe biocomposites market size was valued at USD 13.34 billion in 2024 and is anticipated to reach USD 15.37 billion in 2025 to USD 42.23 billion by 2033, growing at a CAGR of 15.16% during the forecast period from 2025 to 2033.

Biocomposites are engineered materials that combine natural fibers, such as flax, hemp, jute, and wood, with bio-based or conventional polymer matrices to create sustainable alternatives to traditional plastics and composites. These materials are used in automotive interiors, building panels, furniture, re-packaging, and consumer goods, where reduced carbon footprint and end-of-life biodegradability are prioritized. In 2025, the market operates at the confluence of circular economy poli,c, industrial decarbonization, and consumer demand for eco-conscious products. According to studies, a high percentage of Europeans (often cited around 80-83% in older Eurobarometer surveys) consider environmental impact an important aspect of their purchasing decisions generally. As per the European Environment Agency, the EU generated approximately 42.5 million tonnes of plastic waste in 2022, or about 25.8 million tonnes. This regulatory and behavioral shift positions biocomposites not as niche substitutes but as strategic enablers of Europe’s material transition toward climate neutrality and resource resilience.

MARKET DRIVERS

Stringent EU Regulations Mandating Sustainable Materials in Automotive and Construction

European policy frameworks are compelling industries to replace petroleum-based composites with renewable alternatives, which accelerates the growth of the Europe biocomposites market. According to research, upcoming EU regulations on end-of-life vehicles require automakers to ensure higher recyclability rates, driving material innovation and circular design integration across the automotive manufacturing sector. Leading automotive companies in Europe are increasingly adopting natural fiber-reinforced composites made from materials such as flax, hemp, and kenaf to reduce vehicle weight and improve sustainability in interior components. These regulatory levers transform biocomposites from optional innovations into compliance necessities, which ensures sustained industrial demand across two of Europe’s largest material-consuming sectors.

Rising Consumer and Corporate Demand for Circular and Low-Carbon Products

European consumers and brands are increasingly rejecting single-use plastics and fossil-derived materials in favor of bio-based alternatives, which in turn bolsters the expansion of the Europe biocomposites market. A notable share of EU citizens support the mandatory use of renewable materials in everyday products, as per sources. This sentiment is mirrored by corporate sustainability commitments. Companies use biocomposite trays, furniture frames, and sports equipment made from flax biopolyethylenene. This market demand is driven not by regulation, but by brand reputation and customer loyalty, which creates opportunities for premium pricing for certified biocomposites that offer demonstrable life cycle benefits and end-of-life compostability.

MARKET RESTRAINTS

Performance Limitations in Moisture Resistance and Long-Term Durability

Inherent technical constraints restrict their use in demanding applications and hinder the growth of the Europe biocomposites market. Natural fibers are hydrophilic, making biocomposite panels susceptible to swelling, warping, and microbial degradation in humid environments. According to research, flax reinforced composites lose tensile strength after notable hours of high humidity exposure, unacceptable for automotive or outdoor construction use. Mitigation through coupling agents and coatings is possible, yet this approach raises costs and adds complexity. Apart from these, thermal stability remains a challenge. Most bio-based matrices degrade above 180°C, limiting compatibility with standard injection molding processes. Adoption will only move beyond non-critical interior and short-life cycle applications when material science provides improved moisture resistance and thermal performance.

High Production Costs and Fragmented Supply Chain for Natural Fibers

The cost of biocomposites remains higher than conventional glass fiber reinforced plastics due to immature supply chains and low economies of scale, which in turn inhibits the expansion of the Europe biocomposites market. Europe produces fewer metric tons of technical flax annually, insufficient to meet projected demand, which forces reliance on imports from China and Eastern Europe with inconsistent quality. The fragmentation increases lead times and price volatility. Mass industrial adoption of biocomposites depends on coordinated investment in agronomic research, fiber processing hubs, and standardized grading protocols to ensure cost parity and reliable supply.

