Europe Ducted Heat Pump Market Research Report By Installation Type ( Replacement Installations, New Installations ) Capacity, Application, Efficiency Rating & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of EU) - Industry Analysis From 2026 to 2034

Market Size, 2025

$1.56 BnMarket Estimate, 2026

$1.83 BnMarket Forecast, 2034

$6.56 BnCAGR, 2026–2034

17.30%Europe Ducted Heat Pump Market Size

The Europe Ducted Heat Pump Market Size was valued at USD 1.56 billion in 2025, is expected to have 17.3 % CAGR from 2026 to 2034 and be worth USD 6.56 billion by 2034 from USD 1.83 billion in 2026.

The Europe ducted heat pump market refers to the installation and use of central heating and cooling systems that utilize ductwork to distribute conditioned air throughout residential, commercial, and institutional buildings. These systems operate by transferring heat from ambient sources such as air, ground, or water to provide efficient space heating in winter and reversible cooling in summer. Ducted heat pumps offer a holistic solution for whole-building climate control, making them particularly suitable for larger homes, schools, offices, and healthcare facilities.

According to Eurostat, a significant portion of total energy consumption in European households is attributed to space heating, highlighting the sector’s significance in overall energy efficiency strategies. The European Commission has emphasized the role of heat pumps in achieving decarbonization goals under the EU Green Deal, aiming for carbon neutrality by 2050.

MARKET DRIVERS

Rising Demand for Decarbonized Heating Solutions in Residential and Commercial Buildings

One of the primary drivers of the Europe ducted heat pump market is the growing demand for clean, low-emission heating solutions in both residential and commercial sectors. Governments across the continent have introduced stringent regulations aimed at phasing out fossil fuel-based heating systems, particularly gas boilers, in line with the European Union’s Fit for 55 policy package. As per McKinsey & Company, over 20 European countries have either announced or implemented bans on new gas boiler installations by 2030 or earlier.

This regulatory push has prompted homeowners, builders, and facility managers to seek viable alternatives, with ducted heat pumps emerging as a preferred option due to their capacity to deliver uniform temperature control across large spaces. In urban areas like Copenhagen, Amsterdam, and Vienna, local authorities are incentivizing heat pump adoption through subsidies, tax breaks, and streamlined permitting processes.

In addition, as reported by BloombergNEF, the integration of heat pumps into new build and deep renovation projects has gained momentum, especially in multi-family housing developments where centralized, energy-efficient HVAC systems are essential.

Integration of Renewable Energy and Smart Technologies in HVAC Systems

Another key driver fueling the Europe ducted heat pump market is the increasing integration of renewable energy sources and smart technologies into heating, ventilation, and air conditioning (HVAC) systems. As Europe accelerates its shift toward grid decarbonization and renewable electricity generation, consumers and businesses are seeking compatible, flexible heating solutions that align with sustainable energy trends and digital building management systems.

According to Fraunhofer ISE, renewables accounted for over 45% of electricity generation in the EU in 2023, reinforcing the viability of electrically driven heat pumps as a clean alternative to conventional heating. Ducted heat pump manufacturers are responding by incorporating intelligent control features, such as AI-assisted zoning, occupancy sensing, and remote operation via mobile apps, which enhance user experience and optimize energy consumption.

Furthermore, as noted by McKinsey & Company, the convergence of heat pumps with rooftop solar panels and battery storage systems is enabling greater energy independence and cost stability for end-users. Countries such as Sweden and Norway have pioneered hybrid installations that combine photovoltaic arrays with high-efficiency ducted heat pumps, demonstrating scalable pathways for broader European adoption.

In addition, as per the European Environment Agency, smart building codes in Germany, France, and the Netherlands now require newly constructed commercial and multifamily housing units to support integrated, low-carbon HVAC infrastructures.

MARKET RESTRAINTS

High Initial Installation Costs Compared to Conventional HVAC Systems

A major restraint affecting the Europe ducted heat pump market is the relatively high initial investment required for system procurement and installation compared to traditional heating and cooling alternatives. While ducted heat pumps offer long-term energy savings and environmental benefits, the upfront costs including equipment, labor, and necessary modifications to existing ductwork pose a significant barrier to widespread consumer adoption, particularly among budget-conscious homeowners and small businesses. This represents a premium over standard gas or oil-fired heating systems.

