Europe Butterfly Valve Market Research Report By Product Type ( High-Performance Butterfly Valve , Lined Butterfly Valve ) Material Type , Design & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of EU) - Industry Analysis on Size, Share, Trends & Growth Forecast (2026 to 2034)

Europe Butterfly Valve Market Size

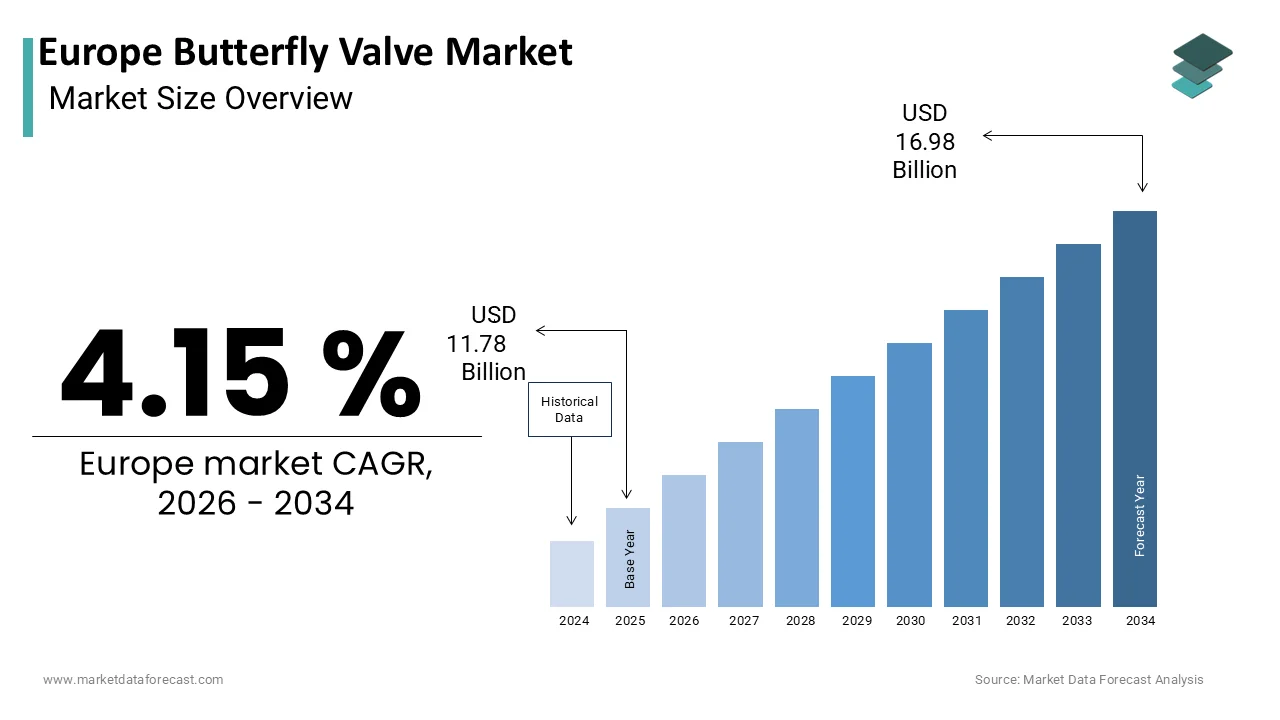

The Europe Butterfly Valve Market Size was valued at USD 11.78 billion in 2025, is expected to have 4.15 % CAGR from 2026 to 2034 and be worth USD 16.98 billion by 2034 from USD 12.27 billion in 2026.

The Europe butterfly valve market refers to a segment of industrial flow control equipment used in various sectors such as water treatment, oil and gas, chemical processing, power generation, and HVAC systems. Butterfly valves are quarter-turn rotational valves that regulate the flow of liquids or gases through pipelines by rotating a disc within the flow path. Known for their compact design, lightweight construction, and cost-effectiveness compared to other valve types, butterfly valves are widely adopted across medium-to-high volume applications.

The market is shaped by stringent regulatory requirements regarding safety, efficiency, and environmental compliance, especially under directives from the European Pressure Equipment Directive (PED) and ISO standards on pipeline integrity.

