Europe Electric Two-Wheeler Market Size, Share, Trends & Growth Forecast Report By Vehicle Type (Electric Scooter/Moped, Electric Motorcycle), Battery Type, Voltage Type, Peak Power, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Market Size, 2025

$25.73 BnMarket Estimate, 2026

$27.40 BnMarket Forecast, 2034

$45.38 BnCAGR, 2026–2034

6.51%Europe Electric Two-Wheeler Market Size

The Europe electric two-wheeler market size was valued at USD 25.73 billion in 2025. The European market size is estimated to be worth USD 45.38 billion by 2034 from USD 27.40 billion in 2026, growing at a CAGR of 6.51% from 2026 to 2034.

The Europe electric two-wheeler market involves a growing range of battery-powered motorcycles, scooters, and mopeds designed for urban mobility, personal transport, and last-mile logistics. As cities across the continent grapple with rising air pollution, traffic congestion, and carbon emissions, electric two-wheelers are emerging as a sustainable alternative to traditional internal combustion engine (ICE) vehicles. These vehicles offer advantages such as lower operating costs, reduced noise pollution, and compliance with increasingly stringent emissions regulations.

European governments have been proactive in promoting clean transportation through subsidies, tax incentives, and low-emission zone policies. According to the European Environment Agency, over 100 cities in Europe had implemented or were planning to introduce ultra-low emission zones by the end of 2023. This regulatory push is encouraging consumers and businesses to shift toward cleaner mobility options, including electric two-wheelers.

In addition, improvements in lithium-ion battery technology, along with expanding charging infrastructure, are making electric two-wheelers more practical and accessible. The European Alternative Fuels Observatory reports that public charging points for light electric vehicles have increased significantly in Germany, France, and the Netherlands since 2021. Moreover, shared micro-mobility services and e-scooter rentals in urban centers are further boosting consumer awareness and acceptance.

MARKET DRIVERS

Stringent Emission Regulations and Urban Air Quality Policies

One of the primary drivers of the Europe electric two-wheeler market is the implementation of stringent emission regulations aimed at improving urban air quality and reducing greenhouse gas emissions. The European Union has set ambitious climate targets under the European Green Deal, which includes achieving climate neutrality by 2050. As part of this initiative, several member states have introduced low-emission zones (LEZs) and ultra-low emission zones (ULEZs) that restrict the entry of high-polluting vehicles. According to the European Environment Agency, more than 100 cities in Europe had established or were preparing to implement LEZs. These policies are directly influencing consumer behavior, pushing riders to consider electric alternatives that meet the new regulatory standards. In countries like France and Germany, local authorities provide financial incentives such as purchase subsidies and exemptions from road taxes for electric two-wheeler buyers. For example, the French government’s “Prime à la Conversion” program offers financial incentives toward the purchase of an electric scooter or motorcycle. In addition, major metropolitan areas such as London, Milan, and Madrid have begun enforcing stricter access rules for ICE-based two-wheelers, especially older models.

Rising Demand for Cost-Effective and Sustainable Personal Mobility

Rising Demand for Cost-Effective and Sustainable Personal Mobility

Another key driver fueling the expansion of the Europe electric two wheeler market is the increasing demand for cost-effective and sustainable personal mobility solutions, particularly in densely populated urban areas. With rising fuel prices and the overall cost of car ownership becoming less viable for many city dwellers, two-wheelers—especially electric ones—are gaining traction as an efficient and economical means of commuting. Electric two-wheelers, with their significantly lower per-kilometer energy costs, present an attractive option. Besides, maintenance requirements for electric models are minimal compared to traditional scooters and mopeds, further enhancing their appeal. This trend is especially pronounced among younger demographics and gig economy workers who rely on lightweight vehicles for delivery services and ride-hailing platforms. Cities like Berlin, Amsterdam, and Barcelona have witnessed a surge in e-scooter adoption, supported by shared mobility operators offering rental services. As urbanization continues and environmental consciousness grows, electric two-wheelers are becoming an integral part of Europe’s evolving mobility ecosystem.

