Europe Bronchoscopes Market Size, Share, Trends, & Growth Forecast Report By Type (Flexible, Rigid), Usage, End-Use and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Bronchoscopes Market Report Summary

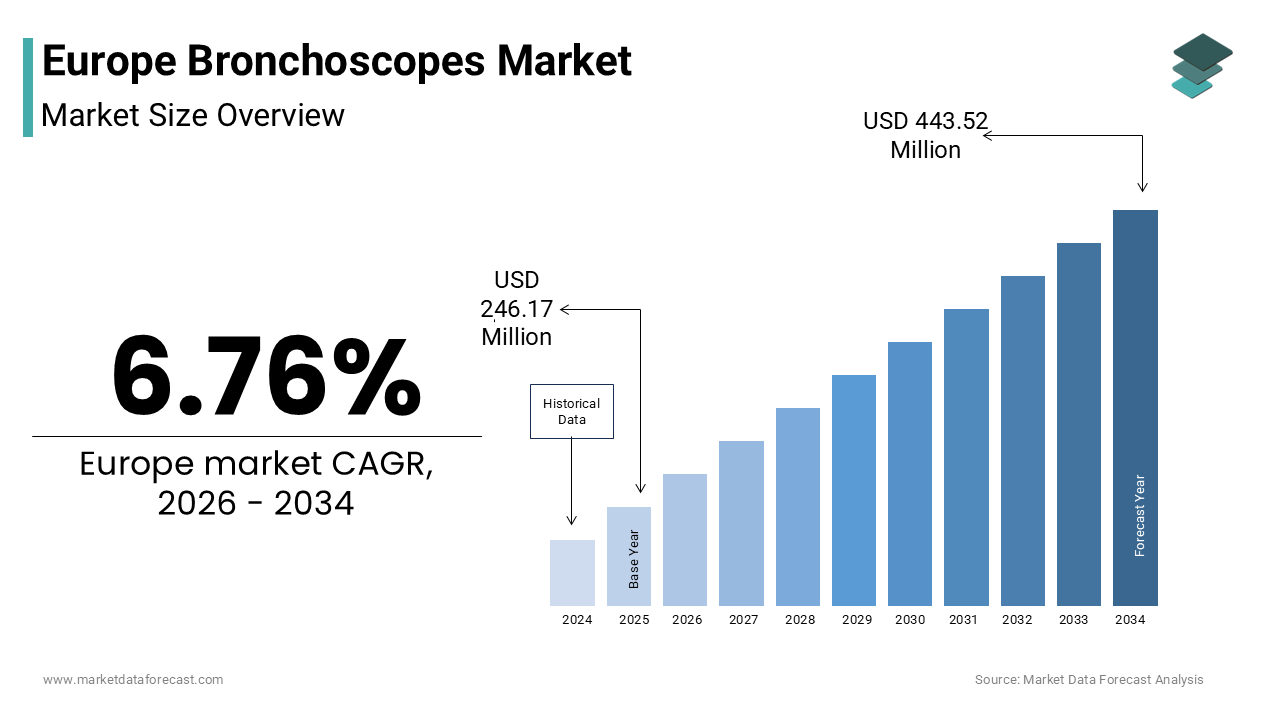

The Europe bronchoscopes market was valued at USD 246.17 million in 2025, is expected to reach USD 262.81 million in 2026, and is projected to grow to USD 443.52 million by 2034, registering a CAGR of 6.76% during the forecast period from 2026 to 2034. The growth of the Europe bronchoscopes market is driven by the rising burden of chronic respiratory diseases, expanding lung cancer screening programs, and increasing adoption of single-use bronchoscopes to enhance infection control. Technological advancements such as advanced imaging, navigation-assisted bronchoscopy, and portable point-of-care devices are further supporting market expansion. Additionally, the aging European population and stricter regulatory standards under EU MDR are reshaping device innovation, procurement strategies, and clinical workflows across respiratory care settings.

Key Market Trends

-

Growing adoption of single-use bronchoscopes to reduce hospital-acquired infections and reprocessing challenges.

-

Integration of electromagnetic navigation, AI-assisted imaging, and real-time visualization technologies to improve diagnostic accuracy.

-

Rising demand for portable and bedside bronchoscopy systems in intensive care and emergency departments.

-

Expansion of lung cancer screening programs across Europe is increasing procedural volumes.

-

Increasing focus on sustainability and lifecycle assessment of disposable bronchoscopic devices.

