Europe Business Analytics Software Market Size, Share, Trends & Growth Forecast Report, Segmented By Component, Deployment, Organization, Application, Industry Verticals And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2026 to 2034)

Europe Business Analytics Software Market Size

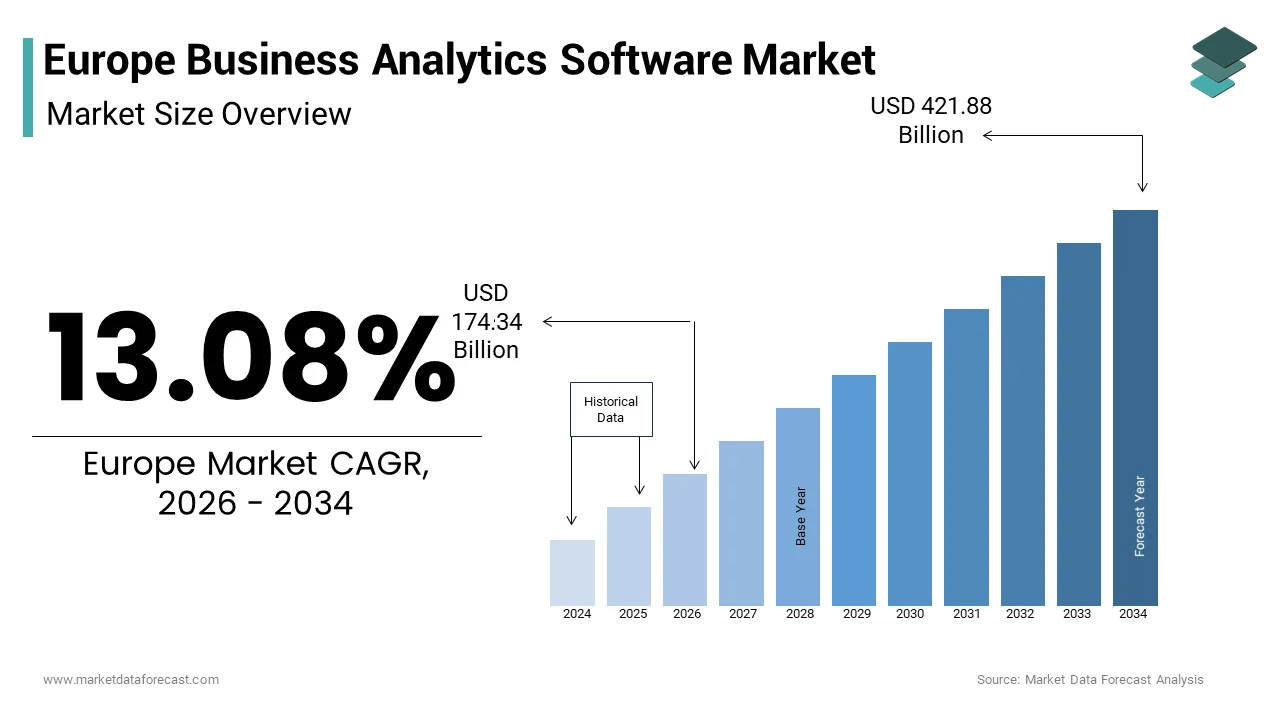

The Europe business analytics software market size was valued at USD 154.14 billion in 2025 and is anticipated to reach USD 174.34 billion in 2026 to reach USD 421.88 billion by 2034, growing at a CAGR of 13.08% during the forecast period from 2026 to 2034.

Europe Business Analytics Software Market Overview

Business analytics software encompasses a sophisticated ecosystem of tools and platforms designed to transform raw data into actionable strategic insights for organizations across various industries. This sector includes descriptive, diagnostic, predictive, and prescriptive analytics solutions that enable enterprises to optimize operations, enhance customer experiences, and drive revenue growth. The region is characterized by a robust digital infrastructure and a strong regulatory framework that influences data handling practices. As per Eurostat, 89% of enterprises in the European Union with ten or more persons employed used cloud computing services in 2023, indicating a foundational readiness for advanced analytics deployment. Furthermore, the European Commission reported that 54% of large enterprises in the EU utilized big data technologies in 2022, reflecting a growing reliance on data driven decision making. The General Data Protection Regulation continues to shape the landscape by mandating strict privacy standards, compelling vendors to integrate security and compliance features directly into their software architectures. According to the International Data Corporation, the volume of data created, captured, copied, and consumed globally is expected to reach 175 zettabytes by 2025, with Europe contributing a significant portion due to its industrial and financial sectors. This data explosion necessitates advanced analytical capabilities to manage complexity and extract value. The shift towards remote work has further accelerated the adoption of cloud based analytics platforms, allowing distributed teams to access real time insights. Consequently, the market is evolving from traditional reporting tools to intelligent, AI enhanced systems that support autonomous decision making and operational agility in a competitive economic environment.

