Europe Digital Content Market Size, Share, Trends, & Growth Forecast Report, Segmented By Component, Deployment, Enterprise Size, End-User Industry, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Digital Content Market Report

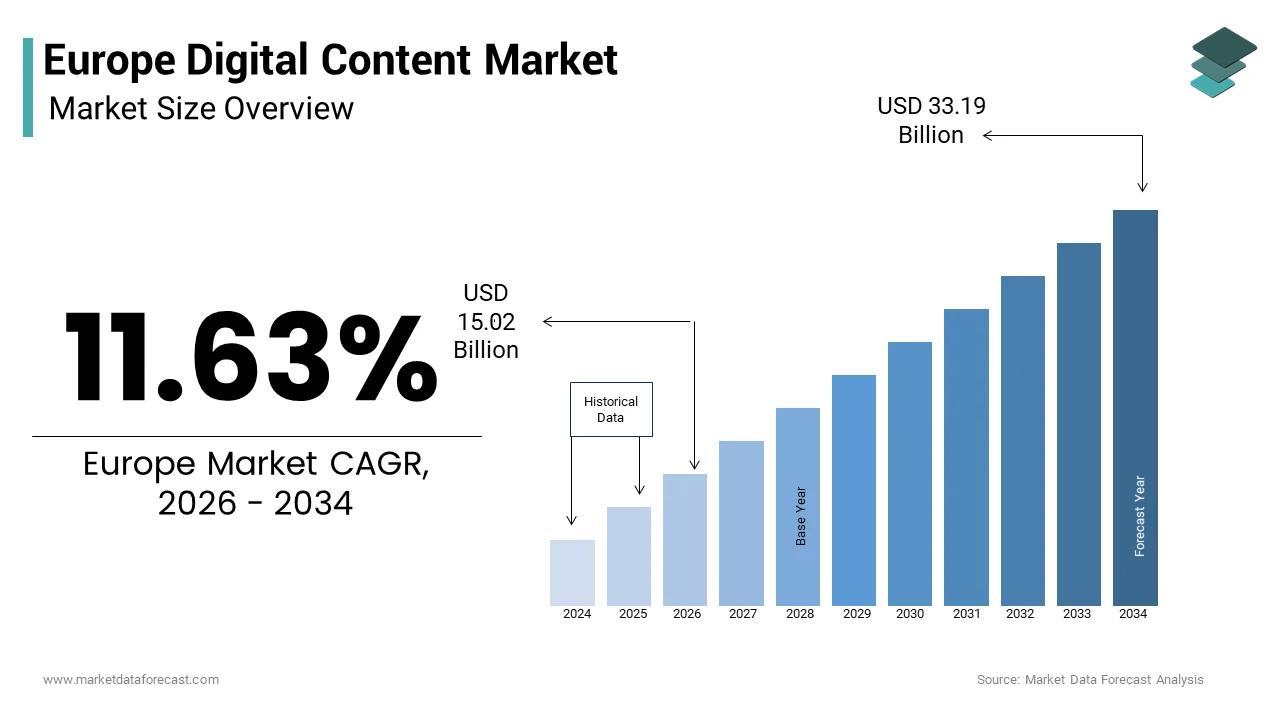

The Europe digital content market was valued at USD 13.45 billion in 2025, is projected to reach USD 15.02 billion in 2026, and is expected to grow to USD 33.19 billion by 2034, registering a strong CAGR of 11.63% during the forecast period. The market growth is driven by the rapid digital transformation across industries, increasing consumption of online media, and rising demand for content creation, management, and distribution solutions. The expansion of streaming platforms, social media, and AI-powered content tools is further accelerating market adoption across Europe.

Key Market Trends

- Growing demand for digital media and streaming content, fueled by changing consumer consumption patterns.

- Increasing adoption of cloud-based content platforms for scalability, flexibility, and cost efficiency.

- Rising use of AI and automation in content creation, editing, and personalization.

- Expansion of user-generated content and social media platforms driving content volume.

- Increasing focus on multilingual and localized content to cater to diverse European audiences.

Segmental Insights

- By component, the solutions segment dominated the market in 2025, driven by the growing need for content creation, management, and analytics tools.

- By deployment, the cloud segment held the largest share due to its advantages in accessibility, scalability, and remote collaboration.

- By enterprise size, large enterprises accounted for the dominant share, supported by higher investments in digital transformation and content strategies.

- By end-user industry, the media and entertainment segment led the market, driven by the rapid growth of OTT platforms, gaming, and digital publishing.

Regional Insights

- Germany led the Europe digital content market with a 24.1% share in 2025, supported by its strong economy and advanced digital infrastructure.

- The United Kingdom ranked second, driven by its well-established creative industries and media sector.

