Europe Commercial Telematics Market Size, Share, Trends & Growth Forecast Report, Segmented By Type, System Type, Provider Type, End-User And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2026 to 2034)

Market Size, 2025

$24.91 BnMarket Estimate, 2026

$28.75 BnMarket Forecast, 2034

$90.55 BnCAGR, 2026–2034

15.42%Europe Commercial Telematics Market Size

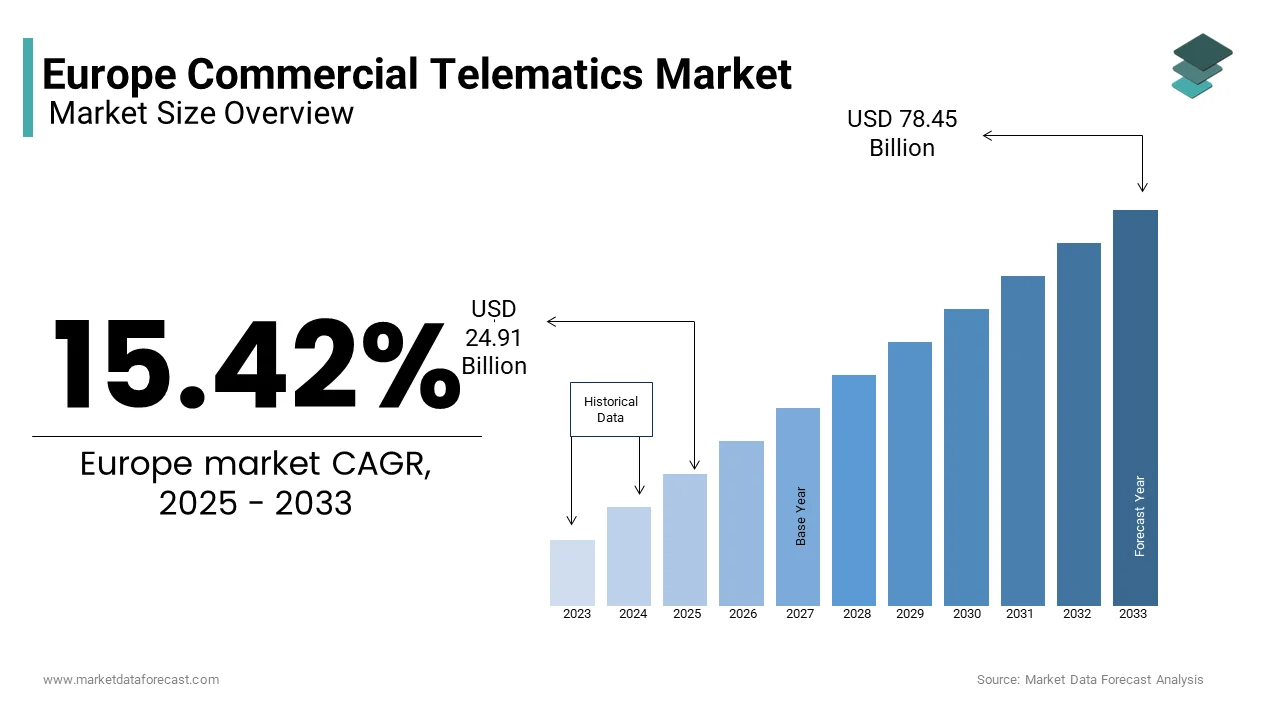

The European commercial Telematics Market Size was valued at USD 24.91 billion in 2025 and is anticipated to reach USD 28.75 billion in 2026 to reach from USD 90.55 billion by 2034, growing at a CAGR of 15.42% during the forecast period from 2026 to 2034.

