- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

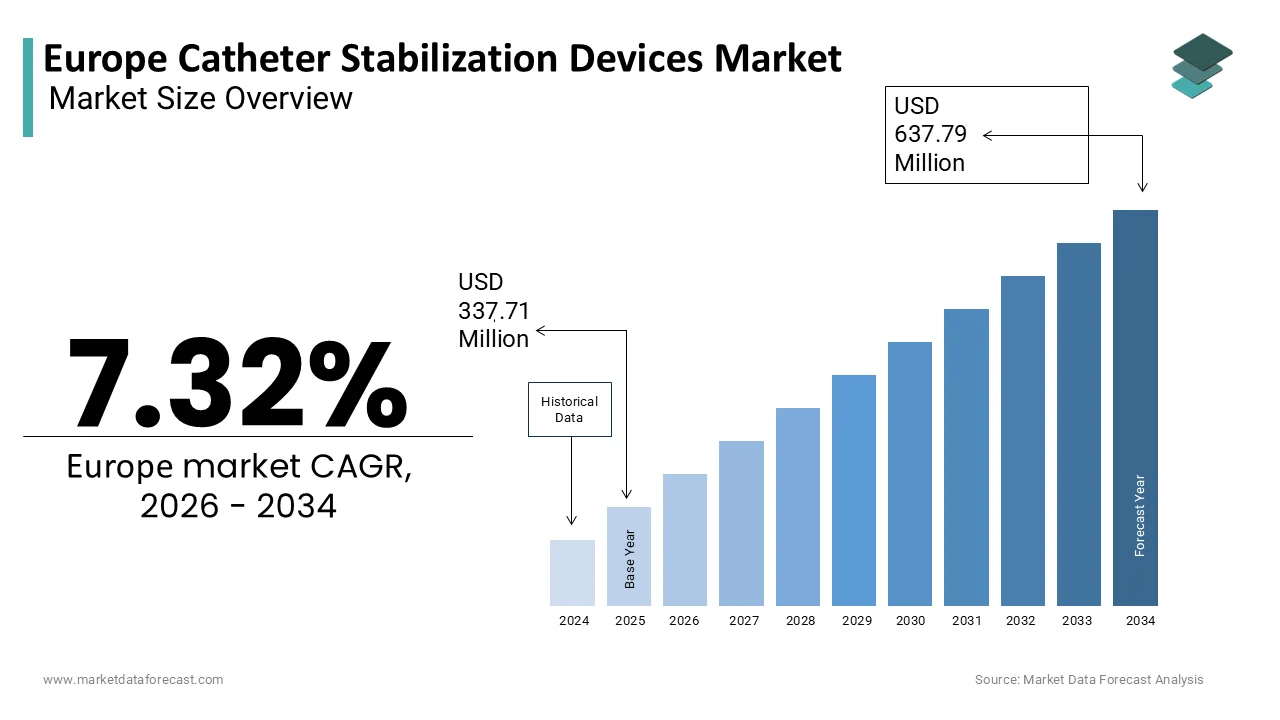

Market Size, 2025

$337.71 MnMarket Estimate, 2026

$362.44 MnMarket Forecast, 2034

$637.79 MnCAGR, 2026–2034

7.32%Europe Catheter Stabilization Devices Market Size

The Europe Catheter Stabilization Devices Market is projected to grow from USD 337.71 million in 2025 to USD 362.44 million in 2026 and reach USD 637.79 million by 2034, registering a CAGR of 7.32% during the forecast period from 2026 to 2034.