MARKET RESTRAINTS

Limited Charging Infrastructure and Range Anxiety

A significant restraint affecting the Europe electric two wheeler market is the relatively underdeveloped charging infrastructure compared to other electric vehicle segments. While passenger cars benefit from extensive fast-charging networks funded by both public and private entities, dedicated charging stations for electric two-wheelers remain sparse in many regions. According to the European Alternative Fuels Observatory, as of 2023, only a small percentage of publicly accessible EV charging points in Europe were compatible with or specifically designated for use by electric two-wheelers. This lack of infrastructure contributes to widespread range anxiety , deterring potential buyers who fear being stranded without nearby charging options. Unlike cars, most electric scooters and mopeds do not come equipped with large battery packs, limiting their maximum range to between 60 and 100 kilometers on a single charge. For daily commuters in rural or semi-urban areas where charging facilities are limited, this presents a considerable barrier to adoption. Moreover, unlike household plug-in charging for cars, many apartment dwellers in European cities lack access to secure off-street parking or electrical outlets for overnight charging.

High Upfront Costs and Limited Consumer Awareness

Despite lower long-term operating costs, the high upfront price of electric two-wheelers remains a major obstacle to widespread adoption in Europe. Compared to conventional gasoline-powered scooters and mopeds, electric models often carry a significant price premium due to the cost of lithium-ion batteries and advanced electronic components. According to data from the European Cyclists’ Federation, the average cost of an electric scooter in Europe is notably higher than its ICE counterpart, discouraging budget-conscious buyers. Apart from these, there is a notable gap in consumer awareness regarding the benefits and incentives associated with electric two-wheelers. Many potential buyers remain unfamiliar with available government subsidies, total cost-of-ownership comparisons, and the performance capabilities of modern electric models. A survey conducted by Transport & Environment in 2023 revealed that only 37% of respondents in major European cities were aware of national incentive programs for electric two-wheelers. This knowledge deficit is particularly pronounced among older demographics and in Eastern European markets where electric mobility adoption lags behind Western counterparts.

MARKET OPPORTUNITIES

Expansion of Shared Micro-Mobility Services

One of the most promising opportunities for the Europe electric two wheeler market lies in the rapid expansion of shared micro-mobility services, including e-scooter rentals and app-based ride-sharing platforms. Over the past few years, cities across the continent have embraced shared electric scooters as a flexible, eco-friendly solution for short-distance urban travel. According to data from the European Transport Federation, more than 250 cities in Europe had launched or expanded shared e-scooter programs between 2021 and 2023. These services not only increase public exposure to electric two-wheelers but also serve as a gateway for future personal purchases. Companies like Lime, Dublin-based Moby, and German operator Nextbike have deployed tens of thousands of electric scooters across major metropolitan areas, reinforcing the viability of zero-emission personal transport. Furthermore, municipal authorities view these services as a way to reduce reliance on private cars and enhance first-mile/last-mile connectivity within public transit networks. The integration of shared e-scooters with digital mobility apps and multi-modal transit systems is strengthening their appeal.

Integration with Smart City and Zero-Emission Urban Planning Initiatives

An emerging opportunity for the Europe electric two wheeler market is the alignment with smart city development and zero-emission urban mobility strategies. Municipal governments across the continent are prioritizing sustainable transportation solutions as part of broader efforts to reduce traffic congestion, improve air quality, and meet climate action targets. According to the European Commission’s Smart Cities and Communities Initiative, over 120 European cities had integrated electric mobility into their long-term urban development plans by 2023. Electric two-wheelers are well-suited to support these objectives due to their compact size, low emissions, and ability to navigate dense urban environments efficiently. Cities like Oslo, Paris, and Barcelona have introduced dedicated lanes and preferential parking for electric scooters and mopeds, incentivizing residents to make the switch from fossil-fueled alternatives. Furthermore, advancements in IoT-enabled vehicle tracking, geofencing, and real-time fleet management are enabling better integration of electric two-wheelers into citywide mobility ecosystems. Public-private partnerships are facilitating the deployment of electric delivery fleets for logistics companies, aligning with green city goals.

MARKET CHALLENGES

Battery Technology Limitations and Recycling Concerns

One of the foremost challenges facing the Europe electric two wheeler market is the limitations in current battery technology and concerns surrounding battery lifecycle management. Most electric scooters and mopeds rely on lithium-ion batteries, which, while lighter and more efficient than older lead-acid alternatives, still suffer from issues related to weight, longevity, and thermal stability. Beyond performance constraints, recycling and disposal of used lithium-ion batteries pose significant environmental and logistical challenges. As sales volumes grow, so does the volume of spent batteries requiring proper handling. However, as reported by the European Environment Agency, only small portion of lithium-ion batteries in the EU were collected for recycling in 2023, noting gaps in waste management infrastructure. Regulatory frameworks for battery traceability, second-life applications, and responsible sourcing of raw materials are still evolving, creating uncertainty for manufacturers and policymakers alike.

