Europe Ethylene Market Size, Share, Trends, & Growth Forecast Report By Feedstock ( Naphtha, Ethane, Propane, Butane, Others), Application, End-user Industry and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Ethylene Market Report Summary

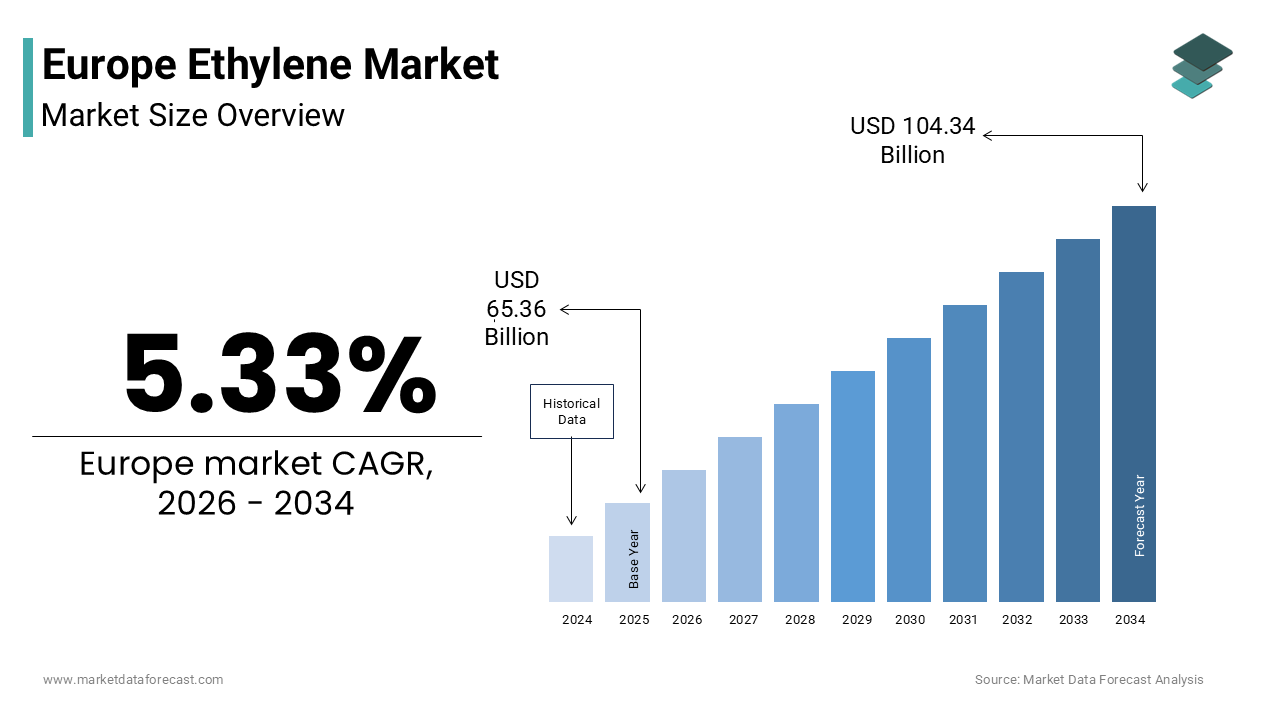

The Europe ethylene market was valued at USD 65.36 billion in 2025, is estimated to reach USD 68.85 billion in 2026, and is projected to reach USD 104.34 billion by 2034, growing at a CAGR of 5.33% during the forecast period from 2026 to 2034. The growth of the Europe ethylene market is driven by strong demand from the packaging, automotive, and construction industries, along with increasing reliance on ethylene as a key building block for essential polymers and chemical derivatives. The rising demand for polyethylene in packaging applications, the expansion of electric vehicle production, and growing construction activities are further supporting market expansion. Moreover, the increasing focus on circular economy practices, including advanced recycling and the use of renewable feedstocks, is reshaping the market landscape across Europe.