Commercial telematics represents a sophisticated ecosystem of integrated telecommunications and informatics designed to optimize the performance, safety, and compliance of commercial vehicle fleets across the continent. This technology leverages global positioning systems, onboard diagnostics, and cellular networks to transmit real time data regarding vehicle location, driver behavior, fuel consumption, and mechanical health to centralized management platforms. The strategic imperative for these solutions stems from the critical role of the logistics sector in the European economy which relies heavily on road transport for the movement of goods. As per Eurostat, road freight transport accounted for the majority of inland freight tonnage in the European Union in 2023, which highlights the necessity for efficient fleet management tools. As per the European Commission, the transport sector is responsible for a significant portion of total greenhouse gas emissions in the region, which is driving the adoption of telematics to monitor and reduce carbon footprints. Furthermore, the implementation of the European Electronic Toll Service mandates interoperable systems that facilitate seamless cross border travel for heavy goods vehicles. National authorities utilize data from these systems to enforce driving hour regulations, and ensure road safety standards are met. The convergence of connectivity standards, and the rollout of fifth generation networks further enhance the capability of these systems to support autonomous driving features, and predictive maintenance protocols.

MARKET DRIVERS

Stringent Regulatory Mandates for Safety and Compliance

The rigorous regulatory framework governing commercial transport in Europe is one of the major factors propelling the growth of the European commercial telematics market. Legislation such as the European Union Mobility Package and the tachograph regulations require precise monitoring of driver working hours, rest periods, and vehicle speeds to prevent fatigue related accidents and ensure fair competition. According to the European Commission, heavy goods vehicles operating within the European Union must be equipped with digital tachographs that increasingly integrate telematics capabilities for remote enforcement checks. The introduction of the Smart Tachograph version two mandates enhanced security features and global navigation satellite system connectivity which drives fleets to upgrade their existing hardware to avoid penalties. National transport authorities in countries like Germany and France conduct frequent roadside inspections where non-compliant vehicles face substantial fines and operational delays. Telematics systems provide the automated logging and real time reporting necessary to demonstrate adherence to these complex rules without burdening drivers with manual paperwork. The General Data Protection Regulation also influences how fleet data is managed, requiring robust systems that protect driver privacy while fulfilling legal obligations. This regulatory pressure creates an inelastic demand for compliant telematics solutions as operators view them as essential tools for maintaining their licenses to operate rather than optional efficiency enhancers.

Operational Efficiency and Cost Reduction Imperatives

The relentless pressure to optimize operational costs and improve logistical efficiency drives commercial entities to invest heavily in advanced telematics platforms, which is further boosting the European commercial telematics market expansion. Rising fuel prices and volatile energy markets have made fuel management a top priority for fleet managers who seek to minimize consumption through better route planning and driver behavior monitoring. As per the International Energy Agency, diesel prices in Europe have experienced significant volatility in recent years which has prompted transport companies to seek immediate ways to reduce expenditure on fuel. Telematics solutions offer granular insights into idling times, harsh acceleration, and inefficient routing, allowing managers to implement corrective measures that yield immediate savings. The ability to track vehicle location in real time enables dynamic dispatching which reduces empty miles and improves asset utilization rates significantly. Maintenance costs are also curtailed through predictive analytics that alert operators to potential mechanical issues before they result in costly breakdowns or roadside failures. Large logistics providers report that implementing comprehensive telematics strategies can reduce overall fleet operating expenses by up to 15% annually. The competitive nature of the European logistics market forces companies to adopt these technologies to maintain profit margins and offer competitive pricing to clients. As supply chains become more complex, the need for visibility and control over every aspect of fleet operations ensures sustained growth in telematics adoption.

MARKET RESTRAINTS

Data Privacy Concerns and Regulatory Complexity

The intricate landscape of data privacy regulations presents a significant restraint to the European commercial telematics market growth. The General Data Protection Regulation imposes strict requirements on the collection, storage, and processing of personal data which includes detailed information on driver behavior and location patterns. According to the European Data Protection Board, fleet operators must navigate complex consent mechanisms and data minimization principles to ensure they do not infringe upon the privacy rights of their employees. The ambiguity surrounding the classification of certain telematics data as personal versus operational creates legal uncertainty that discourages some companies from fully utilizing advanced monitoring features. Drivers and labor unions frequently raise concerns about excessive surveillance, leading to resistance against the installation of intrusive tracking devices. Companies must invest heavily in secure data infrastructure and legal compliance teams to manage these risks, which increases the total cost of ownership for telematics solutions. Cross border data transfers within multinational fleets add another layer of complexity as different member states may interpret privacy laws differently. The fear of substantial fines for non-compliance causes some smaller operators to delay adoption or limit the scope of their telematics implementations. Until clearer guidelines and standardized frameworks emerge, the tension between operational visibility and privacy rights will continue to hinder the full potential of the market.

