Europe Emulsion Polymer Market Size, Share, Trends, & Growth Forecast Report By Type (Acrylics, Vinyl Acetate Polymer, SB Latex, Others), End Use Industries and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Emulsion Polymer Market Report Summary

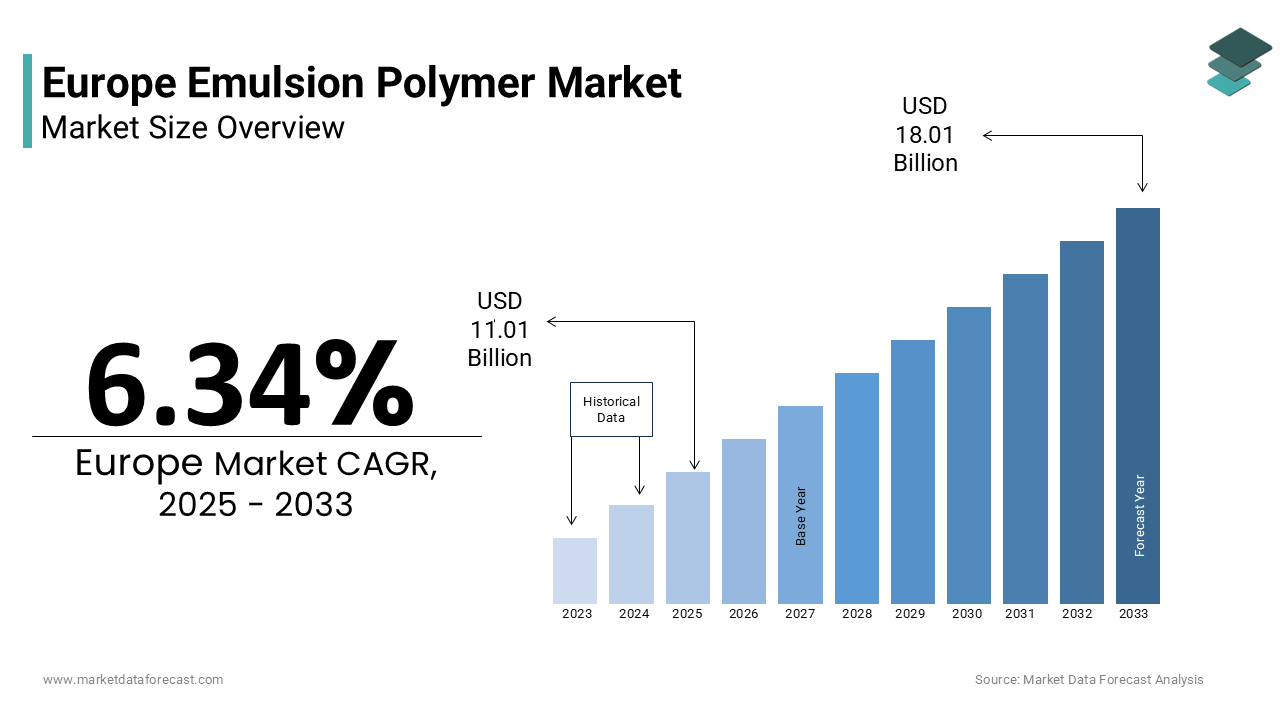

The Europe emulsion polymer market was valued at USD 10.36 billion in 2024, is estimated to reach USD 11.01 billion in 2025, and is projected to reach USD 18.01 billion by 2033, growing at a CAGR of 6.34% during the forecast period from 2025 to 2033. The growth of the Europe emulsion polymer market is driven by stringent environmental regulations promoting low-VOC materials, rising demand from the construction and coatings industries, and the widespread shift toward water-based formulations. Increasing renovation and infrastructure development, growing use of emulsion polymers in adhesives and paper coatings, and expanding adoption of sustainable and bio-based polymer dispersions are further fueling market growth. Moreover, regulatory initiatives under REACH and the European Green Deal are accelerating innovation in eco-friendly and high-performance emulsion polymer systems across Europe.

Key Market Trends

- Growing shift from solvent-based to water-based coatings and adhesives due to stringent EU VOC regulations.

- Rising adoption of acrylic and vinyl acetate emulsion polymers in construction and renovation applications.