Key Market Trends

- Rising demand for polyethylene is driven by its extensive use in packaging applications, supported by the growth of e-commerce and food safety requirements.

- Increasing shift toward circular economy models, with growing investments in advanced recycling technologies to produce circular ethylene from plastic waste.

- Growing adoption of electric steam cracking technologies powered by renewable energy to reduce carbon emissions in ethylene production.

- Rising demand for ethylene derivatives in automotive and electric vehicle applications, particularly for lightweight materials and battery components.

- Expansion of bio-based and renewable feedstocks, enabling the development of low-carbon and sustainable ethylene products.

Segmental Insights

- Based on feedstock, the naphtha segment was the largest and held a significant share of the Europe ethylene market in 2025. The dominance of this segment is attributed to the well-established integration of refineries and petrochemical complexes across Europe, ensuring consistent feedstock availability despite global price volatility.

- Based on application, the polyethylene segment accounted for the largest share of the Europe ethylene market in 2025. The segment’s leadership is driven by its widespread use in packaging, construction, and consumer goods, along with its compatibility with recycling processes aligned with EU sustainability mandates.

- Based on end-use industry, the packaging segment was the largest, occupying a prominent share of the Europe ethylene market in 2025. The dominance of this segment stems from the essential role of plastic packaging in food preservation, logistics, and e-commerce, where lightweight and durable materials remain indispensable.

Regional Insights

The Europe ethylene market is witnessing steady growth across major economies, supported by strong industrial demand, integrated chemical infrastructure, and ongoing transition toward sustainable production technologies.

- Germany was the largest contributor, accounting for 28.4% of the European ethylene market share in 2025, driven by its large-scale chemical clusters, strong automotive sector, and advanced manufacturing ecosystem.

- France holds a significant position in the market, supported by its diversified industrial base and investments in low-carbon and bio-based ethylene production.

- The Netherlands serves as a key hub for ethylene production and distribution, leveraging its strategic location and advanced logistics infrastructure centered around the Port of Rotterdam.

- Italy is emerging as an important market driven by high-value applications in packaging, agriculture, and automotive sectors, while the United Kingdom is transitioning toward low-carbon ethylene production through carbon capture and hydrogen-based technologies.

Competitive Landscape

The Europe ethylene market is characterized by intense competition among leading global chemical companies focusing on sustainability, technological innovation, and integrated production capabilities. Major players are investing in electric cracking technologies, advanced recycling systems, and renewable feedstocks to reduce carbon emissions and align with strict European environmental regulations. Strategic partnerships, vertical integration, and expansion into high-value derivatives are key approaches adopted to strengthen market presence. Prominent players in the Europe ethylene market include BASF SE, INEOS Group AG, LyondellBasell Industries, Exxon Mobil Corporation, Shell plc, SABIC, Borealis AG, Chevron Phillips Chemical Company, Dow Inc., Mitsubishi Chemical Corporation, Mitsui Chemicals, and Equistar Chemicals.

Europe Ethylene Market Size

The Europe ethylene market size was valued at USD 65.36 billion in 2025 and is anticipated to reach USD 68.85 billion in 2026 from USD 104.34 billion by 2034, growing at a CAGR of 5.33% during the forecast period from 2026 to 2034

The ethylene is the foundational pillar of the continental petrochemical industry, encompassing the production, trade, and downstream conversion of ethene into essential polymers, intermediates, and chemical derivatives. As the simplest alkene, this colorless gas serves as the primary building block for polyethylene, ethylene oxide, ethylene dichloride, and styrene, which are indispensable to packaging, automotive, construction, and healthcare sectors. In 2024, the European Union produced approximately 19.5 million metric tons of ethylene, with Germany and France accounting for nearly 45% of this output, according to data from Cefic. Furthermore, the region faces a critical dependency on imported feedstocks, with over 90% of naphtha sourced from global markets, exposing the industry to geopolitical volatility. This complex interplay between established industrial capacity, feedstock constraints, and aggressive sustainability targets defines the strategic trajectory of the European countries.