Catheter stabilization devices are specialized medical tools designed to secure indwelling catheters, minimizing the risks of accidental dislodgement, migration, or infection. In Europe, these devices play a pivotal role in critical care, surgical settings, and long-term patient management where maintaining catheter integrity is essential for both clinical outcomes and patient safety. The advanced healthcare infrastructure of Europe, combined with a strong emphasis on infection control protocols, is fuelling the adoption of such devices across hospitals, ambulatory surgical centers, and home care environments. According to the European Centre for Disease Prevention and Control (ECDC), millions of patients in the European Union contract healthcare-associated infections each year, with intravascular catheter-related bloodstream infections representing a significant component of this burden. Meanwhile, the population aged 65 and over in the EU was approximately 21.6 % of the total as of early 2025, which indicates a growing demand for complex venous access and associated stabilization solutions. Regulatory frameworks such as the European Medicines Agency’s medical-device regulation also emphasize device-related safety improvements, which are further shaping the clinical and regulatory landscape for catheter-stabilization technologies.

MARKET DRIVERS

Rising Incidence of Catheter-Related Bloodstream Infections Drives Adoption

The persistent burden of catheter-related bloodstream infections across European healthcare facilities acts as a primary catalyst for catheter stabilization device utilization, which is primarily driving the European catheter stabilization devices market growth. These infections not only jeopardize patient safety but also lead to prolonged hospital stays, increased treatment costs, and elevated mortality rates. According to the European Centre for Disease Prevention and Control, device-associated bloodstream infections in intensive-care units occur at rates of approximately 4 episodes per pe1,00000 central-line (catheter) days in EU/EEA hospitals. Economic analyses in Europe estimate that each episode of catheter-related bloodstream infection adds on the order of €13,000–30,000 to hospital costs. In response, many healthcare institutions have implemented evidence-based infection-prevention bundles that include securement and stabilization of intravascular catheters alongside aseptic insertion and maintenance. As per the sources, an increased awareness was noticed about the importance of minimizing catheter movement and securing the device to reduce microbial ingress and infection risk. National bodies in several countries have incorporated catheter-securement protocols into broader hospital-hygiene guidelines. These systemic shifts reflect a growing recognition in Europe that catheter stabilization is not simply a procedural convenience but a clinical necessity in mitigating iatrogenic infection risk and aligning with global patient-safety imperatives.

Growing Geriatric Population Fuels Demand for Secure Vascular Access

The rapidly expanding elderly population in Europe is significantly increasing the need for reliable and durable vascular access solutions, which in turn elevates demand for catheter stabilization devices and boosts the regional market expansion. Older adults often present with multiple comorbidities such as cardiovascular disease, diabetes, and chronic kidney disease, which require frequent intravenous therapy and long-term catheterization. According to Eurostat data, roughly 1 in 5 residents of the European Union is aged 65 years or over, which indicates the demographic shift toward an older population. Elderly patients are more prone to fragile skin, reduced mobility, and cognitive impairments that heighten the risk of accidental catheter dislodgement. According to research literature, engineered catheter-securement devices can reduce the incidence of unplanned catheter removal compared with standard adhesive dressings, particularly in high-risk populations. Additionally, chronic disease programmes in Europe involve large cohorts of patients requiring long-term venous access, many of whom use tunnelled central venous catheters. Given the age-related decline in skin integrity, reliance on standard tapes is increasingly challenged, and many providers are adopting purpose-built stabilization platforms that accommodate the physiological changes of older patients.

MARKET RESTRAINTS

Stringent Regulatory Requirements Pose Market Entry Barriers

The regulatory landscape governing medical devices in Europe has grown increasingly complex, particularly following the full implementation of the European Union Medical Device Regulation in 2021, which is hindering the regional market growth. Catheter stabilization devices classified as Class IIa or higher must now meet exhaustive clinical evidence, conformity assessment, and post-market surveillance obligations, which present formidable challenges, especially for small and medium-sized enterprises. According to documents published by the Medical Devices Coordination Group and the European Commission, capacity constraints among Notified Bodies are placing pressure on the certification process for medical devices under the MDR, particularly as many legacy devices transition from previous directives. Typical timelines for CE certification of devices subject to conformity assessment vary widely (often ranging from 9 to 24 months) and may lengthen further for novel or complex technologies. These extended regulatory timelines increase development costs, disrupt supply chains, and delay market access. Many manufacturers also cite resource-intensive requirements for comprehensive technical documentation, clinical evaluation, and post-market surveillance. The cumulative effect is a more challenging regulatory environment that may favour larger manufacturers with established regulatory infrastructure and thereby reduce competitive diversity and slow the pace of innovation in device categories such as catheter-stabilization systems across the region.

