Europe Digital Camera Market Size, Share, Trends & Growth Forecast Report – Segmented By Lens (Built in, Interchangeable), Product, End Use, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Digital Camera Market Report Summary

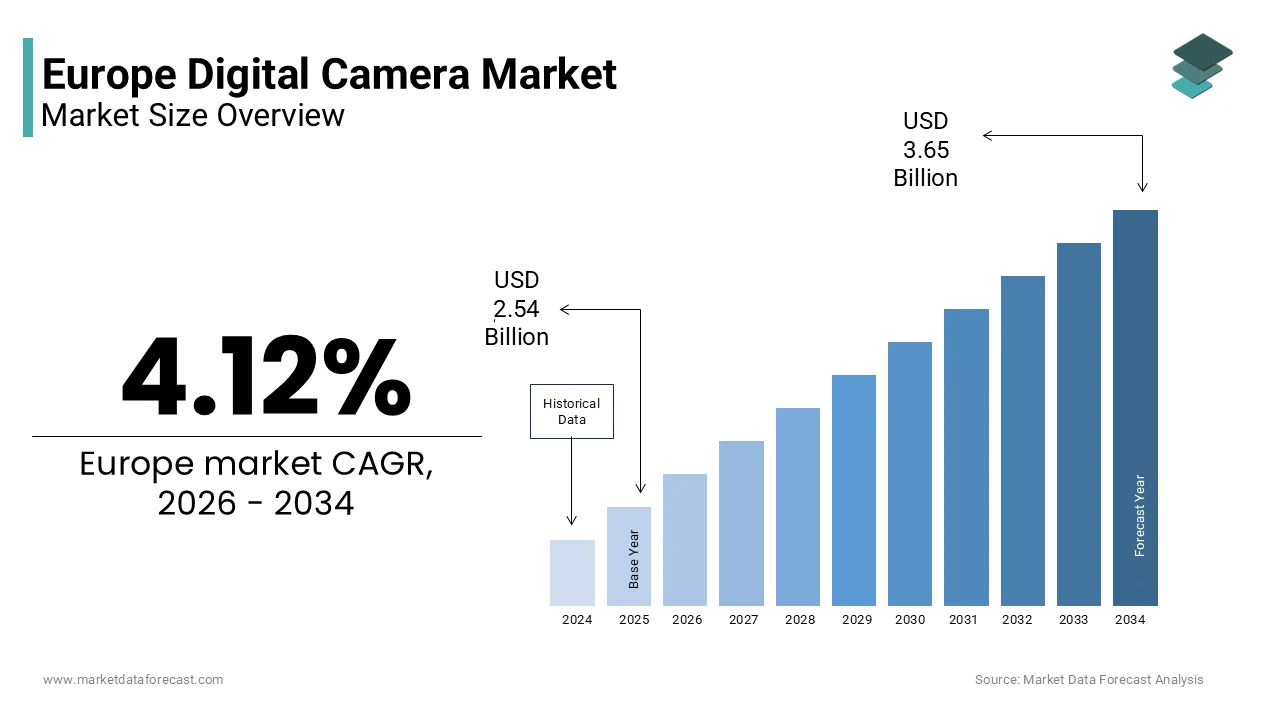

The Europe digital camera market was valued at USD 2.54 billion in 2025, is estimated to reach USD 2.64 billion in 2026, and is projected to reach USD 3.65 billion by 2034, growing at a CAGR of 4.12% during the forecast period. Market growth is driven by rising demand for high quality imaging, increasing adoption among content creators and prosumers, and growing interest in photography and videography for social media, travel, and professional use. Advancements in sensor technology, image processing, and video capabilities, along with strong demand for interchangeable lens cameras, are further supporting market expansion across Europe.

Key Market Trends

- Growing preference for interchangeable lens cameras due to superior image quality, flexibility, and advanced manual controls.