Segmental Insights

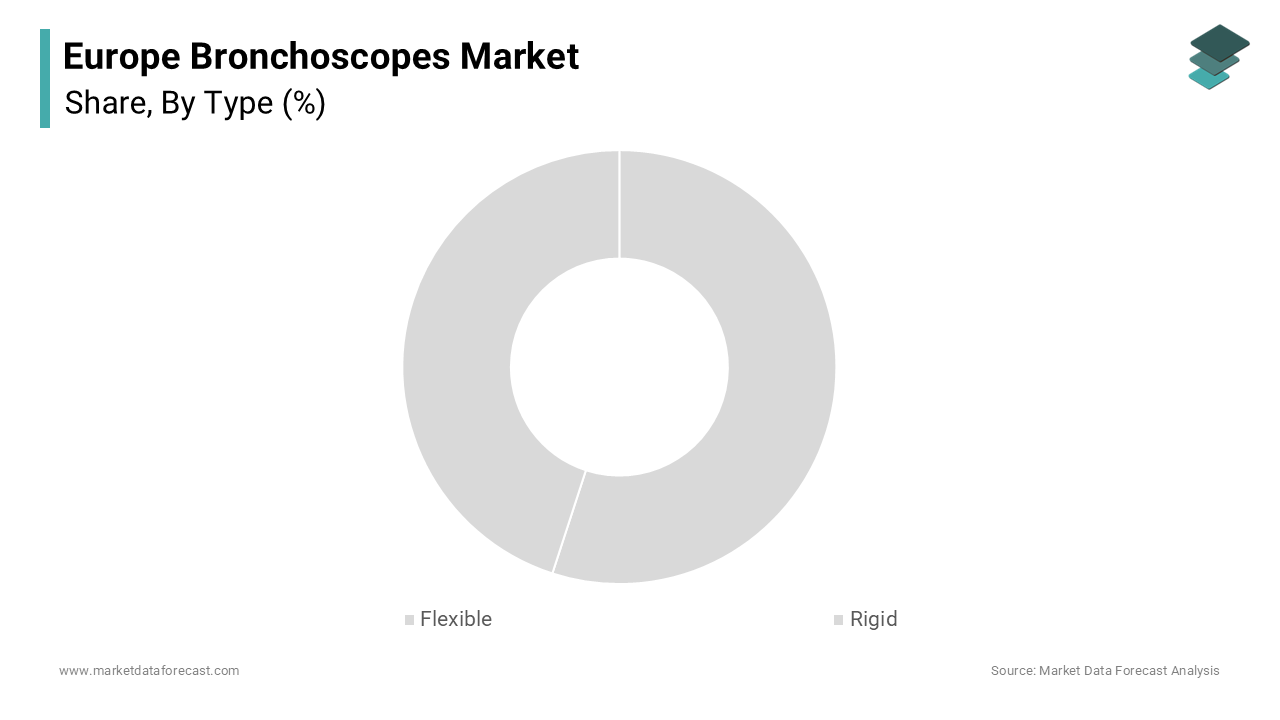

- Based on Type, the flexible bronchoscope segment dominated the Europe bronchoscopes market in 2025 owing to its versatility, patient comfort, and widespread use in diagnostic and therapeutic procedures. Continuous advancements in imaging resolution and maneuverability further reinforce its clinical dominance.

- The rigid bronchoscope segment is projected to grow at a notable pace during the forecast period due to rising demand for complex airway interventions, including tumor debulking and airway stent placement in specialized interventional pulmonology centers.

- Based on usage, reusable bronchoscopes held the leading market share in 2025 supported by their high image quality and cost efficiency in high-volume hospitals. However, the disposable bronchoscope segment is expected to grow rapidly owing to infection prevention mandates, ICU adoption, and simplified workflow requirements.

- Based on end use, the hospital segment dominated the Europe bronchoscopes market due to the need for advanced infrastructure, anesthesia support, and emergency response capabilities. Meanwhile, outpatient facilities are anticipated to witness steady growth driven by minimally invasive diagnostic procedures and the shift toward ambulatory respiratory care.

Regional Insights

Germany led the Europe bronchoscopes market in 2025 supported by strong pulmonology infrastructure, nationwide lung cancer screening initiatives, and high procedural volumes in tertiary hospitals.

- The United Kingdom holds a significant market share driven by centralized NHS cancer pathways, strict infection control policies, and increasing adoption of disposable bronchoscopes in critical care settings.

- France is expected to grow steadily owing to universal healthcare coverage, strong academic research networks, and organized screening programs enhancing early diagnosis.

- Italy is projected to witness healthy growth due to rising lung disease prevalence and increasing adoption of advanced bronchoscopy technologies across regional healthcare systems.

- The Netherlands continues to gain traction supported by integrated outpatient respiratory clinics, sustainable procurement policies, and early adoption of simulation-based training programs.

Competitive Landscape

The Europe bronchoscopes market is highly competitive and technology-driven, with companies focusing on advanced imaging capabilities, infection prevention solutions, and integrated digital platforms to strengthen market presence. Leading players operating in the Europe bronchoscopes market include Olympus Corporation, Fujifilm Holdings Corporation, HOYA Corporation (PENTAX Medical), KARL STORZ GmbH & Co. KG, Ambu A/S, Boston Scientific Corporation, Teleflex Incorporated, Richard Wolf GmbH, Cook Medical, Verathon Inc., CONMED Corporation, Medtronic plc, and Novatech SA. These companies are investing in innovation, training ecosystems, and regulatory compliance strategies to address evolving clinical and sustainability demands across Europe’s respiratory care landscape.

