Europe Breast Imaging Market Size, Share, Trends & Growth Forecast Report By Technology, and By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

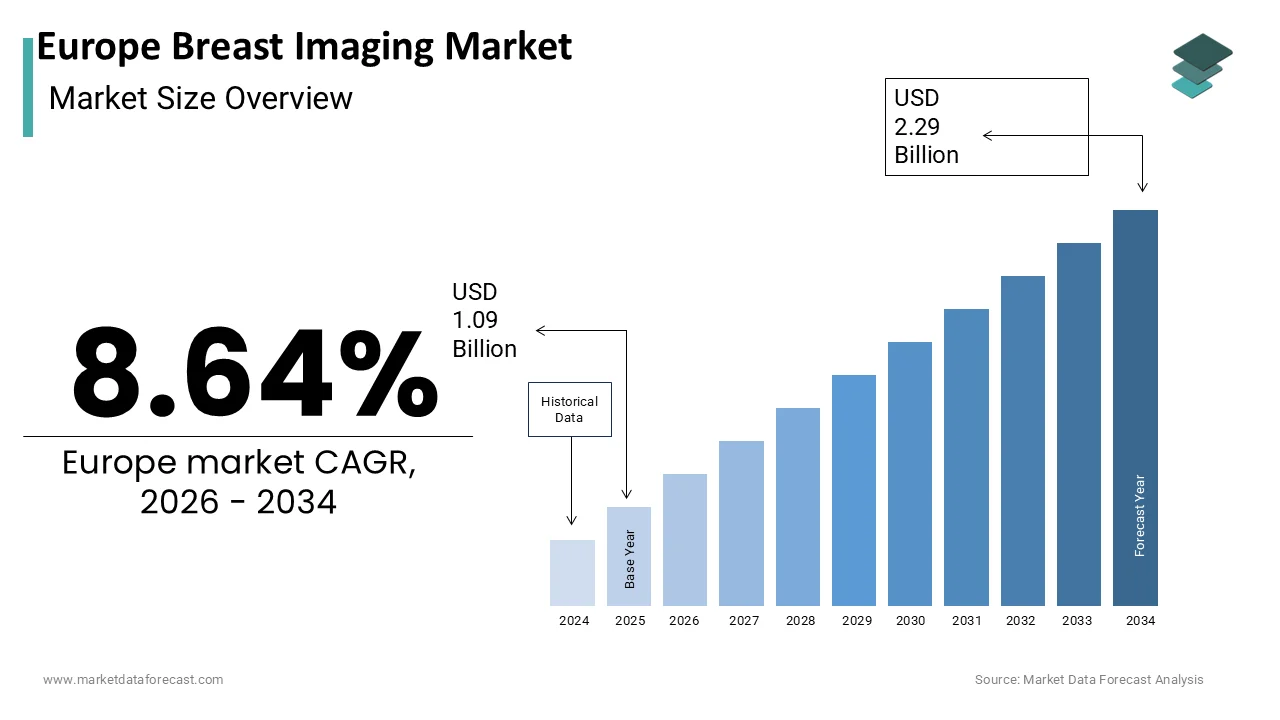

$1.09 BnMarket Estimate, 2026

$1.18 BnMarket Forecast, 2034

$2.29 BnCAGR, 2026–2034

8.64%Europe Breast Imaging Market Size

The Europe Breast Imaging Market Size was valued at USD 1.09 billion in 2025, is expected to have an 8.64% CAGR from 2026 to 2034 and be worth USD 2.29 billion by 2034 from USD 1.18 billion in 2026.

The breast imaging is designed to detect and characterize breast abnormalities with high sensitivity and specificity. The clinical imperative for early detection is the burden of breast cancer ,which remains the most frequently diagnosed malignancy among women in the region. According to the World Health Organization, breast cancer accounts for nearly 30 percent of all new cancer cases in European women, with over 500000 new diagnoses annually. National screening programs mandated under the European Commission’s Council Recommendation on Cancer Screening cover approximately 60 percent of the eligible female population aged 50 to 69, as per the Joint Research Centre.

MARKET DRIVERS

Mandatory National Screening Programs Drive Consistent Imaging Demand

The organized population-based breast cancer screening initiatives across European Union member states constitute a foundational driver of sustained demand for breast imaging services and equipment is a major factor propelling the growth of the Europe breast imaging market. According to the European Commission’s Joint Research Centre, 27 out of 27 EU countries have implemented national screening programs targeting women aged 50 to 69 with biennial mammography as the standard of care. The European Guidelines for Quality Assurance in Breast Cancer Screening and Diagnosi,s updated in 20,23 further stipulate minimum technical standa,rds including the use of digital detectors and double reading protocols, which compel healthcare providers to upgrade legacy analog systems.

