Europe Electric Vehicle Charging Station Market Size, Share, Trends & Growth Forecast Report, Segmented By Level of Charging, Mode, Connection Phase, Dc Fast Charging Type, Charging Point Type, Application, Installation, Charging Infrastructure, Electric Bus Charging Type, Charging Service Type, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2026 to 2034)

Market Size, 2025

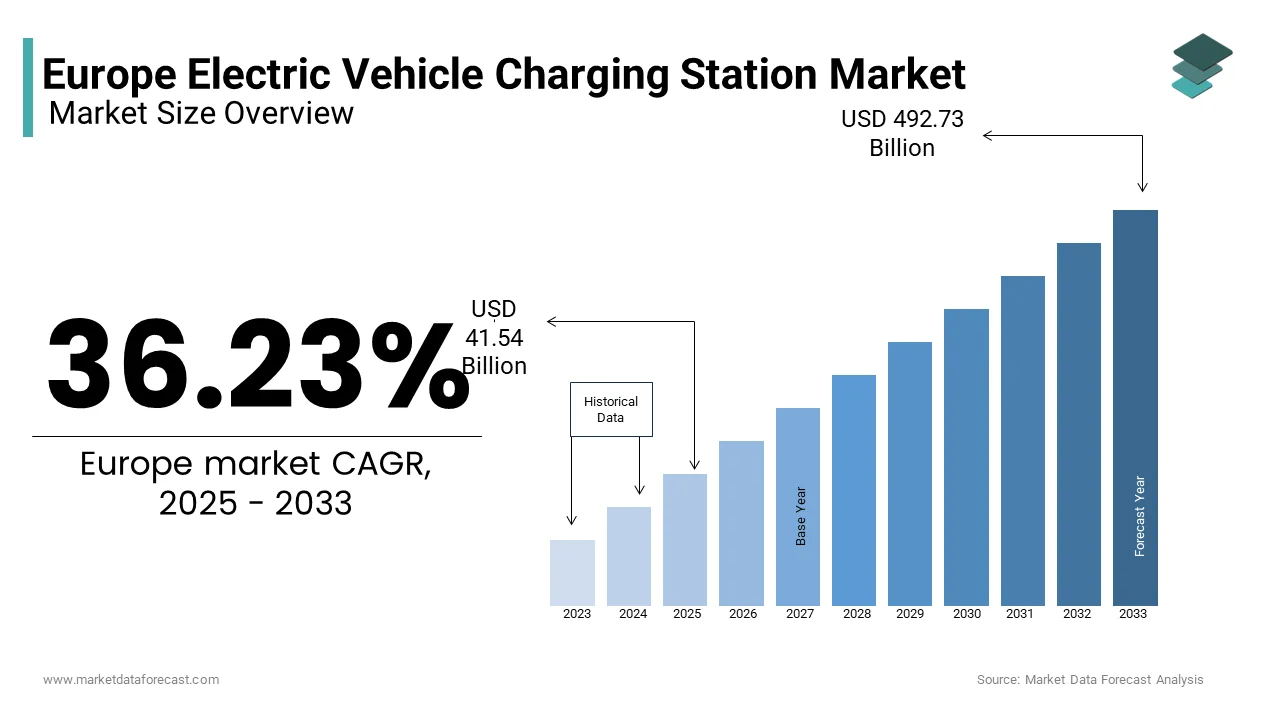

$41.54 BnMarket Estimate, 2026

$56.59 BnMarket Forecast, 2034

$671.31 BnCAGR, 2026–2034

36.23%Europe Electric Vehicle Charging Station Market Size

The Europe electric Vehicle charging station market size was valued at USD 41.54 billion in 2025 and is anticipated to reach USD 56.59 billion in 2026 to reach USD 671.31 billion in 2034, growing at a CAGR of 36.23% during the forecast period from 2026 to 2034.

