Europe Energy Market Research Report By End-User ( Industrial Sector, Residential Sector ) Energy Sources & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of EU) - Industry Analysis From 2026 to 2034

Market Size, 2025

$1.48 BnMarket Estimate, 2026

$1.56 BnMarket Forecast, 2034

$2.35 BnCAGR, 2026–2034

5.23%Europe Energy Market Size

The Europe Energy Market Size was valued at USD 1.48 billion in 2025, is expected to have 5.23 % CAGR from 2026 to 2034, and be worth USD 2.35 billion by 2034 from USD 1.56 billion in 2026.

The Europe energy market includes traditional fossil fuels such as coal, oil, and natural gas, alongside rapidly expanding renewable energy sources like wind, solar, hydroelectric, and bioenergy. The market is undergoing a significant transformation driven by environmental concerns, regulatory mandates, and technological advancements aimed at reducing carbon emissions and achieving energy independence. Besides, geopolitical tensions—particularly those involving energy supply disruptions from Russia—have accelerated efforts to diversify energy sources. Countries like Germany and France have significantly ramped up investments in offshore wind and nuclear energy alternatives. Meanwhile, the European Commission’s REPowerEU Plan has set ambitious targets to reduce dependency on imported fossil fuels while boosting domestic production of green hydrogen and renewables. With rising consumer awareness about sustainability, growing electrification of transport, and increasing digitalization of grid infrastructure, the Europe energy market is positioned at a critical juncture. Governments, private sector players, and consumers are collectively shaping a future that prioritizes cleaner, smarter, and more resilient energy systems.

MARKET DRIVERS

Strong Policy Support and Regulatory Push Toward Renewable Energy

One of the primary drivers of the Europe energy market is the robust policy framework and regulatory initiatives aimed at accelerating the transition to renewable energy sources. The European Union has been at the forefront of setting binding climate and energy targets under the European Green Deal , which aims to make Europe climate-neutral by 2050. As per the European Environment Agency , in 2023, renewable energy accounted for over 22% of total energy consumption in the EU , surpassing earlier projections due to strong implementation of national energy and climate plans. Moreover, financial incentives such as subsidies, tax credits, and feed-in tariffs have encouraged both public and private sector participation in renewable energy deployment.

Rising Energy Demand Due to Electrification and Digitalization Trends

Another key driver fueling the Europe energy market is the growing demand for electricity driven by the widespread electrification of transportation, heating, and industrial processes, alongside rapid digitalization of infrastructure and services. The European Data Centre Association reported in 2025that data centers across Europe consumed approximately 3% of the region's total electricity , a figure expected to grow as cloud computing and artificial intelligence applications expand. Similarly, the European Automobile Manufacturers’ Association (ACEA) noted that sales of electric vehicles surged in 2025compared to the previous year , significantly increasing electricity demand for charging infrastructure. In response, governments and utilities are investing heavily in upgrading grid capacity and integrating variable renewable energy sources to meet this rising demand sustainably. The European Network of Transmission System Operators for Electricity (ENTSO-E) emphasized that enhanced interconnectivity and grid modernization will be essential to manage the load from new energy-intensive sectors .

MARKET RESTRAINTS

Geopolitical Instability and Fossil Fuel Supply Disruptions

A major restraint affecting the Europe energy market is the ongoing geopolitical instability that impacts the availability and pricing of fossil fuels, particularly natural gas and oil. Historically reliant on imports from Russia, Europe faced severe energy shocks following the conflict in Ukraine, leading to volatile prices and supply shortages. According to the European Commission , in 2022, Russia supplied nearly 40% of the EU’s natural gas imports , a dependency that became increasingly untenable due to sanctions and political tensions. This led to sharp increases in energy costs, with household electricity prices rising in some regions in 2023. While efforts have been made to diversify supply through liquefied natural gas (LNG) imports from the U.S., Qatar, and Africa, infrastructure limitations and global competition for LNG have constrained immediate relief. The International Energy Agency (IEA) noted that European LNG import capacity remains below required levels to fully replace pipeline gas from Russia , limiting flexibility during peak demand periods.

High Upfront Costs and Long Development Timelines for Renewable Projects

Another critical constraint impeding the growth of the Europe energy market is the high capital expenditure and lengthy approval timelines associated with developing renewable energy infrastructure. While long-term benefits of clean energy are well-documented, the initial investment required for wind farms, solar parks, battery storage, and grid upgrades often poses a barrier to rapid deployment. Additionally, regulatory hurdles, permitting delays, and community opposition have slowed project execution.

