Europe Bromine Market Size, Share, Trends & Growth Forecast Report – Segmented By Product (Elemental Bromine, Calcium Bromide, Sodium Bromide), Application, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Bromine Market Size

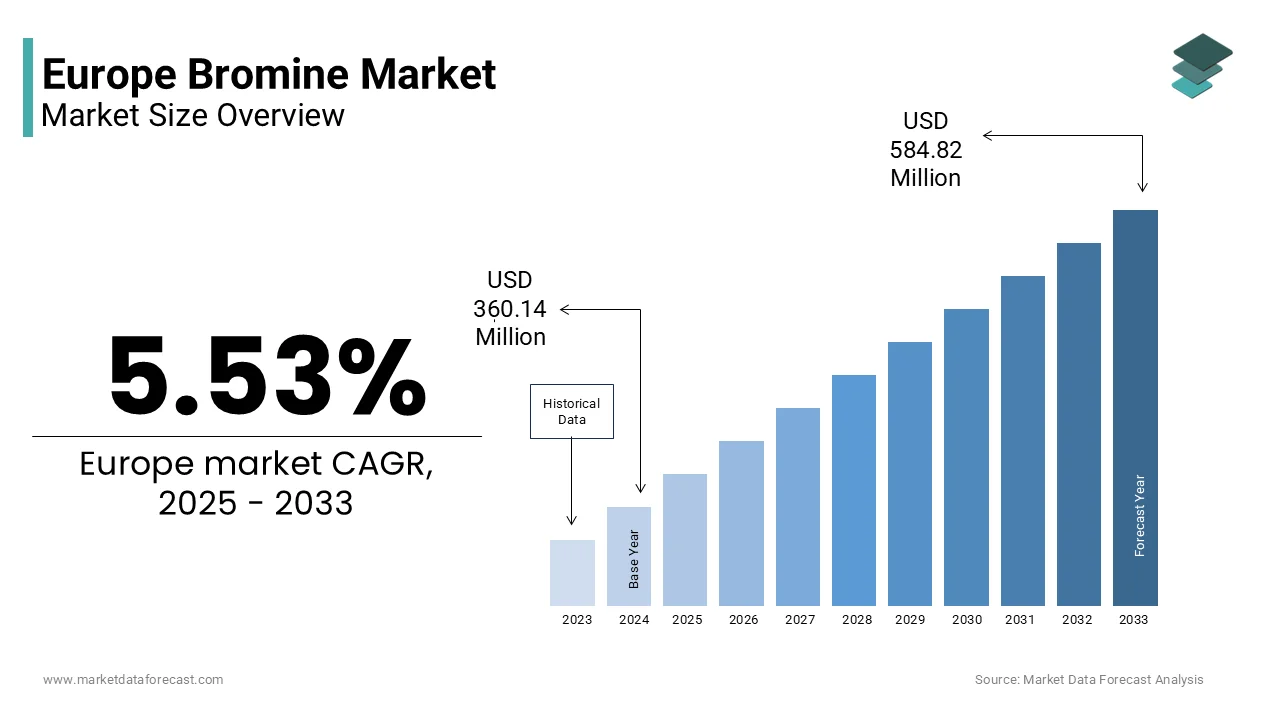

The Europe bromine market size was valued at USD 360.14 million in 2024 and is projected to reach USD 584.82 million by 2033 from USD 380.09 million in 2025, growing at a CAGR of 5.53%.

bromine is a volatile, red-brown liquid halogen element essential for many industrial applications. It is primarily used as flame retardants, drilling fluids, water treatment agents, and chemical intermediates across industrial, construction, and energy sectors. Bromine is a naturally occurring halogen extracted mainly from brine wells and salt deposits, with Europe relying significantly on imports due to limited domestic reserves. The region’s demand is shaped by stringent safety regulations, infrastructure development, and environmental policies governing chemical usage. According to ECHA's 2023 regulatory strategy for flame retardants, halogenated and organophosphorus compounds account for approximately 70% of the organic flame retardants market in the EU. As per Eurostat, the industry sector accounted for 24.6% of the EU's total final energy consumption in 2023, while the services sector accounted for 13.5%. The industrial utility of bromine remains strong due to essential uses that fall under REACH exemptions, even as some of its compounds face persistent regulatory scrutiny, which strengthens its status as a critical but debated element within Europe's chemical value chain.

