Europe Entertainment Market Size, Share, Trends, & Growth Forecast Report By Type (Video, Audio, Games, Internet, Radio, Others), Application, Devices and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Entertainment Market Report Summary

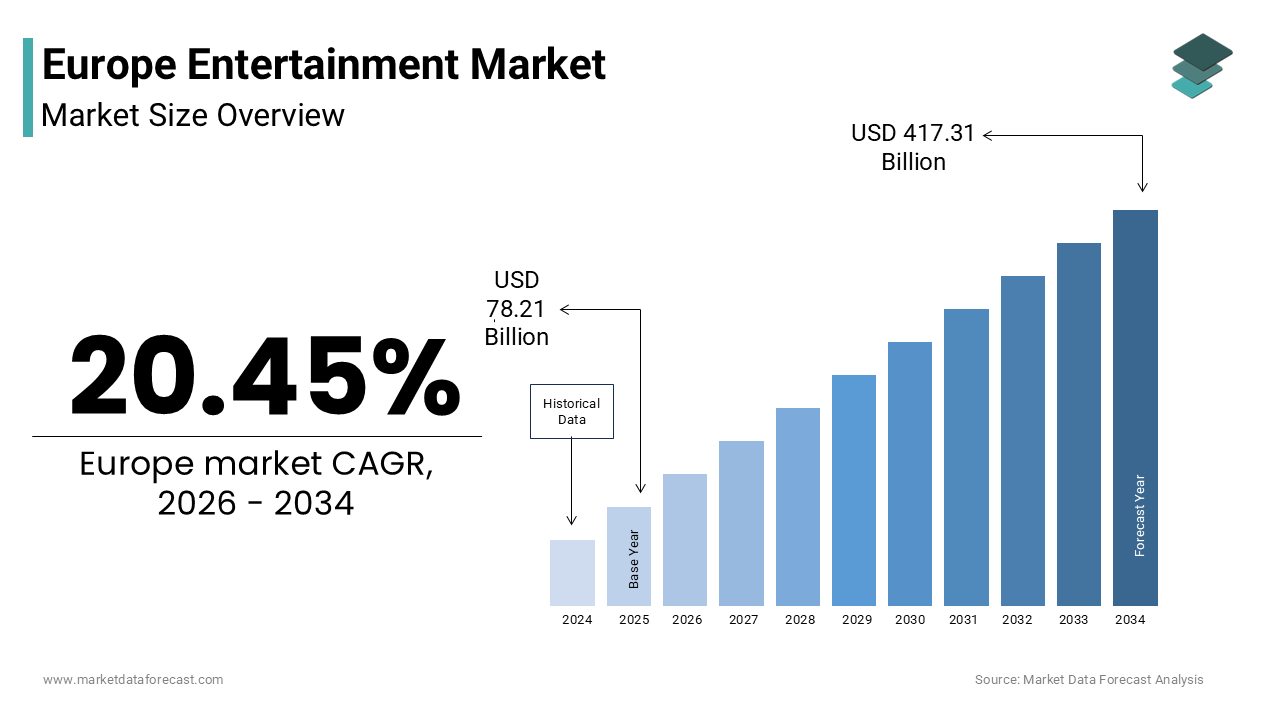

The Europe entertainment market was valued at USD 78.21 billion in 2025, is estimated to reach USD 94.20 billion in 2026, and is projected to reach USD 417.31 billion by 2034, growing at a CAGR of 20.45% during the forecast period from 2026 to 2034. The growth of the Europe entertainment market is driven by rapid digital infrastructure expansion, increasing adoption of streaming and interactive platforms, strong public funding for cultural production, and revival of experiential entertainment formats. Europe combines deep cultural heritage with cutting-edge immersive technologies such as AI-driven storytelling, cloud gaming, and virtual concerts. High broadband and 5G penetration levels are enabling seamless on-demand content consumption, while institutional backing through programs such as Creative Europe sustains film, music, theatre, and cross-border collaborations. Although regulatory fragmentation and inflationary pressures pose challenges, innovation in artificial intelligence, immersive experiences, and hybrid physical-digital entertainment models continues to fuel strong long-term market expansion across the region.

