Europe Enterprise Software Market Size, Share, Trends, & Growth Forecast Report By Enterprise Type (SMEs Large Enterprises), Deployment, Business Function, End-User and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Enterprise Software Market Report Summary

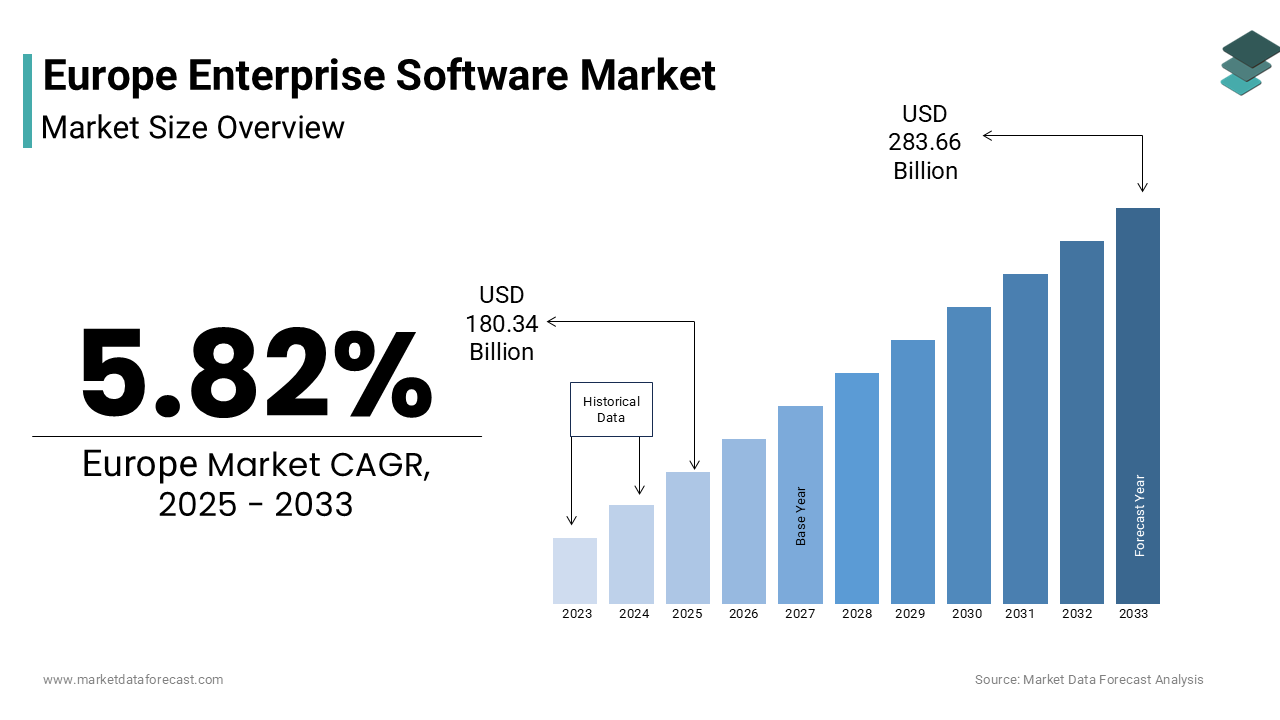

The Europe enterprise software market was valued at USD 170.44 billion in 2024, is estimated to reach USD 180.34 billion in 2025, and is projected to reach USD 283.66 billion by 2033, growing at a CAGR of 5.82% during the forecast period from 2025 to 2033. Market expansion is driven by accelerating digital transformation across industries, mandatory regulatory compliance (GDPR, DORA, CSRD), and rising adoption of cloud and hybrid platforms. Demand for AI-powered decision engines, industry-specific cloud solutions, and integrated suites that unify finance, HR, supply chain and sustainability reporting is further fueling growth. Additionally, initiatives around data sovereignty, workforce automation, and ESG disclosure requirements are shaping procurement priorities and increasing enterprise software spend across Europe.

Key Market Trends

- Rapid embedding of AI and ML into core enterprise applications for forecasting, automation and anomaly detection.

- Steady migration to cloud and hybrid architectures driven by scalability, resilience and sovereign-cloud offerings.

- Increasing emphasis on regulatory compliance and sustainability modules to meet CSRD, DORA and national reporting mandates.

- Growth of verticalized industry clouds tailored for manufacturing, energy, healthcare and logistics.

- Rising investments in cybersecurity, identity management and supply-chain resilience across software stacks.

Segmental Insights

- Based on enterprise type, the large enterprises segment was the largest in 2024, reflecting their complex multi-jurisdictional operations, heavy compliance burdens, and capacity for large-scale digital transformation investments. Large firms require unified platforms that consolidate reporting, governance and cross-border process orchestration.