MARKET DRIVERS

Stringent Fire Safety Regulations in Construction and Electronics Are Sustaining Demand for Brominated Flame Retardants

The region’s rigorous fire safety standards mandate the use of effective flame retardants in building materials and electronic devices, a factor that drives the growth of the Europe bromine market. The EU Construction Products Regulation requires materials to meet specific fire performance classifications, and brominated flame retardants, particularly tetrabromobisphenol A and decabromodiphenyl ether under controlled exemptions, offer high efficiency at low additive levels. In the construction sector, the drive for increased building energy efficiency has led to the widespread use of insulation materials that must meet fire safety standards. These regulatory and performance advantages ensure continued industrial reliance on bromine despite environmental concerns, particularly where technically viable substitutes remain limited.

Expansion of Offshore Energy Activities in the North Sea Is Driving Demand for Brominated Drilling Fluids

Bromine-based clear brine fluids are essential in high pressure high temperature drilling operations, particularly in Europe’s mature yet active offshore oil and gas fields, and this propels the expansion of the Europe bromine market. These fluids provide density control without damaging reservoir integrity, a critical requirement in complex geological settings. According to the Norwegian Offshore Directorate (formerly NPD) reported that 42 exploration wells were drilled in 2024, yielding 16 discoveries. As per sources, brominated fluids reduce non productive time compared to conventional alternatives, enhancing operational efficiency. Europe is shifting towards renewables, but the persistent necessity for hydrocarbon extraction, particularly for energy security in an unstable geopolitical climate, guarantees an ongoing demand for bromine in drilling uses until at least 2030.

MARKET RESTRAINTS

Regulatory Restrictions Under REACH and Persistent Environmental Concerns Are Limiting Certain Brominated Applications

The European Union’s Registration Evaluation Authorisation and Restriction of Chemicals framework imposes strict controls on several brominated compounds due to their persistence, bioaccumulation, and toxicity, which restricts the growth of the Europe bromine market. Substances like hexabromocyclododecane have been banned since 2016, and others face authorization requirements that increase compliance costs and discourage use. The European Chemicals Agency (ECHA) has identified several brominated substances as Substances of Very High Concern (SVHCs) or placed them on the Authorisation List (Annex XIV), leading to their phase-out. These findings have prompted voluntary phase outs by major electronics manufacturers such as Siemens and Philips, who now prioritize halogen free alternatives in new product lines. The regulatory uncertainty discourages long term investment in bromine dependent formulations and accelerates substitution, particularly in consumer facing sectors where brand reputation is tied to environmental stewardship.

Limited Domestic Bromine Production Capacity Forces Heavy Reliance on Imports and Exposes Supply Chains to Geopolitical Risk

The region possesses minimal bromine extraction infrastructure, with virtually no active bromine mines or brine processing facilities on the continent, and this hinders the expansion of the Europe bromine market. As per sources, a significant share of Europe’s bromine supply is imported, and some of the regions are subject to geopolitical instability and export controls. According to the European Commission’s 2024 Critical Raw Materials list, bromine is not formally classified as critical, but its derivative applications in fire safety and energy are deemed strategically important. Disruptions such as the Red Sea shipping crisis in early 2024 caused bromine derivative prices to spike. This import reliance not only inflates logistics costs but also complicates compliance with the EU’s Conflict Minerals Regulation and upcoming supply chain due diligence laws, creating operational vulnerabilities for downstream industries.