Key Market Trends

-

Strong growth of subscription-based video-on-demand and localized streaming content.

-

Rapid expansion of cloud gaming, esports, and mobile-first entertainment consumption.

-

Increasing integration of artificial intelligence in content creation, personalization, and localization.

-

Revival of live events, music festivals, immersive theatre, and experiential entertainment venues.

-

Growing smartphone dominance as the primary entertainment access device across Europe.

Segmental Insights

- Based on type, the video segment held 47.4% of the Europe entertainment market share in 2025, driven by the convergence of streaming platforms, theatrical releases, public broadcasting, and user-generated content ecosystems.

- Based on application, the residential segment accounted for 81.1% of the Europe entertainment market share in 2025, reflecting strong home-based media consumption patterns supported by high broadband penetration and smart device ownership.

- Based on devices, the smartphones segment held 51.5% of the Europe entertainment market share in 2025, owing to near-universal ownership, 5G rollout, app-based streaming services, and portable media consumption behavior.

Regional Insights

The Europe entertainment market demonstrates varied growth dynamics across key countries shaped by digital maturity, public cultural funding, and creative industry ecosystems.

-

United Kingdom led the market with 19.5% share in 2025, supported by globally influential creative industries, strong gaming development hubs, and high streaming penetration.

-

Germany accounted for 16.1% of the market share in 2025, driven by its strong music industry, public broadcasting system, and balanced digital adoption.

-

France maintains a prominent position, reinforced by cultural protection policies, film production incentives, and investment mandates for streaming platforms.

-

Italy continues to expand, supported by strong television consumption, gaming growth, and improving fiber connectivity infrastructure.

-

Spain exhibits steady growth, driven by vibrant live entertainment scenes, festival culture, gaming adoption, and expanding 5G coverage.

Competitive Landscape

The Europe entertainment market features intense competition among global streaming platforms, multinational media conglomerates, regional broadcasters, gaming companies, and experiential venue operators. Leading companies compete on localized content production, advanced streaming technology, regulatory compliance, and cross-media integration strategies. Major players are investing in multilingual content libraries, AI-driven recommendation engines, immersive audiovisual formats, and experiential expansions such as theme parks and live events. Strategic co-productions with European studios, compliance with national quotas, and adherence to GDPR and media pluralism regulations are critical differentiators. Prominent players operating in the Europe entertainment market include The Walt Disney Company, Netflix, Warner Bros. Discovery, Comcast Corporation, Sony Group Corporation, Vivendi SE, RTL Group, ITV plc, ProSiebenSat.1 Media SE, Banijay Group, BBC Studios, and Sky Group.

Europe Entertainment Market Size

The Europe entertainment market size was valued at USD 78.21 billion in 2025 and is anticipated to reach USD 94.20 billion in 2026 from USD 417.31 billion by 2034, growing at a CAGR of 20.45% during the forecast period from 2026 to 2034.

Entertainment encompasses a dynamic and multifaceted ecosystem of live performances, digital content delivery, theme parks, cinema, music festivals, and interactive experiences that collectively shape cultural consumption across the continent. Unlike narrower definitions focused solely on media or gaming, this market integrates both physical and virtual modalities through which audiences engage with narrative, spectacle, and leisure. Europe’s entertainment landscape in 2025 is distinguished by its deep historical legacy, home to many professional theatres and opera houses, and its rapid adoption of immersive technologies such as virtual reality concerts and AI driven storytelling. Cultural participation remains high. According to Eurostat, many European Union residents attended cultural events in 2023, while cinema admissions rebounded strongly, surpassing pre pandemic levels. The region also hosts numerous major music festivals annually, drawing large audiences, as per the European Live Events Association. This blend of tradition and innovation, coupled with strong public funding for the arts and robust intellectual property frameworks, positions Europe as a global leader in diverse, high quality entertainment experiences that extend far beyond commercial metrics.