MARKET DRIVERS

Robust Demand from the Packaging and Circular Economy Sector

The sustained and evolving demand from the packaging industry, which remains the largest consumer of polyethylene derived from ethylene, even amidst the transition to circular economy models is propelling the growth of Europe ethylene market. Despite regulatory pressures to reduce single-use plastics, the sheer volume of food safety requirements, e-commerce growth, and the need for lightweight, durable materials ensures that virgin and recycled polyethylene remain crucial. In 2024, the European packaging sector consumed over 8.2 million metric tons of polyethylene, representing approximately 35% of total ethylene derivative demand, according to Plastics Europe. The drive toward recyclable mono-material structures, which often rely on specific grades of linear low-density polyethylene (LLDPE) and high-density polyethylene (HDPE), has shifted demand toward higher-performance ethylene derivatives rather than eliminating it. Furthermore, the European Union's mandate for minimum recycled content in plastic bottles and packaging by 2030 has spurred investment in advanced recycling technologies that convert waste plastics back into pyrolysis oil, which is then cracked to produce circular ethylene.

Expansion of Downstream Derivative Industries in Automotive and Construction

The persistent demand from the automotive and construction sectors for high-performance ethylene derivatives, such as ethylene-propylene-diene monomer (EPDM) rubber, polyvinyl chloride (PVC), and engineering thermoplastics is elevating the growth of Europe ethylene market. The European automotive industry, despite its transition to electric vehicles, continues to rely heavily on ethylene-based materials for lightweighting components, wiring insulation, and interior trim to improve energy efficiency and range. Simultaneously, the construction sector's renovation wave, aimed at improving energy efficiency in buildings, drives substantial consumption of PVC pipes, window profiles, and insulation foams derived from ethylene. Additionally, the shift toward electric vehicles increases the need for specialized ethylene-based battery separators and cable shielding, creating new niche applications. As per the European Chemical Industry Council, the construction and automotive sectors collectively account for over 40% of non-packaging ethylene derivative consumption.

MARKET RESTRAINTS

Structural Disadvantage Due to Naphtha Feedstock Dependency

The structural cost disadvantage arising from its heavy reliance on naphtha as a cracking feedstock, compared to competitors in North America and the Middle East, who utilize cheaper ethane is majorly prompting the growth of Europe ethylene market. Approximately, 75% of European ethylene production capacity is designed for naphtha cracking by making the region highly vulnerable to global crude oil price fluctuations and refining margins. The situation is exacerbated by the fact that naphtha yields a broader spectrum of co-products, which can become a burden when demand for those co-products is weak, further distorting the economic balance of the cracker. This fundamental feedstock mismatch creates a persistent profitability crisis, forcing many operators to consider permanent closures or costly conversions, thereby constraining supply growth and investment confidence.

Soaring Energy Costs and Carbon Compliance Burdens

The exorbitant cost of energy and the increasing financial burden of carbon compliance under the European Union Emissions Trading System is additionally degrading the growth of Europe ethylene market. Steam cracking is an extremely energy-intensive process, requiring vast amounts of natural gas and electricity to achieve the high temperatures necessary for breaking hydrocarbon bonds. In 2025, industrial natural gas prices in Europe remained 40% higher than pre-2022 levels, significantly inflating operational expenditures for ethylene producers according to Eurostat energy data. Compounding this issue is the rising cost of carbon allowances, which exceeded 85 euros per ton of CO2 in 2024 by adding a substantial premium to every ton of fossil-based ethylene produced. The CBAM mechanism further complicates the landscape by altering trade dynamics while domestic producers face strict decarbonization mandates without equivalent global pressure on competitors.