- France is expected to witness significant growth due to increasing digital adoption

- The Italy and Spain are projected to register healthy growth rates supported by rising digital content consumption and expanding online platforms.

Competitive Landscape

The Europe digital content market is highly competitive, with key players focusing on innovation, AI integration, and cloud-based solutions to strengthen their market position. Leading companies include Adobe Inc., Microsoft Corporation, Netflix, Apple Inc., Spotify, Canva Pty Ltd, Corel Corporation, PicsArt Inc., Acrolinx GmbH, Integra Software Services Pvt Ltd, MarketMuse Inc., Quark Software Inc., Drawtify Inc., Shutterstock Inc., Vimeo Inc., Wix.com Ltd., HubSpot Inc., Figma Inc., Descript Inc., Contentful GmbH, Bynder B.V., Notion Labs Inc., Lightricks Ltd., InVideo Inc., CapCut, Animoto Inc., Renderforest LLC, Magisto Ltd., and Biteable Pty Ltd. These players are leveraging advanced technologies, strategic partnerships, and digital platforms to expand their market presence and enhance user engagement.

Europe Digital Content Market Size

The Europe digital content market size was valued at USD 13.45 billion in 2025 and is anticipated to reach USD 15.02 billion in 2026 to reach USD 33.19 billion by 2034, growing at a CAGR of 11.63% during the forecast period from 2026 to 2034.

Digital content constitutes the vast ecosystem of intangible media assets distributed electronically across the continent, encompassing streaming video, digital music, e-books, online gaming, and interactive educational materials. This domain has transcended simple file distribution to become a sophisticated network of on-demand services driven by high-speed connectivity and cloud infrastructure. The landscape is uniquely defined by the European Union's Digital Single Market strategy, which aims to dismantle national barriers to cross-border access while enforcing strict cultural and linguistic preservation mandates. As per Eurostat, households in the European Union widely have internet access, which is creating a ubiquitous foundation for digital consumption that varies significantly between urban and rural demographics. According to the European Audiovisual Observatory, the number of video-on-demand services available in Europe has grown substantially, reflecting a hyper fragmented yet vibrant competitive environment. The market functions as a critical pillar of the modern creative economy where intellectual property rights are rigorously protected under directives like the Copyright in the Digital Single Market. This evolving definition now includes user generated content and immersive experiences such as virtual reality, which blur the lines between creator and consumer. The sector operates within a complex regulatory framework that balances the free flow of information with the protection of local cultural heritage and data privacy standards.

MARKET DRIVERS

Ubiquitous High-Speed Connectivity and Fifth Generation Network Rollout

The pervasive deployment of high-speed broadband and fifth generation mobile networks is one of the major factors driving the expansion of the European digital content market. The ability to stream ultra-high-definition video, engage in low latency cloud gaming, and download massive digital libraries instantly relies entirely on robust network infrastructure. According to the Body of European Regulators for Electronic Communications, a large majority of European households now have access to very high-capacity networks, which is a figure that continues to rise as telecom operators accelerate fiber and fifth generation deployments. As per the European Commission, fifth generation coverage now reaches a significant portion of populated areas in the Union, facilitating mobile consumption patterns that were previously impossible due to bandwidth constraints. This technological backbone allows content providers to offer richer and more immersive experiences without buffering or quality degradation, directly influencing user engagement and subscription retention. The reduction in latency is particularly crucial for emerging sectors like live sports streaming and interactive entertainment where real time interaction is paramount. As network speeds increase and costs decrease, the barrier to entry for consuming data heavy content diminishes, driving widespread adoption among all demographic segments. This infrastructure maturity ensures that the demand for premium digital content remains insatiable and continuously expanding.

Shift in Consumer Behavior Toward On-Demand and Subscription Models

The fundamental transformation in consumer preferences away from physical media and linear broadcasting toward flexible on demand and subscription-based access models is further fuelling the growth of the European digital content market. European consumers increasingly value the convenience of accessing vast libraries of content anytime and anywhere on multiple devices, a shift accelerated by the pandemic and now entrenched as the standard expectation. As per the European Audiovisual Observatory, subscription video on demand revenues have overtaken traditional box office earnings in several major European markets, which is signalling a permanent change in how audiences consume entertainment. According to the International Federation of the Phonographic Industry, paid streaming subscriptions for music in Europe have grown consistently, with users favoring unlimited access over individual track purchases. This behavioral shift is driven by the desire for personalization and control, where algorithms curate content tailored to individual tastes, enhancing user satisfaction and loyalty. The proliferation of smart televisions, tablets, and smartphones has further embedded these services into daily life, making digital content an essential utility rather than a luxury. The success of bundling strategies that combine video, music, and gaming into single packages also reinforces this trend by offering perceived value and simplicity. This enduring change in consumption habits ensures sustained growth for digital content providers who can adapt to the on-demand economy.

