Europe Brass Market Size, Share, Trends & Growth Forecast Report, Segmented By Type, Application, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Brass Market Report Summary

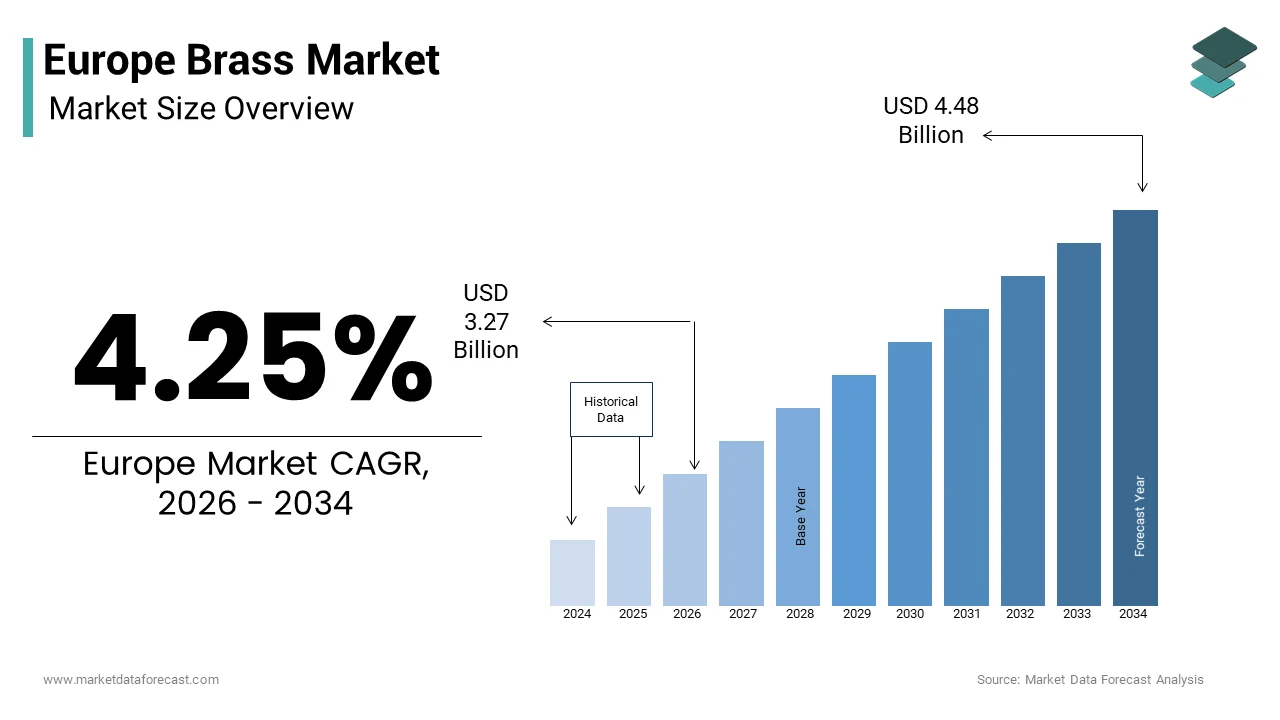

The European brass market was valued at USD 3.14 billion in 2025 and is projected to reach USD 3.27 billion in 2026, further expanding to USD 4.48 billion by 2034, growing at a CAGR of 4.25% from 2026 to 2034.

Market growth is primarily driven by rising demand from plumbing, construction, electrical, automotive, and industrial manufacturing sectors. Increasing investments in water infrastructure modernization, energy-efficient buildings, and sustainable material usage are further strengthening brass consumption across Europe. The material’s durability, corrosion resistance, recyclability, and machinability make it highly suitable for sanitary fittings, valves, connectors, and precision components.

Additionally, growing focus on eco-friendly alloys, circular economy initiatives, and advanced brass processing technologies is supporting long-term market expansion.

Key Market Trends

- Increasing demand for lead-free and eco-friendly brass alloys to comply with stringent European environmental regulations.