Europe Bronchoscopes Market Size

The Europe bronchoscopes market size was valued at USD 246.17 million in 2025 and is anticipated to reach USD 262.81 million in 2026 from USD 443.52 million by 2034, growing at a CAGR of 6.76% during the forecast period from 2026 to 2034

Bronchoscopes are specialized medical endoscopic devices used to visualize, diagnose, and treat conditions within the trachea and bronchial tree that play a critical role in pulmonology, critical care, and thoracic surgery. These instruments enable procedures ranging from diagnostic biopsies and airway clearance to stent placement and laser ablation. The European market is distinguished by its emphasis on infection control, technological integration, and alignment with stringent regulatory standards under the EU Medical Device Regulation (MDR) 2017/745. According to the European Respiratory Society, chronic respiratory diseases affect over 60 million people in the European Union. As reported by the International Agency for Research on Cancer, lung cancer alone accounts for more than 380,000 new cases annually. Furthermore, the European Centre for Disease Prevention and Control notes that hospital acquired infections affect 3.5 million patients each year in the EU, driving demand for single use bronchoscopes to mitigate cross contamination risks. As per Eurostat, the share of the population aged 65 and older reached 22.3% in 2023, which is intensifying the burden of age-related pulmonary conditions requiring bronchoscopic intervention. This confluence of demographic pressure, clinical necessity, and regulatory evolution positions bronchoscopes not merely as diagnostic tools but as essential components of Europe’s advanced respiratory care infrastructure.

MARKET DRIVERS

Rising Burden of Respiratory Diseases and Lung Cancer Screening Programs

The escalating prevalence of chronic respiratory conditions and the rollout of organized lung cancer screening across Europe are majorly driving the growth of the European bronchoscopes market. According to the World Health Organization Europe, chronic obstructive pulmonary disease affects over 30 million adults in the EU, while asthma impacts an additional 30 million, frequently necessitating bronchoscopic evaluation for differential diagnosis or therapeutic intervention. More significantly, the European Commission’s 2022 recommendation to implement population-based lung cancer screening for high-risk individuals have institutionalized early detection pathways that rely heavily on bronchoscopy for confirmatory biopsy. Data from the European Reference Network for Respiratory Diseases indicates that over 15 EU member states launched pilot screening programs in 2023, with Germany and the Netherlands achieving national coverage. In these programs, low dose CT scans identify nodules, and bronchoscopy with navigation or radial probe EBUS is used for tissue sampling, increasing procedural volumes significantly as validated by the German Cancer Consortium. With lung cancer survival rates doubling when detected at stage I, bronchoscopy transitions from reactive diagnostics to proactive lifesaving intervention within structured public health frameworks.

Strict Infection Control Protocols and Adoption of Single Use Devices

The rising awareness of healthcare associated infections and updated reprocessing guidelines have accelerated the shift toward single use bronchoscopes across European hospitals, which is further boosting the expansion of the European bronchoscopes market. According to the European Centre for Disease Prevention and Control, bronchoscopy is among the top five semi critical medical procedures linked to outbreaks of multidrug resistant organisms, primarily due to biofilm formation in complex internal channels that resist standard cleaning. As per a 2023 audit by the French National Authority for Health, 32% of reusable bronchoscopes in tertiary hospitals showed residual microbial contamination post reprocessing, which is prompting stricter enforcement of EN ISO 15883 standards. In response, countries like Sweden and the Netherlands now mandate single use devices for immunocompromised patients and intensive care units. The UK’s National Health Service issued guidance in 2023 recommending disposable bronchoscopes for all bedside procedures in critical care to eliminate reprocessing delays and cross contamination risks. Clinical studies published in the European Respiratory Journal demonstrate that single use bronchoscopes reduce infection rates by up to 60% in ventilated patients while improving workflow efficiency. As MDR compliance increases scrutiny on device safety and traceability, single use models offer a compelling solution that aligns clinical efficacy with public health imperatives.

MARKET RESTRAINTS

High Procurement and Maintenance Costs of Reusable Systems

Despite clinical familiarity, the total cost of ownership for reusable bronchoscopes poses a significant financial barrier for many European healthcare institutions and a notable restraint to the growth of the European bronchoscopes market. According to a 2023 analysis by the German Hospital Federation, the average capital cost for a high-end flexible bronchoscope exceeds 25,000 euros, with annual maintenance and repair expenses adding another 5,000 to 7,000 euros per unit. Reprocessing alone requires dedicated staff, sterile processing departments, and costly enzymatic cleaners validated under EN ISO 15883, amounting to 30 to 50 euros per procedure as documented by the Dutch Health Care Institute. Moreover, device fragility leads to frequent repairs. According to the data from the Swedish Association of Local Authorities, reusable bronchoscopes require servicing every 12 to 18 procedures on average, causing workflow disruptions. Public hospitals operating under constrained budgets, particularly in Southern and Eastern Europe, struggle to maintain adequate fleets, resulting in procedure backlogs. As per a 2024 report by the European Court of Auditors, only 45% of regional hospitals in Italy and Spain met minimum bronchoscope availability standards due to funding gaps. Until sustainable financing models or cost sharing consortia emerge, these economic pressures will continue to limit access and drive interest in alternative models despite initial resistance to disposable adoption.