Rising Incidence of Breast Cancer Intensifies Diagnostic Workload

The escalating burden of breast cancer across Europe directly amplifies the need for advanced and frequent imaging interventions beyond routine screening is additionally to leverage the growth of the Europe breast imaging market. In the United Kingdom, breast cancer incidence has increased by 6 percent over the past decade, with one in seven women now expected to develop the disease during their lifetim,e as per Cancer Research UK.

MARKET RESTRAINTS

Workforce Shortages Limit Imaging Capacity and Interpretation Quality

The radiologists and specialized breast imaging professionalconstrainns the scalability and diagnostic accuracy is a primary factor inhibiting the growth of the Europe breast imaging market. According to the European Society of Radiology, the EU faces a deficit of over 8000 radiologists, with breast imaging being among the most underserved subspecialties.

Fragmented Reimbursement Policies Discourage Technology Adoption

The inconsistent and often restrictive reimbursement frameworks across European healthcare systems impede the widespread deployment ofnext-generationn breast imaging technologies, is additionallyhindersr the growth of the Europe breast imaging market. While digital breast tomosynthesis demonstrates superior cancer detection rates and lower recall rates, numerous countries still reimburse it at the same rate as conventional 2D mammography or exclude it entirely from public funding. According to the European Federation of Radiographer Societies, only 11 EU member states provide full reimbursement for tomosynthesis as of 202,3 with countries like Spain and Greece, whiclimitng coverage to symptomatic or high-risk cases. These financial disincentives deter hospitals from investing in capital-intensive upgrades, particularly in publicly funded settings where budgets are tightly controlled.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence Enhances Diagnostic Precision and Workflow

The incorporation of artificial intelligence into breast imaging workflows to augment radiologist performance and optimize resource utilization is creating new opportunities for the growth of the Europe breast imaging market. AI algorithms trained on diverse European datasets can assist in lesion detection risk stratification and workflow prioritization with demonstrated clinical impact. The European Medicines Agency has cleared over 25 AI-based breast imaging software solutions since 2021, including tools from Lunit and ScreenPoint that are now deployed in Franc,e Ita,ly and Belgium.

Expansion of Screening to Younger and High-Risk Cohorts Creates New Demand

Evolving clinical guidelines that broaden breast cancer screening eligibility to younger women and genetically predisposed populations will additionally enhance the growth of the Europe breast imaging market. Additionally, several countries, including the United Kingdom and German,y are pilotinrisk-stratifieded screening that incorporates genetic and lifestyle factors to tailor imaging frequency and modality. This shift from age-based to risk-based screening multiplies the number of imaging encounters per patient and necessitates multimodal diagnostic platforms.

MARKET CHALLENGES

Radiation Dose Concerns Impede Adoption of Advanced Modalities

Persistent patient and clinician apprehension regarding ionizing radiation exposure continues to challenge the adoption of certain advanced breast imaging technologies, despite their diagnostic benefits is likely to degrade the growth of the Europe breast imaging market. According to a 2023 survey by the European Patients Forum, 38 percent of women aged 40 to 60 expressed reluctance to undergo repeated mammograms due to radiation fears.

Data Interoperability Gaps Undermine Integrated Care Pathways

The absence of standardized data formats and seamless integration between breast imaging systems and electronic health is alsoinhibitingt the growth of the Europe breast imaging market. Most imaging departments operate on proprietary Picture Archiving and Communication Systems that do not readily exchange structured reports or quantitative imaging biomarkers with oncology or primary care platforms. This fragmentation forces manual data entry, delays multidisciplinary tumor board reviews, and increases the risk of information loss during care transitions. Although the EU’s eHealth Digital Service Infrastructure promotes health data exchang,e breasimaging-specificic profiles under the Integrating the Healthcare Enterprise framework remain inconsistently implemented.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Technology and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Hologic, Inc., GE Healthcare, Siemens Healthcare, Philips Healthcare, Fujifilm Holdings Corporation, Gamma Medica, Inc., Toshiba Corporation, Sonocine, Inc., Aurora Imaging Technology, Inc., Dilon Technologies, Inc. |

SEGMENTAL ANALYSIS

By Technology Insights

The ionizing technologies segment held a dominant share of the Europe breast imaging market in 2025, with the entrenched role of mammography,, both 2D digital and digital breast tomosynthesis,, in national screening programs across all 27 EU member states. In Germa,ny over 95% of accredited screening units use digital mammogra,phy with tomosynthesis adoption exceeding 60 percent in diagnostic settings as per the German Radiological Society. The regulatory infrastruc,ture including dose monitoring protocols and equipment accreditation standards established under the Euratom Basic Safety Stan,dards further entrenches ionizing technologies within public health systems.