MARKET OPPORTUNITIES

Development of Electric Cracking and Renewable Feedstock Integration

The pioneering adoption of electric steam cracking technologies and the integration of renewable feedstocks to achieve deep decarbonization and secure a first-mover advantage in green chemicals is certainly creating new opportunities for the growth of Europe ethylene market. Several consortiums involving major chemical players and technology providers are actively developing large-scale electric crackers powered by renewable electricity, which could eliminate direct Scope 1 emissions from the cracking process. In 2025, the European Union allocated 3 billion euros through the Innovation Fund to support pilot and demonstration projects for electric cracking, aiming to commercialize the technology by 2028 according to the European Climate, Infrastructure and Environment Executive Agency. Simultaneously, the shift toward bio-naphtha and pyrolysis oil derived from plastic waste offers a pathway to produce circular ethylene with a significantly lower carbon footprint, appealing to brand owners committed to net-zero goals. As per the Nova-Institute, the market potential for bio-based and circular ethylene in Europe could reach 4 million metric tons by 2030 if scaling challenges are overcome. This technological leap not only addresses regulatory pressures but also creates a premium product segment where European producers can differentiate themselves from global competitors relying on fossil feedstocks.

Expansion of Advanced Recycling Infrastructure for Circular Ethylene

The rapid expansion of advanced (chemical) recycling infrastructure to secure a domestic supply of circular feedstocks and reduce dependency on imported virgin polymers is additionally to leverage the growth of Europe ethylene market. Unlike mechanical recycling, advanced recycling can handle mixed and contaminated plastic waste by converting it back into naphtha-like streams that can be fed directly into existing steam crackers to produce circular ethylene indistinguishable from virgin material. The European Union's stringent targets for recycled content in packaging, mandating 30% recycled plastic in PET bottles and significant shares in other formats by 2030, create a guaranteed demand pull for circular ethylene derivatives. As per the Ellen MacArthur Foundation, closing the loop on plastics through chemical recycling could capture 10 billion euros in annual value for the European economy. This opportunity allows ethylene producers to integrate vertically into waste management, securing feedstock sovereignty and creating a closed-loop value chain that aligns perfectly with the circular economy action plan. Companies that successfully scale these operations will gain access to premium markets and regulatory credits, establishing a resilient and future-proof business model.

MARKET CHALLENGES

Risk of Permanent Capacity Closure and Deindustrialization

The escalating risk of permanent capacity closures and the subsequent deindustrialization of the continent's chemical value chain due to prolonged unprofitability is key challenge for the growth of Europe ethylene market. Faced with structurally high energy costs, expensive carbon compliance, and fierce global competition, several major producers have already announced the indefinite shutdown of older, less efficient steam crackers across Germany, France, and the Netherlands. This contraction threatens the integrity of the integrated chemical clusters that rely on ethylene as a feedstock for dozens of downstream derivatives by potentially triggering a cascade of production cuts in polyethylene, glycols, and vinyls. As per the German Chemical Industry Association, the loss of ethylene capacity could jeopardize up to 50,000 jobs in the broader chemical sector and force downstream manufacturers to relocate production to regions with secure and affordable feedstock. The long lead times and massive capital requirements needed to build new, sustainable capacity, creating a dangerous gap between retiring assets and future replacements.

Complexity in Scaling Circular and Bio-Based Value Chains

The technical and logistical complexity of scaling circular and bio-based value chains to a level that can meaningfully replace fossil-based ethylene production is another attribute to limit the growth of Europe ethylene market. While the potential for bio-naphtha and pyrolysis oil is vast, the current collection, sorting, and pre-treatment infrastructure for plastic waste and biomass in Europe is fragmented and insufficient to support the volumes required by large-scale crackers. Furthermore, the lack of harmonized standards for mass balance accounting and the certification of circular content creates regulatory uncertainty and hampers cross-border trade of recycled feedstocks. As per the European Commission's Joint Research Centre, the cost of collecting and processing plastic waste for chemical recycling remains 3 times higher than producing virgin naphtha, requiring significant subsidies or mandatory premiums to bridge the gap. The technological hurdles in ensuring consistent feedstock quality for sensitive cracking units also pose operational risks.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.33% |