- Increasing focus on bio-based and circular emulsion polymers to align with sustainability goals.

- Expanding use of emulsion polymers in paper, packaging, and recyclable adhesive applications.

- Technological advancements are improving the durability, weather resistance, and performance of emulsion formulations.

Segmental Insights

- Based on type, the acrylics segment was the largest and held a significant share of the Europe emulsion polymer market in 2024. The segment’s dominance is attributed to superior weather resistance, durability, and compliance with low-VOC regulations in architectural and industrial coatings.

- Based on end-use industry, the paints and coatings segment accounted for the largest share of the Europe emulsion polymer market in 2024. This is driven by high renovation activity, strict environmental standards, and strong demand for water-based decorative and protective coatings.

Regional Insights

The Europe emulsion polymer market is witnessing steady growth across major economies, supported by regulatory enforcement, construction activity, and sustainable material adoption.

- Germany was the largest contributor, accounting for a major share of the European emulsion polymer market in 2024, driven by its strong chemical manufacturing base, energy-efficient renovation programs, and high demand for compliant coatings and construction chemicals.

- France and the United Kingdom continue to perform strongly, supported by strict indoor air quality standards, large-scale renovation initiatives, and growing use of water-based adhesives and coatings.

- Italy and Spain are emerging as high-growth markets, fueled by renovation incentives, infrastructure upgrades, and increasing use of polymer-modified construction materials.

Competitive Landscape

The Europe emulsion polymer market is characterized by the presence of global chemical leaders and specialized regional manufacturers with strong technical expertise and regulatory compliance capabilities. Companies are focusing on sustainable product development, bio-based polymer innovation, and application-specific formulations to strengthen their market position. Strategic investments in R&D, partnerships with downstream industries, and expansion of eco-friendly product portfolios are key competitive strategies. Prominent players in the Europe emulsion polymer market include BASF, Dow, Arkema, Wacker Chemie AG, Synthomer, Allnex, OMNOVA Solutions, DIC Corporation, Celanese Corporation, Clariant, Asahi Kasei, The Lubrizol Corporation, Mallard Creek Polymers, 3M, and Trinseo.

Europe Emulsion Polymer Market Size

The europe emulsion polymer market size was valued at USD 10.36 billion in 2024 and is anticipated to reach USD 11.01 billion in 2025 from USD 18.01 billion by 2033, growing at a CAGR of 6.34% during the forecast period from 2025 to 2033.

Emulsion polymers include water-based dispersions of synthetic polymers such as acrylics, styrene, butadiene, vinyl acetate and vinyl versatate used as binders film formers and rheology modifiers across coatings adhesives construction and textile applications. Unlike solvent based systems these polymers offer lower volatile organic compound emissions aligning with the European Union’s stringent environmental regulations. According to the European Environment Agency, over 70% of decorative paints sold in the EU in 2023 were water-based formulations largely dependent on emulsion polymers. The market is further shaped by the EU’s REACH regulation which continuously evaluates chemical safety and restricts hazardous monomers like nonylphenol ethoxylates. As per Eurostat data, the construction sector accounted for 42% of total polymer consumption in the EU in 2023, which is indicating its role as a primary demand driver. Additionally, the European Green Deal’s Circular Economy Action Plan promotes recyclable and low impact materials pushing formulators to develop bio based and easily separable emulsion systems. These regulatory behavioral and industrial dynamics position emulsion polymers not as commodity chemicals but as enablers of compliant sustainable and high-performance end products across the European value chain.