MARKET DRIVERS

Stringent Regulatory Compliance Requirements Drive Adoption of Governance Features

The implementation of stringent regulatory frameworks such as the General Data Protection Regulation and the upcoming Artificial Intelligence Act is majorly driving the growth of the European business analytics software market. Organizations are compelled to invest in advanced analytics platforms that offer robust data governance, lineage tracking, and privacy protection capabilities to ensure compliance with legal mandates. As per the European Data Protection Board, fines for non-compliance with data protection regulations can reach up to 4% of global annual turnover, creating a significant financial incentive for companies to adopt compliant software solutions. Business analytics tools equipped with automated compliance monitoring and audit trails enable enterprises to manage data usage transparently and mitigate legal risks. According to a survey by the International Association of Privacy Professionals, 70% of European organizations have increased their investment in data governance technologies since the enforcement of GDPR. These platforms facilitate the identification and anonymization of personal data, ensuring that analytical processes do not violate privacy rights. Furthermore, the requirement for explainable AI under new regulations drives demand for analytics software that provides clear insights into algorithmic decision making. This regulatory pressure transforms compliance from a burden into a strategic advantage, as companies leveraging governed analytics can build trust with customers and partners. The need for real time reporting to regulatory authorities also necessitates agile analytics systems capable of generating accurate and timely reports. Consequently, the imperative to adhere to evolving legal standards sustains strong demand for sophisticated business analytics software across the European region.

Increasing Volume of Unstructured Data Necessitates Advanced Processing Capabilities

The exponential growth in the volume and variety of unstructured data generated by digital interactions, social media, and Internet of Things devices is further boosting the expansion of the European business analytics software market. Traditional analytical tools struggle to process text, images, and video data, creating a need for sophisticated platforms equipped with natural language processing and machine learning algorithms. As per the International Data Corporation, unstructured data accounts for approximately 80% of all enterprise data, highlighting the inefficiency of legacy systems in capturing comprehensive business insights. European enterprises are increasingly adopting analytics software that can integrate and analyze diverse data sources to uncover hidden patterns and trends. According to Eurostat, 41% of EU enterprises used artificial intelligence in 2023, primarily for data analysis and process automation, indicating a shift towards intelligent analytics solutions. These advanced platforms enable organizations to derive value from customer feedback, sensor data, and multimedia content, enhancing decision making accuracy. The ability to process real time data streams allows businesses to respond swiftly to market changes and operational anomalies. Furthermore, the integration of big data technologies with analytics software facilitates scalable processing of massive datasets without compromising performance. This capability is crucial for industries such as manufacturing and logistics, where IoT sensors generate continuous data flows. By leveraging advanced processing capabilities, European companies can optimize supply chains, personalize marketing strategies, and improve product quality. Thus, the necessity to harness unstructured data drives sustained investment in next generation business analytics solutions.

MARKET RESTRAINTS

Shortage of Skilled Data Professionals Impedes Effective Implementation

A critical shortage of skilled data scientists, analysts, and engineers is a significant restraint to the growth of the Europe business analytics software market, as organizations struggle to fully utilize advanced analytical tools. The complexity of modern analytics platforms requires specialized expertise for configuration, maintenance, and interpretation of results, which is scarce in the current labor market. As per the European Centre for the Development of Vocational Training, there is a projected deficit of 1.2 million digital specialists in the European Union by 2025, with data roles being among the most difficult to fill. This talent gap leads to underutilization of software capabilities, delayed projects, and increased reliance on external consultants, raising overall costs. According to a report by McKinsey and Company, 56% of European executives cite the lack of analytical talent as a major barrier to deriving value from data initiatives. Without qualified personnel, organizations cannot effectively clean, model, or visualize data, resulting in inaccurate insights and poor decision making. The high competition for skilled professionals also drives up salary expectations, straining budgets particularly for small and medium sized enterprises. Furthermore, the rapid evolution of analytics technologies requires continuous training, which many organizations fail to provide adequately. This skills mismatch slows down the adoption of sophisticated features such as predictive modeling and artificial intelligence. Consequently, the inability to staff analytics teams effectively hinders the realization of potential benefits from business analytics software, limiting market expansion and return on investment for many European firms.