Moreover, retrofitting older properties can add additional expenses, particularly when upgrading insulation, electrical wiring, or modifying existing duct networks. As per the European Consumer Organization (BEUC), many consumers remain hesitant to commit to heat pump investments due to uncertainty regarding return on investment timelines and maintenance costs. While subsidies and green loans help offset some of these expenditures, the lack of clarity around financing options and payback periods continues to limit market expansion.

Limited Installer Expertise and Supply Chain Bottlenecks

An ongoing challenge impeding the growth of the Europe ducted heat pump market is the shortage of skilled installers and disruptions in supply chains that affect product availability and lead times. The specialized knowledge required for proper sizing, configuration, and commissioning of ducted systems creates a bottleneck in scaling adoption, particularly in markets with aging technician workforces and limited vocational training programs.

As reported by the European Heat Pump Association (EHPA), there is a notable gap in qualified HVAC professionals across several member states, with less number of heating installers certified to handle advanced heat pump systems. According to McKinsey & Company, this skills deficit results in longer project timelines, inconsistent installation quality, and higher service costs, discouraging potential adopters.

Apart from these, global supply chain constraints particularly in semiconductors, refrigerants, and copper components have led to extended delivery schedules for heat pump units. These challenges are exacerbated by the need for coordinated retrofitting interventions that involve not only HVAC upgrades but also improvements in building insulation and electrical infrastructure.

MARKET OPPORTUNITIES

Expansion of Deep Retrofit Programs Under the Renovation Wave Strategy

A significant opportunity shaping the future of the Europe ducted heat pump market is the expanding scope of deep retrofit initiatives under the European Union’s Renovation Wave Strategy. Launched as part of the European Green Deal, this initiative aims to double the annual energy renovation rate of buildings by 2030, targeting the vast stock of older, energy-inefficient residential and commercial structures across the continent.

According to the European Environment Agency, nearly 75% of the EU’s building stock was built before 2000, with most structures exhibiting poor thermal performance and heavy reliance on fossil-fuel-based heating. As part of the Renovation Wave, national governments are offering substantial subsidies, grants, and low-interest loans to facilitate comprehensive upgrades including the replacement of outdated HVAC systems with high-performance heat pumps.

In particular, ducted heat pumps are well-suited for comprehensive renovations that involve re-engineering internal layouts and improving ventilation systems. Moreover, cities such as Brussels, Berlin, and Milan are mandating energy performance certificates (EPCs) for property transactions, incentivizing homeowners to invest in energy-efficient upgrades.

Growing Popularity of Net-Zero and Nearly Zero-Energy Building Standards

An emerging opportunity within the Europe ducted heat pump market lies in the rapid adoption of net-zero emissions and nearly zero-energy building (nZEB) standards. As part of the EU’s Clean Energy Package, all new buildings must meet nZEB requirements, meaning they consume almost as much energy as they produce, typically through renewable sources.

According to the European Committee for Standardization (CEN), the implementation of nZEB policies has intensified since 2022, with countries like France, Austria, and Ireland mandating near-zero energy performance for all new constructions. In response, architects and developers are increasingly specifying ducted heat pump systems as core components of integrated HVAC solutions designed to minimize energy demand and maximize thermal efficiency.

Like, ducted heat pumps are particularly advantageous in commercial and high-density residential applications where zoned temperature control, air distribution, and energy recovery are critical. Their compatibility with photovoltaic systems and district heating networks further enhances their appeal in sustainable building designs.

Moreover, as per the European Construction Industry Federation (FIEC), the construction sector accounts for roughly 40% of the EU’s total energy consumption, making it a focal point for energy efficiency policies. The requirement for highly efficient, low-carbon heating and cooling systems in new builds and retrofitted structures is expected to drive sustained demand for ducted heat pumps across Europe’s evolving green building landscape.

MARKET CHALLENGES

Seasonal Performance Limitations in Cold Climate Zones

One of the most pressing challenges facing the Europe ducted heat pump market is the seasonal performance limitations of air-source heat pumps in cold climate zones, which constitute a significant portion of the continent. While modern heat pumps have made significant strides in efficiency and output, sub-zero temperatures can still hinder performance, necessitating supplementary heating sources during extreme winter conditions.

