Europe District Cooling Pipeline Network Market Size, Share, Trends & Growth Forecast Report By Type (Mobile Cranes, Fixed Cranes), End Use, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe), Industry Analysis From 2025 To 2033

Europe District Cooling Pipeline Network Market Size

The Europe district cooling pipeline network market size was calculated to be USD 1.28 billion in 2024 and is anticipated to be worth USD 1.94 billion by 2033, from USD 1.34 billion in 2025, growing at a CAGR of 4.74% during the forecast period.

The Europe district cooling pipeline network market involves centralized systems that distribute chilled water through an underground network of insulated pipes to provide efficient, large-scale cooling for commercial buildings, industrial complexes, and urban developments. Unlike conventional air conditioning systems that rely on individual units, district cooling offers a more sustainable and energy-efficient alternative by consolidating cooling generation at a central plant and distributing it across multiple consumers. This model is particularly effective in densely populated cities where space constraints and rising energy costs make decentralized cooling solutions less viable. Europe has been progressively adopting district cooling as part of its broader strategy to meet climate targets under the European Green Deal. Countries like Sweden, Denmark, and Finland have led the way, integrating surplus heat recovery and waste cold utilization into their district cooling systems to improve efficiency. Moreover, increasing urbanization and the proliferation of high-density commercial and residential developments are driving demand for integrated cooling infrastructure.

MARKET DRIVERS

Rising Urbanization and High-Density Development

One of the key drivers of the Europe district cooling pipeline network market is the rapid pace of urbanization and the corresponding rise in high-density building projects. This demographic shift is intensifying demand for space-efficient and energy-conscious infrastructure solutions, particularly in city centers where land availability is limited and traditional HVAC systems contribute significantly to heat island effects. District cooling addresses these challenges by enabling centralized cooling distribution, which reduces the need for individual chillers and rooftop cooling units. In cities like Copenhagen and Stockholm, district cooling has become integral to new urban development projects such as Norra Djurgårdsstaden and Hammarby Sjöstad, both of which prioritize sustainability and smart resource management. According to the International Energy Agency, district cooling can reduce electricity consumption for cooling compared to conventional air conditioning in dense urban settings. Furthermore, municipal planning authorities across Germany, France, and the Netherlands are incorporating district cooling mandates into zoning regulations for new commercial and mixed-use developments.

Integration of Renewable Energy and Waste Cold Recovery

A significant driver accelerating the adoption of district cooling pipeline networks in Europe is the integration of renewable energy sources and waste cold recovery mechanisms. The European Union's commitment to decarbonizing its energy system under the European Green Deal has spurred innovation in sustainable cooling technologies. According to the European Environment Agency, nearly 22% of final energy consumption in the EU is attributed to heating and cooling, making it a critical area for emissions reduction. District cooling providers are increasingly leveraging excess cold from industrial processes, seawater, or ice storage systems to supplement or replace mechanical chilling. This approach significantly reduces reliance on electric chillers and lowers operational carbon footprints. Besides, advancements in thermal energy storage and absorption cooling technologies are enabling greater use of solar thermal and biomass energy in district cooling applications. As reported by the International Renewable Energy Agency, such hybrid systems can cut primary energy consumption compared to standard electric cooling methods.

MARKET RESTRAINTS

High Initial Investment and Infrastructure Complexity

One of the primary restraints hindering the widespread expansion of the Europe district cooling pipeline network market is the substantial initial investment required for system deployment. Establishing a district cooling network involves extensive underground piping infrastructure, centralized chiller plants, control systems, and integration with existing district heating or energy grids. Moreover, the complexity of installing pipelines beneath urban environments presents logistical and regulatory hurdles. Excavation work must be coordinated with municipal utilities, transportation networks, and building codes, often leading to prolonged project timelines and increased financial risk. These economic and technical barriers deter private sector participation, particularly in regions lacking strong government subsidies or public-private partnership frameworks.