Stringent Regulatory Requirements Under EU MDR Delay Innovation

The implementation of the European Union Medical Device Regulation has significantly extended approval timelines and increased compliance burdens for bronchoscope manufacturers, which is slowing the introduction of next generation technologies and hindering the regional market expansion. Unlike the previous Medical Devices Directive, MDR mandates comprehensive clinical evaluation reports, post market surveillance plans, and unique device identification for all Class IIa and higher devices, including most bronchoscopes. According to the European Commission’s Medical Devices Coordination Group, average certification time for new bronchoscopes increased from 9 months under MDD to over 18 months under MDR as notified bodies face backlog and heightened scrutiny. Startups and mid-sized innovators are disproportionately affected. As per a 2023 survey by MedTech Europe, 68% of small device companies delayed European launches due to MDR documentation complexity, particularly around biocompatibility and software validation for imaging integrated scopes. Furthermore, the regulation’s emphasis on equivalence has restricted reliance on predicate devices, forcing redundant testing even for incremental improvements. While patient safety is enhanced, the innovation pipeline suffers. As per industry data, fewer than five novel bronchoscope platforms received CE Mark under MDR in 2023 compared to over 15 annually under the old regime. This regulatory friction impedes access to advanced features like narrow band imaging or AI assisted lesion detection that could improve diagnostic yield across European clinics.

MARKET OPPORTUNITIES

Integration of Advanced Imaging and Navigation Technologies

The incorporation of real time imaging enhancements and electromagnetic navigation into bronchoscopes presents a high value opportunity for the European bronchoscopes market. Traditional bronchoscopy achieves diagnostic yields of only 50 to 60% for nodules smaller than 2 centimetres, but augmented systems dramatically increase success rates. According to clinical trials published by the European Respiratory Society, electromagnetic navigation bronchoscopy combined with cone beam CT raised diagnostic yield to 82% in multicenter EU studies. Companies like Olympus and Boston Scientific now offer integrated platforms that overlay pre procedural CT scans onto live bronchoscopic views, enabling targeted biopsies deep in the lung periphery. The European Society of Thoracic Surgeons recommends such technologies for early-stage lung cancer workup where tissue confirmation is critical before minimally invasive resection. National reimbursement bodies are responding, as Germany’s GBA Federal Joint Committee approved separate payment codes for navigated bronchoscopy in 2023 recognizing its cost effectiveness in reducing repeat procedures. As artificial intelligence algorithms for real time nodule detection mature, validated in pilot studies at Karolinska University Hospital, these smart scopes will transform bronchoscopy from operator dependent skill to standardized precision intervention, aligning with Europe’s push for value-based diagnostics.

Expansion of Point of Care Bronchoscopy in Critical Care and Emergency Settings

The decentralization of bronchoscopic procedures from specialized pulmonary units to intensive care, emergency departments, and operating rooms creates significant demand for portable user-friendly devices, which is another potential opportunity in the European bronchoscopes market. According to the European Society of Intensive Care Medicine, over 70% of mechanically ventilated patients in EU ICUs require urgent bronchoscopy for mucus plug removal, foreign body extraction, or bleeding control, yet access remains limited by equipment availability and specialist staffing. Single use ultra slim bronchoscopes with smartphone connectivity now enable bedside use by non-pulmonologists, critical in rural or understaffed hospitals. The UK’s National Institute for Health and Care Excellence endorsed this approach in 2023 for rapid airway management in trauma and post-operative complications. As per the data from the Scandinavian Critical Care Trials Group, ICU teams using portable bronchoscopes reduced time to airway clearance by 45% compared to waiting for specialist consultation. Moreover, the European Resuscitation Council includes bronchoscopy in its advanced airway algorithms for difficult intubations, which is expanding training requirements across anaesthesia and emergency medicine. With compact high-definition systems costing under 10,000 euros and requiring minimal setup, point of care bronchoscopy bridges critical gaps in acute care delivery, transforming the device from a diagnostic specialty tool into a lifesaving emergency asset across Europe’s diverse healthcare landscape.

