Europe Connected Vehicle Market Size, Share, Trends, Growth Forecast, Segmented By Application, Technology Type, Connectivity, Vehicle, Vehicle Connectivity, And By Country (UK, Russia, Germany, Italy, France, Spain, Sweden, Denmark, Poland, Switzerland, Netherlands, and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Connected Vehicle Market Size

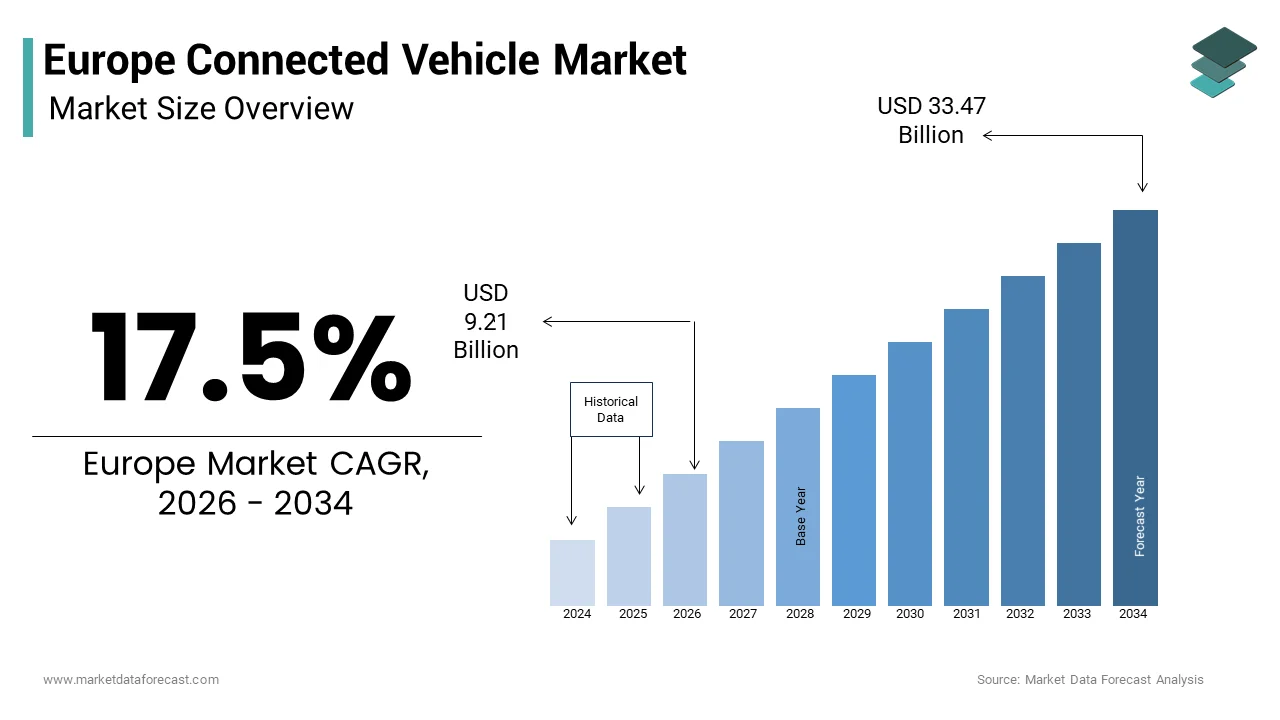

The Europe-connected vehicle market size was valued from USD 7.84 billion in 2025 and is anticipated to reach USD 9.21 billion in 2026 to reach from USD 33.47 billion by 2034, growing at a CAGR of 17.5% during the forecast period from 2026 to 2034.