MARKET DRIVERS

Stringent EU Environmental Regulations Accelerate Shift to Low VOC Formulations

The European Union’s comprehensive regulatory framework targeting air quality and chemical safety has become the foremost driver of emulsion polymer adoption by mandating the replacement of solvent-based systems across multiple industries. According to Directive 2004/42/EC, the EU limits volatile organic compound (VOC) content in decorative paints to 30 grams per liter for matte finishes, which is a threshold only achievable with advanced acrylic and styrene-acrylic emulsions. The Industrial Emissions Directive (2010/75/EU) further restricts VOC emissions from manufacturing facilities, compelling adhesive and coating producers to reformulate entire product lines. According to Germany’s Federal Environment Agency, 89% of architectural coatings sold domestically in 2023 were water-based, up from 62% in 2015, which is directly correlating with tightening VOC limits. Similarly, France’s Grenelle II Law prohibits solvent-based adhesives in public building projects and is driving demand for vinyl acetate ethylene (VAE) emulsions with superior open time and bond strength. As per the European Chemicals Agency, ongoing substance evaluations under REACH have led to the restriction or phase-out of over 45 monomers and additives, including legacy co-monomers such as butyl acrylate, accelerating innovation in safer alternatives like 2-ethylhexyl acrylate. This regulatory cascade transforms environmental compliance from a constraint into a catalyst for emulsion polymer innovation and substitution across Europe.

Robust Construction and Renovation Activity Sustains Demand for Building Chemicals

Europe’s sustained investment in residential and infrastructure development continues to fuel demand for emulsion polymers as essential components in construction chemicals, including exterior insulation finishing systems, tile adhesives, and renders, which is further boosting the growth of the European emulsion polymers market. According to Eurostat, the EU issued building permits for over 1.9 million new dwellings in 2023, with Germany, France, and Spain leading in volume. Simultaneously, the European Commission’s Renovation Wave Strategy targets upgrading 35 million buildings by 2030 to meet energy efficiency standards, which is a program that heavily relies on polymer-modified mortars and plasters. As per the Italian Revenue Agency, Italy’s Superbonus 110% tax incentive supported over 500,000 deep energy retrofits in 2023 alone, many requiring acrylic emulsion-based façade coatings for water resistance and breathability. Additionally, aging infrastructure necessitates repair as Germany’s Federal Ministry of Transport allocated €12 billion in 2023 for bridge and tunnel rehabilitation, where styrene-butadiene latexes enhance concrete durability. The European Committee for Standardization’s EN 1504 series mandates polymer modification for structural repair mortars, ensuring consistent technical demand. This confluence of new build activity, energy retrofitting, and civil maintenance secures emulsion polymers as indispensable enablers of modern sustainable construction across the continent.

MARKET RESTRAINTS

Restrictive REACH and CLP Classifications Increase Formulation Complexity

The European Union’s Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) framework imposes significant constraints on emulsion polymer composition by classifying certain monomers and additives as substances of very high concern (SVHCs), which is primarily hindering the growth of the European emulsion polymers market. According to the European Chemicals Agency, over 45 monomers commonly used in emulsion polymerization have faced authorization requirements or usage restrictions since 2020. This forces manufacturers to reformulate without compromising performance, which is a technically demanding process that extends development cycles and increases R&D costs. For example, replacing nonylphenol ethoxylate emulsifiers with bio-based alternatives often reduces colloidal stability, requiring co-stabilizers that may themselves face regulatory scrutiny. As per a 2023 survey by the European Polymer Federation, 68% of formulators reported delays in product launches due to REACH compliance assessments. Furthermore, the Classification, Labelling and Packaging (CLP) Regulation mandates hazard communication for residual monomers even at parts-per-million levels, complicating safety data sheet preparation and customer acceptance. These administrative and technical burdens disproportionately affect small and medium enterprises that lack dedicated regulatory affairs teams, thereby slowing innovation and increasing market concentration among larger players with compliance infrastructure.

Volatility in Petrochemical Feedstock Pricing Impacts Cost Stability

The European emulsion polymer market remains highly sensitive to fluctuations in crude oil and natural gas-derived feedstocks such as styrene, butadiene, and acrylic acid, whose prices are subject to geopolitical disruptions and energy policy shifts. According to the European Central Bank, petrochemical input costs for polymer producers exhibited a standard deviation of 18% between 2021 and 2023, driven by the Russia–Ukraine conflict and EU carbon pricing mechanisms. As per Platts European Petrochemical Analysis, European styrene prices surged by 62% in 2022 following gas rationing in Germany, which led to the idling of steam crackers. Although emulsion polymers contain 40–60% water, their performance is dictated by the synthetic backbone, making cost pass-through difficult in price-sensitive segments like construction adhesives. As per a 2024 study by the German Chemical Industry Association, 54% of emulsion producers absorbed raw material price spikes rather than risk customer loss. Unlike bio-based alternatives, which offer partial insulation, feedstock diversification remains limited due to performance gaps and scale constraints. This exposure to fossil fuel markets introduces persistent cost unpredictability that undermines long-term supply agreements and investment planning across the value chain.