MARKET DRIVERS

Proliferation of High-Speed Digital Infrastructure Enabling On-Demand Content Consumption

The widespread deployment of fiber optic networks and 5G connectivity has fundamentally reshaped how Europeans access and interact with entertainment content, which is one of the major factors driving the entertainment market growth in Europe. According to the European Commission’s Digital Decade report, broadband coverage and gigabit capable connections have expanded significantly across households. This infrastructure leap has enabled seamless streaming of ultra-high-definition video, cloud based gaming, and real time interactive experiences that were previously constrained by latency or bandwidth limitations. In countries such as Sweden and Denmark, 5G penetration is reported to be very high, facilitating mobile first entertainment consumption among younger demographics who increasingly bypass traditional broadcast channels. As per the European Audiovisual Observatory, Europeans spend substantial time on digital entertainment platforms, with on demand video accounting for a major share of viewing. Moreover, low latency networks support emerging formats like live virtual concerts and multiplayer augmented reality experiences, which have seen notable increases in user engagement. The digital backbone thus acts not merely as a conduit but as an enabler of entirely new entertainment paradigms that prioritize personalization, immediacy, and interactivity.

Strong Public and Institutional Support for Cultural Production and Distribution

Europe’s entertainment vitality is significantly sustained by consistent public investment in arts and cultural institutions, which is creating a fertile environment for both heritage preservation and contemporary innovation and further contributing to the regional market expansion. The European Union allocated funding to the Creative Europe program for the 2021 to 2027 period, which is directly supporting film, theater, music, and cross border collaborative projects. Nationally, countries like France and Germany maintain robust subsidy systems. According to UNESCO, Europe accounts for a large share of globally registered intangible cultural heritage elements, many of which are actively integrated into modern entertainment offerings such as folk music festivals in Romania and historical reenactments in Spain. Furthermore, public broadcasters such as BBC, ARD, and RAI commission extensive original programming annually, maintaining high production standards and cultural relevance. As per the European Audiovisual Observatory, European films captured a significant portion of the non-US global box office in 2024. This symbiosis between public policy and creative enterprise sustains a resilient and pluralistic entertainment ecosystem.

MARKET RESTRAINTS

Fragmented Regulatory and Language Barriers Limiting Pan European Scale

Despite its geographic cohesion, the Europe entertainment market remains hindered by linguistic diversity and inconsistent regulatory frameworks that impede content scalability and audience reach. The continent is home to many official EU languages and numerous regional or minority languages, requiring costly localization efforts for films, games, and digital platforms. Dubbing and subtitling increase production expenses, often leading producers to prioritize only major markets like Germany, France, and Italy. Additionally, audiovisual regulations vary significantly. According to the European Commission, only a small share of European films achieve distribution in more than five EU countries, highlighting the market fragmentation. Streaming platforms face similar hurdles, licensing rights are often negotiated on a country-by-country basis due to territorial copyright laws, resulting in uneven catalog availability. This balkanization inflates operational complexity and dilutes marketing impact, preventing the emergence of truly pan European entertainment franchises comparable to US or Korean counterparts.

Rising Cost of Living Pressuring Discretionary Entertainment Spending

Economic pressures stemming from inflation and stagnant wage growth have begun to constrain household budgets for non-essential leisure activities across Europe, which is further hindering the growth of the European entertainment market. According to Eurostat, inflation in the eurozone has impacted entertainment costs, with live event prices rising faster than general inflation. As per the European Consumer Organisation, households in countries like Italy and the UK reported cutting back on paid entertainment, with many consumers opting to cancel subscription services. Cinema attendance, while recovering overall, shows vulnerability as premium format tickets have become more expensive, pricing out younger and lower income groups. Similarly, music festival passes are reported to be costly, limiting accessibility despite high demand. This financial squeeze is accelerating a shift toward free or ad supported alternatives, compressing revenue for premium content providers. Although public funding buffers some sectors, commercial entertainment relies heavily on consumer willingness to pay, which is increasingly sensitive to macroeconomic conditions. Without innovative pricing models or bundled value propositions, sustained growth in paid entertainment may stall even as digital access expands.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence in Content Creation and Personalization