MARKET OPPORTUNITIES

Integration into EU Green Public Procurement and Eco Design Frameworks

"The European Union’s Green Public Procurement criteria, which prioritize materials with high bio-based content and low carbon footprints in government tenders for furniture, vehicles, and infrastructure, are setting up new opportunities for the growth of the Europe biocomposites market. According to the European Commission, public procurement in the EU is a significant economic driver, valued at approximately €2 trillion annually (14% of EU GDP). Simultaneously, the Ecodesign for Sustainable Products Regulation requires digital product passports that disclose material composition and recyclability, which favours traceable bio-based inputs. Companies have developed biocomposite sheets compliant with these standards for desks and cabinetry. This policy-driven demand reduces risks of early adoption and provides stable revenue for producers scaling up production capacity under EU industrial strategy support.

Development of Hybrid Biocomposites Using Recycled Polymers and Agricultural Waste

Innovators are creating next-generation biocomposites that blend natural fibers with post-consumer recycled plastics or bio-based resins from non-food biomass, which drives the expansion of the Europe biocomposites. This enhances sustainability without sacrificing performance. The European Union's BIO4SELF project developed fully bio-based self-reinforced polymer composites (SRPC) using polylactic acid (PLA), which can be used for automotive applications. The project aimed to create a material that is entirely bio-based, easily recyclable, and whose stiffness can rival commercial self-reinforced polypropylene composites. These hybrid approaches address both plastic waste and rural economic development while improving cost and mechanical properties. The mandatory nature of life cycle assessment under the CSRD means that dual benefit materials inherently gain a competitive advantage within B2B markets.

MARKET CHALLENGES

Lack of Standardized Certification End-of-Life Infrastructure

The region lacks harmonized standards for defining, measuring, and verifying the bio-based content, biodegradability, and compostability of biocomposites, which challenges the growth of the Europe biocomposites market. This creates confusion among buyers and regulators. This gap allows greenwashing and large-scale procurement. Most biocomposites end up in landfills or incinerators, negating their environmental benefit. "The circular promise of biocomposites remains unattainable without mandatory labeling, harmonized testing protocols, and investment in organic waste processing. The market cannot achieve true credibility or scalability until policymakers address this loophole, which is currently hindering the benefits of strong upstream innovation.

Competition from Advanced Recycled Plastics and Alternative Bio Materials

Intense competition from mechanically and chemically recycled plastics that offer similar carbon reductions without performance trade-offs hampers the expansion of the Europe biocomposites market. In addition, novel bio-based polymers like polyhydroxyalkanoates (PHA) and polylactic acid (PLA) provide fully biodegradable alternatives for packaging and disposable goods. Companies are scaling these materials with superior moisture resistance and processability. The diversification of sustainable material options fragments demand and pressures biocomposite producers to prove unique value, either through superior life cycle metrics, lower cost, or niche performance attributes. The market risks being displaced by more adaptable or scalable competitors if differentiation is absent.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2023 |

| Forecast Period | 2025 to 2033 |

| CAGR | 15.16% |

| Segments Covered | By Fiber, Polymer, End-User, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden. |

| Market Leaders Profiled | Fiberon LLC, FlexForm Technologies, Trex Company, Universal Forest Products, Inc., Meshlin Composites ZRT, Tecnaro GmbH, and Nanjing Jufeng Advanced Materials Co., Ltd. |