| Segments Covered | By Feedstock, Application, End-user Industry and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | BASF SE, INEOS Group AG, LyondellBasell Industries Holdings B.V., Exxon Mobil Corporation, Royal Dutch Shell plc, SABIC (Saudi Basic Industries Corporation), Borealis AG, Chevron Phillips Chemical Company LLC, Dow Inc., Mitsubishi Chemical Corporation, Mitsui Chemicals Inc., and Equistar Chemicals LP. |

SEGMENTAL ANALYSIS

By Feedstock Insights

The naphtha segment was the largest by holding a prominent share of the Europe ethylene market in 2025 with the structurally embedded in the region's refining landscape, where the majority of steam crackers were historically designed and optimized to process liquid hydrocarbons rather than gaseous ethane. The deep integration between European refineries and petrochemical complexes, which ensures a steady supply of naphtha as a primary output of crude oil distillation by creating a symbiotic relationship that stabilizes feedstock availability despite global fluctuations. The flexibility of naphtha cracking, which yields a valuable slate of co-products including propylene, butadiene, and benzene, all of which are in high demand, across the European chemical value chain. As per the European Petroleum Refiners Association, the economic viability of many refineries depends on this integrated model, where the margin from selling these co-products subsidizes the higher cost of naphtha compared to shale gas. This structural interdependence and the lack of sufficient domestic ethane infrastructure cement naphtha's position as the backbone of European ethylene production.

The "Others" segment is esteemed to witness a fastest CAGR of 18.5% from 2026 to 2034 with the aggressive regulatory push toward circularity and carbon neutrality, which compels producers to seek alternatives to fossil-based inputs. The European Union's Circular Economy Action Plan and the Carbon Border Adjustment Mechanism, which create powerful financial incentives for producing "circular ethylene" with a significantly lower carbon footprint. The investments in advanced recycling facilities capable of converting mixed plastic waste into pyrolysis oil surged by 40%, with over 15 new plants announced across Germany, France, and the Netherlands, according to the study. The rising demand from brand owners for certified sustainable polymers, who are willing to pay a premium for mass-balanced ethylene derived from renewable sources to meet their own net-zero commitments is also propelling the growth of segment. As per the Nova-Institute, the volume of bio-based and circular naphtha available for cracking in Europe is expected to reach 2.5 million metric tons by 2030, up from less than 200,000 tons in 2024. Furthermore, technological advancements in pre-treatment processes have improved the quality of recycled feedstocks, making them compatible with existing cracker furnaces without requiring massive retrofitting.

By Application Insights

The polyethylene segment was accounted in holding 58.5% of the Europe ethylene market owing to the material's unparalleled versatility, cost-effectiveness, and essential role in packaging, construction, and consumer goods across the continent. The insatiable demand from the packaging sector, which relies on polyethylene films, bottles, and containers for food safety, e-commerce logistics, and industrial wrapping, which is driven by the need for lightweight and durable materials. The material's adaptability to recycling streams, particularly mechanical recycling, which aligns with EU mandates for increased recycled content in single-use plastics is also escalating the growth of segment. The ability to blend virgin and recycled polyethylene, while maintaining performance standards makes it the preferred choice for manufacturers navigating the transition to a circular economy. As per the survey, the requirement for 30% recycled content in PET bottles by 2030 has spurred similar initiatives for polyethylene packaging, driving innovation in recyclable grades. Furthermore, the construction sector's reliance on HDPE for pressure pipes and geomembranes ensures a stable baseline demand independent of consumer trends.