Connected vehicle encompasses automobiles equipped with internet connectivity and onboard sensors that facilitate communication between the vehicle, its driver, other vehicles, and surrounding infrastructure. This ecosystem transforms standard transportation into a dynamic network where data exchange optimizes traffic flow, enhances safety protocols, and enables advanced infotainment services. The region stands at the forefront of this technological shift due to stringent regulatory frameworks and a mature automotive manufacturing base. According to the European Commission, road transport is the largest contributor to transport related carbon dioxide emissions in the European Union, which is creating an urgent imperative for connected solutions that improve fuel efficiency, and reduce environmental impact. As per Eurostat, the vast majority of households in the European Union had internet access in 2023, which is providing the necessary digital backbone for widespread vehicle connectivity adoption. The integration of fifth generation cellular networks is also accelerating, with the European Electronic Communications Code aiming to ensure uninterrupted coverage along major transport paths by 2030. This digital transformation extends beyond convenience, as it fundamentally alters how vehicles interact with smart city infrastructures. The push toward zero emission mobility, coupled with the digitization of public services, creates an environment where connected vehicles serve as critical nodes in a broader intelligent transport system rather than isolated mechanical units.

MARKET DRIVERS

Stringent Government Safety Regulations and Mandates

The implementation of rigorous safety legislation by European authorities is primarily driving the growth of the European connected vehicle market. As per the General Safety Regulation updated by the European Parliament, systems such as intelligent speed assistance, and emergency lane keeping became compulsory for all new cars registered from July 2022 onwards. These regulations force original equipment manufacturers to integrate sophisticated sensor suites, and communication modules that allow vehicles to receive real time data regarding road conditions, and speed limits. The European Transport Safety Council notes that speeding contributes significantly to fatal road accidents in Europe, which justifies the legislative push for connected speed assistance systems. Additionally, the eCall system, which automatically contacts emergency services in the event of a severe crash, has been mandatory since 2018, and as per the European Commission, it has reduced emergency response times considerably in rural areas. This regulatory pressure ensures that connectivity is no longer a premium feature but a standard requirement for market entry.

Rising Consumer Demand for Advanced Infotainment and Seamless Mobility

A profound shift in consumer expectations regarding in vehicle experiences drives the rapid adoption of connected car technologies throughout Europe, which is further boosting the expansion of the European connected vehicle market. Modern European drivers increasingly view their vehicles as extensions of their digital lives, and demand seamless integration with smartphones, and cloud-based services. As per the European Automobile Manufacturers Association, a majority of new car buyers in Western Europe consider connected services such as real time navigation, and remote diagnostics as essential factors in their purchasing decision. This demographic shift is particularly evident among younger consumers who expect over the air software updates, and high-speed internet access similar to what they experience in their homes. Eurostat reports that smartphone penetration among individuals aged 16 to 74 in the EU was very high in 2023, supporting this trend. Automakers are responding by embedding advanced infotainment systems that support voice recognition, and personalized content streaming directly through the vehicle interface. The demand extends beyond entertainment to include practical mobility services such as predictive maintenance alerts, and integrated payment systems. Consumers are willing to pay a premium for subscriptions that offer enhanced security tracking, and remote vehicle control capabilities, transforming the business model for manufacturers toward recurring revenue streams.

MARKET RESTRAINTS

Critical Cybersecurity Vulnerabilities and Data Privacy Concerns

Escalating cyber threats, and strict privacy laws create significant barriers to consumer trust, and system deployment, which is likely to impede the expansion of the European connected vehicle market. As vehicles become increasingly software defined, they expand the attack surface for malicious actors seeking to compromise critical driving functions, or steal sensitive user data. As per the European Union Agency for Cybersecurity, modern cars contain vast amounts of code, making them potentially more vulnerable to hacking than traditional computer systems. Demonstrations by security researchers have shown that unauthorized remote access can allow attackers to manipulate steering, braking, and acceleration systems. This reality creates apprehension among consumers, and regulators regarding the safety implications of constant connectivity. Furthermore, the General Data Protection Regulation imposes strict requirements on how automotive companies collect, and process location data, and driving behavior information. Non-compliance with these privacy laws can result in significant fines, discouraging some manufacturers from fully utilizing data gathering capabilities. The complexity of securing supply chains adds another layer of difficulty as components from various third-party vendors must all meet rigorous security standards. The industry also faces a shortage of specialized cybersecurity talent, slowing down the development of robust defense mechanisms necessary to protect connected fleets.

