Europe Carbon Footprint Management Market Size, Share, Trends & Growth Forecast Report – Segmented By Deployment (On-premise, Cloud), Type, End Use, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Carbon Footprint Management Market Size

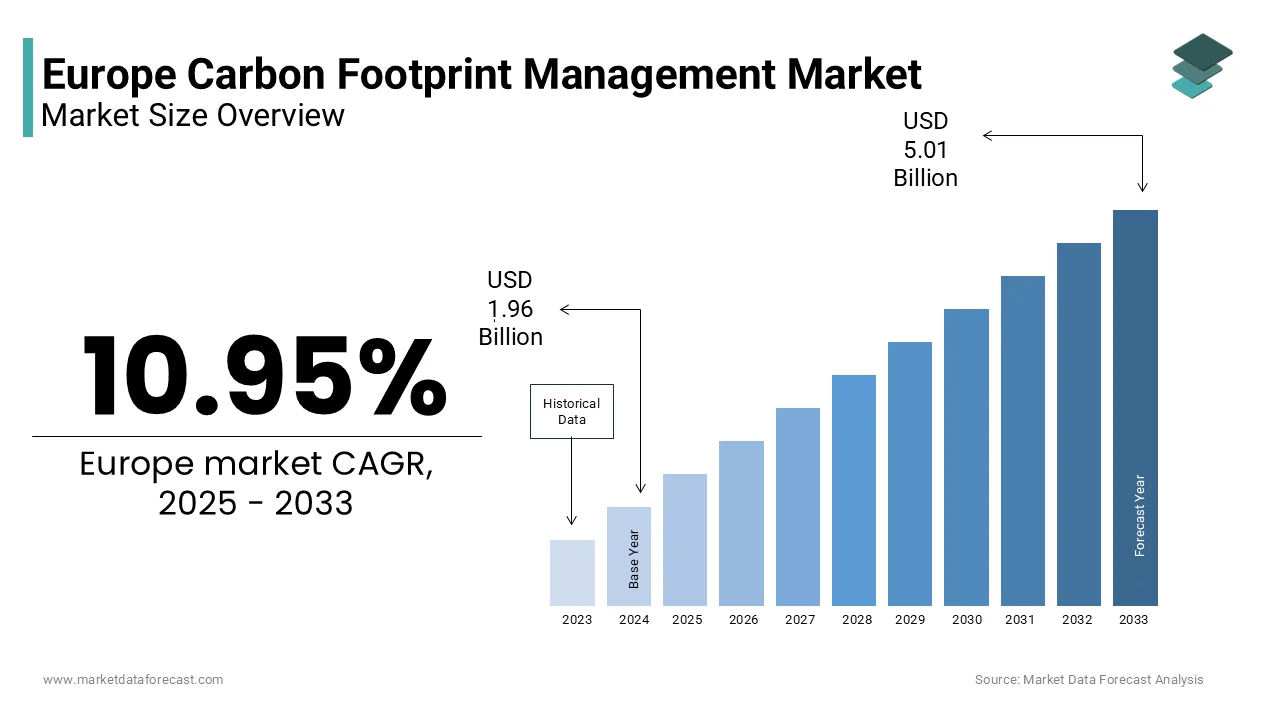

The Europe carbon footprint management market size was valued at USD 1.96 billion in 2024 and is projected to reach USD 5.01 billion by 2033 from USD 2.18 billion in 2025, growing at a CAGR of 10.95%.