High Implementation Costs and Integration Complexities Limit Accessibility

Substantial initial investment requirements and technical complexities associated with integrating business analytics software into existing IT infrastructures is further impeding the growth of the European business analytics software market, particularly for small and medium sized enterprises. The cost of licensing, customization, and hardware upgrades can be prohibitive, while the process of connecting new analytics platforms with legacy systems often involves significant time and resources. As per the European Investment Bank, access to finance remains a challenge for SMEs, with 15% of firms citing high costs as a primary obstacle to digital transformation. Integration issues frequently arise due to incompatible data formats and proprietary protocols, leading to data silos and inconsistent insights. According to a study by Gartner, 60% of big data and analytics projects fail to deliver expected value due to poor data integration and management practices. The need for extensive data cleansing and migration further exacerbates costs and delays deployment timelines. Additionally, ongoing maintenance and support expenses add to the total cost of ownership, making it difficult for smaller organizations to justify the investment. The complexity of configuring security settings and ensuring compliance with data protection regulations also requires specialized expertise, increasing implementation burdens. These financial and technical hurdles discourage widespread adoption, limiting the market to larger corporations with substantial resources. Consequently, the high barrier to entry restricts the potential customer base and slows the overall growth of the business analytics software market in Europe.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Machine Learning Enhances Predictive Capabilities

The seamless integration of artificial intelligence and machine learning technologies into business analytics software is a lucrative opportunity for the European business analytics software market. AI driven analytics can automate data preparation, identify complex patterns, and generate accurate forecasts, enabling organizations to make proactive decisions. As per the European Commission’s Artificial Intelligence Strategy, the EU aims to become a global leader in trustworthy AI, fostering an environment conducive to the development and adoption of AI enhanced analytics tools. According to a survey by PwC, 72% of European business leaders believe that AI will be a significant business advantage in the next three years, driving demand for intelligent analytics solutions. These tools enable predictive maintenance in manufacturing, fraud detection in finance, and personalized recommendations in retail, delivering tangible business value. The ability to automate routine analytical tasks frees up human analysts to focus on strategic initiatives, improving overall productivity. Furthermore, natural language processing features allow users to query data using conversational interfaces, democratizing access to insights across the organization. The growing availability of pre-built AI models and low code platforms reduces the technical barrier to entry, enabling broader adoption. Vendors who innovate in this space can differentiate themselves by offering superior accuracy and ease of use. As European companies strive for competitive advantage through data driven innovation, the demand for AI integrated analytics software is poised for substantial growth, creating significant revenue opportunities for market participants.

Expansion of Cloud Based Analytics Solutions Supports Scalability and Flexibility

The rapid migration of enterprise workloads to cloud environments offers significant opportunities for the expansion of the European business analytics software market. Cloud native analytics platforms enable organizations to process large volumes of data without the need for extensive on premise infrastructure, reducing capital expenditure and maintenance burdens. As per Eurostat, the share of EU enterprises using cloud computing services increased to 45% in 2023, reflecting a strong trend towards cloud adoption. Cloud based solutions facilitate real time collaboration among distributed teams, which is essential in the post pandemic work environment. According to the European Cloud Partnership, the development of a secure and interoperable cloud infrastructure supports the growth of digital services, including analytics. These platforms offer elastic computing resources that can scale up or down based on demand, ensuring optimal performance during peak periods. The subscription based pricing model of cloud analytics makes advanced tools accessible to small and medium sized enterprises, expanding the potential customer base. Furthermore, cloud providers often include built in security and compliance features, addressing regulatory concerns. The ability to integrate with other cloud services such as customer relationship management and enterprise resource planning systems enhances data visibility and operational efficiency. As European businesses continue to prioritize digital agility and cost optimization, the demand for cloud based analytics solutions is expected to surge, driving market growth and innovation.

MARKET CHALLENGES

Data Privacy Concerns and Regulatory Fragmentation Create Compliance Burdens

Persistent concerns regarding data privacy and the fragmented nature of regulatory interpretations across European countries create significant challenges for the business analytics software market in Europe. While the General Data Protection Regulation provides a unified framework, varying national implementations and additional local laws complicate compliance for multinational organizations. As per the European Data Protection Supervisor, inconsistencies in enforcement and guidance lead to legal uncertainty, hindering the free flow of data across borders. Organizations must navigate complex requirements for data consent, storage, and processing, which can restrict the scope of analytical activities. According to a report by the International Chamber of Commerce, 40% of European companies face difficulties in complying with cross border data transfer regulations, impacting their ability to leverage global data sets for analytics. The fear of reputational damage and financial penalties makes companies cautious about adopting advanced analytics features that involve personal data. Furthermore, the emergence of new regulations such as the Data Governance Act and the Data Act adds layers of complexity to compliance strategies. Analytics vendors must continuously update their software to meet evolving legal standards, increasing development costs and time to market. The need for localized data storage and processing further fragments the market, preventing economies of scale. These regulatory complexities deter some organizations from fully exploiting the potential of business analytics, limiting market growth and innovation. Addressing these challenges requires harmonized regulatory approaches and robust compliance tools within analytics platforms.