- Rising investments in water infrastructure and sanitation systems are boosting demand for brass fittings and valves.

- Growth in automotive electrification and electrical components, supporting brass rod and strip consumption.

- Expansion of precision engineering and industrial machinery sectors across Germany and Italy.

- Strong emphasis on metal recycling and circular economy practices, enhancing sustainable brass production.

Segmental Insights

By Type

The brass rods segment dominated the European brass market, accounting for 55.1% of the total market share in 2025. Brass rods are widely used in machining applications, plumbing fittings, fasteners, and electrical connectors due to their excellent formability and corrosion resistance.

By Application

The plumbing and sanitary applications segment was the largest, capturing 40.7% of the market share in 2025. The dominance of this segment is attributed to increased residential and commercial construction activities, modernization of water supply systems, and stringent quality standards for sanitary components across Europe.

Regional Insights

- Germany was the leading country in the European brass market, accounting for 28.6% of the market share in 2025. The country’s strong industrial base, advanced manufacturing ecosystem, and robust automotive and engineering sectors drive high brass consumption.

- Italy followed with 20.5% market share in 2025, supported by its well-established metal processing industry and strong presence of brass component manufacturers.

- France maintains a significant share due to government-driven investments in water infrastructure and aerospace manufacturing.

- The United Kingdom is experiencing steady growth, supported by construction and industrial recovery.

- The Netherlands is expected to witness steady expansion over the forecast period, driven by sustainable infrastructure projects and industrial modernization.

Competitive Landscape

The European brass market is moderately consolidated, with leading manufacturers focusing on alloy innovation, sustainability, and capacity expansion to strengthen their regional presence. Companies are investing in advanced processing technologies, recycling facilities, and strategic partnerships to meet evolving industrial and environmental requirements.

Prominent players operating in the European brass market include Wieland Group, KME Group S.p.A., Aurubis AG, Ningbo Jintian Copper (Group) Co., Ltd., Mitsubishi Materials Corporation, Poongsan Corporation, Luvata, Diehl Metall Stiftung & Co. KG, Midland Industries, and TS Brass.

These companies are strengthening their footprint through product diversification, sustainable alloy development, and expansion across high-growth European industrial sectors.

Europe Brass Market Size

The Europe brass market size was valued at USD 3.14 billion in 2025 and is anticipated to reach USD 3.27 billion in 2026 to USD 4.48 billon by 2034, growing at a CAGR of 4.25% during the forecast period from 2026 to 2034.

Current Introduction of the Europe Brass Market

Brass is a versatile metal alloy primarily composed of copper and zinc. It is highly valued for its golden appearance, durability, and ease of machining, making it a staple in both industrial and decorative applications. Unlike generic metal markets, brass in Europe is defined by its strategic role in precision engineering and heritage conservation. European brass demand is concentrated within a few major manufacturing nations, with Germany, Italy, and France acting as the primary drivers of consumption. Brass is indispensable in plumbing fittings, valves, and heat exchangers due to its antimicrobial properties and pressure tolerance—attributes recognized under the updated European Drinking Water Directive, which strictly limits allowable lead content in potable water components, and accelerates the transition to high-purity, lead-free brass alloys across the EU. The European Committee for Standardization enforces strict alloy classifications (e.g., CW602N, CZ121) to ensure performance consistency. Brass production in Europe relies heavily on recycled materials, with a high proportion of input sourced from post-consumer scrap, aligning the sector with circular economy principles. Artisanal foundries in Italy and France also sustain demand for architectural and decorative brass, preserving centuries-old casting traditions. This dual identity, as both a high-performance engineering material and a cultural heritage medium, positions brass as a uniquely resilient and regulated segment within Europe’s non-ferrous metals landscape.