According to IEA Heat Pump Center, the coefficient of performance (CoP) for many air-source heat pumps drops below 2.5 in outdoor temperatures below -10°C, reducing efficiency and increasing electricity demand. Also, this limitation poses a concern for wider adoption in Nordic and Eastern European countries where winter temperatures frequently fall below freezing.

To address this issue, manufacturers are investing in enhanced compressor technologies, synthetic refrigerants, and hybrid system integrations that pair heat pumps with biomass boilers or thermal storage. However, the added complexity and cost associated with optimizing performance in colder climates can deter consumers who expect seamless operation without auxiliary heating inputs.

Moreover, as reported by the European Environment Agency, concerns about power grid capacity during peak winter demand further complicate the scalability of all-electric heat pump reliance in northern regions.

Grid Capacity Constraints and Electricity Cost Volatility

Another critical challenge affecting the Europe ducted heat pump market is the strain placed on electricity grids and the impact of fluctuating energy prices on consumer adoption. As the continent shifts toward electrification of heating, the increased load from heat pump usage especially during peak winter hours has raised concerns about grid stability and reliability.

According to the International Energy Agency (IEA), the widespread adoption of heat pumps could increase European electricity demand by as much as 15% by 2030 if deployment forecasts are met. As per ENTSO-E (European Network of Transmission System Operators for Electricity), this trajectory could pose challenges for grid operators managing intermittency from renewable sources and ensuring stable power supply during cold spells.

Additionally, recent volatility in electricity pricing spurred by energy security concerns and wholesale market fluctuations has created economic uncertainty for potential heat pump users. Unlike gas, whose price trends are more predictable, electricity tariffs are subject to frequent changes, affecting the attractiveness of heat pumps based on lifetime cost assessments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Installation Type ,Capacity, Application, Efficiency Rating and Country. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, Germany, Italy, France, Spain, Sweden, Denmark, Poland, Switzerland, Netherlands, Rest of Europe. |

| Market Leaders Profiled | Trane, Danfoss, Daikin, Carrier, SAMSUNG, Bard HVAC, Mitsubishi Electric Corporation, Bosch Thermotechnology Corp |