Regulatory Variability Across European Countries

A critical challenge confronting the Europe electric two wheeler market is the lack of harmonized regulations governing the classification, speed limits, licensing requirements, and road usage of electric scooters and mopeds across different countries. Unlike passenger cars or motorcycles, which follow standardized EU-wide classifications, electric two-wheelers face a fragmented legal landscape that varies significantly from one jurisdiction to another.

For instance, in Germany and Austria, certain classes of electric scooters require a valid driver’s license and mandatory insurance, whereas in Italy and Spain, similar models can be operated without formal registration. This inconsistency not only hampers market expansion but also creates confusion among consumers regarding permissible usage and safety standards.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.51% |

| Segments Covered | By Vehicle Type, Battery Type, Voltage Type, Peak Power, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | BMW AG, Energica Motor Company S.p.A., Harley-Davidson, Inc., Honda Motor Co., Ltd., Kawasaki Heavy Industries, Ltd., KWANG YANG MOTOR CO., LTD. (KYMCO), Piaggio & C. SpA, PIERER Mobility AG (KTM, Husqvarna, GasGas), Sanyang Motor Co., Ltd. (SYM), Triumph Motorcycles Ltd., Yamaha Motor Co., Ltd., and Zero Motorcycles, Inc., and others. |

SEGMENT ANALYSIS

By Vehicle Type Insights

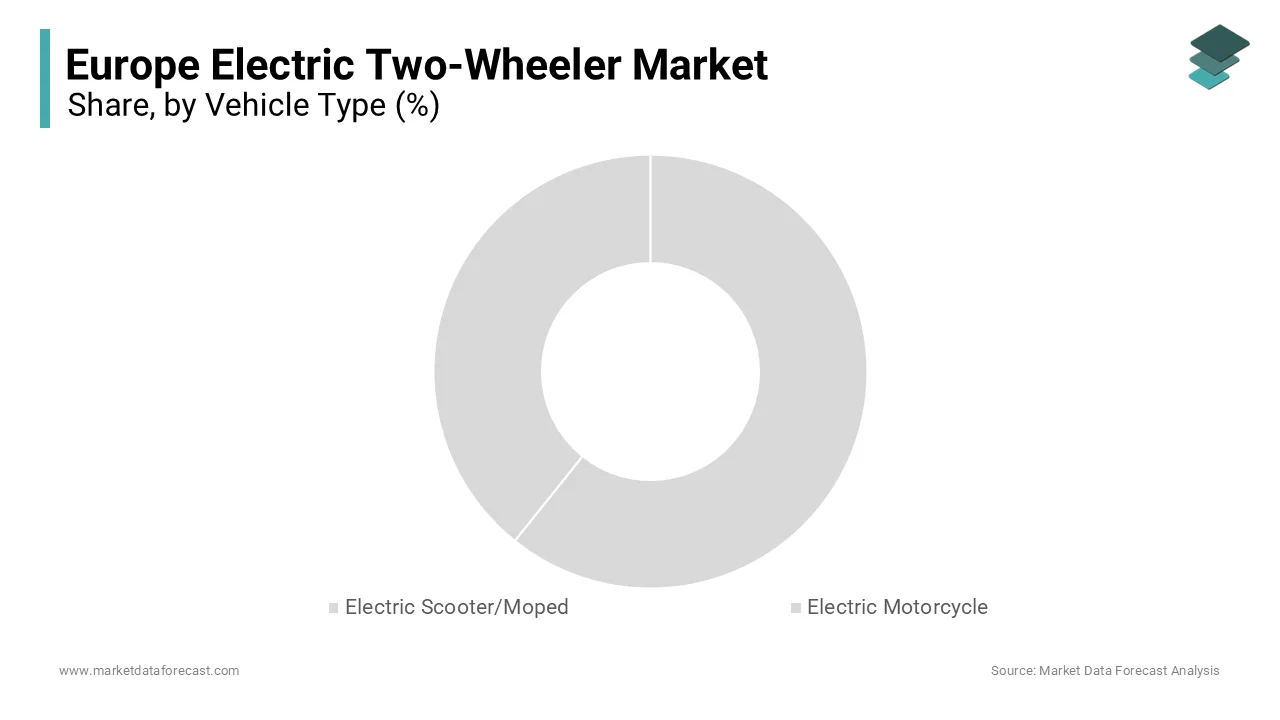

The electric scooter/moped segment dominated the Europe electric two-wheeler market by capturing 68.5% of total sales in 2025. This segment includes lightweight, easy-to-maneuver vehicles primarily used for short-distance urban commuting and last-mile logistics. Their popularity is largely attributed to their affordability, ease of use, and compliance with city mobility regulations. One key driver behind this dominance is the widespread adoption of shared micro-mobility services , particularly in major metropolitan areas. According to data from Transport & Environment, over 150 cities across Europe had implemented or expanded public e-scooter sharing programs between 2021 and 2023. Companies like Lime, Dublin-based Moby, and Nextbike have deployed tens of thousands of electric scooters in cities such as Paris, Berlin, and Barcelona, significantly boosting awareness and acceptance of personal electric mobility. In addition, regulatory frameworks in many European countries classify electric scooters under less stringent licensing requirements , making them accessible to a broader consumer base. As per the International Transport Forum, many European nations allow riders to operate electric scooters without a full motorcycle license, further encouraging uptake among younger demographics and urban professionals seeking efficient transportation alternatives.