Carbon footprint management refers to the systematic measurement, monitoring, reduction, and reporting of greenhouse gas emissions across organisational value chains using digital platforms, data analytics, cs and regulatory compliance frameworks. This market has evolved from voluntary sustainability initiatives into a mandatory operational function driven by the European Union’s legally binding climate architecture. The region’s regulatory landscape now mandates emissions disclosure for thousands of entities under frameworks such as the Corporate Sustainability Reporting Directive and the EU Emissions Trading System. As of the latest available annual data (2023 preliminary estimates), the EU (EU27) emitted approximately 3.22 billion metric tons of greenhouse gases (Gt CO2eq) according to the European Commission's EDGAR report, with the power industry, industrial processes, and manufacturing being major sectors for emissions. The International Energy Agency emphasises that accurate emissions accounting is a prerequisite for credible net-zero pathways, and the European Commission’s Green Deal Industrial Plan further tie access to state aid to verified decarbonization progress. Unlike generic environmental software, carbon footprint management solutions in Europe integrate real-time utility data, logistics records, procurement databases and supplier declarations to generate audit-ready reports aligned with the European Sustainability Reporting Standards. This granular compliance imperative, combined with investor and consumer pressure, has transformed carbon accounting from a peripheral ESG task into a core enterprise capability.

MARKET DRIVERS

Mandatory Sustainability Disclosure Drives Enterprise Adoption

The European Union’s binding regulatory mandates for emissions reporting have encouraged the growth of the European carbon footprint management market. The Corporate Sustainability Reporting Directive became applicable from January 2024 for a specific wave of large companies (those already subject to the NFRD), with reporting in 2025. It applies to listed SMEs from January 2026 (for the 2026 financial year, reporting in 2027). According to the European Commission, this regulation directly affects over 50,000 companies operating in the EU, including subsidiaries of European multinationals. Non-compliance carries significant financial and reputational risk. Apart from these, the EU Taxonomy Regulation mandates that financial market participants classify economic activities based on their alignment with climate objectives, requiring portfolio-level emissions calculations. These overlapping requirements create a structural need for robust digital platforms that automate data collection, ensure audit trails, and align with evolving standards. Consequently, enterprises prioritise carbon footprint management not as a sustainability initiative but as a legal and financial compliance necessity.

Investor and Financial Market Pressure Amplifies Corporate Accountability

The integration of climate risk into financial decision-making has intensified corporate demand, which in turn boosts the expansion of the European carbon footprint management market. The European Central Bank’s 2024 Climate Risk Stress Test revealed that 72 per cent of euro area companies are at risk of ecosystem degradation. Similarly, the Sustainable Finance Disclosure Regulation requires financial products promoting environmental or social characteristics (Article 8) or those with explicit sustainable investment objectives (Article 9) to disclose how these objectives are met using specific sustainability indicators, which can include quantified environmental metrics such as carbon intensity. Institutional investors are also acting collectively. Failure to provide reliable scope three data can result in exclusion from major indices such as the STOXX Europe 600 ESG. This financial ecosystem ensures that carbon footprint management is no longer optional but a prerequisite for capital access, market valuation, and stakeholder trust across the European economic landscape.

MARKET RESTRAINTS

Fragmented Data Sources Impede Accurate Emissions Accounting

The lack of standardised and accessible emissions data across complex global supply chains remains an important barrier to the European carbon footprint management market. Scope three emissions, which encompass purchased goods, services, logistics and upstream raw materials, often constitute 70 to 95 per cent of a company’s total footprint yet rely on supplier self-reporting that is frequently inconsistent or absent. The absence of a universal product-level emissions database forces companies to rely on industry-average proxies. Furthermore, internal data silos between procurement, logistics and energy management systems prevent automated aggregation. Universal adoption and enforcement of interoperable data standards (such as the Product Environmental Footprint method) are essential to prevent data fragmentation from affecting the accuracy and credibility of corporate carbon disclosures.

Shortage of Skilled Personnel Limits Effective Implementation

The scarcity of professionals with combined expertise in environmental science, data engineering, and regulatory compliance constrains its effective deployment, which negatively impacts Europe's carbon footprint management. Software handles automated calculations; however, critical functions like data validation, target setting, and interpreting results depend on specialised skills that are currently at a premium. Universities have been slow to develop curricula that blend life cycle assessment with data science. Consequently, many companies rely on external consultants, creating bottlenecks and escalating costs. This human capital deficit not only delays compliance but also increases the risk of methodological errors and greenwashing allegations, particularly as regulatory scrutiny intensifies under the Green Claims Directive.

