Europe Cell Fractionation Market Research Report By Product, Type Of Cell, End User & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, Size, Share, Trends & Growth Forecast (2026 to 2034)

Europe Cell Fractionation Market Summary

Europe cell fractionation market reached USD 0.92B in 2024, estimated at USD 1.02B in 2025, and projected to hit USD 2.28B by 2033 (CAGR 10.6%, 2025–2033), driven by precision-medicine adoption, biobank expansion, and organelle-targeted drug discovery workflows.

Market snapshot

2024 value: USD 0.92 billion

2025 (est): USD 1.02 billion

2033 forecast: USD 2.28 billion

CAGR (2025–2033): 10.6%

Quick growth drivers

- Precision medicine programs requiring nuclear/mitochondrial/organelle-level profiling.

- Expansion of academic & industrial biobanks shifting to organelle-specific sample storage.

- Rising use of fractionation in proteomics, metabolomics & spatial omics platforms.

- Drug developers investing in organelle-targeted therapeutics (mitochondrial/lysosomal).

- EU-wide R&D investment (223B EUR in 2023) strengthening molecular research ecosystems.

Principal restraints

- High operational complexity, reproducibility gaps & lack of harmonized EU protocols.

- Strict ethical and regulatory constraints (Clinical Trials Regulation, GDPR) limiting human-sample access.

- Variability from manual workflows leading to cross-contamination & inconsistent yields.

- Administrative delays for tissue approvals, especially in France & the UK.

High-value opportunities

- Growth of organelle-targeted drug discovery, requiring validated high-throughput fractionation workflows.

- Integration with spatial omics, cryo-EM, and AI-driven localization models.

- Commercial demand for CE-IVD–certified reagents for diagnostic development.

- Rising adoption of automation-friendly bead-based systems across pharma R&D.

Key operational challenges

- Skill shortages in density centrifugation, gradient design & organelle purity assessment.

- Managing endogenous enzyme contamination that distorts omics readouts.

- Large variability in human clinical samples (ischemia times, donor differences).

- Achieving scalable, reproducible workflows across decentralized research environments.

Fastest-growing segments (short)

- Bead-based isolation systems: 11.4% CAGR — automation-ready & pharma-driven demand.

- Biotechnology companies: 12.1% CAGR — driven by organelle-targeted therapeutics & outsourced fractionation.

- Microbial cell fractionation: 9.8% CAGR — bioeconomy & enzyme engineering programs.

Regional leadership & dynamics

Germany (22.3%) — leading center for subcellular research with Max Planck/Fraunhofer networks; strong biobanking footprint.

United Kingdom (17.2%) — major hub for organelle-based diagnostics, NHS Genomic Medicine Service, Crick Institute workflows.

France — national-scale fractionation infrastructure; high CE-IVD adoption across academic labs.

Rest of Europe — growing through EU-funded spatial omics, biobank expansion & workforce training programs.

What wins commercially (competitive edge)

- End-to-end validated kits with CE-IVD approval for diagnostics and clinical workflows.

- Automation-ready fractionation systems (magnetic beads, closed protocols).

- Strong collaborations with biobanks, academic cores & spatial omics consortia.

- High reproducibility reagents (stabilizers, buffers, inhibitors) designed for multi-center studies.

- Deep technical support hubs enabling protocol standardization.

Top strategic ask for executives

Accelerate standardized reagent development, expand EU manufacturing & regulatory compliance footprints, and integrate automation + spatial-omics compatibility—while building training partnerships to close Europe’s skills gap in organelle isolation.

Leading players (short)

Thermo Fisher Scientific · Merck KGaA · QIAGEN · Beckman Coulter · BD · Bio-Rad · Miltenyi Biotec · Roche · Qsonica