EV charging stations comprises the infrastructure network essential for replenishing the energy storage systems of electric vehicles including battery electric vehicles and plug in hybrid electric vehicles. This ecosystem encompasses alternating current slow chargers typically installed at residential or workplace locations and direct current fast chargers situated along highways and public hubs. The strategic expansion of this infrastructure is a prerequisite for the widespread adoption of electromobility across the continent. According to the European Alternative Fuels Observatory, the number of publicly accessible charging points in the European Union reached 632,423 by the end of 2023, reflecting a year on year growth rate of approximately 35%. Despite this progress, the density of charging infrastructure varies significantly across member states. As per the European Commission, the Alternative Fuels Infrastructure Regulation mandates that member states install fast charging stations of at least 150 kW every 60 kilometers along the core trans-European transport network by 2025. This regulatory push aims to eliminate range anxiety and facilitate cross border travel. According to the International Energy Agency, the global average of approximately 10 electric cars for every one public charger is a key benchmark for ensuring adequate accessibility. Currently, the ratio in leading markets like the Netherlands approaches this target, while lagging regions struggle to keep pace with vehicle registrations. The integration of smart charging technologies and vehicle to grid capabilities further defines the modern charging landscape enabling better grid management and energy efficiency.

MAJOR MARKET DRIVERS

Regulatory Mandates and Infrastructure Investment Targets

The stringent regulatory framework established by the European Union that sets mandatory deployment targets for charging infrastructure is majorly driving the Europe EV charging stations market expansion. The Alternative Fuels Infrastructure Regulation requires each member state to ensure a minimum power output of one kilowatt per battery electric car and 0.66 kilowatts per plug in hybrid electric car registered. According to the European Commission, the European Union needs approximately 3.5 million public charging points by 2030 to support the projected fleet of 30 million zero emission vehicles. Member states are legally bound to submit national policy frameworks detailing how they will achieve these targets. The Connecting Europe Facility has allocated 1.5 billion euros specifically for the deployment of alternative fuel infrastructure including high power charging corridors. As per the European Climate Infrastructure and Environment Executive Agency, this funding supports projects that fill gaps in the trans-European transport network. The regulation also mandates that all new public chargers be smart capable allowing for dynamic pricing and grid interaction. This legislative certainty de risks investment for private operators and utility companies. Furthermore the Fit for 55 packages reinforces these measures by linking infrastructure development to carbon reduction goals. The clear timeline and financial support mechanisms provided by these regulations accelerate the planning and construction of charging networks ensuring that infrastructure growth keeps pace with vehicle electrification.

Rising Electric Vehicle Adoption and Range Anxiety Mitigation

The rapid increase in electric vehicle registrations that creates an urgent demand for accessible and reliable charging solutions to mitigate range anxiety is further boosting the expansion of the Europe EV charging stations market. According to the European Automobile Manufacturers Association, battery electric vehicles accounted for 14.6% of new car registrations in the European Union in 2023, with plug in hybrids adding another 7.7%. This surge in vehicle ownership necessitates a proportional expansion of charging infrastructure to prevent congestion and ensure convenience. Range anxiety remains a top concern for potential buyers as highlighted by surveys conducted by the Consumer Technology Association, which indicate that 60% of non EV owners cite lack of charging availability as a barrier to purchase. The visibility of public chargers serves as a psychological reassurance even for home charging users. As per Eurostat, the average daily driving distance in Europe is under 50 kilometers, yet the perception of limited long distance capability persists. The deployment of ultra fast chargers with power outputs exceeding 150 kilowatts reduces charging times to under 30 minutes making long distance travel viable. Companies like Ionity and Tesla are expanding their high power networks to cover major transit routes. The correlation between charger density and EV adoption rates is evident in markets like Norway, where extensive infrastructure has led to over 80% electric vehicle market share. This demand pull ensures continuous investment in charging station deployment.

MAJOR MARKET RESTRAINTS

High Initial Capital Expenditure and Grid Upgrade Costs

The substantial initial capital expenditure required for installation and the associated costs of upgrading electrical grid infrastructure is a significant restraint to the Europe EV charging stations market expansion. Installing a direct current fast charger can cost between 50,000 and 150,000 euros depending on power output and site conditions. According to the European Investment Bank, the total investment needed for charging infrastructure in Europe is estimated at 120 billion euros by 2030. A significant portion of this cost is attributed to grid connections which often require transformers and substations to handle the increased load. Many existing distribution networks in urban and rural areas lack the capacity to support multiple high power chargers simultaneously. As per the European Distribution System Operators Association, grid reinforcement projects can take several years to complete due to planning permissions and civil works. This delay bottlenecks the deployment of charging stations particularly in dense city centers where space and power are scarce. Small and medium sized charge point operators often struggle to secure financing for these upfront costs without substantial government subsidies. The complexity of negotiating connection agreements with distribution system operators further adds to administrative burdens and timelines. Until grid modernization accelerates and costs decrease the pace of infrastructure rollout will remain constrained by these financial and technical barriers.