The SME segment is the fastest growing as subscription-based cloud offerings and pre-configured workflows lower adoption barriers and enable smaller firms to meet digital reporting and automation needs. - Based on deployment, the cloud & hybrid segment dominated the market in 2024 due to demand for scalable, resilient and regulation-aware infrastructures. Sovereign cloud initiatives and Gaia-X aligned offerings have accelerated cloud uptake while hybrid models address data residency concerns. This segment is also forecast to register the fastest growth through 2033.

- Based on business function, financial management was the largest segment in 2024 owing to non-discretionary compliance, e-invoicing mandates and the integration of ESG and financial disclosures. Human capital management (HCM) is the fastest growing function as organisations adopt AI-driven skills, pay-gap reporting and workforce planning tools to manage talent shortages.

- Based on end user, BFSI led the market in 2024 given intense regulatory oversight, real-time monitoring needs and investments in digital resilience. Healthcare & life sciences is the most rapidly expanding vertical, driven by digital health initiatives, traceability rules and clinical IT modernization.

Regional Insights

- Europe shows differentiated adoption patterns with strong leadership from advanced digital economies.

- Germany was the largest contributor, accounting for a significant share in 2024, driven by its manufacturing base, Industrie 4.0 initiatives, vocational upskilling and strong uptake of integrated supply-chain and sustainability platforms.

- The United Kingdom remains a major market with its mature financial services sector, regulatory sandboxes and public-sector cloud modernization programs.

- France is notable for policies emphasising digital sovereignty and certified cloud procurement that favour local and compliant enterprise solutions.

- The Netherlands leads on logistics and port-centric enterprise systems that integrate customs and carbon accounting.

- Sweden is accelerating adoption through “Digital First” public procurement, climate reporting mandates and interoperable enterprise systems.

Competitive Landscape

The Europe enterprise software market is characterized by a mix of global incumbents and strong regional specialists. Competition centers on regulatory alignment, data sovereignty guarantees, AI integration depth and industry-specific functionality. Vendors pursue sovereign cloud partnerships, embedded AI features, and pre-configured vertical templates to win large, compliance-sensitive accounts. Strategic alliances with system integrators and vocational training initiatives are common to address talent gaps and speed deployments. Key market players include SAP SE, Microsoft Corporation, Oracle Corporation, Salesforce, IBM, Unit4, Zucchetti, TeamSystem, Centro Software, Eurosoft, Fluentis, SB Italia, Sisthema, Sage Group, Infor, Workday, Adobe, and ServiceNow.

Europe Enterprise Software Market Size

The europe enterprise software market size was valued at USD 170.44 billion in 2024 and is anticipated to reach USD 180.34 billion in 2025 from USD 283.66 billion by 2033, growing at a CAGR of 5.82% during the forecast period from 2025 to 2033.

Enterprise software refers to the integrated digital systems designed to manage complex business operations across finance, human resources, supply chain, customer relations, and compliance functions within medium to large scale organizations. Unlike fragmented point solutions, these platforms deliver end to end process orchestration under unified data governance, increasingly delivered via cloud infrastructure to support remote operations and real time analytics. The European enterprise software landscape is shaped not only by digital transformation imperatives but also by region specific regulatory frameworks including the General Data Protection Regulation, Digital Operational Resilience Act, and the Corporate Sustainability Reporting Directive. According to Eurostat, over 78 percent of enterprises with 250 or more employees in the EU used enterprise resource planning systems in 2023, reflecting deep institutionalization. Simultaneously, the European Commission estimates that the bloc faces a significant digital skills gap, as substantially less than the target proportion of adults possess at least basic digital skills, directly influencing software adoption patterns and customization demands. As per the European Investment Bank (EIB), the strategic priority placed on integrated software systems and stress that many European firms, particularly smaller ones, are lagging behind in digital investment compared to their international peers, such as those in the United States. This convergence of compliance, operational efficiency, and workforce readiness defines the unique contours of Europe’s enterprise software ecosystem.

MARKET DRIVERS

Mandatory EU Regulatory Compliance Drives Enterprise Software Adoption Across Sectors

The European Union’s expanding regulatory architecture drives the growth of the Europe enterprise software market. This has transformed enterprise software from a productivity tool into a compliance necessity. The Corporate Sustainability Reporting Directive (CSRD), which began to apply to the first set of companies from the 2024 financial year, requires a significant number of large and listed companies to publish audited sustainability information in a specified, digitally tagged format. As per the European Financial Reporting Advisory Group, compliant data collection demands integrated software that links operational systems with sustainability modules, a capability absent in legacy setups. Similarly, the Digital Operational Resilience Act (DORA) requires financial entities to have an ICT risk management framework and relevant processes for incident logging and real-time monitoring of threats in place by January 2025. German banks are increasingly undertaking core system upgrades to address evolving regulatory requirements. Regulations regarding data protection continue to influence operations, leading to a greater need for tools that manage identity and consent processes automatically. Insurers must provide software-driven audit trails to ensure compliance with governance standards for managing model risk. These legal obligations eliminate discretionary adoption, embedding enterprise software as non-negotiable infrastructure for legal operation across the European single market.