High Initial Implementation and Integration Costs

The substantial upfront investment required for hardware installation, software licensing, and system integration acts as a formidable barrier to entry for many small and medium sized enterprises in the transport sector, which is further impeding the growth of the European commercial telematics market. Deploying a comprehensive telematics solution involves purchasing onboard devices, paying for cellular connectivity subscriptions, and integrating the software with existing enterprise resource planning systems. As per the European Association of Craft Small and Medium Sized Enterprises, a significant portion of the transport industry consists of owner operators and small fleets who lack the capital reserves to fund such technological upgrades. The complexity of integrating legacy vehicles with modern telematics units often requires custom engineering work which further escalates costs and extends deployment timelines. Additionally, the rapid pace of technological advancement means that hardware can become obsolete quickly, creating hesitation among investors who fear stranded assets. Training staff to effectively use these sophisticated platforms adds to the initial expense and operational disruption during the transition period. While the long term return on investment is well documented, the immediate financial burden remains a deterrent for cash strapped businesses operating on thin margins. The fragmentation of the European market with varying languages and regulatory requirements also increases the cost of deploying standardized solutions across multiple countries. These financial hurdles slow down the penetration rate of advanced telematics, particularly among the smaller players who form the backbone of regional logistics networks.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Predictive Analytics

The incorporation of artificial intelligence and machine learning algorithms into telematics platforms offers a transformative opportunity for the European commercial telematics market. These advanced technologies enable the analysis of vast datasets to identify patterns, predict maintenance needs, and optimize routes with unprecedented accuracy. As per the European Technology Platform on Smart Systems Integration, the application of AI in logistics can improve fuel efficiency and reduce accident rates through proactive risk assessment. Predictive maintenance capabilities allow fleet managers to schedule repairs based on actual component wear rather than fixed intervals, minimizing downtime and extending vehicle lifespan. AI driven systems can also analyse driver behavior in real time to provide instant feedback and personalized coaching that enhances safety and reduces insurance premiums. The ability to forecast traffic conditions and weather impacts enables dynamic rerouting that ensures timely deliveries and reduces stress on drivers. Logistics companies are increasingly leveraging these insights to offer value added services to their customers such as precise delivery windows and real time cargo condition monitoring. The scalability of cloud-based AI solutions makes these advanced capabilities accessible to fleets of all sizes, fostering broader adoption. As data volumes grow, the competitive advantage gained from intelligent analytics will drive further investment and innovation in the telematics sector.

Expansion of Electric Vehicle Fleet Management Solutions

The rapid transition toward electrification in the commercial transport sector creates a lucrative opportunity for the European commercial telematics market. Managing an electric fleet requires monitoring battery health, charging status, and range optimization which traditional telematics systems are not fully equipped to handle. As per the European Automobile Manufacturers Association, sales of electric light commercial vehicles in Europe have surged, signaling a shift that demands new management tools. Telematics providers are developing features that locate available charging stations, plan routes based on battery capacity, and schedule charging during off peak hours to reduce energy costs. Integration with smart grid technologies allows fleets to participate in vehicle to grid programs where they can sell stored energy back to the grid during peak demand. The ability to monitor thermal management systems and regenerative braking performance ensures optimal battery longevity and safety. Government incentives for zero emission zones in major cities like London and Paris further accelerate the adoption of electric commercial vehicles and the associated telematics infrastructure. Companies that offer comprehensive electric fleet management suites position themselves as essential partners in the green transition. This niche represents a high growth avenue as more logistics providers commit to decarbonization targets and replace their internal combustion engine fleets.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in Connected Vehicles