Artificial intelligence is unlocking efficiencies and creative possibilities across Europe’s entertainment value chain from scriptwriting to audience targeting, which is a promising opportunity in the European entertainment market. As per pilot programs in Finland and the Netherlands, generative AI tools are being deployed to automate subtitling in multiple languages, reducing localization time significantly. AI driven recommendation engines now power most content discovery on major European streaming platforms, increasing viewer retention by tailoring suggestions based on behavioral patterns. In music, AI composition tools are being used by indie artists in Berlin and Lisbon to generate royalty free background scores. More significantly, immersive experiences are being enhanced through real time AI avatars and adaptive storytelling. According to the European Innovation Council, investments in creative AI startups have been rising, which is signalling strong institutional confidence. These applications not only reduce costs but also enable hyper personalized engagement, allowing European creators to compete globally through innovation rather than scale.

Revival of Experiential and Location Based Entertainment Formats

A growing consumer preference for tangible, social, and memorable experiences is driving renewed investment in physical entertainment venues across Europe, which is another prominent opportunity in the European entertainment market. Audiences are seeking authenticity and human connection, fuelling demand for immersive theatre, themed dining, escape rooms, and pop-up art installations. As per the European Festival Association, music festivals have evolved beyond concerts to include wellness zones, culinary villages, and interactive art, contributing to higher attendee spending. Theme parks also report strong recovery, with Disneyland Paris welcoming large visitor numbers in 2024. According to a Eurobarometer survey, many Europeans aged 18 to 35 prioritize experiences over material goods. Operators are responding by integrating technology such as AR scavenger hunts and NFC enabled wearables to blend digital interactivity with physical presence. This hybrid model offers resilience against online competition while fostering community loyalty.

MARKET CHALLENGES

Persistent Piracy and Unauthorized Content Distribution Undermining Revenue Integrity

Despite legal advancements, digital piracy continues to erode legitimate revenue streams across Europe’s entertainment sectors, particularly in film, television and music, which is a challenging factor to the growth of the European entertainment market. According to the European Union Intellectual Property Office, piracy websites targeting EU users recorded billions of visits in 2024, with streaming piracy accounting for most infringing activity. Popular new releases often appear on illicit platforms within hours of official launch, diverting potential subscribers and ticket buyers. As per the European Audiovisual Observatory, the audiovisual industry loses billions annually due to unlicensed access. Enforcement remains challenging due to jurisdictional complexities and the use of decentralized hosting and cryptocurrency payments. While site blocking orders have increased, the cat and mouse nature of domain hopping limits long term effectiveness. Moreover, according to a Eurobarometer study, many Europeans aged 16 to 24 view streaming from unofficial sources as acceptable. This normalization weakens the deterrents necessary for sustainable content financing, especially for independent creators who lack the marketing budgets to compete with free alternatives.

Talent Shortages in Emerging Creative Technology Disciplines

The growth of the European entertainment market is also expected to be challenged by the convergence of entertainment and advanced technology has created acute demand for hybrid professionals skilled in both artistic expression and technical execution, yet Europe faces a critical gap in this workforce. Roles such as virtual production supervisors, real time engine developers, and spatial audio designers are increasingly essential for next generation content, but educational pipelines have not kept pace. As per a survey by the European Film Academy, many production companies reported difficulty hiring staff proficient in Unreal Engine or volumetric capture techniques. Similarly, the gaming sector struggles to fill AI narrative design positions, with vacancies in countries such as Sweden and Poland remaining open for long periods. This shortage stems from fragmented curricula, while countries like France and Finland offer specialized programs, most EU nations lack standardized accreditation for emerging creative tech fields. Consequently, studios either outsource key functions or delay innovation. According to the European Commission, the creative industries will require hundreds of thousands of additional digital creatives by 2027, yet current graduation rates in relevant disciplines fall short. Without coordinated investment in vocational training and cross sectoral apprenticeships, Europe risks losing its competitive edge in immersive and interactive entertainment just as global demand accelerates.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 20.45% |

| Segments Covered | By Type, Application, Devices and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | The Walt Disney Company, Netflix, Warner Bros. Discovery, Comcast Corporation, Sony Group Corporation, Vivendi SE, RTL Group, ITV plc, ProSiebenSat.1 Media SE, Banijay Group, BBC Studios, and Sky Group. |