Resistance to Cultural Change and Data Driven Decision Making

Deep seated resistance to cultural change and the adoption of data driven decision making processes within European organizations is another significant challenge to the European business analytics software market. Many employees and managers rely on intuition and experience rather than data insights, viewing analytics tools as threats to their autonomy or job security. As per a study by Harvard Business Review, 70% of digital transformation initiatives fail due to employee resistance and lack of cultural alignment. This skepticism hinders the adoption of analytics platforms, as users may bypass them or input inaccurate data, compromising the quality of insights. According to the European Foundation for Quality Management, organizations with a strong data culture are five times more likely to make faster decisions, yet cultivating such a culture requires significant effort and leadership commitment. The lack of data literacy among staff further exacerbates the problem, as employees struggle to interpret and act on analytical findings. Training programs often fail to address underlying behavioral biases and organizational silos that impede data sharing. Furthermore, the perceived complexity of analytics tools can intimidate non-technical users, which is leading to low engagement rates. Overcoming this resistance requires comprehensive change management strategies, including executive sponsorship, clear communication of benefits, and incentives for data usage. Without a supportive culture, even the most advanced analytics software cannot deliver value, limiting market potential and return on investment for European enterprises.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 13.08% |

| Segments Covered | By Component, Deployment, Organization, Application, Industry Verticals, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe |

| Market Leaders Profiled | Microsoft (U.S.), SAP (Germany), Oracle (U.S.), IBM (U.S.), SAS Institute (U.S.), Tableau (Salesforce) (U.S.), Qlik (U.S.), Alteryx (U.S.), MicroStrategy (U.S.), TIBCO Software (U.S.) |

