Europe Clean Technology Market Size, Share, Trends, & Growth Forecast Report By Type (Renewable Energy Technologies, Energy Storage Solutions, Energy Storage Solutions, Water and Waste Management, Agriculture and Food Systems, Air and Environment Management), Application and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Clean Technology Market Size

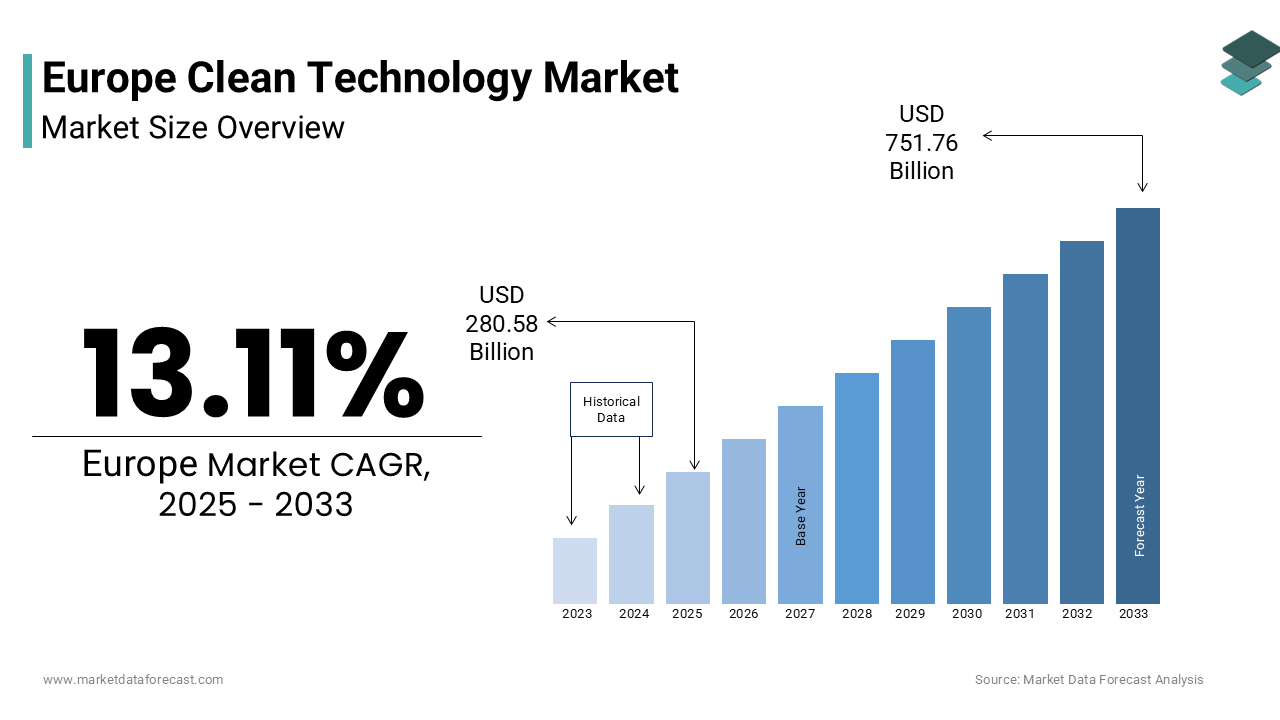

The europe clean technology market size was valued at USD 248.05 billion in 2024 and is anticipated to reach USD 280.58 billion in 2025 from USD 751.76 billion by 2033, growing at a CAGR of 13.11% during the forecast period from 2025 to 2033.

The clean technology, includes renewable energy systems, green hydrogen infrastructure, circular material solutions, sustainable water treatment, and carbon capture innovations. According to the European Environment Agency, the European Union emitted 3.4 billion metric tons of greenhouse gases in 2023, with the energy and industrial sectors accounting for over 60% of the total by creating urgent decarbonization pressure. Furthermore, the European Investment Bank reports that clean tech now accounts for 38% of all industrial innovation projects funded under Horizon Europe.

MARKET DRIVERS

Legally Binding Climate Targets Under the European Green Deal

The European Green Deal serves as the paramount driver of clean technology adoption across the continent by establishing enforceable decarbonization milestones and sector specific roadmaps. The rising legally binding climate targets is substantially leveraging the growth of Europe clean technology market. The Fit for 55 package mandates a 55% net reduction in greenhouse gas emissions by 2030 compared to 1990 levels with binding targets for renewable energy, energy efficiency, and carbon pricing. The Industrial Emissions Directive now compels over 50000 large installations to adopt Best Available Techniques, many of which involve clean tech retrofits such as electrified furnaces or solvent recovery systems. The Carbon Border Adjustment Mechanism further incentivizes domestic industry to decarbonize by imposing tariffs on carbon intensive imports from less regulated regions.