The increasing connectivity of commercial vehicles exposes fleets to significant cybersecurity risks that threaten operational continuity and data integrity, which is challenging the growth of the European commercial telematics market. As telematics systems become more integrated with vehicle control units, they present potential entry points for malicious actors seeking to disrupt operations or steal sensitive information. As per the European Union Agency for Cybersecurity, the number of cyber-attacks targeting the transport sector has risen, with hackers exploiting vulnerabilities in wireless communication protocols and outdated software. A successful breach could lead to unauthorized vehicle control, theft of cargo, or manipulation of logistics data causing severe financial and reputational damage. The complexity of securing a heterogeneous fleet with devices from multiple vendors exacerbates the challenge as inconsistent security standards create weak links in the network. Fleet operators often lack the specialized expertise required to implement robust cybersecurity measures, leaving them vulnerable to evolving threats. Regulatory bodies are beginning to mandate higher security standards, but compliance remains a moving target as attack methods advance rapidly. The cost of implementing end to end encryption, regular security audits, and intrusion detection systems adds to the operational burden. Until the industry adopts unified security frameworks and prioritizes cyber resilience, the threat of digital attacks will remain a critical challenge hindering trust and adoption.

Interoperability Issues Across Fragmented Systems

The lack of standardization and interoperability among diverse telematics platforms and vehicle manufacturers creates significant operational inefficiencies for fleets operating across Europe, which is further challenging the expansion of the European commercial telematics market. Different original equipment manufacturers utilize proprietary data formats and communication protocols which makes it difficult to integrate vehicles from various brands into a single management interface. As per the European Telematics Industry Association, the fragmentation of the market forces fleet managers to use multiple disjointed systems to monitor their mixed fleets, leading to data silos and increased administrative overhead. The absence of a universal standard for data exchange hinders the seamless flow of information between telematics providers, toll operators, and regulatory authorities. This incompatibility complicates cross border operations where vehicles must interact with different national systems for tolling and compliance reporting. Efforts to establish common standards such as the Open Telematics Protocol have made progress, but widespread adoption remains slow due to competitive interests and technical barriers. The resulting inefficiencies increase costs and reduce the effectiveness of fleet optimization strategies. Resolving these interoperability challenges requires collaborative efforts from industry stakeholders and regulators to define and enforce open standards. Without a unified ecosystem, the full potential of connected commercial transport cannot be realized, limiting the scalability and utility of telematics solutions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 15.42% |

| Segments Covered | By Type, System Type, Provider Type, End-User Industry, and Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Webfleet Solutions BV, Verizon Communications Inc., ABAX UK Ltd, Masternaut Limited, Targa Telematics SpA. |

SEGMENTAL ANALYSIS

By Type Insights

Market Dominance of Solutions

The solutions segment dominated the market by commanding for the highest share of the European commercial telematics market in 2025. The dominance of solutions segment in the European market is driven by the fundamental necessity for hardware and software platforms that enable data collection and visualization. This dominance stems from the mandatory requirement for fleet operators to install onboard units to comply with European regulations regarding tachographs and emissions monitoring. As per the European Commission, heavy goods vehicles operating within the European Union must be equipped with digital tracking devices to operate legally, creating a massive baseline demand for physical solutions. The complexity of modern logistics requires sophisticated software capable of integrating global positioning system data with engine diagnostics to provide actionable insights into fuel efficiency and route optimization. Fleet managers rely on these centralized dashboards to monitor thousands of assets simultaneously, which is impossible without robust solution architectures. The initial capital expenditure for these systems is often justified by the immediate regulatory compliance they ensure, preventing costly fines and operational shutdowns. Furthermore, the rise of connected vehicle standards mandates that new commercial trucks come pre equipped with advanced telematics units, further solidifying the volume leadership of this segment. As supply chains become more digitized, the need for comprehensive solutions that offer real time visibility across borders remains the primary investment priority for transport companies seeking to maintain competitiveness in a saturated market.

The services segment is on the rise and is anticipated to witness a CAGR of 15.5% over the forecast period owing to the shifting business models of fleet operators who increasingly prefer subscription-based offerings over large upfront capital investments in hardware. The key driver is the growing demand for value added services such as predictive maintenance, driver coaching, and over the air software updates which extend the lifecycle of vehicles and reduce downtime. As per the European Technology Platform on Smart Systems Integration, the adoption of managed services allows small and medium sized enterprises to access enterprise grade analytics without needing internal technical expertise. The complexity of managing electric vehicle fleets has also spurred demand for specialized consulting and charging management services that optimize battery usage and energy costs. Insurance companies are partnering with telematics providers to offer usage-based insurance policies which require continuous data processing and risk assessment services. The transition toward outcome-based contracts where providers guarantee specific efficiency improvements further accelerates the uptake of service-oriented models. As artificial intelligence becomes more prevalent, the need for ongoing algorithm training and data interpretation services will continue to outpace the growth of static hardware sales, making this segment the primary engine of future market revenue.