Limited Reimbursement Coverage Restricts Device Utilization

Despite clinical evidence supporting their efficacy, catheter stabilization devices face constrained adoption in several European healthcare systems due to inadequate or inconsistent reimbursement mechanisms, which are also impeding the growth of the European market. Unlike pharmaceuticals and high-risk implants, these devices are frequently categorized as disposable ancillary items and are not separately reimbursed under national diagnosis-related group or ambulatory payment classification systems. Several European countries currently lack dedicated reimbursement codes for engineered catheter-securement devices, which means these products are often bundled into broader procedural or ward cost pools. This financial ambiguity can discourage procurement departments from investing in higher-cost solutions even when they demonstrate long-term savings through infection prevention. In some national settings where healthcare budgets are tightly controlled, hospital decision-makers report that reimbursement constraints rather than purely clinical considerations often determine whether advanced securement devices are adopted. In regions with lower per-capita health expenditure, budgetary pressures frequently lead hospitals to opt for low-cost alternatives such as adhesive tapes. The absence of robust health-technology assessment data specific to catheter-securement devices further complicates advocacy for dedicated funding. Consequently, this misalignment between clinical best practices and economic incentives may hamper equitable access to safer vascular-access care across Europe.

MARKET OPPORTUNITIES

Integration of Smart Monitoring Capabilities Presents Growth Potential

The convergence of catheter stabilization with digital health technologies offers a lucrative opportunity for market expansion in Europe. Next-generation devices embedded with sensors for real-time monitoring of catheter position, temperature, and moisture levels can alert clinicians to early signs of complications such as dislodgement or local infection. This aligns with the European Union’s Digital Transformation of Health and Care strategy, which encourages interoperable and preventive digital solutions. According to the European Health Telematics Observatory, hospitals in several major EU member states are advancing digital-maturity initiatives that include the adoption of connected medical devices. As per the research from leading academic institutions, sensor-integrated stabilization technologies can reduce catheter-related adverse events when compared with conventional methods. The European Institute of Innovation and Technology has also directed substantial support toward startups developing smart medical-device ecosystems, including platforms for catheter monitoring. Regulatory pathways are evolving as we, with recent European Commission guidance clarifying that software embedded in medical devices follows the same CE-marking framework as hardware. This regulatory clarity, together with rising clinician acceptance of data-driven decision-making, is creating a favourable environment for intelligent stabilization systems that enhance patient safety and operational efficiency across Europe’s increasingly digital healthcare infrastructure.

Expansion of Home Healthcare Services Creates New Demand Channels

The structural shift toward decentralized care models in Europe is opening promising opportunities for the European catheter stabilization devices market. Home-based infusion therapy and long-term catheter management are becoming increasingly prevalent due to the aging demographics, budget constraints, and patient preferences. According to sources, a substantial number of patients in the European Union now receive intravenous antibiotic therapy at home, and this trend is expected to grow in the coming years. These patients rely heavily on secure and user-friendly catheter stabilization solutions that ensure safety during ambulation and self-care. As per a recent study by a home-care providers’ organization, catheter dislodgement is among the most frequently cited causes of emergency readmissions in the home-infusion setting, which is prompting increased procurement of engineered securement devices. In countries with mature home-care infrastructures, such as Sweden and the Netherlands, stabilization protocols for vascular access in the home have already been incorporated into national home-infusion guidelines. Moreover, innovation partnerships in Europe have endorsed patient-centric medical-device solutions, including catheter-securement systems designed for ease of use by non-clinical caregivers. With many reimbursement models evolving to include home-care medical supplies, the shift of care delivery from hospital to community settings is driving demand for reliable, portable, and easy-to-apply stabilization technologies.