Fragmented Regulatory Landscape and Permitting Bottlenecks

The fragmented regulatory environment and lengthy permitting processes across different European jurisdictions that create operational inefficiencies for charging network operators are further impeding the growth of the Europe EV charging stations market. While the European Union provides overarching directives the implementation details such as zoning laws building codes and electricity tariffs vary significantly between member states and even municipalities. According to the European Commission, obtaining permits for new charging installations can take up to two years in some member states. This inconsistency increases the complexity and cost of scaling operations across borders. In some countries local authorities lack clear guidelines for installing chargers on public land leading to legal uncertainties and delays. As per the European Automobile Manufacturers Association, the lack of harmonized permitting and grid connection procedures further complicates compliance. Operators must navigate a patchwork of regulations regarding safety inspections environmental assessments and land use rights. This bureaucratic burden discourages investment and slows down the deployment of charging infrastructure. Furthermore the absence of harmonized rules for curbside charging in residential areas limits the ability to serve users without private parking. The European Union is working to streamline these processes through the Alternative Fuels Infrastructure Regulation but full harmonization will take time. Until permitting becomes faster and more predictable the market will face headwinds in achieving the necessary scale.

MAJOR MARKET OPPORTUNITIES

Integration of Smart Charging and Vehicle to Grid Technologies

The integration of smart charging and vehicle to grid technologies that enable bidirectional energy flow and enhanced grid stability is a major opportunity for the Europe EV charging stations market. Smart charging allows charging sessions to be optimized based on electricity prices grid load and renewable energy availability. According to the European Commission, smart charging could save European consumers up to 250 million euros a year through reduced charger purchases and optimized energy use. Vehicle to grid technology takes this a step further by allowing electric vehicles to discharge energy back into the grid during peak demand periods. As per the International Energy Agency, this capability can provide valuable ancillary services such as frequency regulation and voltage support. The European Union’s New Battery Regulation encourages the development of batteries suitable for second life applications and grid integration. Pilot projects in countries like the Netherlands and Denmark have demonstrated the technical feasibility and economic benefits of vehicle to grid systems. Utilities are increasingly interested in aggregating electric vehicle batteries as virtual power plants to balance intermittent renewable energy sources. As per the European Distribution System Operators Association, the flexibility offered by electric vehicles could offset the need for billions of euros in grid infrastructure investments. By leveraging these technologies charging station operators can create new revenue streams beyond simple electricity sales. This transformation of charging infrastructure into active grid assets presents a substantial growth opportunity for the market.

Expansion of High Power Charging Corridors for Long Distance Travel

The expansion of high power charging corridors along major highways and trans-European transport networks to facilitate long distance electric travel is another significant opportunity for the regional market. The European Union’s Alternative Fuels Infrastructure Regulation mandates the installation of fast charging stations every 60 kilometers on the core network by 2025. According to the European Climate Infrastructure and Environment Executive Agency, this initiative aims to create a seamless charging experience across borders. There is a growing demand for ultra-fast chargers with power outputs of 350 kilowatts or more which can add 200 kilometers of range in under 10 minutes. As per the International Council on Clean Transportation, the utilization rate of highway chargers is increasing as more consumers adopt electric vehicles for long trips. Private consortia such as Ionity are investing heavily in expanding their high power networks. Additionally the tourism sector is recognizing the value of charging infrastructure in attracting electric vehicle drivers to remote destinations. Hotels campsites and attractions are installing chargers to capture this growing demographic. As per the European Travel Commission, sustainable travel is becoming a key decision factor for tourists. By strategically locating high power chargers at key intervals and destinations operators can capture high value traffic. This expansion not only supports mobility but also stimulates economic activity in rural and semi urban areas.

