Europe Facility Management Market Size, Share, Trends & Growth Forecast Report By Mode of Delivery Insights (Outsourced Facility Management, In-House Facility Management), End User Insights, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe), Industry Analysis From 2026 To 2034

Market Size, 2025

$333.72 BnMarket Estimate, 2026

$351.54 BnMarket Forecast, 2034

$532.99 BnCAGR, 2026–2034

5.34%Executive Summary: Europe Facility Management Market

- Market Scope: Comprehensive regional Europe facility management market analysis covering delivery modes, end-user vertical segments, smart-building technologies, sustainability requirements, and country-level leadership frameworks.

- Market Valuation: Valued at USD 333.72 billion (2025 base year), estimated at USD 351.54 billion (2026), and projected to reach USD 532.99 billion by 2034, registering a steady CAGR of 5.34% (2026–2034).

- Primary Growth Drivers: Corporate outsourcing, integrated facility management adoption, smart-building technology integration, and strict sustainability mandates. Key operational, financial, and infrastructural highlights include ~€200 billion projected to be invested in European smart-city projects by 2025, commercial buildings accounting for nearly 25% of Europe’s total energy consumption, the top five market players collectively capturing ~40% of the market share, and ~70% of key players having adopted IoT-enabled facility systems.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Mode of Delivery | Outsourced Facility Management (dominated with a 65.2% market share in 2025) | In-House Facility Management (projected to register an 8.5% CAGR) |

| By End-User Sector | Commercial Buildings (led end-user segment with a 35.1% share in 2025) | Government & Public Entities (projected to expand at a 9.2% CAGR) |

| By Technology & Services | Standard Hard & Soft Facility Maintenance Services | IoT-Enabled Infrastructure, Real-Time Monitoring, AI & Predictive Maintenance |

| By Country / Region | Germany (led geographically with a 22.8% market share in 2025) | Pan-European Smart-City & Energy-Efficient Building Hubs |

Major Market Players & Market Structure

Market Structure: Moderately consolidated and highly competitive European facility management landscape featuring major multinational real estate services and property management conglomerates competing intensely on integrated service delivery, digital transformation, AI and predictive maintenance integration, sustainability compliance, and strategic enterprise partnerships.

Key Companies: CBRE Group, ISS A/S, Sodexo, Compass Group, Jones Lang LaSalle (JLL), Cushman & Wakefield, Atalian Servest, Mitie Group plc, Vinci Facilities, and G4S plc.

Europe Facility Management Market Size

The Europe Facility Management Market is projected to grow from USD 333.72 billion in 2025 to USD 351.54 billion in 2026 and reach USD 532.99 billion by 2034, registering a CAGR of 5.34% from 2026 to 2034.

The Europe facility management market is a changing landscape which is shaped by the region's emphasis on operational efficiency, sustainability, and technological adoption. Moreover, the market has witnessed steady growth due to stringent energy regulations and an increasing focus on green buildings across countries like Germany, France, and the UK. The demand for integrated facility management solutions is particularly strong, driven by corporate entities seeking cost-effective and streamlined operations.

The rise of smart cities and IoT-enabled infrastructure further propels this sector, as businesses increasingly adopt predictive maintenance and data-driven decision-making tools. In addition, the post-pandemic recovery phase has accelerated outsourcing trends, with small and medium enterprises turning to specialized service providers.

MARKET DRIVERS

Increasing Demand for Sustainable and Energy-Efficient Solutions

The European facility management market is significantly propelled by the growing emphasis on sustainability and energy efficiency, driven by stringent environmental regulations and corporate responsibility initiatives. The European Union’s Green Deal, which aims for carbon neutrality by 2050, has mandated stricter energy performance standards for buildings, pushing organizations to adopt energy-efficient facility management practices. Facility management providers are increasingly integrating smart technologies like IoT-enabled sensors and energy management systems to optimize resource utilization. Furthermore, a survey by a leading sustainability consultancy revealed that facilities adopting green practices reported an average reduction in energy costs within two years.

Rising Adoption of Outsourcing and Integrated Facility Management Services

Another major driver of the Europe facility management market is the increasing trend of outsourcing non-core functions to specialized service providers, enabling businesses to focus on their primary operations. This shift is particularly prominent among small and medium enterprises (SMEs), which lack the internal expertise to manage complex facility operations. Integrated facility management (IFM) solutions, which combine multiple services such as cleaning, security, and maintenance under a single provider, have gained traction due to their ability to enhance operational efficiency.