Rising Energy Security Imperatives Following Geopolitical Disruptions

The urgent need to reduce dependence on imported fossil fuels has accelerated clean technology deployment as a strategic pillar of energy sovereignty, which is additionally prompting the growth of Europe clean technology market. According to the International Energy Agency Europe imported 90% of its natural gas in 2021, with Russia supplying 45% prior to the Ukraine conflict. The REPowerEU Plan launched in 2022 aims to end reliance on Russian fossil fuels by 2027 and increase renewable energy to 45% of the EU’s energy mix by 2030. Countries like Denmark and Portugal now generate over 60% of their electricity from wind and solar, reducing exposure to volatile global markets.

MARKET RESTRAINTS

Complex and Fragmented Permitting Processes for Clean Infrastructure

The deployment of clean technology is significantly delayed by bureaucratic and inconsistent permitting procedures that vary widely between member states, which is degrading the growth of Europe clean technology market. According to the European Commission, the average approval time for onshore wind projects exceeds four years while solar farms face 24 to 36 month timelines due to environmental impact assessments and local opposition. In Germany, for instance over 15000 megawatts of renewable capacity were stuck in permitting queues as of early 2024 as reported by the German Energy Agency. The revised Renewable Energy Directive mandates that member states designate “go to areas” with pre-approved environmental and grid readiness by 2024 yet implementation remains uneven. In Italy and Spain local zoning laws and heritage protections frequently block projects even in designated zones.

Supply Chain Vulnerabilities for Critical Raw Materials

Europe’s clean technology sector faces acute supply chain risks due to heavy reliance on imported critical raw materials essential for solar panels batteries and electrolyzers. This factor is also hindering the growth of Europe clean technology market. According to the European Commission, the EU imports over 97% of its lithium 93% of its magnesium and 98% of its rare earth elements, with China dominating processing capacity. As per some reports, Europe will require 18 times more lithium and 5 times more cobalt by 2030 to meet its clean energy targets. While the Critical Raw Materials Act aims to diversify supply through international partnerships and domestic mining, only three lithium projects are operational in Europe as of 2024. Recycling infrastructure remains underdeveloped with less than 5% of lithium currently recovered from end of life batteries as per the Joint Research Centre.

MARKET OPPORTUNITIES

Integration of Clean Tech into Circular Economy Industrial Parks

Europe is pioneering the development of circular industrial ecosystems where clean technology enables closed loop resource flows across co located manufacturers. This factor is creating new opportunities for the growth of Europe clean technology market. The European Commission’s Circular Economy Action Plan supports over 50 industrial symbiosis parks where waste heat from steel plants powers district heating, CO2 from cement kilns feeds algae bioreactors, and scrap metals are remelted on site using green hydrogen. The Port of Rotterdam’s Brightlands Chemelot Campus integrates renewable hydrogen electrolyzers with chemical production creating a zero carbon feedstock chain. Similarly, Sweden’s H2 Green Steel facility uses 100% green hydrogen and recycled scrap to produce fossil free steel with 95% lower emissions. The Innovation Fund has allocated 4.2 billion euros to scale such integrated systems through 2027.

Export Potential of European Clean Tech Standards and Solutions

Europe’s stringent environmental regulations and technical standards are becoming global benchmarks, which is creating significant opportunities for the growth of Europe clean technology makret. The EU Taxonomy for Sustainable Activities and the upcoming Carbon Border Adjustment Mechanism are prompting countries from Canada to Japan to align their own frameworks with European criteria. According to the European External Action Service over 40 nations have adopted elements of the EU’s Green Deal in national legislation. As global decarbonization accelerates European clean tech firms benefit not only from domestic demand but from positioning as trusted providers of auditable, high integrity climate solutions in a world increasingly wary of greenwashing.

MARKET CHALLENGES

Workforce Skill Gaps in Emerging Clean Technology Sectors

The lack of skilled professionals capable of designing, installing, and maintaining advanced clean technology systems across renewable energy, hydrogen, and carbon management is a new challenge for the growth of Europe clean technology market. According to the European Commission’s Pact for Skills, over 1 million clean tech workers will be needed by 2030 yet current training pipelines produce fewer than 300000 annually. In the hydrogen sector the European Clean Hydrogen Alliance estimates a shortfall of 150000 technicians by 2035. Vocational education remains siloed in traditional engineering disciplines with limited curricula in electrolysis carbon capture or circular design.