MAJOR MARKET CHALLENGES

Interoperability and Roaming Platform Fragmentation

The lack of seamless interoperability and the fragmentation of roaming platforms that complicate the user experience is a primary challenge to the expansion of the Europe EV charging stations market. Although the European Union mandates ad hoc access and transparent pricing the reality is that drivers often need multiple apps and membership cards to access different networks. According to the European Consumer Organisation, 60% of EV drivers report difficulties with payment systems and authentication when using public chargers abroad. The existence of numerous e mobility service providers with proprietary roaming agreements creates a complex web of connections that do not always function reliably. As per the European Commission, efforts to standardize communication protocols such as Open Charge Point Interface are ongoing but adoption is uneven. This fragmentation leads to failed transactions and customer frustration undermining confidence in public charging. Furthermore the lack of real time data accuracy regarding charger availability and status misleads drivers. The European Union’s Alternative Fuels Infrastructure Regulation aims to address these issues by requiring common payment methods and data sharing. However implementation varies across member states. Until a unified roaming ecosystem is fully realized the inconvenience of managing multiple accounts will remain a barrier to widespread adoption. Overcoming this challenge requires stronger enforcement of standards and collaboration among stakeholders.

Cybersecurity Risks and Data Privacy Concerns

The growing exposure to cybersecurity risks and data privacy concerns associated with connected charging infrastructure is further challenging the expansion of the Europe EV charging stations market. Modern charging stations are internet of things devices that collect and transmit sensitive data including user identities payment information and location history. According to the European Union Agency for Cybersecurity, the energy sector is a prime target for cyberattacks due to its critical importance. A successful attack on charging networks could disrupt mobility services or even destabilize the electrical grid if vehicle to grid systems are compromised. As per the International Energy Agency, the lack of uniform cybersecurity standards for charging equipment leaves vulnerabilities open to exploitation. Manufacturers and operators must invest heavily in encryption authentication and monitoring systems to protect against threats. The General Data Protection Regulation imposes strict requirements on how personal data is handled adding compliance complexity. Any breach can result in severe financial penalties and reputational damage. Furthermore the integration of charging stations with smart home systems and mobile apps expands the attack surface. As per the European Commission, new cybersecurity certification schemes for critical products are being developed but full implementation will take time. Ensuring the resilience of charging infrastructure against cyber threats is essential for maintaining public trust and operational continuity. This ongoing security arms race poses a persistent challenge for market participants.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 36.23% |

| Segments Covered | By Level Of Charging, Mode, Connection Phase, DC Fast Charging, Charging Point, Application, Installation, Charging Infrastructure, Electric Bus Charging, Charging Service, and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | BYD (China), EVBox (Netherlands), ChargePoint (US), Tesla (US), TGOOD (China), ENGIE (France), State Grid Corporation of China (China), BP (UK), Shell (UK), TotalEnergies (France), Enel X (Italy), Virta (Finland), Delta Electronics (Taiwan), Star Charge (China) |

SEGMENTAL ANALYSIS

By Level Of Charging Insights

The Level 2 charging segment dominated the European EV charging station market by accounting for 85.8% of all publicly accessible charging points in 2025. Its widespread adoption stems from its balance of affordability, speed, and compatibility with most EV models. Offering 20-40 kilometers of range per hour, Level 2 chargers are ideal for residential, workplace, and urban public parking settings. The European Commission highlights that their lower installation costs compared to DC fast chargers make them a practical choice for mass deployment. As the backbone of Europe’s EV infrastructure, Level 2 charging supports daily commuting needs and reduces reliance on slower Level 1 chargers, making it critical for sustained EV adoption.

The Level 3 charging or DC fast charging segment is anticipated to witness the fastest CAGR of 3%. This is influenced by the increasing demand for long-distance travel and the rise of high-capacity EV batteries. ENTSO-E reports that DC fast chargers can deliver up to 100 kilometers of range in 10 minutes, addressing range anxiety effectively. Despite representing only 10% of Europe’s current charging infrastructure, their strategic placement along highways and urban hubs ensures quick recharging for travelers. The IEA emphasizes that expanding Level 3 networks is vital for supporting Europe’s goal of achieving 30 million EVs on roads by 2030, making it a key enabler of sustainable mobility.