MARKET OPPORTUNITIES

Development of Bio-Based and Circular Emulsion Polymers Opens New Applications

The push toward circularity and renewable content is creating significant opportunities for the Europe emulsion polymer market growth. According to the European Bioplastics Association, bio-based polymer production in the EU grew by 19% in 2023, with emulsion systems leading adoption in pressure-sensitive adhesives and textile binders. Companies such as BASF and Arkema have commercialized acrylic emulsions using lactic acid or tall oil derivatives, achieving up to 50% renewable carbon content, as verified by ASTM D6866 testing. The European Commission’s Packaging and Packaging Waste Regulation further incentivizes recyclable formulations with water-based adhesive labels using vinyl acetate emulsions enable clean paper deinking, which is a critical requirement for fiber recycling, as documented by CEPI, the European Paper Federation. Additionally, Horizon Europe research consortia are developing enzymatically cleavable emulsion films that disintegrate during mechanical recycling, preserving material value. In the Netherlands, a pilot with DSM demonstrated that bio-based styrene-acrylic dispersions met EN 13501 fire safety standards for interior coatings. These innovations position emulsion polymers at the forefront of the EU’s transition to bio-based, circular, and non-toxic material systems.

Expansion of High-Performance Applications in Medical and Electronics

Emerging demand for emulsion polymers in precision industrial sectors such as medical devices and flexible electronics is a high-value growth frontier for the Europe emulsion polymer market. According to the European Medical Devices Coordination Group, water-based acrylic and polyurethane dispersions are increasingly used as binders in transdermal patches, wound dressings, and diagnostic test strips due to their skin compatibility and controlled drug release profiles. The EU Medical Devices Regulation (MDR) mandates full material disclosure and biocompatibility testing, which emulsion systems satisfy through low residual monomer content and absence of solvent residues. In electronics, the shift toward printed and flexible circuits relies on conductive inks stabilized by vinyl acetate ethylene (VAE) emulsions, which prevent nanoparticle agglomeration and enable low-temperature curing. A 2024 Eureka Eurostars project demonstrated that emulsion-based silver inks achieved 25% higher conductivity than solvent alternatives on PET substrates. Germany’s Fraunhofer Institute reported that over 30 European medical startups adopted tailored emulsion polymers in 2023 for wearable health monitors. These applications command premium pricing and foster deep technical collaboration between polymer suppliers and end users, creating sticky customer relationships and differentiation beyond commodity performance.

MARKET CHALLENGES

Fragmented End-User Requirements Hinder Standardized Product Development

The European emulsion polymer market faces persistent challenges in product standardization due to highly divergent performance expectations across application segments and national construction norms. A single polymer grade cannot simultaneously meet the freeze-thaw stability required for Scandinavian exterior paints, the high shear adhesion demanded by Italian tile installers, and the low foaming profile needed for German machine-applied renders. According to the European Construction Chemicals Association, over 120 national and regional technical approvals govern construction chemical formulations, creating a patchwork of test methods and performance thresholds. In adhesives, the EN 204 classification system defines four durability classes, but individual countries impose additional requirements. France mandates VOC limits below 10 g/L for wood adhesives, while Poland allows up to 30 g/L. This fragmentation forces suppliers to maintain extensive product portfolios with minor compositional tweaks, increasing inventory complexity and quality control costs. A 2023 survey by FEICA found that 72% of adhesive formulators customized emulsion recipes for specific national markets. Until harmonization advances through European Technical Assessments or CE marking expansions, manufacturers will continue bearing the inefficiency of localized development in an otherwise integrated single market.