MARKET CHALLENGES

Clinician Resistance to Workflow Disruption Hinders Adoption

Despite demonstrated clinical benefits, the integration of advanced catheter stabilization devices into routine practice is often impeded by entrenched clinical workflows and practitioner inertia, which is one of the major challenges to the growth of the European market. Many European healthcare professionals, particularly in resource-constrained settings, continue to rely on traditional adhesive tapes or sutures, citing familiarity, speed, and perceived cost efficiency. As per a survey conducted across multiple hospitals in Southern and Eastern Europe, some nurses and physicians remain hesitant to adopt newer catheter-securement devices, often citing concerns about added application time and limited training exposure. In high-turnover environments such as emergency departments, where rapid vascular access is essential, staff may bypass engineered solutions to avoid perceived delays. Differences in professional education contribute to inconsistent adoption as well, since catheter-securement protocols are not uniformly emphasized in nursing or medical training across Europe. Nursing organizations have noted that only a portion of EU member states include structured vascular-access management content within national certification pathways, which perpetuates variability in practice and affects perceptions of the need for advanced devices. Even in countries with well-developed infection-control policies, observational studies have documented protocol deviations when workload pressures increase. Addressing these challenges requires not only simplified product designs but also targeted change-management efforts that align clinical incentives with patient-safety goals through simulation-based training and real-time performance feedback.

Material Biocompatibility and Skin Sensitivity Concerns Limit Product Acceptance

Adverse skin reactions to adhesives and materials used in catheter stabilization devices represent a persistent clinical and commercial challenge across Europe, which is further inhibiting the expansion of the European catheter stabilization devices market. Patients, particularly neonates, the elderly, and those with chronic conditions, often exhibit increased skin sensitivity that results in complications such as contact dermatitis, blistering, and skin tears upon device removal. According to a 2025 systematic review published in J Tissue Viability, medical-adhesive related skin injuries occur in approximately 16% of adult inpatients, with cohort studies reporting incidence rates of up to 25%. These events not only cause patient discomfort but also increase infection risk and nursing workload. Regulatory scrutiny has intensified under the updated Medical Device Regulation, which mandates rigorous biocompatibility testing per ISO 10993 standard, yet material innovation remains slow due to the high cost of clinical validation. Moreover, the diversity of European skin types and environmental conditions complicates universal product design, as formulations effective in Northern Europe may underperform in Mediterranean climates with higher humidity and perspiration rates. According to an observational study published in the International Journal of Environmental Research and Public Health, a 36.4% rate of adhesive-related skin injury among postoperative adults, which indicates the clinical relevance of material choice; however, advanced alternatives such as hydrocolloid-based securement devices remain significantly more expensive, limiting their adoption in cost-sensitive settings.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Application, Product, End User and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Medtronic plc (U.S.), C. R. Bard, Inc. (U.S.), Centurion Medical Products (U.S.), Smiths Group plc (U.K.), Baxter International, Inc. (U.S.), B. Braun Melsungen AG (Germany), ConvaTec Inc. (U.S.), Merit Medical Systems, Inc. (U.S.), 3M Company (U.S.), M.C. Johnson Company, Inc. (U.S.). |