SEGMENTAL ANALYSIS

By Component Insights

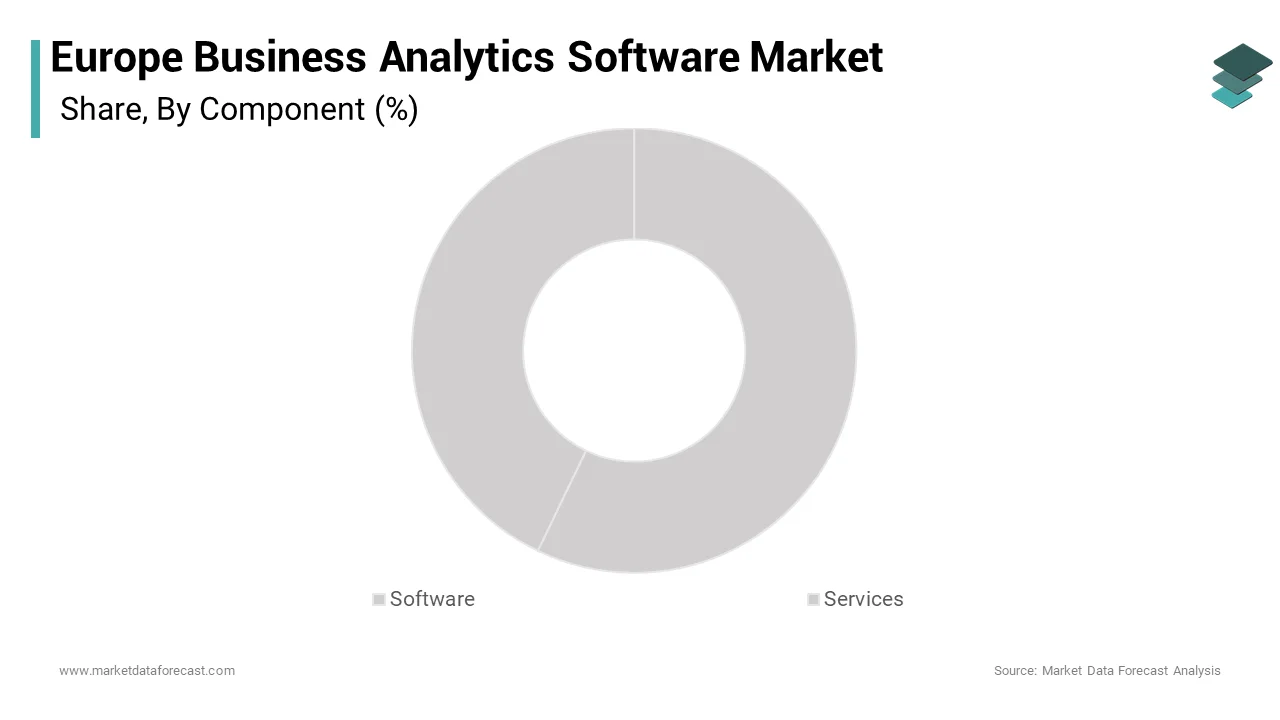

The software segment dominated the market by holding 61.6% of the regional market share in 2025. The dominance of software segment in the European market is primarily driven by the fundamental necessity of analytical platforms to process, visualize, and interpret data that forms the core value proposition for enterprises. As per the International Data Corporation, spending on analytics software in Western Europe continues to outpace hardware and services due to the shift towards subscription based licensing models that provide recurring revenue streams for vendors. The proliferation of self-service analytics tools has democratized data access, allowing non-technical users to generate insights without heavy reliance on IT departments. According to Gartner, by 2025, half of all new business intelligence clients will be acquired through low code or no code platforms, further boosting software adoption. The continuous innovation in features such as real time dashboards, predictive modelling, and natural language query capabilities ensures that organizations regularly upgrade their software licenses to stay competitive. The European Commission’s Digital Decade targets emphasize the importance of digital intensity in businesses, prompting widespread investment in software solutions that enhance operational efficiency. Furthermore, the integration of artificial intelligence into standard analytics packages increases their utility and stickiness within organizational workflows. Companies prefer owning or subscribing to robust software suites that can scale with their data growth, rather than relying solely on external consulting. This intrinsic demand for capable analytical engines solidifies the software segment’s leading share, as it serves as the foundational layer upon which all data driven strategies are built in the European corporate landscape.

On the other hand, the services segment is growing exponentially and is estimated to grow at a CAGR of 15.1% over the forecast period owing to the complex nature of business analytics implementations and the need for specialized customization. Unlike off the shelf software, analytics solutions often require significant configuration to align with specific business processes, data structures, and industry regulations. As per the European Centre for the Development of Vocational Training, there is a persistent skills gap in data science and analytics, with a shortage of over 500,000 professionals in Europe, forcing organizations to rely on external consultants for deployment. Service providers offer expertise in data migration, model development, and system integration that internal teams often lack. According to a report by Deloitte, 65% of European executives state that they lack the internal capabilities to fully exploit their data assets, leading to increased outsourcing of analytics projects. These services include strategic consulting, technical implementation, and change management, which are critical for ensuring successful adoption and return on investment. The complexity of integrating legacy systems with modern cloud based analytics platforms further necessitates professional assistance. Additionally, the rapid evolution of analytics technologies requires continuous training and support, which service firms provide through managed services contracts. As organizations strive to accelerate their digital transformation journeys, the demand for expert guidance and hands on support grows, propelling the services segment’s rapid expansion. This reliance on external expertise ensures that services remain a high growth area, complementing software sales and enhancing overall project success rates.

By Deployment Mode Insights

The cloud-based segment dominated the market by capturing 54.1% of the regional market share in 2025. This dominance is primarily driven by the inherent scalability, flexibility, and cost efficiency offered by cloud platforms that allow organizations to adjust resources based on demand without significant upfront capital expenditure. As per Eurostat, the proportion of EU enterprises using cloud computing services reached 45% in 2023, reflecting a broad shift towards cloud first strategies. Cloud based analytics enable rapid deployment and easier collaboration among distributed teams, which is essential in the post pandemic work environment. According to the European Investment Bank, small and medium sized enterprises particularly benefit from cloud models as they avoid the high costs of maintaining on premises infrastructure. The ability to access advanced analytics capabilities via subscription models lowers the barrier to entry for smaller firms, expanding the customer base. Furthermore, cloud providers continuously update their platforms with the latest features and security patches, ensuring that users always have access to state of the art tools. The European Commission’s support for digital sovereignty and cloud infrastructure development further encourages adoption. The elasticity of cloud resources allows businesses to handle large data volumes during peak periods without performance degradation. This operational agility and financial predictability make cloud based deployment the preferred choice for modern enterprises, solidifying its leading position in the European market and driving continued migration from legacy on premises systems.

However, the on-premises segment is experiencing steady growth in specific sectors and is driven by stringent data sovereignty laws and security requirements that mandate local data storage. Although cloud adoption is widespread, certain industries such as defense, government, and highly regulated financial institutions prefer on premises solutions to maintain complete control over sensitive data. As per the European Data Protection Supervisor, concerns about cross border data transfers and foreign surveillance continue to influence deployment decisions, particularly for critical infrastructure entities. According to the German Federal Office for Information Security, many public sector organizations are required to keep data within national borders, favoring on premises installations. This regulatory pressure ensures a consistent demand for on premises analytics software, particularly in countries with strict data localization policies. Furthermore, organizations with existing substantial investments in data center infrastructure may find it cost effective to retain on premises deployments for certain workloads. The ability to customize security protocols and isolate networks from public internet exposure provides an additional layer of protection against cyber threats. According to a report by the European Union Agency for Cybersecurity, hybrid approaches are becoming common, but core sensitive data often remains on premises. This need for absolute control and compliance with niche regulatory frameworks drives the specialized growth of on premises solutions, ensuring their relevance in the European market despite the broader cloud trend.