SEGMENTAL ANALYSIS

By Type Insights

The video segment dominated the market by commanding for 47.4% of the European market share in 2025. The dominance of video segment in the European market is attributed to the convergence of on demand streaming, cinematic releases, and user generated content platforms that cater to diverse viewing preferences. According to the European Audiovisual Observatory, Europeans spend significant time watching video content, with subscription video on demand services capturing a major share of that time. The proliferation of high definition and 4K content has further elevated engagement, as per the European Commission, many broadband households in Western Europe own 4K capable devices. Major streaming platforms have localized their libraries extensively, with Netflix offering content in multiple European languages. Additionally, cinema admissions rebounded strongly across the EU, exceeding pre pandemic levels, according to the European Audiovisual Observatory. Public broadcasters also contribute substantially, commissioning extensive hours of original drama annually. This ecosystem spanning free, ad supported, subscription, and theatrical models ensures video remains the cornerstone of European entertainment consumption.

The games segment is the fastest growing category in the Europe entertainment market and is expected to exhibit a CAGR of 10.5% over the forecast period owing to the mainstreaming of gaming as a social and cultural activity rather than a niche hobby. According to the Interactive Software Federation of Europe, the region is home to a large gaming population. Mobile gaming leads adoption, with smartphones serving as the primary platform for most players. Cloud gaming is emerging rapidly, with Microsoft’s Xbox Cloud Gaming reporting strong growth in European active users. Esports viewership has also surged, with the League of Legends European Championship drawing significant concurrent audiences. Furthermore, regulatory clarity in markets like Germany and the Netherlands has enabled licensed real money gaming integrations. Educational institutions are increasingly incorporating game-based learning, while public festivals such as Gamescom in Cologne attract large audiences annually. These converging trends position gaming not just as entertainment but as a central pillar of digital culture across generations.

By Application Insights

The residential segment led the market by holding 81.1% of the regional market share in 2025. The growth of the residential segment in the European market can be credited to the deep entrenchment of home-based leisure as the primary mode of entertainment engagement across urban and rural populations. According to Eurostat, most European households owned at least one internet connected entertainment device in 2024, with smart TVs present in many homes. The post pandemic normalization of remote work and hybrid lifestyles has sustained high at home media usage. Subscription services thrive in this environment, as per the European Audiovisual Observatory, most streaming revenue originates from residential accounts. Home audio systems have also evolved, with wireless speaker adoption rising steadily. Cultural habits reinforce this trend, family movie nights, solo gaming sessions, and music listening remain deeply embedded in domestic routines. Public investment in broadband infrastructure further enables high quality home experiences, making residential entertainment not only convenient but increasingly immersive and socially connected.

The commercial segment is anticipated to record a healthy CAGR of 12.2% over the forecast period owing to the resurgence of experiential venues seeking to differentiate from digital alternatives through physical immersion and social interaction. Live entertainment spaces including cinemas, concert halls, theme parks, and immersive art installations have undergone significant technological upgrades to enhance audience engagement. As per the European Live Events Association, music festivals reported strong attendance, with millions of people attending major events such as Glastonbury and Roskilde. Retail and hospitality sectors are also integrating entertainment, with shopping malls in Spain and Italy featuring interactive gaming zones and live DJ booths. Corporate demand for event-based entertainment has risen, with business conferences increasingly incorporating live performances and virtual reality activations. These commercial renaissance leverages technology not to replace but to amplify human presence, creating memorable, shareable moments that digital platforms cannot replicate.