Fragmented Infrastructure and Interoperability Issues

Inconsistent network coverage and lack of unified standards hinder seamless cross border vehicle communication, which is further hampering the regional market growth. While the European Union strives for a single market, the deployment of necessary supporting infrastructure such as fifth generation networks, and roadside units varies significantly between member states. As per the European Court of Auditors, disparities exist in fifth generation coverage between urban centers, and rural regions, with some countries lagging behind in the rollout of high-speed networks required for real time vehicle communication. This fragmentation prevents connected vehicles from maintaining consistent performance when crossing borders, or traveling through less developed areas. Additionally, the absence of universally adopted standards for vehicle to infrastructure communication leads to interoperability challenges where cars from different manufacturers cannot effectively exchange data with local traffic management systems. The European Committee for Standardization has worked on harmonizing protocols, yet full implementation remains years away in many jurisdictions. Municipalities often deploy proprietary solutions that work only with specific brands or service providers, creating silos that limit the overall utility of connected features. The high cost of upgrading legacy traffic signals, and road sensors to support smart communication further delays infrastructure maturity. Public funding constraints in several economies slow down the necessary investments to create a cohesive network. Without a reliable, and uniform infrastructure backbone, the promised benefits of platooning, and coordinated traffic flow remain largely theoretical in many parts of the continent.

MARKET OPPORTUNITIES

Expansion of Smart City Initiatives and Integrated Urban Mobility

The aggressive pursuit of smart city projects by European municipal governments presents a substantial opportunity for the growth of the connected vehicle market in Europe. Cities across Europe are investing heavily in digital infrastructure to manage congestion, and reduce pollution, creating fertile ground for vehicles that can communicate with urban systems. As per Eurostat, a large majority of the European population resides in urban areas, intensifying the need for intelligent transport solutions that optimize traffic flow, and parking availability. Initiatives such as the Living Labs in Barcelona, and smart traffic management systems in Amsterdam demonstrate how connected vehicles can integrate with citywide networks to receive real time signal prioritization, and route guidance. The European Innovation Partnership on Smart Cities and Communities facilitates collaboration between local authorities, and automotive stakeholders to pilot new mobility concepts. Connected vehicles enable precise monitoring of air quality, and noise levels, allowing cities to enforce low emission zones more effectively. The opportunity extends to public transport integration where private connected cars can share data with buses, and trams to improve multimodal journey planning. Municipalities are increasingly offering incentives for connected vehicles such as preferential parking, or access to restricted zones.

Emergence of Vehicle to Grid Technology and Energy Management

The transition toward electric mobility opens a transformative opportunity for connected vehicles to participate actively in energy distribution networks through vehicle to grid technology. Europe aims to achieve climate neutrality by 2050, necessitating a flexible energy grid that can handle the variable output of renewable sources. Connected electric vehicles can serve as distributed storage units that absorb excess energy during peak production times, and feed it back to the grid during high demand periods. As per the International Energy Agency, Europe hosts millions of electric vehicles that could collectively provide significant storage capacity if properly integrated via bidirectional charging systems. Automotive manufacturers are partnering with utility companies to develop platforms that automate this energy exchange based on real time pricing signals, and grid stability requirements. Regulatory frameworks in countries like Germany, and the Netherlands are evolving to support peer to peer energy trading. The connectivity required to manage these complex transactions ensures that vehicles must remain online, and capable of secure data transmission. This synergy between the automotive, and energy sectors drives demand for advanced telematics units that can handle dual roles of mobility, and energy management.