MARKET DRIVERS

Stringent Regulations on Lead Content in Potable Water Systems

The EU’s aggressive phase-out of lead in drinking water infrastructure has led the way for specialized brass demand across the region, which fuels the growth of the Europe brass market. European regulations are enforcing stricter lead limitations for materials used in drinking water, compelling a industry-wide shift toward nearly lead-free components. This has spurred widespread adoption of lead-free brass alloys such as CW510L and CW602N, which substitute bismuth or silicon for lead while maintaining machinability. Compliance with new European material standards for plumbing fittings is rising rapidly as manufacturers proactively adopt new, low-lead alloys ahead of the mandatory, official deadlines. Germany is moving to remove legacy plumbing materials by updating national standards for the reduction of lead in water systems. Stricter, EU-wide, environmental and health policies are aimed at reducing lead in drinking water to mitigate childhood exposure risks and improve long-term health outcomes. This regulatory shift not only ensures public health but also creates a stable, non-discretionary market for high-purity, certified brass alloys, insulating the sector from broader economic fluctuations.

Revival of Heritage Architecture and Urban Restoration Projects

The region’s commitment to preserving its architectural legacy spurs consistent demand for traditional brass in restoration and high-end interior design, which in turn boosts the expansion of the Europe brass market. Historic buildings, protected under national heritage laws and EU cultural funding programs, require authentic materials for door hardware, lighting fixtures, and decorative elements. Europa Nostra and associated European heritage initiatives are promoting the sustainable restoration of Europe’s historic building stock, increasing demand for authentic, hand-finished metalwork to maintain original building specifications. France’s specialized lottery for cultural heritage continues to fund the restoration of national monuments, fostering the revival of traditional artisanal metal casting and restoration businesses in major French cities. Similarly, Italy’s extensive tax incentive programs for building energy efficiency and seismic upgrading have facilitated the renovation of historic buildings, leading to increased demand for high-quality, period-appropriate fixtures during restorations. The European Commission’s Cultural Heritage Strategy further funds cross-border projects like the rehabilitation of Art Nouveau facades in Brussels and Barcelona, where brass detailing is essential. This cultural imperative transcends cost considerations, ensuring premium demand for specialty alloys and skilled craftsmanship that cannot be replicated by substitutes.

MARKET RESTRAINTS

Volatility in Copper and Zinc Raw Material Prices

Brass production in the region faces significant cost instability due to extreme fluctuations in copper and zinc prices, the two primary constituents of the alloy, which inhibit the growth of the Europe brass market. Copper, which typically comprises 60 to 70 percent of brass, saw its London Metal Exchange saw significant volatility between 2023 and 2024 due to supply chain disruptions in Chile and speculative trading. Zinc costs spiked following the idling of major European processing facilities in response to rising power expenses. Industrial trade groups indicate that the vast majority of brass manufacturing expenses are tied to the price of raw metals, which limits the ability of producers to absorb sudden market fluctuations. Unlike integrated steel producers, most European brass mills operate on a tolling or semi-tolling basis, unable to hedge long-term metal exposure. This volatility discourages fixed-price contracts, delays investment in new capacity, and forces smaller workshops to absorb losses during price spikes. Lacking hedging tools and strategic reserves, the sector is exposed to volatile commodity cycles, which hinders pricing stability and long-term planning.

Complexity of Alloy Certification and Fragmented Standards

Compliance challenges and trade barriers because of varying national interpretations of alloy standards hinder the expansion of the Europe brass market. This is despite EU harmonization efforts. In addition to European standards, Germany and France impose specific,, rigorous certifications for pressure and plumbing applications, adding complexity to compliance. The existence of numerous specific alloy designations within the European standardization system complicates cross-border procurement, requiring careful navigation of diverse material specifications. A valve manufacturer in Poland may need three separate test reports to sell the same CW614N alloy in Italy, Spain, and Sweden. This fragmentation increases administrative costs, extends time-to-market, and disadvantages SMEs lacking regulatory expertise. Furthermore, the lack of a unified digital material passport system hinders traceability for recycled content claims. The brass industry remains stuck with a fragmented, inefficient patchwork of regulations across the single market, hindering innovation and competitive growth until full alignment under the Construction Products Regulation is achieved.