MARKET RESTRAINTS

Fragmentation of Licensing Rights and Geo Blocking Practices

The persistent fragmentation of intellectual property licensing rights across different European member states is impeding the regional market growth, which is preventing the realization of a truly unified digital single market and limiting consumer access to content. Content owners often sell distribution rights on a country-by-country basis due to historical language differences and varying valuation of local markets, which forces platforms to implement geo blocking measures that restrict access based on user location. According to the European Commission, many consumers in the European Union encounter geo blocking when attempting to access digital content while traveling or living in another member state. The European Audiovisual Observatory notes that the availability of films and series varies drastically between nations, with some titles accessible in one country but completely unavailable in a neighbouring state. Such restrictions frustrate consumers who expect borderless access in the digital age and hinder the scalability of European content platforms compared to global giants. Until licensing frameworks are harmonized or rights holders adopt more flexible pan European approaches, this fragmentation will continue to stifle market potential and cross border competition.

Stringent Regulatory Compliance and Content Moderation Burdens

The rigorous and often complex regulatory environment governing digital content in Europe, including the General Data Protection Regulation and the Digital Services Act, which creates substantial compliance burdens that can slow innovation and increase operational costs for providers and further hampering the growth of the European digital content market. Organizations must navigate intricate rules regarding data privacy, copyright enforcement, hate speech removal, and the protection of minors, which require significant investment in legal expertise and automated moderation technologies. As per the Centre for European Policy Studies, the cost of compliance with European digital regulations can be disproportionately high for smaller and medium sized enterprises, potentially stifling competition and consolidating market power among large incumbents. The Digital Services Act mandates rigorous risk assessments and transparency reporting for very large online platforms, forcing them to allocate vast resources to monitor and remove illegal content within strict timelines. According to European Digital Rights, the fear of hefty fines for non-compliance leads some platforms to over censor content or limit features, potentially impacting user experience and freedom of expression. The requirement to maintain data sovereignty and ensure local representation adds further layers of complexity for international players entering the European market. These regulatory hurdles act as a brake on rapid deployment and experimentation, forcing companies to prioritize compliance over agility.

MARKET OPPORTUNITIES

Expansion of Immersive Technologies and Metaverse Applications

The emergence of immersive technologies such as virtual reality, augmented reality, and the developing concept of the metaverse is a promising opportunity for the European digital content market. These technologies allow users to step inside digital environments, interact with three-dimensional content, and participate in shared virtual spaces, opening up revenue streams beyond traditional passive consumption. According to the European Virtual and Augmented Reality Association, enterprise and consumer adoption of immersive hardware in Europe is projected to grow significantly over the coming years, which is creating a hungry audience for specialized content. As per the European Commission, funding initiatives like Horizon Europe are actively supporting research and development in immersive media, which is fostering a vibrant ecosystem of startups and creators. This shift enables new applications in education, tourism, and cultural heritage where users can virtually visit museums or historical sites with unprecedented realism. The gaming industry is already leveraging these tools to create deeper engagement, and the expansion into social networking and live events offers further potential. As hardware becomes more affordable and networks faster, the demand for high quality immersive content will surge. Early movers who invest in creating compelling virtual experiences stand to capture significant market share in this nascent but rapidly evolving sector.

Growth of Local Language and Culturally Specific Content Production

The increasing demand for locally produced content in native languages offers a substantial opportunity for the European digital content market. While global blockbusters attract wide audiences, European consumers show a strong preference for stories that reflect their own cultures, histories, and social contexts, driving a renaissance in local production. As per the European Audiovisual Observatory, local language films and series often outperform international titles in domestic markets, demonstrating the enduring power of cultural relevance. According to the Creative Europe MEDIA program, investments in local content production have led to higher viewer retention and subscription loyalty for regional streaming services. This trend encourages platforms to commission original productions in diverse European languages, from Nordic noir to Mediterranean dramas, enriching the overall content landscape. The support for local creators also aligns with EU cultural policies aimed at preserving linguistic diversity and promoting European works. By focusing on hyper local storytelling and niche genres, providers can build dedicated communities that are less sensitive to price competition. This emphasis on cultural authenticity not only satisfies consumer demand but also strengthens the European digital content ecosystem against homogenization.