The non-ionizing technologies segment is likely to grow with an expected CAGR of 11.4% during the forecast period,, with the rising demand for radiation-free alternatives,, particularly among younger women dense dense-breasted populations and those requiring frequent monitoring. Breast ultrasound now serves as a mandatory adjunct in 14 EU countries for women with heterogeneously or extremely dense breasts,, which constitute nearly 48 percent of women under 50 as per the European Dense Breast Consortium. The declining cost of handheld and automated ultrasound systemhasve fallen by 35 percent since 2020,according tor Eurostat has enabling deployment in outpatient and primary care settings.

COUNTRY LEVEL ANALYSIS

Germany Breast Imaging Market Analysis

Germany was the top performer of the Europe breast imaging market with 21.3% of share in 2025,, with its rigorous national cancer screening progra,m, high healthcare expenditure,, and early adoption of advanced imaging technologies. Over 98% of German screening units are certified under the European quality assurance framework, with digital breast tomosynthesis installed in more than65%t of diagnostic centers as per the German Radiological Society. Germany also hosts Europe’s highest density of certified breast imaging specialists with over 4500 radiologists holding subspecialty credentials.

France Breast Imaging Market Analysis

France was ranked second by accounting for 16.7% of the Europe breast imaging market share in 2025, with the screening program that achieves 58 percent participation among eligible women and a progressive regulatory stance on emerging technologies. France was among the first EU nations to approve reimbursement for digital breast tomosynthesis in both screening and diagnostic contexts following a 2021 health technology assessment that demonstrated a 30 percent reduction in recall rates. Furthermore, France leads in genetic risk stratification with BRCA testing integrated into routine care forhigh-riskk families, enabling targeted MRI surveillance.

United Kingdom Breast Imaging Market Analysis

The United Kingdom breast imaging market is anticipated to grow with a significant CAGR during the forecast period. The NHS Breast Screening Programme serves 2.1 million women annually and has piloted AI triage in 12 centers,, reducing radiologist workload by 40 percent as per the Royal College of Radiologists. The recent approval ocontrast-enhanceded mammography for symptomatic clinics in England offers a cost-effective alternative to MRI.

Italy Breast Imaging Market Analysis

Italy's's breast imaging market growth is growing rapidly with significant growth opportunities during the forecast period,, with its extensive, organized screening network covering 95% of the eligible population and high disease burden with over 55000 new cases annually. The Ministry of Health’s National Oncology Plan allocates 85 million euros to upgrade 300 imaging units with tomosynthesis and AI support by 2025. Furthermore, Italy hosts Europe’s largest number of private imaging centers,, which complement public services and accelerate technology diffusion.

TOP LEADING PLAYERS IN THE MARKET

- HologiInc.nc is a leading innovator in breast imaging with a strong footprint across Europe through its 3D mammography and Genius AI Detection platform. The company pioneered digital breast tomosynthesis and continues to shape clinical standards through extensive validation studies conducted with European institutions. In recent years,, Hologic has expanded its European service network and secured regulatory approvals for its Clarity HD high-resolution imaging and SmartCurve patient comfort technology in over 20 countries. The company also partnered with national screening programs in Sweden and the Netherlands to integrate its AI tools into routine workflows,, enhancing detection accuracy while reducing radiologist workload in alignment with EU diagnostic efficiency goals.

- Siemens Healthineers plays a pivotal role in the Europe breast imaging market by offering a comprehensive portfolio that spans mammography, ultrasound,, and magnetic resonance imaging systems,, tailored to European clinical protocols. The company’s MAMMOMAT Fusion and Selenia Dimensions platforms are widely deployed in public screening centers and academic hospitals. Recently, Siemens Healthineers launched its AI Roi solution across Germany,, Fran,ce and Italy,, enabling automated region of interest identification to streamline reading workflows. The company also strengthened its position by integrating breast imaging data into its Teamplay digital health platform facilitating cross modality analytics and supporting the EU’s push for interoperable diagnostic ecosystems under the Digital Europe Programme.

- GE Healthcare maintains a significant presence in Europe through its Senographe Pristina and Pristina Dueta mammography systems which emphasize patient comfort and dose efficiency. The company actively collaborates with European radiology societies to validate its AI powered tools such as TrueLook and TrueRecall for use in dense breast populations. In 2023, GE Healthcare rolled out its Edison Enterprise platform across UK and Spanish hospitals enabling centralized management of imaging analytics and workflow optimization. The company also expanded its service agreements with national health systems to include predictive maintenance and remote diagnostics ensuring high equipment uptime.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe breast imaging market employ several strategic approaches to reinforce their competitive standing. They prioritize regulatory alignment by actively engaging with the European Medicines Agency and national health technology assessment bodies to secure timely approvals and reimbursement for new technologies. Companies invest heavily in clinical evidence generation through multicenter trials with European hospitals to validate performance in local populations. Strategic partnerships with national screening programs enable large scale deployment and real-world data collection.

