Europe Bionematicides Market Size, Share, Trends & Growth Forecast Report, Segmented By Type, Crop Type, Form, Mode of Application, Infestation And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Bionematicides Market Size

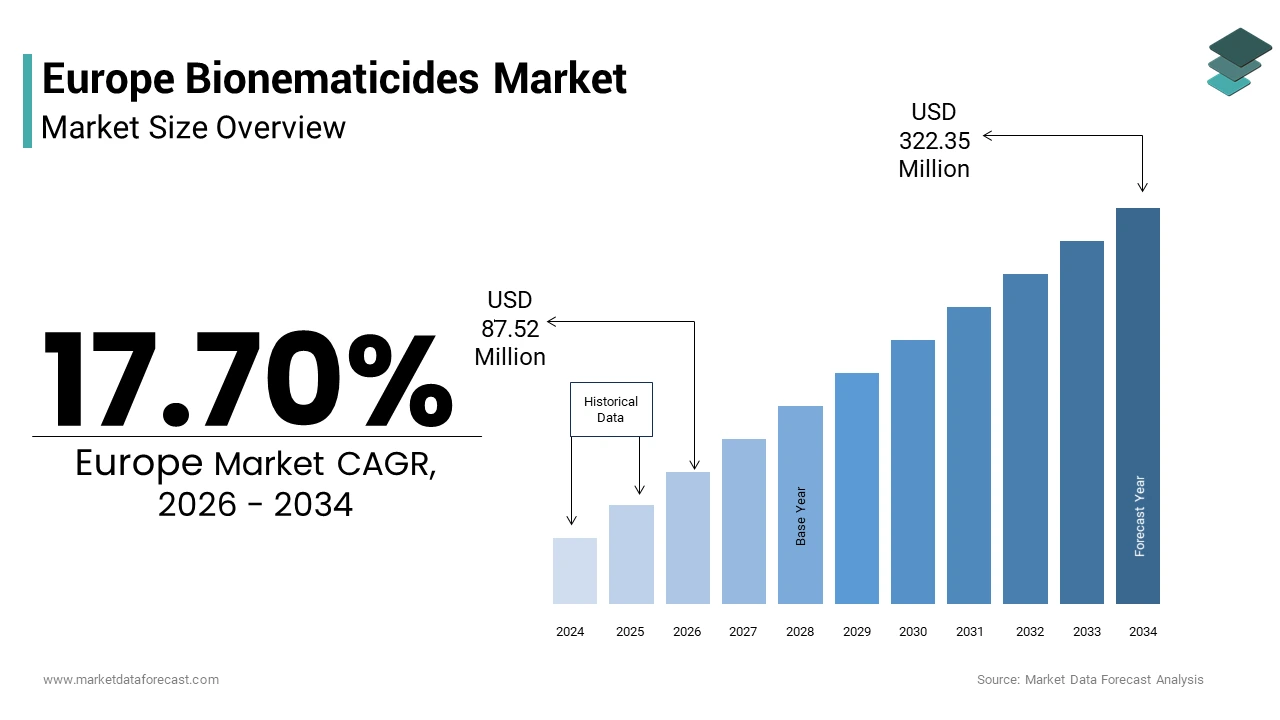

Europe's bio-nematicides market was valued at USD 74.36 million in 2025 and is anticipated to reach USD 87.52 million in 2026 and USD 322.35 million by 2034, growing at a CAGR of 17.70% during the forecast period from 2026 to 2034.

Current Introduction of the European Bionematicides Market

Bionematicides are biological pest control agents used to manage plant-parasitic nematodes (PPNs), such as root-knot and cyst nematodes, which damage crop roots and reduce yields. Unlike synthetic nematicides, which face increasing regulatory restrictions due to environmental and human health concerns, bionematicides offer a targeted, biodegradable, residue-free alternative aligned with the European Union’s sustainable agriculture agenda. These products function through mechanisms such as parasitism, antibiosis, or induced systemic resistance, and are applied via seed treatment, soil drench, or drip irrigation. As per Eurostat, over 155 million hectares of land were used for agricultural production (Utilised Agricultural Area) in the European Union in 2024. Root knot and cyst nematodes infest an estimated 6 to 20 percent of global crops (with higher losses in specific high-value, intensive EU crops), including potatoes, tomatoes, and sugar beets. Besides, the European Food Safety Authority (EFSA) is conducting ongoing assessments of many active substances under Regulation (EC) No 1107/2009, with numerous conventional nematicides (such as metham, oxamyl, and ethoprophos) undergoing phase-outs or having restricted approvals, causing significant pressure on high-value crop production, particularly in the wake of the proposed Sustainable Use of Plant Protection Products (SUR) framework. These ecological and regulatory pressures have positioned bionematicides not as niche supplements but as essential components of integrated pest management strategies across Europe’s evolving agricultural landscape.