Limited Industrial-Scale Production of Sustainable Alternatives Constrains Transition

Despite strong regulatory and consumer pull toward greener emulsion polymers, the industrial-scale availability of bio-based monomers and circularly designed dispersions remains insufficient to support broad substitution, which is further challenging the expansion of the Europe emulsion polymer market. According to the European Renewable Fuels Association, less than 5% of acrylic acid used in EU polymer production in 2023 was derived from renewable sources, due to limited fermentation capacity and high production costs. Bio-ethylene from sugarcane, while commercially available, is primarily allocated to polyethylene rather than vinyl acetate monomer synthesis, as per the European Biofuels Technology Platform. Furthermore, recycling infrastructure for post-consumer polymer dispersions is virtually nonexistent as water-based coatings and adhesives are typically incinerated or landfilled, as separation from substrates is economically unviable. A 2024 study by the Dutch Institute for Sustainable Process Technology concluded that less than 2% of emulsion polymers in construction applications are recoverable with current technology. While pilot projects like Carbios’ enzymatic depolymerization show promise, they remain at lab scale. This supply-side bottleneck means that even willing formulators cannot achieve high bio-content or circularity without compromising performance or cost competitiveness. Until integrated biorefineries and collection systems mature, the sustainability transition in emulsion polymers will remain aspirational rather than operational across Europe.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 7.84% |

| Segments Covered | By Type, End Use Industries and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | BASF, Dow, Arkema, Wacker Chemie AG, Synthomer, Allnex, OMNOVA Solutions, DIC Corporation, Celanese Corporation, Clariant, Asahi Kasei, The Lubrizol Corporation, Mallard Creek Polymers, 3M, and Trinseo. |

SEGMENTAL ANALYSIS

By Type Insights

The acrylics segment commanded for the highest share of the Europe emulsion polymer market in 2024 due to their exceptional balance of durability, weather resistance, and low environmental impact across architectural and industrial coatings. Over 65% of water-based decorative paints sold in the EU in 2023 utilized pure or styrene-modified acrylic emulsions as primary binders. As per Apollo Research, acrylics accounted for approximately 46.9% of the total market value in 2023, contributing €4.72 billion to the regional emulsion polymer economy. Their dominance is reinforced by compliance with stringent VOC directives. Directive 2004/42/EC limits interior matte paint emissions to 30 grams per liter, a threshold easily met by modern acrylic dispersions with engineered glass transition temperatures that eliminate the need for co-solvents. Additionally, acrylic polymers exhibit superior UV stability compared to alternatives, preventing chalking and yellowing on exterior facades. In Germany, the Federal Environment Agency reported that 92% of facade renovation projects under the KfW energy efficiency program specified acrylic-based exterior paints for their breathability and thermal shock resistance. The versatility of acrylic chemistry also enables customization as cationic variants improve adhesion to metal substrates, while self-crosslinking grades enhance scrub resistance in high-traffic areas. This combination of regulatory alignment, performance adaptability, and architectural necessity solidifies acrylics as the backbone of Europe’s emulsion polymer demand.

The vinyl acetate polymers segment is the fastest growing type segment and is predicted to witness a CAGR of 6.65% over the forecast period owing to the growing demand in construction adhesives, paper coatings, and nonwoven binders, where their cost-performance balance and low toxicity offer distinct advantages. In the building sector, vinyl acetate ethylene (VAE) copolymers are increasingly specified for tile adhesives and wood bonding due to their high initial tack and flexibility. As per France’s CSTB technical approval agency, over 180 VAE-based adhesive formulations were certified in 2023 for use in public housing projects. Additionally, the EU’s REACH regulation restricting formaldehyde-based resins in wood products has shifted panel manufacturers toward polyvinyl acetate dispersions, which contain no added aldehydes. In paper recycling, the European Paper Federation documented that VAE binders enable 99.5% deinking efficiency, preserving fiber quality, which is a critical factor as the EU mandates 75% paper packaging recycling by 2025. Furthermore, innovations such as vinyl acetate versatate copolymers offer enhanced water resistance, expanding use into exterior applications. This convergence of regulatory substitution, performance refinement, and circular economy alignment propels vinyl acetate polymers as Europe’s most dynamically expanding emulsion segment.