Labor Productivity Pressures Accelerate Investment in Integrated Workflow Platforms

Persistent labor shortages and stagnant productivity growth have compelled the regional enterprises to seek operational leverage through integrated software systems to further boost the expansion of the Europe enterprise software market. Eurostat data indicates a general widening of the labor productivity gap between the EU and the US over time, with the EU's productivity growth experiencing a slowdown in recent years. Job vacancy rates have been high in some sectors in the EU. In response, firms are deploying enterprise platforms that automate cross functional workflows to extract maximum output from constrained workforces. A notable trend in Germany is the increasing adoption of integrated ERP and supply chain management systems among midsize industrial firms to streamline operations across procurement, production, and logistics. Enterprises in the Nordic region, particularly Sweden, are increasingly implementing unified human capital and financial management software to accelerate financial processes and improve administrative efficiency. Across the UK, businesses leveraging fully integrated enterprise systems are reporting enhanced overall productivity and higher revenue generation per employee compared to those using disparate, disconnected tools These efficiency gains are not merely cost driven but strategic, which enables European firms to compete globally despite demographic and wage pressures through intelligent process orchestration.

MARKET RESTRAINTS

Fragmented Data Sovereignty Requirements Increase Implementation Complexity

The deployment of these integrated digital systems faces significant friction due to divergent national interpretations of data sovereignty and localization mandates, despite the EU’s single trading bloc, which ultimately restricts the growth of the Europe enterprise software market. "Germany prioritizes robust data protection and selectively encourages data localization for certain government-related data, but EU law generally permits critical infrastructure operators to store industrial data outside national borders, provided appropriate safety measures are in place. Multinational enterprises are finding it necessary to maintain varied software configurations across different regions due to regulatory differences. Integrating systems can become more complex for pan-European vendors when specific nations mandate the use of locally based identity providers for public procurement software. Separate national certification requirements for specialized software modules (such as those related to taxation) can lead to delays in product rollouts. These regulatory asymmetries prevent true standardization, forcing enterprises to choose between compliance fragmentation or market withdrawal. Enterprise software adoption will continue to be hampered by fragmented legal landscapes as long as the EU lacks a unified approach to digital sovereignty rules.

Legacy System Entrenchment Constrains Modernization in Key Industrial Sectors

Many regional enterprises, particularly in manufacturing and utilities, remain locked into decades old enterprise systems that resist integration with modern cloud platforms, and thereby hinders the expansion of the Europe enterprise software market. Germany’s mechanical engineering sector, for instance, relies heavily on customized SAP R3 instances installed in the 1990s, with a portion of member firms still operate on unsupported legacy versions due to fear of operational disruption. In France, EDF and other energy incumbents maintain mainframe-based asset management systems that lack APIs for real time data exchange, impeding predictive maintenance initiatives. As per a study, a significant portion of core banking systems across the euro area are older, established systems. Rewriting or replacing these systems carries immense risk. Major software transition projects sometimes face substantial challenges that interrupt normal business activities. Consequently, firms often resort to middleware layers that add cost and latency without delivering true digital transformation. This technological inertia, rooted in risk aversion and sunk cost fallacy, throttles innovation and sustains vulnerability to cyber threats and operational inefficiencies.

MARKET OPPORTUNITIES

Integration of AI Powered Decision Engines Within Core Enterprise Platforms

European enterprises are increasingly embedding artificial intelligence directly into their core software stacks to convert data into strategic action, which provides potential opportunities for the Europe enterprise software market. Unlike standalone AI tools, next generation enterprise platforms integrate machine learning models into financial planning, supply chain optimization, and talent management workflows. Large European firms are increasingly leveraging AI-driven forecasting within their ERP systems to enhance efficiency, resulting in a reduction in inventory carrying costs. SAP is advancing its generative AI copilot, Joule, to enable more sophisticated data analysis by integrating structured data from SAP S/4HANA with unstructured data sources (via technologies like Retrieval-Augmented Generation for enterprise, or RAGe). Similarly, Oracle Fusion Cloud offers an application named Oracle Fusion Cloud Sustainability (part of its broader Fusion Cloud suite), launched in September 2024. Enterprises are increasingly adopting native AI in HR modules to streamline human resources operations, which leads to faster internal mobility matching and overall enhanced operational efficiency. This shift from data aggregation to intelligent automation positions enterprise software as the central nervous system of corporate decision making in Europe’s increasingly regulated and resource constrained economy.