On the other hand, the electric motorcycle segment is emerging as the fastest-growing category in the Europe electric two-wheeler market, projected to expand at a CAGR of 19.4% through 2034. This growth is driven by increasing demand for high-performance, long-range electric alternatives to traditional motorcycles, particularly among professional riders, delivery fleets, and environmentally conscious consumers. A primary factor fueling this expansion is the advancement in lithium-ion battery technology, which has enabled manufacturers to develop electric motorcycles with ranges exceeding 200 kilometers on a single charge. Moreover, government incentives are playing a crucial role in accelerating adoption. These financial benefits are making electric motorcycles more competitive with internal combustion engine models.

By Battery Type Insights

The lithium-ion battery segment held the largest share of the Europe electric two wheeler market in 2025. This dominance is attributed to the superior energy density, longer lifespan, and faster charging capabilities of lithium-ion batteries compared to alternative chemistries. One of the main reasons for this widespread adoption is the declining cost of lithium-ion cells , which has made electric two-wheelers more affordable for consumers. In addition, government-backed initiatives promoting clean transportation technologies have encouraged the shift away from older sealed lead-acid (SLA) batteries. The European Battery Alliance reports that lithium-ion battery production capacity in Europe is expected to increase fivefold by 2027, supporting local supply chains and reducing dependency on imports. Another contributing factor is the superior weight-to-power ratio of lithium-ion batteries , which enhances vehicle efficiency and range—critical considerations for urban commuters.

On the contrary, the sealed lead acid (SLA) battery segment is experiencing steady growth, projected to expand at a CAGR of approximately 6.2%. This progress is mainly propelled by cost-sensitive markets and entry-level electric two-wheeler segments , where affordability remains a key purchasing factor. SLA batteries continue to be widely used in budget-friendly mopeds and low-speed scooters, especially in Eastern European countries where electric mobility adoption is still in its early stages. Moreover, SLA batteries are favored in shared micro-mobility applications where frequent battery swaps and simple maintenance are required. Some operators prefer SLA units for their durability in high-usage rental environments, despite their heavier weight and shorter lifespan compared to lithium-ion alternatives.

By Voltage Type Insights

The low-voltage (<48V) segment had the biggest portion of the Europe electric two wheeler market by capturing a 56.1% of total sales in 2025. This voltage range is predominantly used in electric scooters and mopeds designed for urban commuting, where regulatory classifications often exempt these vehicles from requiring formal driver’s licenses or insurance. One of the primary drivers of this segment's dominance is favorable legislation across multiple European countries. According to the European Transport Safety Council, several EU member states, including Spain, Italy, and Austria, restrict motor power output for <48V electric two-wheelers to below 1 kW, allowing riders to operate them with minimal legal restrictions. This accessibility makes these vehicles highly attractive to younger riders and first-time buyers. Also, lower manufacturing and battery costs associated with sub-48V systems make these models more affordable for budget-conscious consumers.