MARKET OPPORTUNITIES

Development of Next Generation Bromine Based Water Treatment Solutions for Municipal and Industrial Use

It’s efficacy as a biocide in water treatment, particularly in cooling towers and industrial wastewater, offers a growing opportunity to the European bromine market. Unlike chlorine, bromine remains effective over a wider pH range and produces fewer regulated disinfection by products. According to studies, Legionnaires’ disease cases in the EU rose, prompting stricter controls on cooling system hygiene. Bromine based biocides such as bromochlorodimethylhydantoin are increasingly adopted in thermal power plants and data centers to prevent microbial fouling. Companies are piloting closed loop bromine regeneration systems, which reduces chemical consumption. These innovations align with the EU’s Zero Pollution Action Plan and circular economy goals, opening new avenues for bromine in sustainable water management.

Innovation in Bromine Mediated Organic Synthesis for Pharmaceutical and Agrochemical Intermediates

Bromine serves as a versatile reagent in the synthesis of active pharmaceutical ingredients and crop protection chemicals, an application that offers selectivity and yield advantages in halogenation reactions, and thereby creates potential opportunities for the expansion of the Europe bromine market. The European pharmaceutical sector, which accounts for a portion of global medicine production, relies on brominated intermediates for drugs treating cardiovascular and neurological conditions. Similarly, bromomethane alternatives in soil fumigation, such as iodomethane bromine blends, are gaining traction under the EU’s Sustainable Use of Pesticides Directive. The EU's Pharmaceutical Strategy for Europe, which encourages local production of essential medicines, is expected to drive up demand for high-purity bromine reagents. This niche but high value application offers stable growth insulated from broader flame retardant controversies.

MARKET CHALLENGES

Intensifying Competition from Halogen Free and Bio Based Flame Retardant Alternatives Is Eroding Traditional Bromine Applications

Mounting burden from rapidly advancing non halogenated flame retardants derived from phosphorus nitrogen or mineral sources challenges the growth of the Europe bromine market. Driven by corporate sustainability commitments and green building certifications like BREEAM and LEED, manufacturers are reformulating products to eliminate brominated compounds. According to sources, many member companies have reduced brominated flame retardant use, citing customer demand and Ecolabel requirements. In the electronics sector, some of the companies mandate halogen free components across their European supply chains, accelerating industry wide shifts. The diminishing performance gap in high heat applications, a result of ongoing R&D efforts, is jeopardizing long-term demand in crucial sectors and forcing bromine manufacturers to justify essential use claims to increasingly doubtful regulators.

High Energy Intensity and Carbon Footprint of Bromine Production Conflict With EU Climate Neutrality Goals

The extraction and purification of bromine are energy-intensive processes that generate significant greenhouse gas emissions, and consequently those processes impede the expansion of the Europe bromine market. This creates misalignment with Europe’s Green Deal objectives. Brine evaporation and chlorine oxidation, the core steps in bromine production, require substantial thermal and electrical input. According to research, production of bromine emits tonnes of carbon dioxide equivalent, primarily due to fossil fuel based electricity in source countries. The EU's implementation of CBAM tariffs on imported chemicals means that bromine derivatives could face extra charges unless their producers decarbonize their operations. Furthermore, major European customers in construction and automotive are adopting science based targets that exclude high carbon footprint inputs. Major bromine exporters must invest in renewable power or carbon capture to avoid exclusion from low-carbon supply chains vital to Europe’s industrial future.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 5.53% |

| Segments Covered | By Product, Application, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Albemarle Corporation, ICL Group Ltd., Lanxess AG, Honeywell International Inc., Chemtura Corporation, Tata Chemicals Ltd., Jordan Bromine Company, Cosmo Chemical Co., Ltd., Hikma Pharmaceuticals PLC, and Bromine Compounds Ltd. |