SEGMENTAL ANALYSIS

By Fiber Insights

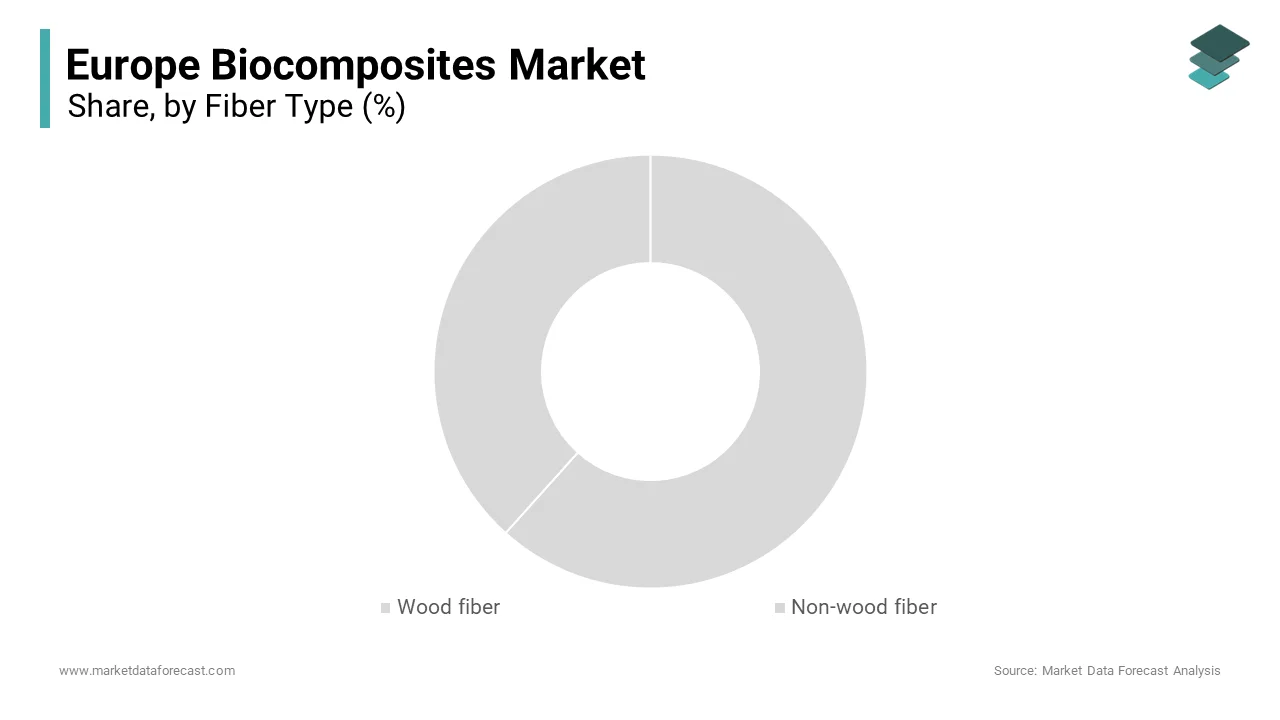

The wood fiber segment dominated the Europe biocomposites market and accounted for a 58.7% share in 2024. The dominance of the wood fiber segment is attributed to the continent’s abundant forestry resources, established supply chains, and compatibility with existing wood processing infrastructure. Millions of hectares of forest cover Europe, a portion of which is sustainably managed under PEFC and FSC certification, which provides a steady stream of sawmill residues and pulp byproducts for fiber extraction. Companies integrate wood fiber into construction boards, automotive door modules, and furniture with consistent quality and low moisture variability compared to agricultural fibers. Apart from these, wood fiber composites align with the EU Timber Regulation and circular economy goals by valorizing waste streams. This combination of resource availability, industrial integration, and regulatory alignment ensures wood fiber remains the foundational input for Europe’s biocomposites sector.

The non-wood fiber segment is estimated to register the fastest CAGR of 19.4% from 2025 to 2033 due to superior mechanical properties and strong policy support for agricultural diversification. Flax fibers exhibit tensile strength comparable to glass fiber, yet with lower density, making them ideal for lightweight automotive parts. According to research, thousands of hectares of industrial hemp and flax were cultivated in the EU, supported by subsidies for non-food crops. Some of the companies use flax-reinforced biocomposites in seat backs and parcel shelves, achieving weight reduction versus conventional plastics. Apart from these, non-wood fibers sequester carbon during growth and require minimal irrigation, which enhances life cycle credentials. The EU’s Farm to Fork Strategy encourages better soil health and crop rotation, which means these fibers function both as industrial inputs and as beneficial regenerative agricultural products.