Financing Gaps for Early Stage and Deep Tech Innovations

The persistent “valley of death” where promising deep tech innovations fail to secure growth capital for commercial scale up is also inhibiting the growth of Europe’s clean technology market. According to the survey, early stage clean tech startups receive only 22% of available venture capital compared to software and biotech. The average Series A round for European clean tech was 8 million euros in 2023 compared to 15 million in the United States, as per some report data. Capital intensity is a key barrier; scaling a novel carbon capture process can require over 100 million euros before first revenue. While the Innovation Fund provides grants it rarely covers operational scaling costs. Additionally private investors perceive clean tech as high risk due to long development cycles and regulatory uncertainty.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Type, Application & Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, and the Czech Republic. |

| Key Market Players | Siemens AG, Schneider Electric SE, ABB Ltd., Vestas Wind Systems A/S, Ørsted A/S, Nordex SE, Enel Green Power, Alstom SA, Veolia Environnement S.A., Iberdrola S.A., ENGIE SA, Rockwool International A/S, Kingspan Group, Neste Corporation, and Climeworks AG. |

SEGMENTAL ANALYSIS

By Type Insights

The renewable energy technologies segment held 52.3% of the Europe clean technology market share in 2024 with the binding legislative mandates and rapid grid integration of wind and solar power. The European Union’s Renewable Energy Directive sets a binding target of 42.5% renewable energy in the final energy mix by 2030, with many member states adopting even more ambitious national goals. The REPowerEU Plan has fast tracked permitting for renewable projects in designated “go to areas,” with the European Investment Bank financing over 25 billion euros in wind and solar infrastructure since 2022. Additionally, corporate power purchase agreements for renewables exceeded 15 gigawatts in 2023 across Europe according to SolarPower Europe, reflecting strong private sector demand.

The energy storage solutions segment is likely to grow with an anticipated CAGR of 24.7% throughout the forecast period owing to the increasing intermittency of renewable generation and the urgent need for grid stability as fossil fuel plants retire. As per the European Commission’s Net Zero Industry Act identifies electrochemical storage as a strategic net zero technology and targets 100 gigawatt hours of annual domestic manufacturing capacity by 2030. The Innovation Fund has allocated 1.8 billion euros to support next generation storage including solid state batteries and green hydrogen systems.

REGIONAL ANALYSIS

Germany Clean Technology Market Analysis

Germany was the largest contributor in the Europe clean technology market by holding 26.3% of share in 2024 with its Energiewende energy transition policy, industrial decarbonization mandates, and leadership in renewable manufacturing. The country’s industrial sector, which accounts for 22% of national emissions is undergoing deep transformation under the Carbon Contracts for Difference scheme that subsidizes green hydrogen and electrified processes. Companies like Siemens Energy and SMA Solar supply clean tech globally while domestic demand is amplified by the phase out of nuclear and coal by 2030 and 2038 respectively. The KfW Development Bank has disbursed over 40 billion euros in low interest loans for building efficiency and renewable retrofits since 2020.

France Clean Technology Market Analysis

France clean technology market was next by holding 19.2% of share in 2024 with its nuclear powered grid, state led industrial strategy, and focus on low carbon innovation. The France 2030 investment plan dedicates 30 billion euros to clean tech including 8 billion for green hydrogen, 4 billion for low carbon aircraft, and 3 billion for circular economy infrastructure. This clean baseload supports electrification of transport and industry while surplus power drives electrolysis. The country aims to install 100 gigawatts of solar and 50 gigawatts of wind by 2050 with accelerated permitting under the Renewable Acceleration Law of 2023. French champions like Orano and McPhy are scaling nuclear waste recycling and hydrogen electrolyzers for global export. France’s unique energy mix and centralized industrial policy position it as a leader in deep decarbonization technologies beyond variable renewables.

The United Kingdom Clean Technology Market Analysis

The United Kingdom clean technology market growth is likely to be driven by offshore wind leadership, carbon pricing maturity, and post Brexit regulatory autonomy. The UK Emissions Trading Scheme covers power industry and aviation with a 2024 allowance price of 85 pounds per ton, creating strong decarbonization incentives. In 2023, the UK added 3.2 gigawatt hours of grid scale battery storage with the highest in Europe and launched the Green Hydrogen Investment Scheme to support 10 gigawatts of electrolysis capacity by 2030. Companies like Octopus Energy and Zenobe are pioneering virtual power plants that aggregate distributed storage and EVs.