Limited Awareness and Technical Expertise

Another significant challenge impeding the growth of the Europe district cooling pipeline network market is the lack of awareness and technical expertise among stakeholders involved in urban planning, real estate development, and facility management. Unlike district heating, which has a well-established presence in Northern and Eastern Europe, district cooling remains a relatively nascent concept in many parts of the continent. According to the European Heat Pump Association, a smaller percentage of local authorities surveyed in Southern and Central Europe had incorporated district cooling into their long-term urban energy strategies. This knowledge gap extends to design engineers, architects, and construction firms who may not be familiar with the integration requirements of district cooling systems. The absence of standardized training programs and certification courses for district cooling technicians further compounds the issue. The European Building Automation and Controls Association highlights that only a small portion of HVAC professionals received formal education on centralized cooling technologies, limiting the availability of skilled labor for system installation and maintenance. As a result, potential adopters often perceive district cooling as complex, expensive, and untested—despite proven success stories in cities like Paris, Helsinki, and Amsterdam.

MARKET OPPORTUNITIES

Expansion of Smart City Initiatives and Digital Integration

A compelling opportunity emerging in the Europe district cooling pipeline network market is the expansion of smart city initiatives and the integration of digital monitoring and control technologies. Across Europe, cities are investing in intelligent infrastructure solutions that enhance energy efficiency, optimize resource utilization, and improve urban livability. According to the European Commission’s Directorate-General for Communications Networks, Content, and Technology, over 100 European cities had launched smart urban mobility and energy transition programs by the end of 2023. District cooling systems are well-positioned to benefit from these initiatives through the adoption of IoT-enabled sensors, AI-driven load forecasting, and real-time energy analytics. These technologies enable operators to dynamically adjust cooling output based on demand fluctuations, reducing energy waste and improving system longevity. In Barcelona, the implementation of a digitally managed district cooling grid reduced peak load consumption, as reported by the Spanish Association of District Heating and Cooling. Apart from these, integration with smart building management systems allows seamless coordination between district cooling networks and individual consumer usage patterns. Municipalities in Germany and the Netherlands are piloting blockchain-based energy trading platforms that allow users to monitor and trade excess cooling capacity, enhancing flexibility and cost-efficiency.

Growing Emphasis on Circular Economy and Waste Heat Utilization

An emerging opportunity in the Europe district cooling pipeline network market lies in the growing emphasis on circular economy principles and the utilization of waste heat and cold for sustainable cooling. Governments and industry leaders are increasingly recognizing the value of repurposing residual thermal energy that would otherwise be released into the environment. District cooling systems can harness this untapped potential by integrating absorption chillers that convert waste heat into cooling energy. In Rotterdam, the Eneco Cool network leverages excess heat from data centers and wastewater treatment plants to power district cooling, significantly reducing reliance on mechanical refrigeration. Similarly, in Copenhagen, surplus cold generated during district heating production is redirected to serve cooling needs, optimizing overall system efficiency. Public funding programs such as Horizon Europe and the LIFE program are supporting pilot projects that explore novel ways to integrate waste heat and cold into district cooling operations.

MARKET CHALLENGES

Regulatory Fragmentation and Policy Uncertainty

One of the foremost challenges affecting the Europe district cooling pipeline network market is the fragmented regulatory landscape and inconsistent policy support across member states. While some countries have established clear frameworks and incentives for district cooling development, others lack standardized regulations, making cross-border replication and scaling difficult. Inconsistencies in taxation policies, grid connection rules, and subsidy eligibility further complicate investment decisions. Some municipalities impose additional fees on underground infrastructure installations, discouraging developers from adopting district cooling despite its long-term benefits. Also, the absence of uniform technical standards for pipeline materials, insulation requirements, and energy metering creates inefficiencies and increases compliance burdens for operators. Policy uncertainty also arises from fluctuating government priorities, especially in regions where district cooling competes with other green initiatives for funding and legislative attention.