Expansion of Industry Specific Cloud Platforms Tailored to European Value Chains

A new wave of vertical enterprise software is emerging to address the unique operational and compliance needs of specialized industries in the region, which introduces fresh possibilities for the expansion of the Europe enterprise software market. Unlike generic global platforms, these solutions embed sector specific logic for sectors like precision agriculture, renewable energy integration, and circular manufacturing. In the Netherlands, agricultural enterprise platforms now integrate real time nitrogen emission data from farm machinery with national quota systems, enabling compliance with the EU’s Nitrates Directive. Dutch dairy cooperatives and farmers are increasingly exploring and adopting technologies and eco-schemes in response to a growing emphasis on sustainability, environmental challenges (like the nitrogen crisis), and evolving regulations, rather than adopting platforms specifically to avoid production caps. In Germany, enterprise software for the Mittelstand includes modules for EU Battery Passport compliance, tracking raw material provenance from mine to recycling as required under the 2023 Battery Regulation. Energinet, Denmark's state-owned transmission system operator, developed and implemented a national DataHub (launched its first version in 2013 and a new generation in 2022) to centralize energy data, enable market flexibility, and integrate a high share of variable renewable energy sources with the power system under the European Union's Clean Energy Package obligations. These industry cloud ecosystems reduce configuration burdens while ensuring regulatory alignment, creating sticky customer relationships and opening new monetization avenues beyond traditional licensing. This verticalization trend reflects Europe’s move toward sovereign, context aware digital infrastructure.

MARKET CHALLENGES

Talent Shortages in Enterprise Software Configuration and Governance

The region faces a serious shortage of professionals skilled in configuring, governing, and optimizing complex enterprise platforms, which, despite robust demand, is one of the key challenges to the Europe enterprises market. The European Union faces a persistent and significant shortage of ICT specialists, a trend that hinders progress toward its digital economy goals. The German labour lanscape experiences an acute shortage of skilled workers in the IT sector, and the demand for specialists, particularly those with expertise in SAP S/4HANA migration, consistently outpaces supply. In addition, A general skills gap exists within the French market for consultants possessing dual expertise in new financial regulations and specific enterprise cloud technologies, which has the potential to cause project delays. Moreover, rising complexity in hybrid cloud environments demands professionals who understand data residency, cybersecurity, and business process design, a rare combination. Across the European business landscape, many enterprises identify internal skill deficiencies as a primary obstacle to effectively leveraging their software investments for maximum business value. The digital talent shortage will persist and restrain transformation unless addressed by unified upskilling through vocational programs and vendor academies, regardless of how much is invested in software.

Security Vulnerabilities in Overlapping and Poorly Integrated Software Stacks

The proliferation of best of breed applications alongside core enterprise platforms has created fragmented digital ecosystems vulnerable to cyber threats that slow down the expansion of the Europe enterprise software market. European enterprises are increasingly relying on a diverse array of software tools, and managing the security of their numerous and often fragile integrations remains a significant challenge, with a need for improved end-to-end encryption and consistent access controls. The European Union Agency for Cybersecurity (ENISA) has documented a rising trend in supply chain attacks targeting enterprise software interfaces, with the manufacturing and logistics sectors among the most affected. In one high profile incident, a misconfigured integration between a legacy ERP and a cloud based procurement system allowed unauthorized data exfiltration at a major Belgian port operator, disrupting customs clearance for weeks. The lack of unified identity management across these stacks exacerbates risks. European financial institutions continue to face challenges in consistently enforcing robust multifactor authentication across all enterprise applications, despite regulatory pushes by the European Banking Authority (EBA) to mandate stronger customer authentication for online transactions. These vulnerabilities are not merely technical but strategic, as the Digital Operational Resilience Act holds executives personally liable for systemic ICT failures. A strong security posture for Europe's digital infrastructure depends on businesses consolidating or rigorously governing their software environments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Enterprise Type, Deployment, Business Function, End-User & Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, and the Czech Republic. |

| Key Market Players | SAP SE, Microsoft Corporation, Oracle Corporation, Salesforce, Inc., IBM Corporation, Unit4, Zucchetti S.p.A, TeamSystem S.p.A, Centro Software Srl, Eurosoft Srl, Fluentis Srl, SB Italia Srl, Sisthema S.p.A, Sage Group plc, Infor, Workday, Inc., Adobe Inc., and ServiceNow, Inc.. |