Top of Form

MARKET RESTRAINTS

High Initial Investment and Cost Sensitivity Among SMEs

One of the primary restraints impacting the Europe facility management market is the high initial investment required for advanced technologies and infrastructure upgrades, which often deters smaller businesses from adopting comprehensive facility management solutions. Technologies such as IoT-enabled systems, building automation platforms, and predictive maintenance tools require significant upfront capital, making them less accessible to small and medium enterprises (SMEs). This financial burden is further exacerbated by economic uncertainties, such as inflationary pressures and fluctuating energy prices, which have tightened budgets for many organizations. These factors collectively highlight how cost sensitivity and budget constraints among SMEs act as a significant restraint, limiting the broader adoption of advanced facility management solutions across Europe.

Fragmented Market Structure and Lack of Standardization

Another critical restraint in the Europe facility management market is its highly fragmented nature, characterized by the presence of numerous local and regional players offering diverse services with varying quality standards. This fragmentation creates challenges in achieving consistency and scalability, particularly for multinational corporations seeking uniform facility management solutions across multiple locations. The lack of standardization in service delivery further complicates matters, as clients often face difficulties in comparing offerings and ensuring compliance with regulatory requirements. These structural challenges impede market consolidation and hinder the seamless integration of facility management services, posing a significant obstacle to industry growth.

Top of Form

MARKET OPPORTUNITIES

Expansion of Smart City Initiatives and Urbanization Trends

The proliferation of smart city projects across Europe presents a significant growth opportunity for the facility management market, as urbanization drives demand for advanced infrastructure and operational efficiency. These initiatives create a fertile ground for facility management providers to offer IoT-driven solutions such as real-time monitoring, energy optimization, and predictive maintenance. Furthermore, as per analysis, nearly €200 billion is projected to be invested in European smart city projects by 2025, creating opportunities for facility managers to partner with municipalities and private developers.

Growing Demand for Healthcare and Senior Living Facility Management

The aging population in Europe and the subsequent rise in healthcare infrastructure present another lucrative opportunity for the facility management market. This demographic shift necessitates specialized facility management services tailored to the unique needs of hospitals, clinics, and assisted living centers. A report by a healthcare advisory group highlighted that the European healthcare real estate market is projected to significantly grow annually, with facility management playing a critical role in ensuring compliance, hygiene, and operational efficiency.

Top of Form

MARKET CHALLENGES

Resistance to Digital Transformation and Skills Gap

A significant challenge facing the Europe facility management market is the resistance to digital transformation, compounded by a lack of skilled professionals capable of managing advanced technologies. While digital tools such as IoT, AI, and data analytics are becoming integral to modern facility management, many organizations remain hesitant to adopt these innovations due to perceived complexity and cultural inertia. This skills gap is exacerbated by an aging workforce, The combination of technological resistance and workforce limitations hinders the ability of facility management providers to deliver cutting-edge services, creating a barrier to innovation and competitiveness in the market.

Regulatory Complexity and Compliance Pressures

The European facility management market operates in a highly regulated environment, where compliance with diverse and evolving regulations poses a significant challenge for service providers. Different countries within the European Union have varying standards related to energy efficiency, waste management, health and safety, and labor laws, making it difficult for facility managers to ensure uniform adherence across multiple jurisdictions. For instance, the Energy Performance of Buildings Directive (EPBD) mandates stringent energy efficiency requirements, which necessitate continuous upgrades and monitoring. These regulatory complexities not only increase operational costs but also require constant adaptation, diverting resources away from innovation and strategic growth initiatives.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Mode of Delivery, End User Insights, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and Czech Republic |

| Market Leaders Profiled | CBRE Group, ISS A/S, Sodexo, Compass Group, Jones Lang LaSalle (JLL), Cushman & Wakefield, Atalian Servest, Mitie Group plc, Vinci Facilities, G4S plc |