MARKET DRIVERS

Expansion of Water and Wastewater Infrastructure

One of the primary drivers of the Europe butterfly valve market is the expansion and modernization of water and wastewater infrastructure. These projects involve replacing outdated gate and globe valves with more efficient butterfly valves, which offer lower maintenance costs and better flow regulation. With the European Commission allocating €60 billion under the LIFE program for sustainable water management through 2030, the demand for durable, corrosion-resistant butterfly valves is expected to grow significantly across the continent.

Growth in Renewable Energy and District Heating Systems

Another significant driver of the Europe butterfly valve market is the rapid growth of renewable energy and district heating systems, particularly in Northern and Central Europe. Countries like Denmark, Sweden, and Finland have prioritized district heating networks as part of their decarbonization strategies, requiring precise flow control solutions to manage heat distribution efficiently. According to the International Energy Agency, district heating now supplies significant share of residential heating needs in Scandinavian cities, reinforcing the need for reliable butterfly valves in thermal transfer pipelines. In addition, the expansion of biomass, geothermal, and waste-to-energy plants has intensified demand for butterfly valves capable of handling variable temperatures and pressures. As the EU accelerates its transition toward clean energy sources, the need for robust flow control equipment will continue to drive growth in the butterfly valve industry across Europe.

MARKET RESTRAINTS

Volatility in Raw Material Prices and Supply Chain Disruptions

A major restraint affecting the Europe butterfly valve market is the volatility in raw material prices and ongoing supply chain disruptions, which have significantly impacted production timelines and pricing structures. Steel, stainless steel, ductile iron, and thermoplastic materials constitute a large portion of manufacturing costs, and fluctuations in global commodity markets have introduced unpredictability into procurement planning. According to the London Metal Exchange, steel prices rose between 2021 and 2023 due to energy shortages and geopolitical tensions. Besides, the war in Ukraine disrupted critical supply routes for valve components, particularly affecting manufacturers in Italy and Austria that rely on Eastern European foundries for castings and forgings. The European Chemical Industry Council notes that polytetrafluoroethylene (PTFE) and rubber seal prices increased during the same period, further inflating production costs. Many small- and medium-sized enterprises reported order backlogs exceeding several months.

Regulatory Complexity and Certification Requirements

Another critical constraint on the Europe butterfly valve market is the complexity of regulatory frameworks and certification requirements that vary across EU member states. While harmonized standards exist under the Pressure Equipment Directive (PED) and ATEX directive for explosive environments, national implementation often introduces additional testing, documentation, and compliance burdens. According to the European Committee for Standardization (CEN), discrepancies in fire-safe certification, pressure rating classifications, and non-destructive testing protocols complicate cross-border trade and product standardization. Similarly, in Italy, the Italian National Institute for Insurance against Accidents at Work (INAIL) enforces stricter sealing and leak-tightness tests for industrial valves beyond EU norms. These challenges are compounded by evolving directives under the European Green Deal, which emphasize recyclability and reduced carbon footprints in manufacturing processes.

MARKET OPPORTUNITIES

Digitalization and Smart Valve Integration

A compelling opportunity emerging in the Europe butterfly valve market is the integration of digital technologies and smart valve systems. As industries move toward predictive maintenance and real-time monitoring, butterfly valve manufacturers are incorporating IoT-enabled actuators, position sensors, and condition-based diagnostics into their products. According to McKinsey & Company, the adoption of smart industrial valves in Europe grew between 2021 and 2023, driven by advancements in Industry 4.0 and process automation. Germany stands out as a leader in this trend, with Siemens and Endress+Hauser launching intelligent valve control platforms that interface directly with SCADA and building management systems. Additionally, Norway’s Equinor integrated digital butterfly valves into offshore oil and gas platforms to enhance process efficiency and reduce unplanned downtime.

Rise of Decentralized Energy and Water Treatment Plants

Another transformative opportunity for the Europe butterfly valve market lies in the proliferation of decentralized energy and water treatment facilities. Driven by local resilience initiatives and decentralization policies, many municipalities and private operators are shifting away from centralized utility models toward smaller, modular treatment units that require efficient and scalable flow control mechanisms. These facilities rely extensively on butterfly valves for regulating water flow, managing filtration processes, and ensuring system reliability. With continued investment in localized energy and water infrastructure, the butterfly valve market is positioned to benefit from rising demand in decentralized industrial and municipal applications.