SEGMENTAL ANALYSIS

By Enterprise Type Insights

The large enterprises segment dominated the Europe enterprise software market and accounted for a 63.6% share in 2024. The dominance of the large enterprises segment is driven by their complex operational footprints, stringent compliance obligations, and centralized procurement power. Large firms operate across multiple jurisdictions, requiring integrated platforms that unify financial reporting, supply chain visibility, and data governance in line with EU mandates like the Corporate Sustainability Reporting Directive. As per sources, the adoption of advanced operational resilience frameworks, such as those mandated by the European Union's Digital Operational Resilience Act, is driving a significant technology modernization trend among large Eurozone banks as they work toward full compliance deadlines. Similarly, Germany's manufacturing giants—many of which form the backbone of the Mittelstand export ecosystem—deploy enterprise software to manage global supplier networks under the due diligence requirements of the Act on Corporate Due Diligence Obligations in Supply Chains (Lieferkettensorgfaltspflichtengesetz, or LkSG). The scale of these organizations justifies high upfront investments in customization, integration, and change management, which SMEs often cannot absorb. Moreover, large enterprises benefit from dedicated internal IT governance teams that can manage complex implementations, a structural advantage absent in smaller firms. These institutional, regulatory, and financial factors collectively anchor large enterprises as the core demand engine of Europe’s enterprise software landscape.

The small and medium enterprises (SMEs) segment is predicted to witness the highest CAGR of 10.8% from 2025 to 2033. The rapid acceleration of SMEs segment is fuelled by the convergence of affordable cloud platforms, regulatory pressure, and digital skilling initiatives. Unlike a decade ago, modern enterprise software for SMEs is now offered via subscription models with pre configured workflows, eliminating the need for large capital outlays. European small and medium-sized enterprises (SMEs) are adopting integrated financial and inventory management platforms. This trend is related to the need to comply with digital reporting requirements under a regional initiative. A national program in one country has supported the uptake of cloud enterprise resource planning (ERP) licenses for businesses. Businesses utilizing unified enterprise software may experience a reduction in administrative tasks. This reduction potentially allows resources to be reallocated to activities that generate more value. Apart from these, sector specific platforms embed local compliance and logistics logic, lowering adoption barriers. This democratization of enterprise capabilities is transforming SMEs from passive users into active digital contributors across European value chains.

By Deployment Insights

In 2024, the cloud and hybrid segment captured the majority share of the Europe enterprise software market. A fundamental shift toward agility, remote accessibility, and compliance aligned infrastructure has mainly contributed to the prominence of the cloud and hybrid segment. The General Data Protection Regulation initially slowed cloud adoption due to data residency concerns, but EU certified hyperscalers like AWS Europe and Microsoft Azure EU Regions have since addressed these through sovereign cloud offerings with local data residency guarantees. As per research, a portion of new enterprise software contracts signed included hybrid architectures that keep sensitive HR or financial data on private nodes while running analytics in certified public clouds. The Digital Operational Resilience Act further accelerated this trend by mandating continuous backup and failover capabilities, features native to cloud platforms but costly to replicate on premise. The BSI (Federal Office for Information Security) mandates that operators of critical infrastructure in Germany must implement appropriate organizational and technical measures, including state-of-the-art attack detection systems, and that these operators remain fully responsible for the security and availability of their critical services, even when using cloud service providers. Besides, the cost structure of cloud eliminates capital expenditure spikes, allowing firms to scale usage with business cycles, a vital advantage amid economic volatility. These technical, regulatory, and financial synergies have made cloud and hybrid the default deployment choice across Europe.

The cloud and hybrid segment is also the fastest growing and is projected grow at a CAGR of 11.3% from 2025 to 2033. The swift expansion of the cloud and hybrid segment is attributed to the EU’s Gaia X initiative, which has established a federated data infrastructure framework enabling enterprises to share industrial data securely across borders while retaining sovereignty. The dual status, as both dominant and fastest growing, emphasizes its structural alignment with the region’s digital future. As per studies, many software platforms are aligning with common standards to improve data exchange between different companies. This alignment helps businesses in various industries, such as automotive and energy, work together more easily. The use of these shared standards is growing among technology providers. The goal of adopting these standards is to create a seamless environment for collaboration and data sharing across organizations. Simultaneously, workforce transformation is driving cloud adoption. Many businesses with remote or hybrid teams are using cloud-based systems. These systems help organizations keep their operations consistent and running smoothly. National governments are reinforcing this shift. Public sector entities have a preference for cloud solutions that align with data residency and control considerations. Furthermore, artificial intelligence integration is inherently cloud native. These converging forces ensure cloud and hybrid deployment will not only grow rapidly but deepen its functional footprint within enterprises.