By Charging Stations

The AC charging/normal charging station segment dominated the Europe EV charging stations market by holding 80.6% of the regional market share in 2025. The dominance of AC charging segment in the European market is majorly driven by the prevalence of residential and workplace charging which constitutes the majority of daily charging events for electric vehicle owners. According to the International Energy Agency, approximately 80% of all electric vehicle charging in Europe occurs at private residences or workplaces where vehicles are parked for extended periods. AC chargers typically ranging from 3.7 kilowatts to 22 kilowatts are sufficient to fully recharge a vehicle battery within these long dwell times. The European Alternative Fuels Observatory states that the vast majority of the over 630,000 public and private charging points installed in the European Union are AC units due to their lower installation complexity and cost. Installing an AC charger requires minimal grid upgrades compared to high power DC systems making it accessible for individual homeowners and property managers. As per Eurostat, the majority of European households have access to private parking or garages facilitating the installation of wall boxes. This convenience factor ensures that AC charging remains the default method for daily mobility needs. Furthermore the lower hardware costs of AC chargers encourage widespread adoption among early adopters and fleet operators who prioritize cost efficiency over rapid charging speeds. The established standardization of AC connectors such as Type 2 across Europe further reinforces this segment's ubiquity and ease of use for consumers.

However, the DC charging/super charging station segment is projected to be the fastest growing category and register a CAGR of 30.3% over the forecast period owing to the urgent need to support long distance travel and reduce charging times for commercial and private users. The exponential growth of the DC Charging/Super Charging Station segment is primarily attributed to stringent regulatory mandates requiring comprehensive coverage along major highways. The European Union’s Alternative Fuels Infrastructure Regulation mandates the installation of fast charging stations with a minimum output of 150 kilowatts every 60 kilometers along the core trans-European transport network by 2025. According to the European Commission, this legislative requirement has triggered a wave of investments from both public and private sectors to close infrastructure gaps. The regulation ensures that electric vehicle drivers can travel across borders without range anxiety thereby boosting confidence in long distance electromobility. As per the European Climate Infrastructure and Environment Executive Agency, billions of euros in funding are being allocated to support the deployment of these high power corridors. The urgency to meet the 2025 deadline accelerates permitting and construction processes for DC stations. Furthermore the rise in electric vehicle registrations for larger segments such as SUVs and vans which have larger batteries necessitates faster charging solutions to minimize downtime. According to the International Council on Clean Transportation, the utilization rates of highway DC chargers are increasing rapidly as more consumers adopt electric vehicles for intercity travel. This regulatory push combined with rising demand creates a robust growth trajectory for the DC charging segment.

By Vehicle Insights

The battery electric vehicle segment led the market by capturing the highest share of 62.6% of the regional market share in 2025. The growth of battery electric vehicle segment in the European market is primarily driven by the exclusive reliance of BEVs on external charging infrastructure for all their energy needs. The leading position of the Battery Electric Vehicle segment is further attributed to its complete dependence on charging stations for operation unlike plug in hybrids which can rely on internal combustion engines. According to the European Automobile Manufacturers Association, battery electric vehicles require regular and substantial energy replenishment from the grid to maintain daily mobility. This absolute dependency ensures that every kilometer driven by a BEV translates directly into charging station usage. As per the International Energy Agency, the average BEV in Europe consumes approximately 15 to 20 kilowatt hours per 100 kilometers necessitating frequent charging sessions. The growing stock of BEVs which reached over 11 million in Europe in 2023 creates a sustained and predictable demand for charging infrastructure. Unlike PHEVs which may operate in hybrid mode for long distances BEVs must charge before every significant trip. According to Eurostat, the share of BEVs in new car registrations is growing faster than any other vehicle type amplifying their impact on charging infrastructure utilization. This consistent and high volume usage makes BEVs the primary customer base for charging network operators. The shift towards larger battery capacities in newer BEV models further increases the energy demand per session reinforcing the segment’s dominance in the charging market.

By Installation Insights

The individual houses segment dominated the market by holding 54.1% of the European market share in 2025. The growth of the individual houses segment in the European market can be credited to the high rate of home ownership in Europe and the unparalleled convenience of charging vehicles overnight at home. According to Eurostat, approximately 68% of Europeans live in owned accommodations providing the physical space and legal right to install private charging equipment. Home charging allows users to start each day with a full battery eliminating the need for daily visits to public stations. As per the International Energy Agency, home charging is the most cost effective and convenient method for EV owners accounting for the majority of energy consumption. The simplicity of installing a wall box in a private garage or driveway encourages widespread adoption. Government incentives in countries like Germany and France often include subsidies for home charger installations further boosting this segment. According to the European Alternative Fuels Observatory, the majority of new charging points installed annually are located at private residences. The psychological comfort of having a dedicated charger at home alleviates range anxiety and enhances the ownership experience. This fundamental convenience ensures that individual houses remain the primary location for EV charging infrastructure.