- Rising adoption of digital cameras among prosumers driven by content creation, vlogging, and semi professional photography needs.

- Increasing demand for high resolution video and low light performance supported by technological innovation.

- Continued relevance of digital cameras despite smartphone competition, especially in professional and enthusiast segments.

- Expanding online and specialty retail channels improving access to premium and niche camera models.

Segmental Insights

- Based on lens type, the interchangeable lens cameras segment dominated the Europe digital camera market in 2025.

- Based on end use, the prosumers segment led the market by capturing 52.1% share in 2025.

Regional Insights

- Germany emerged as the largest contributor to the Europe digital camera market, accounting for 24.5% share in 2025.

- The United Kingdom was the second largest country in the Europe digital camera market by capturing a 19.7% share in 2025.

Competitive Landscape

The Europe digital camera market is moderately competitive, with established global manufacturers focusing on innovation, product differentiation, and performance upgrades. Leading companies are investing in advanced sensors, mirrorless systems, and video centric features to strengthen their market position. Prominent players operating in the Europe digital camera market include BenQ Corp., Canon Inc., Eastman Kodak Co., FUJIFILM Holdings Corp., GoPro Inc., HP Inc., Konica Minolta Inc., Leica Camera AG, Nikon Corp., OM Digital Solutions Corp., Panasonic Holdings Corp., Ricoh Co. Ltd., Samsung Electronics Co. Ltd., Sharp Corp., SIGMA Corp., Sony Group Corp., and Victor Hasselblad AB.

Europe Digital Camera Market Size

The Europe digital camera market size was valued at USD 2.54 billion in 2025 and is projected to reach USD 3.65 billion by 2034 from USD 2.64 billion in 2026, growing at a CAGR of 4.12%.

A digital camera is a device that captures and stores photographs and videos using a light-sensitive electronic image sensor and digital memory, rather than traditional light-sensitive film. Unlike mobile imaging, digital cameras offer superior optical zoom, interchangeable lenses, manual controls, and larger image sensors that deliver professional grade results in low light and high motion scenarios. A substantial portion of the European population remains actively engaged in photography, maintaining demand for specialized equipment through community participation and online platforms. The European digital camera market is experiencing a significant structural transition, with consumer and professional demand strongly favoring mirrorless models over traditional DSLRs. The market is further shaped by cultural factors such as Europe’s strong heritage in visual arts, documentary photography, and analog film revival movements. Regulatory frameworks like the EU Ecodesign Directive also influence product lifecycles by mandating repairability and spare parts availability for up to seven years, reinforcing the segment’s orientation toward durability over disposability.

MARKET DRIVERS

Resurgence of Film Culture and Analog Aesthetics Fuels Enthusiast Demand

A growing cohort of European consumers, particularly among Gen Z and millennials, is embracing digital cameras as a deliberate alternative to algorithm driven smartphone photography, seeking authenticity and tactile engagement. This acts as a major accelerator of the Europe digital camera market. The trend is deeply intertwined with the global film revival. Sales of 35mm film in Europe have experienced a significant surge, indicating a growing preference among photographers for a more thoughtful and deliberate approach to capturing images. Digital cameras, especially retro styled mirrorless models from Fujifilm and Olympus, cater to this mindset by offering film simulation modes, mechanical dials, and manual focus rings that replicate analog workflows. A large segment of new camera buyers in France, influenced by a strong cultural appreciation for photography, is selecting cameras that offer manual, creative control over their images rather than relying on automatic, mobile-based solutions. Workshops on manual exposure and street photography flourish in cities like Berlin and Barcelona, creating community-driven demand. This movement reframes digital cameras not as obsolete tech but as tools for mindful creation in an age of digital saturation, sustaining a loyal enthusiast base insulated from mass market volatility.