SEGMENTAL ANALYSIS

By Product Insights

The elemental bromine segment dominated the Europe bromine market by capturing 52.4% of the regional market share in 2024. The dominance of the elemental bromine segment is attributed to its role as the foundational feedstock for nearly all brominated derivatives. Its high reactivity and versatility make it indispensable in synthesizing flame retardants, biocides, and drilling fluid components. According to studies, a portion of brominated compounds manufactured in the EU originate from elemental bromine inputs sourced via imports. The segment’s dominance is further reinforced by its irreplaceable function in high performance applications, such as tetrabromobisphenol A production for circuit boards, where alternative halogens fail to deliver equivalent thermal stability. Besides, major chemical distributors maintain strategic stockpiles of elemental bromine to ensure supply continuity for pharmaceutical and agrochemical clients. This centrality in the value chain, coupled with limited substitution pathways in critical industrial processes, sustains elemental bromine’s dominance despite regulatory headwinds.

The calcium bromide segment is predicted to witness the highest CAGR of 6.8% from 2025 to 2033 due to its critical role in high density clear brine fluids for deepwater and geothermal drilling. Unlike sodium bromide, calcium bromide achieves higher densities without crystallization risks, which makes it ideal for complex well environments. The expansion of geothermal energy projects further amplifies demand. "As per the European Geothermal Energy Council (EGEC), installed geothermal heat pump and district heating capacity has generally grown across Europe, including in Germany and Italy, with specialized biocides and corrosion inhibitors employed in closed-loop heat exchange systems to prevent microbial corrosion. Furthermore, the compound’s use in oilfield workover operations has increased due to Europe’s focus on maximizing recovery from mature fields. The technical advantages of calcium bromide will support sustained growth, given that energy security is a policy priority and deep drilling activity is projected to climb.

By Application Insights

The flame retardants segment led the Europe bromine market and accounted for 58.7% share in 2024. Stringent fire safety mandates across construction electronics and transportation have majorly contributed to the growth of the flame retardants. Brominated flame retardants remain unmatched in efficacy for polymers used in insulation panels printed circuit boards and automotive interiors. In electronics, the EU’s Low Voltage Directive requires all consumer devices to pass glow wire ignition tests, a standard most economically met using tetrabromobisphenol A. As per sources, brominated formulations reduced peak heat release rates compared to phosphorus based alternatives in polyamide 6. Despite regulatory scrutiny, essential use exemptions under REACH continue to permit specific brominated compounds where alternatives compromise safety or performance. This regulatory carve out combined with technical superiority ensures flame retardants retain dominance in the European bromine application landscape.

The clear brine fluids segment is estimated to register the fastest CAGR of 7.2% over the forecast period owing to the renewed offshore hydrocarbon exploration and the rise of geothermal energy development. These high density non damaging fluids—primarily composed of calcium and zinc bromide, are essential for well completion and workover operations in high pressure reservoirs. Moreover, geothermal drilling activity increased year on year, with bromide brines used to stabilize boreholes in fractured rock formations. Unlike conventional muds, clear brine fluids minimize formation damage, enhancing long term well productivity, a critical factor in Europe’s push for energy independence. As per research, brominated fluids reduce well intervention frequency, lowering lifecycle costs. These operational and strategic advantages drive accelerated adoption across both fossil and renewable subsurface energy sectors.

REGIONAL ANALYSIS

Germany Market Analysis

Germany was the top performer in the Europe bromine market and occupied 22.6% share in 2024. The domination of Germany is primarily driven by its advanced chemical manufacturing base, stringent fire safety codes, and robust industrial demand. Germany, which is Europe's largest chemical producer, hosts significant facilities where imported elemental bromine is used to formulate flame retardants for the automotive and electronics sectors. According to sources, the country’s construction industry consumed significant tonnes of fire rated insulation materials in 2024, most containing brominated additives. The Energiewende policy also drives geothermal drilling in the Upper Rhine Valley, where bromide brines are standard. Germany leverages substantial research and development investment in halogen chemistry to play a key role in influencing Europe's industrial approach to bromine.