By Business Function Insights

The financial management segment was the largest segment in the Europe enterprise software market and held a 28.8% share in 2024. The leading position of the financial management segment is credited to the non-discretionary nature of financial compliance and the centrality of accounting systems to enterprise operations. Sustainability and financial reporting are converging, prompting organizations to integrate data collection processes for both financial and environmental, social, and governance (ESG) metrics. Firms are transitioning from older accounting systems to more modern platforms, facilitating improved data extraction from various internal systems such as procurement, logistics, and human resources. The adoption of unified financial management suites is increasing among companies, which is a response to the need for better audit trails and the ability to disclose information efficiently. Accounting regulations favor digital, secure bookkeeping methods, a standard which appears to be primarily met by advanced enterprise software platforms. Financial institutions are adapting their core software to meet requirements for detailed credit exposure reporting, by incorporating specific internal reporting mechanisms. Besides, e invoicing laws in Italy, France, and Spain, covering a portion of EU B2B transactions by 2025, necessitate direct integration between enterprise financial systems and national clearance platforms. These legal imperatives transform financial management from a back-office function into a strategic compliance backbone, ensuring its continued market leadership.

The human capital management segment is anticipated to witness the fastest CAGR of 12.1% over the forecast period owing to Europe’s acute labor market imbalances and the rise of skills-based workforce planning. Enterprises in Europe have been facing recruitment difficulties. This situation has contributed to a changing environment for human resource departments. Consequently, there has been a shift in focus for human resources toward more strategic talent management. Modern HCM platforms now embed AI powered skills ontologies that map internal capabilities against future project needs, reducing external hiring. Legislation requires organizations to perform regular pay gap reporting, a capability now commonly integrated within human capital management (HCM) platforms. Workplace regulations encourage the monitoring of workload balance, leading some companies to adopt HCM modules that track employee well-being indicators through standard work patterns and communications analysis. Concurrently, the European Skills Agenda has incentivized upskilling, with platforms integrating directly with national credential registries in Sweden and the Netherlands. These regulatory, demographic, and strategic pressures position HCM as the most dynamically evolving function in enterprise software.

By End User Insights

The BFSI segment led the Europe enterprise software market and occupied a share of 22.9% in 2024. The sector’s intense regulatory oversight, data intensity, and systemic importance to the European economy have boosted the expansion of the BFSI segment. The Digital Operational Resilience Act requires all significant financial institutions to implement enterprise software with real time incident logging, third party risk monitoring, and cyber threat simulation capabilities. As per sources, a share of major insurers upgraded their core policy administration systems to embed these functions. Simultaneously, the EU’s Instant Payments Regulation has forced banks to modernize legacy transaction engines through integrated enterprise platforms. Apart from these, anti-money laundering directives compel real time transaction monitoring across jurisdictions, a task impossible without centralized data architectures. The sector’s high margins and strict capital adequacy rules further enable sustained software investment, unlike more margin constrained industries. These structural, regulatory, and economic factors cement BFSI as the anchor end user segment in Europe’s enterprise software ecosystem.

The healthcare and life sciences segment is likely to experience the fastest CAGR of 13.4% from 2025 to 2033 due to the digital transformation of care delivery, regulatory harmonization, and pandemic driven infrastructure investments. The EU’s European Health Data Space, launched in 2023, mandates interoperable electronic health records across member states, compelling hospitals to adopt enterprise platforms that unify clinical, administrative, and billing data. Hospitals, including numerous university facilities, are increasingly adopting enterprise software solutions. Funding initiatives are encouraging the achievement of digital maturity benchmarks. Public health strategies emphasize the implementation of integrated resource planning systems. These systems are intended to optimize resource allocation, such as managing beds and staff more effectively. Concurrently, pharmaceutical firms face new traceability rules under the Falsified Medicines Directive, necessitating enterprise systems that track products from manufacturing to pharmacy. These converging clinical, compliance, and operational imperatives make healthcare Europe’s most rapidly digitizing enterprise software vertical.

REGIONAL ANALYSIS

Germany Enterprise Software Market Analysis

Germany was the top performer in the Europe enterprise software market and accounted for a 21.3% share in 2024. Its manufacturing dominance, regulatory rigor, and public private digitalization partnerships are the key factors attributed to the dominance of Germany in the regional market. The country’s Industrie 4.0 initiative has institutionalized enterprise software as the digital thread connecting design, production, and service across the value chain. A majority of major industrial firms have adopted integrated platforms that connect production machinery with business planning and supply chain functions. Regulations are requiring companies to track raw material origins, increasing the need for software with sustainability analytics capabilities. The national vocational training system now includes enterprise software configuration in advanced apprenticeships, helping to address skill gaps. Besides, regional grants are available, covering a portion of software licensing costs for medium-sized businesses. A notable number of German small and medium enterprises have achieved complete digital process integration, indicating the country's advanced standing in this area compared to the regional average.