MARKET OPPORTUNITIES

Integration of Brass in Renewable Energy and Heat Pump Systems

The European Green Deal is unlocking new high-performance applications for brass in clean energy infrastructure, particularly in heat pumps and solar thermal systems, which is expected to drive the growth of the Europe brass market. Brass’s excellent thermal conductivity, pressure resistance, and compatibility with refrigerants make it ideal for manifolds, connectors, and expansion valves in residential and commercial heat pumps. Following a period of rapid growth, heat pump installations in the EU decreased in 2024 due to market, financial, and policy challenges, which reduced the short-term demand for high-strength brass components. The REPowerEU initiative calls for a major acceleration in the cumulative number of installed heat pumps by 2030 to reduce dependence on fossil fuels, driving high cumulative demand for brass and other components. Additionally, brass is used in solar thermal collectors for its corrosion resistance in glycol-based heat transfer fluids. Companies like IMI Hydronic Engineering and Danfoss are specifying lead-free brass alloys that meet both pressure equipment directives and circularity criteria. The rapid pace of decarbonization is transforming brass from a traditional material into a critical component for Europe’s thermal energy shift.

Development of High-Recycled-Content Brass with Full Traceability

Innovation in closed-loop recycling is transforming brass into a flagship material for the circular economy, which creates premium opportunities in sustainability-conscious landscapes and the Europe brass market. European producers like Aurubis and KME have developed certified brass alloys containing a significant portion of recycled copper and zinc, with full chain-of-custody documentation via blockchain-enabled material passports. According to the International Copper Association, recycling brass significantly reduces energy consumption compared to primary production, resulting in a substantially lower carbon footprint per ton of material. The EU Ecolabel now recognizes high-recycled-content brass in building products, enabling green public procurement. Architectural firms in the Netherlands and Denmark increasingly specify “circular brass” for LEED and BREEAM-certified projects, willing to pay a premium. Pilot programs like Brass2Brass in Belgium demonstrate near-infinite recyclability without quality loss. The expansion of Extended Producer Responsibility (EPR) schemes is driving brass manufacturers to shift from mere commodity suppliers to stewards of resources, directly supporting European net-zero ambitions through scrap recycling.

MARKET CHALLENGES

Labor Shortages in Precision Machining and Foundry Operations

A critical barrier in skilled labor, particularly in precision machining and traditional foundry work, threatens production capacity, quality, and the growth of the Europe brass market. According to reports from the CAEF, the European Foundry Association, a high proportion of the non-ferrous foundry workforce in key manufacturing nations, including Germany, Italy, and France, is composed of older employees, while interest in apprenticeship programs has significantly declined. The decline stems from vocational education shifts toward digital fields and the perception of metalworking as physically demanding and outdated. This shortage delays orders for custom architectural hardware and high-tolerance industrial valves, where hand-finishing and mold-making expertise are irreplaceable. In response, companies invest in CNC automation, but complex heritage reproductions still require artisanal skills. Europe risks losing invaluable tacit knowledge and weakening both industrial production and cultural preservation if targeted skilled-trade immigration and workforce development policies are not implemented.

Geopolitical Disruptions in Copper Scrap Supply Chains

The region’s reliance on imported copper scrap, a key input for brass, creates systemic vulnerability to geopolitical and logistical shocks that further limits the expansion of the Europe brass market. Despite a substantial reliance on domestic recycling to meet demand, the European Union depends on international imports of copper and brass scrap from major global suppliers, including the United States, to sustain its manufacturing sector. Increased volatility in global scrap supply chains, coupled with shifting trade policies in key importing nations, has created upward pressure on European brass mill premiums. Similarly, Red Sea shipping disruptions in early 2024 delayed deliveries from Asian suppliers, forcing mills to ration allocations. Unlike primary metals, scrap quality varies widely, requiring rigorous sorting that few EU ports can perform at scale. The EU Critical Raw Materials Act does not classify copper scrap as strategic, leaving no coordinated reserve system. This dependency on fragmented, overseas sources exposes the brass industry to trade policy shifts, transport bottlenecks, and quality inconsistencies, jeopardizing supply security for a material deemed essential for water safety and energy transition.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.25% |