MARKET OPPORTUNITIES

Integration with Enterprise Resource Planning Systems Unlocks Automation

Its deep integration with core enterprise systems, such as SAP,A Oracle Oracle and Microsoft Dynamics, offers a major opportunity for the European carbon footprint management market. This integration can pave the way for automated emissions tracking and embed sustainability into daily operations. When connected to procurement logistics and energy modules, these platforms can convert financial transactions into real-time emissions data using spend-based or activity-based methodologies. Companies have already implemented such integrations, enabling automatic carbon calculation for every purchase order or shipment. This operational embedding transforms carbon accounting from a periodic reporting exercise into a continuous decision support tool that informs sourcing,, choice and energy procurement. The progression of digital transformation means this synergy will serve as the crucial foundation for effective, scalable, and auditable emissions management in Europe's industrial sector.

Emergence of Verified Carbon Labelling Drives Consumer Demand

The rollout of certified carbon footprint labels on consumer products is creating a powerful market-based incentive for companies to adopt robust systems, which generates potential prospects for the expansion of the European carbon footprint management market. According to sources, a portion of EU shoppers say they would choose a lower carbon product if clearly labelled, even at a price premium. Retail giants have mandated carbon declarations from suppliers for thousands of SKUs, with non-compliant products facing delisting. In March 2024, the EU adopted the Directive on Empowering Consumers for the Green Transition (EU 2024/825), which prohibits a range of misleading environmental claims and self-made labels, and must be transposed into national law by Member States by March 2026. This regulatory consumer and retail convergence creates a direct commercial benefit for companies that can accurately measure and reduce product-level emissions. Carbon footprint management platforms that support granular life cycle assessments and third-party audit trails are thus becoming essential for market access and brand competitiveness across Europe.

MARKET CHALLENGES

Lack of Harmonised Methodologies Across Jurisdictions

The absence of globally aligned standards for calculating and reporting emissions creates compliance complexity and data inconsistency for multinational companies operating in the region, and this impedes the growth of the European carbon footprint management market. The European Sustainability Reporting Standards establish a regional framework that differs from other major systems, including the US Securities and Exchange Commission’s climate disclosure rules and the International Sustainability Standards Board’s global baseline. Even within Europe, methodological gaps persist. The Product Environmental Footprint rules differ from the Corporate Sustainability Reporting Directive in the treatment of biogenic carbon and allocation rules for co-products. Maintaining parallel reporting systems is a necessary burden for companies until true global harmonisation is established. This reality erodes stakeholder confidence in the reported data and undermines efficiency.

Risk of Greenwashing Affects Market Credibility

The proliferation of unsubstantiated or poorly verified environmental claims poses a systemic threat to the expansion of the European carbon footprint management market. Despite regulatory advances, many companies continue to rely on incomplete data, an outdated emission factor, rs selective scope reporting to present an artificially favourable profile. As per sources, a share of green claims related to carbon neutrality lacked sufficient evidence or clear boundaries. This erodes trust among investors, consumers and regulators and increases legal exposure under the Green Claims Directive. The reputational fallout can be severe. Consequently, credible carbon footprint management requires not only accurate data but transparent documentation, audit readiness and conservative boundary setting. However, the absence of mandatory third-party assurance for most disclosures allows low-quality practices to persist, creating a two-tier market where rigour is penalised by complexity and cost, while superficial compliance remains prevalent. This credibility gap must be closed to ensure the market fulfils its role in genuine decarbonization.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 10.95% |

| Segments Covered | By Deployment, Type, End Use, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Ecova, ProcessMAP, Engie SA, Wolters Kluwer NV, IsoMetrix, Dakota Software, SAP SE, International Business Machines Corp (IBM), and Schneider Electric SE. |

SEGMENTAL ANALYSIS

By Deployment Insights

The cloud deployment segment accounted for a substantial share of the European market in 2024. The dominance of the cloud deployment segment is primarily driven by the need for scalability, real-time data integration, and regulatory agility across complex multinational operations. Cloud platforms enable seamless connection to disparate data sources, including utility APIs, logistics, telematics and ERP systems, allowing companies to update emissions calculations dynamically as operational data flows in. A further factor is the rapid evolution of EU sustainability regulations. In contraston-premisessse systems require costly internal IT resources for manual updates. Besides, the subscription-based pricing model reduces upfront capital expenditure, making advanced carbon accounting accessible to small and medium enterprises that constitute a portion of EU businesses as per Eurostat. This combination of operational flexibility, regulatory responsiveness, and financial accessibility solidifies cloud deployment as the default architecture for modern carbon management in Europe.