MARKET DRIVERS

Stringent EU Regulations Phasing Out Conventional Nematicides

The progressive restriction of synthetic chemical nematicides under European Union pesticide legislation serves as a primary accelerator for the European bionematicides market. Under Regulation (EC) No 1107/2009, the European Commission has aggressively restricted synthetic nematicides. Recent non-renewals in 2024 and 2025 include oxamyl (with use ending in 2024/early 2025) and metribuzin. These withdrawals were primarily driven by identified risks to groundwater and non-target organisms. As of 2026, EFSA’s multi-annual programming has successfully transitioned several high-risk substances to non-renewal status, with several "Candidates for Substitution" (CfS) undergoing final safety peer reviews to determine phase-outs by 2027–2028. This regulatory vacuum compels farmers to seek compliant alternatives without compromising yield protection. German potato growers are increasingly adopting Integrated Pest Management (IPM). While exact adoption percentages vary by region, the BVL has emphasized the expansion of biological controls (such as Purpureocillium lilacinum) to replace older organophosphates. Similarly, France’s Ecophyto 2030 plan remains a primary driver for the bionematicide market, providing funding for research and development into non-chemical alternatives for vineyards and vegetable production to reach the synthetic reduction goal by 2030. These policy-driven displacements create a structural and irreversible shift toward biological solutions, transforming regulatory compliance into a core market growth engine across EU member states.

Expansion of High Value Horticulture and Protected Cropping

The rapid growth of protected agriculture and high-value horticultural production in the region has intensified demand for effective and residue-free nematode control, which directly propels the European bionematicides market. According to 2024 EU data, fresh vegetable production (including tomatoes, peppers, and cucumbers) increased by 6% between 2023 and 2024, with Italy, Spain, and the Netherlands remaining the leading producers. While greenhouse areas in some regions saw consolidation, technological advancements have driven higher yields, particularly in tomatoes, in the Netherlands. These crops are highly susceptible to root knot nematodes, and the enclosed nature of greenhouses limits crop rotation and soil fumigation options. Consequently, growers prioritize biological agents that can be safely applied through drip irrigation without phytotoxicity or residue accumulation. The Dutch Agricultural Census indicates a high adoption rate of IPM in greenhouses, with very large farms accounting for a significant share of the total added value and driving sustainability and innovation. Additionally, the EU’s Green Deal Farm to Fork Strategy promotes residue-free produce for domestic and export markets, with retailers like Edeka and Carrefour requiring biological pest control documentation for premium vegetable lines. This convergence of agronomic necessity, market access requirements, ts and environmental stewardship establishes horticulture as a high adoption and high value segment for bionematicide innovation and deployment.

MARKET RESTRAINTS

Limited Field Efficacy and Inconsistent Performance Under Variable Conditions

The variable field performance of biological agents due to environmental sensitivity and complex soil microbiology inhibits the growth of tEuropeanope bionematicides market. Unlike synthetic nematicides, which offer broad spectrum and predictable knockdown, bionematicides, particularly fungal and bacterial strains, require specific moisture temperature and pH conditions to establish and exert control. Trials evaluating Paecilomyces lilacinus products against root-knot nematodes show varying levels of suppression depending on the location, with higher efficacy observed in certain European soil types compared to others. This inconsistency undermines grower confidence and complicates recommendation protocols. Furthermore, the European Plant Protection Organisation indicates that the success of biological control agents is heavily dependent on precise application timing and compatibility with co-applied fertilizers and pesticides, as improper management is a leading cause of performance failure. Regulatory approval processes also do not fully account for these ecological variables, leading to product authorizations that overstate real-world performance. Bionematicides will not achieve commercial-grade reliability in large-scale, rain-fed systems until formulation technology improves their shelf life, soil persistence, and environmental buffering.