SEGMENTAL ANALYSIS

By Application Insights

The cardiovascular segment dominated the market by holding 31.8% of the regional market share in 2025. The dominance of the cardiovascular segment in the European market is driven by the high volume of cardiac interventions and chronic cardiovascular disease burden across the region. According to European Society of Cardiology data, cardiovascular diseases account for approximately 37.4% of all deaths across ESC member countries. These conditions include ischemic heart disease, which causes around 1.7 million deaths per year in Europe. Such procedures often necessitate secure central venous or arterial catheter access for hemodynamic monitoring, contrast administration, and postoperative care. According to Eurostat, diseases of the circulatory system (including cardiovascular diseases) were responsible for about 32.7% of all deaths in the EU in 2022. This persistent clinical demand drives hospitals to adopt advanced securement platforms that aim to minimize movement-related complications during prolonged catheterization. In intensive care units, where central venous catheter use is common, providers prioritize securement to prevent life-threatening thrombosis or dislodgement. Moreover, innovations such as radiopaque securement hubs and antimicrobial-coated devices are gaining traction in cardiology suites, which is supporting procedural safety and compliance with infection-control guidelines issued by national health agencies.

The respiratory segment is predicted to experience a CAGR of 9.2% over the forecast period in the European catheter stabilization devices market. The rising prevalence of chronic obstructive pulmonary disease and the increased use of tracheostomy and endotracheal tubes in critical care are primarily driving the growth of the respiratory segment in the European market. According to the European Lung Foundation, COPD affects over 36 million people in Europe, making COPD one of the continent’s most prevalent chronic diseases. In acute-care settings, accidental extubation remains a critical safety issue. According to a multicentre study published in the European Respiratory Journal, unplanned extubation is associated with mortality rates ranging from 10% to 25%, which indicates the need for reliable airway-stabilization methods. Investment in respiratory-care infrastructure has accelerated in recent years as well. For instance, as per the European Observatory on Health Systems and Policies, several EU countries made substantial post-pandemic ICU-capacity investments as part of national resilience plans. Additionally, the European Resuscitation Council includes securement steps within its airway-management algorithms for emergency and intensive-care practice. Unlike other applications, respiratory catheters are highly mobile and subject to frequent patient repositioning, which makes mechanical stabilization essential. Manufacturers have responded with low-profile adhesive and engineered securement systems designed for contouring and moisture resistance that align with clinical needs and support market growth across Europe.

By Product Insights

The central venous catheter securement devices segment occupied 37.7% of the European market share in 2025 due to their critical role in high acuity care settings and alignment with institutional infection prevention mandates. These devices are indispensable in intensive care oncology and dialysis units where central lines remain in place for extended durations. According to the European Renal Association, a large number of patients in Europe receive hemodialysis each year, many of whom rely on central venous catheters that require reliable sstabilization Likewise, as per the European Society for Medical Oncology, millions of cancer patients are treated annually via implanted ports or central lines, which require securement to avoid complications such as catheter migration or bloodstream infection. The European Centre for Disease Prevention and Control has documented substantial morbidity and mortality associated with central line-associated bloodstream infections in Europe, which indicates clinical and regulatory urgency. Hospitals across countries, including Germany, the Netherlands, and Sweden, have adopted suture-free securement platforms as standard policy following guidelines from national infection-control bodies. These engineered devices significantly reduce catheter movement compared to tape-based methods, as demonstrated in European hospital trials. With central venous access remaining a cornerstone of modern hospital care, the dominance of the central venous catheter securement devices segment is likely to continue in the regional market throughout the forecast period.

The all-site devices segment is anticipated to progress at a CAGR of 10.3% over the forecast period in the European market, owing to their versatility, cost efficiency, and compatibility with evolving care models across diverse clinical environments. These universal platforms can secure multiple catheter types, including peripheral IV line, epidura, LS chest tube,bes, and urinary catheters, using a single product design, reducing inventory complexity and training burdens. According to procurement studies in Europe, a growing number of hospitals in countries such as Belgium, Poland, and Portugal report transitioning to site-wide device-standardization programmes to streamline supply-chain operations amid budget constraints. The shift is further amplified by the rise of short-stay surgical units, where patients receive multiple lines during brief admissions, which makes adaptable catheter-securement essential. As per a research project from a Scandinavian university, standardized securement devices reduced nursing application time compared to specification-specific products while achieving comparable safety outcomes. Additionally, the European Union’s Green Public Procurement criteria now favour reusable or multi-use medical products that minimize waste and packaging, further incentivizing adoption. With healthcare systems across Europe prioritizing operational agility and standardization, the catheter-securement segment is positioned for sustained growth beyond traditional product cycles.