The cloud deployment segment is also predicted to witness the highest CAGR of 19.3% from 2025 to 2033. The rapid expansion of the cloud deployment segment can be attributed to the European Commission's push for digital sustainable finance, which involves policies mandating that all sustainability data used in financial products must be sourced from interoperable digital platforms that support machine-readable reporting, a requirement inherently fulfilled by cloud systems' standardised APIs. The rise of supply chain transparency laws, such as the Corporate Sustainability Due Diligence Directive, forces companies to collect emissions data from thousands of suppliers, many of whom lack internal systems. Cloud platforms offer supplier portals that automate data collection through secure web forms and spend-based estimation, reducing manual burden. These institutional and operational imperatives ensure cloud solutions remain at the forefront of Europe’s decarbonization infrastructure.

By End Use Insights

The manufacturing segment led the European carbon footprint management market and occupied a 37.9% share in 2024. The sector’s exceptionally high emissions intensity and regulatory exposure have mainly contributed to the growth of the manufacturing segment. Manufacturing accounts for a portion of the EU’s total greenhouse gas emissions, with heavy industries like steel, chemicals and cement facing legally binding decarbonization targets under the EU Emissions Trading System. Furthermore, the Corporate Sustainability Reporting Directive mandates comprehensive scope three disclosures covering raw material extraction logistics and product use, domains where manufacturing value chains are longest and most complex. Companies have already deployed enterprise-wide carbon accounting platforms to comply with these overlapping requirements and secure competitive advantage in low-carbon procurement tenders across the EU single market.

The IT and telecommunication segment is estimated to register the fastest CAGR of 22.1% during the forecast period. Dual pressures from digital decarbonization mandates and client-driven supply chain expectations are fuelling the expansion of the IT and telecommunication segment. Moreover, cloud providers and software firms face intense scrutiny from corporate clients. Furthermore, the EU’s Code of Conduct for Data Centre Energy Efficiency mandates annual carbon footprint submissions for signatory operators, which include Amazon Web Services, Microsoft Azure and Google Cloud. Companies are leveraging precise carbon tracking platforms to monitor emissions at a granular level (per server, user, and workload), which facilitates transparent reporting to customers. This regulatory and commercial convergence transforms carbon management from a back-office function into a core component of digital service delivery across Europe.

REGIONAL ANALYSIS

Germany Market Analysis

Germany outperformed other countries in the European carbon footprint management market and accounted for a 27.4% share in 2024. Its position as the continent’s industrial powerhouse and regulatory vanguard drives the domination of the German market. The country is home to thousands of manufacturing facilities classified as energy-intensive under EU law, all of which must comply with stringent emissions monitoring under the Federal Immission Control Act. Major industrial players have developed in-house carbon platforms that integrate with supplier networks across multiple countries. The presence of global software vendors further consolidates Germany’s role as the technological and compliance epicentre of European carbon management.

France Market Analysis

France remained the next most prominent player in the European carbon footprint market by capturing a 20.5% share in 2024. The growth of France is due to its pioneering regulatory frameworks and public sector leadership. According to research, France’s energy and climate legislation requires large enterprises to disclose their annual carbon footprints, with reporting obligations now extending to include indirect or scope three emissions. As per sources, the number of companies conducting verified carbon assessments in France continues to rise, reflecting growing corporate accountability and alignment with national climate transparency standards. Apart from these, France’s PACTE Act requires institutional investors to disclose climate alignment of portfolios, accelerating demforsfor asset-levelions data. The government also leads by example. This public sector leverage cascades through supply chains, compelling thousands of SMEs to adopt carbon accounting tools. Companies have emerged as domestic leaders offering French-language platforms aligned with national methodology. This blend of long-standing policy maturity and institutional procurement power sustains France’s central role in shaping Europe’s carbon transparency ecosystem.