MARKET CHALLENGES

Intensifying Competition from Alternative Valve Technologies

A pressing challenge confronting the Europe butterfly valve market is the intensifying competition from alternative valve technologies such as ball valves, gate valves, and control valves that offer superior performance in specific high-pressure or precision-flow applications. Like, while butterfly valves remain popular for their compact size and cost-efficiency, they are increasingly being replaced in high-end industrial settings by more advanced alternatives offering tighter shut-off capabilities and higher temperature resistance. Similarly, in the pharmaceutical and food processing industries, hygiene and contamination concerns have prompted a preference for full-port ball valves with minimal dead space. This technological shift is pushing butterfly valve manufacturers to innovate in design and materials to retain relevance in niche applications where conventional butterfly valves once dominated.

Labor Shortages and Skilled Technical Support Constraints

Another significant challenge for the Europe butterfly valve market is the shortage of skilled technical personnel required for installation, maintenance, and troubleshooting of complex valve systems. As industries adopt automated and smart valve technologies, the demand for trained technicians who can commission and service these systems has surged. However, the European Centre for the Development of Vocational Training (CEDEFOP) reports that a significant share of mechanical engineering firms in Germany and Austria face difficulties in finding qualified valve fitters and instrumentation engineers. This skills gap is particularly evident in Italy and Poland, where vocational training programs have not kept pace with technological advancements in valve actuation and control systems. Without targeted interventions to bridge the knowledge gap and provide specialized training in valve technology, companies may experience delays in project execution and higher service costs, limiting the market’s ability to scale alongside evolving industrial needs.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Segments Covered | By By Product Type ,Material Type , Design and Country. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, Germany, Italy, France, Spain, Sweden, Denmark, Poland, Switzerland, Netherlands, Rest of Europe. |

| Market Leaders Profiled | Alfa Laval Corporate AB, Curtiss-Wright Corporation, Flowserve Corporation |

