Europe Blockchain Market Size, Share, Trends, & Growth Forecast Report By Component (Solutions, Services), Application, Industry Vertical and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

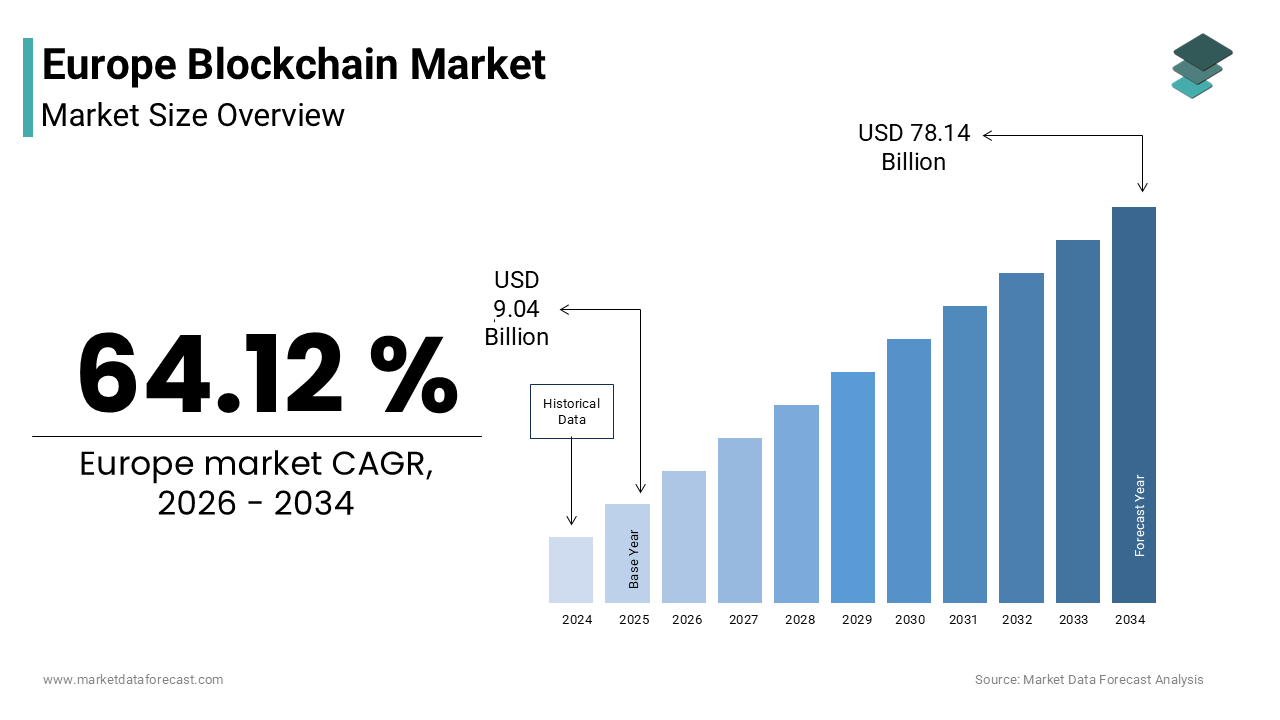

Market Size, 2025

$9.04 BnMarket Estimate, 2026

$14.84 BnMarket Forecast, 2034

$78.14 BnCAGR, 2026–2034

64.12%Europe Blockchain Market Report Summary

The Europe blockchain market was valued at USD 9.04 billion in 2025, is estimated to reach USD 14.84 billion in 2026, and is projected to reach USD 78.14 billion by 2034, growing at a CAGR of 64.12% during the forecast period from 2026 to 2034. The growth of the Europe blockchain market is driven by increasing regulatory clarity under frameworks such as the Markets in Crypto-Assets (MiCA), rising institutional adoption, and strong public sector initiatives supporting distributed ledger infrastructure. The expansion of decentralized finance, cross-border payment systems, and supply chain transparency solutions is further fueling market growth. Moreover, the development of the European Blockchain Services Infrastructure and growing investments in digital transformation initiatives have broadened the scope of blockchain adoption across financial services, government operations, and enterprise applications in Europe.

Key Market Trends

-

Rising adoption of blockchain in financial services is driven by its ability to reduce transaction costs and improve settlement efficiency.

-

Growing implementation of government-led blockchain initiatives for digital identity, notarization, and cross-border data exchange.

-

Increasing demand for decentralized finance solutions within regulated environments across Europe.

-

Expansion of blockchain applications in supply chain transparency, trade finance, and asset tracking.

-

Strong focus on regulatory compliance, interoperability, and sustainability in blockchain infrastructure development.

Segmental Insights

- Based on component, the solutions segment was the largest and held a significant share of the Europe blockchain market in 2025. The segment’s dominance is attributed to strong enterprise investments in blockchain platforms, middleware, and infrastructure required to ensure regulatory compliance, data security, and interoperability across diverse applications.

- Based on application, the payments segment accounted for 45.6% of the Europe blockchain market share in 2025. This dominance is driven by blockchain’s ability to accelerate cross-border payments, reduce reliance on intermediaries, and provide near real-time settlement capabilities, particularly benefiting financial institutions and small and medium enterprises.