The high-voltage (>96V) segment is coming up as quickly expanding category in the Europe electric two wheeler market, projected to expand at a CAGR of 22.8% . This rapid development is caused by the rising demand for high-performance electric motorcycles and premium electric scooters capable of delivering extended range and superior acceleration. One of the key factors behind this surge is the increased adoption of advanced lithium-ion battery packs and high-efficiency electric motors, which enable manufacturers to produce electric two-wheelers with highway-capable speeds and improved hill-climbing ability. According to the European Alternative Fuels Observatory, the number of >96V electric motorcycles registered in Germany increased in 2023 , indicating strong consumer interest in performance-oriented electric mobility. Besides, government incentives targeting premium electric two-wheelers are accelerating market penetration. Countries like France and the Netherlands offer enhanced subsidies for high-voltage models, recognizing their potential to replace traditional gasoline-powered motorcycles in urban settings.

By Peak Power Insights

The mid-range peak power segment (3–6 kW) was at the forefront of the Europe electric two wheeler market by accounting for a 49.8% of total sales in 2025. This power range is ideal for lightweight electric scooters and mopeds used primarily for urban commuting and short-distance travel within city centers. One of the main reasons for this segment’s dominance is alignment with regulatory limits in several European countries, which define 4 kW as the maximum allowable motor power for certain classes of electric two-wheelers without requiring a full motorcycle license. According to the International Transport Forum, over 20 European nations restrict electric mopeds to 4 kW or below , facilitating widespread adoption among young riders and urban commuters. In addition, the affordability and energy efficiency of 3–6 kW models make them highly attractive to budget-conscious consumers. As reported by ACEA, the average energy consumption of a 4 kW electric scooter is approximately 0.5 kWh per 100 km , significantly lower than higher-powered variants, making daily usage more economical.

The high-power segment (>10 kW) is witnessing the highest growth rate in the Europe electric two wheeler market, projected to expand at a CAGR of approximately 24.3%. This swift adoption is driven by the increasing availability of high-performance electric motorcycles and dual-purpose scooters that can match or exceed the capabilities of conventional internal combustion engine bikes. A major factor behind this growth is the rising consumer preference for electric motorcycles with highway-ready speeds and long-range capabilities. Moreover, advancements in battery cooling, motor efficiency, and regenerative braking systems have enabled manufacturers to develop high-power electric two-wheelers with improved thermal management and extended battery life. Brands like Zero Motorcycles, BMW Motorrad, and Energica have introduced models with power outputs ranging from 11 kW to over 100 kW, catering to both recreational riders and commercial delivery fleets.

REGIONAL ANALYSIS

Germany had the largest share of the Europe electric two wheeler market i.e. 23.2% and is driven by strong government support, robust automotive innovation, and rising consumer demand for sustainable mobility solutions. As one of the continent’s largest economies, Germany has been at the forefront of electrification efforts, with federal and state-level policies promoting the adoption of electric scooters and motorcycles. A key driver of market growth is the generous subsidy programs offered. Also, urbanization and traffic congestion in major cities like Munich, Frankfurt, and Berlin are pushing commuters to seek compact, eco-friendly alternatives. Shared micro-mobility providers have also expanded operations in these metropolitan areas, reinforcing consumer familiarity with electric scooters.

France has strong policy support and rapid adoption in the market. It is benefiting from proactive government policies and extensive urban mobility initiatives. Urban centers such as Paris, Lyon, and Marseille have embraced electric scooters as part of broader efforts to reduce air pollution and meet climate targets under the National Low-Emission Mobility Plan. According to the French Road Safety Observatory, electric two-wheeler registrations increased in 2023 , with shared e-scooter operators deploying thousands of units across major cities. Furthermore, municipal authorities have introduced dedicated lanes and parking incentives for electric two-wheelers , enhancing their practicality and appeal.

Italy has strategic focus on urban electrification and is driven by a combination of strong domestic manufacturing, favorable taxation policies, and aggressive urban decarbonization strategies. Cities like Milan, Rome, and Turin have implemented low-emission zones and tax breaks for electric vehicle owners, encouraging a shift away from fossil-fueled two-wheelers. A key contributor to market expansion is the Italian government’s “Ecobonus Mobilità” program, which provides up to €3,000 in rebates for electric scooter purchases, according to data from the Italian Ministry of Ecological Transition. As a result, electric two-wheeler sales surged by 37% in 2023, with shared mobility operators playing a significant role in driving adoption. Moreover, Italy is home to several prominent electric two-wheeler manufacturers, including Piaggio and Italjet, which are investing heavily in research and development to enhance product competitiveness.