By Application Insights

The customer analytics segment led the market by holding 31.3% of the European market share in 2025. The growth of the customer analytics segment in the European market is driven by the intense competition in European retail and service sectors, where understanding customer behavior and preferences is critical for retention and loyalty. As per the European Consumer Organisation, 70% of consumers expect personalized experiences from brands, prompting companies to invest heavily in analytics tools that track and analyze customer interactions. Customer analytics software enables organizations to segment audiences, predict churn, and tailor marketing messages, leading to higher conversion rates. According to a report by Bain and Company, increasing customer retention rates by 5% increases profits by 25% to 95%, highlighting the financial imperative for robust customer analytics. The integration of these tools with customer relationship management systems provides a 360 degree view of the customer journey, allowing for more effective engagement strategies. The General Data Protection Regulation encourages responsible data usage, and analytics platforms help companies comply while still deriving insights. The rise of e commerce has further amplified the need for digital customer analytics to optimize online experiences. By leveraging data to enhance satisfaction and loyalty, businesses can achieve sustainable growth, making customer analytics the most valued application area in the European market.

On the other end, the supply chain analytics segment is projected to register the highest CAGR of 16.1% over the forecast period owing to the urgent need for resilience and risk management in the wake of recent global disruptions. European manufacturers and retailers are prioritizing visibility and agility in their supply chains to mitigate risks associated with geopolitical tensions, pandemics, and natural disasters. As per the European Logistics Association, 60% of supply chain leaders cite visibility as their top priority, driving investment in analytics tools that provide real time tracking and predictive insights. Supply chain analytics software enables organizations to monitor supplier performance, predict delays, and optimize inventory levels, reducing the impact of disruptions. According to a report by McKinsey and Company, companies using advanced supply chain analytics can reduce inventory costs by 20% to 50% while improving service levels. The complexity of global supply networks requires sophisticated modeling capabilities to simulate various scenarios and identify vulnerabilities. The European Commission’s Industrial Strategy emphasizes the importance of resilient supply chains, encouraging adoption of digital tools. Furthermore, the shift towards near shoring and diversification of suppliers necessitates detailed analysis of logistics networks. By enhancing transparency and responsiveness, supply chain analytics helps businesses maintain continuity and competitiveness, driving rapid adoption and growth in this segment across Europe.

By Industry Vertical Insights

The banking, financial services, and insurance (BFSI) segment led the market by holding 26.2% of the regional market share in 2025. The growth of the BFSI segment in the European market is driven by the stringent regulatory requirements for risk management, anti-money laundering and fraud detection that characterize the financial industry. As per the European Banking Authority, financial institutions must maintain robust monitoring systems to comply with directives such as PSD2 and AMLD5, necessitating advanced analytics capabilities. Analytics software enables real time transaction monitoring, identifying suspicious patterns and preventing fraudulent activities. According to a report by Nilson Report, card fraud losses in Europe amounted to 1.8 billion euros in 2022, underscoring the critical need for effective detection tools. Furthermore, banks use analytics for credit scoring, customer segmentation, and personalized product recommendations, enhancing profitability and customer satisfaction. The Basel III regulatory framework requires precise capital adequacy calculations, which rely on sophisticated data modeling and analysis. The high volume of transactions generated by digital banking platforms provides rich data sources for analytical insights. The European Insurance and Occupational Pensions Authority also mandates rigorous risk assessment for insurance providers, driving analytics adoption. By ensuring compliance and mitigating financial risks, analytics software becomes indispensable for BFSI organizations, solidifying the sector’s leading position in the market and driving continuous investment in advanced analytical solutions.

However, the healthcare segment is projected to witness a promising CAGR of 17.4% over the forecast period in the European market owing to the growing aging population in Europe and the increasing prevalence of chronic diseases that require data driven management strategies. As per Eurostat, the share of the population aged 65 and over in the EU is expected to reach 30% by 2050, increasing the demand for healthcare services and efficient resource allocation. Business analytics software helps hospitals and providers optimize patient flow, manage staff schedules, and predict equipment maintenance needs. According to the World Health Organization, chronic diseases account for 86% of deaths in the European region, necessitating long term care management supported by data insights. Analytics enable predictive modeling for patient readmissions, allowing interventions that improve outcomes and reduce costs. The European Commission’s Health Union initiative promotes the use of data to strengthen health systems, encouraging adoption of analytics tools. Electronic health records generate vast amounts of data that, when analyzed, provide insights into treatment effectiveness and population health trends. The need for personalized medicine also drives demand for analytics that can process genomic and clinical data. By improving operational efficiency and patient care quality, analytics software addresses critical challenges in the healthcare sector, driving rapid growth and adoption across European hospitals and clinics.