MARKET CHALLENGES

Shortage of Trained Pulmonologists and Procedural Expertise

Despite growing clinical indications, the availability of skilled operators capable of performing advanced bronchoscopic techniques remains insufficient across much of Europe, which is limiting procedural volume and technological adoption and challenging the European bronchoscopes market expansion. According to the European Respiratory Society, there is a projected deficit of over 5,000 certified interventional pulmonologists by 2030, with severe shortages in Central and Eastern Europe where training programs are underfunded. A 2023 workforce survey revealed that only 38% of district hospitals in Poland and Romania have on site bronchoscopy capability, forcing patient transfers that delay diagnosis and increase mortality. Even in Western Europe, the learning curve for complex procedures like endobronchial ultrasound or cryobiopsy deters widespread uptake, as the German Respiratory Society reports that fewer than 200 physicians nationwide are certified in advanced therapeutic bronchoscopy. This expertise gap discourages investment in high end reusable systems whose value depends on operator proficiency. Simulation based training is emerging as a solution, with centers like Erasmus MC in Rotterdam offering VR bronchoscopy modules, but access remains limited. Without coordinated EU level accreditation standards, expanded fellowship slots, and tele-mentoring networks, the full potential of modern bronchoscopy will remain unrealized, perpetuating geographic disparities in respiratory care quality.

Environmental Impact and Waste Management Concerns of Single Use Devices

The rapid adoption of disposable bronchoscopes, while clinically beneficial, introduces significant sustainability challenges that conflict with Europe’s circular economy and green hospital initiatives, which is further challenging the expansion of the European bronchoscopes market. According to the European Environment Agency, healthcare accounts for 5% of the EU’s total carbon footprint, with single use devices contributing disproportionately to plastic waste and incineration emissions. A typical single use bronchoscope generates over 300 grams of non-recyclable plastic per procedure, and with millions of bronchoscopies performed annually across Europe the cumulative impact is substantial. Hospitals in Sweden and France now face municipal restrictions on medical plastic disposal, which is prompting environmental audits of procedural supplies. The Danish Health Authority issued guidance in 2023 urging facilities to conduct life cycle assessments before switching to disposables, a requirement that has slowed adoption in eco conscious institutions. Moreover, the EU’s Green Public Procurement criteria increasingly factor in environmental performance, pressuring vendors to develop partially recyclable or bio-based alternatives. Until manufacturers introduce take back schemes, compostable materials, or hybrid models with sterilizable cores, the tension between infection control and planetary health will persist, complicating procurement decisions and potentially triggering policy backlash against blanket disposable mandates.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.76% |

| Segments Covered | By Type, Usage, End-Use and Region |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, the Philippines, Indonesia, Singapore, and the Rest of APAC. |

| Market Leaders Profiled | Olympus Corporation, Fujifilm Holdings Corporation, HOYA Corporation (PENTAX Medical), KARL STORZ GmbH & Co. KG, Ambu A/S, Boston Scientific Corporation, Teleflex Incorporated, Richard Wolf GmbH, Cook Medical, Verathon Inc., CONMED Corporation, Medtronic plc, and Novatech SA |

SEGMENTAL ANALYSIS

By Type Insights

The flexible bronchoscope segment dominated the Europe bronchoscopes market by holding 77.4% of the European bronchoscopes market share in 2025. The supremacy of the flexible segment in this regional market is driven by its superior patient comfort, procedural versatility, and suitability for both diagnostic and therapeutic applications across diverse clinical settings. One key driver is its ability to access peripheral airways with minimal trauma, which is a critical advantage in diagnosing early-stage lung cancer and managing complex airway diseases. According to the European Respiratory Society, over 90% of diagnostic bronchoscopies performed in EU hospitals in 2023 utilized flexible scopes due to their manoeuvrability through narrow bronchial branches and compatibility with conscious sedation. Furthermore, national lung cancer screening programs in Germany, the Netherlands, and France rely heavily on flexible bronchoscopy for confirmatory tissue sampling after low dose CT detection. Data from the German Cancer Consortium shows that flexible scopes facilitated 78% of all navigated biopsies in 2023. With continuous advancements in imaging resolution, channel diameter, and ergonomic design, flexible bronchoscopes remain the clinical standard for comprehensive airway evaluation across Europe’s evolving respiratory care landscape.

The rigid bronchoscope segment is the fastest growing and is expected to exhibit a CAGR of 7.12% over the forecast period. The renewed interest in complex therapeutic airway management where rigid platforms offer superior control, hemostasis, and ventilation capabilities is primarily boosting the expansion of the rigid segment in the European market. According to the European Society of Thoracic Surgeons, over 15,000 patients annually in the EU require urgent airway recanalization, a procedure best performed under general anesthesia using rigid bronchoscopy. Leading centers like Karolinska University Hospital in Sweden and Hôpital Cochin in Paris have established dedicated interventional pulmonology units where rigid bronchoscopy volumes grew by 22% year on year in 2023 as reported by national thoracic registries. Moreover, innovations such as hybrid rigid scopes with integrated cameras and working channels have modernized the platform, making it more accessible to non-thoracic surgeons.