By Polymer Insights

The synthetic polymer matrices segment held a substantial share of the Europe biocomposites market in 2024. Their superior processability, compatibility with existing manufacturing equipment, and balanced cost performance ratio fuel the growth of the synthetic polymer matrices segment. Most European injection molding and extrusion lines are calibrated for synthetic polymers, making the transition to biocomposites seamless when natural fibers are added as fillers. As per sources, a notable share of automotive biocomposite parts use polypropylene matrices due to their impact resistance, thermal stability, and recyclability within existing streams. Apart from these, synthetic matrices allow precise tuning of mechanical properties, vital for structural applications in construction and transport. These hybrids offer a practical drop-in solution that provides bio-content without requiring any retooling, despite not being entirely bio-based. This industrial pragmatism ensures synthetic matrices remain the dominant binder despite growing interest in fully renewable alternatives.

The natural polymer matrices segment is anticipated to witness the fastest CAGR of 21.8% from 2025 to 2033, owing to corporate net zero commitments and tightening regulations on fossil content in packaging and disposable goods. According to research, many major European consumer brands require some portion of bio-based content in primary packaging. Companies use PLA flax composites for yogurt cups and coffee capsules that are industrially compostable under EN 13432. Advances in polymer blending have improved moisture resistance. The increasing adoption of life cycle assessments highlights the inherent advantage of natural matrices: they deliver verifiable carbon reductions that synthetics simply cannot, which makes them the superior material for premium eco-friendly offerings.

By End-Use Industry Insights

The building and construction segment led the Europe biocomposites market and accounted for a 42.8% share in 2024. The dominance of the building and construction segment is because of the sector’s urgent need to reduce embodied carbon while meeting energy efficiency mandates. Biocomposite insulation panel,s cladding boards, and interior partitions made from wood fiber biopolypropylene offer thermal performance comparable to conventional materials with lower carbon footprints. Companies integrate biocomposites into drywall and acoustic panels. Apart from these, public procurement policies mandate minimum bio content in public infrastructure projects. The construction sector, a major contributor to EU CO₂ emissions, stands as the largest market for sustainable building materials, a trend driven primarily by public policy.

The transportation segment is likely to experience the fastest CAGR of20.6% from 2025 to 2033, owing to stringent vehicle lightweighting targets under the EU’s CO₂ emission standards for cars and vans. Every reduction in vehicle weight yields an improvement in fuel efficiency, making biocomposites critical for compliance. Automakers are increasingly using natural fiber-reinforced biocomposites made from flax and hemp in vehicle interiors to reduce overall component weight and improve material sustainability. As per sources, automotive prototypes demonstrate the potential of biocomposite materials to significantly lower vehicle weight, which supports broader industry goals for efficiency and emissions reduction. The EU’s End of Life Vehicles Directive further incentivizes the use of recyclable and bio-based materials. As electric vehicles prioritize range extension through weight reduction, biocomposites transition from niche to mainstream in automotive design.

COUNTRY ANALYSIS

Germany Biocomposites Market Analysis

Germany outperformed other regions in the Europe biocomposites market and captureda 23.5% share in 2024. Its world-leading automotive sector and advanced materials engineering drive the demand for biocomposites in Germany. Companies collaborate with research institutes such as Fraunhofer to develop flax and wood fiber composites with automotive-grade durability. The country also hosts major polymer producers that supply bio matrices to composite manufacturers. Strong policy support for industrial clustering, combined with rigorous engineering practices, has positioned Germany as the arbiter of technical standards and performance benchmarks for biocomposites in Europe.

France Biocomposites Market Analysis

France was the second-largest country in the Europe biocomposites market and captured an 18.5% share in 2024 because of its prominence in industrial hemp and flax cultivation and proactive bioeconomy policies. According to studies, thousands of hectares of flax and hemp were grown, supported by CAP subsidies for food crops. Companies use these fibers in automotive biocomposites for Renault and Peugeot. Public procurement rules emphasize bio-based content in state vehicle fleets and public furniture. This fusion of agricultural output, industrial demand, and policy ambition positions France as Europe’s agro-industrial biocomposites pioneer.