The ethylene oxide segment is expected to grow at an anticipated CAGR of 6.8% from 2026 to 2034 with the expanding demand for its downstream derivatives, particularly ethylene glycols and ethoxylates, which are critical for the automotive, pharmaceutical, and personal care industries. The primary driver is the surging production of electric vehicles and the associated need for high-performance battery electrolytes and thermal management fluids, where monoethylene glycol plays a vital role. The robust growth in the pharmaceutical and healthcare sectors, where ethylene oxide is indispensable for the sterilization of medical devices and the synthesis of active pharmaceutical ingredients is also fuelling the growth of the segment. The post-pandemic emphasis on hygiene and medical preparedness has sustained elevated demand for sterile disposable products, relying heavily on ethylene oxide sterilization capabilities. Additionally, the personal care industry's shift toward mild, bio-based surfactants derived from ethoxylation further boosts demand.

By End Use Industry Insights

The packaging industry segment was accounted in holding 42.3% of the Europe ethylene market share in 2025 with the essential nature of plastic packaging in preserving food safety, extending shelf life, and facilitating the booming e-commerce logistics network across the continent. The relentless growth of the food and beverage sector, which requires high-barrier, lightweight, and tamper-evident packaging solutions primarily made from polyethylene and polyethylene terephthalate to meet strict hygiene standards and reduce food waste. The explosion of online retail, which has drastically increased the demand for flexible shipping envelopes, protective air pillows, and stretch films, all predominantly manufactured from ethylene derivatives. Furthermore, the industry's proactive shift toward mono-material structures that are easier to recycle aligns with EU sustainability goals, ensuring continued social license to operate. The inability of alternative materials like glass or metal to match the weight-to-strength ratio and cost efficiency of ethylene-based plastics cements the packaging sector's position as the primary consumer.

The automotive industry segment is lucratively to register a fastest CAGR of 7.2% from 2026 to 2034 with the radical transformation of the vehicle architecture driven by the transition to electric mobility and the imperative for extreme lightweighting to maximize battery range. The increasing substitution of traditional metal components with advanced engineering thermoplastics and composites derived from ethylene, such as high-density polyethylene tanks, polypropylene bumpers, and ethylene-propylene rubber seals, which offer significant weight reduction without compromising safety. The specialized demand for ethylene-based materials in battery systems, including separators, casing, and thermal interface materials, which are for the safety and efficiency of EV powertrains is additionally escalating the growth of segment. As per the European Battery Alliance, the continent's battery manufacturing capacity is set to exceed 600 gigawatt-hours by 2030, creating a massive new addressable market for high-purity ethylene derivatives. Additionally, the push for sustainable interiors has led to the adoption of bio-based polyolefins in cabin components.

REGIONAL ANALYSIS

Germany Ethylene Market Analysis

Germany was the top performer in the Europe ethylene market by holding 28.4% of share in 2025 with its massive, highly integrated chemical clusters along the Rhine River, which serve as the primary processing hubs for naphtha cracking and downstream derivative production. In 2024, German steam crackers produced over 5.5 million metric tons of ethylene, feeding a dense network of manufacturers in the automotive, packaging, and construction sectors according to the German Chemical Industry Association. The country's robust automotive industry, the largest in Europe, drives substantial demand for engineering plastics and rubber components, while its strong export-oriented packaging sector consumes vast volumes of polyethylene. Furthermore, Germany is at the forefront of the energy transition, hosting pilot projects for electric cracking and advanced recycling that aim to decarbonize ethylene production. The "Chemie Hoch 3" initiative supports these innovations, fostering a resilient ecosystem despite high energy costs.

France Ethylene Market Analysis

France ethylene market held second position by holding 18.3% of share in 2025 with its diversified industrial base and strong commitment to nuclear-powered low-carbon manufacturing. The French market is characterized by major integrated sites in Normandy and the Rhone-Alpes region, which produce ethylene for a wide range of applications including agriculture, aerospace, and luxury packaging. The country's ambitious "France 2030" investment plan allocates significant funds to develop bio-based and recycled feedstock value chains by positioning France as a leader in sustainable ethylene production. The aerospace sector, a key pillar of the French economy, drives demand for high-performance ethylene composites, while the agricultural sector utilizes ethylene derivatives for films and agrochemicals. The government's focus on energy sovereignty through nuclear power provides a competitive advantage in electricity costs for electrochemical processes, attracting investment in next-generation cracking technologies.