Europe Cell Fractionation Market Size

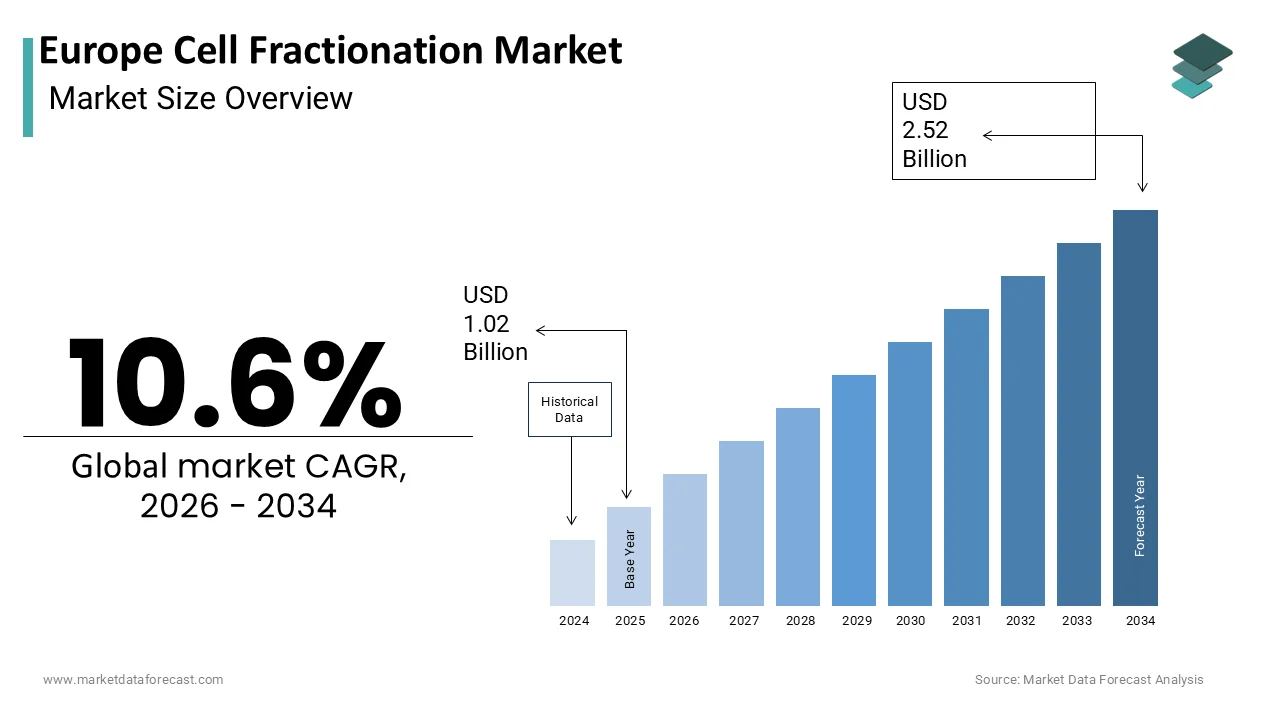

The Europe Cell Fractionation Market is projected to grow from USD 1.02 billion in 2025 to USD 1.13 billion in 2026 and reach USD 2.52 billion by 2034, registering a CAGR of 10.6% during the forecast period from 2026 to 2034.

The cell fractionation is the methodical separation of cellular components, such as nuclei,mitochondrii,, lysosomes,, and cytosol to facilitate detailed biochemical and functional analyses. The precision required in isolating subcellular structures underpins advancements in proteomics, metabolomics,cs,, and targeted drug delivery systems. Furthermore, European Union member states collectively invested 223 billion euros in research and experimental development in 2023, with life sciences accounting for nearly 28% of total expenditure. The persistent emphasis on molecular precision in diagnostics and therapeutics has reinforced demand for high-fidelity cell fractionation protocols across institutions like the Max Planck Society and the Francis Crick Institute. This foundational role in enabling mechanistic biological discovery positions cell fractionation not merely as a laboratory procedure but as a critical enabler of Europe’s scientific sovereignty in the post-pandemic era of biomedical innovation.

MARKET DRIVERS

Accelerated Adoption of Precision Medicine Frameworks Across European Healthcare Systems

The integration of precision medicine into national health strategies has significantly amplified the demand for reliable cell fractionation methodologies, which is driving the growth of the European cell fractionation market. Precision medicine relies on identifying molecular signatures within specific organelles or cellular compartments to guide therapeutic decisions. According to the Organisation for Economic Co-operation and Development, European countries'clinical trials focused onon organelle-specificc drug targets. The United Kingdom’s National Health Service has embedded organelle-based diagnostics into its Genomic Medicine Service, with over 120000 patients receiving mitochondrial DNA profiling in 2023 alone. Similarly, funded oncology studies in 2025required mitochondrial or nuclear fractionation for target validation. These institutional mandates create a sustained pull for standardized reproducible fractionation workflows. Moreover, the European Medicines Agency now recommends subcellular localization data for biologics approvall,, where relevant which further institutionalizes the technique across the regulatory pathway.