However, the commercial segment is another major segment and is expected to witness a CAGR of 27.2% over the forecast period. The commercial segment is growing rapidly due to the aggressive expansion of public charging networks by private operators and utilities to serve users without home charging access. According to the European Alternative Fuels Observatory, the number of public charging points is increasing at a faster rate than private installations in many urban areas. Retailers shopping centers and hotels are installing chargers to attract customers and generate additional revenue streams. As per the European Commission, the Alternative Fuels Infrastructure Regulation mandates increased public charging availability driving commercial investment. The visibility of commercial chargers enhances brand image and customer loyalty for businesses. According to the International Energy Agency, public charging is essential for apartment dwellers and urban residents who lack private parking. The diversification of commercial sites including supermarkets and gyms expands the accessibility of charging infrastructure. This strategic placement captures high footfall traffic and supports the growing EV population. The competitive landscape among charge point operators fuels rapid deployment in commercial locations.

COUNTRY LEVEL ANALYSIS

Germany EV Charging Stations Market Analysis

Germany accounted for the largest share of 26.1% of the European market in 2025. The dominance of Germany in the European market is driven by its large automotive industry and ambitious electrification targets. The country has the largest number of electric vehicles in Europe necessitating extensive charging infrastructure. According to the German Federal Ministry for Economic Affairs and Climate Action, the government aims to install one million public charging points by 2030. Major energy companies and startups are investing heavily in fast charging networks along highways and in cities. As per the German Automotive Industry Association, the collaboration between automakers and energy providers is accelerating deployment. The country’s strong industrial base supports the manufacturing of charging equipment. According to Eurostat, Germany has the highest number of registered EVs in Europe driving corresponding charging demand. The focus on renewable energy integration ensures sustainable charging solutions. This combination of policy support and market size solidifies Germany’s dominance.

France EV Charging Stations Market Analysis

France occupied the second largest share of the Europe EV charging stations market in 2025. The French government has implemented the Advenir program which subsidizes the installation of charging points. According to the French Ministry of Ecological Transition, the country aims to have 400,000 public charging points by 2030. Major cities like Paris are expanding curbside charging to serve urban residents. As per the European Alternative Fuels Observatory, France has seen rapid growth in fast charging stations along motorways. The presence of manufacturers like Renault drives local demand. According to the French Platform for Automotive Industry, the integration of charging with renewable energy is a priority. This supportive policy environment maintains France’s strong market standing.

United Kingdom EV Charging Stations Market Analysis

The United Kingdom is estimated to hold a prominent share of the European EV charging stations market during the forecast period owing to its robust private sector investment and regulatory framework. The UK has banned the sale of new petrol and diesel cars by 2030 driving urgent infrastructure development. According to the UK Department for Transport, the number of public charging devices has grown significantly with a focus on rapid chargers. Private operators like BP Pulse and Shell Recharge are expanding networks. As per the Society of Motor Manufacturers and Traders, the UK has one of the highest densities of rapid chargers in Europe. The government’s plug in grant scheme supports home and workplace installations. According to the Office for National Statistics, the adoption of EVs is rising steadily. This dynamic market sustains the UK’s prominent position.

Netherlands EV Charging Stations Market Analysis

The Netherlands is projected to showcase a healthy CAGR in the European EV charging stations market over the forecast period owing to its early adoption and high density of charging points. The country has the highest ratio of chargers to EVs in Europe. According to the Dutch Ministry of Infrastructure and Water Management, the government has facilitated widespread deployment through public private partnerships. Cities like Amsterdam have extensive curbside charging networks. As per the European Alternative Fuels Observatory, the Netherlands leads in smart charging integration. The strong cycling culture complements micromobility and EV adoption. According to Statistics Netherlands, the high level of urbanization supports dense infrastructure. This mature market positions the Netherlands as a leader.