Netherlands Ethylene Market Analysis

The Netherlands ethylene market growth is likely to grow with its strategic location as the primary gateway for feedstock imports and product distribution via the Port of Rotterdam. The Dutch market is defined by some of the largest and most efficient steam cracking complexes in the world, which process imported naphtha and increasingly bio-based feedstocks to serve the entire Northwest European region. In 2024, the Netherlands produced over 2.8 million metric tons of ethylene, acting as a critical supplier to neighboring Germany and Belgium according to Statistics Netherlands. The country's advanced logistics infrastructure facilitates the seamless movement of raw materials and finished derivatives by making it a pivotal node in the European supply chain. Furthermore, the Netherlands is a global leader in circular economy initiatives, hosting numerous advanced recycling startups and large-scale pyrolysis projects aimed at producing circular ethylene. The "Top Sector Chemistry" agenda fosters collaboration between industry and academia to accelerate the deployment of electric cracking technologies.

Italy Ethylene Market Analysis

Italy ethylene market growth is likely to grow with its strong specialization in high-value added downstream applications, such as luxury packaging, automotive design, and agricultural films. The network of efficient cracking facilities in the south and north, which supply ethylene to a vibrant manufacturing sector known for quality and innovation. The major consumer of ethylene-derived mulch films and greenhouse covers, which is supporting its status as a leading food producer. Furthermore, Italy is actively investing in the modernization of its chemical parks to improve energy efficiency and integrate recycled feedstocks by aligning with EU Green Deal objectives. The "Made in Italy" brand commands a premium, driving the use of high-performance ethylene derivatives that meet strict aesthetic and functional standards.

United Kingdom Ethylene Market Analysis

The United Kingdom ethylene market growth is likely to grow with its ongoing transformation from fossil-based production to low-carbon and hydrogen-ready chemical manufacturing. The British market centers around major complexes in Teesside and the Humber region, which are currently undergoing significant redevelopment to integrate carbon capture and storage technologies. The country's aggressive net-zero targets have spurred the "East Coast Cluster" project by aiming to decarbonize ethylene production through blue hydrogen and electrification, positioning the UK as a testbed for future technologies. As per the UK Department for Energy Security and Net Zero, investments in carbon capture infrastructure for the chemical sector exceeded 2 billion pounds in 2025. The shift toward sustainable aviation fuels also creates new demand for ethylene derivatives.

COMPETITIVE LANDSCAPE

The competition in the Europe ethylene market is characterized by intense rivalry among established multinational giants and regional specialists who vie for dominance through technological innovation and sustainability leadership. Major players leverage their integrated value chains to offer comprehensive product portfolios while striving to reduce production costs amidst high energy prices and carbon compliance burdens. The market landscape features a shift from pure volume competition to differentiation based on carbon footprint and circular content as customers increasingly demand green materials. Competitive pressure drives continuous investment in breakthrough technologies like electric crackers and chemical recycling to future proof operations against regulatory changes. Pricing strategies remain complex due to feedstock volatility forcing firms to balance margin protection with market share retention in a shrinking domestic capacity environment. Strategic alliances with downstream converters and brand owners are common tactics to secure long term off take agreements for sustainable products. The threat of import substitution from regions with lower energy costs requires incumbent companies to constantly prove the value of locally produced low carbon ethylene.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe ethylene market include

- BASF SE

- INEOS Group AG

- LyondellBasell Industries Holdings B.V.

- Exxon Mobil Corporation

- Royal Dutch Shell plc

- SABIC (Saudi Basic Industries Corporation)

- Borealis AG

- Chevron Phillips Chemical Company LLC

- Dow Inc.