MARKET CHALLENGES

Prevalence of Digital Piracy and Copyright Infringement

The persistent and evolving threat of digital piracy remains a formidable challenge for the expansion of the European digital content market. Despite stringent laws and enforcement efforts, illegal streaming sites, torrent networks, and unauthorized sharing platforms continue to siphon off millions of potential subscribers and sales. According to the European Union Intellectual Property Office, piracy causes significant losses annually to the European creative industries, affecting everyone from major studios to independent artists. The ease of accessing pirated content through illicit apps and websites, often offering free access to premium material, tempts consumers especially during periods of economic pressure. As per the Alliance for Creativity and Entertainment in Europe, visits to pirate sites remain stubbornly high, with technology constantly evolving to evade detection and blocking measures. The rise of illegal IPTV services that mimic legitimate platforms further complicates the landscape, confusing consumers and eroding trust in the legal market. Combating this issue requires continuous investment in advanced anti-piracy technologies, legal actions, and public awareness campaigns, yet the cat and mouse game with infringers shows no sign of ending. This constant leakage of value forces legitimate providers to compete not just on quality but against the zero-cost alternative of piracy.

Market Saturation and Subscription Fatigue Among Consumers

The rapid proliferation of digital content services has led to a saturated market where consumers are increasingly overwhelmed by the number of subscriptions required to access their desired content, which is resulting in churn and resistance to new offerings and further challenging the regional market expansion. As major media companies launch their own standalone platforms to retain control over their libraries, users find themselves needing multiple subscriptions to watch all their favourite shows, which is leading to financial strain and decision fatigue. According to Deloitte, many European consumers have cancelled or reduced the number of streaming subscriptions they hold in the past year due to rising costs and fragmented content availability. As per PwC, the average household is unwilling to pay for more than a few services simultaneously, forcing platforms to compete fiercely for a limited share of wallet. This saturation makes customer acquisition increasingly expensive and retention difficult, as users readily switch services to chase specific hits or rotate subscriptions monthly. The pressure to produce exclusive content to justify standalone fees drives up production costs while simultaneously alienating cost conscious viewers. Balancing the need for revenue growth with the reality of consumer limits poses a strategic dilemma that threatens the long-term sustainability of the current multi-platform model.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 11.63% |

| Segments Covered | By Component, Deployment, Enterprise Size, End-User Industry, and Countries |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, & Rest of Europe |

| Market Leaders Profiled | Adobe Inc., Microsoft Corporation, Netflix, Apple Inc., Spotify, Canva Pty Ltd, Corel Corporation, PicsArt Inc., Acrolinx GmbH, Integra Software Services Pvt Ltd, MarketMuse Inc., Quark Software Inc., Drawtify Inc., Shutterstock Inc., Vimeo Inc., Wix.com Ltd., HubSpot Inc., Figma Inc., Descript Inc., Contentful GmbH, Bynder B.V., Notion Labs Inc., Lightricks Ltd., InVideo Inc., CapCut (Shenzhen Lemon Creation Technology Co., Ltd.), Animoto Inc., Renderforest LLC, Magisto Ltd., Biteable Pty Ltd. |

SEGMENTAL ANALYSIS

By Component Insights

The solutions segment dominated the market by accounting for the highest share of the European digital content market in 2025 due to the fundamental necessity for robust software platforms that enable the creation, management, distribution, and monetization of digital assets. This category includes content management systems, digital rights management tools, streaming servers, and analytics engines that form the backbone of the digital ecosystem. The urgent requirement across European media organizations to manage exponentially growing volumes of unstructured data including high resolution video, interactive graphics, and audio files efficiently is also contributing to the dominance of solutions segment in the European market. Traditional file storage methods are inadequate for the demands of modern multi-channel delivery, which is requiring sophisticated content management systems that can organize, tag, and retrieve assets instantly. According to the European Broadcasting Union, a majority of broadcasters in Europe have upgraded their core content management infrastructure in recent years to handle the transition from linear to on demand workflows. As per the International Data Corporation, spending on enterprise content management software accounts for a significant portion of total digital content budgets as organizations prioritize building a solid technological foundation before expanding services. The ability of these solutions to integrate with artificial intelligence for automated tagging and metadata generation further cements their role as indispensable tools. Furthermore, the rise of ultra-high definition and immersive formats requires solutions capable of processing massive file sizes without latency. This universal need for efficient asset governance ensures that the solutions component remains the largest revenue generator in the market landscape.

On the other hand, the services segment is emerging as the fastest growing category in the Europe digital content market and is expected to expand at a CAGR of 15.4% over the forecast period owing to the intense complexity of implementing cutting edge digital strategies and the ongoing need for specialized expertise to optimize content performance. The extraordinary difficulty and risk associated with migrating legacy media archives to modern cloud based digital ecosystems and transforming traditional broadcast operations into fully digital workflows is also aiding the growth of the services segment in this regional market. Organizations cannot simply purchase software as they require meticulous planning, data cleansing, format conversion, and workflow redesign to ensure seamless operation and compliance with new standards. According to McKinsey and Company, many European media companies rely heavily on external consultants and system integrators for their digital transformation initiatives due to the scarcity of internal skills required for such massive undertakings. As per the European Audiovisual Observatory, failed digitization projects often stem from inadequate professional services support, which is prompting companies to invest significantly more in phased implementation and testing services to mitigate risks. The customization needed to adapt global platforms to local languages, cultural nuances, and specific regulatory requirements further extends the duration and cost of service engagements. According to the statistics from the Federation of European Publishers, service costs now account for nearly half of the total expenditure in digital content modernization initiatives. As more organizations embark on these high stakes transitions, the demand for expert guidance and hands on implementation support will continue to accelerate, driving exceptional growth in the services sector.