By Devices Insights

The smartphones segment held the largest share of 51.5% of the European market in 2025. The dominance of smartphones segment in the European market is driven by near universal ownership, advanced hardware capabilities, and seamless integration into daily life. According to the European Commission, most Europeans aged 16 to 74 owned a smartphone in 2024, with many using it daily for media consumption. Mobile networks support this usage, with 5G coverage expanding across the EU urban population. Apps are optimized for vertical and short form content, aligning with attention patterns. As per Spotify, most European listeners accessed content primarily via smartphones. The device’s portability allows entertainment to permeate commutes, breaks, and social settings, making it the default gateway for on demand culture. Manufacturers continue to enhance audiovisual quality, with OLED displays and spatial audio becoming standard in mid-tier models, further cementing the smartphone’s role as the central entertainment hub for European consumers.

The smart TVs segment is estimated to witness a CAGR of 11.5% over the forecast period in the European entertainment market due to falling prices, larger screen adoption, and deep integration with streaming ecosystems. According to Eurostat, smart TV ownership has been increasing steadily across European households. Manufacturers like Samsung and LG have embedded voice assistants and app stores directly into operating systems, reducing reliance on external devices. Streaming platforms prioritize TV interfaces due to higher engagement, with Netflix reporting longer session durations on smart TVs compared to mobile. The rise of ambient and interactive modes adds utility beyond passive viewing. Additionally, public service broadcasters such as BBC and ARD have optimized their on-demand services for smart TV platforms, ensuring accessibility for older demographics. As 4K and HDR content becomes standard, and as AI powered recommendation engines personalize home screens, the smart TV evolves from a display into an intelligent entertainment command center.

REGIONAL ANALYSIS

United Kingdom Entertainment Market Analysis

The United Kingdom dominated the entertainment market in Europe in 2025 with 19.5% of the regional market share. The leading position of the UK in the European market is driven by its globally influential creative industries and advanced digital infrastructure. London serves as a production epicentre for film, television, and music, hosting studios like Pinewood and Shepperton. According to the British Film Institute, British films captured a notable portion of the global non-US box office in 2024. Streaming penetration is among the highest in Europe, with many households subscribing to at least one video service. The country also leads in gaming, home to major developers like Rockstar North and Creative Assembly. Live entertainment thrives, with West End theatres selling millions of tickets in 2023. Government support through the UK Global Screen Fund and tax reliefs for animation and high-end television ensures continued competitiveness. This blend of heritage, innovation, and policy makes the UK a linchpin of European entertainment.

Germany Entertainment Market Analysis

Germany captured a promising position in the European entertainment market in 2025 with 16.1% of the regional market share. The robust public broadcasting system and strong regional cultural identity are driving the German market growth. The country operates numerous public and private television channels, with ARD and ZDF commanding significant viewership through high quality documentaries and drama. Germany’s market status is anchored in dual consumption patterns, traditional broadcast coexists with digital adoption. According to the International Federation of the Phonographic Industry, Germany is Europe’s largest music market, generating substantial recorded music revenue. Berlin and Munich serve as hubs for gaming and film production, supported by federal and state level funding programs. Cinema attendance has been strong, aided by the expansion of premium formats. Strict data privacy laws shape digital entertainment, favoring local platforms that comply with GDPR. This balance of regulation, public investment, and consumer diversity sustains Germany’s position as a stable and influential market.

France Entertainment Market Analysis

France is projected to hold a prominent share of the European entertainment market during the forecast period. The French market is characterized by strong state involvement and cultural protectionism. The country enforces quotas for European works on television and mandates that streaming services invest a portion of French revenue into local production, as per the Audiovisual Law. France’s market status is defined by cinematic excellence. According to FranceAgriMer and government reports, France produces a large number of feature films annually and hosts the Cannes Film Festival, which attracts many industry professionals. Music remains vital, with live concerts generating significant ticket sales. The government’s “France Relance” plan allocated funding to digitize cultural venues and support indie creators. Streaming is growing but tempered by regulations limiting simultaneous releases. With widespread smart TV ownership and high mobile penetration, France blends tradition with modernity, ensuring its cultural output remains both locally rooted and globally resonant.