By End Use Industry Insights

The paints and coatings segment occupied for the largest share of the European emulsion polymers market in 2024. The dominance of the paints and coatings segment in this regional market is driven by regulatory mandates for low-VOC formulations, extensive renovation activity, and high-performance demands in both decorative and protective applications. Water-based coatings accounted for 78% of all architectural paint sales in the EU in 2023, with emulsion polymers serving as the essential film-forming component. The EU Paints Directive enforces strict VOC limits that have rendered solvent-based systems nonviable for most residential and commercial projects. As per Germany’s Federal Ministry for Housing, over 540,000 residential energy retrofit permits were issued in 2023, many of which required exterior insulation systems bound with acrylic or silicone-acrylic emulsions to ensure vapor permeability and crack bridging. Similarly, infrastructure protection relies on styrene-butadiene latex-modified coatings for chemical and abrasion resistance, as documented by the European Federation of Corrosion. The segment’s scale is further amplified by professional applicator preference for water-based systems due to easier cleanup and reduced odor. This regulatory, industrial, and behavioral alignment ensures paints and coatings remain the primary consumption channel for emulsion polymers across Europe.

The adhesives and sealants segment is estimated to register a CAGR of 7.04% over the forecast period in this regional market owing to the structural shifts in construction toward prefabrication, energy-efficient assemblies, and sustainable material bonding. The European Commission’s Renovation Wave Strategy promotes modular building techniques that rely heavily on high-strength emulsion-based adhesives for bonding insulation panels, wood composites, and ceramic tiles. In Italy, over 60% of Superbonus-funded retrofits in 2023 used polymer-modified tile adhesives meeting EN 12004 C2TE classification for deformable, high-adhesion performance, as per the Italian National Institute of Building. Additionally, the EU Ecolabel for adhesives restricts solvent content to below 5%, driving substitution toward vinyl acetate and acrylic dispersions. The rise of engineered wood products further boosts demand, as formaldehyde-free polyvinyl acetate emulsions replace urea-formaldehyde resins under REACH restrictions. In Germany, the Wood Based Panel Association reported a 22% year-on-year increase in PVA-bonded panel production in 2023. These forces transform adhesives from a niche application into a high-growth vector for emulsion polymer innovation and volume.

REGIONAL ANALYSIS

Germany Emulsion Polymer Market Analysis

Germany led the market by holding 23.9% of the regional market share in 2024. The dominance of Germany in the European market is attributed to its advanced chemical manufacturing base, producing over 35% of the EU’s synthetic polymers, with major facilities operated by BASF, Wacker, and Dow. Demand is further fuelled by Germany’s leadership in energy-efficient construction, with 540,000 renovation permits issued in 2023, which is driving widespread use of acrylic and styrene-butadiene emulsions in insulation systems and facade coatings. Regulatory pressure under REACH and the Chemicals Prohibition Ordinance has accelerated the shift toward safer, low-VOC formulations. Germany’s dual education system produces over 12,000 chemistry and materials science graduates annually, ensuring a steady pipeline of skilled professionals. The presence of equipment manufacturers like Hosokawa and Glatt supports localized pilot-scale testing and process optimization. This synergy of industrial scale, regulatory leadership, and technical talent cements Germany’s position as Europe’s emulsion polymer powerhouse.

France Emulsion Polymer Market Analysis

France held the second largest share of the European emulsion polymer market in 2024. The growth of France in this regional market is driven by proactive sustainability policies and strong institutional demand. The MaPrimeRénov scheme funded over 700,000 home energy retrofits in 2023, mandating certified low-VOC coatings and adhesives. The CSTB technical certification body evaluated over 180 vinyl acetate-based adhesive formulations in 2023, ensuring compliance with EN standards. France enforces some of the EU’s strictest indoor air quality regulations, with Decree 2011-389 requiring A+ emission labels on all interior products, which is accelerating the adoption of formaldehyde-free emulsion binders. Domestic producers like Arkema lead in bio-based acrylic dispersions, while the construction of over 100,000 social housing units annually sustains demand for durable, cost-effective polymer systems. These policy-driven dynamics make France a high-compliance, high-volume market for advanced emulsion polymers.

Italy Emulsion Polymer Market Analysis

Italy is expected to account for a prominent share of the European market over the forecast period owing to its robust renovation activity and industrial specialization. Over 500,000 deep energy retrofits were completed in 2023 under the Superbonus 110% tax incentive, requiring polymer-modified renders and tile adhesives compliant with EN 12004 C2TE standards. Italy is the EU’s largest ceramic tile producer, accounting for 30% of continental output, with widespread use of vinyl acetate-ethylene emulsions for flexible, water-resistant installation. The engineered wood sector is also transitioning to formaldehyde-free bonding, with a 25% increase in PVA emulsion usage reported in 2023. Southern regions such as Sicily and Puglia allocated €1.2 billion for school and hospital upgrades, further boosting demand for durable facade coatings. This blend of fiscal stimulus, industrial depth, and regional investment ensures Italy’s diversified demand for emulsion polymers.