MARKET CHALLENGES

Complexity of Legacy System Integration and Technical Debt

Integrating advanced connectivity features into existing vehicle architectures is challenging the expansion of the European connected vehicle market. Many manufacturers operate with legacy electronic control unit designs that were not originally intended for high bandwidth data transmission, or over the air updates. As per the Society of Motor Manufacturers and Traders, the average development cycle for a new vehicle platform spans several years, which is significantly longer than the rapid iteration cycles of consumer electronics, and software. This discrepancy creates a situation where hardware installed in new cars may already be outdated by the time of launch. Retrofitting older architectures with modern connectivity modules often requires extensive reengineering. The sheer volume of software code in modern vehicles introduces complexity that makes debugging, and validation resource intensive. Ensuring that new connected features do not interfere with critical safety systems demands rigorous testing protocols. The industry faces a shortage of software engineers proficient in automotive grade coding standards, which slows down the migration to software defined platforms. Furthermore, the need to maintain backward compatibility with previous model generations adds layers of technical debt that constrain innovation.

High Costs of Development and Uncertain Return on Investment

Soaring software expenses and ambiguous monetization strategies threaten long term financial viability are further challenging the growth of the European connected vehicle market. The substantial financial burden associated with developing, and maintaining connected vehicle ecosystems creates a significant barrier to profitability for market participants. Building a robust connectivity platform requires immense upfront investment in software development, cloud infrastructure, and cybersecurity measures. As per Deloitte, the cost of software, and electronic content in vehicles is projected to rise sharply, potentially accounting for a significant portion of total vehicle costs by 2030. This escalation squeezes profit margins, especially in the mass market segment where price sensitivity remains high. Monetizing connected services proves challenging as European consumers show reluctance to pay recurring subscription fees for features they previously received as standard. The uncertainty regarding which services will generate sustainable revenue streams leads to hesitation in committing long term capital. Additionally, the rapid pace of technological obsolescence means that expensive hardware installations may lose value quickly if newer standards emerge. Insurance liabilities related to software failures, or data breaches add another layer of financial risk. The fragmented nature of the European market necessitates localization efforts for different languages, and regulations, further inflating development expenses. Smaller suppliers struggle to keep up with the investment requirements, leading to consolidation that reduces competition, and innovation diversity. Manufacturers face the dilemma of either absorbing these costs to remain competitive, or passing them to consumers and risking market share loss.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 17.5% |

| Segments Covered | By Application, Technology Type, Connectivity, Vehicle Type, Communication Type, and Country. |

| Various Analyses Covered | Global, Regional, and Country Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Robert Bosch GmbH, Continental AG, Denso Corporation, Visteon Corporation, Harman International, AT&T Inc., TomTom N.V., Airbiquity Inc., Qualcomm Technologies Inc., Sierra Wireless, Infineon Technologies, Magna International, ZF Friedrichshafen AG, and Others. |

SEGMENTAL ANALYSIS

By Application Insights

The telematics segment dominated the market in 2025 with the highest share of the regional market. The dominance of telematics segment in primarily driven by regulatory mandates and fleet optimization needs. This dominance stems from the compulsory integration of emergency call systems and the rising demand for commercial fleet tracking. According to the European Commission, the eCall system has been mandatory in all new cars and light vans since 2018. As per the European Transport Safety Council, this system has significantly reduced emergency response times and saved lives annually across the EU. Furthermore, according to the European Parliament, the General Safety Regulation introduced in 2022 expanded requirements to include intelligent speed assistance and event data recorders, all of which rely on robust telematics architecture. These legal obligations remove market uncertainty and guarantee volume for telematics providers. Manufacturers cannot opt out of these features without losing access to the single market. The continuous evolution of these laws to include more sophisticated data logging for insurance and liability purposes further cements the position of telematics as the foundational application layer. The sheer volume of vehicles complying with these laws ensures that telematics remains the revenue leader in terms of unit shipments and basic service subscriptions.