United Kingdom Enterprise Software Market Analysis

The UK was the second largest player in the Europe enterprise software market and held a 16.8% share in 2024. Its mature financial services sector, agile regulatory sandbox, and post Brexit digital sovereignty strategy have contributed to the growth of enterprise software in the UK. Despite leaving the EU, the UK remains deeply aligned with European enterprise software standards through the Financial Conduct Authority’s operational resilience rules, which mirror the DORA framework. Systemically important UK banks are migrating to cloud-based enterprise platforms. The National Health Service is unifying hospital IT systems through enterprise software. Early adopters of the NHS initiative are achieving faster procurement cycles. The UK's National Cyber Security Centre certifies enterprise platforms, supporting buyer confidence in sovereign deployments. Apart from these, London’s fintech cluster collaborates with enterprise vendors to co-develop solutions for open banking and ESG reporting. These institutional, financial, and innovation drivers sustain the UK’s dominance despite geopolitical shifts.

France Enterprise Software Market Analysis

France is an attractive country in the Europe enterprise software market because of its strategic emphasis on digital sovereignty and public sector transformation. The country’s “Cloud Souverain” initiative, led by ANSSI and supported by GAIA-X, has created a trusted ecosystem where enterprise software must meet strict data residency, encryption, and auditability criteria. New central government software agreements frequently incorporate a specific certification requirement within their criteria. Legislation requires defense and essential infrastructure operators to utilize platforms that are governed domestically. This regulatory environment is contributing to the growth of local vendors in the technology sector. Simultaneously, France’s energy transition law requires large enterprises to report carbon footprints via certified software, driving adoption in manufacturing and transport. This fusion of national security, ecological planning, and industrial policy makes France a uniquely assertive market shaping Europe’s digital autonomy agenda.

Netherlands Enterprise Software Market Analysis

The Netherlands grew steadily in the Europe enterprise software market due to its position as Europe’s logistics gateway to pioneer integrated trade and supply chain software. Terminal operators at the Port of Rotterdam are required to use enterprise platforms that interface with national customs systems. This requirement facilitates connectivity via a central Port Community System. A significant majority of logistics firms operating within the port have adopted unified software solutions. These unified solutions cover essential functions like freight management, documentation processing, and carbon accounting. The country’s advanced agrifood sector, Europe’s second largest exporter, relies on enterprise platforms that track produce from greenhouse to supermarket shelf to meet EU food safety and sustainability rules. Apart from these, the Netherlands’ progressive stance on remote work has spurred cloud based enterprise deployments across professional services.

Sweden Enterprise Software Market Analysis

Sweden is predicted to expand notably in the Europe enterprise software market from 2025 to 2033 owing to its integration of enterprise software into the social contract and green transition. The country’s “Digital First” public procurement policy mandates that all state agencies use interoperable enterprise systems that share citizen data securely under the eIDAS framework. Sweden’s climate law targets net zero greenhouse gas emissions by 2045. The Swedish Agency for Digital Government (DIGG) is the responsible agency for aspects of public sector digitalization and electronic identification in Sweden. They have conducted studies on the public sector's use of digital tools like e-invoicing. Sweden's Discrimination Act requires employers to analyze workforce data, specifically an annual report on gender pay gaps, to identify and address bias. State-owned enterprises like Vattenfall (an energy company) are significant actors in the context of Sweden's climate goals, as the energy sector is crucial for meeting emissions targets. This holistic approach positions Sweden as a values driven innovator in Europe’s enterprise software landscape.

COMPETITIVE LANDSCAPE

The Europe enterprise software market is characterized by intense competition among global incumbents, regional specialists, and emerging cloud native vendors. While multinational giants dominate large scale deployments through integrated suites, niche players gain traction by offering agile, compliance focused solutions for specific industries or national markets. Competition is increasingly defined not by price but by regulatory alignment, data sovereignty guarantees, AI integration depth, and ecosystem partnerships. European firms demand vendors that understand local labor laws, tax regimes, and sustainability mandates, creating barriers for non compliant entrants. The rise of sovereign cloud infrastructure has further regionalized competition, with vendors adapting architectures to meet country specific security certifications. At the same time, open standards initiatives like Gaia X are fostering interoperability, pressuring vendors to adopt modular designs. This dynamic environment rewards adaptability, local engagement, and regulatory foresight over pure scale.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the europe enterprise software market include

- SAP SE

- Microsoft Corporation

- Oracle Corporation

- Salesforce, Inc.

- IBM Corporation

- Unit4

- Zucchetti S.p.A

- TeamSystem S.p.A

- Centro Software Srl

- Eurosoft Srl

- Fluentis Srl

- SB Italia Srl

- Sisthema S.p.A

- Sage Group plc

- Infor

- Workday, Inc.