Italy Biocomposites Market Analysis

Italy remains a notable country in the Europe biocomposites market, which is fueled by its globally renowned furniture and design sector’s shift toward sustainable materials. According to research, a portion of premium furniture brands now offer biocomposite collections using wood flour biopolyethylene for tables, chairs, hair, and shelving. Companies collaborate with chemical firms to develop aesthetically refined yeco-certified products for European and global markets. Apart from these, the National Recovery and Resilience Plan includes funding for circular material innovation in small and medium enterprises. Italy is capitalizing on biocomposites to create a unique market proposition, which melds superior design and export orientation with both environmental and competitive benefits.

Sweden Biocomposites Market Analysis

Sweden witnessed moderate growth of the Europe biocomposites market due to its integration of biocomposites into green building and public infrastructure. Companies use locally sourced spruce and birch fibers in construction panels and furniture with full life cycle transparency. The country’s initiative provides tax incentives for companies using agricultural or forestry residues in durable goods. This holistic approach, where policy procurement and industry align around carbon neutrality, positions Sweden as a model for systemic biocomposite adoption in the built environment.

Netherlands Biocomposites Market Analysis

The Netherlands is likely to expand in the Europe biocomposites market from 2025 to 203,3, owing to its serving as a hub for circular material innovation across sectoral collaboration. Many biocomposite startups operate in the country, focusing on hybrid materials from agricultural waste and recycled polymers. Companies partner with Dutch universities to develop flax PLA composites for packaging and automotive use. The Port of Rotterdam hosts Europe’s largest bio-based material cluster with shared processing and testing infrastructure. This ecosystem of policy supports innovation and logistics, making the Netherlands a critical incubator for next-generation biocomposites with continental scalability.

COMPETITIVE LANDSCAPE

The Europe biocomposites market features a dynamic mix of large forest industry incumbents, specialized material innovators, and agile startups. Competition is defined not by price alone but by fiber traceability, mechanical performance, and alignment with EU regulatory frameworks. Global players leverage scale and integration, while European firms differentiate through local sourcing, circular design, and policy alignment. The market remains fragmented by application, with automotive construction and consumer goods each demanding distinct material specifications and certification pathways. High entry barriers exist due to the need for processing expertise, fiber consistency, and application validation—yet startups thrive in niche domains like high-performance flax composites or agricultural waste valorization. Public funding through Horizon Europe and national recovery plans further shapes the landscape by de-risking innovation. Overall, the market rewards those who view biocomposites not as generic substitutes but as engineered solutions that deliver verified environmental and functional value within Europe’s circular economy vision.

KEY MARKET PLAYERS

A few of the market players in the Europe biocomposites market include

- Fiberon LLC

- UPM-Kymmene Oyj

- Stora Enso Oyj

- Bcomp Ltd

- FlexForm Technologies

- Trex Company

- Universal Forest Products, Inc

- Meshlin Composites ZRT

- Tecnaro GmbH

- Nanjing Jufeng Advanced Materials Co., Ltd.

Top Players In The Market

- UPM-Kymmene is a Finnish forest industry leader that plays a pivotal role in the Europe biocomposites market through its UPM BioComposites business unit. The company produces wood fiber reinforced polypropylene compounds used in automotive, building materials, and consumer goods across the continent. UPM has strengthened its position by leveraging its integrated forestry and pulp operations to ensure e traceable, sustainable fiber supply. These initiatives reflect UPM’s global strategy of transforming renewable wood into high-performance materials that replace fossil-based plastics while serving customers in multiple countries with certified circular solutions.

- Stora Enso is a Finnish-Swedish biomaterials company that contributes significantly to the Europe biocomposites market through its DuraSense product line. The company combines wood fibers from sustainably managed forests with bio-based and recycled polymers to create injection moldable compounds for automotive construction and packaging applications. Stora Enso has reinforced its market presence by partnering with major European carmakers and furniture brands to co-develop certified low-carbonrbonn components. Stora Enso is a reliable catalyst for Europe's material transition, embedding robust circularity traceability and industrial scalability into its wide range of offerings.