Expansion of Content Creation Economy Drives Professional and Semi Professional Adoption

The rise of YouTube, Instagram, and TikTok has transformed visual storytelling into a viable career path, increasing demand for high-quality imaging equipment among the regional creators, which further contributes to the expansion of the Europe digital camera market. The European creator economy is experiencing rapid professionalization, leading a significant portion of creators to move beyond smartphones and invest in high-end, dedicated camera hardware to improve video production value. Mirrorless models like the Sony Alpha series and Canon EOS R5 are favored for their 4K/6K video capabilities, flip screens, and compact form factors ideal for vlogging and studio work. Driven by a robust digital creative industry, Swedish content creators are increasingly purchasing high-performance cameras, leading to significant growth in dedicated camera sales within this professional segment. Educational institutions have responded by integrating camera training into media curricula. Germany’s federal vocational schools now include digital cinematography modules using industry standard gear. This convergence of economic opportunity, platform monetization, and accessible technology positions digital cameras as essential production tools rather than mere consumer gadgets, anchoring demand in functional necessity over nostalgia.

MARKET RESTRAINTS

Smartphone Imaging Capabilities Erode Entry Level Camera Relevance

The continuous advancement of smartphone cameras has rendered basic point and shoot digital camera largely redundant for casual users, which restrains the growth of the Europe digital cameras market. Modern flagship smartphones feature computational photography, multi lens arrays, and AI enhanced processing that rival or exceed the image quality of sub €300 digital cameras in daylight conditions. The widespread adoption of mobile photography has driven a significant, long-term contraction in the global market for compact digital cameras, as consumers increasingly rely on smartphones for daily image capture. Even mid range phones now offer night mode, portrait blur, and 4K video, features once exclusive to dedicated cameras. Retailers like MediaMarkt and Fnac have reduced shelf space for entry level models, redirecting customers to premium mirrorless systems. This technological substitution compresses the market into two extremes: ultra affordable smartphones and high end interchangeable lens cameras, leaving little room for the traditional mid tier segment that once sustained volume and brand loyalty.

High Upfront Cost and Steep Learning Curve Limit Mass Accessibility

Digital cameras, particularly mirrorless and DSLR systems, require significant investment not only in the body but also in lenses, memory cards, and accessories, which creates a formidable barrier for new users and for the Europe digital camera market. Entry-level mirrorless cameras provide superior image quality at a higher investment, while smartphone photography is perceived as having no additional cost. A significant portion of potential buyers are deterred by the technical learning curve of traditional cameras, favoring the simplicity of automated smartphone photography. Unlike smartphones that automate nearly all decisions, cameras demand technical literacy that many lack time or interest to acquire. Online tutorials help but cannot replicate hands on guidance, and retail staff are often undertrained on advanced features. This knowledge gap discourages trial, especially among younger demographics accustomed to instant results. The category faces becoming an insular space for experts if it does not offer simplified entry and bundled training to attract casual consumers.

MARKET OPPORTUNITIES

Growth of Hybrid Photo Video Cameras for Independent Filmmaking

The demand for cinematic-quality video at accessible price points is driving adoption of hybrid digital cameras among European indie filmmakers, documentarians, and educators, which is likely to promote the growth of the Europe digital camera market. Models like the Panasonic Lumix GH6 and Blackmagic Pocket Cinema Camera offer 10 bit color log profiles and RAW video recording previously available only on rigs costing tens of thousands of euros. Film schools in Poland and Spain have updated curricula to include these tools, recognizing their role in democratizing production. Additionally, the rise of micro budget streaming content, fueled by platforms like MUBI and ARTE, creates professional opportunities requiring broadcast ready footage. These cameras bridge the gap between prosumer affordability and professional output, enabling creators to produce festival worthy work without studio backing. This functional repositioning transforms digital cameras from stills devices into versatile storytelling engines, opening new revenue streams beyond traditional photography.