COUNTRY LEVEL ANALYSIS

Germany Business Analytics Software Market Analysis

Germany accounted for 23.6% of the regional market share in 2025 and emerged as the most dominating country in the European market. The growth of Germany in the European market is driven by its strong industrial base, particularly in manufacturing and automotive sectors, which heavily rely on data for operational efficiency. The country’s Industry 4.0 initiative promotes the integration of digital technologies, including analytics, into production processes. As per the German Federal Ministry for Economic Affairs and Climate Action, digital investment in German industry has increased by 12% annually, supporting analytics adoption. The presence of major software vendors and a skilled workforce further strengthens the market. According to Bitkom, the German digital association, 75% of companies with more than 100 employees use data analytics tools. The manufacturing sector utilizes analytics for predictive maintenance and quality control, driving significant demand. The financial sector in Frankfurt also contributes to market growth through risk management and compliance applications. Government support for digital sovereignty and data infrastructure enhances confidence in analytics solutions. The strong emphasis on engineering precision and process optimization aligns well with the capabilities of business analytics software. This combination of industrial strength, regulatory support, and technological readiness positions Germany as the leading market for business analytics in Europe, setting benchmarks for innovation and adoption.

United Kingdom Business Analytics Software Market Analysis

The United Kingdom held a prominent share of the European business analytics software market in 2025 due to a dynamic financial services sector and a vibrant tech ecosystem. London is a global hub for data science and AI innovation, attracting significant venture capital investment in analytics startups. As per the Office for National Statistics, the digital sector contributes over 150 billion pounds annually to the UK economy, with data analytics being a key subsector. The strong presence of international corporations and tech savvy SMEs drives widespread adoption of advanced analytical tools. According to TechUK, 60% of British businesses plan to increase their investment in data analytics and AI in the coming years. The retail sector in the UK extensively uses customer analytics to optimize multi channel experiences and loyalty programs. The government’s National Data Strategy aims to unlock the value of data across the economy, fostering a supportive environment for analytics deployment. High levels of digital literacy and a focus on data driven innovation among British executives ensure a mature market for analytics software. The integration of analytics into public services, including the NHS, further expands market reach. This robust demand across multiple sectors and a favorable innovation environment solidify the UK’s prominent role in the European analytics landscape.

COMPETITIVE LANDSCAPE

The competition in the Europe business analytics software market is intense and characterized by the presence of global technology giants alongside specialized niche vendors. Major players leverage their extensive product portfolios and established customer bases to maintain dominance while smaller firms differentiate themselves through innovative features and industry specific solutions. The market exhibits high barriers to entry due to the need for significant investment in research and development and compliance with strict regulatory standards. Companies compete on the basis of ease of use scalability and integration capabilities with existing enterprise systems. The shift towards cloud based deployments has intensified rivalry as vendors strive to offer flexible and cost effective subscription models. Strategic alliances and acquisitions are common as firms seek to expand their technological capabilities and geographic reach. Data security and privacy remain critical differentiators with vendors emphasizing compliance with European regulations to build trust. The rapid pace of technological advancement requires continuous innovation to stay ahead of competitors. Customer support and professional services also play a vital role in retaining clients and ensuring successful implementation. This dynamic environment drives constant improvement in product quality and service delivery benefiting end users across the region.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe business analytics software market are

- Microsoft (U.S.)

- SAP (Germany)

- Oracle (U.S.)

- IBM (U.S.)

- SAS Institute (U.S.)

- Tableau (Salesforce) (U.S.)

- Qlik (U.S.)

- Alteryx (U.S.)

- MicroStrategy (U.S.)

- TIBCO Software (U.S.)

Top Players In The Market

- SAP SE maintains a formidable presence in the Europe business analytics software market by leveraging its extensive enterprise resource planning ecosystem to deliver integrated analytical solutions. The company empowers organizations to transform raw data into actionable insights through its SAP Analytics Cloud platform which combines business intelligence planning and predictive capabilities. SAP recently enhanced its artificial intelligence functionalities within the cloud environment to enable automated insight generation and natural language querying for users. This innovation allows European enterprises to make faster decisions without requiring deep technical expertise. The company actively collaborates with industry partners to ensure seamless integration with existing legacy systems which is crucial for large European manufacturers. SAP continues to invest heavily in data governance features to help clients comply with strict European privacy regulations. By focusing on sustainability analytics the company helps businesses track and reduce their carbon footprints effectively. These strategic initiatives reinforce its position as a trusted partner for digital transformation across various industries in the region.