By System Insights

Market Dominance of Embedded Systems

The embedded systems segment held the dominant position in the Europe commercial telematics market by accounting for the leading share of the regional market in 2025. The leading position of embedded systems segment in the European market is attributed to their seamless integration into vehicle manufacturing processes and superior reliability for critical operations. Original equipment manufacturers increasingly install these-factory fitted units as standard features in new commercial vehicles to meet regulatory requirements for eCall and digital tachography. As per the European Automobile Manufacturers Association, new heavy-duty trucks sold in Europe since 2020 come equipped with embedded telematics modules that connect directly to the vehicle controller area network. This direct connection ensures higher data accuracy and security compared to aftermarket alternatives which often rely on external ports that can be tampered with or disconnected. The durability of embedded systems makes them ideal for the harsh operating conditions faced by commercial fleets including extreme temperatures and constant vibration. Fleet operators favor these systems because they eliminate the need for retrofitting older vehicles and reduce installation time and labor costs significantly. The ability of embedded units to support over the air updates ensures that vehicles remain compliant with evolving safety and emissions standards throughout their lifespan. As the average age of the European commercial fleet decreases due to stricter emission zones, the proportion of vehicles with factory installed telematics continues to rise, reinforcing the market leadership of this system type.

The smartphone integrated systems segment is expected to witness a promising CAGR of 17.2% over the forecast period owing to the ubiquity of mobile devices and the rise of the gig economy. This surge is primarily attributed to the cost effectiveness and ease of deployment offered by applications that transform standard smartphones into powerful telematics devices using built in sensors. As per Eurostat, the number of self-employed drivers and courier workers in Europe has increased, creating a vast user base that cannot justify expensive dedicated hardware. These systems leverage global positioning system, accelerometers, and gyroscopes within phones to track location, monitor driving behavior, and manage deliveries without additional equipment. The flexibility of smartphone-based solutions allows logistics platforms to onboard drivers instantly which is crucial for on demand delivery services operating in urban centers. Advances in mobile network connectivity including five generation networks have improved the reliability and speed of data transmission, making these systems viable for real time fleet management. Small businesses appreciate the scalability of app-based models, which allow them to pay per user and expand their fleet tracking capabilities as they grow. The continuous improvement in smartphone battery life and processing power further enhances the functionality of these systems, enabling features like augmented reality navigation and voice commanded reporting that appeal to modern drivers.

By End Use Industry Insights

The transportation and logistics segment captured the major share of the European commercial telematics market in 2025. The growth of the transportation and logistics segment in the European market can be credited to its absolute dependence on efficient fleet operations to sustain supply chains and meet consumer demands. This dominance is underpinned by the sheer volume of commercial vehicles operating in this sector which requires constant monitoring to ensure timely deliveries and regulatory compliance. As per Eurostat, road freight transport handles the majority of inland freight tonnage in the European Union, making it the most critical application area for telematics technologies. The intense competition among logistics providers forces companies to adopt advanced tracking solutions to optimize routes, reduce fuel consumption, and improve asset utilization rates. Regulatory pressures such as the Mobility Package mandate strict adherence to driving hours and rest periods which can only be effectively managed through automated telematics systems. The rise of e commerce has further amplified the need for last mile delivery visibility, requiring granular tracking capabilities that only sophisticated telematics can provide. Cross border trade within the single market necessitates interoperable systems that can handle diverse tolling and reporting requirements across multiple jurisdictions. As supply chains become more complex and customers demand real time shipment updates, the reliance on telematics within this sector will continue to deepen, ensuring its position as the primary revenue generator for the market.