Integration with Cloud Workflows and AI Assisted Editing Enhances Post Production Efficiency

Modern digital cameras are increasingly designed as nodes in end-to-end creative ecosystems that streamline editing and sharing, thereby paving the way for new opportunities in the Europe digital camera market. Features like built in Wi-Fi, automatic cloud backup to Adobe Creative Cloud, and AI powered in camera tagging reduce post production friction. Fujifilm’s X Series cameras, for instance, sync metadata directly to Lightroom, while Sony’s Imaging Edge software uses machine learning to suggest optimal crops and color grades. Photographers integrating AI into their workflows are significantly accelerating their editing processes while maintaining their personal artistic vision. Dutch professional photographers are increasingly prioritizing seamless camera-to-cloud workflows and cloud-based management tools as essential components of their purchasing decisions. These enhancements address a critical pain point: the time lag between capture and delivery. Embedded AI transforms cameras from static hardware into smart, agile creative tools, answering the demand for speed from both professional and social media creators.

MARKET CHALLENGES

E Waste Regulations and Limited Repair Infrastructure Increase Ownership Burden

Many digital cameras remain difficult and costly to service, despite the EU’s Right to Repair framework, due to proprietary components and scarce technician networks, which constrain the growth of the Europe digital camera market. European environmental assessments indicate that a vast majority of consumer electronics are discarded rather than fixed, driven by high labor costs and limited access to spare parts. While the EU's Ecodesign Directive mandates long-term spare part availability, these rules currently focus on mobile devices and large household appliances rather than cameras. Furthermore, high repair costs for advanced electronics often exceed the price of replacement, discouraging repairs, although new EU legislation aims to extend support and repairability for consumer electronics. Additionally, lithium ion batteries degrade over time and are rarely user replaceable, rendering otherwise functional cameras unusable. This contradiction between sustainability policy and practical reality undermines the environmental argument for durable electronics and fuels consumer skepticism. High total ownership costs, driven by a lack of modular standardization and repair, will continue to discourage eco-conscious consumers seeking durable technology alternatives.

Supply Chain Vulnerability to Semiconductor Shortages Disrupts Availability and Pricing

High susceptibility to global semiconductor constraints, particularly for image processors and sensor components sourced from a limited number of Asian foundries, limits the expansion of the Europe digital camera market. Global supply chain disruptions, involving component shortages and sensor manufacturing bottlenecks, caused inventory shortages for popular mirrorless camera models across major retailers in 2023. These supply constraints, which forced manufacturers like Sony to prioritize internal production, led to increased gray market prices as demand for high-end, in-demand models outstripped available retail supply. Unlike smartphones with diversified component sourcing, camera makers rely on custom chips with long development cycles, leaving them exposed to geopolitical and logistical shocks. This fragility erodes consumer confidence and pushes hesitant buyers toward more readily available alternatives, threatening market stability even amid strong underlying interest.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.12% |

| Segments Covered | By Lens, Product, End Use, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | BenQ Corp., Canon Inc., Eastman Kodak Co., FUJIFILM Holdings Corp., GoPro Inc., HP Inc., Konica Minolta Inc., Leica Camera AG, Nikon Corp., OM Digital Solutions Corp., Panasonic Holdings Corp., Ricoh Co. Ltd., Samsung Electronics Co. Ltd., Sharp Corp., SIGMA Corp., Sony Group Corp., and Victor Hasselblad AB |