By Deployment Insights

The cloud deployment segment held the dominant position in the Europe digital content market in 2025 by accounting for the majority of the regional market share. The growth of the cloud deployment segment in the European market can be credited to its unparalleled scalability, cost efficiency, and ability to support global distribution networks. Most modern digital content platforms are born in the cloud or have migrated there to leverage elastic resources. The overwhelming preference for Cloud deployment is also driven by the critical need for infrastructure that can scale instantly to accommodate fluctuating traffic patterns inherent in digital content consumption, such as during live sports events or prime time premieres. Traditional on premises systems often struggle to handle sudden surges in viewership without significant over provisioning, whereas cloud platforms allow resources to expand and contract automatically based on real time demand. According to the European Cloud Partnership, most major streaming services in Europe utilize cloud infrastructure to manage peak loads, ensuring uninterrupted service quality for millions of concurrent users. As per Amazon Web Services, cloud-based content delivery networks can scale capacity dramatically within minutes, a feat impossible for physical data centers. This elasticity prevents service outages and buffering issues which are primary drivers of customer churn. The ability to deploy content closer to end users through a global network of edge locations further enhances performance and reduces latency. Furthermore, the pay as you go pricing model aligns costs directly with usage, which is eliminating the financial risk of idle capacity. This operational agility and reliability solidify Cloud deployment as the prevailing model for delivering digital content across the continent.

On the other hand, the on-premises deployment segment is the fastest growing segment in the Europe digital content market and is estimated to grow at a CAGR of 13.1% over the forecast period owing to the specific sectors requiring absolute data sovereignty, ultra-low latency for production workflows, and strict regulatory control that public cloud environments cannot always guarantee. The rigorous data protection laws and regulatory expectations in Europe that mandate that certain types of sensitive content and user data remain under the direct physical and logical control of the organization are further supporting the expansion of the on-premises segment in the European market. While general consumer content thrives in the cloud, sectors like government broadcasting, defense related media, and highly regulated financial content distribution often require air gapped or strictly localized infrastructure to comply with national security mandates. According to the European Data Protection Board, many public sector broadcasters in the EU continue to host their core archival and distribution systems on premises to ensure absolute compliance with data residency laws and to avoid potential legal ambiguities associated with cross border cloud storage. As per the German Federal Office for Information Security, concerns about unauthorized access by foreign entities or cloud provider employees remain a top issue for Chief Information Officers in sensitive industries. The ability to physically isolate critical assets and enforce bespoke security protocols provides a level of assurance that public cloud environments struggle to match in the eyes of conservative regulators. This regulatory caution and the desire for complete autonomy over data governance drive aggressive investment in modernized on premises private clouds and hybrid architectures.

By Enterprise Size Insights

The large enterprises segment commanded for the largest share of the Europe digital content market in 2025 and is primarily driven by their vast content libraries, extensive customer bases, and substantial financial resources required to build and maintain sophisticated digital distribution ecosystems. This group includes major broadcasters, streaming giants, publishing houses, and music labels. The sheer scale of their operations that involves managing petabytes of digital assets and serving millions of concurrent users across multiple countries and languages. These organizations possess extensive back catalogs of movies, series, music, and books that require robust infrastructure for storage, management, and delivery, creating immense demand for enterprise grade digital content solutions. According to the European Audiovisual Observatory, the top ten media groups in Europe control over 70% of the total digital content revenue, which is reflecting their massive market footprint and investment capacity. As per the International Federation of the Phonographic Industry, major record labels and publishers account for the vast majority of licensed digital tracks and ebooks available in the region due to their ownership of valuable intellectual property rights. The need to support complex multi-channel strategies spanning linear TV, SVOD, AVOD, and social media requires integrated platforms that only large entities can afford to develop and operate. Additionally, the regulatory burden regarding copyright reporting and tax compliance across different jurisdictions necessitates advanced automated systems. This combination of volume, complexity, and systemic importance ensures that large enterprises remain the primary consumers and revenue drivers for the digital content market.