SEGMENT ANALYSIS

By Installation Type Insights

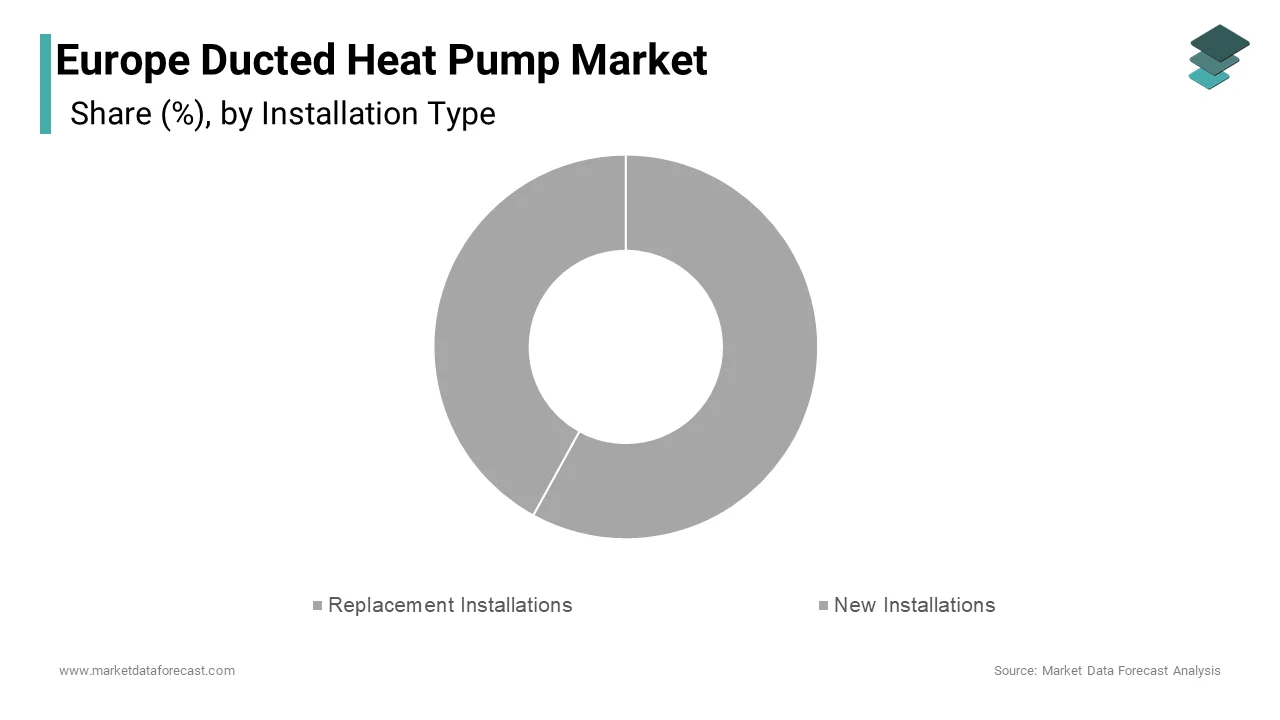

The replacement installations segment represented the largest category in the Europe ducted heat pump market by capturing 58.8% of total demand in 2025. This dominance is primarily driven by the aging building stock across the continent and the increasing need to replace outdated, fossil fuel-based heating systems with more energy-efficient alternatives.

According to Eurostat, a major portion of residential buildings in the EU were constructed before 1980, with many still relying on gas or oil boilers that are now subject to phase-out policies. Moreover, as reported by the European Environment Agency, national retrofit programs such as Germany’s KfW funding scheme and the UK’s Boiler Upgrade Scheme have significantly accelerated replacement cycles.

Additionally, as per ACEEE (American Council for an Energy-Efficient Economy), deep renovation trends where entire HVAC systems are modernized alongside insulation and ventilation upgrades are increasingly favoring ducted models due to their compatibility with whole-house energy efficiency strategies.

The New installations are emerging as the fastest-growing segment in the Europe ducted heat pump market, expanding at a CAGR of 14.2%. This rapid expansion is fueled by the surge in eco-conscious housing developments, stricter building codes, and growing adoption of nearly zero-energy building (nZEB) standards across the region. Like, nearly all new residential constructions in Sweden, Denmark, and the Netherlands now include ducted heat pump systems as standard HVAC solutions, aligning with national energy efficiency mandates. These large-scale developments benefit from the scalability and zoning capabilities of ducted systems, which offer superior comfort and energy management compared to split units.

Additionally, as reported by BloombergNEF, developers are increasingly bundling heat pumps with solar PV and battery storage solutions, enhancing the appeal of all-electric HVAC systems in new builds.

By Capacity Insights

The 5–10 ton capacity range was the top performing segment in the Europe ducted heat pump market by accounting for 42.6% of total installations in 2025. This segment is predominantly used in mid-sized residential properties, small commercial spaces, and multi-family dwellings, where balanced cooling and heating output is essential without excessive energy consumption.

According to the International Energy Agency (IEA), the average floor area of single-family homes in Western Europe ranges between 120 and 200 square meters. Also, this size class offers optimal efficiency and cost-effectiveness for households seeking year-round climate control without the complexity of larger industrial-grade systems.

Moreover, this capacity range benefits from widespread availability among major manufacturers such as Daikin, Mitsubishi Electric, and NIBE, ensuring broad accessibility through both direct sales and installer networks. Government-backed incentive programs also tend to target this segment, as it aligns well with mainstream residential decarbonization efforts.

The 15 tons and above segment is the quickest advancing capacity category in the Europe ducted heat pump market, registering a CAGR. This rapid expansion is driven by the increasing deployment of high-capacity heat pumps in large residential complexes, commercial facilities, and public infrastructure projects.

Like, large-scale residential developments including apartment blocks and eco-villages are increasingly adopting centralized ducted heat pump systems capable of serving multiple units simultaneously. In countries like Sweden and Austria, district-level heat pump integration into community heating networks has become a strategic approach for reducing carbon emissions in multi-dwelling environments.

Furthermore, commercial and institutional buildings such as schools, hospitals, and office campuses are prioritizing high-capacity ducted heat pumps to meet stringent energy performance regulations. The ability of these systems to integrate with renewable energy sources, including solar thermal and geothermal, enhances their appeal for long-term operational sustainability.