United Kingdom Market Analysis

The United Kingdom was the second-largest country in the European bromine market by occupying 16.3% of the regional market share in 2024. Its active offshore oil and gas sector and evolving building safety regulations fuels the growth of bromine in the UK. Following the Grenfell Tower tragedy, the UK implemented rigorous fire performance standards for high rise cladding, indirectly sustaining demand for brominated flame retardants in non combustible insulation alternatives. Moreover, the North Sea remains a key driver. The UK’s chemical distribution network, led by firms, ensures efficient delivery of bromine derivatives to industrial users. The country compensates for its lack of domestic output with a strong import infrastructure and a stable regulatory framework, which creates a reliable environment for industries reliant on bromine.

France Market Analysis

France is also a major player in the Europe bromine market, with its nuclear energy infrastructure, geothermal ambitions, and aerospace manufacturing. The country’s 56 nuclear reactors require bromine based biocides for cooling tower water treatment to prevent biofouling and Legionella growth. According to studies, significant tonnes of brominated biocides were used annually across nuclear sites. Apart from these, France leads Europe in geothermal district heating, with some projects utilizing calcium bromide brines for well stability. The aerospace sector, centered around Airbus and Safran, relies on brominated flame retardants in aircraft interior composites to meet EASA flammability standards. These high value industrial applications, combined with strong technical expertise, sustain France’s prominent market role.

Italy Market Analysis

Italy grew steadily in the Europe bromine market due to its construction boom, offshore gas exploration in the Adriatic, and pharmaceutical manufacturing. The National Recovery and Resilience Plan has allocated funds to building renovation, much of it requiring fire safe insulation compliant with EU standards. According to research, thousands of residential units were retrofitted using brominated polystyrene panels. In the energy sector, Eni’s operations in the Adriatic Sea continue to use brominated drilling fluids for high pressure gas wells. Furthermore, Italy is home to major generic drug producers like Zentiva and EG, which utilize bromine as a reagent in active pharmaceutical ingredient synthesis. This blend of construction energy and pharma applications supports Italy’s steady market presence.

Netherlands Market Analysis

The Netherlands is likely to expand in the European bromine market over the forecast period owing to its role as a logistics and chemical distribution hub. The Port of Rotterdam, the largest chemical port in Europe, handles the majority of bromine imports into the continent, serving as a transshipment point for Germany Belgium and France. Domestic demand is fueled by high tech manufacturing and water treatment. Dutch semiconductor facilities use bromine etchants in chip production, while municipal cooling systems in data centers rely on brominated biocides. The Netherlands also hosts European headquarters for global bromine suppliers like ICL Group, facilitating regulatory engagement and technical support. This strategic advantage cements the Netherlands as a critical node in the European bromine supply chain.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the notable key players in the Europe bromine market are

- Albemarle Corporation

- ICL Group Ltd.

- Lanxess AG

- Honeywell International Inc.

- Chemtura Corporation

- Tata Chemicals Ltd.

- Jordan Bromine Company

- Cosmo Chemical Co., Ltd.

- Hikma Pharmaceuticals PLC

- Bromine Compounds Ltd.

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the Europe bromine market focus on regulatory alignment by actively engaging with EU agencies to secure essential use exemptions for critical brominated compounds. They invest in technical service capabilities to help customers navigate REACH and fire safety compliance. Companies are developing low carbon bromine production pathways and promoting circular economy initiatives such as bromine recovery from waste streams. Strategic logistics optimization through European distribution hubs ensures supply reliability amid import dependency. Collaboration with downstream industries—particularly in construction electronics and energy—drives co innovation in high performance formulations. Product differentiation via high purity grades and application specific derivatives enhances value proposition. Digital platforms are used to provide real time regulatory updates and safety data. These strategies collectively reinforce market relevance in a highly scrutinized chemical environment.