| Segments Covered | By Type, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, & Rest of Europe |

| Market Leaders Profiled | Wieland Group (Germany), KME Group S.p.A. (Italy), Aurubis AG (Germany), Ningbo Jintian Copper (Group) Co., Ltd. (China), Mitsubishi Materials Corporation (Japan), Poongsan Corporation (South Korea), Luvata (Finland), Diehl Metall Stiftung & Co. KG (Germany), Midland Industries (U.S.), TS Brass (U.S.) |

SEGMENTAL ANALYSIS

By Type Insights

The brass rods segment dominated the Europe brass market by accounting for a 55.1% share in 2025. The dominance of the brass rods segment is primarily driven by its versatility in precision machining and industrial component manufacturing. These solid cylindrical forms serve as the primary feedstock for CNC lathes producing valves, fittings, gears, and plumbing hardware, applications where dimensional stability and machinability are critical. According to various studies, the tightening of the EU Drinking Water Directive has accelerated the transition in the European market toward lead-free brass alloys, making compliant materials like CW510L the primary choice for new, eco-friendly sanitary fittings and water applications. The segment’s leadership is reinforced by established supply chains linking integrated producers like Aurubis and KME to thousands of small and medium machining workshops across Germany, Italy, and France. Unlike wires, which serve niche electrical roles, rods support high-volume, high-precision applications in construction, automotive, and machinery sectors. Their compatibility with automated bar-fed machining centers ensures consistent throughput and minimal waste, making them the backbone of Europe’s precision engineering ecosystem.

The brass wires segment is anticipated to witness the fastest CAGR of 5.3% from 2026 to 2034 due to rising demand for fine-diameter conductive and decorative elements in electronics, automotive sensors, and architectural mesh systems. In the electrical sector, brass wire is increasingly used in connectors and terminals for electric vehicle charging infrastructure due to its superior spring properties and corrosion resistance compared to pure copper. Driven by the increasing electrification of automobiles, the demand for specialized copper-based components, such as brass wire in electrical systems, has experienced significant growth, although the pace of this consumption growth has faced fluctuations due to the shifting speed of European electric vehicle adoption. Simultaneously, architectural firms in Scandinavia and the Benelux are specifying woven brass mesh for solar shading and façade cladding, leveraging its aesthetic warmth and durability. Innovations in continuous casting and drawing technologies now enable diameters below 0.1 millimeters with tight tolerances, opening micro-electronics applications. The intersection of miniaturization and green design is transforming brass wire from a simple commodity into a vital enabler of beautiful, intelligent infrastructure.

By Application Insights

The plumbing and sanitary applications segment was the largest segment in the Europe brass market by capturing a 40.7% share in 2025. The supremacy of the plumbing and sanitary applications segment is attributed to stringent regulations on potable water safety and urban infrastructure renewal. Brass is the material of choice for faucets, valves, and pipe fittings due to its pressure tolerance, antimicrobial properties, and machinability, attributes codified in national building codes across the EU. Driven by tightening EU Drinking Water Directives, the European plumbing industry is rapidly shifting toward lead-free brass alloys, significantly reducing lead content in new residential installations to comply with stricter regulatory standards. Following the revision of its national Drinking Water Ordinance, Germany is actively pursuing the removal of legacy lead piping in building installations to meet stringent, updated safety requirements. The European Environment Agency, in conjunction with public health initiatives, projects that complete compliance with stringent environmental regulations will substantially lower the occurrence of elevated blood lead levels in children. This regulatory mandate creates non-discretionary, recession-resilient demand that anchors the brass market far beyond aesthetic or cost considerations, ensuring steady consumption regardless of economic cycles.