Competition from Decentralized Cooling Technologies

Another significant challenge confronting the Europe district cooling pipeline network market is the growing competition from decentralized cooling technologies, particularly high-efficiency air conditioning systems and localized heat pumps. Advances in variable refrigerant flow (VRF) systems, absorption chillers, and smart thermostatic controls have made standalone cooling solutions more attractive to certain commercial and residential developers. Decentralized cooling offers perceived advantages such as lower upfront costs, easier retrofitting, and greater control over individual building temperatures. Unlike district cooling, which requires long-term contractual commitments and infrastructure investments, decentralized alternatives can be deployed rapidly without the need for extensive pipeline networks. This flexibility appeals to small- and medium-sized enterprises that may lack the capital or incentive to connect to centralized systems.

Besides, misconceptions about the reliability and scalability of district cooling persist among property developers and investors unfamiliar with its benefits.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 4.74% |

| Segments Covered | By Type of Pipeline, Cooling Fluid, Application, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and Czech Republic |

| Market Leaders Profiled | Veolia, Ramboll, Alfa Laval, Siemens, Danfoss, Keppel Corporation, Engie, Vattenfall, Fortum, Logstor |

SEGMENTAL ANALYSIS

By Type of Pipeline Insights

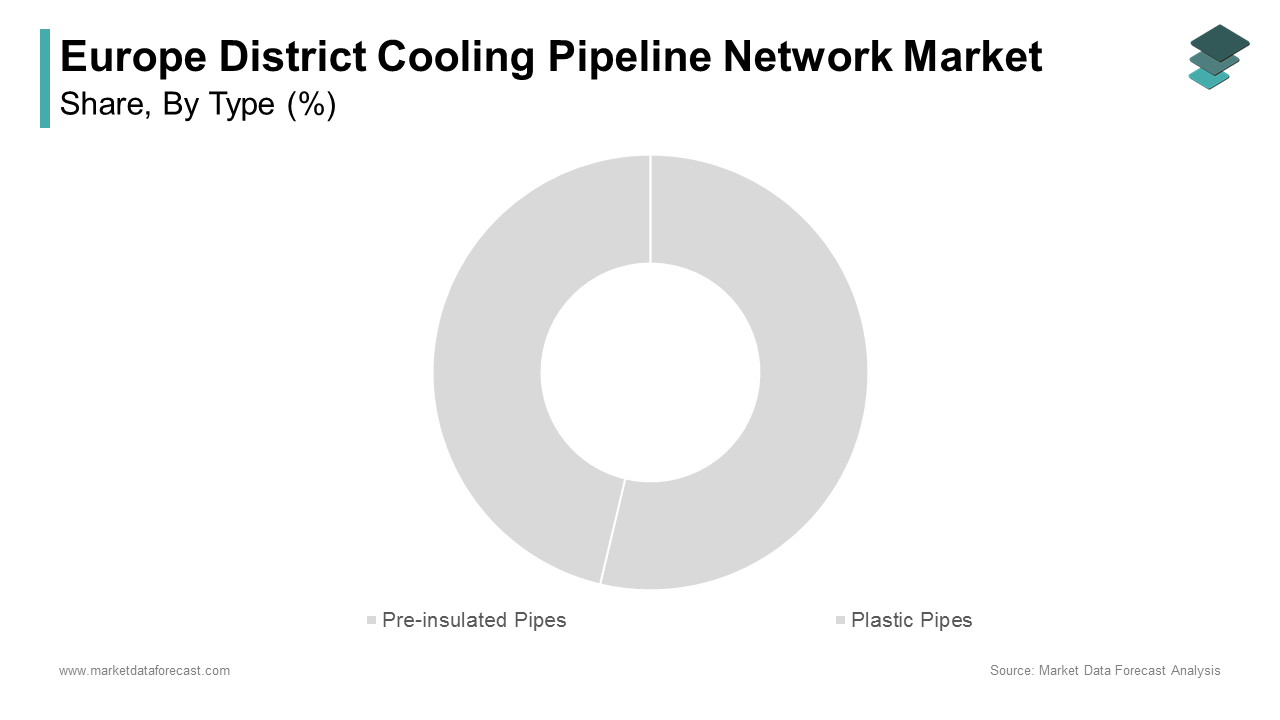

The pre-insulated pipes segment had the largest share of the Europe district cooling pipeline network market by accounting for 48.5% of total installations. These pipelines are widely adopted due to their superior thermal efficiency, durability, and ease of installation, making them ideal for underground district cooling networks where minimizing heat gain is critical. One key factor driving the dominance of pre-insulated pipes is their ability to reduce energy losses during chilled water transportation. According to the International Energy Agency, pre-insulated systems can cut thermal losses notably compared to non-insulated or loosely insulated alternatives. This efficiency is crucial in urban environments like Copenhagen and Stockholm, where district cooling networks span hundreds of kilometers and operate year-round. Also, regulatory mandates under the European Union’s Energy Performance of Buildings Directive (EPBD) encourage the use of high-performance materials in district energy infrastructure. Moreover, these pipes come with integrated leak detection systems, which enhance system reliability and reduce maintenance costs.

Among the different types, plastic pipes are emerging as the fastest-growing segment, predicted to expand at a CAGR of 9.1% through 2033. This rapid adoption is primarily driven by their lightweight nature, corrosion resistance, and cost-effectiveness, making them particularly suitable for smaller-scale and retrofitting applications. Unlike steel or copper pipes, plastic variants such as polyethylene (PE) and polypropylene (PP) do not require extensive anti-corrosion coatings, significantly lowering lifecycle maintenance costs. Another contributing factor is the growing emphasis on modular construction techniques where prefabricated components are rapidly deployed with minimal disruption. Plastic pipes are well-suited for trenchless installation methods, reducing both time and labor expenses.

By Cooling Fluid Insights