However, the small and mediumsized enterprises segment is projected to be the fastest growing category in the Europe digital content market and is estimated to grow at a CAGR of 15.7% over the forecast period. Factors such as the democratization of technology through cloud-based solutions, the increasing viability of niche content business models and the availability of affordable cloud based digital content solutions that eliminate the need for heavy upfront capital investment in hardware and software licenses are primarily propelling the growth of the small and medium-sized enterprises segment in the European market. Historically excluded from the market due to cost barriers, small studios, independent publishers, and niche streamers can now access enterprise grade features like content delivery networks, DRM, and analytics on a flexible subscription basis. According to the European Small Business Alliance, over 60% of creative SMEs have adopted cloud content management tools in the past two years to professionalize their distribution operations and compete with larger rivals. As per the OECD, the shift to operational expenditure models has lowered the barrier to entry, enabling startups and independent creators to launch platforms in days rather than months. The ease of deployment allows these businesses to set up fully functional digital storefronts rapidly, accelerating their time to value. Furthermore, the scalability of cloud solutions means SMEs only pay for what they use, allowing them to grow their capabilities in line with audience expansion without risking overinvestment. This technological leveling of the playing field unlocks a massive previously untapped market, driving exceptional growth rates.

By End User Industry Insights

The media and entertainment segment held the major share of the European digital content market in 2025 due to its core business model which revolves entirely around the creation, aggregation, and distribution of digital media assets to mass audiences. This sector includes streaming services, broadcasters, film studios, and music labels. The fundamental shift in its revenue model from physical sales and advertising supported linear broadcasting to digital subscriptions and transactional video on demand is further boosting the growth of the media and entertainment segment in the European market. For these organizations, digital content is not just a channel but the entire product, which is requiring massive investments in platforms that can deliver high quality experiences globally. According to the European Audiovisual Observatory, revenues from digital distribution now account for over 60% of total income for major European media groups, which is surpassing traditional sources. As per the International Federation of the Phonographic Industry, streaming represents 90% of recorded music revenue in Europe, forcing the entire industry to orient its operations around digital delivery infrastructure. The need to manage vast libraries of content, negotiate complex licensing deals, and analyze viewer behavior in real time drives continuous spending on advanced content management and analytics solutions. Furthermore, the intense competition among streaming services forces constant innovation in user interface and recommendation algorithms. This existential dependency on digital channels ensures that Media and Entertainment remains the largest consumer of digital content technologies.

However, the education segment is estimated to grow at a CAGR of 19.4% over the forecast period in the European market due to the permanent integration of digital learning tools into curricula, the rise of lifelong learning, and the demand for interactive and personalized educational experiences. The structural transformation of educational institutions across Europe that have permanently embedded digital content into their teaching methodologies following the pandemic accelerated shift to remote and hybrid learning is further aiding the expansion of the education segment in the European market. Schools, universities, and training centers are no longer viewing digital resources as temporary supplements but as essential components of the curriculum, driving sustained demand for learning management systems and interactive content libraries. According to the European Commission, over 80% of educational institutions in the EU have increased their budgets for digital content procurement in the last two years to support blended learning models. As per the European Schoolnet, the usage of digital textbooks and interactive simulations has tripled since 2020, with teachers increasingly relying on multimedia content to engage students. The need for accessible and inclusive content that supports diverse learning styles further accelerates adoption. Government initiatives like the Digital Education Action Plan provide funding and frameworks that encourage the widespread deployment of digital learning materials. This institutional commitment to digitalization ensures a steady and rapidly growing market for educational content providers.

COUNTRY ANALYSIS

Germany Digital Content Market Analysis

Germany captured 24.1% of the European market share in 2025 and this dominance is driven by its robust economy, high internet penetration, and strong tradition of public broadcasting transitioning to digital platforms. The German market is characterized by a dual system where powerful public broadcasters coexist with a vibrant commercial sector, both investing heavily in digital infrastructure. According to the German Federal Statistical Office, over 90% of households in Germany have broadband internet access, which is providing a solid foundation for digital content consumption. According to the data from the State Media Authorities, spending on digital media services has surpassed traditional cable TV subscriptions, marking a definitive shift in consumer behavior. Strict data privacy laws influence platform designs, which is leading to highly secure and compliant content management systems. The gaming industry also acts as a major growth engine, with Germany being one of the largest gaming markets globally. Furthermore, government initiatives in digital education and culture foster innovation, keeping Germany at the forefront of the European digital content landscape.

United Kingdom Digital Content Market Analysis

The United Kingdom secured the second largest position in 2025 due to its mature creative industries, global leadership in streaming services, and early adoption of new media formats. The UK market is defined by a highly competitive environment where global giants and local innovators drive rapid evolution in content delivery. According to Ofcom, the UK has one of the highest rates of subscription video on demand penetration globally, with most households subscribing to at least one service. Data from the British Film Institute highlights the UK’s production sector as a global powerhouse, exporting vast amounts of digital content and driving domestic investment in high-end production technologies. London serves as a hub for fintech and medtech convergence, fostering innovation in monetization and rights management. The prevalence of English language content gives UK providers a natural advantage in global expansion. Post-Brexit regulations have spurred independent standards for digital safety and content moderation. The combination of a deep talent pool, strong IP frameworks, and a culture of early adoption maintains the UK as a pivotal market for digital content growth.