MARKET OPPORTUNITIES

Expansion of Offshore Wind Power Across Coastal Member States

An emerging opportunity shaping the future of the Europe energy market is the rapid expansion of offshore wind power, particularly in coastal nations such as the UK, Germany, Denmark, and the Netherlands. With abundant wind resources and favorable policy environments, offshore wind is becoming a cornerstone of Europe’s energy strategy.

According to the European Wind Energy Association (WindEurope) , planned offshore wind projects across Europe could deliver more than 250 GW of capacity by 2040 , enough to power over 230 million households. Several countries have already committed billions in funding to support this growth, including Germany’s "Wind at Sea" initiative , which aims to install 30 GW of offshore wind by 2030. Moreover, technological advancements in turbine design, floating platforms, and grid integration are reducing costs and improving efficiency.

Growth of Green Hydrogen as a Decarbonization Tool

Another transformative opportunity within the Europe energy market lies in the development and deployment of green hydrogen as a key enabler of deep decarbonization across hard-to-abate sectors such as steelmaking, shipping, aviation, and heavy industry.

According to the Hydrogen Europe association, the EU aims to deploy 40 GW of electrolyzer capacity by 2030 , producing hydrogen using renewable electricity and eliminating carbon emissions from industrial and transport applications. Several countries, including Spain, Portugal, and Poland, have launched national hydrogen strategies to attract investment and establish themselves as regional production hubs.

MARKET CHALLENGES

Grid Infrastructure Limitations Hindering Renewable Integration

A major challenge facing the Europe energy market is the aging and insufficient grid infrastructure, which hampers the efficient integration and distribution of renewable energy across the continent. As intermittent sources like wind and solar become increasingly dominant, the existing transmission and distribution networks struggle to accommodate fluctuations in supply and demand. These constraints lead to curtailment of renewable output and higher balancing costs, reducing the overall efficiency of the system. Moreover, the lack of cross-border interconnections limits the ability to transfer surplus renewable energy from high-generation zones to areas experiencing deficits. The European Commission identified that only a small percentage of planned interconnector projects were completed on schedule , citing bureaucratic delays and insufficient funding as key obstacles.

Social and Environmental Opposition to New Energy Infrastructure

Another critical challenge influencing the Europe energy market is the growing social and environmental resistance to new energy infrastructure, particularly in relation to wind farms, power lines, and mining for critical minerals needed for energy transition technologies. Public opposition has delayed numerous renewable energy projects, especially onshore wind and solar farms, due to concerns about visual impact, noise, land use, and biodiversity disruption. According to WindEurope , more than half of all proposed onshore wind projects in France and Germany faced legal or administrative challenges in 2025, contributing to slower-than-expected capacity additions. Similarly, the extraction of raw materials such as lithium, cobalt, and rare earth metals—essential for batteries, turbines, and electric vehicles—has sparked environmental concerns. The European Environment Agency noted that mining activities linked to green technologies raised over 150 environmental lawsuits in 2025, slowing down resource availability and increasing input costs.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By End-User, Energy Sources and Country. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, Germany, Italy, France, Spain, Sweden, Denmark, Poland, Switzerland, Netherlands, Rest of Europe. |

| Market Leaders Profiled | Enel, EDF, E.ON, RWE, Iberdrola, Vattenfall, Fortum |