Water remained the dominant cooling fluid in the Europe district cooling pipeline network market. Its widespread adoption is attributed to its high heat capacity, availability, and cost-effectiveness, making it the most practical medium for transporting chilled energy over long distances within urban environments. One of the primary reasons for water’s dominance is its thermal efficiency. This property enhances the overall efficiency of district cooling systems, particularly in large metropolitan areas such as Stockholm, Helsinki, and Amsterdam, where centralized cooling plants serve thousands of buildings. Furthermore, water-based cooling systems benefit from established engineering standards and operational best practices, enabling seamless integration with existing district heating and renewable energy sources. Apart from these, environmental regulations favor the use of non-toxic, non-flammable fluids, positioning water as the safest and most compliant option.

On the other hand, glycol-based fluids are gaining traction at the fastest pace, estimated to grow at a CAGR of 8.4%. These fluids—primarily composed of ethylene glycol or propylene glycol —are increasingly being used in district cooling systems that require freeze protection, enhanced thermal stability, and corrosion inhibition. A major driver behind this growth is the expansion of industrial and data center cooling applications, where sub-zero temperatures and high reliability are essential. According to the European Data Centre Association, over 35 new hyperscale data centers were commissioned in Europe in 2023, many of which incorporated glycol-based cooling loops to maintain optimal server temperatures even under extreme load conditions. Additionally, glycol-based fluids offer improved compatibility with absorption chillers and ice storage systems, aligning with the increasing use of waste heat-driven cooling technologies in urban districts. Cities like Vienna and Berlin have integrated glycol into hybrid cooling networks that combine district cooling with solar-assisted refrigeration, enhancing system resilience and energy efficiency. Regulatory support for non-conductive and fire-resistant coolants in sensitive environments such as hospitals and research facilities is further boosting demand.

By Application Insights

The commercial application segment commanded the Europe district cooling pipeline network market by accounting for 45.8% of total installations in 2024. This includes office buildings, shopping malls, hotels, and business parks, where consistent and efficient cooling is essential for occupant comfort and operational efficiency. One of the main drivers behind the commercial sector’s leadership is the rapid expansion of urban business hubs, particularly in cities like London, Paris, Frankfurt, and Madrid. District cooling supports compliance with these sustainability benchmarks by offering centralized, low-carbon cooling solutions that outperform conventional HVAC systems. Besides, the rise of mixed-use developments and smart city projects is accelerating the adoption of district cooling in commercial zones. Like, a considerable portion of new commercial constructions in Scandinavia and the Benelux region incorporate district cooling as part of integrated energy management systems. These networks not only reduce electricity consumption but also optimize space utilization by eliminating rooftop chillers and individual air conditioning units. Government incentives and municipal zoning policies are further reinforcing this trend.