SEGMENTAL ANALYSIS

By Mode of Delivery Insights

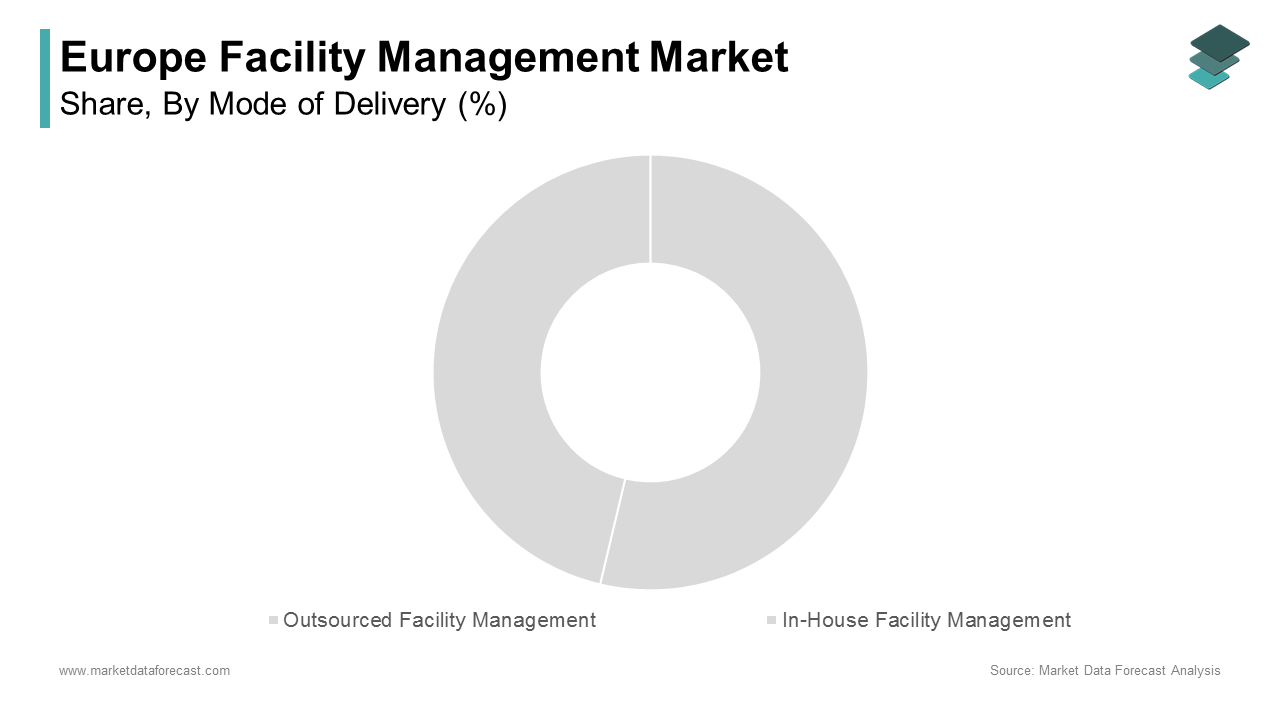

Outsourced facility management dominated the Europe facility management market by holding a market share of 65.2% in 2025. This segment's dominance is driven by the growing trend among businesses to delegate non-core functions to specialized service providers, enabling them to focus on strategic priorities. Also, outsourcing has become particularly prevalent in sectors such as healthcare, retail, and manufacturing, where operational efficiency and cost optimization are critical. Another key factor propelling this segment is the scalability and flexibility offered by third-party providers. According to insights from a trade association, companies utilizing outsourced services reported a reduction in operational inefficiencies within the first year of implementation. Apart from these, the rise of integrated facility management (IFM) solutions, which combine multiple services under one provider, has further bolstered the popularity of outsourcing.

In-house facility management is emerging as the fastest-growing segment in the Europe facility management market, with a CAGR of 8.5% projected through 2033. This rapid growth is primarily fueled by the increasing emphasis on data security and proprietary control over sensitive operations. As per a report by a cybersecurity think tank, 40% of European organizations have cited concerns about data breaches and intellectual property risks as reasons for retaining facility management functions in-house. Another driving factor is the rise of hybrid working models post-pandemic, which has led companies to invest in internal teams capable of managing dynamic workplace environments. Furthermore, advancements in technology have made it easier for organizations to manage facilities internally.

By End User Insights

Commercial buildings represented the largest end-user segment in the Europe facility management market accounting for 35.1% of the total market share in 2025. This control over the market is primarily driven by the growing demand for sustainable and energy-efficient building operations, which align with stringent European Union regulations such as the Energy Performance of Buildings Directive (EPBD). According to a report by an environmental policy think tank, commercial buildings are responsible for nearly 25% of Europe’s total energy consumption, making them a focal point for energy optimization initiatives. Facility management providers are increasingly integrating IoT-enabled systems and smart technologies to meet these demands, with a notable share of commercial properties in Europe now equipped with some form of smart building solution. Another critical factor propelling this segment is the rise of coworking spaces and flexible office environments, fueled by the post-pandemic shift toward hybrid work models.

The government and public entities segment is developing into the proliferating end-user category in the Europe facility management market, with a projected CAGR of 9.2% through 2033. This rapid expansion is driven by increased government spending on modernizing public facilities such as schools, hospitals, and administrative buildings to meet sustainability and efficiency targets. Another key factor accelerating this segment’s growth is the rising emphasis on outsourcing non-core functions to reduce operational costs and improve service quality. Furthermore, the integration of digital tools such as predictive maintenance and energy monitoring systems has enabled governments to optimize facility operations. For instance, it is observed that public entities implementing IoT-based facility management solutions achieved a reduction in energy usage within two years.