By End User Insights

The hospitals segment captured the most significant share of the European market in 2025. The growth of the hospitals segment in the European market is driven by their role as primary sites for complex procedures, chronic disease management, and critical care. These institutions manage the vast majority of central line placements, surgical drains, and intensive monitoring catheters that require advanced securement. According to Eurostat, the European Union had around 2.3 million hospital beds available in 2023, with nearly three-quarters of those designated for curative (acute) care. Within acute-care hospitals, infection-control protocols endorsed by national agencies like Haute Autorité de Santé (France) and Ministero della Salute (Italy) often mandate the use of engineered securement for high-risk catheter access. Although specific procedural volumes for vascular or airway catheters are not publicly detailed in the surgical operations database, the scale of surgical care in the EU remains substantial. The concentration of specialized staff and reimbursement mechanisms, such as Germany’s DRG system, which includes device costs within procedure tariffs, further supports hospital-based adoption of securement devices. As hospitals continue to serve as the epicentres of advanced medical intervention, their dominance in the catheter-stabilization market remains structurally insulated from near-term disruption.

The home healthcare providers segment is estimated to record a prominent CAGR of 9.98% over the forecast period in the European catheter stabilization devices market. Home healthcare providers represent the fastest-growing end-user segment, fuelled by Europe’s strategic pivot toward community-based care and aging-in-place policies. According to the European Commission, a substantial proportion of the EU population receives formal or informal care at home with intravenous therapies, such as antibiotics, chemotherapy, and nutrition support, which is an increasing component of home-based healthcare. According to sources, home infusion services are expanding at a compound annual growth rate of around 8% in Europe, and several countries have developed national frameworks to support home-care integration. In this context, catheter securement is critical since many patients and caregivers lack clinical expertise to manage dislodgement and related risks safely. Home-care providers report that catheter complications contribute to hospital readmissions, which is prompting procurement of user-friendly securement systems with visual alignment and ease-of-use features. Additionally, reimbursement reforms in countries such as Austria and Denmark now explicitly cover home-medical supplies, including stabilization devices, within integrated care bundles. With patient preference, economic efficiency, and policy alignment converging, the home healthcare providers segment is expected to experience significant growth in this market during the forecast period.

COUNTRY LEVEL ANALYSIS

Germany Catheter Stabilization Devices Market Analysis

Germany stood as the largest national market for catheter stabilization devices in Europe and accounted for 23.1% of the regional market share in 2025. The dominance of Germany in the European market is driven by its advanced healthcare infrastructure, high procedural volume, and stringent infection control standards. Germany’s aging demographic, with approximately 22.8% of citizens being aged 65 and over, intensifies demand for long-term vascular access in both hospital and home care settings. The statutory health-insurance system of Germany that covers the vast majority of the population provides a strong reimbursement environment for medical devices that demonstrate patient safety and operational benefits. Hospitals and leading university centres in Germany have implemented standardized catheter‐securement protocols, which reflect strong clinical reliance on securement solutions amid high volumes of central venous access. Combined with a robust domestic med-tech manufacturing base, Germany exhibits structural advantages that sustain its leadership position in this device segment.

France Catheter Stabilization Devices Market Analysis

France occupied the second leading share of the European catheter stabilization market in 2025. The leading position of France in the European market is driven by centralized healthcare planning, high ICU utilization, and a strong focus on nosocomial infection reduction. According to Santé publique France, catheter-related infections account for approximately 30% of device-associated bacteremia in French acute-care hospitals. In response, national infection-prevention strategies mandate enhanced securement protocols for central lines in public hospitals. France also performs a very large number of cardiovascular and other interventional procedures each year, which drives demand for secure catheter access. France’s National Authority for Health has issued favourable evaluations of advanced securement platforms under its device-assessment framework, which is facilitating uptake in hospital settings. With a public-spending share approaching 80% of total health expenditure, reimbursement barriers are minimal. France’s systematic integration of device protocols into national clinical pathways supports consistent and scalable market growth for securement technologies.