SEGMENTAL ANALYSIS

By Lens Insights

The interchangeable lens cameras segment dominated the Europe digital camera market by accounting for a substantial share in 2025. The dominance of the interchangeable lens cameras segment is driven by superior image quality, creative flexibility, and professional adoption. Interchangeable lens systems empower users to select optics tailored to specific scenarios, wide angle for landscapes, telephoto for wildlife, macro for detail, offering unmatched creative latitude. European amateur photographers frequently invest in multiple lenses to expand their creative capabilities beyond a single kit lens. This modularity fosters long term brand loyalty, as switching ecosystems incurs significant cost. Photography students in France are increasingly adopting mirrorless systems, utilizing a variety of lenses for their educational studies. Manufacturers reinforce this through lens roadmaps. The Canon RF mount offers a comprehensive and growing range of native lenses, supporting long-term system investment. Unlike fixed lens cameras that constrain artistic expression, interchangeable systems grow with the user’s skill, transforming from entry level tools into professional rigs without replacement. This scalability makes them the rational choice for anyone committed to photography beyond casual snapshots. Videographers, photojournalists, and commercial creators depend on lens interchangeability to maintain consistent image quality across diverse shooting conditions. A wedding photographer might switch from a 35mm f1.4 for ceremonies to an 85mm f1.2 for portraits, all within the same camera body, ensuring color and sensor consistency. Professional content creators across Europe are rapidly adopting interchangeable lens camera systems, driven by the need for superior autofocus, low-light capability, and lens versatility. Major European broadcasters are prioritizing high-performance camera systems that offer extensive accessory options and reliable service support for documentary production. Rental houses in major European hubs are dominated by interchangeable lens bodies, reflecting a industry-wide standardization around flexible imaging tools. This professional entrenchment creates a self reinforcing cycle: pros demand lenses, manufacturers invest in R&D, and enthusiasts follow, cementing dominance beyond consumer trends.

The built-in lens segment is estimated to register the fastest CAGR of 5.2% between 2026 and 2034 due to niche innovation and experiential appeal. High end fixed lens cameras like the Fujifilm X100VI and Ricoh GR III are gaining traction among urban photographers seeking simplicity and discretion. These models feature large APS-C sensors, fast prime lenses, and tactile controls that encourage deliberate composition over rapid scrolling. A large portion of UK consumers are adopting digital detoxing, influencing them to purchase compact cameras to reduce their daily screen time. Driven by a desire for a "slow living" aesthetic, there is a marked increase in the purchase of high-end compact cameras throughout Sweden. These devices function as antidotes to smartphone overload, no notifications, no apps, just pure image making. Their compact size enables street photography without intimidation, appealing to creatives who value presence over productivity. Brands are carving out a sustainable niche, insulated from smartphone competition, by repositioning built-in lens cameras as philosophical objects rather than technical compromises. Modern compacts now offer features once exclusive to system cameras: 4K video, in body image stabilization, and AI powered subject recognition. The Sony RX100 VII packs a 20MP 1 inch sensor, 24–200mm zoom, and real time eye autofocus into a pocketable form, ideal for travel and vlogging. Wildlife photographers use superzoom bridge cameras like the Nikon P1000 with 125x optical reach for distant subjects without carrying heavy telephotos. These innovations transform built-in lens cameras from obsolete relics into purpose built tools for specific workflows. Targeting specific niches like travel or street photography allows the market to grow steadily, proving that relevance matters more than volume.

By End Use Insights

The prosumers segment led the Europe digital camera market by capturing a share of 52.1% in 2025. The leading position of the prosumers segment is attributed to aspirational upgraders seeking professional capabilities without full commitment, as well as educational and community infrastructure that nurtures skill development and brand loyalty. Prosumers, serious enthusiasts, semi professionals, and content creators, demand near professional performance at accessible price points. They invest in mirrorless systems with weather sealing, dual card slots, and 4K video but may not rely on photography for primary income. In Germany, vocational schools training multimedia technicians require students to purchase mid tier mirrorless kits, creating institutional demand. Brands like Sony and Fujifilm target this segment with models like the a6700 and X-S20 that offer significant portion of flagship features at half the cost. This group drives volume because they upgrade frequently as technology advances, unlike hobbyists who buy once or professionals who amortize gear over a decade. Their blend of technical literacy, disposable income, and creative ambition makes them the engine of sustainable market growth. Europe’s dense network of photography clubs, workshops, and online forums actively cultivates prosumer engagement. Online platforms like Photoclass in the Netherlands provide structured curricula using specific camera models, encouraging standardized purchases. Retailers like Foto Erhardt in Germany host weekly hands on sessions where customers test lenses and settings under expert guidance. This ecosystem reduces the learning curve and builds confidence, converting curious beginners into committed system owners. Additionally, social media groups showcase user generated content, creating peer validation that reinforces investment. Unlike hobbyists who may abandon photography after initial frustration, prosumers are supported through structured pathways that justify ongoing expenditure, ensuring consistent demand for mid tier bodies and lenses.