Complex and Costly Regulatory Approval Pathways

Disproportionately burdensome and expensive regulatory requirements treat biological agents similarly to synthetic pesticides, despite their lower risk profile, which hinders the expansion of the European bionematicides market. The process for registering bionematicide active substances requires significant financial investment and time, creating obstacles for smaller companies. Data requirements, including extensive toxicology and environmental studies, may be considered unnecessary for naturally occurring microorganisms. These regulatory challenges contribute to manufacturers abandoning promising bionematicide candidates. Furthermore, mutual recognition of approvals across member states remains inefficient, despite the zonal system, a product approved in Germany may face additional data requests in France or Italy, thereby delaying market access. This regulatory asymmetry stifles innovation and limits the diversity of biological solutions available to farmers. Bionematicides will stay hindered by market constraints that empower established, large-scale agrochemical companies over nimble startups, unless a risk-appropriate, Green Deal-aligned pathway is implemented.

MARKET OPPORTUNITIES

Integration into Precision Agriculture and Digital Farming Platforms

The convergence of bionematicides with precision agriculture technologies provides a major opening to enhance efficacy monitoring and adoption, which is anticipated to create new opportunities for thEuropeanpe bionematicides market. As per research, a portion of EU farms now use GPS-guided equipment and soil sensors, creating infrastructure for targeted biological applications. Companies are developing bionematicide formulations compatible with variable rate technology and fertigation systems, enabling site-specific deployment only where nematode pressure is confirmed via DNA soil testing. Academic institutions and private enterprises are collaborating to incorporate predictive mapping tools into agricultural software to better manage soil-borne pests. The integration of historical productivity data and remote sensing information allows for more localized assessments of biological risks within cultivation areas. Digital management platforms are increasingly featuring dedicated modules that suggest specific biological treatment protocols based on identified soil conditions. Agricultural technology frameworks are shifting toward automated systems that guide the application of biological agents. This data-driven approach reduces input waste, improvecost-benefitit perception, and generates performance evidence that supports regulatory dossiers. Integrating bionematicides into digital decision support systems transforms nematode management from reactive responses to proactive, predictive strategies, aligning biological solutions with European smart farming trends.

Public Funding for Biocontrol Innovation Under Horizon Europe

Substantial public investment through the European Union’s Horizon Europe research program is accelerating the development and validation of next-generation bionematicides. This offers fresh possibilities for the expansion of the European bionematicides market. European research funding is increasingly supporting projects centered on biological methods for managing pests, with a notable emphasis on initiatives targeting nematodes in crops. A collaborative effort involving research institutions and small-to-medium enterprises is exploring the use of fungi that colonize plant roots and release substances to defend against nematode attacks. Preliminary field assessments indicate that these fungal applications can substantially reduce nematode-induced gall formation without negatively affecting crop yield. Research initiatives are demonstrating that specific bacterial strains can promote nutrient uptake while simultaneously suppressing nematode populations. These publicly funded partnerships de-risk R&D for small innovators, provide field validation data required for registration,n and build scientific credibility among skeptical agronomists. EU investments in biocontrol are fueling a transition toward more robust bionematicide solutions, ensuring that scientific breakthroughs reach commercial scale to benefit Europe’s diverse farming landscapes.

MARKET CHALLENGES

Lack of Standardized Efficacy Testing and Performance Metrics

The absence of harmonized protocols to evaluate and compare product performance is a persistent issue in the European bionematicides market. This leads to inconsistent claims and eroded trust among end users. The assessment of bionematicide effectiveness is characterized by a high degree of variation in methodologies across different locations, including differences in the types of crops, the timing of evaluations, and the density of nematode inoculation. This lack of standardized testing makes it difficult to compare results across different trials and complicates the process of conducting meta-analyses for regulatory purposes. Variations in trial design contribute to inconsistencies in the reported efficacy of the same active ingredient, which can create confusion for growers and agronomists attempting to assess product performance. Furthermore, unlike synthetic pesticides, which have standardized dose-response curves, bionematicides often exhibit nonlinear responses where higher concentrations do not guarantee better control. The lack of official EU guidelines for biological nematicide testing, despite repeated calls from the European Biocontrol Manufacturers Association, allows substandard products to enter the market with inflated claims. Mainstream agricultural adoption will be hindered until the EU establishes standardized testing and realistic performance benchmarks to ensure scientific rigor and transparency.