United Kingdom Emulsion Polymer Market Analysis

The United Kingdom maintains a strong position in the European emulsion polymer market owing to the infrastructure renewal, regulatory continuity, and industrial specialization. Over 220,000 residential renovation projects were completed in 2023, many specifying water-based coatings to comply with Building Regulations Part L. The UK’s aging infrastructure drives demand for styrene-butadiene latex-modified coatings for concrete repair. The country also leads Europe in paper recycling, with a 71% collection rate, increasing the use of VAE binders for efficient deinking. In the professional decorating sector, over 80% of trade paint sales are water-based, favored for their low odor and scrub resistance. Despite Brexit, the UK remains aligned with EU VOC directives, ensuring continued demand for compliant emulsion systems.

Spain Emulsion Polymer Market Analysis

Spain is expected to exhibit a notable CAGR in the European market over the forecast period owing to the building rehabilitation, tourism-fueled construction, and coastal infrastructure upgrades. The Plan de Vivienda scheme supported over 320,000 home energy upgrades in 2023, requiring breathable acrylic-based exterior paints suited to Mediterranean climates. Spain’s tourism sector has spurred hotel renovations and new resort construction, where low-odor coatings are mandated for indoor spaces. Coastal cities like Barcelona and Valencia are investing in sea-level rise adaptation, specifying polymer-modified renders for salt spray resistance. The paper industry is also expanding recycled content, with over 75% of graphic paper now containing post-consumer fiber, increasing demand for deinkable VAE emulsions. The 2023 Industrial Emissions Register tightened VOC limits for small applicators, accelerating the shift to emulsion systems. These intersecting drivers of climate adaptation, tourism, and circularity position Spain as a high-growth emulsion polymer market in Southern Europe.

COMPETITIVE LANDSCAPE

Competition in the Europe emulsion polymer market is characterized by a blend of global chemical giants regional specialists and emerging bio-based innovators vying through technical differentiation regulatory foresight and sustainability credentials. Unlike commoditized segments success here hinges on the ability to balance performance purity and compliance across fragmented end use sectors such as construction paper and coatings. Incumbents like BASF and Wacker leverage scale integrated production and decades of application expertise while challengers like Synthomer and Trinseo focus on niche high margin segments such as medical binders or recyclable adhesives. The regulatory environment acts as both a barrier and a catalyst. REACH VOC and Ecolabel requirements raise entry costs but reward agile reformulation. Collaboration is common with suppliers working closely with CSTB DIBt and CEPE to navigate technical approvals. Ultimately competition revolves not around price but around trust in safety consistency and future proofing against Europe’s rapidly evolving chemical policy landscape.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the europe emulsion polymer market include

- BASF

- Do

- Arkema

- Wacker Chemie AG

- Synthome

- Allnex

- OMNOVA Solutions

- DIC Corporation

- Celanese Corporation

- Clariant

- Asahi Kasei

- The Lubrizol Corporation

- Mallard Creek Polymers

- 3M

- Trinseo

Top Players in the Market

BASF SE

BASF SE is a German multinational and a global leader in chemical innovation with a deeply integrated presence in the Europe emulsion polymer market. The company supplies a wide portfolio of acrylic vinyl acetate and styrene butadiene dispersions tailored for coatings adhesives and construction applications. BASF contributes globally by pioneering sustainable polymer technologies including bio-based monomers and low residual emulsion systems compliant with EU REACH and VOC directives. In 2024 BASF expanded its Acronal portfolio with a new generation of formaldehyde free acrylic binders for interior paints featuring enhanced scrub resistance and ultra-low emissions. The company also launched a digital formulation assistant to help European formulators accelerate compliance with national building regulations. These initiatives reinforce BASF’s role as a technology and sustainability enabler in both European and global emulsion polymer value chains.