The hobbyist segment is anticipated to witness the fastest CAGR of 6.8% during the forecast period owing to cultural revival and accessible entry points. Young Europeans are discovering photography through retro styled digital cameras that mimic film workflows, driven by TikTok and Instagram trends celebrating grain, vignetting, and manual focus. A significant number of young adults are selecting digital cameras featuring film-emulating presets, driven by a desire for nostalgic and classic aesthetics. Moreover, due to the high popularity of street photography and the "analog revival," hobbyist camera sales in Spain, as part of the broader European market, are experiencing a consistent rise in interest for both new and vintage-style equipment. Brands respond with simplified interfaces, Olympus’ OM-D E-M10 Mark IV includes guided menus that explain aperture and shutter speed in real time. This educational layer lowers barriers while preserving authenticity, transforming hobbyists from passive smartphone users into active learners. The emotional appeal of “making” rather than “capturing” images fosters deep engagement, reversing years of decline in entry level adoption. Manufacturers now offer capable mirrorless cameras under €500, such as the Canon EOS R50 and Nikon Z30, complete with kit lenses and beginner tutorials. Bundled with free online courses from Adobe or manufacturer academies, they provide a complete learning package. In Sweden, government cultural grants for youth arts participation cover up to €300 of camera costs, as confirmed by the Swedish Arts Council. These initiatives recognize photography as a valuable creative skill, not just a hobby. Lowering financial and educational barriers turns interest into engagement, growing the enthusiast base that drives the professional market. This strategic inclusivity ensures long term market health beyond short term sales cycles.

REGIONAL ANALYSIS

Germany Digital Camera Market Analysis

Germany was the top performer in the Europe digital camera market by accounting for a 24.5% share in 2025. The country serves as both a manufacturing center, home to Leica and Zeiss, and a high volume consumption market driven by technical literacy and vocational training. German consumers prioritize build quality sensor performance and lens precision over brand hype, favoring systems with long term reliability. The federal dual education system includes numerous schools offering photographic technician programs, creating institutional demand for mid tier mirrorless kits. Retailers like Foto Erhardt provide extensive hands on testing zones and repair services, reinforcing trust in durable electronics. This blend of engineering culture educational infrastructure and after sales support makes Germany the benchmark for serious photography in continental Europe.

United Kingdom Digital Camera Market Analysis

The United Kingdom was the second largest country in the Europe digital camera market by capturing a 19.7% share in 2025. The expansion of the Uk market is credited to its world leading creative industries and digital content economy. London hosts major advertising agencies film studios and influencer networks that drive demand for high end video capable cameras. The UK creative sector remains a major source of national employment, with a significant portion of its workforce specifically engaged in the production of film, television, and professional photography. Universities like Ravensbourne and Goldsmiths integrate camera training into media degrees, producing a steady stream of skilled users. Digital content creators are increasingly investing in professional-grade camera equipment and specialized kits to differentiate their work in a highly competitive online market. Despite smartphone ubiquity, the UK maintains strong enthusiast culture. This synergy between professional necessity educational pipeline and community engagement sustains robust demand across prosumer and professional tiers.