- Adobe Inc.

- ServiceNow, Inc

Top Players in the Europe Enterprise Software Market

SAP SE

SAP SE is a German multinational that serves as a cornerstone of enterprise software across Europe and globally, offering integrated suites for finance, supply chain, human resources, and sustainability management. The company plays a pivotal role in shaping EU digital standards through its alignment with regulatory frameworks such as the Corporate Sustainability Reporting Directive and Digital Operational Resilience Act. It also deepened partnerships with national cloud providers in France and Germany to ensure data residency under the Gaia X framework. These initiatives reinforce SAP’s position as a trusted infrastructure provider for Europe’s largest enterprises while extending its influence on global enterprise architecture.

Oracle Corporation

Oracle maintains a strong footprint in the Europe enterprise software market through its cloud based Fusion Applications, particularly in financial services, public sector, and life sciences. The company has intensified its focus on regulatory alignment by embedding EU specific compliance modules into its Financials and HCM Cloud suites. It also integrated AI driven carbon accounting capabilities into its ERP Cloud to support CSRD reporting. By co developing industry templates with European banks and pharmaceutical firms, Oracle ensures its platforms address local business processes while scaling globally. These actions solidify its role as a strategic enabler of digital transformation under Europe’s evolving regulatory landscape.

Microsoft Corporation

Microsoft leverages its Azure cloud infrastructure and Dynamics 365 suite to deliver integrated enterprise solutions across European industries, with particular strength in manufacturing, retail, and public administration. The company has prioritized European digital sovereignty by expanding its EU Data Boundary initiative, ensuring customer data remains within the bloc. It also embedded AI powered sustainability calculators into its supply chain modules to automate CSRD disclosures. Through partnerships with local system integrators and vocational training programs, Microsoft enhances adoption among SMEs. These efforts position Microsoft not only as a technology vendor but as a co architect of Europe’s trusted digital ecosystem

Top Strategies Used by the Key Market Participants

Key players in the Europe enterprise software market are embedding artificial intelligence and generative AI capabilities directly into core enterprise applications to enable real time decision making and regulatory compliance. They are establishing sovereign cloud regions within EU borders to guarantee data residency and meet national cybersecurity requirements. Companies are co developing industry specific solutions with local enterprises and public institutions to ensure alignment with regional business processes and legal mandates. Strategic partnerships with European system integrators and vocational training bodies help bridge talent gaps and accelerate adoption. Additionally, vendors are proactively integrating sustainability and ESG reporting modules to align with the Corporate Sustainability Reporting Directive and other green regulations, transforming software from operational tools into compliance infrastructure.

MARKET SEGMENTATION

This research report on the europe enterprise software market has been segmented and sub–segmented into the following categories.

By Enterprise Type

- SMEs

- Large Enterprises

By Deployment

- Cloud

- Hybrid vs On-premise

By Business Function

- Financial Management

- Human Capital Management

By End User

- BFSI

- Healthcare & Life Sciences

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe enterprise software market?

It refers to software solutions used by European organizations to manage operations, including ERP, CRM, financial management, HR systems, analytics, and industry-specific applications.

What factors are driving the growth of the market?

Digital transformation, regulatory compliance requirements, cloud adoption, automation, and the need for integrated workflows are key drivers.

Which business function segment leads the market?

The Financial Management segment leads with a 28.8% share due to mandatory compliance, audit requirements, and digital bookkeeping standards.

Which business function segment is expected to grow fastest?

Human Capital Management (HCM) is expected to grow at the fastest CAGR of 12.1%, supported by labor shortages, pay-gap reporting laws, and AI-enabled talent tools.

What regulatory factors are shaping the market?

EU laws such as the Digital Operational Resilience Act (DORA), ESG reporting requirements, e-invoicing mandates, and the European Health Data Space significantly impact software adoption.

Why is financial management software in high demand?

Its non-discretionary nature, compliance needs, audit trails, real-time reporting, and e-invoicing laws make it essential for business operations.

Which deployment model is preferred in Europe?

Cloud-based deployments are rapidly growing, though hybrid models remain popular among organizations with legacy systems.

What opportunities exist for vendors in Europe?

Opportunities include offering localized compliance solutions, industry-specific platforms, AI-powered automation, integration services, and secure cloud hosting.

How has the pandemic impacted enterprise software demand?

It accelerated digital transformation, remote work requirements, cloud migrations, and the need for automated enterprise workflows.

What is the long-term outlook for the Europe enterprise software market?

The market is set for strong growth, driven by regulation-driven adoption, cloud expansion, and continued digital transformation across verticals.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com