Arkema SA

Arkema SA a French specialty chemicals company is a key player in the Europe emulsion polymer market renowned for its high performance and bio sourced polymer dispersions. Its EnVia and Cevian product lines serve architectural coatings paper treatment and sustainable adhesives with a strong emphasis on circularity and reduced carbon footprint. Arkema contributes globally by advancing the use of renewable carbon in emulsion polymers achieving up to 50% bio content in certain acrylic grades verified by third party certification. In early 2024 Arkema inaugurated a dedicated emulsion innovation center in Gennevilliers France focusing on low VOC and recyclable binder technologies aligned with the EU Green Deal. It also partnered with European paper recyclers to optimize deinking efficiency using tailored vinyl acetate systems. These actions position Arkema at the forefront of the ecological transition in polymer science across Europe and beyond.

Wacker Chemie AG

Wacker Chemie AG a German chemical manufacturer holds a strategic position in the Europe emulsion polymer market through its VINNAPAS brand of vinyl acetate and ethylene-based dispersions. The company specializes in high purity low emission binders for construction adhesives tile bonding and eco-friendly interior paints. Wacker contributes globally by setting benchmarks in polymer purity and consistency essential for sensitive applications like medical nonwovens and food contact paper coatings. In 2023 Wacker enhanced its production site in Burghausen Germany with a new energy efficient reactor line reducing CO2 emissions by 15% per ton of emulsion produced. It also introduced a digital batch traceability system enabling real time compliance with EU chemical safety regulations. These investments strengthen Wacker’s reputation for quality sustainability and regulatory excellence in European and international markets.

Top Strategies Used by the Key Market Participants

Key players in the Europe emulsion polymer market prioritize the development of low VOC and formaldehyde free formulations to comply with EU environmental directives and national building codes. They invest in bio-based monomer integration to increase renewable carbon content while maintaining performance parity with fossil-based systems. Companies establish regional innovation centers to co-develop application specific solutions with local formulators and end users. Strategic partnerships with paper recyclers construction certifiers and adhesive assemblers ensure alignment with downstream circularity requirements. Additionally, firms deploy digital tools for formulation support regulatory compliance tracking and batch traceability to enhance customer service and operational transparency in a highly regulated landscape.

MARKET SEGMENTATION

This research report on the europe emulsion polymer market has been segmented and sub–segmented into the following categories.

By Type

- Acrylics

- Vinyl Acetate Polymer

- SB Latex

- Others

By End Use Industries

- Paints & Coatings

- Adhesives & Sealants

- Paper & Paperboard

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is an emulsion polymer?

An emulsion polymer is a polymer produced through emulsion polymerization, where monomers are polymerized in water using surfactants and initiators to form stable polymer dispersions.

What is driving the growth of the Europe emulsion polymer market?

The market is driven by increasing demand from paints & coatings, adhesives, construction materials, and the shift toward water-based and environmentally friendly products.

Which industries are the major end users of emulsion polymers in Europe?

Key end-use industries include paints & coatings, construction, adhesives & sealants, textiles, paper & packaging, and automotive.

Why are emulsion polymers preferred over solvent-based polymers?

Emulsion polymers offer low VOC emissions, better environmental compliance, improved safety, and cost-effective processing compared to solvent-based polymers.

What are the major types of emulsion polymers used in Europe?

Major types include acrylic polymers, styrene-butadiene latex (SBL), vinyl acetate polymers, and vinyl acetate-ethylene (VAE) emulsions.

Which application segment holds the largest share in Europe?

Paints and coatings represent the largest application segment due to extensive use in residential, commercial, and industrial construction.

What challenges does the Europe emulsion polymer market face?

Challenges include raw material price volatility, high R&D costs, and competition from alternative polymer technologies.

Which European countries are major contributors to the market?

Germany, France, the UK, Italy, and Spain are key contributors due to strong industrial, automotive, and construction activities.

What is the competitive nature of the Europe emulsion polymer market?

The market is moderately consolidated, with global chemical majors and regional specialty polymer manufacturers competing on performance and sustainability.

What is the future outlook of the Europe emulsion polymer market?

The market is expected to witness steady growth, supported by green construction, eco-friendly coatings, and technological advancements.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com