France Digital Camera Market Analysis

France holds a notable position in the Europe digital camera market due to its deep-rooted visual arts tradition and government support for photographic culture. The French Ministry of Culture actively funds a extensive, nation-wide network of photographic galleries and local clubs that promote both analog and digital practices. High participation in photography workshops across France is fostering greater technical skill and appreciation for the medium from an early age, supported by national initiatives and cultural passes. Paris remains a global fashion and documentary hub where professionals rely on Leica and Sony systems for discreet yet high fidelity capture. Brands like Fujifilm thrive by aligning with French aesthetic sensibilities, film simulations named after Parisian neighborhoods resonate strongly. The national curriculum includes visual literacy modules in secondary schools, normalizing camera use beyond casual snaps. This institutional embedding of photography as cultural expression, not just utility, ensures consistent demand across generations and income levels.

Netherlands Digital Camera Market Analysis

The Netherlands grew steadily in the Europe digital camera market and served as a launchpad for new imaging technologies due to high digital literacy and compact creative industries. Dutch design schools emphasize visual storytelling, integrating camera training into industrial and graphic design programs. Additionally, the flat landscape and abundant natural light make it ideal for outdoor photography, fueling enthusiast activity. Retailers like BCC offer bilingual support and trade in programs that encourage upgrades. This combination of accessibility education and practical utility positions the Netherlands as a responsive and agile market for emerging camera innovations.

Sweden Digital Camera Market Analysis

Sweden is predicted to expand its share in the Europe digital camera market from 2026 to 2034. It leads in ethical consumption and slow photography movements. The country has a thriving vintage camera market, yet also adopts new mirrorless systems that emphasize longevity, Sony and Fujifilm report high retention rates among Swedish users. Government grants for youth arts participation subsidize camera purchases, as confirmed by the Swedish Arts Council. In cities like Gothenburg and Malmö, “camera walk” communities organize weekly outings to practice manual techniques, fostering peer learning. This cultural emphasis on intentionality over immediacy creates a loyal user base that values durability and creative depth, making Sweden a key indicator of post consumerist trends in the European camera market.

COMPETITIVE LANDSCAPE

The Europe digital camera market features intense yet specialized competition among Japanese manufacturers who dominate technological innovation and brand perception. Unlike commoditized electronics rivalry here centers on optical quality sensor performance and ecosystem depth rather than price alone. Canon Sony and Fujifilm lead with distinct identities—Canon excels in professional reliability Sony in video and autofocus prowess and Fujifilm in aesthetic authenticity, allowing coexistence without direct confrontation. Nikon and Panasonic hold niche positions in sports and cinema respectively while Leica commands ultra premium loyalty. New entrants face high barriers due to lens mount lock in manufacturing complexity and decades of optical R&D. Competition is further shaped by regulatory pressures including Ecodesign repairability rules and GDPR compliant software. Success depends on balancing heritage with innovation serving both aspirational hobbyists and working professionals in a market where emotional connection and technical trust outweigh fleeting trends.

KEY MARKET PLAYERS

Some of the notable key players in the Europe digital camera market are

- BenQ Corp.

- Canon Inc.

- Eastman Kodak Co.

- FUJIFILM Holdings Corp.

- GoPro Inc.

- HP Inc.

- Konica Minolta Inc.

- Leica Camera AG

- Nikon Corp.

- OM Digital Solutions Corp.

- Panasonic Holdings Corp.

- Ricoh Co. Ltd.

- Samsung Electronics Co. Ltd.

- Sharp Corp.

- SIGMA Corp.

- Sony Group Corp.

- Victor Hasselblad AB

Top Players in the Market

- Canon Inc maintains a strong presence across the Europe digital camera market through its EOS R mirrorless and PowerShot compact lines catering to professionals prosumers and hobbyists alike. The company contributes globally by pioneering RF lens mount technology and advancing hybrid photo video capabilities in accessible bodies. In Europe Canon has strengthened its position by expanding its educational outreach including free online workshops via Canon Academy tailored to German French and Spanish speaking users. It also enhanced service infrastructure by opening certified repair centers in Warsaw Prague and Lisbon to support the EU Right to Repair framework. Additionally, Canon launched firmware updates enabling AI powered subject recognition for older models extending product lifecycles and reinforcing brand loyalty among cost conscious European shooters.