The electrical and electronic components segment is likely to experience the fastest CAGR of 6.1% owing to the continent’s digital transformation and electrification of transport and energy systems. Brass’s unique combination of electrical conductivity, strength, and corrosion resistance makes it ideal for terminals, connectors, and relay components in electric vehicle charging stations, renewable energy inverters, and smart grid infrastructure. According to recent European infrastructure reports, the rapid expansion of public EV charging networks across the EU is driving increased demand for high-precision brass components within charging connectors, with a significant number of new public points deployed throughout the region in 2024. Additionally, data center expansion, driven by AI and cloud computing, demands reliable brass connectors for server racks and cooling systems. The shift toward miniaturized, high-reliability electronics favors brass over alternatives like aluminum or steel, ensuring sustained growth in this high-tech, high-value segment aligned with Europe’s strategic autonomy goals.

COUNTRY ANALYSIS

Germany Brass Market Analysis

Germany led the Europe brass market by holding a 28.6% share in 2025. The leading position of the German market is driven by its world-class machinery, automotive, and plumbing industries. The country’s market status reflects deep integration of brass into precision engineering: thousands of small and medium enterprises use brass rods to produce valves, gears, and hydraulic components for global supply chains. German machinery manufacturers continue to be major consumers of brass, with high demand for metal, although the overall sector experienced a decline in export volume during 2024. The nation’s strict enforcement of the Drinking Water Ordinance has accelerated adoption of lead-free brass in all new plumbing installations. Major producers like Wieland-Werke and Diehl Metall operate advanced rolling and extrusion facilities, supplying high-tolerance rods and wires across Europe. Germany operates a significant copper alloy recycling infrastructure, with manufacturing processes heavily reliant on the extensive use of recycled scrap rather than virgin materials. This blend of industrial scale, regulatory rigor, and circularity solidifies Germany’s position as the continent’s brass innovation and consumption leader.

Italy Brass Market Analysis

Italy followed closely in the European brass market by accounting for a 20.5% share in 2025. The growth of the Italian market is fuelled by its dual identity as a hub for industrial machining and artisanal heritage craftsmanship. The market status is defined by thousands of small foundries and workshops in Lombardy and Emilia-Romagna producing precision brass components for luxury automotive, HVAC, and sanitary brands like Caleffi and Grohe. Italian manufacturers of semi-finished brass products, particularly in the rods and forgings sector, maintain a high volume of international exports, solidifying the country’s position as a significant European supplier. Simultaneously, historic cities like Florence and Venice drive demand for hand-cast brass door handles, lighting fixtures, and decorative elements under national heritage restoration laws. The “110 Percent Superbonus” tax incentive includes brass fixtures in eligible renovation expenses, sustaining premium demand. Companies like Luvata Italia specialize in high-recycled-content alloys, aligning tradition with sustainability. This fusion of industrial precision and cultural preservation makes Italy a uniquely resilient and diversified player in the European brass landscape.

France Brass Market Analysis

France maintains a significant share of the European brass market due to strong policy-driven demand in water infrastructure and aerospace. The market status reflects national mandates under the Loi Eau et Assainissement, which requires all new plumbing to use lead-free brass certified under NF EN 12165 standards. In accordance with its national water conservation strategy, France is actively implementing measures to improve water efficiency in public infrastructure by upgrading plumbing fixtures to reduce consumption. Additionally, aerospace giants like Safran and Airbus use high-strength brass alloys in fuel system components and sensor housings, demanding ultra-pure, traceable materials. Pechiney (now part of Constellium) and Tréfimétaux operate major rod and wire mills in Isère and Normandy, supplying both industrial and heritage sectors. France also leads in brass recycling, with a significant of input derived from domestic scrap streams. This combination of regulatory enforcement, high-tech manufacturing, and circular economy practices sustains France’s dynamic and quality-oriented brass ecosystem.