France Digital Content Market Analysis

France is expected to command for a prominent share of the European digital content market during the forecast period owing to the strong government support for cultural exception policies and a thriving local production ecosystem. National regulations mandate investment in local content creation and promote French language media across digital platforms. According to the National Center for Cinema and the Moving Image, French producers are required to reinvest a portion of revenues into new productions, fueling a constant stream of high-quality digital content. Data from the Higher Council for Audiovisual Media shows record highs in consumption of local films and series on streaming platforms. France is also a leader in animation and visual effects, driving demand for advanced production tools. Paris has emerged as a hub for startup innovation in the cultural sector, attracting investment in niche streaming services and interactive storytelling. The strategic alignment of cultural protectionism with digital innovation creates a resilient market that prioritizes diversity and quality, ensuring France remains a key player in the European domain.

Italy Digital Content Market Analysis

Italy is predicted to showcase a healthy CAGR in the European digital content market over the forecast period due to its rich cultural heritage, passion for cinema and sports, and accelerating digitization of media consumption. The market is marked by a significant shift from traditional television to digital platforms, driven by improved broadband infrastructure and changing generational habits. According to the Italian Communications Authority, internet video consumption has grown by over 50% in the last three years, with younger demographics leading the charge. Data from the Italian Film Industry Association indicates a resurgence in local film production funded by digital distributors. The love for football and other sports drives massive demand for live streaming rights. The government’s National Recovery and Resilience Plan includes substantial funding for digitalizing cultural assets and promoting creative industries. This blend of historical richness with modern digital ambition positions Italy as a high-potential market for future expansion.

Spain Digital Content Market Analysis

Spain is expected to account for a notable share of the European digital content market over the forecast period. Spain is demonstrating dynamic growth fueled by its role as a global hub for Spanish language content, a thriving tourism sector, and aggressive fiber optic expansion. The market is characterized by high mobile connectivity and a young population eager to adopt new digital formats. According to the National Markets and Competition Commission, Spain boasts one of the highest fiber optic coverage rates in Europe, enabling seamless consumption of high-definition content even in rural areas. Data from the Federation of Video Game Associations reveals Spain as a top gaming market, driving demand for interactive content and cloud gaming services. The global success of Spanish series and films has boosted domestic production and investment in infrastructure. The tourism industry leverages digital content for virtual experiences and marketing, adding another layer of demand. The combination of excellent connectivity, cultural export strength, and youthful demographics ensures Spain remains a critical market for next-generation digital content solutions.

COMPETITIVE LANDSCAPE

The competition in the Europe digital content market is intensely fierce characterized by a dynamic struggle between global streaming giants specialized regional players and emerging niche platforms vying for dominance amidst strict regulatory scrutiny. Global giants leverage their vast content libraries and extensive resources to capture large audience shares while local competitors compete on cultural relevance and specialized content offerings. The battleground has shifted from mere price competition to value added services including original local productions high-definition streaming capabilities and personalized user experiences that address specific European preferences. Regulatory frameworks like the Audiovisual Media Services Directive act as both a barrier and a catalyst forcing all participants to invest in local content creation and adhere to strict data privacy standards. New entrants specializing in niche genres or interactive content are challenging established norms by offering tailored experiences that resonate with specific demographic groups. Strategic partnerships with telecom providers and hardware manufacturers have become commonplace as companies seek to secure distribution channels and reduce customer acquisition costs. This complex ecosystem ensures that no single entity can rest on its laurels as changing consumer habits and technological advancements constantly reshape the competitive hierarchy.

KEY MARKET PLAYERS

A few of the dominating players that are in the Europe digital content market are

- Adobe Inc.

- Microsoft Corporation

- Netflix

- Apple Inc.

- Spotify

- Canva Pty Ltd

- Corel Corporation

- PicsArt Inc.

- Acrolinx GmbH

- Integra Software Services Pvt Ltd

- MarketMuse Inc.

- Quark Software Inc.

- Drawtify Inc.

- Shutterstock Inc.

- Vimeo Inc.

- Wix.com Ltd.

- HubSpot Inc.

- Figma Inc.

- Descript Inc.

- Contentful GmbH

- Bynder B.V.

- Notion Labs Inc.

- Lightricks Ltd.

- InVideo Inc.

- CapCut (Shenzhen Lemon Creation Technology Co., Ltd.)

- Animoto Inc.

- Renderforest LLC

- Magisto Ltd.