The institutional application segment is quickly moving ahead in the Europe district cooling pipeline network market, expected to expand at a CAGR of 9.3%. This segment encompasses hospitals, universities, government buildings, and research institutions, which require stable, energy-efficient, and environmentally responsible cooling solutions. A primary factor fueling this growth is the increasing focus on sustainable public infrastructure. Governments across Europe are prioritizing green building upgrades in healthcare and education sectors to meet climate targets under the European Green Deal. Hospitals, in particular, are adopting district cooling due to its reliability and precision in maintaining critical indoor climates. For example, Karolinska Institute in Sweden implemented a district-cooled hospital complex, achieving a reduction in cooling-related energy use compared to traditional systems. Similarly, university campuses in Germany and the Netherlands are integrating district cooling to support data centers, laboratories, and student housing with minimal environmental impact. Public funding programs such as the EU’s Horizon Europe initiative and national energy renovation schemes are further accelerating adoption.

By Diameter Insights

The medium-diameter pipeline segment (6–12 inches) accounted for the largest portion of the Europe district cooling pipeline network market by capturing 42.8% of total installations in 2024. These pipelines are extensively used in mid-sized urban developments, commercial districts, and mixed-use complexes, where they provide an optimal balance between flow capacity and installation feasibility. One of the primary reasons for the dominance of medium-diameter pipelines is their adaptability to existing urban infrastructure. Many European cities undergoing redevelopment prefer pipelines in this range because they can be installed with minimal disruption to roads and utilities, unlike larger-diameter conduits that require extensive excavation. Also, these pipelines support efficient thermal distribution without requiring excessive pumping power, thereby reducing energy consumption. Municipalities in Denmark and the Netherlands have integrated medium-diameter systems into eco-urban renewal projects, leveraging their scalability and cost-effectiveness.

The large diameter pipeline segment (> 12 inches) is experiencing the highest growth rate in the Europe district cooling pipeline network market, calculated to expand at a CAGR of 8.9% through 2033. This surge in demand is primarily driven by the development of large-scale urban cooling networks in major metropolitan areas, where centralized systems supply cooling to entire city districts, industrial parks, and data center clusters. A key factor behind this growth is the increasing implementation of city-wide district cooling systems, particularly in Nordic countries and Eastern Europe, where municipal authorities are investing heavily in climate-neutral infrastructure. According to the International Energy Agency, large-diameter pipelines are essential for transporting high volumes of chilled water with minimal thermal loss, making them ideal for serving densely populated areas such as Stockholm, Helsinki, and Warsaw Besides, the integration of waste cold recovery and thermal storage systems is boosting the need for large-diameter pipelines that can handle higher flow rates and longer transmission distances. Projects like Gothenburg’s Exergi Cool and Vienna’s Energie AG network demonstrate how these pipelines enable efficient cooling distribution across multiple sectors, including residential, commercial, and industrial applications.

REGIONAL ANALYSIS

Germany was at the forefront of the Europe district cooling pipeline network market by accounting for 21.9%, owing to its strong industrial base, progressive urban planning policies, and commitment to decarbonization. The country’s dense urban centers such as Berlin, Munich, and Frankfurt have seen significant investments in district cooling infrastructure particularly in commercial and institutional buildings aiming for BREEAM and DGNB certifications. One of the key drivers of market growth is the integration of district cooling with existing district heating networks, maximizing energy efficiency and reducing redundancy. Additionally, government-backed initiatives such as the National Action Plan for Energy Efficiency (NAPE) and KfW funding programs have supported the deployment of smart cooling grids in urban redevelopment zones. These efforts, coupled with rising investments in data centers and biotech research facilities reinforce Germany’s leadership in the European district cooling pipeline network market.