United Kingdom Brass Market Analysis

The United Kingdom experienced a steady expansion in the European brass market, with growth centered on plumbing, heritage restoration, and defense applications. The market status is shaped by the Water Supply Regulations 1999, which mandate lead-free brass (<0.1 percent Pb) for all potable water fittings, a standard rigorously enforced by WRAS certification. UK government social housing retrofit programs are increasing their focus on sustainability, leading to widespread replacement of outdated plumbing components in older properties. Legal protections for listed buildings encourage the use of traditional materials like brass for repairs, maintaining demand for specialized, traditional craftsmanship. Heritage agencies continue to provide financial support and technical guidance for the restoration of historic architectural metalwork, such as ironwork and bronze, to ensure the longevity of listed sites. Companies like British Alloys and Aalco supply high-precision rods to defense contractors for naval valve systems, leveraging brass’s seawater corrosion resistance. Despite Brexit, the UK continues to align with EU alloy standards, ensuring seamless integration into European supply chains. This mix of regulatory compliance, cultural heritage, and strategic defense needs ensures the UK remains a high-value segment in the regional market.

Netherlands Brass Market Analysis

The Netherlands is predicted to grow in the European brass market over the forecast period due to its focus on circular economy models and high-tech electronics. The market status is also supported by leadership in brass recycling and remelting: companies like Metallo and Aurubis Netherlands process thousands of metric tons of copper alloy scrap annually into certified lead-free ingots. The Dutch government is accelerating the adoption of a circular economy in the construction sector, prompting public projects to prioritize materials with verified, recycled, or sustainable content, which in turn increases demand for high-performance, infinitely recyclable metal alloys in building infrastructure systems. Simultaneously, the Eindhoven high-tech campus, home to ASML and NXP, requires ultra-pure brass wires for semiconductor equipment connectors and sensor housings. The Port of Rotterdam facilitates efficient import of scrap and export of semi-finished products, enhancing logistical reach. This forward-looking approach, prioritizing traceability, recycling, and precision engineering, positions the Netherlands as a sustainability and innovation benchmark in Europe’s evolving brass landscape.

COMPETITIVE LANDSCAPE

The Europe Brass Market features a concentrated yet specialized competitive landscape dominated by integrated producers with strong recycling capabilities and technical expertise. Companies like Aurubis KME and Wieland compete on alloy purity certification compliance and sustainability credentials rather than price alone. New entrants face high barriers including capital intensity scrap sourcing logistics and stringent regulatory requirements for lead-free compositions. The market is bifurcated between industrial segments where precision and consistency matter and heritage applications where artisanal quality is paramount. Competition is not characterized by aggressive pricing but by long term partnerships with machining workshops plumbing OEMs and restoration architects. Innovation focuses on circularity through closed loop recycling and decarbonization via renewable powered melting rather than material substitution. Regulatory alignment with EU drinking water and construction product directives is critical for market access. This environment rewards operational excellence regulatory foresight and strategic alignment with Europe’s green and digital transitions over scale or marketing intensity.

KEY MARKET PLAYERS

- Wieland Group (Germany)

- KME Group S.p.A. (Italy)

- Aurubis AG (Germany)

- Ningbo Jintian Copper (Group) Co., Ltd. (China)

- Mitsubishi Materials Corporation (Japan)

- Poongsan Corporation (South Korea)

- Luvata (Finland)

- Diehl Metall Stiftung & Co. KG (Germany)

- Midland Industries (U.S.)

- TS Brass (U.S.)

Top Players In The Market

- Aurubis AG is a leading European copper and brass producer headquartered in Germany with integrated operations across the continent. The company supplies high-purity brass rods, wires, and ingots to automotive, plumbing, and electronics sectors while maintaining a significant global footprint through its recycling and smelting expertise. Aurubis contributes to the worldwide market by pioneering closed-loop recycling systems that transform complex copper alloy scrap into certified lead-free brass. Recently, the company expanded its Hamburg facility to produce EN 12165-compliant brass rods with a significant share of recycled content, supporting EU drinking water safety mandates. It also launched a blockchain-based material passport system to provide full traceability of recycled content, reinforcing its leadership in sustainable non-ferrous metals and strengthening its position as a trusted partner for green infrastructure projects.