Sweden EV Charging Stations Market Analysis

Sweden is anticipated to record a notable CAGR in the European EV charging stations market over the forecast period. The high EV penetration and green energy focus are propelling the Swedish market expansion. The country has a comprehensive network of fast chargers along major routes. According to the Swedish Energy Agency, the government supports infrastructure development through grants and incentives. Volvo and Polestar drive local demand for charging solutions. As per Statistics Sweden, the share of electric cars in new sales is among the highest globally. The cold climate has spurred innovation in battery pre conditioning and charging efficiency. According to the European Battery Alliance, Sweden is a hub for sustainable charging technologies. This innovation driven approach strengthens Sweden’s market presence.

COMPETITIVE LANDSCAPE

The competition in the Europe ev charging stations market is highly fragmented and characterized by a mix of established energy utilities specialized charging network operators and automotive manufacturers. Major players compete on network density charging speed reliability and user experience to attract and retain customers. Energy companies leverage their existing infrastructure and customer bases to offer integrated energy solutions while specialized operators focus on technological innovation and service quality. Automotive manufacturers are increasingly entering the market to control the charging ecosystem and enhance brand loyalty. Strategic alliances and joint ventures are common as companies seek to share investment risks and accelerate network expansion. Regulatory compliance and access to government funding are critical differentiators in this capital intensive sector. Price competition is intensifying as operators strive to offer attractive tariffs and subscription models. Innovation in smart charging and vehicle to grid technologies provides opportunities for differentiation. The market is witnessing consolidation as larger entities acquire smaller players to expand their footprint. Continuous investment in technology and customer service is essential for maintaining competitive advantage in this dynamic environment.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe EV charging stations market are

- BYD (China)

- Ionity GmbH

- Allego NV

- EVBox (Netherlands)

- ChargePoint (US)

- Tesla (US)

- TGOOD (China)

- ENGIE (France)

- State Grid Corporation of China (China)

- BP (UK)

- Shell (UK)

- TotalEnergies (France)

- Enel X (Italy)

- Virta (Finland)

- Delta Electronics (Taiwan)

- Star Charge (China)

Top Players In The Market

- Ionity GmbH is a joint venture established by major automotive manufacturers including BMW Ford Mercedes Benz and Volkswagen Group to build a high power charging network across Europe. The company focuses on installing ultra fast charging stations with power outputs up to 350 kilowatts along major highways and transit routes. Ionity contributes to the global market by setting standards for interoperability and rapid charging reliability. Recent actions include expanding its network to cover remote areas and integrating renewable energy sources into its operations. The company has also partnered with local energy providers to ensure stable grid connections. By prioritizing high speed and cross border accessibility Ionity strengthens its position as a premium charging provider. Its strategic alliances with automakers ensure seamless integration with vehicle navigation systems enhancing user experience and reinforcing its leadership in the Europe ev charging stations market.

- Allego NV is a leading independent electric vehicle charging network operator with a significant presence in multiple European countries. The company offers a comprehensive portfolio of charging solutions ranging from standard AC chargers to ultra fast DC units for various customer segments. Allego contributes to the global market by demonstrating scalable business models for public and private charging infrastructure. Recent actions include the acquisition of Chargedot to enhance its technology platform and expand its footprint in key markets. The company also focuses on improving user experience through its mobile app which provides real time availability and seamless payment options. Allego collaborates with municipalities and businesses to deploy charging infrastructure in urban centers and workplaces. By leveraging data analytics for optimal site selection Allego strengthens its operational efficiency. This customer centric approach and strategic expansion solidify its competitive stance in the Europe ev charging stations market.

- Enel X Way SRL is a global leader in advanced energy services and a major player in the European electric vehicle charging sector. As a subsidiary of the Enel Group the company leverages extensive expertise in energy management and grid integration. Enel X Way contributes to the global market by offering innovative smart charging solutions that support grid stability and renewable energy integration. Recent actions include the expansion of its JuiceNet platform which enables intelligent load management and vehicle to grid capabilities. The company has also formed strategic partnerships with automotive manufacturers and fleet operators to provide tailored charging solutions. Enel X Way focuses on sustainability by powering its networks with renewable energy sources. By combining hardware installation with software driven energy services the company enhances value for customers. This holistic approach and technological innovation strengthen its market position in the Europe ev charging stations market.