Expansion of Academic and Industrial Biobanking Infrastructure Requiring Subcellular Integrity Preservation

Europe’s strategic investment in biobanking has necessitated advanced cell fractionation protocols to maintain subcellular integrity for long-term storage and retrieval. The expansion of academic and industrial biobanking infrastructure requiring subcellular integrity is ascribed to bolstering the growth of the cell fractionation market. The Biobanking and Biomolecular Resources Research Infrastructure Europe now coordinates over 500 biobanks across 23 countries, housing more than 62 million biological samples as per its 2025operational report. The ecosystem is the shift from whole cell or tissue preservation totoward wardorganelle-specificc repositories. For example, the German Centre for Neurodegenerative Diseases maintains a mitochondrial biobank containing over 18000 enriched samples collected from post-mortem brain tissues. The academic biobanks plan to incorporate subcellular fractionation by 2026 to meet rising demand from proteomics consortia. Industrial players, including Novo Nordisk and Roche, have also established organelle-specific repositories to support biomarker validation pipelines, with Roche’s Basel facility alone processing over 24000 fractionated samples annually, as stated in its internal operational disclosure.

MARKET RESTRAINTS

High Operational Complexity Leading to Variable Reproducibility Across Laboratories

The cell fractionation remains technically demandingg,,g with reproducibility challenges that impede widespread standardization across European laboratories. The high operational complexity leading to variable reproducibility across laboratories significantly hampers the growth of the European cell fractionation market. The technique often requires precise control over centrifugation speed, temperature, and buffer composition, with even minor deviations leading to tcross-contaminationon between organelle fractions. According to a multicenter validation study conducted by the European Molecular Biology Laboratory in 2023, some participating institutions achieved consistent mitochondrial purity above 90% across replicate runs. This variability is exacerbated by the absence of universally accepted protocols. As per the European Committee for Standardization, no harmonized technical specification exists for organelle isolation despite repeated calls from the Innovative Medicines Initiative. Consequently, researchers frequently develop in-house methods, increasing validation costs and delaying cross-institutional collaboration. Moreover, the reliance on manual handling introduces operator-dependent biases, with junior technicians showing 22% lower yield consistency compared to senior staf,,as reported in a competency assessment by the European Federation of Biotechnology. These technical inefficiencies not only inflate operational costs but also undermine the reliability of downstream omics analyses, which depend on fraction purity.

Stringent Regulatory and Ethical Constraints Governing Human Tissue Utilization

The use of human biological materials is heavily circumscribed by evolving ethical and regulatory mandates that vary significantly across member states, which is additionally hampering the growth of the European cell fractionation market. The European Union’s Clinical Trials Regulation 536 2014, coupled with the General Data Protection RRegulation imposes rigorous consent and anonymization requirements for any human-derived sample. Only 11 of 27 EU countries had harmonized tissue donation frameworks that explicitly permit subcellular research, reducing cross-border sample sharing. In France, for example, tissue collection for organelle studies requires dual approval from both ethics committees and national biobank oversight bodies, leading to an average approval delay of 5.2 months. Similarly, the United Kingdom’s Human Tissue Authority recorded a 34% decline in approvfractionation-related applications between 2021 and 2023 due to stricter provenance tracking rules. These constraints disproportionately affect rare disease research, where sample scarcity is already critical. Althoug, the European Health Data Space aims to streamline access by 2026, current fragmentation continues to stifle innovationn particularly for startups lacking legal infrastructure to navigate jurisdictional variability.