SEGMENT ANALYSIS

By End-User Insights

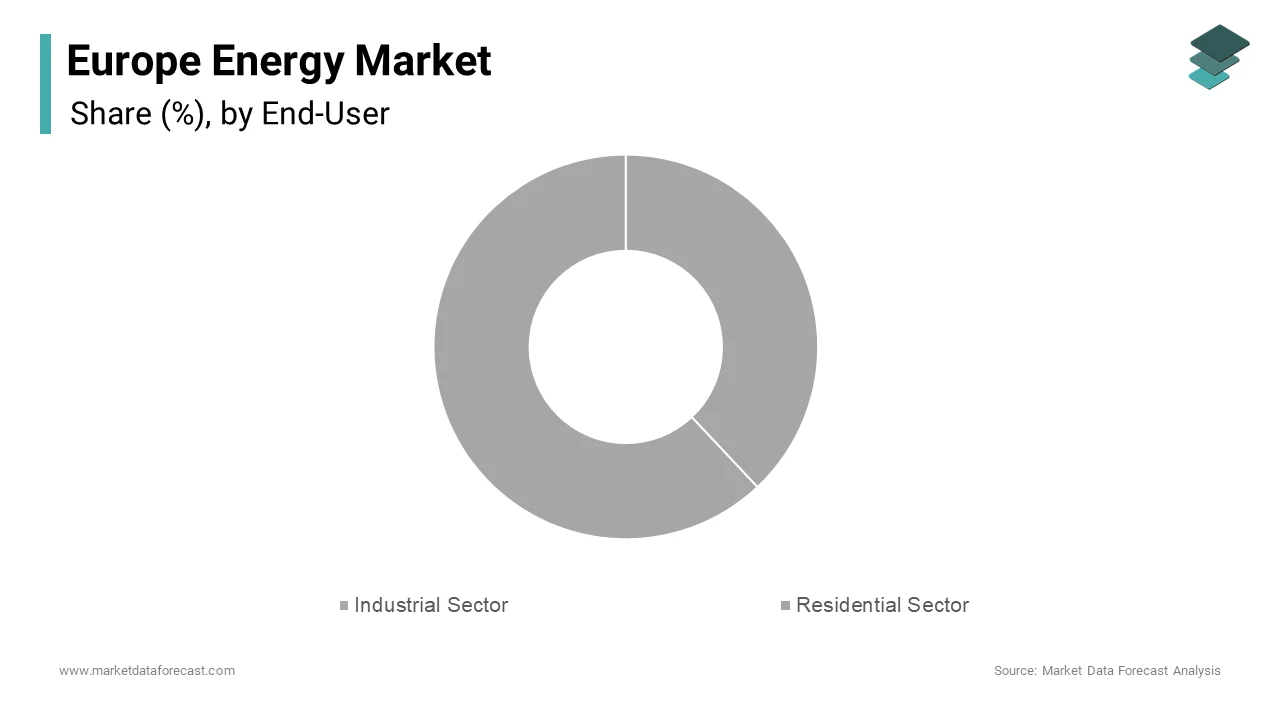

The industrial sector represented the biggest end-user segment in the Europe energy market by accounting for a 38.4% of total energy consumption in 2025. This dominance stems from the high energy demands of manufacturing, chemical processing, steelmaking, and heavy industry, which collectively form the backbone of several European economies. Countries such as Germany, Italy, and Poland rely heavily on energy-intensive industries. Moreover, the ongoing shift toward electrification and process heating using renewable energy sources is reshaping industrial energy consumption patterns.

The residential sector is the rapidly expanding end-user segment in the Europe energy market, calculated to rise at a CAGR of 6.2%. This growth is propelled by increased adoption of electric heating systems, smart home technologies, and the rise in remote working, all of which have elevated household energy consumption. In addition, the European Data Centre Association noted that home data usage increased notably, further contributing to higher residential electricity loads. A 2025survey by Eurobarometer found that over 60% of European households had adopted at least one energy-efficient appliance in the past three years , reflecting a broader trend toward electrified and connected living environments.

By Energy Sources Insights

The renewables segment held the largest share of the Europe energy market by capturing a 41.3% of total energy production and consumption in 2025. This leading position is primarily driven by aggressive policy support, technological advancements, and growing public awareness about sustainability and climate change. One key driver behind this segment’s dominance is the European Union's binding target to achieve at least 42.5% renewable energy share in final energy consumption by 2030, as outlined in the Renewable Energy Directive (RED III). According to the European Environment Agency , renewables already contributed over 22% of total energy use across EU member states in 2025, with wind and solar leading the charge. Apart from these, investment in clean energy has surged, supporting large-scale wind farms, photovoltaic installations, and green hydrogen initiatives. The International Renewable Energy Agency (IRENA) highlighted that Europe added more than 35 GW of new renewable capacity in 2025alone , reinforcing its role as a global leader in clean energy transition.

The renewables segment is also the fastest-growing within the Europe energy market by expanding at a CAGR of 8.7% between 2025 and 2033. This rapid growth trajectory is underpinned by ambitious decarbonization goals, falling technology costs, and increasing electrification across sectors. According to the European Wind Energy Association (WindEurope) , offshore wind capacity alone is expected to grow by more than 250 GW by 2040 , supported by national strategies from countries like Germany, France, and Poland. In 2023, solar PV installations reached record levels , with over 50 GW of new capacity added across the continent , as reported by SolarPower Europe. Another major factor fueling this expansion is the decline in the levelized cost of wind and solar , which has made them more competitive than fossil fuels in many regions. The Fraunhofer Institute for Solar Enery Systems noted that onshore wind and utility-scale solar are now the cheapest sources of electricity generation in most European countries , accelerating adoption rates. Furthermore, corporate procurement of renewable energy through Power Purchase Agreements (PPAs) has gained momentum.