The mobility management segment is projected to register a promising CAGR of 25.5% over the forecast period in the European market owing to the shift toward Mobility as a Service models and the integration of multimodal transport platforms in smart cities. According to the International Association of Public Transport, urban populations in Europe are increasingly rejecting private car ownership in favor of on demand mobility solutions. As per the European Commission, shared mobility services could reduce the number of private vehicles in urban centers significantly by 2030. Cities like Helsinki and Vienna have pioneered integrated apps that allow users to plan, book, and pay for trips combining buses, trains, bike shares, and ride hailing services in a single interface. Connectivity enables real time availability updates and dynamic pricing which are essential for these platforms to function effectively. Consumers demand frictionless transitions between transport modes, driving investment in software that manages these complex interactions. The growth of subscription-based mobility packages further accelerates this trend as users prefer predictable monthly costs over variable travel expenses. Automakers are partnering with tech firms to offer their own branded mobility services, expanding the market beyond traditional public transport operators.

By Technology Insights

The 4G LTE technology segment held the dominant share in the Europe connected vehicle market in 2025. The growth of the 4G LTE segment in the European market is attributed to its extensive network coverage and established ecosystem maturity. According to the European Electronic Communications Code, member states have achieved near universal 4G coverage across the EU population. As per the Global mobile Suppliers Association, 4G remains the most widely used mobile technology globally, providing a mature and cost-effective supply chain for automotive telematics control units. The latency and bandwidth offered by 4G are sufficient for most current connected car services including navigation, streaming, and basic vehicle diagnostics. This technological adequacy combined with widespread availability reduces the risk for automakers launching new models. The extensive existing infrastructure means no additional capital expenditure is required to support 4G connected vehicles, unlike emerging technologies.

The 5G technology segment is anticipated to witness the fastest CAGR of 31.3% during the forecast period in this regional market owing to the rising need for ultra-low latency communications and the enablement of advanced autonomous driving capabilities. According to the European Telecommunications Standards Institute, 5G networks can achieve latencies as low as one millisecond, which is essential for real time decision making in high-speed traffic scenarios. As per the European Commission, 5G has been identified as a key enabler for cooperative intelligent transport systems, with spectrum allocated specifically for automotive use. This technological leap allows vehicles to share sensor data in real time, creating a collective awareness that extends beyond line of sight. The ability to process vast amounts of data at the edge of the network reduces the computational load on individual vehicles, lowering hardware costs. Safety regulations are evolving to encourage the adoption of these advanced systems, creating a regulatory pull for 5G integration. As automakers race to achieve higher levels of automation, 5G becomes a non-negotiable requirement rather than an optional upgrade.

By Communication Insights

The vehicle to infrastructure segment captured the largest share of the European connected vehicle market in 2025 due to extensive government investments in smart road infrastructure and traffic management systems. According to the European Investment Bank, significant funding has been allocated to deploy smart traffic lights, roadside units, and digital signage across major European corridors. The Connecting Europe Facility specifically targets the deployment of intelligent transport systems to enhance cross border mobility and safety. Municipalities are upgrading legacy traffic management centers to interact with connected fleets, optimizing traffic flow and reducing congestion. This top down approach ensures that the necessary hardware is in place to support V2I services before widespread vehicle adoption occurs. The standardization efforts by the European Committee for Standardization facilitate interoperability between different national systems, encouraging broader deployment. Public sector leadership reduces the risk for private investors and automakers, creating a stable environment for V2I growth. The focus on public safety and efficiency aligns with political agendas, ensuring sustained funding and priority status. This robust infrastructure backbone makes V2I the most viable and widely available communication type in the current market landscape.

The vehicle-to-vehicle segment is projected to grow at the fastest CAGR of 25.5% over the forecast period in this regional market due to the critical safety benefits of collision avoidance and the rise of cooperative driving manoeuvres. According to the European Transport Safety Council, road accidents continue to claim many lives annually in the EU, with a significant portion caused by limited visibility or delayed reaction times. V2V technology allows vehicles to exchange speed, position, and direction data multiple times per second, creating a 360-degree awareness field that surpasses human senses and onboard sensors. This capability enables cooperative collision warning systems that can alert drivers to impending crashes at blind intersections or during lane changes. The technology is particularly effective in preventing chain reaction accidents on highways by broadcasting sudden braking events to following vehicles instantly. Regulatory bodies are increasingly recognizing the potential of V2V to save lives, leading to discussions on future mandates similar to eCall. Automakers are integrating V2V into advanced driver assistance systems to differentiate their safety offerings in a competitive market. The potential to reduce accident severity and frequency provides a compelling value proposition for consumers and insurers alike. As the technology matures and costs decline, it will become a standard safety feature, driving exponential growth in this segment.