Spain Entertainment Market Analysis

Italy is anticipated to record a healthy CAGR in the European entertainment market during the forecast period. The rich artistic heritage, evolving digital landscape, historic opera houses and film studios coexist with a booming mobile entertainment sector are driving the Italian entertainment market growth. As per AGCOM, Italians spend more time watching television than any other EU nation. Rai, the public broadcaster, remains dominant but faces competition from Sky Italia and streaming entrants. Italy is Europe’s second largest music market, with live events rebounding strongly. The government supports cinema through tax credits covering production costs, which is fuelling growth in domestic film output. Gaming is surging, with millions of active players in 2024. Infrastructure improvements, including nationwide fiber rollout, enable high quality streaming, positioning Italy as a high potential market where tradition and technology increasingly converge.

Spain Entertainment Market Analysis

Spain is estimated to showcase a steady CAGR in the European entertainment market over the forecast period. Spain is notable for its dynamic live entertainment scene, rapid digital adoption, a youthful population and Mediterranean lifestyle that prioritizes social and outdoor leisure. Spain hosts numerous major music festivals annually, including Primavera Sound and Mad Cool, drawing large international audiences, as per the European Live Events Association. Cinema attendance has been strong, supported by a network of multiplexes and government subsidies for local films. Streaming penetration has grown steadily, with Movistar+ leading domestic offerings. The gaming sector is expanding fast. According to the Spanish Association of Video Game Developers, millions of Spaniards played video games in 2024. Barcelona and Madrid have emerged as tech creative hubs, attracting investment in virtual production and esports. With 5G coverage expanding across urban areas and strong tourism inflows, Spain leverages its cultural vibrancy and connectivity to drive entertainment growth across both physical and digital domains.

COMPETITIVE LANDSCAPE

Competition in the Europe entertainment market is characterized by intense rivalry among global streaming giants, established media conglomerates, and agile regional creators vying for consumer attention in a fragmented yet highly regulated environment. Unlike unified markets, Europe’s linguistic and cultural diversity demands significant investment in localization, making scale alone insufficient for success. Major players compete not only on content volume but on authenticity, technological quality, and compliance with national quotas and data privacy laws. Simultaneously, traditional broadcasters are transforming into digital platforms, while gaming and live entertainment sectors blur boundaries through cross media franchises. The rise of user generated content and short form video adds pressure on professional producers to innovate faster. Regulatory scrutiny around market dominance, tax contributions, and cultural preservation further shapes competitive dynamics. Success hinges on balancing global efficiency with local relevance, ensuring that entertainment offerings resonate emotionally while adhering to Europe’s unique socio legal framework governing media pluralism and consumer protection.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Cocoa Market include

- The Walt Disney Company

- Netflix

- Warner Bros. Discovery

- Comcast Corporation

- Sony Group Corporation

- Vivendi SE

- RTL Group

- ITV plc

- ProSiebenSat.1 Media SE

- Banijay Group

- BBC Studios

- Sky Group

Top Players in the Market

Netflix Inc

Netflix Inc maintains a formidable presence in the Europe entertainment market through its extensive library of localized and original content tailored to diverse linguistic and cultural preferences. The company operates in all European countries, offering programming in over 18 regional languages and investing heavily in local productions from Spain, Germany, and Poland. In recent years, Netflix has expanded its interactive storytelling initiatives and enhanced its recommendation algorithms using machine learning to improve user retention. It also strengthened partnerships with European public broadcasters for co productions and secured exclusive streaming rights for major film festivals like San Sebastián. These actions reinforce its commitment to cultural relevance and technological innovation while deepening audience engagement across the continent.