The Netherlands is expanding its micro-mobility ecosystem which is benefiting from a well-established cycling culture and progressive urban mobility policies. Dutch cities such as Amsterdam, Utrecht, and Rotterdam have integrated electric scooters into broader multi-modal transportation networks, making them a natural extension of existing mobility habits. One of the key drivers of market growth is the expansion of shared micro-mobility services, with companies like Deezer Nextbike and Bolt deploying thousands of electric scooters in urban centers. Additionally, the Dutch government offers tax reductions for businesses incorporating electric two-wheelers into corporate fleets, encouraging logistics and delivery companies to transition from traditional mopeds.

Spain holds notable share of the Europe electric two-wheeler market, with strong growth momentum concentrated in Madrid, Barcelona, Valencia, and Seville . These cities have emerged as hotspots for electric scooter adoption, driven by expanding public micro-mobility programs and favorable regulatory conditions . Additionally, the national government provides purchase subsidies, further incentivizing consumer adoption. Shared mobility platforms such as Lime, Circ, and Yellow Mobicity have contributed to rising awareness and accessibility.

COMPETITIVE LANDSCAPE

are leveraging their legacy, distribution networks, and brand trust, while new entrants are disrupting the space with agile business models, innovative technologies, and cost-effective solutions tailored for urban environments.

Market participants differentiate themselves through product design, battery efficiency, performance capabilities, and integration with smart mobility ecosystems. While some focus on premium electric motorcycles targeting performance enthusiasts, others concentrate on affordable, lightweight scooters designed for daily commuting and last-mile delivery applications.

The growing influence of shared mobility providers and government-backed electrification initiatives is also reshaping competitive dynamics. Companies are increasingly aligning with municipal authorities to deploy fleets in urban centers, enhancing visibility and user adoption. As regulations evolve and charging infrastructure expands, the battle for dominance will hinge on innovation speed, localization strategies, and the ability to deliver compelling value propositions to a rapidly maturing consumer base.

KEY MARKET PLAYERS

BMW AG, Energica Motor Company S.p.A., Harley-Davidson, Inc., Honda Motor Co., Ltd., Kawasaki Heavy Industries, Ltd., KWANG YANG MOTOR CO., LTD. (KYMCO), Piaggio & C. SpA, PIERER Mobility AG (KTM, Husqvarna, GasGas), Sanyang Motor Co., Ltd. (SYM), Triumph Motorcycles Ltd., Yamaha Motor Co., Ltd., and Zero Motorcycles, Inc. are the key market players in the Europe electric two wheeler market.The competition in the Europe electric two wheeler market is intensifying as traditional motorcycle manufacturers, emerging startups, and international brands converge to capture market share. Established players

TOP PLAYERS IN THIS MARKET

- Piaggio Fast Forward, a subsidiary of the Italian Piaggio Group, is a key player in the European electric two wheeler market. Known for its innovative approach to urban mobility, the company has developed advanced electric scooters that blend performance with smart connectivity features. Its products emphasize rider safety, lightweight design, and integration with digital platforms, appealing to both individual consumers and shared mobility operators. The company’s contribution extends beyond Europe, influencing global trends in compact electric vehicles tailored for congested city environments.

- Zero Motorcycles is a prominent brand in the high-performance electric motorcycle segment and plays a crucial role in expanding the premium end of the European electric two wheeler market. The company is recognized for its powerful, long-range electric motorcycles that rival traditional combustion engines in capability while maintaining zero emissions. Its influence reaches global markets, where it sets benchmarks for electric powertrain efficiency, battery longevity, and performance engineering. Zero Motorcycles’ commitment to innovation and sustainability has inspired other manufacturers to elevate their electric offerings, reinforcing its leadership position in the broader EV ecosystem.

- KYMCO is a leading manufacturer in the electric scooter segment and has significantly contributed to the adoption of clean urban mobility in Europe. With a strong product lineup focused on affordability, reliability, and practicality, KYMCO has positioned itself as a preferred choice among commuters and fleet operators. The company's strategic partnerships with European distributors and its emphasis on localized service networks have enhanced accessibility and after-sales support. KYMCO’s push into smart scooter technology and battery leasing models has influenced industry practices worldwide, making it a key driver in the global shift toward electrified two-wheel transportation.