SEGMENT ANALYSIS

By Product Type Insights

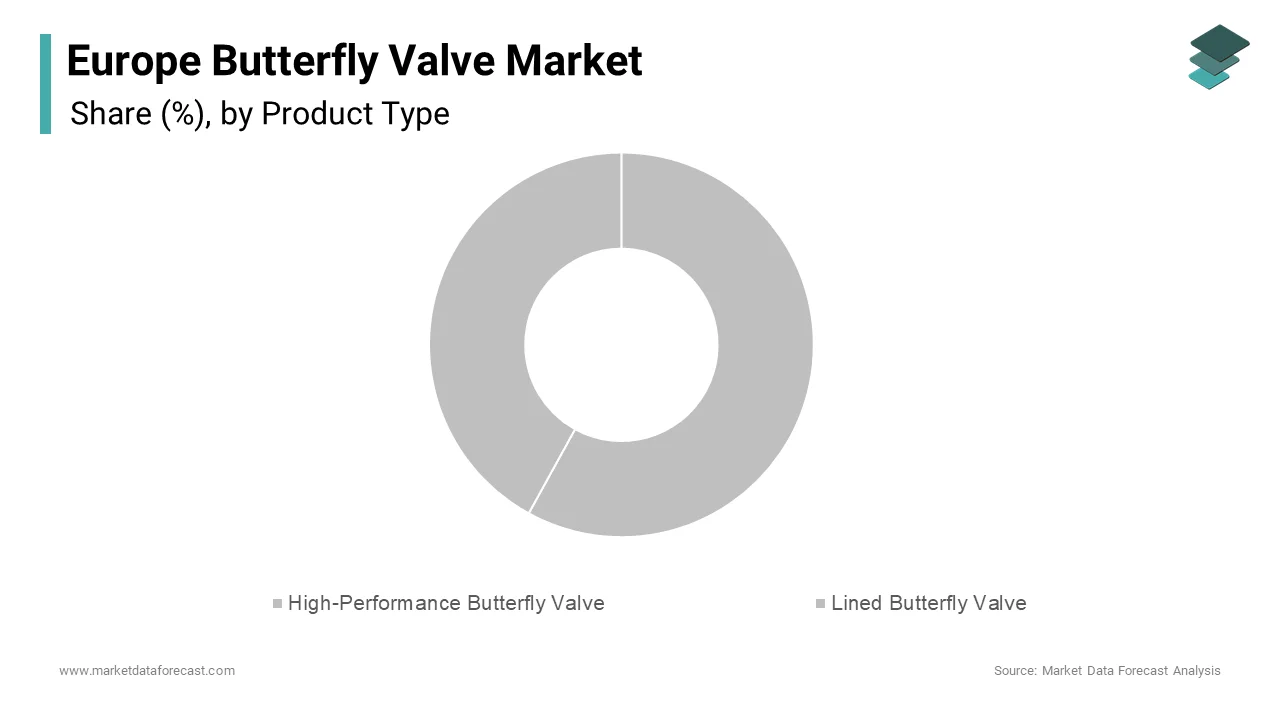

The high-performance butterfly valve segment dominated the Europe butterfly valve market by capturing a 58.4% of total revenue in 2025. This is primarily attributed to its widespread adoption across critical industrial applications such as oil and gas, chemical processing, and power generation, where reliable shut-off capabilities, pressure containment, and minimal leakage are essential. Additionally, the UK’s Environment Agency emphasized the importance of leak-proof systems in municipal water infrastructure upgrades, further reinforcing demand for this product category. With ongoing industrial modernization and increasing focus on operational efficiency, the high-performance butterfly valve segment continues to maintain a dominant position across the region.

The lined butterfly valve segment is projected to grow at the highest CAGR of 6.9% and is driven by rising demand in corrosive media handling applications within the chemical, pharmaceutical, and wastewater treatment sectors. These valves feature internal linings made from materials such as EPDM, PTFE, or rubber, offering enhanced resistance to aggressive fluids and ensuring long-term durability. The Swedish Environmental Protection Agency also noted an increase in lined butterfly valve usage in industrial effluent management systems, particularly in pulp and paper mills along the coast. In Italy, the Italian National Institute for Insurance against Accidents at Work (INAIL) mandated the use of lined valves in food and beverage processing units to prevent contamination and ensure compliance with hygiene standards. As industries prioritize longevity and material compatibility in harsh environments, the lined butterfly valve segment is poised for accelerated adoption across Europe.

By Material Type Insights

The stainless steel remained the largest material type in the Europe butterfly valve market by accounting for a 42.6% of total revenue in 2025. This dominance is primarily attributed to its exceptional corrosion resistance, mechanical strength, and suitability for high-temperature and chemically aggressive environments. According to the European Stainless Steel Development Association (Euro Inox), stainless steel valves are preferred in industries such as petrochemicals, pharmaceuticals, and marine engineering due to their longevity and compliance with stringent safety standards. With continued investment in clean technology and process industries, stainless steel butterfly valves remain central to the region's industrial fluid control landscape.

The aluminum butterfly valve segment is anticipated to grow at the fastest CAGR of approximately 7.1% which is fueled by increasing demand in lightweight, non-corrosive applications across HVAC, marine, and renewable energy sectors. In Sweden, the Swedish Energy Agency reported a significant rise in aluminum butterfly valves being deployed in district heating distribution networks due to their lightweight properties and resistance to atmospheric corrosion. As manufacturers seek lighter alternatives that still provide adequate performance, the aluminum butterfly valve segment is positioned for sustained high-growth momentum across Europe.

By Design Insights

The centric butterfly valve design contributed the biggest share of the Europe butterfly valve market i.e. 38.8% of total revenue in 2025. This position is primarily attributed to its simplicity, cost-effectiveness, and suitability for low-to-medium pressure applications across water supply, HVAC, and general industrial settings. Moreover, the International Water Association reports that a large share of newly commissioned irrigation and wastewater pumping stations in Spain and Portugal utilized centric butterfly valves for basic flow control. With strong footholds in public infrastructure and commercial building services, the centric butterfly valve design continues to dominate due to its versatility and affordability in standard operating conditions.

The triple-eccentric butterfly valve segment is estimated to rise at the highest CAGR of 8.3%. It is caused by rising demand in high-pressure and high-temperature applications within the energy, refining, and power generation sectors. Unlike conventional designs, triple-eccentric butterfly valves offer metal-to-metal sealing and zero friction during operation, making them ideal for critical service environments. In Denmark, Ørsted reported increased deployment of these valves in offshore wind farm substations to manage steam and condensate flows efficiently.