- Bcomp is a Swiss technology innovator that has emerged as a key player in high-performance natural fiber composites for premium automotive and sports applications. The company’s proprietary ampliTex and powerRibs technologies use flax fibers to create lightweight, stiff, and vibration-damping materials that outperform conventional composites in specific metrics. Bcomp has strengthened its European footprint by supplying interior panels to BMW, Polestar, and McLaren while expanding production in Fribourg. This focus on operation-driven composites allows Bcomp to command premium positioning and influence material standards in high-value sectors globally.

Top Strategies Used By The Key Market Participants

Key players in the Europe biocomposites market pursue five core strategies to drive adoption and ensure competitiveness. Fi integrates vertically by securing sustainable fiber sources through owned forests or long-term agricultural partnerships to ensure supply stability. Secondly, they develop hybrid formulations that blend natural fibers with recycled or bio-based polymers to balance performance cost and circularity. Thirdly, they invest in application engineering support to help customers redesign parts for biocomposite compatibility without retooling. Fourth, they obtain third-party certifications such as the OK Biobased EU Ecolabel and Cradle to Cradle to validate environmental claims and meet procurement requirements. FiFifththey collaborate with automotive OE, Ms construction firms, and designers to co-innovate application-specific solutions that demonstrate measurable carbon and weight savings. These strategies reflect a market where technical credibility, proof, and industrial integration are decisive success factors.

MARKET SEGMENTATION

This research report on the Europe biocomposites market is segmented and sub-segmented into the following categories.

By Fiber Type

- Wood fiber

- Non-wood fiber

By Polymer Type

- Synthetic

- Natural

By End-Use Industry

- Building & Construction

- Transportation

- Consumer Goods

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is driving growth in the Europe Biocomposites Market?

The Europe Biocomposites Market is expanding due to the EU Green Deal, Circular Economy Action Plan, and corporate net-zero commitments—pushing automotive, construction, and packaging sectors to replace glass-fiber composites with natural fiber-reinforced alternatives.

Which natural fibers dominate the Europe Biocomposites Market?

Flax, hemp, and wood flour are the most used—thanks to strong agricultural supply in France, Germany, and the Benelux region, plus their favorable mechanical properties and low carbon footprint in the Europe Biocomposites Market.

How is the automotive industry influencing the Europe Biocomposites Market?

OEMs like BMW, Stellantis, and Volvo are integrating biocomposites into door panels, dashboards, and trunk liners to cut vehicle weight and lifecycle emissions—making automotive the largest end-use segment in the Europe Biocomposites Market.

Are biocomposites cost-competitive with traditional composites?

Not yet at parity—but with rising fossil-based resin prices and EU carbon pricing, the total cost gap is narrowing, especially when factoring in end-of-life recyclability and ESG reporting benefits in the Europe Biocomposites Market.

Which countries lead the Europe Biocomposites Market?

Germany (automotive innovation), France (hemp/flax farming and processing), Italy (design-driven applications), and the Netherlands (circular material hubs) are at the forefront of the Europe Biocomposites Market.

What are the main technical challenges in the Europe Biocomposites Market?

Moisture sensitivity, inconsistent fiber quality, and limited high-temperature performance restrict use in structural applications—driving R&D into compatibilizers, hybrid fibers, and bio-based resins in the Europe Biocomposites Market.

How does EU regulation support biocomposites?

While no direct mandates exist, the EU Ecodesign for Sustainable Products Regulation (ESPR) and End-of-Life Vehicle (ELV) Directive incentivize recyclable, bio-based content—giving biocomposites a strategic edge in the Europe Biocomposites Market.

Is there demand beyond automotive and construction?

Yes—consumer goods (furniture, electronics casings), sports equipment, and agricultural trays are emerging segments, leveraging biocomposites for brand storytelling and circular design in the Europe Biocomposites Market.

Are biocomposites truly recyclable or compostable?

Most are not compostable—they’re designed for mechanical recycling or energy recovery. True circularity requires mono-material designs, which are still in pilot stages across the Europe Biocomposites Market.

What’s the outlook for the Europe Biocomposites Market through 2030?

Strong growth (CAGR ~9–11%) is expected, fueled by policy, brand sustainability targets, and advances in fiber treatment—positioning the Europe Biocomposites Market as a cornerstone of the EU’s bioeconomy strategy.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com