- Sony Corporation is a key innovator in the Europe digital camera market with its Alpha series mirrorless cameras renowned for industry leading autofocus video performance and compact design. The company drives global standards in sensor technology supplying imaging chips to competitors while advancing its own lineup. In Europe Sony has reinforced its foothold by partnering with major rental houses in London Berlin and Amsterdam to increase accessibility for creators. It also introduced localized cloud workflows integrating Imaging Edge Mobile with European data centers to comply with GDPR. Recent initiatives include sustainability labeling on packaging detailing repairability scores and spare parts availability aligning with EU Ecodesign requirements and appealing to environmentally conscious consumers across Nordic and Benelux markets.

- Fujifilm Holdings Corporation distinguishes itself in Europe through retro styled mirrorless cameras that blend analog aesthetics with digital precision targeting enthusiasts and mindful photographers. The company contributes globally by reviving film simulation culture and promoting tactile manual controls as an antidote to smartphone automation. In Europe Fujifilm has deepened its engagement by collaborating with photography schools in Paris Barcelona and Copenhagen to integrate X Series cameras into curricula. It also expanded its second hand program offering certified refurbished units with full warranties reducing entry barriers for students and hobbyists. Furthermore, Fujifilm launched region specific film simulations inspired by European light conditions such as “Alpine Glow” and “Mediterranean Contrast” enhancing creative relevance and emotional connection with local users.

Top Strategies Used by the Key Market Participants

Key players in the Europe digital camera market are prioritizing system ecosystem development by expanding native lens lineups and accessories to lock in user loyalty and increase lifetime value. They are investing in firmware driven feature upgrades to extend product usability and support EU right to repair mandates. Companies are enhancing educational content through localized online academies workshops and school partnerships to reduce learning barriers for new users. Strategic collaborations with rental platforms and content creators improve trial and visibility among semi professional segments. Additionally they are adopting sustainable packaging repairability labeling and certified refurbished programs to align with European environmental regulations and conscious consumer values.

MARKET SEGMENTATION

This research report on the European digital camera market has been segmented and sub-segmented based on categories.

By Lens

- Built-in

- Interchangeable

By Product

- Compact Digital Camera

- DSLR

- Mirrorless

By End Use

- Pro Photographers

- Prosumers

- Hobbyists

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is a digital camera?

A digital camera is an electronic device that captures photographs and videos in digital format for storage and sharing.

2. What is the Europe digital camera market?

The Europe digital camera market includes production, distribution, and sales of digital cameras across countries such as Germany, France, the United Kingdom, and Italy.

3. What factors are driving the digital camera market in Europe?

Growth is driven by demand from professional photographers, content creators, tourism growth, and advancements in imaging technology.

4. Which countries dominate the Europe digital camera market?

Germany, the United Kingdom, France, and Italy are key markets due to strong consumer demand and professional photography communities.

5. What types of digital cameras are popular in Europe?

Popular types include DSLR cameras, mirrorless cameras, compact digital cameras, and action cameras.

6. What are the major applications of digital cameras?

Digital cameras are widely used for professional photography, videography, surveillance, media production, and personal use.

7. How do mirrorless cameras impact the Europe digital camera market?

Mirrorless cameras drive market growth due to their lightweight design, advanced autofocus, and high image quality.

8. What role does tourism play in the digital camera market?

Tourism increases demand for digital cameras as travelers seek high quality imaging devices for travel photography.

9. What challenges affect the Europe digital camera market?

Challenges include competition from smartphone cameras, high product costs, and declining demand for entry level cameras.

10. Who are the major end users of digital cameras in Europe?

Major end users include professional photographers, prosumers, hobbyists, media companies, and content creators.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com