The Walt Disney Company

The Walt Disney Company exerts significant influence in the Europe entertainment market through its integrated portfolio of streaming, theatrical, theme parks, and consumer products. Disney+ launched localized versions across all major European markets by 2021 and continues to invest in region specific content, including French animated series and Nordic crime dramas. The company recently upgraded its streaming infrastructure to support 4K HDR and Dolby Atmos across Europe, enhancing home viewing quality. Additionally, Disneyland Paris underwent a €2 billion expansion completed in 2024, adding immersive Star Wars and Frozen zones that attracted record visitor numbers. These strategic moves solidify Disney’s position as a leader in both digital and experiential entertainment throughout the region.

Sony Group Corporation

Sony Group Corporation plays a pivotal role in the Europe entertainment market through its dual strength in hardware and content creation. Its PlayStation gaming consoles dominate the console segment, supported by first party studios like Guerrilla Games in the Netherlands and Firesprite in the UK. Sony Pictures Entertainment produces and distributes films widely across European cinemas, while Sony Music represents top artists from Sweden, France, and Italy. In 2024, Sony launched a cloud-based game streaming enhancement for PlayStation Plus in key European markets, reducing latency through local data centers. It also expanded its spatial audio technology into music and film production workflows, aligning with Europe’s demand for premium immersive experiences. These initiatives underscore Sony’s integrated approach to entertainment delivery.

Top Strategies Used by the Key Market Participants

Key players in the Europe entertainment market prioritize localization through multilingual content and culturally resonant storytelling to deepen audience connection. They invest in advanced streaming infrastructure to deliver high quality 4K HDR and low latency experiences across diverse broadband environments. Strategic co productions with European studios and public broadcasters enhance authenticity and regulatory alignment. Companies also expand into experiential domains such as theme parks and live events to complement digital offerings. Additionally, they deploy artificial intelligence for personalized recommendations and real time content moderation to meet GDPR and youth protection standards. Continuous innovation in immersive audiovisual technologies further differentiates their services in a saturated landscape.

MARKET SEGMENTATION

This research report on the Europe Entertainment Market has been segmented and sub-segmented based on the following categories.

By Type

- Video

- Audio

- Games

- Internet Radio

- Others

By Application

- Residential

- Commercial

By Devices

- Smartphones

- Smart TVs

- Projectors

- Laptop

- Desktops

- Tablets

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe Entertainment Market?

The Europe Entertainment Market refers to the industry covering film, television, music, gaming, live events, digital streaming, and sports entertainment across European countries.

What are the major growth drivers of the Europe Entertainment Market?

Growth is driven by rising digital streaming adoption, expanding gaming industry, increasing internet penetration, and higher consumer spending on leisure and media content.

Which countries dominate the Europe Entertainment Market?

The United Kingdom, Germany, France, Italy, and Spain are major contributors due to strong digital infrastructure and high media consumption rates.

How is OTT streaming impacting the market?

OTT platforms have significantly transformed content consumption by promoting on-demand viewing, subscription-based models, and original content production.

What role does gaming play in the Europe Entertainment Market?

Gaming is one of the fastest-growing segments, supported by increasing console adoption, mobile gaming growth, and the expansion of eSports competitions.

How has digital transformation influenced the market?

Digital transformation has enabled personalized content recommendations, multi-device accessibility, and growth in cloud gaming and virtual entertainment.

What are the challenges faced by the Europe Entertainment Market?

Challenges include content piracy, regulatory compliance, high production costs, and intense competition among streaming platforms.

What trends are shaping the future of the Europe Entertainment Market?

Key trends include localized content production, AI-driven content recommendations, hybrid theatrical-streaming releases, immersive AR/VR experiences, and expansion of subscription-based revenue models.

What impact does regulatory policy have on the Europe Entertainment Market?

European content regulations, data protection laws (such as GDPR), and quotas for local content production influence operational strategies and investment decisions of entertainment companies.

How is technology shaping the future of the Europe Entertainment Market?

Technologies such as AI-based recommendation engines, virtual reality (VR), augmented reality (AR), cloud gaming, and advanced streaming infrastructure are enhancing user engagement and transforming content delivery models.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com