Europe Consumer Electronics Market Size, Share, Trends & Growth Forecast Report by Sales Channel, Product, and Country (Germany, UK, France, Italy, Rest of Europe) – Industry Analysis from 2026 to 2034.

Market Size, 2025

$383.51 BnMarket Estimate, 2026

$407.94 BnMarket Forecast, 2034

$668.57 BnCAGR, 2026–2034

6.37%Europe Consumer Electronics Market Report Summary

The Europe consumer electronics market was valued at USD 383.51 billion in 2025 and is projected to grow from USD 407.94 billion in 2026 to USD 668.57 billion by 2034, registering a CAGR of 6.37% from 2026 to 2034. Market growth is driven by increasing consumer demand for smart devices, rising adoption of connected home technologies, and continuous advancements in artificial intelligence and IoT-enabled electronics. The growing popularity of smartphones, wearable devices, smart appliances, and entertainment systems is further accelerating market expansion across Europe. Additionally, increasing focus on sustainability, energy-efficient electronics, and circular economy initiatives is shaping the future of the regional consumer electronics industry.

Key Market Trends

- Rising adoption of smart home and connected consumer devices.

- Increasing integration of AI-powered and IoT-enabled electronics.

- Growing consumer preference for premium smartphones and wearable technologies.

- Expansion of sustainable electronics and right-to-repair initiatives across Europe.

- Continuous advancements in smart entertainment systems and energy-efficient appliances.

Segmental Insights

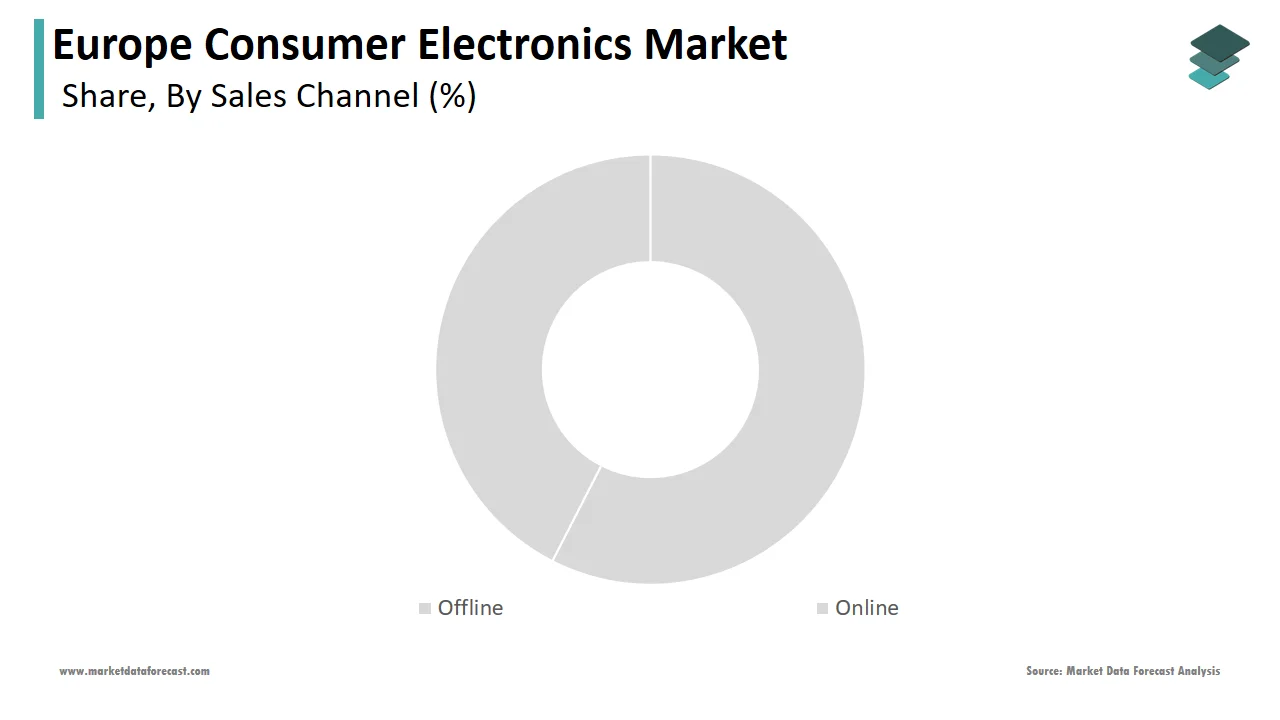

- Based on sales channel, the offline segment dominated the Europe consumer electronics market in 2025 by accounting for 54.5% market share, driven by strong consumer preference for in-store product demonstrations, personalized purchasing experiences, and established retail networks.

- Based on product, the smartphones segment led the market by capturing 52.6% share in 2025, supported by rising smartphone penetration, continuous technological innovation, and growing demand for advanced mobile connectivity features.

Regional Insights

The global consumer electronics industry is witnessing rapid technological transformation across major regions, supported by increasing smart device adoption and digital lifestyle integration.

- Asia-Pacific continues to strengthen its manufacturing dominance and is witnessing strong adoption of smart home electronics, supported by the presence of major manufacturers and expanding consumer demand across emerging economies.

- North America is expected to experience high levels of smart ecosystem integration and growing adoption of premium AI-enabled consumer electronics solutions.

- Europe is projected to expand its focus on sustainability, right-to-repair frameworks, and circular supply chain infrastructure, supporting long-term growth in environmentally responsible consumer electronics adoption.

Competitive Landscape

The Europe consumer electronics market is characterized by strong competition among global technology companies and electronics manufacturers focusing on innovation, smart connectivity, and premium user experiences. Market participants are emphasizing development of AI-enabled devices, expansion of smart ecosystem integration, and investment in sustainable manufacturing practices to strengthen market positioning. Strategic product launches, partnerships, and advancements in connected technologies are shaping competitive dynamics across the market.

Prominent companies operating in the Europe consumer electronics market include Acer Inc., Apple Inc., ASUSTeK Computer Inc., Canon Inc., Dell Technologies, Google LLC, Hewlett Packard Enterprise Development LP, HTC Corporation, Huawei Technologies Co., Ltd., Lenovo, LG Electronics, Micromax, Motorola Mobility LLC, Nikon, Panasonic Holdings Corporation, Samsung Electronics Co., Ltd., Seagate Technology LLC, Sony Corporation, Toshiba Corporation, and ZTE Corporation.

Europe Consumer Electronics Market Size

The consumer electronics market size in Europe was valued at USD 383.51 billion in 2025. The European market is estimated to be worth USD 668.57 billion by 2034 from USD 407.94 billion in 2026, growing at a CAGR of 6.37% from 2026 to 2034.

Consumer electronics encompasses devices designed for everyday personal and household use, including smartphones, wearables, home entertainment systems, and smart home infrastructure. Within the European context, this market operates against a backdrop of advanced digital adoption and stringent regulatory frameworks. According to Eurostat, 95% of households in EU cities had internet access in 2023, while 91% of rural households maintained connectivity, illustrating a narrowing digital divide that underpins device demand. As per the GSMA, Europe anticipates 533 million mobile connections by 2030, representing an 89% penetration rate across the region. Furthermore, Eurostat data indicates that 89% of individuals aged 16 to 74 in urban areas used smartphones to access the internet in 2023, compared to 82% in rural settings. The European Union has also established comprehensive sustainability regulations, with the Ecodesign for Sustainable Products Regulation covering smartphones and tablets from June 2025, as per the European Commission. These foundational elements of connectivity, device adoption, and regulatory oversight shape the operational environment for consumer electronics stakeholders across Europe without directly referencing market valuation metrics.

MARKET DRIVERS

Pervasive High Speed Connectivity Infrastructure Fuels Device Ecosystem Expansion

The proliferation of high-speed internet infrastructure across European households is majorly driving the expansion of the Europe consumer electronics market. According to Eurostat, 95% of households in EU cities maintained internet access in 2023, with 91% of rural households also connected, creating a ubiquitous foundation for smart device integration. This connectivity enables seamless operation of Internet of Things-enabled products, from voice-activated assistants to intelligent home security systems. As per the GSMA, 80% of mobile connections in Europe will utilize 5G technology by 2030, facilitating low-latency applications that demand advanced hardware capabilities. According to Eurostat, 86% of households in Europe had access to fast broadband by mid-2019, which reflects a significant expansion from earlier infrastructure baselines and accelerating consumer readiness for bandwidth-intensive electronics. This infrastructure maturity reduces friction in device onboarding and encourages replacement cycles as consumers seek products that leverage improved network performance. The convergence of fixed and mobile connectivity creates an environment where electronics manufacturers can introduce feature-rich devices with confidence that underlying network support exists. Consequently, infrastructure advancement operates as a structural demand driver independent of short-term economic fluctuations, sustaining long-term market momentum across diverse European demographics and geographies.

Regulatory Push For Sustainable Design Stimulates Innovation-Led Demand

European sustainability regulations are actively reshaping consumer electronics demand by compelling manufacturers to innovate around durability, repairability, and resource efficiency, which is further boosting the expansion of the Europe consumer electronics market. According to the European Commission, the European Union's Ecodesign requirements mandate that smartphone batteries must withstand 800 charge cycles while maintaining 80% capacity, with critical spare parts available within 5 to 10 working days for 7 years post-sales. This regulatory framework encourages consumers to view electronics as long-term investments rather than disposable commodities, elevating demand for premium devices with verified sustainability credentials. As per the European Commission, stricter collection targets and harmonised producer responsibility schemes are imminent, incentivising brands to design products with end-of-life recovery in mind. The Digital Product Passport requirement, with implementation timelines rolling out, will provide consumers with transparent lifecycle data, empowering informed purchasing decisions that favour environmentally responsible electronics. This regulatory environment transforms compliance from a cost centre into a competitive differentiator, stimulating demand for devices that demonstrably reduce carbon footprints and extend usable lifespans. Manufacturers responding with innovative circular design principles capture growing consumer segments prioritising sustainability, thereby expanding market opportunities through regulatory alignment rather than despite it.

MARKET RESTRAINTS

Persistent Supply Chain Fragility Constrains Production Scalability

European consumer electronics manufacturers face significant constraints due to persistent fragility in global semiconductor supply chains, which is hindering the growth of the Europe consumer electronics market. According to Eurostat, significant shares of digital technology components used by European firms are imported from outside the European Union, creating acute vulnerability to geopolitical disruptions and logistical bottlenecks. The ongoing geopolitical adjustments have highlighted critical choke points, disrupting key manufacturing materials essential for microchip processing. European domestic production covers only a fraction of regional semiconductor demand, limiting the industry's capacity to absorb external shocks or scale production rapidly in response to demand surges. As per the European Court of Auditors, current efforts under the European Chips Act require continuous mobilization to address global market share targets, leaving structural dependencies to be progressively managed. This supply chain exposure translates into production delays, component shortages, and elevated input costs that constrain manufacturers' ability to fulfil orders or introduce new product lines competitively. The dual-use nature of semiconductors in civilian and strategic applications further complicates procurement, as export controls and national security considerations restrict access to advanced components. Until Europe develops greater semiconductor sovereignty or diversifies its supplier base meaningfully, this structural restraint will continue to limit market growth potential and operational resilience across the consumer electronics sector.

Escalating Electronic Waste Management Costs Impede Market Fluidity

The mounting challenge of electronic waste management imposes significant operational and financial constraints on the European consumer electronics market. According to the United Nations Global E-waste Monitor, e-waste generation reached 62 million tonnes globally in 2022 and is projected to hit 82 million tonnes by 2030, growing five times faster than documented recycling capacity. As per the United Nations Global E-waste Monitor, only 22.3% of this e-waste mass was properly collected and recycled in 2022, leaving substantial environmental liabilities and resource recovery opportunities unrealised. European manufacturers face escalating extended producer responsibility obligations, requiring investment in take-back infrastructure, recycling partnerships, and compliance reporting systems that divert capital from innovation and market expansion. The European Commission indicates that upcoming regulatory updates will increase compliance burdens to enhance critical raw material recovery. As per the United Nations Global E-waste Monitor, the raw materials in global e-waste were valued at an estimated 91 billion US dollars in 2022, highlights of which are increasingly targeted through strict regulatory internalisation mechanisms. These mounting obligations constrain pricing flexibility, particularly for mid-tier and budget segment manufacturers operating on thin margins. The logistical complexity of managing end-of-life products across 27 European jurisdictions further fragments operational efficiency, creating a structural restraint that limits market fluidity and slows the pace of new product introduction across the region.

MARKET OPPORTUNITIES

Circular Economy Business Models Unlock New Revenue Streams

The transition toward circular economy principles presents a substantial opportunity for the European consumer electronics market. According to the European Commission, increasing the useful lifespan expectancy of electronic devices can mitigate a significant portion of total greenhouse gas emissions, creating compelling value propositions for refurbishment, repair, and device-as-a-service offerings. As per industry observations, companies embracing circular design principles can capture value through certified refurbishment programmes, component harvesting, and material recovery operations that appeal to environmentally conscious European consumers. The European Union's Digital Product Passport framework will enable transparent product lifecycle tracking that facilitates secondary market transactions and builds consumer trust in pre-owned electronics. This infrastructure supports business models where manufacturers retain ownership of devices and lease functionality to customers, generating recurring revenue while maintaining control over end-of-life recovery. According to environmental lifecycle assessments, the raw materials phase accounts for a substantial percentage of a typical device's carbon footprint, meaning increased recycled content represents both an environmental benefit and a cost management opportunity when supply chains stabilise. Manufacturers who invest early in circular capabilities position themselves to capture growing demand for sustainable electronics while building resilience against resource price volatility and regulatory shifts toward extended producer responsibility.

Artificial Intelligence Integration Creates Premium Differentiation Pathways

The strategic integration of artificial intelligence capabilities into consumer electronics offers European manufacturers a powerful avenue for premium product differentiation and margin enhancement, which is another prominent opportunity for the regional market. According to the GSMA, artificial intelligence transformation is a key trend shaping the mobile ecosystem in Europe, enabling personalised user experiences and predictive functionality that justify higher price points. As per Eurostat, 89% of individuals aged 16 to 74 in EU cities used smartphones to access the internet in 2023, creating a substantial installed base ready to adopt AI-enhanced devices that improve productivity, entertainment, and home automation. European consumers demonstrate willingness to pay premiums for devices offering tangible AI benefits, from advanced photography processing to intelligent energy management in smart home ecosystems. The European Union's regulatory framework for trustworthy artificial intelligence provides a compliance advantage for manufacturers who embed ethical AI principles into product design, differentiating European brands in global markets. As per the GSMA, 5G network expansion across Europe is expected to add around 164 billion euros of economic value by 2030, with AI-enabled applications representing a significant portion of this value creation. Manufacturers who successfully integrate on-device AI processing, privacy-preserving machine learning, and context-aware automation can command premium positioning while building customer loyalty through continuously improving user experiences that deepen engagement and extend replacement cycles.

MARKET CHALLENGES

Geopolitical Tensions Disrupt Critical Component Sourcing Strategies

The growing geopolitical tensions present a major challenge to the European consumer electronics market. According to international trade analysis, Europe's structural dependence on resource and chip imports from outside the European Union creates acute exposure to trade restrictions, export controls, and regional conflicts that can abruptly sever supply lines. As per regional logistical assessments, international infrastructure disruptions have already affected critical material flows essential for semiconductor manufacturing, demonstrating how regional instability can cascade into European production delays. The strategic competition between global powers introduces additional complexity, with various nations implementing legislation to regulate technology exports and promote domestic production, as per trade policy reports. European manufacturers, politically aligned with major Western partners yet economically dependent on international foundries, face difficult navigation between competing regulatory regimes that can limit access to advanced components or markets. This geopolitical fragmentation forces costly supply chain diversification efforts, duplicate inventory buffers, and complex compliance programmes that erode operational efficiency and margin performance. As per the European Court of Auditors, current European semiconductor initiatives require extended development timelines to achieve meaningful supply chain sovereignty, leaving manufacturers vulnerable to continued external disruption. Until Europe develops greater strategic autonomy in critical technology sourcing, geopolitical volatility will remain a persistent challenge, constraining planning certainty and competitive positioning across the consumer electronics sector.

Rapid Technological Obsolescence Pressures Consumer Adoption Cycles

The accelerating pace of technological innovation creates a challenging environment where consumer electronics products face shortened relevance windows that pressure both manufacturers and end users, which is further challenging the growth of the Europe consumer electronics market. According to global environmental tracking, the consumer electronics sector contributes a notable percentage of greenhouse gas emissions, a share set to grow as device shipments increase despite efforts to extend product lifespans through regulatory intervention. As per Eurostat data showing 95% of EU households had internet access in 2023, the ubiquity of connectivity enables rapid software updates and feature deployments that can render hardware capabilities outdated within short cycles. This obsolescence pressure creates a paradox where sustainability regulations encourage longer device usage while technological advancement incentivises frequent replacement to access new capabilities. European consumers face decision fatigue navigating this tension, potentially delaying purchases or opting for lower specification devices that extend usability but limit engagement with emerging applications. Manufacturers must balance innovation investment against the risk of cannibalising recent product sales, complicating roadmap planning and inventory management. According to the United Nations Global E-waste Monitor, short product lifespans exacerbate the e-waste crisis, with waste generation growing five times faster than documented recycling capacity, creating reputational and regulatory risks for brands perceived as accelerating disposable consumption patterns. This dynamic challenges the industry to develop innovation models that deliver meaningful advancement without triggering premature replacement cycles, a complex equilibrium that remains elusive in a highly competitive and fast-moving market segment.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Sales Channel, Product, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leader Profiled | Acer Inc., Apple Inc., ASUSTeK Computer Inc., Canon Inc., Dell Technologies, Google LLC, Hewlett Packard Enterprise Development LP, HTC Corporation, Huawei Technologies Co., Ltd., Lenovo, LG Electronics, Micromax, Motorola Mobility LLC, Nikon, Panasonic Holdings Corporation, Samsung Electronics Co., Ltd., Seagate Technology LLC, Sony Corporation, Toshiba Corporation, ZTE Corporation, and others. |

SEGMENTAL ANALYSIS

By Sales Channel Insights

SEGMENTAL ANALYSIS

By Sales Channel Insights

The offline segment led the market by holding 54.5% of the regional market share in 2025. The physical retail format retains its significant standing, reflecting consumer preference for tactile product evaluation, immediate possession, and personalized sales assistance when purchasing high-value electronics. As per Eurostat, 95% of households in EU cities had internet access in 2023, yet many consumers still visit physical stores to test device ergonomics, display quality, and audio performance before committing to purchase. Specialty electronics retailers provide knowledgeable staff who can explain technical specifications, compare competing models, and demonstrate ecosystem compatibility that reduces post-purchase regret. The ability to bundle devices with installation services, extended warranties, and trade-in programs creates additional value that pure play e-commerce platforms struggle to replicate. Manufacturers support offline channels through exclusive product launches, in-store demonstrations, and co-branded marketing campaigns that drive foot traffic and conversion. The experiential nature of electronics shopping, where consumers seek to validate product claims through direct interaction, ensures that physical retail remains a critical touchpoint even in an increasingly digital commerce landscape.

The Online retail segment is estimated to progress at a promising CAGR of 13.4% during the forecast period in the European market. Online retail operations continue to expand swiftly, driven by expanding internet penetration, mobile payment adoption, and logistics infrastructure that enable seamless online shopping experiences across urban and rural markets. As per Statista, consumer electronics remain significant in European e-commerce, climbing from EUR 90 billion in 2023 to an expected EUR 107 billion in 2025, reflecting strong digital channel momentum. The ability to compare specifications, read verified reviews, and access exclusive online promotions empowers consumers to make informed purchasing decisions without geographic constraints. Manufacturers leverage e-commerce platforms for direct consumer engagement, limited edition launches, and data-driven personalization that enhances conversion rates and customer lifetime value. The integration of augmented reality product visualization and virtual try-on features reduces the tactile evaluation gap that previously favored physical retail. Flexible return policies, extended warranty options, and bundled digital services further enhance the value proposition of online electronics purchases. These conveniences ensure that e-commerce continues to gain share as digital literacy improves and logistics networks expand into underserved regions.

By Product Insights

The smartphones segment dominated the market by commanding 52.6% of the regional market share in 2025. The smartphone segment maintains market leadership through the device's evolution into a multifunctional hub that consolidates communication, entertainment, productivity, and financial services. As per Eurostat, 89% of individuals aged 16 to 74 in EU cities used smartphones to access the internet in 2023, creating a vast installed base that drives accessory purchases, app ecosystem spending, and regular upgrade cycles. The integration of advanced imaging systems, biometric security, and artificial intelligence capabilities transforms smartphones into indispensable personal assistants that justify premium pricing and frequent replacement. Manufacturers leverage carrier partnerships and trade-in programs to lower entry barriers while maintaining high average selling prices through feature differentiation. The convergence of 5G connectivity and edge computing enables new use cases from augmented reality to real-time language translation that further entrench smartphone centrality in daily life. This multifaceted utility ensures sustained demand across demographic segments and geographic markets, reinforcing the segment's revenue leadership despite increasing competition from specialized wearable and home devices.

On the other hand, the wearables segment is the fastest-growing product segment in the European consumer electronics market and is estimated to register a CAGR of 16.4% during the forecast period. The wearables category experiences accelerated growth, propelled by the convergence of health consciousness, miniaturization technology, and artificial intelligence that transforms wearables from novelty gadgets into essential health monitoring tools. The integration of medical-grade sensors for electrocardiogram, blood oxygen saturation, and sleep staging enables wearables to support preventive healthcare and chronic disease management, attracting interest from insurers and healthcare providers. Manufacturers differentiate through battery life optimization, seamless smartphone synchronization, and personalized coaching algorithms that enhance user engagement and retention. The expansion of use cases into enterprise safety, industrial productivity, and elder care monitoring opens new revenue streams beyond the consumer segment. Regulatory frameworks that recognize wearable data for clinical decision making further validate the category's utility and stimulate institutional procurement. This multifaceted value proposition ensures that wearables maintain their growth leadership as technology advances and consumer expectations evolve.

REGIONAL ANALYSIS

Asia Pacific Consumer Electronics Market Analysis

The Asia Pacific region is expected to strengthen its dominant manufacturing presence and achieve continuous double-digit adoption rates in smart home electronics over the next few years. The presence of major manufacturers such as Samsung, LG, Sony, and Xiaomi creates a robust supply chain ecosystem that enables cost-effective production and rapid innovation cycles. Rising disposable incomes, urbanization trends, and expanding middle-class populations fuel demand for smartphones, wearables, and smart home devices across the region. Government initiatives promoting digital infrastructure, electronics manufacturing, and export competitiveness further strengthen the region's market position. The convergence of 5G deployment, artificial intelligence adoption, and e-commerce growth creates fertile ground for new product categories and business models. These structural advantages ensure that the Asia Pacific maintains its leadership position as the primary growth engine for the global consumer electronics industry.

North America Consumer Electronics Market Analysis

The North American region is anticipated to experience high levels of smart ecosystem integration and steady growth in premium on-device AI applications over the next few years. The presence of leading technology companies such as Apple, Google, and Amazon fosters a culture of innovation that accelerates product development and consumer adoption. High internet penetration, widespread smartphone usage, and robust e-commerce platforms enable seamless digital experiences that drive electronics consumption. Consumer preferences for premium features, ecosystem integration, and sustainable design influence global product strategies and pricing models. The region's regulatory environment, including data privacy standards and sustainability requirements, shapes industry practices and competitive dynamics. These factors ensure that North America remains a critical market for premium electronics and a testing ground for emerging technologies before global expansion.

Europe Consumer Electronics Market Analysis

The European region is projected to register an increased focus on the right-to-repair framework and expand its circular supply chain infrastructure over the next few years. The European Union's comprehensive regulations on data protection, product sustainability, and right to repair influence global manufacturer strategies and product design priorities. Consumers demonstrate a strong preference for energy-efficient devices, repairable products, and transparent supply chains that align with environmental values. High internet penetration, advanced digital infrastructure, and widespread smartphone adoption create fertile ground for smart home, wearable, and connected device ecosystems. The region's diverse linguistic and cultural landscape requires localized marketing, product adaptation, and distribution strategies that challenge global manufacturers. These dynamics ensure that Europe remains a sophisticated market that rewards innovation, sustainability, and consumer-centric design in the consumer electronics sector.

Latin America Consumer Electronics Market Analysis

The Latin American region is likely to witness progressive mid-range smartphone upgrades and gradual expansions of localized digital retail platforms over the next few years. As per GSMA reports, 5G connections in Latin America are projected to reach 62 million by 2025, featuring approximately 10% adoption rate of 5G connections and approximately 67% adoption rate of 4G connections, enabling new use cases for connected devices. Rising smartphone penetration, growing middle-class populations, and increasing internet access drive demand for affordable electronics across the region. Manufacturers adapt product portfolios to local preferences, price sensitivities, and distribution challenges that characterize Latin American markets. The expansion of e-commerce platforms, mobile payment systems, and logistics networks enhances accessibility to consumer electronics across urban and rural areas. Government initiatives promoting digital inclusion, technology education, and local manufacturing create opportunities for market growth and innovation. These factors ensure that Latin America represents a high-potential growth market for consumer electronics manufacturers willing to invest in localized strategies and long-term market development.

Middle East and Africa Consumer Electronics Market Analysis

The Middle East and Africa region is expected to accelerate its urban smart city transformations and experience rapid mobile device adoption among its youth population over the next few years. As per market observations, growing efforts from players to expand business in untapped areas are likely to support market expansion in these regions, with manufacturers launching region-specific products and marketing campaigns. Rising urbanization, improving internet connectivity, and increasing smartphone penetration drive demand for consumer electronics across major metropolitan areas. The young demographic profile, with significant populations under 30 years old, creates strong demand for mobile devices, gaming consoles, and social media-enabled technologies. Government investments in digital transformation, smart city initiatives, and technology education foster market development and consumer adoption. Manufacturers adapt to regional preferences, religious considerations, and price sensitivities through localized product features and distribution strategies. These dynamics ensure that the Middle East and Africa represent a long-term growth opportunity for consumer electronics companies willing to navigate complex market conditions and invest in sustainable market development.

COMPETITIVE LANDSCAPE

The Consumer Electronics Market features intense competition among global technology giants, regional specialists, and emerging innovators vying for consumer attention and market share. Established players leverage brand equity, distribution networks, and research capabilities to maintain leadership positions while adapting to shifting consumer preferences and regulatory requirements. New entrants challenge incumbents through disruptive business models, niche product categories, and aggressive pricing strategies that force market evolution. The convergence of hardware, software, and services creates complex competitive dynamics where ecosystem strength often outweighs individual product superiority. Manufacturers balance innovation investment with cost management to deliver compelling value across diverse price segments and geographic markets. Intellectual property portfolios, supply chain relationships, and customer data assets serve as critical competitive moats that protect market positions. The rapid pace of technological change ensures that competitive advantages remain transient, requiring continuous adaptation and strategic agility to sustain long-term success in this dynamic industry.

KEY MARKET PLAYERS

Some notable companies that dominate the Europe consumer electronics market profiled in this report are

- Acer Inc.

- Apple Inc.

- ASUSTeK Computer Inc.

- Canon Inc.

- Dell Technologies

- Google LLC

- Hewlett Packard Enterprise Development LP

- HTC Corporation

- Huawei Technologies Co., Ltd.

- Lenovo

- LG Electronics

- Micromax

- Motorola Mobility LLC

- Nikon

- Panasonic Holdings Corporation

- Samsung Electronics Co., Ltd.

- Seagate Technology LLC

- Sony Corporation

- Toshiba Corporation

- ZTE Corporation

TOP PLAYERS IN THE MARKET

- Apple Inc maintains a prominent position in the Europe consumer electronics market through its integrated ecosystem of hardware, software, and services that deliver seamless user experiences. The company's strategic focus on premium design, proprietary silicon, and privacy-centric features differentiates its products in competitive categories. Recent actions include expanding artificial intelligence capabilities across iPhone, iPad, and Mac portfolios while enhancing services revenue through Apple Music, iCloud, and Apple TV+. The company invests heavily in research and development to advance display technology, battery performance, and environmental sustainability across its product lines. Apple's retail strategy combines physical stores with online channels to provide personalized customer experiences and technical support that foster brand loyalty. The company's commitment to carbon neutrality, recycled materials, and repairability initiatives aligns with evolving consumer expectations and regulatory requirements. These strategic elements ensure Apple remains an influential force shaping innovation, pricing, and consumer preferences across the global consumer electronics landscape.

- Samsung Electronics commands significant influence in the Europe consumer electronics market through its diversified portfolio spanning smartphones, televisions, home appliances, and semiconductor components. The company's vertical integration strategy enables cost-effective production, rapid innovation cycles, and quality control across its product ecosystem. Recent actions include expanding artificial intelligence integration across Galaxy devices, launching sustainable product lines with recycled materials, and strengthening partnerships with content providers for smart TV platforms. Samsung invests in next-generation display technologies, foldable form factors, and connected home ecosystems that differentiate its offerings in competitive segments. The company's global manufacturing footprint and distribution network enable rapid market response and localized product adaptation across diverse regions. Samsung's commitment to circular economy principles, energy efficiency, and responsible sourcing aligns with regulatory trends and consumer values. These strategic initiatives ensure Samsung maintains a competitive advantage through innovation, scale, and customer-centric design across the global consumer electronics industry.

- Sony Group sustains a distinctive position in the Europe consumer electronics market through its expertise in imaging technology, audio engineering, and entertainment content integration. The company's strategic focus on premium cameras, gaming consoles, and high-fidelity audio systems appeals to enthusiasts and professionals seeking superior performance. Recent actions include advancing computational photography capabilities in Xperia smartphones, expanding PlayStation ecosystem services, and developing spatial audio technologies for immersive entertainment experiences. Sony invests in sensor innovation, artificial intelligence processing, and sustainable materials that enhance product differentiation and environmental responsibility. The company's content creation capabilities through music, film, and gaming divisions create unique synergies that enrich its hardware offerings and consumer engagement. Sony's commitment to carbon neutrality, resource efficiency, and ethical supply chains aligns with global sustainability expectations and regulatory frameworks. These strategic elements ensure Sony remains a respected innovator, shaping premium segments and enthusiast markets within the global consumer electronics industry.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Leading participants in the Consumer Electronics Market employ ecosystem integration strategies that connect devices, services, and content to enhance user retention and cross-selling opportunities. Companies invest heavily in artificial intelligence research to enable personalized experiences, predictive functionality, and automated workflows that differentiate their offerings. Sustainability initiatives focusing on recycled materials, energy efficiency, and repairability address regulatory requirements and consumer values while reducing long-term costs. Strategic partnerships with content providers, telecommunications operators, and software developers expand distribution reach and enhance product value propositions. Manufacturers leverage data analytics to understand consumer behavior, optimize product development, and personalize marketing communications that improve conversion rates. Vertical integration strategies, controlling key components, manufacturing processes, and distribution channels, enable cost advantages and quality control. These multifaceted approaches ensure market leaders maintain a competitive advantage through innovation, efficiency, and customer-centric design in the dynamic consumer electronics landscape.

MARKET SEGMENTATION

This Europe consumer electronics market research report is segmented and sub-segmented into the following categories.

By Sales Channel

- Online Retailers

- Offline Retailers

- Brand-Owned Stores

- Supermarkets/Hypermarkets

By Product

- Smartphones

- Tablets

- Desktops

- Laptops/Notebooks

- Wearable Devices

- Digital Cameras

- Hard Disk Drives

- Television

- E-readers

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe consumer electronics market?

The Europe consumer electronics market includes electronic devices designed for everyday consumer use, such as smartphones, laptops, TVs, and smart home gadgets sold across European countries.

Why is the Europe consumer electronics market growing?

The Europe consumer electronics market is growing due to rising disposable income, digital innovation, demand for smart devices, and increased adoption of connected technology among European consumers.

Who buys products from the Europe consumer electronics market?

Consumers across Europe, including individuals, families, and businesses, purchase from the Europe consumer electronics market for personal devices, home entertainment, and smart technology solutions.

What products are included in the Europe consumer electronics market?

The Europe consumer electronics market covers smartphones, laptops, tablets, TVs, audio systems, wearables, gaming consoles, smart home devices, cameras, and home entertainment systems.

How does innovation impact the Europe consumer electronics market?

Innovation drives the Europe consumer electronics market through advanced features, AI integration, connectivity improvements, sustainable designs, and next-generation consumer tech developments.

What challenges face the Europe consumer electronics market?

Challenges in the Europe consumer electronics market include supply chain disruptions, stringent regulations, environmental compliance, competition, and evolving consumer preferences.

Which countries lead the Europe consumer electronics market?

Major contributors to the Europe consumer electronics market include Germany, the United Kingdom, France, Italy, and Spain, due to strong retail networks and high consumer spending.

How does e-commerce affect the Europe consumer electronics market?

E-commerce boosts the Europe consumer electronics market by offering wider product selection, competitive pricing, convenient shopping, and faster delivery across European regions.

What role does smart home technology play in the Europe consumer electronics market?

Smart home technology is central to the Europe consumer electronics market, enabling connected devices, automation, energy efficiency, and enhanced convenience for European households.

Is the Europe consumer electronics market competitive?

The Europe consumer electronics market is highly competitive with global brands, regional players, innovation-driven pricing, and continuous product launches to capture consumer attention.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com