By Application Insights

The residential applications commanded the Europe ducted heat pump market by capturing 66.9% of total installations in 2025. This overwhelming dominance stems from the extensive focus on residential building decarbonization, coupled with policy-driven incentives aimed at replacing traditional heating systems.

According to Eurostat, a large percentage residential buildings exist in the EU, with more than half classified as energy inefficient. As part of the Renovation Wave Strategy, the European Commission aims to renovate at least 30 million buildings by 2030, directly boosting demand for high-efficiency ducted heat pumps.

Moreover, homeowners are increasingly prioritizing indoor air quality, noise reduction, and even temperature distribution factors where ducted systems outperform split or mini-split alternatives. Besides, the integration of smart thermostats and zoning controls has enhanced user experience, making ducted heat pumps more appealing to modern consumers.

The commercial applications are the rapidly expanding segment in the Europe ducted heat pump market, expanding at a CAGR of 15.4%. This growth is primarily driven by the tightening energy efficiency requirements for non-residential buildings and the increasing emphasis on corporate sustainability commitments.

According to the European Environment Agency, commercial buildings account for around 40% of final energy consumption in the EU, prompting governments to introduce mandatory energy performance certificates (EPCs) and minimum efficiency standards for HVAC systems.

Moreover, educational institutions, healthcare facilities, and retail centers are increasingly opting for ducted heat pumps due to their ability to maintain stable indoor climates while reducing operational costs. Public procurement guidelines in several EU member states now prioritize low-carbon HVAC solutions, further reinforcing demand.

By Efficiency Rating Insights

The SEER 16–18 efficiency rating was the largest segment in the Europe ducted heat pump market by accounting for a 38.8% of total sales in 2025. This range strikes a balance between energy efficiency, affordability, and compliance with current regulatory standards, making it the preferred choice for both residential and light commercial applications.

As per the European Environment Agency, these models offer greater efficiency than lower-tier units, making them a cost-effective upgrade for homeowners transitioning away from older heating systems.

Besides, as reported by the European Heat Pump Association (EHPA), manufacturers are optimizing SEER 16–18 systems for moderate climate regions, where extreme temperatures are less frequent but seasonal comfort remains a priority. Their compatibility with hybrid configurations and ease of integration into existing ductwork further supports widespread adoption.

The SEER 21 and above efficiency segment is the fastest-growing in the Europe ducted heat pump market, expanding at a CAGR of 19.3%. This rapid adoption is driven by the push for ultra-low energy buildings and the integration of high-efficiency HVAC systems into net-zero energy and passive house designs.

Moreover, advancements in variable-speed compressors, advanced refrigerants, and intelligent zoning controls have enabled higher efficiency levels without compromising system reliability or increasing maintenance demands. Manufacturers such as Vaillant, Bosch Thermotechnology, and Panasonic have introduced next-generation models that combine SEER 21+ ratings with AI-based load optimization features, enhancing overall value proposition. With ongoing improvements in energy labeling and smart home integration, this high-efficiency segment is expected to maintain its leadership in future market expansion.

COUNTRY LEVEL ANALYSIS

Germany had the top position in the Europe ducted heat pump market by commanding a 24.9% of total regional installations in 2025. As Europe's largest economy and a leader in energy transition policies, Germany has been at the forefront of heat pump adoption, supported by substantial subsidies and ambitious building decarbonization targets.

According to McKinsey & Company, over 180,000 heat pumps were installed in Germany in 2023, with nearly half being ducted models tailored for single-family homes and multi-unit buildings. The country’s KfW funding program provides generous grants for energy-efficient renovations, making heat pumps an attractive alternative to gas boilers. Furthermore, as reported by the Federal Environment Agency (UBA), Germany aims to install one million heat pumps annually by 2030 as part of its national climate strategy.

France has strong policy support and urban adoption in the Europe ducted heat pump market. The country benefits from a comprehensive incentive structure, including MaPrimeRénov’, which covers a large majority of installation costs for eligible homeowners, driving significant uptake in both rural and urban settings. Moreover, as reported by ADEME (French Environment and Energy Management Agency), the French government has allocated €5 billion under its National Low Carbon Strategy to accelerate heat pump deployment, particularly in large housing projects and public buildings.