MARKET OPPORTUNITIES

Rising Integration of oOrganelle-Targeteded Drug Discovery Platforms

The emergence of organelle-targeted therapeutics is certainly to create new opportunities for the growth of the European cell fractionation market. Pharmaceutical developers are increasingly designing molecules that localize to specific subcellular compartments, such as lysosomes,mitochondria,,or the endoplasmic reticulum, to enhance efficacy and reduce off-target effects. Companies like Sanofi and Bayer have established dedicated subcellular delivery units, with Sanofi’s Lyon facility conducting over 1500 fractionation assays monthly to validate mitochondrial accumulation of its antifibrotic compounds as per its 2025pipeline update. This shift is further reinforced by the Innovative Medicines Initiative’s Organelle Medicine Consortiumm which allocated 89 million euros in 2023 to develop develofractionation-baseded quality control benchmarks for organelle-targeted biologics. As these platforms mature, the demand for high-throughput fractionation, compatible with pharmacokinetic profiling, will iintensif,ytransforming the technique from a research tool into a regulatory necessity within drug development workflows across Europe.

Convergence with Advanced Imaging and Spatial Omics Technologies

The fusion of cell fractionation with spatially resolved omics asuper-resolutionion imaging, i,s unlocking new analytical dimensions that amplify its strategic relevance. The emergence of advanced imaging and spatial omics technologies is eventually to enhance the growth of the European cell fractionation market. Researchers increasingly couple fractionation outputs with techniques like cryo-electron tomography and spatial transcriptomics to map molecular distributions within organelles. As per the survey, over 68 core imaging facilities across Europe now offer integrated fractionation imaging pipelines,with demand growing by 27% annually since 2021. The Human Cell Atlas initiative, ve for instance relies on nuclear and cytosolic fractionation to deconvolute single-cell RNA sequencing data with the European branch processing over 12 million cells in 2024. Similarly, the EU-funded OrgAtlas project uses fractionation-derived organelle maps to train machine learning models that predict subcellular protein localization,, hieving 94% accuracy across 15 tissue types. Core facilities at institutions like Karolinska Institutet and EMBL Heidelberg now mandate fractionation as a prerequisite for spatial omics submissions, ensuring sustained utilization.

MARKET CHALLENGES

Persistent Shortage of Skilled Personnel Trained in Subcellular Isolation Techniques

The acute scarcity of laboratory professionals proficient in advanced organelle isolation methods is one of the challenging factors impeding the growth of the Europe cell fractionation market. Unlike standardized molecular biology workflows, fractionation demands nuanced expertise in density gradient design ,centrifugation physics, and organelle integrity assessment. According to the European Biotechnology Skills Observatory, some ofthe life science graduates in the European Union possess hands-on experience with differential centrifugation protocols as of 2024. This gap is particularly acute in Southern and Eastern Europe, where specialized training programs remain limited. Moreover, commercial vendors such as Thermo Fisher and Merck, over 40% of their technical support inquiries from European clients relate to protocol troubleshooting rather than equipment failur,,e indicating a deeper competency deficit. Although initiatives like the EU-funded BioTrain Project aim to accredit subcellular techniques within vocational curricula,, nationwide rollout remains fragmented.

Interference from Endogenous Contaminants Compromising Downstream Analytical Validity

The presence of endogenous proteases,, lipases and nucleases in crude cellular lysates poses a persistent analytical threat that undermines the reliability of fractionation outputs across European laboratories is an additional factor to degrade the growth of the Europe cell fractionation market. These enzymes remain active during homogenization and can degrade target organelles or modify their molecular cargo before separation is complete. This contamination skews results in sensitive applications such as metabolomics, where even trace enzymatic activity alters metabolite profiles. The problem is exacerbated in clinical sample,s which often arrive with variable ischemia times. While commercial inhibitor cocktails exi,st their efficacy varies by tissue type and species, limiting generalizability. Attempts to standardize quenching protocols under the EU’s METACELL initiative have yielded inconsistent results across multicenter trials.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Cell Type, End User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Beckman Coulter, Inc., Becton, Dickinson and Company, Bio-Rad Laboratories, Inc., Cell Signaling Technology, Inc., F. Hoffman-La Roche AG, Merck KGaA, Miltenyi Biotec, QIAGEN N.V., Qsonica, Thermo Fisher Scientific Inc. |

SEGMENTAL ANALYSIS

By Product Insights

The reagents segment accounted in holding 38.2% of the European cell fractionation market share in 2025 to their indispensable role in maintaining organelle integrity during isolation and enabling high specificity in downstream assays. Reagents,, including density gradient medi,,a protease inhibitor cocktail,,s and organelle stabilization buffers, are consumed in every fractionation workflow regardless of scale or cell type. Europe’s strategic commitment to molecular profiling has amplified reagent consumption. The EU-funded METACELL consortium alone procured 1.7 million euros worth of organelle isolation reagents in 2023 to support metabolic mapping across 12 disease models. The European Medicines Agency’s 2023 guidance on biomarker validation mandates the use of CE-marked reagents for any fractionation step involved in diagnostic development. This regulation has increased certified reagent adoption by 31% among biotech firms since 2022. Companies like Abcam and Qiagen have responded by expanding their CE IVD portfolios with oorganelle-specifickits, now accounting for over 40% of their European diagnostic reagent sales.