COMPETITIVE LANDSCAPE

The Europe breast imaging market is characterized by intense competition among global medical imaging leaders with differentiation centered on technological innovation regulatory compliance and integration into national healthcare workflows. Unlike markets driven purely by commercial sales Europe’s landscape is shaped by public procurement processes stringent quality assurance mandates and population based screening frameworks. Companies must navigate diverse national reimbursement policies language specific user interfaces and varying levels of digital maturity across member states. Competition extends beyond hardware to encompass software ecosystems AI analytics and service support as healthcare systems seek end to end solutions that improve diagnostic accuracy while managing radiologist shortages. The entry of specialized AI startups has intensified pressure on incumbents to demonstrate clinical utility and interoperability.

KEY MARKET PLAYERS

Some of the prominent companies leading the Europe Breast Imaging Market profiled in the report are

- Hologic, Inc.

- GE Healthcare

- Siemens Healthcare

- Philips Healthcare

- Fujifilm Holdings Corporation Gamma Medica, Inc.

- Toshiba Corporation

- Sonocine, Inc.

- Aurora Imaging Technology, Inc.,

- Dilon Technologies, Inc.

EUROPE BREAST IMAGING MARKET NEWS

- In October 2025 GE Healthcare implemented its Edison Enterprise imaging analytics platform in five major UK National Health Service trusts facilitating centralized AI deployment and workflow optimization for breast imaging departments.

MARKET SEGMENTATION

This research report on the europe breast imaging market has been segmented and sub-segmented into the following categories

By Technology

- Ionizing Technologies

- Mammography

- Digital Mammography

- 3D Mammography

- Molecular Breast-Specific Gamma Imaging (MBI/BSGI)

- Positron Emission Tomography and Computed Tomography (PET-CT)

- Cone-Beam Computed Tomography (CBCT)

- Positron Emission Mammography (PEM)

- Non-ionizing Technologies

- Breast MRI

- Breast Ultrasound

- Automated Whole-Breast Ultrasound (AWBU)

- Breast Thermography

- Optical Imaging

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What are the main technologies used in the Europe Breast Imaging Market?

Key technologies in the Europe Breast Imaging Market include digital mammography, breast tomosynthesis (3D mammography), breast ultrasound, and magnetic resonance imaging (MRI), offering enhanced diagnostic accuracy

2. How is digital mammography impacting the Europe Breast Imaging Market?

Digital mammography is significantly impacting the Europe Breast Imaging Market by improving image quality, reducing false positives, and enabling quicker and more accurate breast cancer detection and diagnosis.

3. What role does breast tomosynthesis play in the Europe Breast Imaging Market?

Breast tomosynthesis provides 3D imaging in the Europe Breast Imaging Market, increasing diagnostic precision and reducing unnecessary follow-up exams, thus driving its growing adoption across European healthcare providers.

4. How are government initiatives influencing the Europe Breast Imaging Market?

Government initiatives across Europe are boosting the Breast Imaging Market by promoting breast cancer awareness, enhancing screening programs, and supporting the adoption of advanced imaging technologies.

5. What is the importance of early detection in the Europe Breast Imaging Market?

Early detection in the Europe Breast Imaging Market is crucial for improving breast cancer survival rates, which is why advanced imaging technologies and widespread screening programs are prioritized.

6. How is AI integrated into the Europe Breast Imaging Market?

Artificial intelligence integration in the Europe Breast Imaging Market helps improve image analysis, enabling earlier and more accurate breast cancer detection, thereby enhancing patient outcomes and workflow efficiency.

7. Which countries dominate the Europe Breast Imaging Market?

Germany, the United Kingdom, France, Italy, and Spain dominate the Europe Breast Imaging Market because of advanced healthcare infrastructure and active breast cancer screening initiatives.

8. What are the main challenges facing the Europe Breast Imaging Market?

Challenges include high equipment costs, unequal access to screening in rural or underserved areas, shortage of skilled radiologists, and regulatory compliance issues in the Europe Breast Imaging Market.

9. How does the Europe Breast Imaging Market benefit hospitals and diagnostic centers?

-

Hospitals and diagnostic centers benefit from the Europe Breast Imaging Market through access to improved imaging technologies that facilitate early breast cancer detection and personalized patient care.

10. What is the impact of aging population on the Europe Breast Imaging Market?

-

The aging population in Europe increases the risk of breast cancer, thus expanding the demand for breast imaging services and fueling market growth over the coming years.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com