COUNTRY LEVEL ANALYSIS

Germany held the top position in the Europe energy market by capturing a 22.5% of total regional energy consumption in 2023. As Europe’s largest economy and a major industrial hub, Germany’s energy demand is driven by its extensive manufacturing base, chemical industry, and growing reliance on digital infrastructure. The country has been phasing out coal and nuclear power while significantly ramping up investments in wind and solar. The German Wind Energy Association (BWE) reported that wind power alone supplied more than 25% of Germany’s electricity needs in 2023, highlighting the nation's leadership in renewable integration. Also, Germany plays a pivotal role in cross-border energy trade, acting as a key transit country for gas and electricity. The European Network of Transmission System Operators for Electricity (ENTSO-E) indicated that Germany exported over 100 TWh of electricity to neighboring countries in 2025, underscoring its strategic importance in regional energy flows.

France has a strong nuclear infrastructure and green transition. The country's unique energy profile is dominated by its robust nuclear infrastructure. However, recent policy shifts have seen France diversifying its energy mix. Simultaneously, France is investing heavily in green hydrogen and small modular reactor (SMR) technology to maintain energy security while transitioning toward a low-carbon future. The French Alternative Energies and Atomic Energy Commission (CEA) reported that hydrogen research funding tripled between 2020 and 2023, signaling a strategic pivot towards diversified clean energy solutions. Moreover, France leads in nuclear waste recycling and next-generation fission technology development. The Institute for Radiological Protection and Nuclear Safety (IRSN) emphasized that France’s closed nuclear fuel cycle reduces radioactive waste compared to open-cycle reactors , enhancing environmental sustainability.

The United Kingdom has emerged as a global leader in offshore wind and continues to phase out coal-fired power plants in line with its net-zero commitments. According to the UK Department for Business, Energy & Industrial Strategy (BEIS) , renewables accounted for over 40% of UK electricity generation in 2025, with offshore wind contributing nearly 25% of total electricity supply . The Offshore Wind Industry Council highlighted that UK offshore wind capacity surpassed 14 GW in 2025, with several gigawatt-scale projects underway, including Dogger Bank and Hornsea 3. Despite leaving the EU, the UK remains interconnected with continental Europe via interconnector cables, allowing for dynamic energy exchanges.

Spain is positioning itself as the fourth-largest contributor. The country has undergone a dramatic energy transformation in recent years, shifting away from fossil fuels toward solar and wind energy. According to the Spanish Association for Renewable Energy (APPA) , renewable sources supplied over 47% of Spain’s electricity demand in 2025, with solar photovoltaic and wind energy leading the way. Additionally, Spain is leveraging its geographic advantage to become a green hydrogen export hub. The Spanish Ministry for the Ecological Transition estimated that by 2030, Spain could produce over 4 GW of green hydrogen annually , positioning itself as a key supplier to Northern and Central Europe.

Italy has rapidly redefined its energy strategy following Russia’s reduction of natural gas supplies, pivoting toward liquefied natural gas (LNG) imports and domestic renewable development. At the same time, Italy is accelerating its renewable deployment. The Ministry of Ecological Transition reported that Italy added over 5 GW of new solar PV capacity in 2025, bringing total installed solar to over 30 GW , with similar growth observed in wind and bioenergy sectors. Italy is also embracing green hydrogen, with Enel, Edison, and Snam leading pilot projects aimed at integrating hydrogen into industrial and transport applications.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the Europe Energy Market are Enel, EDF, E.ON, RWE, Iberdrola, Vattenfall, Fortum, Statkraft, SSE, Naturgy, Equinor, National Grid, Verbund, CEZ Group, EnBW, Terna, TenneT, Endesa.

The competition in the Europe energy market is highly dynamic and multifaceted, shaped by the convergence of traditional utility providers, emerging renewable developers, and technology-driven energy service companies. As the continent accelerates its transition toward a net-zero economy, market participants are under increasing pressure to innovate, diversify, and adapt to evolving regulatory landscapes. Incumbent energy firms are repositioning themselves around cleaner portfolios, while independent power producers and startups are disrupting the status quo with agile business models and cutting-edge technologies.