- Based on industry vertical, the Banking, Financial Services, and Insurance (BFSI) segment was the largest, occupying a prominent share of the Europe blockchain market in 2025. The leadership of this segment stems from early adoption of blockchain technologies for transaction processing, compliance automation, digital asset custody, and trade finance optimization.

Regional Insights

The Europe blockchain market is witnessing robust growth across major economies, supported by strong regulatory frameworks, institutional adoption, and increasing investments in digital infrastructure.

-

Germany was the largest contributor, accounting for 24.6% of the Europe blockchain market share in 2025, driven by its strong fintech ecosystem, high investment inflows, and increasing adoption across manufacturing, automotive, and financial sectors.

-

The United Kingdom continues to perform strongly, fueled by its global fintech leadership, strong venture capital ecosystem, and growing implementation of blockchain in financial services and public sector initiatives.

-

France remains a key market supported by government-backed regulatory frameworks, increasing enterprise adoption, and a strong presence in sectors such as luxury goods authentication and digital finance.

-

The Netherlands is emerging as a significant hub due to its advanced digital infrastructure, innovation-friendly regulatory environment, and growing startup ecosystem.

-

Switzerland continues to play a strategic role with its well-established blockchain ecosystem, strong institutional participation, and leadership in secure digital asset infrastructure.

Competitive Landscape

The Europe blockchain market is characterized by the presence of global technology providers, enterprise solution vendors, and blockchain-native companies with strong capabilities in infrastructure, compliance, and innovation. Leading companies are focusing on integrating blockchain with existing enterprise systems, enhancing security protocols, and developing scalable and interoperable platforms. Strategic partnerships with financial institutions, investments in decentralized finance, and expansion of enterprise blockchain solutions are strengthening market positions. Prominent players in the Europe blockchain market include IBM Corporation, Microsoft Corporation, Amazon Web Services, Inc., Oracle Corporation, SAP SE, Accenture plc, Infosys Limited, Ripple Labs Inc., R3, and ConsenSys.

Europe Blockchain Market Size

The Europe blockchain market size was valued at USD 9.04 billion in 2025 and is anticipated to reach USD 14.84 billion in 2026 from USD 78.14 billion by 2034, growing at a CAGR of 64.12% during the forecast period from 2026 to 2034.

Blockchain is a shared, digital ledger that records transactions across a network of computers. This technological ecosystem facilitates decentralized verification mechanisms that eliminate intermediaries while enhancing trust in digital interactions across financial services supply chain management and governmental operations. The European public sector is actively constructing its own blockchain services infrastructure which should soon achieve interoperability with private sector platforms according to the European Commission. Nearly 40 public bodies from all European countries connect through a unified blockchain network under the European Blockchain Services Infrastructure initiative as per official European Union documentation. The region demonstrates substantial digital transformation momentum with approximately 1.3 billion euros allocated for digital initiatives (including AI, data, and cybersecurity) during the 2023 to 2024 period, according to the European Commission's Digital Europe Programme work programmes. Germany has solidified its position as a primary blockchain hub in the region, securing a leading proportion of both total European financing and deal volume according to multiple studies. The implementation of comprehensive regulatory frameworks like the Markets in Crypto Assets regulation has established harmonized standards across 27 member states creating a cohesive environment for technological adoption. European blockchain startups have cumulatively raised over 7.5 billion euros in funding with significant concentration in innovation hubs, according to assessments by the European Blockchain Observatory and Forum (2023). This foundational infrastructure positions Europe as a strategic contender in global distributed ledger technology deployment while addressing unique regional compliance and interoperability requirements.

MARKET DRIVERS

Regulatory Clarity Through Unified Framework Implementation Accelerates Institutional Adoption

The introduction of comprehensive regulatory frameworks fuels the growth of the Europe blockchain market. This has fundamentally transformed institutional confidence in blockchain deployment across European markets. The MiCA regulation introduces a single set of rules for the entire European Union, enabling licensed digital asset firms to provide services across all member states without needing separate approvals in each country. While firms initially face new administrative requirements, the move toward a harmonized market is intended to streamline long-term compliance efforts for companies operating in multiple European jurisdictions. Germany and the Netherlands have issued early licenses under the new framework demonstrating accelerated regulatory processing timelines. The regulatory clarity has prompted traditional financial institutions to explore blockchain based services with major banks launching digital asset custody and trading solutions. Transaction volumes in Europe showed a significant increase toward the end of 2024, reflecting a high level of engagement from large-scale professional and institutional market participants. The framework mandates strict reserve requirements for stablecoins and transparent disclosure protocols which enhance consumer protection while fostering innovation. Major financial hubs, including France, Germany, and Luxembourg, have established specialized regulatory units to handle digital asset applications, aiming to provide clearer guidance and more efficient processing than previous uncoordinated systems. This regulatory coherence attracts international firms seeking predictable compliance environments thereby expanding the regional ecosystem and stimulating cross border technological collaboration.