The beads segment is projected to grow atthea fastest CAGR of 11.4% from 2025 to 2033. Magnetic and affinity beads enable rapid organelle capture with minimal equipment dependency,, making them ideal fohigh-throughputut and automation-friendly workflows. Pharmaceutical companies are increasingly leveraging bead-based isolation for rapid organelle enrichment in early drug screening. According to the survey, 67% of new oncology screening platforms in Europe incorporated bead-mediated mitochondrial or lysosomal isolation to assess compound accumulation. Novartis’s Basel facility alone processed over 8500 bead-based fractionation runs in 2024, with a 42% increase from 2022.

By Cell Type Insights

The mammalian cells segment was the largest by holding a prominent share ofthe the Europe cell fractionation market in 2024, with human disease modeling and therapeutic developmen,t where mammalian systems provide physiologically relevant insights. Europe is a global leader ilarge-scalele human cell mapping, with the European branch of the Human Cell Atlas contributing over 40% of globalsingle-celll datasets as per its 2025coordination report. These initiatives rely heavily on fractionating primary human cells to deconvolute nuclear and cytoplasmic transcriptomes. For instance, the LifeTime Initiative withana EU Flagship project processed over 9.3 million humatissue-deriveded cells through fractionation workflows in 2025alone to study dynamic organelle responses in neurodegeneration and cancer. Contract research organizations like Charles River Laboratories have expanded their mammalian fractionation capacity by 50% since 2022 to meet this demand.

The microbial cell fractionation segment is projected to witness the fastest CAGR of 9.8% from 2025 to 2033. The European Commission’s 2023 Bioeconomy Strategy targets a reduction in fossil-based chemical production by 2030 through microbial cell factories. Companies like Novozymes and BASF use bacterial and yeast fractionation to optimize enzyme localization and secretion efficiency. According to the Bio-Based Industries Joint Undertaking, some industrial biotech projects funded between 2022 and 2025required subcellular analysis of microbial strains,, with average annualbead-basedd fractionation runs increasing. The European Centre for Disease Prevention and Control has prioritized bacterial organelle studies to combat antimicrobial resistance. Institutions like the Institute of Microbiology in Prague now run weekly fractionation workflows on clinical P. aeruginosa isolates to study resistance compartmentalization as documented in their annual research summary.

By End User Insights

The research laboratories segment was the largest by holding 54.1% of theEuropeane cell fractionation market share in 2024. Horizon Europe has designated subcellular dynamics as a cross-cutting priority with over 1.2 billion euros allocated to related projects between 2021 and 2024, as per the research. Institutions like the Max Planck Institute of Biochemistry and the Gurdon Institute receive multi-year grants specifically for organelle isolation infrastructure, with average annual fractionation consumable budgets exceeding 180000 euros. Countries like Sweden and Switzerland have invested heavily in centralized fractionation cores.

The biotechnology companies segment is anticipated to register the fastest CAGR of 12.1% from 2025 to 2033. European biotechs are pioneering therapies that require precise organelle delivery. For example, Oxford Biomedica uses mitochondrial fractionation to validate AAV vector localization in its Parkinson’s disease program,, processing over 600 runs monthly as per its 2025pipeline review. Companies like Mitotherapeutix in Germany raised 28 million euros in Series A funding in March 2025,, specifically for mitochondrial drug validation infrastructure. Biotechs increasingly outsource fractionation to specialized CDMOs. Catalent’s Brussels site launched a dedicated organelle analytics unit in November 2024, which now serves 34 biotech clients across Europe as stated in its service expansion press release. This ecosystem enables even early stage biotechs to access high end fractionation without capital investment accelerating market penetration.