Sweden sees strong adoption and this is largely due to its pioneering role in sustainable urban energy systems. Cities like Stockholm, Gothenburg, and Malmö have been early adopters of integrated district cooling solutions, leveraging natural cold sources such as seawater, lakes, and waste cold from district heating production. A major contributor to this success is the proactive involvement of municipal energy companies, such as Vattenfall and Fortum which have developed large-scale cooling networks serving thousands of buildings . Moreover, stringent environmental regulations and national climate goals targeting net-zero emissions by 2045 have accelerated the transition away from conventional air conditioning. Public-private partnerships and innovation grants for thermal storage and absorption cooling technologies have further strengthened Sweden’s position as a leader in advanced district cooling infrastructure.

France holds a significant position in the Europe district cooling pipeline network market, driven by strategic investments in Paris, Lyon, and Marseille, where urban density and climate challenges necessitate efficient and scalable cooling solutions. The French government has recognized district cooling as a key component of its low-carbon urban mobility and energy transition strategy, leading to increased adoption in commercial and institutional buildings. One of the major growth catalysts is the implementation of the Climate and Resilience Law which mandates energy-efficient cooling systems in new large-scale developments . Additionally, Veolia and Engie have expanded their district cooling portfolios, deploying absorption chillers and thermal storage systems that integrate with existing district heating infrastructures.

The Netherlands commands a notable share of the Europe district cooling pipeline network market and is benefiting from its advanced urban planning frameworks and proactive sustainability policies. Cities like Amsterdam, Rotterdam, and Utrecht are implementing district cooling as part of broader smart city initiatives, focusing on circular energy flows and zero-emission urban development. A key driver of market expansion. According to the Netherlands Enterprise Agency (RVO), this policy has spurred significant private and public investment in underground cooling infrastructure, particularly in business parks and eco-districts Also, the integration of seawater-based cooling and aquifer thermal energy storage (ATES) systems has enhanced the efficiency and environmental performance of Dutch district cooling networks.

Denmark is maintaining a strong foothold through its long-standing expertise in district energy systems . The country has successfully extended its district heating model to include district cooling, creating integrated thermal networks that optimize energy use throughout the year. Cities like Copenhagen and Aarhus have developed hybrid district energy grids, where excess heat is converted into cooling via absorption chillers, and surplus cold from refrigeration and wastewater treatment is reused. Government policies such as the Danish Climate Act, which sets a target of 70% emissions reduction by 2030, have further incentivized district cooling adoption. With continued innovation in thermal storage, smart control systems, and circular cooling strategies, Denmark remains a key player in the evolution of Europe’s district cooling pipeline network market.

LEADING PLAYERS IN THE EUROPE DISTRICT COOLING PIPELINE NETWORK MARKET

Fortum

Fortum is a leading energy company that plays a pivotal role in shaping district cooling infrastructure across the Nordic region and beyond. The company has been instrumental in integrating district cooling with existing district heating systems, enhancing overall energy efficiency and sustainability. Fortum's commitment to carbon-neutral solutions has led to the development of innovative cooling networks that utilize surplus cold from natural sources such as lakes and seawater.

Vattenfall

Vattenfall is a major player in the European district cooling sector, known for its large-scale, environmentally responsible cooling solutions. The company operates extensive district cooling networks in cities like Stockholm and Berlin, where it integrates renewable energy sources and waste heat recovery to optimize system performance. Vattenfall’s approach emphasizes reducing electricity consumption and lowering carbon footprints through intelligent grid management and seasonal thermal storage.

Veolia Environnement

Veolia Environnement is a global leader in environmental services and plays a crucial role in advancing district cooling pipeline networks in Europe. The company offers comprehensive solutions that integrate cooling with broader resource management strategies, focusing on energy efficiency, water conservation, and emissions reduction. Veolia has developed several high-performance district cooling systems in France, Italy, and Eastern Europe, often incorporating absorption chillers and hybrid cooling technologies.