Insufficient Technical Knowledge Among Agricultural Advisors

The limited understanding and training of agricultural extension agents and crop advisors, who influence farm decisions, is also a major barrier to the European insecticide market. Agricultural advisors in some European areas demonstrate low confidence in suggesting bionematicides because they are not familiar with how they work, how to apply them, or whether they can be mixed with other products. This lack of knowledge often leads to incorrect use, like mixing biologicals with incompatible products that reduce their effectiveness. Advisors frequently prefer well-known synthetic options over biological ones due to these knowledge gaps, and the limited attention given to biologicals in national training programs supports the ongoing use of traditional chemical methods. Even in progressive markets like the Netherlands, advisors report insufficient access to field demonstration plots and peer-reviewed case studies. The full potential of bionematicides will not be reached without targeted knowledge transfer through EU-funded advisor academies, regional demonstration farms, and digital training modules. Bridging this extension gap is essential to translate regulatory and technological advances into actual field-level adoption across Europe’s diverse farming communities.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 17.70% |

| Segments Covered | By Type, Crop Type, Form, Mode of Application, Infestation, and Region. |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, c & Rest of Europe |

| Market Leaders Profiled | Bayer CropScience AG, Monsanto Company, BASF SE, Certis USA L.L.C, Syngenta AG, FMC Corporation, Dow AgroSciences LLC, Valent BioSciences Corporation, and Marrone Bio Innovations, Inc. |

SEGMENTAL ANALYSIS

By Type Insights

Tmicrobialals segment was the top-performing segment of the European bionematicides market by accounting for a substantial share in 2025. The prominence of the microbial segment is driven by proven field efficacy, compatibility with organic farming standards, and alignment with EU regulatory preferences for naturally occurring active substances. This category includes living organisms such as Bacillus firmus, Purpureocillium lilacinum, and Paecilomyces lilacinus that parasitize or inhibit plant parasitic nematodes through direct contact or metabolite production. An additional driver is the scientific validation and registration success of microbial strains under EU pesticide legislation. As per a study, many microbial species have received full or provisional approval for nematode control since 2020, compared to only a few biochemicals. Products like VOTiVO (based on Bacillus firmus) are now standard in potato and sugar beet programs across Northern Europe due to consistent yield protection. Additionally, microbials integrate seamlessly into integrated pest management systems, unlike many biochemicals that degrade rapidly or lack residual activity. This combination of regulatory acceptance, agronomic reliability, and system compatibility solidifies microbials as the cornerstone of Europe’s biological nematode control strategy.

The biochemicals segment is expected to exhibit a noteworthy CAGR of 11.3% from 2026 to 2034 due to the rising demand for residue-free and non-living solutions in organic and export-oriented horticulture. This category includes plant-derived compounds such as neem extracts, chitosan, and harpin proteins that disrupt nematode behavior or induce plant defense responses without toxic residues. Unlike microbials, which require specific storage and handling conditions, biochemicals offer greater shelf stability and ease of tank mixing, appealing to small and medium growers. Organic vineyards in key European regions are increasingly adopting plant-derived products for pest management, utilizing options that address both soil-borne nematodes and foliage insects. Regulatory frameworks for certain plant-based substances are evolving to support faster registration processes. Agricultural technology companies are developing stabilized protein formulations designed to enhance systemic resistance in plant roots. Trials indicate that these new, targeted protein formulations can effectively reduce root damage in specialized crop systems. This convergence of regulatory advantage,e user convenience,ce and multi-target activity positions biochemicals as the high-growth frontier in Europe’s evolving bionematicide landscape.

By Mode of Application Insights

The soil treatment segment held the largest share of 54.6% of the European bionematicides market in 2025. The supremacy of the soil treatment is attributed to the ecological necessity of targeting nematodes at their site of action. This method involves direct incorporation of microbial or biochemical agents into the root zone via drenching, injection, or drip irrigation—ensuring contact with soil-dwelling nematodes during their most vulnerable juvenile stages. Plant parasitic nematodes spend most of their lifecycle in the soil, making foliar or seed-only approaches insufficient for sustained control. Observations indicate that applying the biocontrol agent Purpureocillium lilacinum directly to the soil results in higher levels of egg parasitism in sugar beet cultivation compared to applying it to the foliage. The growth of protected horticulture often incorporates the delivery of bionematicides through fertigation systems for precise application. In specific European regions, a significant portion of tomato producers utilize drip-applied bionematicides integrated with closed-loop nutrient management practices. Regulatory frameworks also favor soil application. The EU Sustainable Use Directive encourages non-spray methods to minimize drift and operator exposure. This alignment of biological efficacy, agronomic practice,e and policy ensures soil treatment remains the primary and most effective deployment channel for bionematicides across European cropping systems.