COUNTRY LEVEL ANALYSIS

Germany Cell Fractionation Market Analysis

Germany was the largest contributor of the Europe cell fractionation market by occupying 22.3% of share in 2025with its unparalleled density of life science research institutions and industrial biopharma activity. The country hosts over 35 Fraunhofer and Max Planck institutes that routinely perform high volume fractionation alongside global players like Bayer and BioNTech. According to the German Federal Ministry of Education and Research public spending on subcellular research exceeded 480 million euros in 2024. Furthermore, Germany’s centralized biobanking network BioMaterialBank processes over 15000 fractionated clinical samples annually.

United Kingdom Cell Fractionation Market Analysis

The United Kingdom cell fractionation market held 17.2% of share in 2025with its world class academic infrastructure and advanced biotech cluster. The Francis Crick Institute alone performs over 12000 fractionation assays annually across its 150 research groups as documented in its 2025technical services report. The UK’s Life Sciences Vision allocated 260 million pounds in 2023 to organelle-based diagnostics with specific funding for mitochondrial biomarker validation in neurodegenerative diseases. NHS England’s Genomic Medicine Service processed 128000 patient samples through nuclear fractionation workflows in 2025to support whole genome sequencing, as confirmed by NHS Digital. Additionally, the UK’s Medicines and Healthcare products Regulatory Agency has streamlined approvals for fractionation based companion diagnostics reducing review timelines by 35% since 2022. This regulatory efficiency combined with strong translational research output from institutions like Oxford and Cambridge ensures the UK remains a dominant force in subcellular analysis.

France Cell Fractionation Market Analysis

France cell fractionation market growth is likely to be driven by the centralized national research strategy and strong public health integration. The French National Institute of Health and Medical Research operates 12 core fractionation facilities serving over 300 research teams with 89% annual utilization as per its 2025infrastructure audit. The French National Cancer Institute mandates organelle fractionation for all biomarker validation in its funded trials a policy that affected 41 studies in 2024. Furthermore, France’s early adoption of the EU’s In Vitro Diagnostic Regulation has accelerated CE marked reagent use with 73% of academic labs now exclusively using certified kits as reported by the French Society for Cell Biology.

TOP LEADING PLAYERS IN THE MARKET

- Thermo Fisher Scientific maintains a strong presence in the Europe cell fractionation market through its comprehensive portfolio of reagents instruments and consumables tailored for subcellular isolation. The company actively supports academic and industrial research by integrating fractionation workflows into its broader omics solutions. Thermo Fisher expanded its Pierce organelle isolation kits with CE IVD certification enabling use in diagnostic development across EU member states. It also launched a dedicated technical support hub in Berlin to accelerate protocol optimization for European clients. These initiatives reinforce its role as a strategic enabler of precision biology while enhancing compliance with regional regulatory expectations.

- Merck KGaA contributes significantly to the European cell fractionation landscape through its MilliporeSigma brand which offers a wide array of high purity reagents and magnetic bead based isolation systems. The company emphasizes reproducibility and scalability aligning with the demands of both research laboratories and biopharmaceutical developers. Merck introduced a new line of organelle stabilization buffers validated for cryopreserved human tissues addressing a critical gap in clinical biobanking. It also partnered with the Biobanking and Biomolecular Resources Research Infrastructure Europe to standardize fractionation protocols across 23 countries. This collaboration strengthens data interoperability and cements Merck’s influence in shaping best practices.

- Qiagen plays a pivotal role in advancing subcellular analysis in Europe through its proprietary sample preparation technologies and automated fractionation solutions. The company integrates cell fractionation into its molecular diagnostics and biomarker discovery platforms serving both academic institutions and biotech firms. Qiagen enhanced its Qproteome Mitochondria Isolation Kit with improved yield consistency across diverse tissue types based on feedback from European consortia. It also expanded its automated QIAcube Connect workflows to include organelle separation protocols reducing hands on time by 40%. These updates position Qiagen as a key facilitator of high throughput and standardized subcellular research across the region.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe cell fractionation market prioritize strategic product innovation through the development of standardized high-fidelity reagents and automation compatible workflows. They actively pursue regulatory alignment by obtaining CE IVD certifications to facilitate adoption in diagnostic settings. Collaborations with academic consortia and biobanking networks enable protocol harmonization and expand market reach. Companies invest in regional technical support infrastructure to accelerate user adoption and reduce implementation barriers. Additionally, they integrate fractionation technologies into broader omics and drug discovery platforms to enhance value proposition and lock in long term customer relationships across research and industrial segments.