COUNTRY LEVEL ANALYSIS

Germany held the largest share of the Europe butterfly valve market i.e. 21.5% of total regional revenues in 2025. This is attributed to the country’s robust industrial base, advanced manufacturing infrastructure, and proactive policies promoting energy efficiency and industrial automation. Additionally, the push for Industry 4.0 integration has led to greater adoption of smart butterfly valves equipped with digital actuators and condition monitoring features. Supported by stable economic conditions and policy alignment with EU sustainability goals, Germany remains the dominant force in the European butterfly valve market.

France accounts for a significant share of the Europe butterfly valve market which is driven by strategic investments in infrastructure modernization and energy transition programs. Also, Major industrial players like Schneider Electric and Alstom have also integrated butterfly valves into their modular plant designs for easier maintenance and scalability. With continued policy backing and growing investor interest in ESG-aligned industrial assets, France maintains a key position in the European butterfly valve market.

The United Kingdom market is supported by strong investments in water infrastructure upgrades and utility modernization. The UK Environment Agency emphasized that leakage rates in aging water mains exceeded 25% in some regions, prompting Anglian Water, Thames Water, and Yorkshire Water to invest heavily in durable butterfly valves capable of withstanding fluctuating pressures and preventing system failures. Also, the Department for Business, Energy & Industrial Strategy incentivized the adoption of energy-efficient pump and valve systems through the Industrial Energy Transformation Fund. With ongoing investment in sustainable utilities and stricter regulatory oversight, the UK remains a key player in the European butterfly valve industry.

Italy is expanding process industry applications in the Europe butterfly valve market that is propelled by expanding applications in process industries such as petrochemicals, food and beverage, and pharmaceuticals. The Italian National Institute for Insurance against Accidents at Work (INAIL) mandated the use of lined and triple-eccentric butterfly valves in hazardous environments to improve safety and reduce maintenance cycles. It also saw a surge in butterfly valve retrofits in food processing facilities due to hygiene-driven upgrades. With ongoing PNRR implementation and regulatory reforms, Italy is strengthening its role in the European butterfly valve market.

Spain market is driven by increasing demand in renewable energy projects and smart city development initiatives. Additionally, Barcelona and Madrid implemented urban regeneration programs that incorporated butterfly valves into smart water distribution grids. With continued investment in clean energy and sustainable infrastructure, Spain is solidifying its position in the European butterfly valve market.

COMPETITIVE LANDSCAPE

The competition in the Europe butterfly valve market is highly dynamic, featuring a mix of multinational corporations, specialized regional manufacturers, and niche suppliers serving specific industrial applications. Established players such as Crane Co., Velan, and Flowserve dominate due to their broad product portfolios, technical expertise, and deep-rooted relationships with end-user industries. However, mid-sized firms and local valve manufacturers are gaining traction by focusing on cost-effective alternatives, rapid delivery, and tailored engineering services.

A defining feature of the competitive landscape is the increasing emphasis on material quality, sealing performance, and digital integration, with companies racing to develop smart butterfly valves equipped with IoT-enabled actuators and condition monitoring capabilities. Additionally, the growing adoption of Industry 4.0 and predictive maintenance strategies has intensified demand for intelligent flow control solutions that enhance process efficiency and reduce unplanned downtime.

Brand differentiation is increasingly tied to technical certification, environmental credentials, and customer-centric service delivery. As industrial modernization accelerates and regulatory frameworks evolve, the ability to deliver compliant, high-performance butterfly valves will determine long-term success in this technically demanding and highly regulated market.

KEY MARKET PLAYERS

Companies playing a prominent role in the Europe Butterfly Valve Market are

- Alfa Laval Corporate AB

- Curtiss-Wright Corporation

- Flowserve Corporation

- Emerson Electric Co.

- Pentair plc

- Weir Group PLC

- AVK Group A/S

- Crane Company

- Schlumberger Limited

- Velan Inc.

- KSB SE & Co. KGaA

Top Players in the Market

Crane Co.

Crane Co. is a leading global manufacturer of industrial valves, including butterfly valves, with a strong presence in the Europe market. The company supplies high-performance and triple-eccentric butterfly valves tailored for oil and gas, power generation, and chemical processing applications. Crane is known for its engineering excellence, reliability, and compliance with international standards such as API and ISO.

The company contributes significantly to the global butterfly valve industry by setting benchmarks in material durability, sealing technology, and automation integration. Through its subsidiary, Crane ChemPharma & Energy, it continues to innovate in flow control solutions that enhance operational efficiency and safety. Its commitment to digitalization and sustainable manufacturing has positioned it as a key influencer in shaping future trends in European and international butterfly valve markets.