Public Sector Digital Transformation Initiatives Create Substantial Implementation Demand

Government led blockchain projects generate significant demand for distributed ledger solutions across the region’s administrative functions, which is among the key factors driving the expansion of the Europe blockchain market. The European Blockchain Services Infrastructure connects public organizations from all member states enabling secure cross border data exchange for notarization diploma verification and digital identity management according to official European Union sources. A comprehensive inventory of government initiatives reveals that blockchain technology is being actively piloted across national and local administrations to improve the delivery of public services. Implementing blockchain for educational records allows for instant verification of academic achievements, greatly reducing the manual labor required while enhancing the security and trustworthiness of digital diplomas. Public administrations leverage blockchain to automate compliance checks in time sensitive processes creating efficiency gains that justify initial infrastructure investments. Digital ledger solutions are being developed to help tax and customs authorities exchange information more securely, with the goal of shortening the time needed to verify tax identification and combat cross-border fraud. Member states participating in the European Blockchain Partnership commit resources to operate network nodes ensuring sustainable infrastructure development. This public sector leadership creates demonstration effects that encourage private sector adoption while establishing technical standards that reduce implementation risks for commercial applications. The convergence of policy support and practical use cases generates sustained demand for blockchain expertise and solution development across the region.

MARKET RESTRAINTS

Complex Multi Jurisdictional Compliance Requirements Increase Operational Burdens

Regulatory harmonization efforts are underway, but blockchain operators in the region still face intricate compliance obligations, which limits the growth of the Europe blockchain market. Consequently, these operators experience elevated operational costs and delayed market entry. Despite overarching European guidelines, national regulators continue to offer varying interpretations of digital asset rules, prompting some businesses to choose specific countries based on more favorable administrative climates. Some member states implement transitional periods allowing firms to operate without full licenses until 2026 while others enforce immediate compliance generating fragmented market conditions. The Travel Rule requirements mandate detailed sender and recipient information for all crypto transfers with no minimum threshold increasing data management complexity according to European Union guidance documents. Firms must implement robust know your customer and anti money laundering protocols that screen wallet addresses against sanctioned entities and high risk behaviors adding significant technology and personnel expenses. Smaller enterprises face a disproportionately high cost for maintaining compliance compared to larger organizations, as a larger portion of their available resources must be dedicated to meeting complex reporting and administrative requirements. The requirement to segregate customer assets maintain incident reporting systems and conduct regular audits creates administrative overhead that disproportionately affects emerging firms. These multifaceted obligations discourage innovation from resource constrained startups while favoring established players with dedicated compliance teams. The resulting market concentration may limit technological diversity and slow the pace of disruptive solution development across the European blockchain ecosystem.

Energy Consumption Concerns and Environmental Sustainability Mandates Limit Technology Choices

Stringent sustainability regulations and public sentiment are creating hurdles in the Europe blockchain market. As a result, environmental considerations significantly constrain blockchain deployment strategies. Tightening environmental targets are placing increased scrutiny on the energy-intensive processes used to secure certain decentralized networks, forcing a shift toward more sustainable consensus methods. Blockchain networks utilizing energy intensive validation processes face scrutiny from regulators and potential restrictions under emerging digital sustainability frameworks. Facilities hosting infrastructure for digital assets are increasingly subject to regional energy efficiency mandates, which can lead to higher overhead costs for maintaining active nodes and validators. Public perception regarding cryptocurrency energy usage influences policy decisions with several member states considering additional levies on high consumption digital infrastructure. The transition to proof of stake and other low energy consensus models requires substantial technical reengineering that delays project timelines and increases development expenses. Organizations are now expected to provide clear disclosures regarding the environmental footprint of their technology choices, a requirement aimed at increasing transparency and encouraging the use of greener digital solutions. These sustainability requirements while environmentally beneficial create adoption barriers for use cases where energy efficient alternatives remain technologically immature. The tension between decentralization benefits and environmental responsibilities forces European firms to navigate complex tradeoffs that may limit the scope and scale of blockchain initiatives across the region.

MARKET OPPORTUNITIES

Cross Border Trade Finance and Supply Chain Transparency Solutions Present Expansion Potential

The region’s cross-border trade and supply chain operations are facing a transformative shift, which is likely to promote the growth of the Europe blockchain market. Blockchain technology provides the enhanced transparency and efficiency needed to drive this change. Distributed ledger systems enable real time tracking of goods from origin to destination reducing documentation errors and fraud risks according to sources. Smart contracts automate payment releases upon verification of delivery conditions accelerating settlement cycles, according to studies. The trusted data sharing use case facilitates secure information exchange between customs authorities and logistics providers reducing border processing times and administrative burdens. European manufacturers leveraging blockchain for component traceability report improvements in recall management efficiency according to research. Small and medium enterprises gain access to trade finance through tokenized invoice platforms that connect them with institutional investors across borders. The European digital identity framework enables secure verification of business credentials reducing onboarding times for new trade partners. These applications align with European Union objectives for resilient supply chains and digital single market integration creating policy support and funding opportunities. Blockchain solutions are positioned for substantial growth across European commercial sectors. This is driven by recovering global trade volumes and the demand for transparent, efficient cross-border transaction systems.