COUNTRY ANALYSIS

Germany Connected Vehicle Market Analysis

Germany dominated the connected vehicle market in Europe in 2025 with 25.5% of the regional market share. The leading position of Germany in the European market is attributed to its robust automotive manufacturing heritage and technological prowess. The country serves as the home base for global giants like Volkswagen, BMW, and Mercedes Benz, who are aggressively integrating connectivity into their entire model ranges. According to the German Association of the Automotive Industry, domestic manufacturers have invested heavily in research and development, with a significant portion dedicated to digitalization and software defined vehicles. The German government supports this transition through initiatives such as the Automotive Summit, which fosters collaboration between industry and policymakers to accelerate 5G rollout along autobahns. The presence of a highly skilled engineering workforce and a dense network of Tier 1 suppliers creates an ecosystem conducive to rapid innovation. Consumer acceptance of advanced technology is exceptionally high, with German buyers often demanding the latest infotainment and driver assistance features. The country's strong export orientation means that technologies developed domestically are quickly scaled globally, reinforcing its market dominance. Furthermore, testbeds for autonomous driving in cities like Munich and Berlin provide real world data that refines connected vehicle algorithms.

France Connected Vehicle Market Analysis

France had the second largest share of the European market in 2025 due to the strong state led initiatives and a vibrant startup ecosystem focused on mobility. The French government has positioned itself as a champion of sovereign technology, investing heavily in connected and autonomous vehicle projects through the France 2030 investment plan. According to the French Ministry of Economy, substantial grants are available for companies developing smart mobility solutions, encouraging both established automakers and innovative startups to innovate. The country boasts several large scale testing zones, including the Saclay plateau, where connected vehicles operate daily to validate new technologies. French consumers are increasingly environmentally conscious, driving demand for connected electric vehicles that offer energy management and eco routing features. The integration of connected services with public transport networks in cities like Paris and Lyon creates a seamless multimodal experience that boosts adoption. Regulatory frameworks in France are progressive, often piloting new rules for data sharing and vehicle to infrastructure communication before EU wide implementation. The strong presence of telecommunications operators ensures robust network coverage to support these services.

United Kingdom Connected Vehicle Market Analysis

The United Kingdom is estimated to command for a prominent share of the European connected vehicle market during the forecast period owing to its world class research institutions and a proactive regulatory environment to foster connected vehicle growth. Despite Brexit, the UK remains a hub for automotive innovation, with major manufacturing plants and engineering centers operated by Nissan, Jaguar Land Rover, and Mini. According to the Society of Motor Manufacturers and Traders, the UK automotive sector contributes significantly to the economy, with a strategic focus on zero emission and connected technologies. The government has established multiple testbeds for connected and autonomous vehicles to trial real world applications. British universities lead in artificial intelligence and machine learning research, providing the intellectual capital necessary for advanced software development. The insurance industry in the UK is pioneering usage-based models that rely on connected vehicle data, creating a unique demand driver. Consumers in the UK are early adopters of telematics, with high penetration rates in both personal and commercial fleets. The commitment to achieving net zero emissions by 2050 accelerates the shift toward connected electric vehicles. Strong collaboration between the public and private sectors ensures that regulatory hurdles are addressed swiftly.