COMPETITION OVERVIEW

The Europe bromine market features a concentrated yet dynamic competitive landscape dominated by global producers with strong technical expertise and regulatory acumen. Competition is less about price and more about reliability of supply regulatory compliance and application support. International players like ICL and Albemarle leverage vertical integration and scale to maintain cost efficiency while European chemical firms such as Lanxess add value through localized formulation and engineering partnerships. The absence of domestic bromine mining intensifies reliance on secure import channels making logistics and inventory management critical differentiators. Regulatory pressure from REACH and green chemistry initiatives has raised barriers to entry limiting participation to firms with robust stewardship programs. Innovation is focused on justifying essential use through performance data and developing circular solutions rather than volume expansion. This environment fosters collaboration between suppliers and end users to co manage risk and maintain access to bromine where alternatives remain technically inadequate.

TOP PLAYERS IN THE MARKET

- ICL Group is a leading global producer of bromine and brominated derivatives with a strong foothold in the Europe bromine market. Headquartered in Israel, the company supplies elemental bromine and specialty compounds to European industries including flame retardants water treatment and oilfield services. ICL leverages its integrated production from the Dead Sea to ensure consistent quality and supply security. It also launched a low carbon bromine initiative aligned with the EU Green Deal, enhancing its appeal to sustainability conscious customers across the region.

- Albemarle Corporation is a major international specialty chemicals company with significant involvement in the Europe bromine market through its flame retardant and clear brine fluid portfolios. The company serves automotive electronics and energy sectors across Germany France and the UK. It also partnered with European polymer manufacturers to co develop halogen free compliant brominated solutions that meet essential use criteria under evolving EU regulations, ensuring continued relevance in high performance applications.

- Lanxess AG is a German specialty chemicals company deeply embedded in the Europe bromine value chain through its production of brominated flame retardants and intermediates. The company integrates imported elemental bromine into high purity additives for engineering plastics used in electric vehicles and consumer electronics. It also collaborated with the VDI Association of German Engineers to update fire safety testing protocols, reinforcing the technical justification for brominated solutions in critical infrastructure applications.

MARKET SEGMENTATION

This research report on the Europe bromine market has been segmented and sub-segmented based on categories.

By Product

- Elemental Bromine

- Calcium Bromide

- Sodium Bromide

By Application

- Clear Brine Fluids (CBF)

- Flame Retardants

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the Europe Bromine Market?

The Europe bromine market covers the production, distribution, and application of bromine and its derivatives across various industries, including chemicals, pharmaceuticals, and electronics.

2. What factors are driving the growth of the bromine market in Europe?

Key drivers include rising demand for flame retardants, increasing use in clear brine fluids for oil drilling, and expanding applications in pharmaceuticals and water treatment.

3. Which bromine product type dominates the European market?

Elemental bromine holds the largest share due to its wide use in manufacturing bromine-based derivatives and industrial chemicals.

4. Which applications contribute most to bromine consumption in Europe?

The flame retardants segment leads the market, followed by clear brine fluids (CBF) used in oil and gas drilling operations.

5. Which countries are leading the bromine market in Europe?

Germany, the United Kingdom, and France are the top markets, driven by strong chemical manufacturing sectors and industrial demand.

6. Who are the major players operating in the Europe bromine market?

Key companies include Albemarle Corporation, ICL Group Ltd., Lanxess AG, Honeywell International Inc., Chemtura Corporation, Tata Chemicals Ltd., Jordan Bromine Company, Cosmo Chemical Co., Ltd., Hikma Pharmaceuticals PLC, and Bromine Compounds Ltd.

7. What challenges does the European bromine market face?

The market faces challenges such as strict environmental regulations, high production costs, and limited bromine reserves in the region.

8. What trends are shaping the future of the Europe bromine market?

Key trends include technological advancements in bromine extraction, growth in energy storage applications, and increasing demand for water purification chemicals.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com