United Kingdom Market Analysis

The United Kingdom grew steadily in the European carbon footprint management market by maintaining robust demand despite its departure from the EU through stringent domestic climate governance. As per sources, a majority of leading UK corporations are adopting third-party verified carbon accounting systems to enhance data credibility and maintain compliance with evolving audit and reporting requirements. Furthermore, British multinationals like Unilever and BP operate global supply chains that must comply with both UK and EU regulations, creating dual reporting needs that favour scalable software solutions. This regulatory continuity and corporate sophistication ensure the UK remains a critical node in Europe’s carbon accountability infrastructure.

Netherlands Market Analysis

The Netherlands is another key player in the European carbon footprint management market, with its role as Europe’s logistics hub and leader in circular economy policy. The Port of Rotterdam handles millions of shipping containers annually and requires all terminal operators to report emissions under the Green Port Program. Retail giants have pioneered product-level carbon labelling, requiring suppliers to input footprint data into shared platforms. The Dutch government also funds the Climate Intelligence Platform, which provides small businesses with free access to emission factor databases and calculation tools. This ecosystem of port authority mandates circular economy policy,cy and corporate leadership in sustainable sourcing creates a dense and interconnected demand base for carbon management solutions across trade and industry.

Sweden Market Analysis

Sweden is predicted to grow in the European carbon footprint management market over the forecast period, owing to its serving as a Nordic beacon for sustainability transparency and cross-border collaboration. The Swedish Environmental Protection Agency requires all companies listed on Nasdaq Stockholm to disclose climate data in line with the Taskforce on Climate-related Financial Disclosures and mandates that state-owned enterprises achieve net zero by 2030. Apart from these, Sweden co-leads the Nordic Carbon Disclosure Project, which harmonises emissions reporting across Denmark, Finland, Norway and Sweden, enabling regional comparability. Companies have extended these standards to global suppliers, requiring verified footprint data for all products sold in Europe. This combination of national ambition, regional coordination and corporate influence establishes Sweden as a high integrity market that sets de facto standards for transparency across Northern Europe.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the notable key players in the European carbon footprint management market are

- Ecova

- ProcessMAP

- Engie SA

- Wolters Kluwer NV

- IsoMetrix

- Dakota Software

- SAP SE

- International Business Machines Corp (IBM)

- Schneider Electric SE

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the European carbon footprint management market focus on deep integration with enterprise resource planning systems, regulatory alignment with EU sustainability standardsddevelopment of multilingual and multijurisdictional calculation engines, strategic partnerships with national agencies and auditors and targeted product development for small and medium enterprises. Companies invest heavily in real-time data connectivity to utility logistics and procurement systems to automate scope one, two, and three calculations. They actively participate in EU technical working groups to influence standard-setting and ensure platform compatibility. Cloud native architecture enables rapid deployment of compliance updates across client bases. Additionally, vendors offer subsidised or freemium tiers for SMEs to expand market reach and build ecosystem lock-in. Certification alliances with accredited verifiers further enhance credibility and reduce client risk under the Green Claims Directive.

COMPETITION OVERVIEW

Competition in the European carbon footprint management market is defined by a dual dynamic between global enterprise software giants and agile European specialists. Large vendors like SAP and Oracle leverage their embedded position in corporate IT infrastructure to offer integrated sustainability modules that reduce implementation friction for multinational clients. In contrast, regional innovators such as Sweep Normative and Plan A focus on user-centric design, regulatory specificity and rapid adaptation to evolving EU standards like the Corporate Sustainability Reporting Directive and Green Claims Directive. The market is highly fragmented, with over 120 active software providers, but consolidation is accelerating as compliance complexity raises entry barriers. Differentiation hinges on data granularity, methodology, transparency and audit readiness and support for scope three supply chain engagement. While price competition exists among budget tools, enterprise buyers prioritise regulatory certainty and interoperability over cost. The absence of mandated software certification allows varied quality, but upcoming EU verification requirements under the Green Claims Directive will likely favour established players with third-party validation partnerships and robust audit trails.