- Mitsubishi Chemical Corporation

- Mitsui Chemicals Inc.

- Equistar Chemicals LP

Top Players in the Europe Ethylene Market

BASF SE

BASF SE stands as a global chemical leader with a profound influence on the Europe ethylene market through its massive integrated production sites. The company supplies essential ethylene derivatives to industries worldwide ranging from automotive to packaging. Recent actions to strengthen its market position include significant investments in electric steam cracking technology to decarbonize production and reduce reliance on fossil fuels. BASF actively collaborates with energy providers to secure renewable electricity for its Ludwigshafen complex ensuring long term sustainability. The firm also expands its circular economy initiatives by incorporating pyrolysis oil from plastic waste into its cracker feedstock mix. These strategic moves demonstrate a commitment to innovation and environmental stewardship while maintaining operational efficiency.

Shell plc

Shell plc operates as a major integrated energy and chemicals company with a substantial footprint in the Europe ethylene sector via its refining and cracking assets. The corporation contributes globally by providing high quality ethylene and downstream polymers essential for modern manufacturing and consumer goods. Recent efforts to bolster its market presence involve the development of advanced recycling facilities that convert post consumer plastic waste into circular feedstocks for ethylene production. Shell has committed to achieving net zero emissions in its European operations by investing in carbon capture and storage projects linked to its chemical plants. The company also optimizes its portfolio by focusing on high value derivatives rather than commodity volumes to enhance margins. Through these targeted investments in sustainability and portfolio optimization Shell reinforces its competitive edge. These initiatives ensure its continued relevance in a rapidly evolving market driven by strict environmental regulations and shifting consumer demands.

INEOS Group

INEOS Group functions as a leading private chemical manufacturer with a dominant position in the Europe ethylene market known for its operational excellence and asset integration. The company serves global customers by delivering reliable supplies of ethylene and its derivatives used in construction healthcare and packaging applications. Recent strategic actions include the acquisition of additional naphtha cracking capacity to secure feedstock flexibility and expand production capabilities in key industrial hubs. INEOS actively pursues partnerships to develop hydrogen infrastructure that will support the decarbonization of its steam crackers and reduce carbon intensity. The firm also invests heavily in digital technologies to optimize plant performance and minimize energy consumption across its European network. These forward looking measures position the company as a robust player capable of navigating the complex transition toward a low carbon future while meeting diverse industrial needs.

Top Strategies Used by Key Market Participants

Key players in the Europe ethylene market predominantly employ decarbonization strategies such as electric cracking and carbon capture to comply with stringent environmental regulations and secure long term viability. Companies frequently pursue vertical integration to control feedstock supply chains and mitigate risks associated with naphtha price volatility and availability. Strategic partnerships with waste management firms enable the development of advanced recycling infrastructures that provide circular feedstocks for sustainable ethylene production. Investment in digitalization and artificial intelligence optimizes operational efficiency reduces energy consumption and enhances predictive maintenance capabilities across large scale complexes. Diversification into high value specialty derivatives allows manufacturers to improve margins and reduce exposure to commodity cycle fluctuations. Mergers and acquisitions are utilized to consolidate assets acquire innovative technologies or exit non core businesses to streamline portfolios. Collaboration with renewable energy providers ensures access to green electricity necessary for electrified production processes. These multifaceted approaches collectively ensure competitiveness and resilience in a dynamic and highly regulated industry facing structural transformation.

MARKET SEGMENTATION

This research report on the Europe ethylene market has been segmented and sub-segmented based on the following categories.

By Feedstock

- Naphtha

- Ethane

- Propane

- Butane

- Others

By Application

- Polyethylene

- Ethylene Oxide

- Ethylbenzene

- Ethylene Dichloride

- Vinyl Acetate

- Others

By End Use Industry

- Packaging

- Automotive

- Building & Construction

- Agrochemical

- Textile

- Chemicals

- Rubber & Plastics

- Soaps & Detergents

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com