The United Kingdom is another key player in the market in the Europe ducted heat pump market. It has seen a notable uptick in installations due to the phasing out of gas boilers in new builds and the introduction of the Boiler Upgrade Scheme (BUS), offering grants for heat pump installations. Also, local authorities and housing associations are increasingly specifying ducted heat pumps in new build social housing developments to comply with Future Homes Standard requirements.

Additionally, as reported by Climate Change Committee (CCC), the UK’s commitment to achieving net-zero emissions by 2050 has intensified the shift away from natural gas, creating a favorable environment for ducted heat pump adoption. With growing installer expertise and expanded financing options, the UK continues to strengthen its presence in the European heat pump ecosystem.

Sweden occupies a prominent position in the Europe ducted heat pump market. The country has long been a leader in clean heating technologies, with a significant number of heat pumps already in operation nationwide.

According to IEA Heat Pump Center, Sweden has the one of the highest per capita heat pump density in Europe, largely due to its cold climate and early adoption of district heating-integrated heat pump systems. With strong policy support, abundant hydroelectric power, and high consumer acceptance, Sweden remains a model for heat pump adoption across Europe.

The Netherlands is witnessing major growth in the market. The nation has experienced a rapid shift toward electrified heating, driven by stringent building codes, aggressive climate goals, and large-scale housing electrification programs.

According to PBL Netherlands Environmental Assessment Agency, the Dutch government plans to phase out gas connections for all new homes by 2030, positioning electric heat pumps as the default HVAC solution for upcoming residential developments.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the Europe Ducted Heat Pump Market are

- Trane,

- Danfoss,

- Daikin,

- Carrier,

- SAMSUNG,

- Bard HVAC,

- Mitsubishi Electric Corporation,

- Bosch Thermotechnology Corp.,

- Rheem Manufacturing Company,

- STIEBEL ELTRON GmbH & Co. KG, OCHSNER,

- Glen Dimplex Group,

- Lennox International Inc,

- Panasonic Corporation,

- FUJITSU GENERAL Europe,

- Vaillant Group.

The competition in the Europe ducted heat pump market is characterized by a dynamic mix of global HVAC giants, regional specialists, and emerging local brands striving to capture market share amid rapid policy-driven growth. Established multinational corporations such as Daikin, Mitsubishi Electric, and NIBE leverage their technological expertise, brand reputation, and extensive distribution networks to maintain leadership positions. These firms benefit from decades of experience in thermal management and a strong foothold in adjacent markets such as commercial HVAC and district heating systems.

At the same time, mid-sized European manufacturers are leveraging localized knowledge, faster response times, and customized offerings to compete effectively, particularly in retrofit segments where installer familiarity and service support play a crucial role. Additionally, rising interest from digital-first startups and smart home integrators is introducing new value propositions centered around AI-driven climate control and grid-interactive systems.

Market participants must continuously innovate to stay ahead, especially as demand shifts toward ultra-efficient, smart-enabled, and hybrid-compatible heat pump solutions. With increasing regulatory scrutiny, fluctuating energy prices, and heightened consumer awareness, differentiation now extends beyond technical specifications to include ease of installation, lifecycle cost analysis, and seamless integration with renewable energy sources. As the sector matures, collaboration between manufacturers, policymakers, and infrastructure planners will be essential in shaping a competitive yet sustainable market environment.

Top Players in the Market

Daikin Industries, Ltd.

Daikin is a global leader in HVAC technology and holds a strong position in the Europe ducted heat pump market due to its advanced air-source and ground-source systems. The company is known for its high-efficiency, quiet, and smart-integrated ducted solutions tailored for residential and commercial applications.

With a focus on innovation, Daikin has been instrumental in developing next-generation refrigerants, variable-speed compressors, and zoning technologies that enhance performance while aligning with European sustainability standards. Its strategic partnerships with local distributors and government-backed programs have strengthened its regional presence.

By continuously investing in R&D and promoting decarbonized heating solutions, Daikin plays a pivotal role in shaping the future of ducted heat pump adoption across Europe and beyond.

Mitsubishi Electric Corporation

Mitsubishi Electric is a key player in the Europe ducted heat pump market, recognized for its highly efficient, durable, and technologically sophisticated systems. The company’s ZUBADAN and CITY MULTI series offer advanced ducted configurations suitable for both residential and large-scale commercial buildings.