The construction segment is anticipated to record a CAGR of 146.5% over the forecast period due to the rising need for rigorous asset management and safety compliance on dynamic job sites. This acceleration is fueled by the high value of construction machinery and the significant losses incurred due to theft, unauthorized use, and inefficient deployment of equipment. As per the European Construction Industry Federation, the sector faces increasing pressure to improve productivity and reduce carbon emissions which telematics addresses by monitoring idle times and optimizing machine usage patterns. The transient nature of construction projects requires flexible tracking solutions that can monitor assets across multiple locations and prevent loss during transit between sites. Safety regulations in Europe are becoming stricter, requiring detailed records of operator behavior and machine health which telematics systems provide through real time data logging. The integration of telematics with building information modeling allows project managers to synchronize equipment availability with project timelines, reducing delays and cost overruns. The rise of rental fleets in the construction sector has also boosted demand as rental companies use these systems to verify usage hours for billing and ensure machines are returned in good condition. As infrastructure projects expand across Europe to support green energy transitions, the deployment of telematics in construction will continue to surge.

COUNTRY ANALYSIS

Germany Commercial Telematics Market Analysis

Germany stood as the undisputed leader in the Europe commercial telematics market by holding 25.5% of the European market share in 2025. The growth of Germany in the European market is attributed to its robust automotive manufacturing base, extensive logistics network and the presence of major original equipment manufacturers who integrate advanced telematics systems into commercial vehicles at the factory level. As per the German Federal Ministry of Transport and Digital Infrastructure, the nation processes the highest volume of road freight in Europe, necessitating sophisticated fleet management solutions to maintain efficiency. The strict enforcement of environmental regulations in German cities has accelerated the adoption of telematics for monitoring emissions and managing access to low emission zones. The strong industrial sector relies heavily on just in time delivery models which require precise real time tracking to prevent production stoppages. German companies are also at the forefront of adopting artificial intelligence driven telematics to predict maintenance needs and optimize fuel consumption across large fleets. The government support for digital infrastructure including widespread five generation network coverage facilitates the seamless operation of connected vehicle technologies. This combination of industrial might, regulatory rigor, and technological advancement ensures Germany remains the central hub for telematics innovation and deployment in the region.

France Commercial Telematics Market Analysis

France had the second largest share of the European commercial telematics market in 2025. The prominent position of France in the European market is driven by its strategic geographic location as a gateway to Southern Europe and its ambitious digital transformation goals. The French market status is characterized by a strong emphasis on regulatory compliance and sustainability which drives fleet operators to adopt telematics for monitoring carbon footprints and driver hours. As per the French Ministry of Ecological Transition, the transport sector is a key target for decarbonization efforts, prompting widespread investment in tools that optimize routes and reduce fuel usage. The extensive network of highways and the high volume of cross border trade with Spain, Italy, and Germany create a complex operational environment that demands advanced tracking capabilities. Government initiatives to modernize the logistics infrastructure include subsidies for fleets that implement eco-friendly telematics solutions. The growing e commerce sector in France has increased the demand for last mile delivery tracking, requiring granular visibility into urban logistics operations. French telecommunications providers are actively collaborating with telematics firms to develop integrated connectivity packages that simplify adoption for small and medium sized enterprises. These factors combine to create a dynamic market where regulatory pressure and economic necessity drive sustained growth in commercial telematics adoption.

United Kingdom Commercial Telematics Market Analysis

The United Kingdom is anticipated to hold a significant position in the Europe commercial telematics market over the forecast period owing to the mature logistics sector and a strong culture of technological innovation. The market status in the UK is defined by the adaptation of fleet operators to post Brexit trade complexities which have increased the need for precise border management and customs documentation tools. As per the Department for Transport, the UK logistics industry is undergoing a rapid digital transformation to maintain competitiveness in global supply chains, driving demand for advanced telematics platforms. The introduction of clean air zones in major cities like London and Birmingham has forced commercial fleets to utilize telematics for monitoring emissions and planning compliant routes. The thriving gig economy and on demand delivery services in the UK have accelerated the adoption of smartphone integrated telematics solutions among independent contractors. British insurers are leading the way in usage based insurance models which rely heavily on telematics data to assess risk and set premiums. The strong presence of fintech and software companies in the UK fosters the development of innovative telematics applications that integrate with broader supply chain management systems. Despite regulatory changes, the UK remains a vital market where agility and technology drive the evolution of commercial fleet management.