Italy Connected Vehicle Market Analysis

Italy is predicted to exhibit a healthy CAGR in the European connected vehicle market during the forecast period due to a strong design led approach to connectivity and a growing focus on smart manufacturing. The Italian automotive sector, anchored by Stellantis, is rapidly transforming its portfolio to include advanced connected features. According to Confindustria, there is a concerted effort to digitize the supply chain and integrate Internet of Things technologies into vehicle production. The country's unique urban landscapes, with many historic cities restricting traffic, create a specific demand for connected solutions that manage access and optimize last mile delivery. Italian consumers place a high value on design and user experience, pushing manufacturers to create intuitive and aesthetically pleasing infotainment interfaces. Government incentives for purchasing low emission connected vehicles have stimulated market activity, particularly in urban centers. The presence of leading telecommunications providers ensures improving network infrastructure to support these services. Collaboration between Italian design houses and tech firms results in distinctive connected car interiors that appeal to global markets.

Sweden Connected Vehicle Market Analysis

Sweden is projected to witness a notable CAGR in the European connected vehicle market during the forecast period due to its exceptional digital infrastructure and leadership in safety and sustainability. Home to Volvo Cars and Volvo Group, Sweden has long been a pioneer in vehicle safety, and this ethos extends naturally to connected vehicle technologies. According to the Swedish Transport Administration, the country aims to achieve zero traffic fatalities by 2030, a goal that drives the rapid deployment of vehicle to infrastructure and vehicle to vehicle systems. Sweden boasts some of the highest internet penetration rates globally, providing a strong foundation for connected services. The government actively supports test sites such as AstaZero, a full-scale urban environment for testing autonomous and connected vehicles under controlled conditions. Swedish consumers are highly environmentally aware, leading to strong sales of connected electric vehicles that offer grid integration and carbon footprint tracking. The collaborative culture between academia, industry, and government facilitates rapid prototyping and deployment of new ideas. Stockholm and Gothenburg serve as living labs where connected mobility solutions are tested in real traffic. The emphasis on open data standards encourages innovation from third party developers.

COMPETITIVE LANDSCAPE

The competition in the Europe Connected Vehicle Market is characterized by intense rivalry between traditional automotive manufacturers and emerging technology companies. Established car makers leverage their deep engineering expertise and extensive supply chains to integrate connectivity into mass production vehicles efficiently. Meanwhile tech giants enter the fray by offering superior software platforms and data analytics capabilities that appeal to modern consumers. This dynamic creates a hybrid landscape where collaboration often coexists with competition as各方 seek to combine hardware prowess with digital innovation. Regulatory pressures regarding data privacy and cybersecurity further complicate the competitive environment by imposing strict compliance requirements on all participants. Companies must continuously innovate to differentiate their offerings through unique user experiences and reliable service ecosystems. The race to dominate the software defined vehicle era drives substantial investment in research and development across the sector. Success depends on the ability to scale digital services rapidly while maintaining high standards of safety and performance for users.

KEY MARKET PLAYERS

These are the market players that are dominating the Europe connected vehicle market.

- Robert Bosch GmbH

- Continental AG

- BMW Group

- Mercedes Benz Group

- Volkswagen Group

- Denso Corporation

- Visteon Corporation

- Harman International

- AT&T Inc.

- TomTom N.V.

- Airbiquity Inc.

- Qualcomm Technologies Inc.

- Sierra Wireless

- Infineon Technologies

- Magna International

- ZF Friedrichshafen AG

Top Players In The Market

- Volkswagen Group stands as a pivotal force in the European connected vehicle landscape through its ambitious software transformation strategy. The company established Cariad as a dedicated software subsidiary to develop a unified operating system across all its brands including Audi and Porsche. This strategic move aims to standardize connectivity features and enable over the air updates for millions of vehicles. Recent actions include partnerships with Qualcomm to integrate advanced Snapdragon digital chassis solutions into future electric models. The group focuses heavily on vehicle to grid integration and autonomous driving capabilities to enhance user experience. By investing billions in digital infrastructure Volkswagen ensures its fleet remains competitive against tech entrants. Their commitment to open standards facilitates broader ecosystem integration and strengthens their global influence in smart mobility solutions.