- KME Group is a major European brass manufacturer with production sites in Germany, Italy, and France, specializing in precision rods, tubes, and profiles for industrial and sanitary applications. The company serves global markets through its high-tolerance machining capabilities and strict compliance with international alloy standards. KME contributes to the global brass industry by developing advanced lead-free formulations like KME ECO BRASS, which meets both EU and US plumbing regulations. Its investment aligns with Europe’s energy transition goals and enhances KME’s ability to supply next-generation clean technology components with verified sustainability credentials.

- Wieland-Werke AG is a German multinational renowned for its high-performance copper and brass semi-finished products used in automotive, electrical, and architectural applications worldwide. The company operates state-of-the-art rolling and extrusion facilities across Europe and supplies premium brass rods and wires to precision engineering workshops. Wieland contributes globally through its innovation in antimicrobial brass alloys and ultra-fine wire for microelectronics. Recently, it launched a new range of WRAS-certified lead-free brass rods for UK and EU plumbing markets, featuring enhanced machinability without bismuth. The company also partnered with a Dutch heritage restoration consortium to develop custom sand-cast brass alloys matching historic specifications, blending industrial excellence with cultural preservation to strengthen its diversified market presence.

Top Strategies Used By The Key Market Participants

Key players in the Europe Brass Market are investing in advanced recycling technologies to produce high-purity brass with up to 95 percent recycled content meeting stringent environmental standards. They are developing lead-free and bismuth-free alloys to comply with EU Drinking Water Directive and WRAS certification requirements. Companies are implementing blockchain based material passports to ensure full traceability of recycled content and support green public procurement. Strategic expansion of continuous casting and precision drawing lines enables production of high tolerance rods and wires for electric vehicle and heat pump components. Collaboration with heritage restoration projects preserves traditional brass applications while promoting circularity. Integration of digital quality control systems ensures consistent compliance with EN DIN and NF alloy standards across member states. Geographic consolidation of melting and extrusion assets improves energy efficiency and reduces carbon footprint. Innovation in antimicrobial and corrosion resistant brass grades addresses healthcare and marine sector demands. Participation in EU funded circular economy initiatives strengthens post consumer scrap collection infrastructure. Development of ultra fine brass wires supports miniaturization trends in electronics and sensor manufacturing.

MARKET SEGMENTATION

This research report on the Europe brass market is segmented and sub-segmented into the following categories.

By Type

- Brass Wires

- Brass Rods

- Others

By Application

- Electrical & Electronic Components

- Machinery & Industrial Components

- Plumbing & Sanitary

- Automotive

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe brass market?

It refers to the regional industry for brass alloys used in construction, automotive, electrical, plumbing, and decorative applications.

What drives growth in the Europe brass market?

Infrastructure development, strong automotive and electrical manufacturing sectors, and rising demand for corrosion-resistant alloys drive market growth.

What is brass made of?

Brass is an alloy primarily composed of copper and zinc, offering strength, conductivity, and corrosion resistance.

Which industries consume the most brass in Europe?

Construction, automotive components, electrical & electronics, hardware fittings, and plumbing sectors are key consumers.

How does brass benefit construction applications?

Brass offers durability, corrosion resistance, and aesthetic appeal, making it ideal for fixtures, fittings, and architectural elements.

Is brass used in automotive manufacturing?

Yes, brass is used for radiators, bearings, connectors, and various precision components in vehicles.

How do brass properties influence electrical applications?

Good electrical and thermal conductivity make brass suitable for connectors, terminals, and electrical components.

What trends are shaping the European brass market?

Trends include demand for eco-friendly alloys, recycled metal usage, and performance-optimized brass for specialty applications.

How does recycling impact the brass market?

High recyclability reduces production costs, conserves raw materials, and supports sustainable manufacturing practices.

Are European regulations affecting the brass industry?

Yes, EU standards on material safety, toxic metals, and environmental compliance influence product development and usage.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com