TOP PLAYERS IN THE MARKET

- SAP SE is a German multinational that plays a pivotal role in the European carbon footprint management market through its integrated sustainability solutions embedded within enterprise resource planning systems. The company’s Sustainability Control Tower and Green Ledger modules enable real-time emissions tracking across finance, procurement, and logistics functions for thousands of European enterprises. SAP actively aligns its platforms with the European Sustainability Reporting Standards and the Corporate Sustainability Reporting Directive, ensuring regulatory readiness. The initiatives position SAP as a critical infrastructure provider that embeds carbon accountability into core business operations across the continent and globally.

- Schneider Electric SE is a French energy management and automation leader that delivers comprehensive carbon footprint management solutions through its EcoStruxure Resource Advisor and AVEVA platforms. The company serves industrial utilities and commercial real estate sectors across Europe with tools that integrate utility data, building management systems, and supply chain records to generate verified emissions reports. Schneider Electric actively participates in shaping EU policy as a member of the Corporate Sustainability Reporting Directive technical working group. Apart from these, Schneider partners with national energy agencies in France, Germany and the Netherlands to offer subsidised software access to small and medium enterprises. This combination of technical leadership, policy engagement, and inclusive deployment strengthens its influence across European decarbonization efforts.

- Sweep SA is a French software innovator specialising in user-friendly carbon accounting platforms designed specifically for European regulatory compliance. The company’s cloud-based solution automates data collection from ERPs, utility bills, and supplier invoices while applying European Sustainability Reporting Standards and Product Environmental Footprint rules. Sweep has gained traction among mid-sized enterprises and public sector organisations seeking audit-ready reporting without extensive IT integration. The company also established a certification partnership with Bureau Veritas to provide pre-verified reports aligned with the EU Green Claims Directive. These regionally attuned features enable Sweep to address the nuanced compliance needs of diverse European markets with precision and speed.

MARKET SEGMENTATION

This research report on the European carbon footprint management market has been segmented and sub-segmented based on categories.

By Deployment

- On-premise

- Cloud

By Type

- Heating Systems

- Ventilation Systems

- Cooling Systems

- Humidifiers & Dehumidifiers

- Integrated Carbon footprint management

By End Use

- Energy & Utilities

- Manufacturing

- Transportation

- IT & Telecommunication

- Residential

- Commercial

- Industrial

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is carbon footprint management?

Carbon footprint management refers to measuring, monitoring, and reducing greenhouse gas (GHG) emissions from business operations, supply chains, and products.

2. Which industries in Europe are adopting carbon footprint management solutions the most?

Energy & utilities, manufacturing, transportation, and IT & telecommunication sectors are the major adopters in Europe.

3. What are the main objectives of carbon footprint management?

The key objectives include minimizing emissions, improving sustainability, ensuring regulatory compliance, and enhancing brand reputation.

4. Which technologies are commonly used in carbon footprint management?

Technologies such as IoT, AI-driven analytics, blockchain, and cloud-based emission tracking platforms are widely used.

5. What are the key components of a carbon footprint management system?

Major components include data collection tools, emission calculation software, reporting dashboards, and reduction strategy modules.

6. How does carbon footprint management benefit organizations?

It helps organizations reduce operational costs, achieve ESG goals, and maintain compliance with EU sustainability regulations.

7. Who are the key end users of carbon footprint management solutions in Europe?

Large enterprises in manufacturing, energy, transportation, and telecom sectors are the primary users.

8. What role do digital innovations play in improving carbon footprint management?

Digital tools like AI, machine learning, and IoT sensors enable real-time emission monitoring and predictive sustainability insights.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com