- BMW Group drives innovation in the connected vehicle sector by prioritizing personalized digital experiences and seamless integration with user lifestyles. The company recently launched its latest iDrive system which features advanced voice assistance and augmented reality navigation to redefine driver interaction. BMW actively collaborates with technology giants like Microsoft to leverage cloud computing for data analytics and predictive maintenance services. Their strategy emphasizes sustainability through connected charging solutions that optimize energy usage for electric vehicles. The group continuously expands its digital services portfolio to include remote software upgrades and third party app integration. By focusing on premium connectivity features BMW maintains a strong reputation for quality and innovation. These efforts solidify their position as a leader in high end connected mobility across global markets.

- Mercedes Benz Group leads the market by integrating luxury with cutting edge connectivity through its proprietary MBUX operating system. The company recently enhanced its voice control capabilities using artificial intelligence to offer more natural and intuitive interactions for drivers. Mercedes Benz focuses on creating a holistic digital ecosystem that connects vehicles with home devices and personal smartphones seamlessly. Strategic partnerships with NVIDIA enable the deployment of powerful onboard computers that support advanced autonomous driving functions. The group invests heavily in cybersecurity measures to protect user data and ensure safe operation of connected features. Their commitment to software defined vehicles allows for continuous improvement and feature addition throughout the vehicle lifecycle. This approach reinforces their status as a pioneer in premium connected automotive technology worldwide.

Top Strategies Used by Key Market Participants

Key players in the Europe Connected Vehicle Market primarily employ strategic partnerships and collaborations to accelerate technology development and reduce time to market. Companies frequently join forces with telecommunications providers to ensure robust fifth generation network coverage for real time data transmission. Another prevalent strategy involves significant investment in internal software divisions to gain control over core operating systems and reduce dependency on external suppliers. Mergers and acquisitions allow established automakers to absorb innovative startups specializing in artificial intelligence and cybersecurity solutions. Organizations also focus on developing open platform architectures to encourage third party developers to create diverse applications for their vehicles. Standardization efforts play a crucial role as industry leaders work together to define universal communication protocols. These combined approaches enable participants to navigate complex regulatory environments while delivering advanced connected services to consumers.

MARKET SEGMENTATION

This research report on the Europe connected vehicle market is segmented and sub-segmented into the following categories.

By Application

- Driver Assistance

- Telematics

- Infotainment

- Mobility management

By Technology

- 5G

- 4G

- 3G

- 2G

By Connectivity

- Integrated

- Embedded

- Tethered

By Vehicle

- Passenger Cars

- Commercial Vehicle

By Communication Type

- Vehicle to Vehicle (V2V)

- Vehicle To Pedestrian (V2P)

- Vehicle to Infrastructure (V2I)

By Country

- UK

- Russia

- Germany

- Italy

- France

- Spain

- Sweden

- Denmark

- Poland

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What defines a connected vehicle in today’s automotive landscape?

A connected vehicle uses internet and communication technologies to exchange data with other systems and devices.

Which features rely most heavily on vehicle connectivity?

Navigation updates, remote diagnostics, infotainment services, and real-time traffic alerts depend on connectivity.

What factors are encouraging connected vehicle adoption in Europe?

Advances in mobile networks and growing demand for digital driving experiences.

Which technologies enable vehicles to communicate with external systems?

Cellular networks, GPS, onboard sensors, and cloud-based platforms support connected vehicle functions.

What role does connectivity play in improving road safety?

Real-time alerts can warn drivers about hazards, traffic congestion, or nearby vehicles.

Which industries collaborate to develop connected vehicle ecosystems?

Automakers, telecom providers, and software companies work together to build integrated solutions.

What advantage do connected vehicles offer for maintenance management?

Remote diagnostics allow early detection of mechanical issues.

Which services benefit from vehicle connectivity in fleet operations?

Tracking, route optimization, and fuel monitoring become easier with connected systems.

What impact does 5G technology have on connected vehicle capabilities?

Faster data exchange enables more advanced communication between vehicles and infrastructure.

Which security considerations are important for connected vehicles?

Cybersecurity measures are required to protect vehicle systems and user data.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com