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

One of the primary strategies employed by key players in the Europe electric two wheeler market is expanding product portfolios to cater to diverse consumer segments . Companies are introducing a wide range of models—from budget-friendly commuter scooters to high-performance electric motorcycles—ensuring there is an offering for every type of rider. This diversification helps capture different market tiers and accelerates adoption across age groups and usage scenarios.

Another critical strategy involves investing heavily in research and development to enhance battery technology, vehicle performance, and digital integration . Leading manufacturers are incorporating smart features such as GPS navigation, mobile app connectivity, and real-time diagnostics to improve user experience and differentiate their products in a competitive landscape.

Lastly, firms are forming strategic collaborations with governments, municipalities, and micro-mobility operators to promote large-scale deployment of electric two-wheelers . These partnerships facilitate integration into public transport systems, support regulatory alignment, and enable participation in incentive programs, strengthening market presence and fostering long-term growth.

RECENT HAPPENINGS IN THE MARKET

- In February 2025, Piaggio Fast Forward launched a new line of AI-integrated electric scooters designed for seamless urban navigation, featuring adaptive route planning and voice-assisted controls, enhancing user experience and positioning the brand at the forefront of smart mobility solutions.

- In August 2023, Zero Motorcycles expanded its European footprint by opening a regional technical center in Amsterdam, aimed at improving after-sales service, conducting localized R&D, and supporting dealer training, thereby strengthening customer confidence and brand loyalty across Western Europe.

- In May 2025, KYMCO partnered with a major German logistics firm to supply a fleet of electric cargo scooters for urban deliveries, reinforcing its role in the last-mile mobility sector and demonstrating scalability for commercial applications in emission-sensitive zones.

- In October 2023, Vergogna, an Italian e-scooter manufacturer, introduced a battery-as-a-service model in collaboration with Italian energy providers, allowing users to lease batteries instead of purchasing them outright, reducing upfront costs and encouraging mass-market adoption.

- In December 2025, BMW Motorrad unveiled a new high-voltage electric motorcycle platform developed specifically for European road conditions, signaling a strong commitment to expanding its presence in the premium electric two-wheeler segment and competing directly with established rivals.

MARKET SEGMENTATION

This research report on the Europe electric two-wheeler market is segmented and sub-segmented into the following categories.

By Vehicle Type Insights

- Electric Scooter/Moped

- Electric Motorcycle

By Battery Type Insights

- Lithium-Ion

- Sealed Lead Acid (SLA)

By Voltage Type Insights

- <48V

- 48-60V

- 61-72V

- 73-96V

- >96V

By Peak Power Insights

- <3 kW

- 3-6 kW

- 7-10 kW

- >10 kW

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the Europe Electric Two Wheeler Market?

The Europe Electric Two Wheeler Market includes electric motorcycles, electric scooters, electric mopeds, and other battery powered two wheel vehicles used for personal and commercial transportation.

2. What factors are driving the growth of the Europe Electric Two Wheeler Market?

Market growth is driven by increasing environmental awareness, supportive government incentives, rising fuel prices, advancements in battery technology, and growing demand for sustainable mobility solutions.

3. Which vehicle type holds the largest share of the Europe Electric Two Wheeler Market?

Electric scooters account for a significant share of the market due to their affordability, convenience, and suitability for urban commuting.

4. How do government policies support the adoption of electric two wheelers in Europe?

Governments across Europe provide subsidies, tax benefits, purchase incentives, and investments in charging infrastructure to encourage electric vehicle adoption.

5. What role does battery technology play in the market?

Advancements in battery technology improve vehicle range, charging speed, energy efficiency, and overall performance, making electric two wheelers more attractive to consumers.

6. Which countries are leading the Europe Electric Two Wheeler Market?

Countries such as Germany, France, Italy, and Netherlands are among the major contributors to market growth.

7. How are electric two wheelers contributing to sustainability goals?

Electric two wheelers help reduce greenhouse gas emissions, lower air pollution levels, and support the transition toward cleaner urban transportation systems.

8. What are the primary applications of electric two wheelers?

They are widely used for personal commuting, shared mobility services, delivery operations, and last mile transportation.

9. What challenges does the Europe Electric Two Wheeler Market face?

Key challenges include high upfront costs, limited charging infrastructure in some regions, battery replacement costs, and concerns regarding charging times.

10. What is the future outlook for the Europe Electric Two Wheeler Market?

The market is expected to experience strong growth due to continued government support, technological advancements, expanding charging networks, and rising consumer preference for eco friendly transportation solutions.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com