Italy Commercial Telematics Market Analysis

Italy is expected to represent a crucial market within the Europe commercial telematics market. The need to modernize its fragmented transport sector and improve cross border efficiency and the dominance of small and medium sized family-owned transport companies that are increasingly adopting cloud-based telematics to compete with larger rivals are propelling the French market growth. As per the Italian National Institute of Statistics, the road freight sector is vital for the national economy yet faces challenges related to aging fleets and inefficiency which telematics helps address through better asset utilization. The geographical shape of Italy with its long coastline and mountainous terrain creates unique logistical challenges that require optimized routing and real time traffic management solutions. Government incentives for fleet renewal and digitalization are encouraging operators to replace old vehicles with new ones equipped with embedded telematics systems. The tourism and agriculture sectors also contribute to demand as they require specialized tracking for perishable goods and seasonal transport spikes. Italian telematics providers are focusing on user friendly interfaces to overcome resistance to technology adoption among traditional drivers. This blend of economic necessity and supportive policy measures ensures steady growth as the sector moves toward greater transparency and efficiency.

Spain Commercial Telematics Market Analysis

Spain is projected to showcase a healthy CAGR in the European commercial telematics market during the forecast period owing to its role as a key logistics bridge between Europe and Africa and its aggressive push for digital connectivity. The market status reflects a rapid modernization effort where transport companies are leveraging telematics to enhance competitiveness in the international freight market. As per the Spanish Ministry of Transport Mobility and Urban Agenda, the country has invested heavily in expanding five generation networks along major freight corridors, enabling high speed data transmission for connected vehicles. The booming e commerce sector in Spain has created a surge in demand for last mile delivery solutions that offer real time visibility and customer communication features. The tourism industry also drives demand for telematics in coach and bus fleets to ensure passenger safety and optimize tour schedules. Regional governments are implementing smart city initiatives that integrate commercial vehicle data with urban traffic management systems to reduce congestion. The adoption of telematics is further accelerated by the need to comply with European regulations on driver working hours and vehicle emissions. As Spain continues to strengthen its position as a logistics hub, the integration of advanced telematics technologies will remain a priority for sustaining economic growth and operational excellence.

COMPETITIVE LANDSCAPE

The competition in the Europe commercial telematics market is intense and characterized by a mix of global technology giants and specialized regional providers vying for dominance. Major corporations leverage their extensive resources to offer end to end platforms that combine hardware software and connectivity services into unified solutions. Smaller niche players differentiate themselves by focusing on specific industry verticals or offering highly customizable features that address unique operational challenges. The landscape is rapidly evolving as companies race to integrate artificial intelligence and Internet of Things capabilities to provide deeper insights and automation. Price competition remains fierce particularly in the standard tracking segment prompting vendors to emphasize value added services like driver coaching and predictive maintenance. Strategic alliances with telecommunications providers and automotive manufacturers are becoming essential to ensure seamless connectivity and factory fit installations. Regulatory compliance serves as a key battleground where providers compete to offer the most robust tools for meeting strict European safety and emissions standards. This dynamic environment fosters continuous innovation and consolidation as firms strive to capture market share in an increasingly digitized transportation sector.

KEY MARKET PLAYERS

A few of the market players in the Europe commercial telematics market include

- Webfleet Solutions BV

- Trimble Inc.

- Verizon Communications Inc.

- TomTom Telematics

- ABAX UK Ltd

- Masternaut Limited

- Targa Telematics SpA

Top Players In The Market

- Verizon Connect stands as a dominant force in the Europe commercial telematics market by delivering comprehensive fleet management solutions that optimize routing and driver safety. The company contributes significantly to the global market by leveraging its vast network infrastructure to provide real time visibility and analytics for diverse vehicle types. Recent actions include the expansion of its artificial intelligence driven analytics platform to help European fleets reduce fuel consumption and improve compliance with local regulations. Verizon Connect actively partners with original equipment manufacturers to embed its technology directly into new commercial vehicles ensuring seamless integration. The firm also invests heavily in cybersecurity measures to protect sensitive fleet data from emerging digital threats. By focusing on scalable cloud based solutions and continuous innovation Verizon Connect strengthens its position as a trusted partner for logistics companies seeking operational excellence and sustainability across the continent.