The seed treatment segment is predicted to witness the highest CAGR of 13.6% over the forecast period, od owing to the integration of bionematicides into industrial seed processing and precision planting systems. This approach involves coating seeds with microbial or biochemical agents that protect emerging seedlings during the critical early growth phase when nematode damage is most detrimental. Large proportions of certified potato and sugar beet seeds in Western Europe are increasingly treated with biological agents prior to reaching the market. The industry is transitioning away from on-farm application toward industrial pre-treatment to enhance the consistency of seed coating. Centralizing the treatment process helps decrease the manual labor requirements traditionally managed by individual growers. New varieties of sugar beet are frequently bundled with specific microbial coatings to support integrated resistance strategies. The integration of biological treatments into seed packaging reflects an evolving approach to crop protection and variety development. This trend is amplified by the EU’s Farm to Fork Strategy,egy which promotes pre-treated seeds to reduce in-field chemical use. Additionally, seed treatment minimizes environmental exposure and aligns with no-till farming adoption, now practiced on a notable share of EU arable land, as per sources. Companies like Syngenta and Incotec have developed polymer encapsulation technologies that extend microbial viability on seeds for several months, enablingyear-roundd logistics. By embedding protection at the source, seed treatment offers scalability, consistency, and compliance—making it the highest growth application method in Europe’s modern agricultural paradigm.

By Infestation Insights

The root knot nematodes segment led the European bionematicides market by occupying a 52.1% share in 2025. The leading position of the root knot nematodes is credited to the economic severity and geographic ubiquity of the pest across European climates. Caused primarily by Meloidogyne species, this infestation affects a wide range of high-value crops, including tomatoes, potatoes, carrots, and greenhouse vegetables, leading to characteristic galls that impair water and nutrient uptake. Root-knot nematodes are associated with significant economic impacts on vegetable production within European horticultural sectors. Infestation levels for these pathogens are notably high in vegetable-growing areas in southern Europe. Meloidogyne species have a broad host range compared to other nematodes, allowing them to persist across various crop rotation systems. A substantial portion of tomato fields in key Spanish production regions show presence of root-knot nematodes. Regulatory pressure further intensifies demand. The EU has banned methyl bromide and restricted fosthiazate, leaving biologicals as the primary compliant control.

The cyst nematodes segment is estimated to register the fastest CAGR of 10.8% from 2026 to 2034. The swift expansion of the cyst nematodes is propelled by the urgent need to protect strategic EU crops following the phase out of synthetic nematicides. Primarily caused by Heterodera and Globodera species, these pests threaten staple crops like sugar beet, potatoes, and cereals with long-lived cysts that persist in soil for over a decade. Observations indicate a significant presence of a specific potato cyst nematode species within agricultural areas of the United Kingdom and the Netherlands. The removal of certain chemical treatments has reduced the options for controlling this pest in affected regions. Agricultural policy initiatives are shifting to support the adoption of biological alternatives for managing nematode infestations. Efforts to mitigate this pest are increasingly focused on utilizing specialized soil treatments in European agricultural zones. Additionally, public breeding programs have accelerated the development of partially resistant varieties, but these still require bionematicide supplementation for full protection. As per research, combining Bacillus seed coatings with resistant cultivars reduced cyst populations over the seasons. The critical nature of sugar beet and potato production for EU food security has elevated cyst nematode management to a policy priority, transforming a previously niche market into the top-growth area for bionematicides.

COUNTRY LEVEL ANALYSIS

Netherlands Bionematicides Market Analysis

The Netherlands dominated the European bionematicides market by accounting for a 19.5% share in 2025. The demand for bionematicides in the Netherlands is driven by its position as Europe’s greenhouse horticulture epicenter, with thousands of hectares of protected vegetable and ornamental production requiring intensive nematode management. Dutch growers operate under strict sustainability certifications such as MPS and GLOBALG.A.P. that mandate biological pest control as the first resort. The Netherlands also hosts Europe’s densest concentration of biocontrol R&D. Koppert Biological Systems and Provivi Europe lead in strain development and formulation science. Furthermore, the country’s closed-loop recycling systems necessitate non-phytotoxic, biodegradable solutions, giving bionematicides a structural advantage over synthetics. This fusion of high-tech agriculture, regulatory rigour, and innovation infrastructure makes the Netherlands the most advanced and value-driven bionematicide market in Europe.