Mitsubishi Electric has contributed significantly to the global HVAC industry through innovations in inverter-driven compressors, hybrid system integration, and adaptive control algorithms that optimize energy use under varying climate conditions.

In Europe, the company collaborates closely with building developers, utility providers, and policy-makers to promote all-electric heating strategies. Its emphasis on quality, reliability, and environmental responsibility has made it a trusted brand among installers and end-users alike, reinforcing its leadership in the region's growing heat pump landscape.

NIBE Industrier AB

NIBE is a major European manufacturer of energy-efficient heating solutions and a leading provider of ducted heat pumps tailored for cold climate performance. The company offers a comprehensive range of air-source and ground-source ducted systems designed for retrofit and new build projects across Scandinavia and Central Europe.

NIBE’s commitment to sustainability and thermal comfort has positioned it as a preferred partner for national renovation initiatives and nearly zero-energy building (nZEB) developments. Through continuous product refinement and strategic acquisitions, NIBE enhances its technological edge and distribution capabilities.

By aligning with EU decarbonization goals and offering locally adapted solutions, NIBE strengthens its influence not only within Europe but also globally, where demand for sustainable heating continues to rise.

Top strategies used by the key market participants

One of the primary strategies employed by leading players in the Europe ducted heat pump market is product innovation and efficiency enhancement , where companies invest heavily in research and development to introduce next-generation models with superior Seasonal Energy Efficiency Ratio (SEER) ratings, intelligent controls, and quieter operation. These advancements cater to evolving consumer preferences and tightening regulatory standards.

Another key approach is strategic partnerships and collaborations , wherein manufacturers work closely with installers, architects, and government agencies to streamline adoption. By engaging early in building design phases and participating in green certification programs, companies ensure their products are specified in new construction and deep retrofit projects.

Lastly, localized production and service expansion is a critical strategy used to strengthen market presence. Companies are setting up regional manufacturing hubs, training centers, and after-sales support networks to improve supply chain resilience, reduce lead times, and provide tailored customer experiences. This localized approach helps firms better respond to regional climate conditions and regulatory requirements, ensuring long-term competitiveness.

RECENT HAPPENINGS IN THE MARKET

- In February 2025, Daikin expanded its production capacity at its plant in Belgium to meet rising demand for high-efficiency ducted heat pumps, signaling a strategic move to localize manufacturing and reduce delivery delays across Western Europe.

- In July 2023, Mitsubishi Electric launched a new line of AI-integrated ducted heat pumps featuring adaptive load management and real-time performance optimization, aimed at enhancing user experience and supporting grid-responsive operations in Germany and the Netherlands.

- In November 2023, NIBE acquired a Swedish-based ventilation system manufacturer to enable deeper integration of heat recovery ventilation with ducted heat pump installations, strengthening its portfolio for holistic building decarbonization strategies.

- In January 2025, Vaillant Group introduced an enhanced installer training program focused on advanced ducted heat pump commissioning and troubleshooting, addressing workforce shortages and improving service quality across France and Spain.

- In May 2025, Bosch Thermotechnology partnered with a German energy consultancy firm to develop turnkey heat pump retrofit packages for older housing stock, simplifying the transition from gas boilers and accelerating market penetration in urban areas.

MARKET SEGMENTATION

This research report on the europe ducted heat pump market has been segmented and sub-segmented into the following categories.

By Installation Type

- Replacement Installations

- New Installations

By Capacity

- 5–10 Tons

- 15 Tons and Above

By Application

- Residential Applications

- Commercial Applications

By Efficiency Rating

- SEER 16–18

- SEER 21 and Above

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe.

Frequently Asked Questions

What is a ducted heat pump, and how does it work?

A ducted heat pump is an HVAC system that distributes heated or cooled air through a network of ducts. It transfers heat using a refrigeration cycle, providing both heating and cooling functions for residential or commercial buildings.

What is driving the growth of the ducted heat pump market in Europe?

Key growth drivers include: EU regulations promoting energy efficiency Phase-out of fossil fuel heating systems Government incentives and subsidies Rising demand for low-carbon, renewable heating technologies

Which countries in Europe are leading the ducted heat pump adoption?

Germany, France, the UK, Italy, and the Netherlands are leading markets due to strong policy support, renovation programs, and high energy efficiency awareness.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com