- Microsoft Corporation dominates the Europe business analytics software market through its comprehensive Power BI platform which offers robust data visualization and sharing capabilities. The company integrates analytics deeply with its Office 365 suite enabling widespread adoption among European businesses of all sizes. Microsoft recently introduced advanced AI driven features such as Copilot which assists users in creating reports and interpreting data trends automatically. This enhancement significantly reduces the time required for data analysis and democratizes access to insights across organizations. The company prioritizes security and compliance ensuring that its cloud services meet stringent European regulatory standards. Microsoft also expands its partner network to provide localized support and specialized industry solutions. By offering flexible deployment options including hybrid and multi cloud environments the company addresses diverse infrastructure needs. Continuous updates and user friendly interfaces keep Power BI at the forefront of self service analytics. These efforts strengthen its market position by delivering scalable and secure analytical tools to European enterprises.

- Oracle Corporation serves as a key player in the Europe business analytics software market by providing powerful database technologies and integrated analytics applications. The company offers Oracle Analytics Cloud which enables organizations to unify data from multiple sources for comprehensive reporting and forecasting. Oracle recently strengthened its portfolio by embedding machine learning algorithms directly into its analytics tools to enhance predictive accuracy. This advancement allows European companies to anticipate market trends and optimize operational efficiency proactively. The firm focuses on delivering industry specific solutions for sectors such as telecommunications finance and retail which are prominent in Europe. Oracle also emphasizes data sovereignty by establishing local cloud regions to ensure compliance with European data protection laws. Its commitment to open standards facilitates easy integration with third party applications and legacy systems. By providing scalable and secure analytics infrastructure Oracle supports the digital transformation goals of major European corporations. These strategic moves巩固 its reputation as a reliable provider of enterprise grade analytics solutions.

Top Strategies Used By Key Market Participants

Key players in the Europe business analytics software market primarily focus on integrating artificial intelligence and machine learning capabilities to enhance predictive analytics and automate data processing tasks. Companies invest heavily in developing user friendly interfaces that enable non technical users to generate insights through self service platforms. Strategic partnerships with cloud infrastructure providers ensure scalable and secure deployment options for enterprise clients. Vendors prioritize compliance with European data protection regulations by implementing robust governance and security features within their software. Continuous innovation through research and development allows firms to offer real time analytics and advanced visualization tools. Expansion of industry specific solutions helps address unique challenges faced by sectors such as healthcare manufacturing and finance. Acquisitions of niche technology startups enable larger players to broaden their functional offerings and acquire specialized talent. Training and certification programs are launched to upskill the workforce and promote widespread adoption of analytical tools. These multifaceted strategies drive competitive advantage and sustain growth in the dynamic European market landscape.

MARKET SEGMENTATION

This research report on the Europe business analytics software market is segmented and sub-segmented into the following categories.

By Component

- Software

- Services

By Deployment

- On-Premises

- Cloud-Based

By Organization

- SMEs

- Large Enterprises

By Application

- Customer Analytics

- Marketing Analytics

- Pricing Analytics

- Supply Chain Analytics

- Others

By Industry verticals

- IT & Telecom

- Healthcare

- Retail

- Manufacturing

- BFSI

- Government

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is currently driving growth in the Europe business analytics software market?

Rising demand for data-driven decision-making and real-time insights is driving market growth.

Why are companies in Europe increasingly adopting business analytics software?

They use it to improve efficiency, forecasting, and competitive advantage.

How would you explain business analytics software in simple terms?

It is software that analyzes data to help businesses make better decisions.

Where is business analytics software most commonly used across Europe?

It is widely used in finance, retail, healthcare, manufacturing, and IT sectors.

What makes business analytics tools essential for modern enterprises?

They transform raw data into actionable insights for better performance.

From a practical standpoint, is investing in analytics software worthwhile?

Yes, it improves productivity and supports smarter business strategies.

What challenges are affecting the Europe business analytics software market?

Data privacy concerns and integration complexities are key challenges.

How is digital transformation influencing demand for analytics solutions?

Increasing digital adoption is boosting the need for advanced data analysis tools.

Which deployment model is most preferred in this market?

Cloud-based solutions are widely preferred for their scalability and flexibility.

Is the Europe business analytics software market growing steadily?

Yes, it is expanding with growing enterprise reliance on data insights.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com