Germany Bionematicides Market Analysis

Germany was the next prominent country in the Europe bionematicides market by occupying a 16.8% share in 2025. The growth of the German market is fuelled by its large-scale arable farming, particularly sugar beet and potato production, where nematodes cause significant economic damage. A portion of Germany’s thousands of hectares of sugar beet isinfested with cyst nematodes, prompting the Federal Ministry of Food and Agriculture to allocate millions of euros for bionematicide adoption grants. Germany enforces the EU’s strictest pesticide reduction targets under its National Action Plan, requiring all professional users to complete certified training in biological alternatives. Consequently, a significant share of sugar beet cooperatives now include Bacillus firmus seed treatments in their standard input packages. The country also hosts leading biocontrol manufacturers like BASF BioSolutions and Andermatt Biocontrol, which invest heavily in field validation trials across diverse soil types. Germany acts as the primary market for deploying evidence-based bionematicides in European field crops, driven by strong technical advice and policy incentives.

Spain Bionematicides Market Analysis

Spain maintains a noteworthy share of the European insecticides market owing to its vast horticultural belts in Andalusia, Murcia, and Valencia. Spain’s year-round growing season intensifies pest pressure, while EU export requirements for residue-free produce mandate biological solutions. Fruit and vegetable producers are increasingly adopting biochemicals derived from neem and formulations based on Paecilomyces to align with standards set by major retail chains. Research initiatives are actively exploring combined agricultural techniques, specifically integrating soil solarization with microbial bionematicides. Despite water scarcity challenges, drip irrigation enables precise delivery, making Spain a high-volume adoption market where agronomic necessity and market access converge to drive rapid bionematicide uptake.

France Bionematicides Market Analysis

France witnessed a consistent expansion in the European bionematicides market due to aggressive national policies under the Ecophyto Plan III, which mandates a reduction in synthetic pesticide use and provides direct subsidies for biological alternatives. Vineyards are experiencing higher levels of nematode pressure, a trend associated with shifting environmental conditions. Root-knot species have been identified in a significant portion of sampled vineyard plots, indicating a widespread presence of these pests. New, expedited regulatory pathways for biological nematode controls have been implemented to assist in agricultural management, and agricultural advisors are increasingly incorporating biological control options into their pest management strategies. The organic agricultural sector continues to expand, with specific vegetable crops showing a high reliance on biological treatments for pest control. Thispolicy-led transitionn, supported by strong research institutions and farmer networks,s positions France as a high-momentum market where regulation actively reshapes pest control practices.

Italy Bionematicides Market Analysis

Italy is anticipated to grow in the European bionematicides market during the forecast period, owing to high crop diversity, ranging from tomatoes and olives to potatoes and cereals, and a predominance of small to medium farms that favor accessible biological solutions. Root knot nematodes severely affect tomato production in southern regions, where infestation rates are significant. Governmental initiatives supporting sustainable agriculture have facilitated the adoption of bionematicides for smaller, localized agricultural operations. The expansion of organic horticulture, driven by market demand for premium produce, is fostering the integration of biological pest control methods, including neem extracts and microbial formulations. Research indicates a rise in the application of microbial bionematicides within specific regional, high-value, processing-crop sectors. Regional partnerships combined with European agricultural development funding facilitate the adoption of sustainable pest management solutions across Mediterranean landscapes.

COMPETITIVE LANDSCAPE

Competition in the European bionematicides market is characterized by a mix of multinational agrochemical firms and specialized biocontrol innovators, all operating within a stringent regulatory and sustainability-driven environment. Success hinges on scientific credibility, regulatory agility, and on-farm validation rather than price alone. Large companies leverage global R&D networks and existing distribution channels to scale biological solutions, while niche players differentiate through proprietary microbial strains and deep agronomic expertise. The market remains fragmented due to crop-specific nematode pressures and regional regulatory interpretations, necessitating localized strategies. Barriers to entry are high due to complex registration requirements and the need for multi-year field trials, yet public funding through Horizon Europe is enabling smaller firms to compete. Trust among advisors and growers is paramount, making demonstration networks and extension services critical competitive assets. As synthetic nematicides continue to be phased out, competition is intensifying around efficacy, consistency,y formulation stability, ty and integration into digital and seed-based delivery systems that meet the practical needs of European farmers across horticulture and arable sectors.