This competitive environment is further intensified by the growing integration of digital tools, such as smart meters, AI-based demand forecasting, and blockchain-enabled peer-to-peer energy trading, which are redefining how energy is generated, distributed, and consumed. At the same time, national governments and supranational bodies like the European Commission are setting aggressive decarbonization targets that require coordinated action across the entire value chain. In this context, differentiation hinges not only on generation capacity but also on customer engagement, data-driven optimization, and integrated energy services. As a result, the European energy market is witnessing a profound restructuring, where agility, innovation, and sustainability are becoming decisive success factors.

Top Players in the Market

E.ON SE

E.ON is a leading integrated energy company headquartered in Germany and plays a pivotal role in shaping the European energy landscape. The company has transitioned from conventional fossil fuel-based generation to focus on renewable energy, grid infrastructure, and customer solutions. E.ON leads in smart metering, decentralized energy systems, and digital energy services, contributing significantly to Europe’s decarbonization goals. Its strategic investments in offshore wind, battery storage, and hydrogen technologies have positioned it as a key player in the continent's energy transition.

ENGIE S.A.

ENGIE, based in France, is a global leader in low-carbon energy solutions and one of the largest players in the Europe energy market. The company focuses on developing renewable energy projects, particularly in wind, solar, and green hydrogen, while also offering energy efficiency and smart infrastructure services. ENGIE plays a crucial role in industrial decarbonization by supplying clean energy and carbon-reduction solutions across sectors such as manufacturing, transport, and public infrastructure, reinforcing its influence in the region’s sustainable energy transformation.

Iberdrola S.A.

Iberdrola, a Spanish multinational corporation, is one of the world’s largest renewable energy producers and a dominant force in the Europe energy market. With significant investments in offshore wind, hydroelectric power, and grid modernization, Iberdrola contributes to enhancing energy security and sustainability. The company actively supports electrification initiatives across industries and transportation, driving innovation in clean technologies. Its leadership in large-scale renewables development and digitalized grid solutions makes it a cornerstone of Europe’s energy future.

Top Strategies Used by Key Market Participants

One of the major strategies employed by key players in the Europe energy market is accelerating investment in renewable energy infrastructure , including wind, solar, and green hydrogen, to align with EU climate targets and reduce dependency on fossil fuels. This approach ensures long-term sustainability and enhances resilience against energy supply disruptions.

Another prominent strategy is expanding digitalization through smart grids, AI-driven demand forecasting, and decentralized energy management platforms , which improve grid stability, optimize consumption, and integrate variable renewable sources more efficiently into the energy mix.

Lastly, companies are increasingly focusing on strategic partnerships and mergers to consolidate their market position , gain access to new technologies, and enhance cross-border energy trading capabilities, allowing them to scale operations and offer more diversified, customer-centric energy solutions.

RECENT HAPPENINGS IN THE MARKET

In January 2025, E.ON launched a new digital energy management platform across Germany and Sweden, enabling residential and commercial users to optimize electricity consumption through real-time monitoring and AI-powered insights, reinforcing its leadership in smart energy solutions.

In March 2025, ENGIE signed a strategic partnership with a leading Portuguese wind developer to co-develop offshore wind farms in the Atlantic, aiming to expand its presence in Southern Europe and support the EU’s renewable energy expansion goals.

In June 2025, Iberdrola initiated construction on a large-scale green hydrogen plant in Spain, designed to supply clean fuel for industrial and transport applications, marking a significant step in the company’s broader decarbonization strategy.

In September 2025, Ørsted expanded its offshore wind operations in Poland through a joint venture with a local energy firm, strengthening its footprint in the Baltic Sea region and supporting the country’s renewable energy ambitions.

In November 2025, TotalEnergies announced a major investment in a next-generation battery storage facility in France, aimed at enhancing grid flexibility and integrating higher shares of intermittent renewables into the national energy system.

MARKET SEGMENTATION

This research report on the europe energy market has been segmented and sub-segmented into the following categories.

By End-User

- Industrial Sector

- Residential Sector

By Energy Sources

- Renewables

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe.

Frequently Asked Questions

What is the European energy market?

The European energy market refers to the interconnected system of electricity and gas trading, generation, and distribution across EU member states and some neighboring countries. It aims to ensure secure, affordable, and sustainable energy for all.

What is the role of the European Union in the energy market?

The EU sets regulatory frameworks Promote renewable energy Reduce carbon emissions Foster cross-border energy integration Enhance market competition

How has the Russia-Ukraine war impacted Europe's energy market?

Europe’s energy mix includes: Renewables (solar, wind, hydro, biomass) Natural gas Nuclear power Coal (declining) The EU targets at least 42.5% renewables by 2030.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com