United Kingdom Catheter Stabilization Devices Market Analysis

The United Kingdom is estimated to grow at a promising CAGR in the European market during the forecast period due to the evidence-based procurement policies and a strong emphasis on patient safety metrics. The UK’s National Health Service (NHS) manages millions of hospital admissions each year, with central-venous and arterial access widely used in oncology, rrenal al and critical-care services. The UK’s National Institute for Health and Care Excellence (NICE) recommends the use of suture-free or engineered catheter-securement devices as part of a device-audit pathway for percutaneous catheters. Hospitals and home-care services are increasingly adopting standardized securement systems to reduce dislodgement and infection risk. The UK’s post-Brexit regulatory framework under the Medicines and Healthcare products Regulatory Agency (MHRA) continues to streamline approvals of innovative medical devices while maintaining safety oversight. In tandem, the NHS Long-Term Plan’s emphasis on home-based care has expanded the role of stabilization devices in community settings. This dual hospital-and-home penetration supports the UK’s sustained relevance in the catheter-securement device market.

Italy Catheter Stabilization Devices Market Analysis

Italy is projected to hold a notable share of the European market during the forecast period, owing to the high burden of chronic diseases and a dense network of private and public hospitals. According to the Italian National Institute of Health, cardiovascular diseases remain the leading cause of mortality in Italy, accounting for about one-third of all deaths nationwide. Italy’s aging population is among Europe’s most pronounced, with 24.3% of residents aged 65 or older as reported by ISTAT in 2025, which is increasing reliance on long-term vascular access for medication and nutrition. Regional health authorities such as those in Lombardy and Emilia-Romagna have implemented infection-control bundles that include securement devices as mandatory components. Clinical audits in Italy have shown that hospitals adopting engineered stabilization systems report fewer catheter-related complications compared with those using conventional methods. Despite regional disparities in funding, the national Essential Levels of Care framework ensures baseline access to critical medical devices. Italy’s strong home-care tradition, which is supported by a large network of informal caregivers, further extends the use of user-friendly securement products into non-hospital environments.

Spain Catheter Stabilization Devices Market Analysis

Spain is expected to register a healthy CAGR in the European catheter stabilization market during the forecast period, owing to the healthcare modernization efforts and rising surgical activity. According to the 2023 Annual Report of the Spanish National Health System, the public health service carried out around 3.5 million surgical interventions nationwide. Spain’s National Health System provides virtually universal coverage, and device-based infection-prevention mechanisms have been progressively incorporated into hospital accreditation criteria. According to a Health Systems in Transition review, Spanish intensive-care services and vascular-access units are increasingly standardizing protocols for central-venous catheter use. The growing aging population of Spain intensifies demand for reliable catheter management in both institutional and home settings. Additionally, Spain hosts numerous regional and international training workshops in vascular access, drawing professionals from across Southern Europe and supporting best-practice adoption. These structural and educational dynamics position Spain as a resilient and expanding market within the European landscape.

COMPETITIVE LANDSCAPE

The competition in the European catheter stabilization devices market is characterized by the presence of established multinational corporations and specialized medical device firms vying for clinical adoption and institutional contracts. Companies differentiate themselves through technological advancements, material science expertise, and alignment with European infection control standards. The implementation of the EU Medical Device Regulation has raised entry barriers favouring players with robust regulatory infrastructure and clinical validation capabilities. Competition is particularly intense in Western Europe, where hospitals demand high-performance devices backed by outcome data. In contrast, Eastern European markets emphasize cost efficiency and ease of use, creating opportunities for value-oriented solutions. Strategic activities such as product launches, clinicianeducation, andd health technology assessment collaborations are common competitive levers. The market also sees growing emphasis on post-market surveillance and digital integration as differentiators. Overall, the landscape rewards innovation, regulatory agility, and deep clinical engagement.