Decentralized Finance Infrastructure Development Attracts Institutional Capital and Innovation

The evolution of decentralized finance protocols within the continent’s regulatory boundaries creates major opportunities for financial infrastructure modernization and service innovation within the Europe blockchain market. New European regulatory frameworks have enabled the issuance of digital assets pegged to the euro, providing a stable and transparent foundation for nearly instantaneous cross-border financial settlements. Circle EURC achieved 2727% growth between July 2024 and June 2025 demonstrating strong market demand for regulatory aligned digital currencies as per Chainalysis research. Institutional investors increasingly allocate capital to decentralized lending and liquidity protocols that offer transparent risk assessment and automated compliance features. Financial institutions across the continent are actively testing and implementing ledger-based systems for settling securities, aimed at significantly lowering operational overhead and minimizing risks between trading parties. The integration of decentralized finance with traditional banking infrastructure creates hybrid models that combine innovation with regulatory oversight. Developer communities across Berlin Paris and Amsterdam contribute open source protocols that enhance interoperability and security standards. As regulatory clarity improves institutional participation in decentralized finance is projected to expand the addressable market substantially. These developments position Europe as a leader in compliant decentralized financial infrastructure with potential for global technology export and standards influence.

MARKET OPPORTUNITIES

Interoperability Gaps Between Legacy Systems and Blockchain Networks Impede Integration

The integration of blockchain solutions with existing European IT infrastructure exhibits substantial technical and organizational challenges that slow down the growth of the Europe blockchain market. Public sector entities operate diverse legacy systems developed over decades with incompatible data formats and security protocols according to sources. Achieving seamless interoperability requires significant investment in middleware solutions and application programming interfaces that translate between traditional databases and distributed ledgers. The European Blockchain Services Infrastructure aims to connect national systems but implementation timelines vary across member states creating coordination complexities according to sources. Research indicate that a portion of blockchain project budgets allocate to integration efforts rather than core functionality development. The lack of universal standards for data representation and transaction validation complicates cross border deployments and increases maintenance costs. Technical teams must balance decentralization benefits with performance requirements of high volume public services creating architectural tradeoffs that delay production launches. These integration hurdles disproportionately affect smaller organizations with limited technical resources potentially widening the digital divide between large and small blockchain adopters across European markets.

Talent Shortages and Skills Gaps Constrain Project Execution and Innovation Capacity

Critical human capital constraints are hampering the growth of the Europe Blockchain Market. As a result, the pace of technological development and commercial deployment is limited. Demand for blockchain developers architects and compliance specialists exceeds available supply. Educational institutions struggle to update curricula rapidly enough to address emerging technical requirements creating a pipeline gap for qualified professionals. Organizations report average recruitment timelines of 4 to 6 months for senior blockchain roles with compensation premiums of 25 to 35% above traditional IT positions according to multiple studies. The complexity of regulatory compliance requirements further narrows the candidate pool to professionals with both technical expertise and legal knowledge. Small and medium enterprises face particular challenges attracting talent away from larger firms with greater resources for training and retention. The concentration of blockchain expertise in major innovation hubs like Berlin London and Paris creates geographic imbalances that limit regional development opportunities. These human capital constraints increase project costs extend implementation timelines and may force organizations to delay or scale back blockchain initiatives. Addressing this challenge requires coordinated investment in education programs professional certification pathways and immigration policies that facilitate knowledge transfer across European labor markets.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 64.12% |

| Segments Covered | By Component, Application, Industry Vertical and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | IBM Corporation, Microsoft Corporation, Amazon Web Services, Inc., Oracle Corporation, SAP SE, Accenture plc, Infosys Limited, Ripple Labs Inc., R3, and ConsenSys. |

SEGMENTAL ANALYSIS

By Component Insights

The solutions component segment dominated the Europe Blockchain Market and captured a substantial share in 2025. The dominance of this segment is driven by substantial enterprise investments in core blockchain frameworks before operational services can be effectively layered. This segment covers middleware platforms integrated applications and infrastructure protocols that form the foundational architecture for blockchain deployment. Major European financial institutions including BNP Paribas and Deutsche Bank have allocated significant capital toward proprietary blockchain infrastructure to support settlement systems and compliance monitoring. The preference for comprehensive platform deployments reflects organizational priorities around data sovereignty regulatory adherence and system interoperability under the Markets in Crypto Assets framework. Furthermore, the European Blockchain Services Infrastructure which connects nearly 40 public bodies across member states relies heavily on standardized solution architectures to enable cross border service delivery. This institutional adoption pattern reinforces solution segment leadership as public sector entities prioritize robust foundational technology before scaling operational services. The stringent regulatory environment across European Union member states creates sustained demand for blockchain solutions that embed compliance capabilities at the architectural level. According to the European Commission the Markets in Crypto Assets regulation establishes harmonized operational standards that require technical infrastructure capable of real time transaction monitoring and audit trail generation. Solutions providers respond by developing platforms with built in governance modules identity verification protocols and reporting interfaces that align with MiCA requirements. As per Coincub analysis only 12 crypto asset service providers had secured full MiCA licensing as of early 2025 indicating that compliant infrastructure represents a critical barrier to market entry. Organizations investing in solutions with embedded compliance features reduce subsequent integration costs and accelerate time to regulatory approval. The European Data Protection Board guidance on distributed ledger technologies further incentivizes solutions that incorporate privacy preserving mechanisms such as zero knowledge proofs and selective disclosure capabilities. The European digital asset market continues to see massive capital inflows and high levels of institutional engagement, placing increased pressure on the underlying technical systems to handle heavy transaction loads while remaining within legal boundaries. This regulatory driven demand cycle ensures continued solutions segment leadership as enterprises prioritize foundational technology investments that guarantee long term operational viability within Europe's evolving legal perimeter.

The services component segment is predicted to witness the highest CAGR of 34.4% during the forecast period due to increasing organizational demand for implementation support maintenance consulting and managed blockchain operations following initial infrastructure deployment. As enterprises complete foundational solution investments they transition toward service engagements that optimize performance ensure regulatory adherence and enable continuous innovation. Blockchain as a Service offerings from providers including Microsoft Azure and IBM Cloud lower technical barriers for small and medium enterprises seeking distributed ledger capabilities without substantial internal development resources. The European Commission's Digital Europe Programme allocates funding for blockchain skills development and technical assistance further stimulating service sector expansion. As per research, the complexity of integrating blockchain with legacy enterprise systems creates sustained demand for specialized consulting and implementation services across financial services supply chain and public sector verticals. This services growth momentum reflects market maturation where organizations prioritize operational excellence and strategic optimization following initial technology adoption. The accelerating pace of digital transformation across European enterprises creates substantial demand for blockchain related professional and managed services. According to sources, organizations increasingly engage external partners to navigate technical complexity regulatory uncertainty and change management challenges associated with distributed ledger adoption. Services providers deliver critical capabilities including system integration staff training performance monitoring and regulatory reporting that enable successful blockchain implementation. As per research, declining internal technology capacity within traditional enterprises intensifies reliance on specialized service partners for blockchain initiatives. The Markets in Crypto Assets framework introduces ongoing compliance obligations that require continuous monitoring updating and reporting services to maintain regulatory standing. Financial institutions particularly value managed services that provide operational resilience security monitoring and disaster recovery capabilities essential for mission critical blockchain applications. This services demand pattern reflects a strategic shift where organizations view blockchain not as a one time technology purchase but as an ongoing operational capability requiring sustained expert support.

By Application Insights

The payments application segment held the majority share or 45.6% of the Europe Blockchain Market in 2025. This supremacy of the segment is attributed to the immediate commercial value blockchain delivers in reducing transaction costs accelerating settlement times and enhancing cross border payment efficiency. European financial institutions including Santander and ING have deployed blockchain based payment rails that process transactions in seconds rather than days while reducing intermediary fees. According to studies, the European region processed substantial amount in cryptocurrency transaction volume between July 2023 and June 2025 with payment related activity representing the largest component. The Instant Payments Regulation adopted by the European Parliament further catalyzes blockchain adoption by establishing expectations for near real time euro transactions that distributed ledger technology can efficiently support. As per sources crypto ownership in the European Union expanded reflecting growing public familiarity with digital payment mechanisms. Small and medium enterprises particularly value blockchain enabled payment solutions for international trade where traditional correspondent banking introduces delays and opacity. This payments segment leadership demonstrates blockchain's ability to address tangible business challenges while delivering measurable efficiency gains that justify continued investment. The expansion of intra European and global commerce creates sustained demand for blockchain enabled payment solutions that overcome limitations of legacy financial infrastructure. According to research the region is experiencing accelerated adoption of instant payment rails which blockchain technology can further enhance through reduced intermediary dependency. Cross border transactions within the single market benefit from blockchain's ability to provide immutable audit trails and near instantaneous finality compared to traditional correspondent banking which can require multiple days for settlement. The integration of euro denominated stablecoins compliant with MiCA further strengthens this driver by providing price stable digital instruments that maintain regulatory alignment. According to studies the restriction of crypto asset service providers to MiCA compliant stablecoins has triggered significant market recalibration favoring locally issued instruments over non compliant alternatives. This regulatory driven shift creates opportunities for financial technology firms to develop innovative payment solutions leveraging blockchain infrastructure while maintaining compliance with European consumer protection standards.

The digital identity application segment is estimated to register the fastest CAGR of 89.2% from 2026 to 2034 owing to increasing organizational and governmental demand for secure portable and privacy preserving identity verification mechanisms that blockchain technology uniquely enables. European Union initiatives including the European Digital Identity Framework establish policy foundations that incentivize blockchain based identity solutions capable of supporting cross border authentication while maintaining citizen control over personal data. The General Data Protection Regulation creates specific requirements for data minimization and user consent that blockchain architectures with selective disclosure capabilities can efficiently address. The digital identity growth momentum reflects convergence between regulatory priorities technological capability and commercial demand for trusted authentication mechanisms. The intersection of European regulatory frameworks with emerging privacy expectations creates powerful tailwinds for blockchain based digital identity solutions. The European Data Protection Board has not issued definitive guidance specifically addressing blockchain implementations creating opportunities for compliant identity solutions that demonstrate regulatory alignment. The European Digital Identity Wallet initiative establishes a reference architecture that blockchain technologies can support through decentralized identifier standards and verifiable credential protocols. This regulatory driven demand cycle ensures continued digital identity segment expansion as organizations prioritize solutions that balance technological capability with legal compliance and user trust.

By Industry Vertical Insights

The Banking Financial Services and Insurance segment led the Europe Blockchain Market and held a 38.1% share in 2025. This position of the segment is credited to the sector's early recognition of blockchain's value for settlement optimization trade finance automation and regulatory compliance enhancement. Major European financial institutions including Euroclear and Clearstream have deployed blockchain infrastructure to streamline securities settlement reducing counterparty risk and operational costs. The Markets in Crypto Assets regulation provides regulatory clarity that enables banks to explore blockchain applications with reduced compliance uncertainty. As per research, traditional banks increasingly view blockchain not as a disruptive threat but as an efficiency enhancing tool for custody payments and cross border transaction optimization. This BFSI segment leadership demonstrates blockchain's ability to address core financial services challenges while delivering measurable operational improvements that justify continued investment. The convergence of institutional demand with regulatory clarity creates sustained momentum for blockchain adoption within European financial services. This regulatory harmonization reduces operational ambiguity and encourages long term infrastructure investment by financial institutions seeking scale. Financial institutions value the predictability that MiCA provides regarding capital requirements governance standards and consumer protection protocols. The integration of euro denominated stablecoins compliant with MiCA further strengthens this driver by providing price stable digital instruments that maintain regulatory alignment. This institutional adoption pattern ensures continued BFSI segment leadership as financial organizations prioritize blockchain investments that deliver operational efficiency while maintaining regulatory compliance.

The Media and Entertainment vertical segment is anticipated to witness the fastest CAGR of 49.5% over the forecast period. This exceptional growth trajectory is propelled by increasing industry demand for blockchain solutions that address content provenance rights management and creator compensation challenges unique to digital media ecosystems. European media organizations including the BBC and RTL Group have piloted blockchain based systems for tracking content usage and automating royalty distributions to rights holders. According to research, smart contracts enable automated enforcement of licensing agreements reducing administrative overhead and dispute resolution costs. As per industry analysis the tokenization of digital assets including music video and gaming content creates new revenue models that blockchain infrastructure can efficiently support. The European Union's Digital Services Act establishes accountability requirements for content platforms that blockchain based audit trails can help satisfy. According to sources, European blockchain startups raised substantial amount in cumulative funding with significant portions allocated to media and entertainment applications. This media and entertainment growth momentum reflects convergence between technological capability commercial opportunity and regulatory expectations for transparent content ecosystems. The evolving economics of digital content creation and distribution create powerful incentives for blockchain adoption within European media and entertainment organizations. According to research, smart contracts enable automated and enforceable agreements across various industries including media where licensing terms can be programmatically executed. Content creators value blockchain based systems that provide immutable proof of authorship transparent usage tracking and instantaneous royalty settlement. The European Digital Single Market strategy encourages cross border content distribution that blockchain based rights management systems can efficiently support. According to studies, data minimization principles are difficult to reconcile with traditional database processing but blockchain based systems with selective disclosure mechanisms enable compliance while preserving utility. This regulatory driven demand cycle ensures continued media and entertainment segment expansion as organizations prioritize solutions that balance technological capability with legal compliance and creator protection.

REGIONAL ANALYSIS

Germany Blockchain Market Analysis

Germany was the top performer in the European blockchain market and accounted for a 24.6% share in 2025. The German blockchain ecosystem demonstrates remarkable resilience and growth driven by robust fintech infrastructure and progressive regulatory frameworks. Germany has established itself as a premier destination for blockchain financing in Europe, capturing a significant portion of both total regional investment and the overall number of project deals. There has been a steady increase in the number of German firms integrating decentralized ledger technology into their business models, with nearly one-tenth of the total economy now either actively using or preparing to deploy these systems. The manufacturing industry currently leads the way in technological integration, with automotive manufacturers showing the highest level of engagement as they utilize these tools for supply chain transparency and component tracking. Beyond the industrial core, sectors such as chemical production, logistics, and professional services are increasingly adopting blockchain to enhance the efficiency and security of their digital processes. Federal Financial Supervisory Authority licensing frameworks provide regulatory certainty that attracts institutional participation. Berlin and Munich have emerged as innovation hubs hosting numerous blockchain startups and enterprise development centers. The government commitment to digital sovereignty and Industry 4.0 initiatives creates sustained demand for supply chain transparency and smart contract applications. Energy sector blockchain pilots for peer to peer trading further expand use case diversity. These converging factors position Germany as the technological and commercial anchor for European blockchain advancement with projected market expansion continuing through 2030.