- Trimble Inc. plays a pivotal role in the Europe commercial telematics market through its advanced transportation and logistics solutions that integrate positioning technology with workflow software. The company enhances global operations by offering tools that improve asset utilization and supply chain efficiency for freight operators worldwide. Recent initiatives involve the acquisition of specialized software firms to broaden its portfolio of last mile delivery and field service management capabilities. Trimble has launched new modules specifically designed to help European fleets manage electric vehicle charging and monitor carbon emissions effectively. The firm collaborates with industry associations to establish standards for data interoperability and safety compliance. By prioritizing user centric design and robust data analytics Trimble enables fleet managers to make informed decisions that drive productivity. These strategic moves solidify its reputation as a leader in transforming commercial transportation through technology and innovation.

- TomTom Telematics maintains a significant presence in the Europe commercial telematics market by providing connected vehicle services that enhance driver productivity and fleet efficiency. The company contributes to the global market by utilizing its renowned mapping data and navigation expertise to offer precise routing and traffic information. Recent actions include the rebranding and expansion of its WEBFLEET platform to support a wider range of third party integrations and mobile applications. TomTom Telematics has strengthened its partnerships with major truck manufacturers to ensure factory fit installations of its units across new vehicle lines. The firm focuses on developing sustainable mobility solutions that help fleets transition to lower emission operations through optimized driving behaviors. By investing in open application programming interfaces TomTom encourages a vibrant ecosystem of developers to create custom solutions. This commitment to connectivity and sustainability reinforces its status as a key enabler of smart logistics in Europe and beyond.

Top Strategies Used By Key Market Participants

Key players in the Europe commercial telematics market primarily focus on strategic acquisitions to expand their product portfolios and gain access to innovative technologies. Companies frequently form partnerships with original equipment manufacturers to integrate telematics systems directly into vehicles during production. Investment in artificial intelligence and machine learning drives the development of predictive analytics that enhance fleet efficiency and safety. Providers are increasingly adopting cloud based architectures to offer scalable and flexible subscription models that appeal to small and medium sized enterprises. Expanding cybersecurity capabilities remains a priority to protect connected vehicles from evolving digital threats. Firms also prioritize sustainability by developing features that help fleets reduce fuel consumption and manage electric vehicle transitions effectively. These strategies collectively enable market participants to maintain competitive advantages and meet the evolving needs of modern logistics.

MARKET SEGMENTATION

This research report on the Europe commercial telematics market is segmented and sub-segmented into the following categories.

By Type

- Solution

- Fleet Tracking and Monitoring

- Driver Management

- Insurance Telematics

- Safety and Compliance

- V2X Solutions

- Others

- Services

- Professional Services

- Managed Services

By System Type

- Embedded

- Tethered

- Smartphone Integrated

By Provider Type

- OEM

- Aftermarket

By End Use Industry

- Transportation and Logistics

- Media and Entertainment

- Government and Utilities

- Travel and Tourism

- Construction

- Healthcare

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

Why are European fleet operators relying more on telematics systems?

They need real-time visibility to control fuel costs, vehicle usage, and driver performance.

What everyday problem does commercial telematics solve first?

It eliminates guesswork by providing accurate data on routes, mileage, and idle time.

How does telematics improve fleet safety management?

Driver behavior monitoring helps reduce risky driving and accident frequency.

Why are logistics companies integrating telematics with dispatch systems?

Connected platforms streamline route planning and delivery coordination.

How do emission regulations influence telematics adoption in Europe?

Fleet tracking helps businesses monitor fuel consumption and meet environmental compliance targets.

What operational benefit do managers notice after installing telematics?

Maintenance schedules become proactive instead of reactive.

Why is data security important in commercial telematics systems?

Fleet data contains sensitive operational information that must be protected.

How does telematics support electric vehicle fleet expansion?

Battery monitoring and charging data optimize vehicle deployment strategies.

Why are small and mid-sized fleets adopting telematics faster now?

Affordable cloud-based solutions make advanced tracking accessible.

How does telematics reduce fuel expenses for transport companies?

Route optimization and idle reduction directly lower fuel consumption.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com