Through strategic partnerships and municipal collaborations, Veolia has helped cities transition away from conventional air conditioning toward more resilient and scalable cooling infrastructures.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the primary strategies adopted by leading players in the Europe district cooling pipeline network market is integrating district cooling with renewable energy and waste heat recovery systems. Companies are increasingly combining cooling networks with solar thermal energy, aquifer thermal energy storage (ATES), and industrial waste cold utilization to enhance system efficiency and reduce dependency on electric chillers.

Another key strategy involves expanding digital monitoring and smart control technologies within the district cooling infrastructure. Firms are deploying IoT-enabled sensors, AI-driven load forecasting, and real-time energy analytics to optimize cooling distribution, minimize energy waste, and improve system responsiveness to fluctuating demand patterns.

Lastly, companies are forming strategic partnerships with municipalities, utility providers, and construction firms to accelerate the adoption of district cooling in new urban developments.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players of the Europe district cooling pipeline network market include Veolia, Ramboll, Alfa Laval, Siemens, Danfoss, Keppel Corporation, Engie, Vattenfall, Fortum, and Logstor.

The competition in the European district cooling pipeline network market is characterized by a dynamic interplay between established energy utilities, engineering firms, and infrastructure developers, all vying to meet the growing demand for sustainable urban cooling solutions. While traditional district heating operators have expanded into cooling, specialized energy service companies and municipal utilities have also entered the space, creating a fragmented yet highly innovative landscape.

Market participants differentiate themselves through technological advancements, such as smart grid integration, waste cold recovery, and hybrid cooling systems, as well as through strategic project financing and public-private partnerships In regions with strong regulatory support, such as the Nordic countries and the Netherlands, competition centers around efficiency, scalability, and environmental impact, whereas in other parts of Europe, the challenge lies in raising awareness and overcoming investment barriers.

RECENT HAPPENINGS IN THE MARKET

- In January 2024, Fortum launched a new district cooling expansion project in Helsinki, integrating surplus cold from wastewater treatment into the city’s cooling grid, reinforcing its leadership in circular energy solutions and enhancing system efficiency.

- In May 2023, Vattenfall announced a partnership with Stockholm Exergi to upgrade the capital’s district cooling infrastructure using advanced thermal storage technology, improving resilience and reducing peak electricity demand during summer months.

- In September 2024, Veolia Environnement acquired a French-based thermal engineering firm specializing in absorption chillers, strengthening its technical capabilities and expanding its portfolio of hybrid cooling solutions tailored for urban districts.

- In March 2023, Copenhagen Energy initiated a large-scale pipeline replacement program using pre-insulated and digitally monitored pipes, increasing system reliability and enabling real-time diagnostics across the city’s district cooling network.

- In November 2024, Engie unveiled a new district cooling initiative in Lyon, combining solar-assisted refrigeration with underground thermal storage, marking a significant step toward decarbonizing urban cooling in Southern Europe.

MARKET SEGMENTATION

This research report on the Europe District Cooling Pipeline Network Market has been segmented and sub-segmented based on the type of pipeline, cooling fluid, application, diameter insights, and region.

By Type of Pipeline Insights

- Pre-insulated Pipes

- Plastic Pipes

By Cooling Fluid Insights

- Water

- Glycol-Based Fluids

By Application Insights

- Commercial

- Institutional

By Diameter Insights

- Medium Diameter (6–12 inches)

- Large Diameter (> 12 inches)

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What are the key drivers of the Europe District Cooling Pipeline Network Market?

Rising demand for energy-efficient cooling systems, urbanization, climate change, and supportive government regulations for sustainable energy infrastructure are major drivers.

2. Which countries in Europe are leading in district cooling adoption?

Countries like Sweden, Denmark, Germany, and Finland are leading due to strong policy support and investments in sustainable energy systems.

3. Who are the major players in the Europe District Cooling Pipeline Network Market?

Key players include Veolia, Ramboll, Alfa Laval, Siemens, Danfoss, Keppel Corporation, Engie, Vattenfall, Fortum, and Logstor.

4. How does district cooling contribute to sustainability?

District cooling reduces energy consumption and carbon emissions compared to traditional air conditioning by utilizing centralized and often renewable or waste heat sources.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com