United Kingdom Blockchain Market Analysis

The United Kingdom followed closely behind in the European blockchain market and captured a 19.2% share in 2025. London serves as a global fintech nexus attracting substantial blockchain investment and talent concentration. The Financial Conduct Authority registration framework for crypto asset service providers has established operational clarity that encourages compliant market participation. Financial services dominate adoption use cases with major banks piloting settlement systems and trade finance applications. The National Health Services implementation of blockchain for vaccine supply monitoring demonstrates public sector leadership. Crypto Valley connections with Switzerland facilitate cross border innovation while Brexit has prompted regulatory divergence that creates both challenges and opportunities. Venture capital activity remains robust despite global headwinds with London based startups securing significant funding rounds. The convergence of deep capital markets technical expertise and regulatory evolution sustains the UK position as a strategic blockchain hub within the European landscape.

France Blockchain Market Analysis

France holds a significant position in the European blockchain market. The French government Crypto Assets Plan has created a welcoming regulatory environment that attracts international blockchain enterprises. The Autorité des Marchés Financiers maintains a public registry of compliant digital asset service providers enhancing market transparency. Paris has emerged as a preferred European headquarters location for global crypto firms seeking MiCA aligned operations. Blockchain adoption in luxury goods authentication and supply chain verification leverages France strong manufacturing and brand heritage. The French banking sector actively explores tokenized asset issuance and cross border payment solutions. Public research institutions contribute significant blockchain innovation through Horizon Europe funding programs. The combination of regulatory support institutional engagement and technological talent positions France for continued market share growth. Enterprise blockchain deployments in aerospace automotive and agriculture sectors demonstrate practical value creation. These dynamics support France trajectory as a leading European blockchain destination with expanding commercial and public sector applications.

Netherlands Blockchain Market Analysis

The Netherlands demonstrates strong performance in the European blockchain market owing to pragmatic regulation and strategic geographic positioning. Amsterdam hosts a vibrant ecosystem of blockchain startups exchanges and development firms benefiting from the country historical trading expertise. De Nederlandsche Bank employs risk based supervision that balances innovation with consumer protection. The number of registered crypto service providers in the Netherlands has increased substantially in recent years according to market research documentation. Dutch enterprises leverage blockchain for port logistics agricultural traceability and energy grid management. The presence of major international exchanges regional offices enhances liquidity and market depth. Academic institutions contribute research excellence in cryptography and distributed systems. The Netherlands digital infrastructure and multilingual workforce facilitate pan European service delivery. These attributes create a favorable environment for blockchain commercialization and cross border expansion. The market continues to attract investment and talent reinforcing the Netherlands role as a critical gateway for blockchain businesses entering the European Union.

Switzerland Blockchain Market Analysis

Switzerland maintains a noteworthy position in the European blockchain market due to its Crypto Valley ecosystem in Zug. The Swiss Financial Market Supervisory Authority principle based regulatory approach provides clarity while accommodating innovation. Numerous blockchain related companies maintain headquarters in Switzerland according to industry assessments. The country reputation for financial security and wealth management naturally extends to digital asset custody and institutional services. Swiss exchanges and infrastructure providers serve high net worth individuals and institutional investors across Europe. Tax policies and legal frameworks support long term blockchain enterprise development. The convergence of banking expertise technological innovation and regulatory stability creates a premium market segment. Switzerland focus on quality over quantity attracts sophisticated participants seeking reliable blockchain infrastructure. This strategic positioning ensures continued influence in European blockchain standards and institutional adoption despite the country smaller population relative to larger EU economies

COMPETITIVE LANDSCAPE

The Europe Blockchain Market features intensifying competition shaped by regulatory harmonization under the Markets in Crypto Assets framework which raises entry barriers and favors well capitalized compliant operators. Global exchanges like Coinbase and Kraken compete directly with established European players such as Bitstamp for market share across trading custody and institutional services segments. Competition increasingly centers on regulatory credibility security infrastructure and integrated financial product offerings rather than transaction fee pricing alone. The transition from fragmented national regimes to unified EU licensing has triggered market consolidation as smaller non compliant operators exit while larger firms invest in multi country authorization processes. Innovation competition focuses on tokenized asset platforms decentralized finance integrations and enterprise blockchain solutions that address specific European industry needs. Talent competition remains acute with firms offering premium compensation to attract scarce blockchain developers and compliance experts. Geographic competition concentrates around innovation hubs in London Berlin Paris Amsterdam and Zug where ecosystem density facilitates partnerships and talent access. The competitive landscape continues evolving as traditional financial institutions enter the market leveraging existing customer relationships while blockchain native firms emphasize technological agility and decentralized governance models. This dynamic environment rewards participants who balance regulatory compliance with technological innovation while delivering superior user experiences across diverse European markets.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Blockchain Market include

- IBM Corporation

- Microsoft Corporation

- Amazon Web Services, Inc.

- Oracle Corporation

- SAP SE

- Accenture plc

- Infosys Limited

- Ripple Labs Inc.