By Usage Insights

The reusable bronchoscope segment commanded for the leading share of 65.5% of the European market in 2025. The growth of the re-usable segment in the European bronchoscopes market is attributed to the established clinical workflows, high image quality, and cost efficiency in high volume centers despite growing infection control concerns. According to the European Association for Bronchology and Interventional Pulmonology, over 85% of academic medical centers in Germany, France, and Italy continue to rely on reusable systems for advanced procedures such as cryobiopsy and electromagnetic navigation due to their reliability and serviceability. Furthermore, long term cost analysis remains favorable in high throughput settings, as a study by the Dutch Health Care Institute found that reusable scopes become cost effective after 120 uses. National reimbursement systems also implicitly support reuse by bundling device costs into procedure fees rather than paying per use.

The disposable bronchoscope segment is the fastest growing and is anticipated to register a CAGR of 17.5% over the forecast period owing to the infection prevention mandates, point of care expansion, and workflow simplification in critical and emergency settings. According to the European Centre for Disease Prevention and Control, bronchoscopy related outbreaks accounted for 12% of endoscope linked transmissions in 2023, prompting stricter policies. The UK’s National Health Service issued guidance in 2023 endorsing disposable bronchoscopes for rapid airway clearance in ventilated patients. Clinical evidence supports this shift, as a multicenter trial published in Intensive Care Medicine demonstrated that ICU teams using disposable scopes achieved airway patency 40% faster than those waiting for sterilized reusable units.

By End Use Insights

The hospitals segment dominated the market by holding 88.4% of the European bronchoscopes market share in 2025 due to the complexity of bronchoscopic procedures which typically require specialized personnel, anaesthesia support, and immediate access to emergency interventions. According to the European Respiratory Society, over 95% of therapeutic bronchoscopies including stent placement, laser ablation, and cryobiopsy are performed in hospital endoscopy suites. Data from the German Hospital Federation shows that tertiary hospitals performed an average of 1,200 bronchoscopies per year in 2023, with volumes rising due to organized screening and aging populations. Moreover, critical care units increasingly rely on bedside bronchoscopy for mucus plug removal and foreign body extraction, procedures that necessitate immediate escalation capabilities only available in hospitals.

The outpatient facilities segment is the fastest growing and is estimated to record a CAGR of 10.3% over the forecast period owing to the shift toward ambulatory care, cost containment pressures, and the maturation of minimally invasive diagnostic protocols. According to the French National Health Insurance Fund, outpatient bronchoscopy volumes grew by 18% in 2023, driven by diagnostic biopsies for indeterminate nodules identified through lung cancer screening. In the Netherlands, integrated respiratory clinics now perform routine bronchoscopies under moderate sedation with same day discharge supported by national guidelines from the Dutch Society of Pulmonology. As healthcare systems prioritize value-based delivery, outpatient bronchoscopy will capture an expanding share of routine diagnostic workloads across Europe.

REGIONAL ANALYSIS

Germany Bronchoscopes Market Analysis

Germany led the European bronchoscopes market by accounting for 24.4% of the European market share in 2025. The dominance of Germany in the European market is driven by its world class pulmonology infrastructure, national lung cancer screening program, and high procedural volumes. According to the German Respiratory Society, the country performs over 250,000 bronchoscopies annually, with every statutory health insurer covering the procedure for indicated conditions. Germany was the first EU nation to implement nationwide lung cancer screening in 2023 targeting 1.2 million high risk individuals, dramatically increasing diagnostic biopsy demand. Leading university hospitals like Charité Berlin and Heidelberg University operate advanced interventional suites equipped with electromagnetic navigation and cryobiopsy systems. The Federal Joint Committee GBA regularly updates reimbursement codes to reflect technological advances, ensuring rapid adoption. Moreover, Germany hosts global manufacturers like Karl Storz whose R&D centers continuously refine scope ergonomics and imaging fidelity. With strong specialist training programs and dense hospital networks, Germany sets the clinical and technological benchmark for bronchoscopy across Europe.

United Kingdom Bronchoscopes Market Analysis

The United Kingdom held the second largest share of the European bronchoscopes market in 2025. The growth of the UK in this regional market is shaped by National Health Service protocols, centralized cancer pathways, and post pandemic infection control reforms. The NHS England Lung Cancer Screening Pilot launched in 2023 across 10 sites is expected to scale nationally by 2025, directly driving bronchoscopy volumes for nodule confirmation. According to the British Thoracic Society, over 120,000 bronchoscopies were performed in NHS hospitals in 2023, with strict guidelines mandating single use devices for all ICU bedside procedures to mitigate cross infection risks. The National Institute for Health and Care Excellence updated its bronchoscopy guidance in 2023 to endorse disposable scopes in critical care, a policy accelerating market transition. Leading centers like Royal Brompton Hospital pioneer advanced techniques including endobronchial valve placement for emphysema. Despite budget constraints, the NHS prioritizes respiratory diagnostics through dedicated cancer funding streams, ensuring consistent device procurement.