Top Strategies Used by the Key Market Participants

Key players in the Europe ev charging stations market primarily employ strategic partnerships with automotive manufacturers and property developers to secure prime locations and ensure steady demand. Companies frequently invest in research and development to enhance charging speeds and integrate smart grid technologies. Another major strategy involves expanding network coverage through acquisitions of smaller regional operators to achieve economies of scale. Manufacturers also focus on improving user experience by developing intuitive mobile applications for seamless payment and station locating. Sustainability initiatives such as powering stations with renewable energy are increasingly used to align with regulatory requirements and consumer preferences. Additionally firms engage in lobbying efforts to shape favorable policies and secure government subsidies. These strategies aim to build brand loyalty optimize operational efficiency and establish a robust competitive presence in the rapidly evolving European landscape.

MARKET SEGMENTATION

This research report on the Europe electric vehicle charging station market is segmented and sub-segmented into the following categories.

By Level Of Charging

- Level 1

- Level 2

- Level 3

By Mode

- Mode 1

- Mode 2

- Mode 3

- Mode 4

By Connection Phase

- Single Phase

- Three Phase

By Dc Fast Charging Type

- Slow Dc

- Fast Dc

- Dc Ultrafast 1

- Dc Ultrafast 2

By Charging Point Type

- Ac Charging

- Dc Charging

By Application

- Private

- Semi-Public

- Public

By Installation Type

- Portable Chargers

- Fixed Chargers

By Charging Infrastructure Type

- Ccs

- Chademo

- Type 1

- Nacs

- Type 2

- Gb/T Fast

By Electric Bus Charging Type

- Off-Board Top-Down Pantographs

- Onboard Bottom-Up Pantographs

- Charging Via Connectors

By Charging Service Type

- EV Charging Services

- Battery Swapping Services

By Country

- UK

- Russia

- Germany

- Italy

- France

- Spain

- Sweden

- Denmark

- Poland

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What’s driving growth in Europe’s EV charging station market?

EU mandates (like AFIR and Fit-for-55), rising EV adoption (1 in 4 new cars sold in 2024 was electric), and national targets for public charger density are accelerating deployment—especially along TEN-T corridors.

How is the Alternative Fuels Infrastructure Regulation (AFIR) shaping the market?

AFIR requires EU member states to install 150 kW+ chargers every 60 km on major highways by 2025, and 350 kW+ by 2028—spurring massive public and private investment in fast-charging networks.

Are ultra-fast (350 kW) chargers becoming mainstream?

Yes—operators like IONITY, Fastned, and Shell Recharge are expanding 350 kW hubs, but utilization remains low outside highways. Most urban charging still relies on 50–150 kW DC or 11–22 kW AC.

Which countries lead in charging infrastructure?

Germany, France, the Netherlands, and Norway have the highest charger-per-EV ratios. The Nordics lead in renewable-powered charging, while Southern Europe is catching up rapidly.

Is interoperability improving for EV drivers?

Significantly—thanks to the EU’s eMobility roaming agreements and ISO 15118 standard, drivers can now use one RFID card or app across 90%+ of public networks in Western Europe.

What’s the biggest challenge for charging operators?

Grid connection delays and high demand charges—many sites face 6–18 month waits for grid upgrades, especially for high-power hubs in urban areas.

Are private investors entering the market?

Aggressively—oil majors (Shell, TotalEnergies), utilities (Enel, E.ON), and automakers (Volkswagen’s Elli, BMW-Ionity) are scaling networks, while startups focus on smart load management and V2G integration.

How is workplace and residential charging evolving?

The EU’s Energy Performance of Buildings Directive (EPBD) now mandates EV-ready wiring in all new buildings and major renovations—boosting AC charger installations in apartments and offices.

Is payment friction still an issue?

Less so—contactless (credit card) and plug-and-charge (ISO 15118) are now widely supported, reducing reliance on multiple apps or RFID cards.

What’s the outlook for 2026–2030?

Robust growth (~18% CAGR), with over 1 million public chargers expected by 2030 (up from ~600K in 2025). Key trends: AI-driven load balancing, solar-integrated stations, and dynamic pricing tied to grid demand.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com