- Biteable Pty Ltd

Top Players In The Market

- Netflix maintains a commanding presence in the Europe digital content market by offering a vast library of streaming video content that caters to diverse linguistic and cultural preferences across the continent. The company contributes globally by pioneering the subscription video on demand model and setting industry standards for original content production and data driven recommendation algorithms. Recent actions to strengthen its European position include significant investments in local language productions in countries like Spain, France, and Germany to attract regional audiences and comply with cultural quotas. Netflix actively partners with local telecommunications providers to bundle services and expand reach into underserved markets. The firm also invests heavily in cloud infrastructure and content delivery networks to ensure high quality streaming experiences even during peak usage times. These strategic initiatives reinforce its reputation as a leader in delivering engaging entertainment while addressing the specific regulatory and cultural needs of European viewers.

- Spotify leverages its deep expertise in audio streaming to drive widespread adoption of digital music and podcast content among European consumers seeking personalized listening experiences. The company contributes globally by democratizing access to music for artists and listeners alike through its freemium model and advanced algorithmic curation. Recent efforts involve expanding its podcast portfolio with exclusive European content and acquiring local production studios to create region specific audio programs. Spotify actively enhances its platform with high fidelity audio options and integrated lyrics features to improve user engagement. The company also collaborates with European automotive manufacturers to integrate its service directly into vehicle infotainment systems. By focusing on hyper personalization and local content discovery Spotify strengthens its market position as a preferred partner for users requiring seamless and intelligent audio solutions that align with diverse European tastes.

- Amazon Prime Video distinguishes itself in the Europe digital content market through superior integration with the broader Amazon ecosystem which empowers businesses and consumers to access premium video content alongside other digital services. Globally the company leads in providing scalable cloud-based content delivery solutions that support high-definition streaming and interactive features. Recent expansions include opening new production hubs in London and Berlin to create original local series and films that resonate with European audiences. Amazon Prime Video places a strong emphasis on leveraging artificial intelligence for content recommendation and dynamic ad insertion to maximize viewer retention. The company recently announced strategic alliances with European sports leagues to secure exclusive broadcasting rights for major events. By offering bundled subscriptions that include shipping benefits and music access Amazon Prime Video empowers organizations to optimize customer loyalty and improve retention rates. These initiatives solidify its reputation as an innovative and reliable provider in the European digital content landscape.

Top Strategies Used By The Key Market Participants

Key players in the Europe digital content market primarily employ strategies centred on local content production and strategic partnerships to navigate complex cultural and regulatory landscapes effectively. Companies are heavily investing in creating original programming in local languages to attract regional audiences and comply with European Union quotas for local content. Another prevalent strategy involves forming alliances with telecommunications operators and device manufacturers to bundle services and expand distribution channels across diverse markets. Major providers are also focusing on technological innovation by integrating artificial intelligence for personalized recommendations and advanced content delivery networks to ensure seamless streaming experiences. Sustainability initiatives serve as a critical differentiator as vendors commit to reducing the carbon footprint of their data centers and production activities to meet European Green Deal objectives. Furthermore, organizations are developing tiered pricing models and ad supported versions to capture price sensitive segments and broaden their user base. Acquisitions of independent studios and technology startups allow these giants to broaden their content libraries and offer integrated ecosystems that retain customer loyalty.

MARKET SEGMENTATION

This research report on the Europe digital content market is segmented and sub-segmented into the following categories.

By Component

- Solutions

- Services

By Deployment Mode

- Cloud

- On-Premises

By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

By Content Format

- Text and Graphics

- Video

- Audio/Podcast

- Interactive (AR/VR, 3D)

By End-user Industry

- Media and Entertainment

- Retail and E-commerce

- Healthcare and Life Sciences

- Automotive

- BFSI

- Education

- Government and Public Sector

- Manufacturing and Industrial

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

How is digital content transforming media consumption across Europe?

Digital content enables users to access entertainment, information, and education instantly through online platforms.

What factors are driving the growth of the digital content market in Europe?

Increasing internet penetration and the popularity of streaming and online platforms are key growth drivers.

Which types of digital content are widely consumed in Europe?

Video streaming, music, gaming, e-books, and online news are among the most popular content formats.

Why are consumers shifting toward digital content platforms?

They offer convenience, on-demand access, and personalized user experiences.

How do subscription-based models influence the digital content market?

They provide steady revenue for providers while offering users unlimited access to content libraries.

Which industries contribute significantly to the digital content ecosystem?

Entertainment, education, publishing, and gaming industries are major contributors.

What challenges affect the Europe digital content market?

Content piracy and regulatory compliance issues can impact market growth.

How is technology shaping digital content delivery?

Advancements in streaming technology and data analytics are improving content accessibility and personalization.

Which countries are leading in digital content consumption in Europe?

The United Kingdom, Germany, France, and Spain are key markets due to high digital adoption.

What future trend is expected in the Europe digital content market?

Growth in immersive content and AI-driven personalization is expected to drive market expansion.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com