- R3

Top Players in the Europe Blockchain Market

ConsenSys operates as a leading global blockchain software company with substantial European presence and influence. The organization specializes in Ethereum based infrastructure tools and enterprise solutions that enable decentralized application development. ConsenSys contributes significantly to global blockchain advancement through open source protocols developer education and institutional partnerships. Recent European actions include pursuing Markets in Crypto Assets licensing to expand compliant service offerings across member states. The company collaborates with European financial institutions on tokenization projects and digital identity frameworks. ConsenSys MetaMask wallet serves millions of European users facilitating secure access to decentralized applications. Strategic investments in European blockchain startups strengthen the regional innovation ecosystem. The organization thought leadership on regulatory engagement and technical standards shapes European blockchain policy discussions. ConsenSys commitment to interoperability and user privacy aligns with European digital values. These activities reinforce the company position as a foundational contributor to European blockchain infrastructure and global decentralized finance evolution.

Ledger stands as a prominent European blockchain security company headquartered in Paris France. The organization specializes in hardware wallet technology and cryptographic solutions for securing digital assets. Ledger contributes to global blockchain adoption by providing trusted custody infrastructure for retail and institutional users worldwide. Recent European initiatives include expanding manufacturing capacity and enhancing compliance with Markets in Crypto Assets requirements. The company Ledger Live application serves European customers with portfolio management and staking features. Strategic partnerships with European banks and fintech firms integrate Ledger security into broader financial services. Research investments in quantum resistant cryptography address future security challenges. Ledger participation in European blockchain standards bodies influences technical specifications and consumer protection frameworks. The company commitment to transparency and open source development builds trust across the ecosystem. These efforts strengthen Ledger market position while advancing secure blockchain usage throughout Europe and globally.

Bitfury operates as a leading blockchain infrastructure provider with significant European operations based in the Netherlands. The organization delivers comprehensive blockchain solutions for governments and enterprises focusing on security scalability and interoperability. Bitfury contributes to global blockchain advancement through proprietary consensus algorithms and enterprise grade platforms. Recent European actions include expanding data center partnerships and enhancing compliance with emerging digital asset regulations. The company Clarify platform enables transparent supply chain tracking for European manufacturers and retailers. Strategic collaborations with European public sector entities support digital identity and land registry implementations. Bitfury research initiatives in energy efficient consensus mechanisms align with European sustainability objectives. The organization participation in European Blockchain Services Infrastructure initiatives demonstrates commitment to public sector innovation. These activities reinforce Bitfury position as a trusted infrastructure partner for European blockchain deployment while influencing global technical standards and enterprise adoption patterns.

Top Strategies Used by Key Market Participants

Key participants in the Europe Blockchain Market deploy regulatory licensing strategies to secure Markets in Crypto Assets authorization enabling cross border service expansion throughout the European Union. Companies invest heavily in compliance infrastructure and legal expertise to navigate complex multi jurisdictional requirements while building institutional trust. Product diversification represents another core strategy with firms expanding beyond basic trading to offer staking lending and tokenized real world asset services that increase customer engagement and revenue resilience. Strategic partnerships with traditional financial institutions and fintech companies enable embedded blockchain services within existing banking ecosystems facilitating mainstream user acquisition. Technology differentiation through enhanced security protocols interoperability standards and user experience improvements creates competitive advantages in crowded market segments. Geographic expansion focuses on establishing regional headquarters in regulatory favorable jurisdictions like France Switzerland and the Netherlands to serve pan European customer bases efficiently. Talent acquisition strategies target blockchain developers compliance specialists and product managers with competitive compensation to address critical skills shortages. These coordinated strategic approaches enable market participants to strengthen positioning while adapting to evolving regulatory and competitive dynamics across the European blockchain landscape.

MARKET SEGMENTATION

This research report on the Europe Blockchain Market has been segmented and sub-segmented based on the following categories.

By Component

- Solutions

- Services

By Application

- Payments

- Digital Identity

By Industry Vertical

- BFSI

- Retail

- Government

- Transportation and Logistics

- Healthcare

- Automotive

- Media and Entertainment

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is blockchain technology?

Blockchain is a decentralized digital ledger that records transactions securely and transparently across a distributed network.

.What is driving the growth of the Europe blockchain market?

Key drivers include increasing fintech adoption, demand for secure transactions, regulatory support, and digital transformation initiatives.

Which industries are adopting blockchain in Europe?

Major industries include BFSI, healthcare, supply chain, retail, government, and energy.

What role does blockchain play in the BFSI sector?

It enables faster payments, fraud reduction, smart contracts, and improved compliance processes.

How is blockchain used in supply chain management?

It enhances transparency, traceability, and efficiency in tracking goods and verifying authenticity.

What are smart contracts in blockchain?

Smart contracts are self-executing agreements with predefined rules stored on blockchain networks.

Which countries are key contributors to the Europe blockchain market?

Germany, the UK, France, Switzerland, and the Netherlands are leading contributors.

What are the major challenges faced by the market?

Challenges include scalability issues, regulatory uncertainty, high implementation costs, and lack of skilled professionals.

What is the impact of regulations on blockchain in Europe?

Regulations such as MiCA are fostering trust while ensuring compliance and consumer protection.

What is the future outlook of the Europe blockchain market?

The market is expected to grow rapidly due to increasing adoption, innovation in Web3 technologies, and strong regulatory support.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com