COMPETITIVE LANDSCAPE

The Europe cell fractionation market features intense but focused competition among global life science leaders and specialized niche innovators. Dominant players leverage extensive distribution networks robust R and D pipelines and regulatory expertise to maintain technological leadership. They differentiate through workflow integration automation readiness and compliance with European standards such as CE IVD and GLP. Meanwhile emerging companies compete by offering novel bead chemistries or organelle-specific kits targeting high growth applications like mitochondrial therapeutics. Competitive intensity is amplified by Europe’s dense research ecosystem which demands both reproducibility and customization. Strategic partnerships with public research infrastructures further shape market dynamics as companies vie to embed their protocols into national and EU funded projects.

KEY MARKET PLAYERS

Companies playing a notable role in the europe cell fractionation market profiled in the report are

- Beckman Coulter, Inc.

- Becton, Dickinson and Company

- Bio-Rad Laboratories, Inc.

- Cell Signaling Technology, Inc.

- F. Hoffman-La Roche AG

- Merck KGaA

- Miltenyi Biotec

- QIAGEN N.V.

- Qsonica

- Thermo Fisher Scientific Inc.

MARKET SEGMENTATION

This research report has been segmented and sub-segmented the European cell fractionation market into the following categories.

By Product

-

Consumables

- Reagents

- Enzymes

- Detergent Solutions

- Beads

- Disposables

- Instruments

- Sonicator

- Homogenizer

By Cell Type

- Microbial

- Mammalian

By End User

- Research Laboratories

- Biopharmaceuticals

- Biotechnology Companies

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What drives growth in the Europe Cell Fractionation Market?

Strong biotechnology infrastructure, government R&D support, and rising demand for personalized therapies fuel the Europe Cell

Fractionation Market. Collaborations between research institutions and industry players enhance bioprocessing efficiency

2. Who are key players in the Europe Cell Fractionation Market?

Leading companies in the Europe Cell Fractionation Market include Thermo Fisher Scientific, Merck KGaA, Danaher, Bio-Rad Laboratories,

and Agilent Technologies, offering advanced instruments and reagents for cell separation applications.

3. What is the role of consumables in the Europe Cell Fractionation Market?

Consumables dominate the Europe Cell Fractionation Market due to widespread use in research and clinical settings for cell lysis and

fractionation. Innovations in specialized materials boost their adoption across biotech labs.

4. How does precision medicine impact the Europe Cell Fractionation Market?

Precision medicine drives the Europe Cell Fractionation Market by increasing needs for biomarker discovery and high-quality reagents

in personalized therapies, particularly in stem cell and regenerative research.

5. What are main applications in the Europe Cell Fractionation Market?

Key applications in the Europe Cell Fractionation Market include cancer research, stem cell studies, tissue regeneration, and biomolecule

isolation, supported by advanced sonicators and enzymes for cell disruption.

6. Which countries lead the Europe Cell Fractionation Market?

Germany, the UK, and France lead the Europe Cell Fractionation Market, benefiting from strong biotech hubs, R&D investments, and

focus on regenerative medicine and bioprocessing technologies.

7. What challenges face the Europe Cell Fractionation Market?

High costs of advanced instruments like sonicators and supply chain issues for specialized reagents challenge the Europe Cell

Fractionation Market, though innovations in scalability address these hurdles.

8. How do regulations affect the Europe Cell Fractionation Market?

EU regulations on biotech products and GMP standards shape the Europe Cell Fractionation Market, ensuring quality in reagents and

instruments while promoting sustainable bioprocessing practices.

9. Why is cell lysis key in the Europe Cell Fractionation Market?

Cell lysis techniques using enzymes and sonicators are central to the Europe Cell Fractionation Market, enabling effective disruption

for downstream applications in microbial and mammalian cell analysis.

10. How does biotech R&D influence the Europe Cell Fractionation Market?

Europe's biotech R&D boom, with funding for life sciences, significantly boosts the Cell Fractionation Market by demanding scalable

solutions for protein expression and biomarker studies.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com