France Bronchoscopes Market Analysis

France is estimated to account for a promising share of the European bronchoscopes market during the forecast period owing to the universal healthcare coverage, strong academic medicine, and proactive national screening initiatives. The French National Cancer Institute rolled out organized lung cancer screening in 2023 targeting 500,000 high risk citizens annually with bronchoscopy as the confirmatory standard. According to the French Society of Pneumology, over 90,000 bronchoscopies were conducted in public hospitals in 2023, supported by full reimbursement under the national health insurance system. France maintains a dense network of pneumology reference centers such as Hôpital Cochin in Paris that serve as training hubs for advanced techniques including rigid bronchoscopy and EBUS. The Haute Autorité de Santé mandates strict reprocessing audits but also encourages disposable adoption in high-risk settings. Moreover, France’s centralized procurement agency ANSM streamlines device approval ensuring rapid access to innovative platforms.

Italy Bronchoscopes Market Analysis

Italy is anticipated to witness a healthy CAGR in the European bronchoscopes market over the forecast period due to its regional healthcare autonomy, high smoking prevalence, and growing adoption of single use technologies. According to ISTAT, lung cancer incidence rose by 8% between 2020 and 2023, intensifying diagnostic demand particularly in Northern regions with aging populations. While the national health service covers bronchoscopy universally, implementation varies by region; Lombardy and Emilia Romagna lead in advanced interventional programs while Southern regions face specialist shortages. As per a 2023 survey by the Italian Respiratory Society, 65% of ICU units in major cities now use disposable bronchoscopes following national infection control alerts. Leading hospitals like San Raffaele in Milan partner with industry to trial next generation scopes with AI assisted lesion detection. Despite economic constraints, Italy’s high disease burden and fragmented yet ambitious regional strategies create a dynamic market where innovation diffuses unevenly but persistently across the peninsula.

Netherlands Bronchoscopes Market Analysis

The Netherlands is expected to account for a notable share of the European bronchoscopes market over the forecast period owing to its integrated care models, early adoption of screening, and leadership in sustainable bronchoscopy practices. The Netherlands launched one of Europe’s first national lung cancer screening programs in 2022, now covering all high-risk individuals with bronchoscopy as the standard confirmatory pathway. According to the Dutch Association of Pulmonologists, over 40,000 bronchoscopies were performed in 2023, with 70% occurring in specialized outpatient respiratory clinics that emphasize efficiency and patient experience. The Netherlands is also at the forefront of environmental stewardship, as Erasmus MC in Rotterdam pioneered a life cycle assessment framework for bronchoscopes influencing national procurement toward partially recyclable models. Moreover, Dutch guidelines strongly encourage simulation-based training ensuring high procedural competency even among non-academic centers. With compact geography, excellent data registries, and a culture of pragmatic innovation, the Netherlands exemplifies how coordinated policy, technology, and sustainability can optimize bronchoscopy delivery across a high-income European health system.

COMPETITIVE LANDSCAPE

Competition in the Europe bronchoscopes market is defined by technological sophistication clinical validation and alignment with stringent regulatory and infection control standards. Incumbent leaders leverage decades of optical engineering expertise to deliver high performance reusable systems favored in academic and high-volume centers. Simultaneously agile innovators disrupt with single use platforms that address urgent infection prevention and workflow challenges in critical care. The market is bifurcated between premium reusable devices requiring significant capital investment and lower cost disposables with per procedure pricing—creating distinct value propositions for different care settings. New entrants face high barriers including MDR certification clinical evidence generation and trust requirements in life critical procedures. Consolidation is limited due to specialized manufacturing capabilities yet collaboration with software and AI firms is rising. Competition extends beyond hardware into services including training simulation and data management. Ultimately leadership is determined by the ability to balance image quality usability safety and sustainability while navigating Europe’s complex mosaic of clinical guidelines reimbursement policies and public health priorities.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe bronchoscopes market include

- Olympus Corporation

- Fujifilm Holdings Corporation

- HOYA Corporation (PENTAX Medical)

- KARL STORZ GmbH & Co. KG

- Ambu A/S

- Boston Scientific Corporation

- Teleflex Incorporated

- Richard Wolf GmbH

- Cook Medical

- Verathon Inc.

- CONMED Corporation

- Medtronic plc

- Novatech SA

Top Players in the Europe Bronchoscopes Market

Olympus Corporation

Olympus is a global leader in endoscopic technologies with a dominant presence in the European bronchoscopy market through its high definition flexible and therapeutic scopes. The company’s EVIS EXERA III and LUCERA platforms are widely used in academic hospitals across Germany France and the UK for advanced procedures including endobronchial ultrasound and navigated biopsies. Olympus leverages deep clinical partnerships to co develop features like narrow band imaging and high torque insertion tubes that enhance peripheral airway access. Recently the company expanded its single use bronchoscope portfolio with the BF TYPE V slim model designed for ICU bedside use featuring smartphone connectivity and integrated light source. It also launched a digital training academy in partnership with the European Respiratory Society to certify pulmonologists on advanced techniques. These initiatives reinforce Olympus’s commitment to clinical excellence infection control and education across Europe’s evolving respiratory care landscape.