KEY MARKET PLAYERS

Key players operating in the europe catheter stabilization devices market profiled in this report are

- Medtronic plc (U.S.)

- C. R. Bard, Inc. (U.S.)

- Centurion Medical Products (U.S.)

- Smiths Group plc (U.K.)

- Baxter International, Inc. (U.S.)

- B. Braun Melsungen AG (Germany)

- ConvaTec Inc. (U.S.)

- Merit Medical Systems, Inc. (U.S.)

- 3M Company (U.S.)

- M.C. Johnson Company, Inc. (U.S.).

TOP LEADING PLAYERS IN THE MARKET

- 3M Company maintains a prominent presence in the European catheter stabilization devices market through its advanced medical solutions portfolio, particularly its Tegaderm and StatLock product lines. The company integrates adhesive science with clinical insights to develop securement platforms that reduce infection risks and improve patient comfort. In recent years, 3M has expanded its portfolio by enhancing device compatibility with diverse catheter types and introducing skin-friendly formulations suitable for sensitive populations. The company collaborates closely with European healthcare institutions to align its innovations with regional infection control guidelines and regulatory expectations under the EU Medical Device Regulation. These initiatives reinforce 3M’s role as a trusted partner in vascular access safety across the continent.

- Braun SE leverages its deep roots in European healthcare to deliver integrated vascular access and catheter stabilization solutions that meet stringent clinical and safety standards. The company emphasizes closed system designs and antimicrobial technologies to minimize complications associated with catheter use. Recently, B. Braun has invested in digital training modules for clinicians across Germany, France, and Italy to promote best practices in catheter securement. Its R&D efforts focus on ergonomic device architectures that simplify application while ensuring long-term adhesion even in high-moisture environments. Through strategic engagement with national health authorities and professional societies, B. Braun continues to shape catheter management protocols across Europe.

- ConvaTec Group plc contributes to the European catheter stabilization devices market through its focus on skin health and advanced wound care technologies applied to securement solutions. The company’s products prioritize gentle adhesion and easy removal to prevent skin trauma, particularly in elderly and neonatal patients. In recent actions, ConvaTec has strengthened its distribution partnerships across Southern and Eastern Europe to broaden access to its stabilization platforms. It has also incorporated real-world evidence generation into its European market strategy, collaborating with hospitals to validate clinical outcomes and cost efficiency. These efforts position ConvaTec as a patient-centric innovator aligned with Europe’s evolving care delivery models.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Leading companies in the European catheter stabilization devices market employ several strategic approaches to reinforce their competitive standing. Product innovation remains central with firms investing in materials that enhance skin compatibility and reduce infection risks. Strategic collaborations with hospitals and clinical societies help align offerings with regional care protocols and regulatory standards. Companies also focus on expanding their distribution networks, especially in Eastern and Southern Europe, to capture emerging demand. Digital enablement through a clinician training platform and a real-world evidence program strengthens product adoption. Additionally, firms actively engage in regulatory preparedness to ensure compliance with the EU Medical Device Regulation, facilitating faster market access and trust building among healthcare providers.

MARKET SEGMENTATION

This research report on the europe catheter stabilization devices market has been segmented and sub-segmented into the following categories.

By Application

- Gastric And Oropharyngeal

- Radiology General Surgery

- Respiratory

- Cardiovascular

- Urological

- Other Applications

By Product

- Peripheral Securement Devices

- Abdominal Drainage Tubes Securement Devices

- Arterial Securement Devices

- Epidural Securement Devices

- Chest Drainage Tube Securement Devices

- Central Venous Catheter Securement Device

- All-Site Devices

By End User

- Hospitals

- Home Healthcare Providers

- Emergency Clinics

- Diagnostic Centres

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe