Europe Diabetic Foot Ulcers Market Research Report By Product Type ( Wound Dressings, Wound Care Devices ) End-User & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of EU) - Industry Analysis From 2026 to 2034

Market Size, 2025

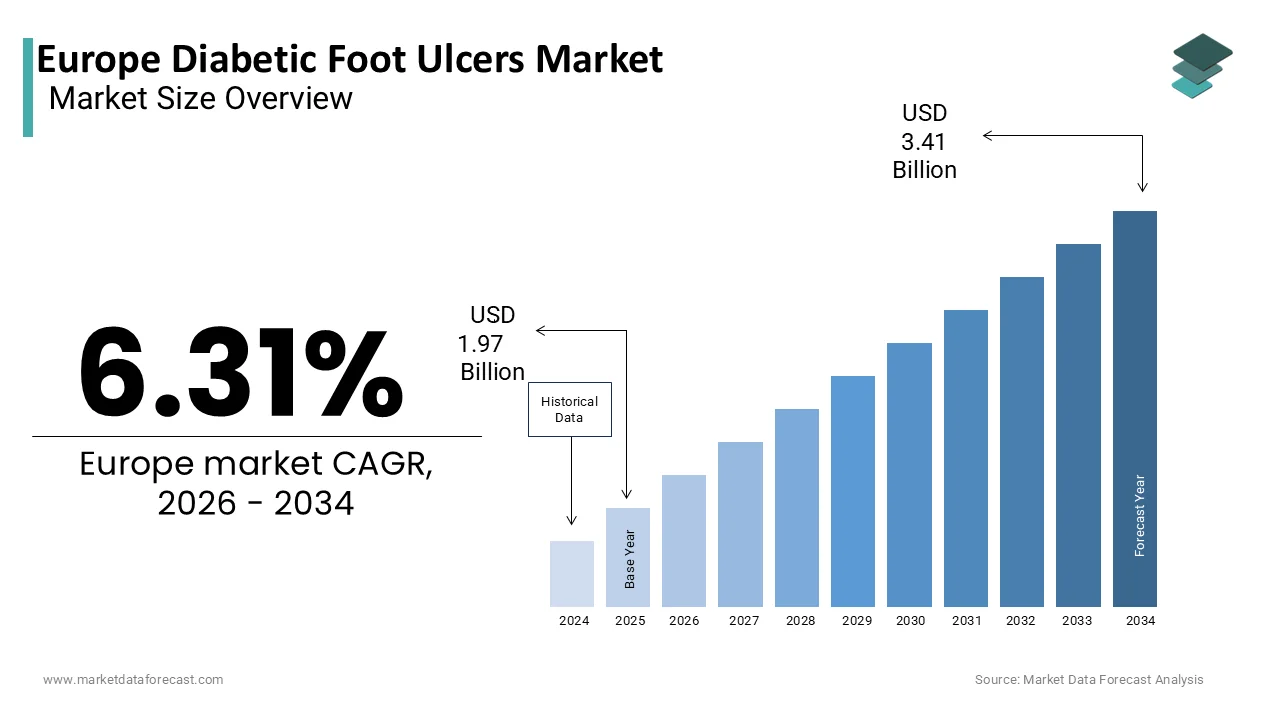

$1.97 BnMarket Estimate, 2026

$2.09 BnMarket Forecast, 2034

$3.41 BnCAGR, 2026–2034

6.31%Europe Diabetic Foot Ulcers Market Size

The Europe Diabetic Foot Ulcers Market Size was valued at USD 1.97 billion in 2025, is expected to have 6.31 % CAGR from 2026 to 2034 and be worth USD 3.41 billion by 2034 from USD 2.09 billion in 2026.

Diabetic foot ulcers (DFUs) are a severe and common complication of diabetes, resulting from prolonged hyperglycemia, peripheral neuropathy, and poor circulation. These ulcers often lead to infections, hospitalizations, and in severe cases, amputations. In Europe, the rising prevalence of diabetes, particularly Type 2 diabetes, has significantly increased the burden of DFUs on healthcare systems. According to the International Diabetes Federation, more than 60 million adults in Europe were living with diabetes in 2023 , many of whom are at risk of developing foot complications. The economic impact is substantial, with DFU-related care accounting for up to 25% of diabetes-related hospital expenditures in several countries. This has prompted health authorities across the region to focus on early detection, multidisciplinary wound care, and preventive strategies. In addition to clinical and financial burdens, lifestyle factors such as obesity, sedentary behavior, and smoking—prevalent across many European nations—further contribute to the rising incidence of DFUs. As per the World Health Organization’s Regional Office for Europe, obesity rates have nearly tripled in some EU countries since 2000 , directly correlating with the rise in diabetes and its complications. Governments and healthcare institutions are increasingly investing in advanced wound care technologies, including bioengineered skin substitutes, negative pressure wound therapy, and antimicrobial dressings, which are driving growth in the Europe diabetic foot ulcers market.

MARKET DRIVERS

Rising Prevalence of Diabetes Across the Region

One of the primary drivers of the Europe Diabetic Foot Ulcers market is the escalating prevalence of diabetes, especially among aging populations. This surge in diabetic patients significantly raises the pool of individuals at risk of developing foot ulcers due to chronic hyperglycemia, nerve damage, and impaired blood circulation. The European Centre for Disease Prevention and Control reported that Type 2 diabetes accounts for over 90% of all diagnosed cases in Europe , with increasing incidence among younger age groups due to rising obesity and sedentary lifestyles. Countries like Germany, Spain, and the UK have seen a sharp rise in diabetes-related complications, prompting greater investment in foot ulcer prevention and treatment programs. Apart from these, national health bodies such as Public Health England and the German Diabetes Society have acknowledged the growing burden of DFUs and have implemented screening initiatives and patient education campaigns.

Increasing Healthcare Expenditure and Government Support for Chronic Wound Care

Another significant driver fueling the Europe Diabetic Foot Ulcers market is the growing healthcare expenditure and increasing government initiatives aimed at improving wound care management. Many European governments have recognized the high cost of treating DFUs and have introduced policies and funding mechanisms to support early diagnosis and advanced treatment options. Several national health services have launched dedicated diabetic foot care pathways to reduce hospitalization rates and lower limb amputation risks. For instance, the National Institute for Health and Care Excellence (NICE) in the UK issued updated guidelines recommending structured foot assessments and access to multidisciplinary foot care teams. Similarly, the Swedish National Board of Health and Welfare has funded mobile wound care units to improve accessibility in rural areas.

MARKET RESTRAINTS

Limited Awareness and Delayed Diagnosis Among Patients

A major restraint affecting the Europe Diabetic Foot Ulcers market is the limited awareness and delayed diagnosis among diabetic patients, which often leads to advanced-stage ulcers requiring more intensive and costly treatments. Despite widespread healthcare infrastructure, many individuals remain unaware of the early warning signs of foot complications, delaying medical consultation until infections or severe tissue damage occur. Moreover, language barriers, lack of patient education materials, and inconsistent follow-up practices in primary care settings further exacerbate the problem. The European Society of Endocrinology highlighted that in Eastern European countries, where public health messaging is less developed, DFU-related amputation rates are significantly higher compared to Western Europe.

High Treatment Costs and Reimbursement Limitations

Another critical constraint limiting the growth of the Europe Diabetic Foot Ulcers market is the high cost of treatment and inconsistent reimbursement policies across different countries. Advanced wound care products such as bioengineered skin substitutes, negative pressure wound therapy devices, and antimicrobial dressings are often expensive, making them inaccessible to many patients without adequate insurance coverage. According to the European Observatory on Health Systems and Policies, reimbursement for DFU treatments varies widely across EU member states , with some countries offering full coverage while others provide partial or no reimbursemet. In countries like Greece and Portugal, patients frequently bear a significant portion of wound care costs out-of-pocket , discouraging adherence to prescribed treatment regimens. Additionally, the complexity of obtaining prior authorization for high-cost therapies delays timely access, particularly in publicly funded healthcare systems.

MARKET OPPORTUNITIES

Expansion of Telemedicine and Remote Wound Monitoring Solutions

An emerging opportunity shaping the future of the Europe Diabetic Foot Ulcers market is the rapid expansion of telemedicine and remote wound monitoring solutions. With advancements in digital health technologies, clinicians can now assess wound progression, monitor healing remotely, and intervene earlier to prevent complications—all without requiring frequent in-person visits. The use of smartphone-based imaging, AI-powered wound analysis, and wearable sensors is gaining traction, particularly in countries like the Netherlands and Denmark, where digital health integration is well-established. The University of Manchester’s Centre for Digital Health reported that in 2023, remote wound monitoring tools improved healing rates by 22% and reduced hospital readmissions by 30% among DFU patients. These benefits make digital wound care solutions attractive to both healthcare providers and payers seeking cost-effective ways to manage chronic wounds.

Growing Adoption of Regenerative Medicine and Bioengineered Therapies

Another promising opportunity within the Europe Diabetic Foot Ulcers market lies in the growing adoption of regenerative medicine and bioengineered therapies. Traditional wound care approaches often fail to address the complex pathophysiology of DFUs, prompting increased interest in advanced biological treatments such as stem cell therapy, growth factor application, and tissue-engineered skin substitutes. According to the European Tissue Repair Society, clinical trials involving regenerative therapies for DFUs have shown a 40–50% improvement in complete wound closure rates compared to conventional treatments . Leading research institutions in Germany and the UK are actively exploring novel cellular therapies and biomaterials designed to restore vascular function and accelerate healing. Regulatory agencies such as the European Medicines Agency have approved several advanced therapy medicinal products (ATMPs) for DFU management, encouraging pharmaceutical and biotech firms to invest in this space. Companies like OrCell and MediWound are expanding their presence in Europe, supported by favorable reimbursement policies in select markets.

MARKET CHALLENGES

Variability in Clinical Guidelines and Treatment Protocols Across Europe

A major challenge facing the Europe Diabetic Foot Ulcers market is the variability in clinical guidelines and treatment protocols across different countries. While organizations such as the International Working Group on the Diabetic Foot (IWGDF) and the European Wound Management Association have developed consensus-based recommendations, implementation remains inconsistent due to differences in healthcare structures and resource availability. According to a 2023 review published in Diabetic Medicine, only 12 out of 27 EU countries had fully adopted IWGDF guidelines into national clinical practice, with significant disparities in foot care team composition and access to advanced wound treatments. This inconsistency leads to variations in treatment efficacy and outcomes, complicating efforts to evaluate and scale best practices. Also, differing reimbursement criteria and diagnostic standards hinder cross-border collaboration and technology adoption.

Shortage of Specialized Healthcare Professionals in Wound Care

Another critical challenge influencing the Europe Diabetic Foot Ulcers market is the shortage of specialized healthcare professionals trained in wound care and diabetic foot management. Effective DFU treatment requires a multidisciplinary approach involving endocrinologists, podiatrists, vascular surgeons, and wound care nurses—many of whom are in short supply across several European countries. In rural and underserved regions, access to specialist foot care is particularly constrained, increasing the risk of infection and amputation. Addressing this workforce gap requires targeted educational reforms, expanded training programs, and incentives for healthcare professionals to specialize in diabetic wound care—steps that are still in early stages across much of the continent.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, End-User and Country. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, Germany, Italy, France, Spain, Sweden, Denmark, Poland, Switzerland, Netherlands, Rest of Europe. |

| Market Leaders Profiled | ConvaTec, Inc.; Acelity L.P. Inc.; 3M Healthcare; Coloplast Corp.; Smith & Nephew Plc |

SEGMENT ANALYSIS

By Product Type Insights

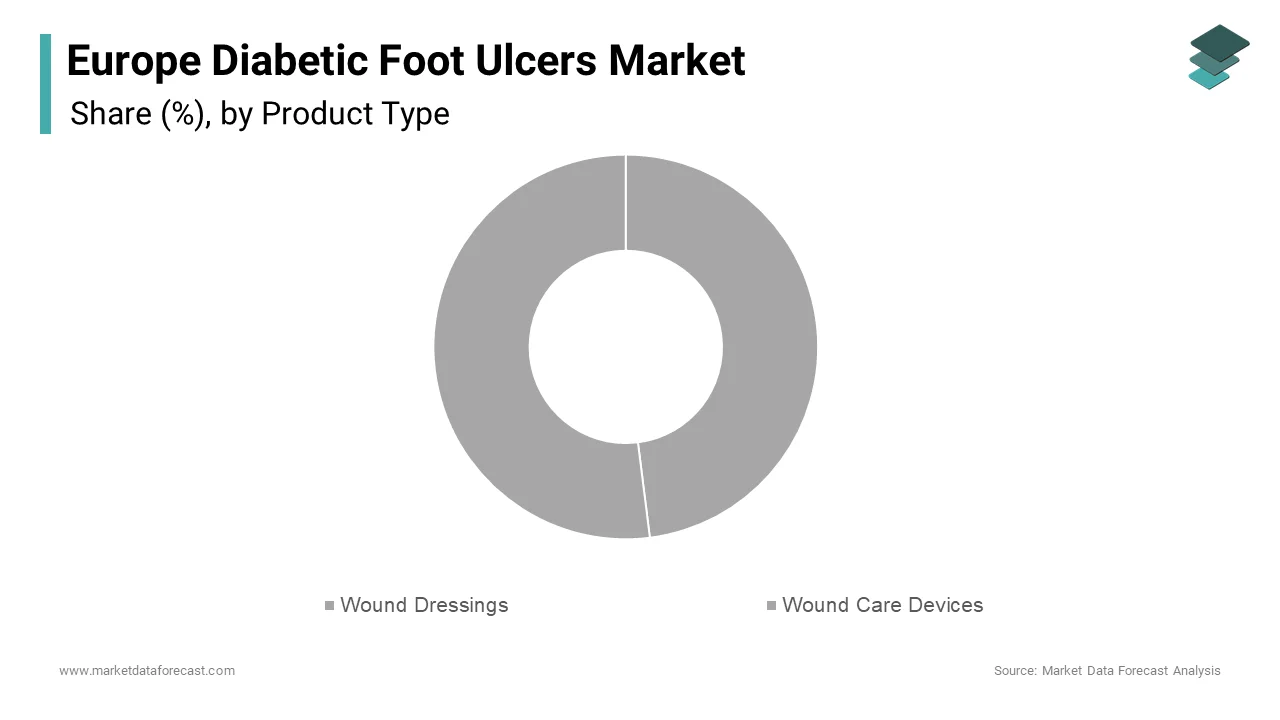

The wound dressings segment dominated the Europe diabetic foot ulcers market by capturing a 48.2% of total revenue in 2025. This leading position is primarily due to the widespread use of advanced wound care products in both hospital and outpatient settings for managing DFUs at various stages of healing. One key driver behind this segment’s dominance is the increasing adoption of silver-impregnated antimicrobial dressings , foam dressings, and hydrocolloid-based products that offer infection control, moisture management, and enhanced healing environments. Apart from these, growing awareness among clinicians about the benefits of modern dressings over traditional gauze has led to higher utilization rates.

The wound care devices segment is the quickest expanding within the Europe diabetic foot ulcers market, projected to expand at a CAGR of 9.6% between 2025 and 2033. This rapid expansion is driven by technological advancements and increasing integration of innovative devices into standard DFU treatment protocols. A key factor contributing to this segment’s momentum is the rising adoption of negative pressure wound therapy (NPWT) systems , which have demonstrated significant improvements in wound closure rates and infection prevention. According to the study, clinical trials showed that NPWT increased complete healing rates compared to conventional dressing changes alone. Moreover, portable and disposable wound care devices are gaining traction in home care settings, particularly in countries like Germany and Sweden where home-based chronic wound management is well-established.

By End-User Insights

The hospitals and clinics represented the largest end-user segment in the Europe diabetic foot ulcers market by accounting for a 67% of total market share in 2025. This influence is due to the high volume of DFU-related admissions, complex wound assessments, and the need for multidisciplinary care in institutional settings. Furthermore, national health services in countries like France and the UK emphasize structured foot care pathways within hospital departments. Besides, hospitals are equipped with specialized wound care teams, including podiatrists, vascular surgeons, and infectious disease specialists, ensuring comprehensive management of DFUs.

Ambulatory surgery centers (ASCs) are the rapidly expanding end-user segment in the Europe diabetic foot ulcers market, expanding at a CAGR of 10.2%. This progress is progressed by the increasing preference for minimally invasive procedures, shorter recovery times, and cost efficiencies associated with outpatient care. In addition, regulatory bodies such as the German Medical Association have endorsed ASCs as viable alternatives to hospital-based procedures for selected DFU cases. As healthcare providers seek to reduce hospital overcrowding and optimize resource allocation, ambulatory surgery centers are emerging as a strategic setting for DFU interventions, driving sustained market expansion in this segment.

COUNTRY LEVEL ANALYSIS

Germany held the top position in the Europe diabetic foot ulcers market by capturing a 23.1% of total regional revenue in 2025. As Europe’s most populous country and a leader in healthcare infrastructure, Germany benefits from high diabetes prevalence, robust public health initiatives, and strong investment in wound care technologies. Moreover, Germany has implemented nationwide screening programs and multidisciplinary foot care teams, particularly in university hospitals and specialized diabetes centers.

France has strong clinical infrastructure and policy support. The country's prominence is driven by its well-developed healthcare system, proactive government policies, and high patient engagement in diabetes management. The French National Agency for the Safety of Medicines and Health Products reported that diabetes affects more than 3.5 million adults in France , with DFUs accounting for a significant portion of diabetes-related hospital costs. In addition, France has been actively promoting multidisciplinary foot care through national guidelines issued by the High Authority for Health (HAS). These guidelines recommend regular foot screenings and access to podiatric services, which have contributed to improved early detection rates.

The United Kingdom has increasing focus on preventive healthcare. The National Health Service (NHS) plays a pivotal role in shaping the adoption landscape, particularly through structured diabetes foot care programs aimed at preventing amputations. NHS Digital reported in 2023 that over 135,000 people in the UK suffer from active foot ulcers , with diabetes-related foot disease costing the NHS more than £1 billion annually. The National Institute for Health and Care Excellence (NICE) has issued updated guidelines recommending immediate access to specialist foot care teams for high-risk patients. Public Health England launched a national campaign in 2023 to raise awareness about DFU prevention, targeting both healthcare professionals and diabetic patients.

Italy is seeing rising incidence of diabetes and complications. The country’s market dynamics are shaped by a rapidly aging population, increasing diabetes prevalence, and rising healthcare expenditure on chronic wound management. The Italian Society of Diabetology emphasized that amputation rates in Italy remain higher than the EU average , largely due to delayed diagnosis and limited access to specialized foot care in rural areas. Despite these challenges, several regions have introduced mobile foot care units and telemedicine-based wound monitoring to improve accessibility.

Spain’s market growth is driven by increasing diabetes prevalence, rising healthcare spending, and growing adoption of advanced wound care technologies. In response, several autonomous communities have expanded access to bioengineered skin substitutes and negative pressure wound therapy. Apart from these, Spain has been actively involved in clinical research related to DFU management. With rising healthcare investments and policy reforms, Spain is emerging as a key player in the European DFU market.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the Europe Diabetic Foot Ulcers Market are

- ConvaTec, Inc.;

- Acelity L.P. Inc.;

- 3M Healthcare;

- Coloplast Corp.;

- Smith & Nephew Plc.;

- B Braun Melsungen AG;

- Medline Industries Inc.;

- Organogenesis, Inc.;

- Molnlycke Health Care AB

- Medtronic

The competition in the Europe diabetic foot ulcers market is intense and highly fragmented, driven by the presence of well-established multinational corporations and emerging regional players. As the burden of diabetes-related complications rises, so does the demand for effective wound care solutions, prompting manufacturers to differentiate themselves through innovation, branding, and patient-centric approaches. While large global firms leverage extensive distribution networks and deep R&D resources, smaller niche players focus on specialized formulations or novel delivery mechanisms to carve out distinct market positions. The market also benefits from ongoing advancements in diagnostics, including AI-driven imaging tools and smart wound dressings, which are reshaping how DFUs are managed. Competitive pressure is further intensified by increasing regulatory scrutiny, reimbursement limitations, and the need for cost-effective therapies—factors that compel companies to continuously refine their offerings and business models. Strategic alliances, geographic expansion, and investment in digital health infrastructure are becoming essential tools for maintaining a competitive edge in this rapidly evolving landscape.

Top Players in the Market

Smith & Nephew plc

Smith & Nephew is a global leader in advanced wound care and plays a dominant role in the Europe diabetic foot ulcers market. The company offers a comprehensive portfolio of wound dressings, negative pressure wound therapy (NPWT) systems, and bioengineered skin substitutes tailored for DFU management. Its commitment to innovation and strong distribution network across European hospitals and clinics have solidified its leadership position.

Mölnlycke Health Care AB

Mölnlycke is a key player known for its high-quality wound care products designed specifically for chronic wounds, including diabetic foot ulcers. The company’s focus on antimicrobial dressings, foam dressings, and patient-centric solutions has made it a preferred choice among healthcare professionals. With a strong presence in Nordic and Western European markets, Mölnlycke continues to drive advancements in DFU treatment through research and clinical collaborations.

Coloplast A/S

Coloplast is a major contributor to the European DFU market with a robust range of wound care products and devices aimed at improving healing outcomes. The company emphasizes user-friendly design, infection prevention, and cost-effective treatment solutions. Through strategic partnerships and continuous product development, Coloplast supports both institutional and home-based DFU care, enhancing accessibility and patient adherence across the region.

Top Strategies Used by Key Market Participants

One of the major strategies employed by key players in the Europe diabetic foot ulcers market is expanding their product portfolios through acquisitions and internal R&D initiatives , enabling them to offer comprehensive wound care solutions across different severity levels of DFUs. This approach helps companies diversify risk and capture multiple market segments simultaneously.

Another prominent strategy is forming collaborations with academic institutions and clinical research organizations to accelerate the development and validation of novel wound healing technologies. These partnerships not only enhance scientific credibility but also facilitate faster regulatory approvals and improved adoption among healthcare professionals.

Lastly, enhancing patient access through digital health platforms and telemedicine integration has become critical for market leaders. By leveraging technology to support remote wound monitoring, patient education, and physician engagement, companies are strengthening their market positioning and improving long-term adherence to treatment regimens.

RECENT HAPPENINGS IN THE MARKET

- In January 2025, Smith & Nephew launched an enhanced version of its negative pressure wound therapy system in Germany and France, featuring improved portability and ease of use for home-based DFU care, aiming to increase adoption beyond hospital settings.

- In March 2025, Mölnlycke Health Care partnered with a leading European diabetes association to launch a nationwide awareness campaign in Italy focused on early detection and preventive foot care, targeting both patients and primary care providers.

- In June 2025, Coloplast introduced a new line of silver-impregnated antimicrobial dressings under its SensiCare brand in the UK, supported by clinical evidence demonstrating superior infection control in DFU patients.

- In September 2025, Urgo Medical expanded its wound care service division in Spain, offering integrated training programs for healthcare professionals on best practices in DFU management, ensuring consistent application of its advanced dressings.

- In November 2025, Medtronic initiated a multi-center clinical trial in Sweden to evaluate the efficacy of its next-generation NPWT system in accelerating DFU healing, reinforcing its scientific leadership in advanced wound care technologies.

MARKET SEGMENTATION

This research report on the europe diabetic foot ulcers market has been segmented and sub-segmented into the following categories.

By Product Type

- Wound Dressings

- Wound Care Devices

By End-User

- Hospitals and Clinics

- Ambulatory Surgery Centers

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe.

Frequently Asked Questions

Which countries in Europe have the highest demand for DFU treatment?

Germany, UK, France, Italy, and Spain lead in demand due to their high diabetic populations, advanced healthcare systems, and reimbursement support.

What types of treatments are commonly used for diabetic foot ulcers in Europe?

Advanced wound dressings (foam, hydrocolloid, alginate) Negative pressure wound therapy (NPWT) Skin grafts and biologics Antibiotic therapy Surgical debridement Hyperbaric oxygen therapy (HBOT)

What are the key drivers of growth in the Europe DFU market?

Key drivers include are Rising prevalence of diabetes Growing geriatric population Advances in wound care technologies Increased healthcare expenditure Awareness campaigns and early diagnosis

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com