KEY MARKET PLAYERS

Some of the major companies dominating ththio-nematicideses market by their products and services include

- Bayer CropScience AG

- Monsanto Company

- BASF SE

- Koppert Biological Systems

- Certis USA L.L.C

- Syngenta AG

- FMC Corporation

- Dow AgroSciences LLC

- Valent BioSciences Corporation,

- Marrone Bio Innovations, Inc.

Top Players In The Market

- BASF SE, headquartered in Germany, is a global leader in agricultural solutions with a robust portfolio in tEuropeanope bionematicides market through its BioSolutions division. The company offers proprietary microbial strains such as Bacillus firmus under the VOTiVO brand, widely adopted in potato and sugar beet production across Northern and Central Europe. BASF is advancing sustainable nematode management by aligning its biological portfolio with EU Green Deal goals and scaling its fermentation technology.

- Koppert Biological Systems, a Netherlands-based pioneer in biological crop protection, plays a strategic role in the European bionematicides market with its proprietary Purpureocillium lilacinum-based products tailored for greenhouse and open field horticulture. The company leverages its deep expertise in microbial ecology to develop formulations compatible with drip irrigation and organic certification standards. It also partnered with Wageningen University to refine shelf life stabilization techniques for fungal spores. Koppert strengthens its position as a trusted leader in the European transition to sustainable, chemical-free nematode control through education, rigorous science, and ecological solutions.

- Syngenta Group, with significant European operations based in Switzerland, contributes to the bionematicides market through its biological seed treatment technologies and integrated crop solutions. The company’s bioinnovation hub in Stein develops microbial seed coatings that protect emerging roots from early nematode attack, particularly in sugar beet and maize. It also collaborated with EU potato cooperatives to validate biological alternatives following the phase-out of synthetic nematicides. Syngenta is fostering yield resilience and ensuring regulatory compliance throughout Europe by combining bionematicides with its seed and digital technology ecosystems.

Top Strategies Used By The Key Market Participants

Key players in the European bionematicides market focus on developing strain-specific microbial formulations with enhanced soil persistence and compatibility with irrigation systems. They invest in digital agronomy platforms that integrate soil testing, weather ddataaa and nematode risk mapping to enable precision application. Companies pursue strategic partnerships with research institutions and farmer cooperatives to generate field validation data required for regulatory dossiers and grower trust. They align product developmenwith the h EU Green Deal and Farm to Fork objectives to secure policy support and public funding. Additionally, firms are expanding seed treatment integration and shelf life stabilization technologies to improve logistics and user convenience across diverse European farming systems.

MARKET SEGMENTATION

This research report on the European bio-nematicides market is segmented and sub-segmented into the following categories.

By Type

- Microbials

- Biochemicals

By Crop Type

- Fruits

- Vegetables

By Mode of Application

- Seed treatment

- Soil treatment

- Foliar spray

- Others

By Infestation

- Root-Knot Nematodes, Cyst Nematodes, Lesion Nematodes, Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe bionematicides market?

The Europe bionematicides market includes biologically derived products used to control plant-parasitic nematodes in crops, offering eco-friendly pest management alternatives to chemical nematicides.

Why is the Europe bionematicides market growing?

Growth is driven by stricter pesticide regulations, demand for sustainable agriculture, organic farming adoption, and environmental safety concerns.

What are bionematicides?

Bionematicides are biological pest control agents derived from bacteria, fungi, or plant extracts that suppress or kill nematodes without harmful chemicals.

What are common sources of bionematicides?

Common sources include Bacillus spp., Purpureocillium lilacinum, Paecilomyces spp., neem extracts, and other microbial or botanical agents.

What crops benefit from bionematicide use?

Major beneficiaries include vegetables, fruits, cereals, tubers, and high-value row crops suffering from nematode infestations.

How do bionematicides work?

Bionematicides control nematodes by infection, toxin production, competition, or inducing plant defense mechanisms in the soil.

What advantages do bionematicides offer?

They offer low toxicity, minimal environmental impact, compatibility with integrated pest management (IPM), and safer residue profiles.

Which countries in Europe lead the bionematicides market?

Markets such as Germany, France, the Netherlands, Italy, and Spain show increasing adoption due to strong sustainable agriculture initiatives.

What challenges does the market face?

Challenges include variable field performance, registration and regulatory barriers, farmer awareness gaps, and formulation stability issues.

How do regulations impact the bionematicides market?

EU and national regulations encourage adoption by restricting hazardous chemicals and promoting safer biological alternatives, though approval processes can be stringent.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com