COMPETITIVE LANDSCAPE

Competition in the Europe clean technology market is characterized by a mix of industrial conglomerates specialized technology firms and state backed champions vying for dominance in a policy driven high stakes environment. German and Danish companies dominate wind and grid infrastructure while French and Swedish firms lead in nuclear enabled decarbonization and green steel. The market is highly capital intensive with competition centered on technological performance project financing capabilities and alignment with EU strategic autonomy goals. Unlike software markets where agility wins here scale integration and regulatory foresight determine success. Consolidation is accelerating as smaller innovators are acquired for niche capabilities in hydrogen carbon capture or battery chemistry. National industrial policies create uneven playing fields with local content requirements favoring domestic players yet European funding mechanisms like the Innovation Fund promote cross border collaboration.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Clean Technology Market include

- Siemens AG

- Schneider Electric SE

- ABB Ltd.

- Vestas Wind Systems A/S

- Ørsted A/S

- Nordex SE

- Enel Green Power

- Alstom SA

- Veolia Environnement S.A.

- Iberdrola S.A.

- ENGIE SA

- Rockwool International A/S

- Kingspan Group

- Neste Corporation

- Climeworks AG

Top Players in the Market

Siemens Energy AG

Siemens Energy AG is a cornerstone of the Europe clean technology market through its leadership in grid solutions, green hydrogen electrolyzers, and decarbonized power generation. The company supplies high voltage direct current transmission systems that integrate offshore wind farms into European grids and provides proton exchange membrane electrolyzers for industrial hydrogen projects. It also launched a digital twin platform for hybrid power plants that optimizes renewable and storage dispatch in real time. These initiatives reinforce Siemens Energy’s global role in enabling large scale energy transition while advancing Europe’s strategic autonomy in critical clean infrastructure.

Ørsted A/S

Ørsted A/S significantly shapes the Europe clean technology market as a global offshore wind developer that has transitioned from fossil fuels to 100% renewable energy generation. Headquartered in Denmark, the company operates over 13 gigawatts of offshore wind capacity in Europe and has pioneered integrated ecosystem approaches that combine wind farms with green hydrogen and power to X facilities. Ørsted also collaborates with coastal communities to enhance biodiversity around turbine foundations. Its vertically integrated model from development to offtake sets a global benchmark for sustainable energy infrastructure.

Vestas Wind Systems A/S

Vestas Wind Systems A/S plays a pivotal role in the Europe clean technology market through its advanced onshore and offshore wind turbine technology and circular design principles. The Danish company supplied over 30% of new offshore wind turbines installed in Europe in 2023 and leads in turbine recyclability with its Zero Waste Turbine initiative targeting 100% recyclable blades by 2030.

Top Strategies Used by the Key Market Participants

Key players in the Europe clean technology market prioritize vertical integration by controlling value chains from technology development to project operation and offtake agreements. They actively align with European Union strategic frameworks such as the Net Zero Industry Act and Critical Raw Materials Act to secure funding and policy support. Companies invest heavily in circular design principles including recyclable components and modular architecture to meet upcoming EU sustainability requirements. Strategic partnerships with energy utilities industrial off takers and research institutions accelerate technology validation and scale up. Additionally, they expand manufacturing capacity within Europe to reduce supply chain risks and comply with local content rules emerging under the Green Deal Industrial Plan.

MARKET SEGMENTATION

The research report on the Europe clean technology market has been segmented and sub-segmented based on categories.

By Type

- Renewable Energy Technologies

- Energy Storage Solutions

- Energy Storage Solutions

- Water and Waste Management

- Agriculture and Food Systems

- Air and Environment Management

By Application

- Residential

- Commercial

- Industrial

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe Clean Technology Market?

The Europe Clean Technology Market includes technologies that reduce environmental impact, such as renewable energy, energy efficiency systems, waste management solutions, and carbon capture technologies. It focuses on achieving sustainability and reducing carbon emissions across industries.

What drives the growth of the Europe Clean Technology Market?

The Europe Clean Technology Market is driven by strict EU environmental regulations, decarbonization goals, and rising investments in renewable energy. Consumer demand for sustainable products also plays a significant role.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com