Velan Inc.

Velan is a major player in the Europe butterfly valve market, recognized for delivering durable, high-quality valves designed for extreme operating conditions across energy, refining, and nuclear power sectors. The company specializes in metal-seated and triple-eccentric butterfly valves that offer superior leak-tight performance and long service life.

Velan contributes to the global market by integrating advanced metallurgy and precision engineering into its valve designs, ensuring compatibility with high-pressure and high-temperature environments. Its products are widely adopted in critical infrastructure projects that demand zero-failure performance and regulatory compliance. With a strong R&D focus and strategic partnerships across the process industries, Velan continues to expand its influence in the European butterfly valve landscape.

Flowserve Corporation

Flowserve is one of the largest manufacturers and suppliers of industrial fluid control equipment, including butterfly valves used extensively in European process industries. The company offers a comprehensive portfolio ranging from standard centric to high-performance and lined butterfly valves suited for water treatment, chemical processing, and energy systems.

Flowserve plays a critical role in advancing flow control technology, particularly through smart actuation and predictive maintenance solutions that improve system reliability and reduce downtime. By leveraging its global distribution network and technical expertise, Flowserve supports large-scale infrastructure upgrades and industrial modernization programs across Europe. As sustainability and digital transformation reshape the sector, Flowserve remains at the forefront of innovation in butterfly valve applications.

Top strategies used by the key market participants

One major strategy employed by leading players in the Europe butterfly valve market is product innovation and technological differentiation , where companies focus on developing advanced sealing mechanisms, corrosion-resistant materials, and smart valve technologies to meet evolving industrial demands and regulatory requirements.

Another key strategy is strategic partnerships and collaborations , particularly with engineering firms, automation specialists, and system integrators to ensure seamless incorporation of butterfly valves into complex industrial setups and digitalized plant operations.

Lastly, localized production and after-sales service expansion allow companies to respond more efficiently to regional demand fluctuations, reduce lead times, and provide customized support for installation, maintenance, and compliance certifications, reinforcing their competitive positioning across diverse industrial segments.

RECENT HAPPENINGS IN THE MARKET

- In January 2025, Crane Co. launched a new line of compact triple-eccentric butterfly valves in Germany, targeting space-constrained applications in refineries and petrochemical plants while improving thermal stability and seal integrity.

- In March 2025, Velan partnered with a French automation specialist to integrate smart actuators into its butterfly valve offerings, enabling remote diagnostics and real-time flow control adjustments for industrial clients seeking enhanced process visibility.

- In June 2025, Flowserve expanded its butterfly valve production facility in Spain, increasing capacity to meet rising demand from renewable energy and desalination projects across Southern Europe and North Africa.

- In September 2025, IMI plc acquired a German valve actuation startup to strengthen its digital valve control capabilities, particularly in HVAC and district heating networks requiring precision flow regulation and energy optimization.

- In November 2025, Neles, a part of Valmet, introduced a next-generation lined butterfly valve series in Sweden, designed specifically for aggressive media handling in pulp and paper mills and wastewater treatment plants, reinforcing its foothold in corrosive environment applications.

MARKET SEGMENTATION

This research report on the europe butterfly valve market has been segmented and sub-segmented into the following categories.

By Product Type

- High-Performance Butterfly Valve

- Lined Butterfly Valve

By Material Type

- Stainless Steel

- Aluminium

By Design

- Centric Butterfly Valve

- Triple-Eccentric Butterfly Valve

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe.

Frequently Asked Questions

What is the future outlook for the Europe butterfly valve market?

The market is set for steady growth, with digitalization and sustainability as major themes. Demand for low-emission and leak-free systems will drive advanced valve solutions, while retrofits in aging infrastructure will support ongoing sales. Investments in renewable energy and hydrogen infrastructure could open new high-growth niches.

Which countries lead the Europe butterfly valve market?

Germany, France, the U.K., and Italy are the largest markets, backed by strong manufacturing bases, stringent environmental regulations, and ongoing upgrades to water and power infrastructures.

What is a butterfly valve and where is it used?

A butterfly valve is a quarter-turn rotational device that uses a “butterfly” disc to regulate flow. It’s commonly used in water treatment, oil & gas, chemical processing, power generation, and HVAC systems for on/off and throttling services.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com