Karl Storz SE & Co KG

Karl Storz is a German medical device pioneer renowned for its rigid endoscopy heritage and expanding flexible bronchoscopy portfolio tailored to European clinical standards. The company supplies high resolution reusable scopes with modular distal chip technology and ergonomic handles favored by thoracic surgeons and interventional pulmonologists in tertiary centers. Karl Storz emphasizes durability precision optics and seamless integration with its IMAGE1 S video systems enabling 4K visualization during complex airway interventions. In recent years the company enhanced its rigid bronchoscopy platform with hybrid scopes featuring working channels and camera integration modernizing a historically analog domain. It also collaborated with university hospitals in Heidelberg and Zurich to develop simulation modules for resident training. By combining German engineering with clinical co creation Karl Storz maintains strong loyalty among specialists performing high acuity therapeutic procedures across Europe.

Ambu A/S

Ambu is a Danish innovator and the world’s leading provider of single use bronchoscopes with a transformative impact on infection prevention and point of care access in Europe. Its aScope 5 series offers high-definition imaging portability and zero reprocessing burden making it the preferred choice for ICUs emergency departments and outpatient clinics across Sweden the Netherlands and the UK. Ambu pioneered the concept of disposable bronchoscopy now endorsed in national guidelines for immunocompromised and ventilated patients. Recently the company introduced the aScope 5 Slim with an ultra-narrow 3.8-millimetre outer diameter enabling neonatal and pediatric use, which is a first in the disposable segment. It also partnered with NHS England to deploy bedside bronchoscopy kits in 50 critical care units reducing procedure wait times. Through relentless focus on usability sustainability and clinical safety Ambu has redefined procedural standards and accelerated the adoption of single use technology across Europe’s acute care continuum.

Top Strategies Used by the Key Market Participants

Key players in the Europe bronchoscopes market pursue strategies centered on clinical differentiation regulatory compliance and ecosystem integration. Companies invest heavily in high resolution imaging narrow band visualization and ergonomic design to enhance diagnostic yield and procedural efficiency. Strategic partnerships with academic hospitals professional societies and training academies build clinical credibility and accelerate skill adoption. Product portfolios increasingly span both reusable and single use segments to address diverse institutional needs and infection control mandates. Digital innovation includes smartphone connectivity AI assisted lesion detection and cloud-based image management to support telemedicine and data analytics. Sustainability initiatives focus on recyclable materials take back programs and life cycle assessments to align with EU green hospital policies. Regulatory preparedness under MDR ensures timely certification while modular designs enable rapid adaptation to evolving clinical workflows. These approaches collectively position bronchoscopy not as a commodity but as an integrated clinical solution within Europe’s advanced respiratory care infrastructure.

MARKET SEGMENTATION

This research report on the Europe bronchoscopes market has been segmented and sub-segmented based on following categories.

By Type

- Flexible

- Video

- Fiberoptic

- Hybrid

- Rigid

By Usage

- Reusable

- Disposable

By End Use

- Hospitals

- Outpatient Facilities

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe Bronchoscopes Market?

The Europe bronchoscopes market focuses on devices used for visualizing and diagnosing conditions within the lungs and airways through minimally invasive procedures.

What factors are driving the growth of the Europe Bronchoscopes Market?

Rising respiratory diseases, increasing lung cancer cases, technological advancements, and demand for minimally invasive diagnostics are key drivers.

Which countries contribute significantly to the Europe Bronchoscopes Market?

Germany, the U.K., France, Italy, and Spain are among the major contributors.

Who are the key players in the Europe Bronchoscopes Market?

Major companies include Olympus Corporation, Fujifilm Holdings Corporation, Ambu A/S, and KARL STORZ GmbH & Co. KG, among others.

What is the role of disposable bronchoscopes in market growth?

Disposable bronchoscopes reduce cross-contamination risks and are increasingly adopted in European healthcare settings.

Which end users dominate the Europe Bronchoscopes Market?

Hospitals, specialty clinics, and ambulatory surgical centers are the primary end users.

How does technological innovation impact the market?

Advancements such as HD imaging, portable devices, and improved maneuverability enhance clinical outcomes and adoption.

What challenges does the Europe Bronchoscopes Market face?

High equipment costs, strict regulatory requirements, and reimbursement limitations may restrain growth.

How did respiratory pandemics influence the bronchoscopes market?

Increased focus on pulmonary diagnostics and infection control boosted demand for advanced and single-use bronchoscopes.

What is the future outlook of the Europe Bronchoscopes Market?

The market is expected to grow steadily due to aging populations, increasing awareness of early diagnosis, and expanding healthcare infrastructure.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com