REGIONAL ANALYSIS

Germany was the largest contributor to the European facility management market and commanded a market share of 22.8% in 2025. This leading position is underpinned by the country’s robust industrial base, stringent environmental regulations, and strong emphasis on technological innovation. Germany’s commitment to the Energiewende (energy transition) policy has also accelerated the adoption of energy-efficient facility management solutions, with a notable share of large enterprises investing in IoT-enabled systems to optimize resource usage. Another critical factor bolstering Germany’s dominance is its highly organized outsourcing ecosystem. Additionally, the presence of global leaders in facility management, such as ISS Facility Services and G4S, has further strengthened the market’s maturity.

The United Kingdom is a hub for innovation and outsourcing in facility management. The country’s prominence is attributed to its advanced adoption of outsourcing models and its leadership in smart building technologies. London, in particular, serves as a hotspot for innovation, with a considerable share of commercial properties in the city equipped with smart building solutions. The UK’s focus on sustainability also plays a pivotal role in shaping the market. According to a study by a sustainability consultancy, the UK government has mandated all new public buildings to achieve net-zero carbon emissions by 2030, creating significant opportunities for facility management providers. These factors highlight how the UK’s innovative landscape and regulatory push are driving its leadership in the European market.

France’s prowess is rooted in its proactive approach to sustainability and energy efficiency, driven by ambitious national targets such as achieving carbon neutrality by 2050. Another key driver of France’s market growth is its thriving commercial real estate sector. Additionally, as per data from a workforce development organization, the demand for skilled facility management professionals in France grew annually between 2020 and 2022, reflecting the increasing complexity of service requirements. These factors collectively underscore how France’s commitment to sustainability and its dynamic real estate landscape contribute to its strong market position.

Italy is a progressing player with a focus on modernization. The country’s market growth is fueled by extensive investments in modernizing aging infrastructure and adopting digital solutions. The rise of smart technologies is another significant factor propelling Italy’s market. Like, Italian businesses adopting IoT-based facility management solutions reported a improvement in operational efficiency within two years. These trends highlight how Italy’s focus on infrastructure modernization and technological adoption is elevating its standing in the European facility management landscape.

Spain is largely driven by rapid urbanization and its booming tourism industry, which necessitates efficient facility management solutions. Additionally, Spain’s commitment to sustainability is reshaping the market landscape. According to a study by an environmental policy think tank, the Spanish government has introduced tax incentives for businesses adopting energy-efficient practices, encouraging the integration of smart technologies in facility management. These factors illustrate how Spain’s urbanization trends and sustainability initiatives are propelling its growth in the European facility management market.

LEADING PLAYERS IN THE EUROPEAN FOOD ENZYME MARKET

ISS Facility Services

ISS Facility Services is a global leader in the Europe facility management market, renowned for its comprehensive service offerings and innovative solutions. Headquartered in Denmark, the company plays a pivotal role in shaping the industry through its focus on sustainability and digital transformation. ISS has developed proprietary IoT-enabled platforms to optimize energy usage and enhance operational efficiency, aligning with Europe’s stringent environmental regulations. Its commitment to social responsibility is evident in initiatives like "Responsible Business," which emphasizes workforce diversity and environmental stewardship. By integrating advanced technologies and maintaining a client-centric approach, ISS continues to set benchmarks in service quality.

Sodexo

Sodexo, a France-based multinational, is another dominant player in the Europe facility management market, known for its integrated solutions that combine facility management with food services and employee well-being programs. The company serves over 100 million consumers daily across diverse sectors, including healthcare, education, and defense. As per insights from a business consultancy, Sodexo has invested heavily in predictive maintenance tools and AI-driven analytics to improve service delivery. Its "Better Tomorrow 2025" strategy underscores its dedication to sustainability, aiming to reduce carbon emissions across its operations. Sodexo’s emphasis on innovation and holistic service models strengthens its position as a key contributor to the global facility management landscape.

G4S

G4S, headquartered in the UK, is a leading provider of security-focused facility management services, with a strong presence across Europe. The company leverages cutting-edge technology, such as AI-powered surveillance systems and data analytics, to deliver tailored solutions for industries like retail, manufacturing, and government. With operations spanning over 80 countries, G4S contributes significantly to the global market by addressing complex security challenges while ensuring seamless facility operations. Its strategic acquisitions and partnerships further solidify its leadership in delivering secure and sustainable facility management solutions.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Emphasis on Digital Transformation and Smart Technologies

Key players in the Europe facility management market are increasingly investing in digital transformation to enhance service delivery and operational efficiency. Companies like ISS Facility Services and Sodexo are leveraging IoT, AI, and data analytics to offer predictive maintenance, energy optimization, and real-time monitoring solutions. These innovations not only improve client satisfaction but also align with Europe’s stringent sustainability goals, such as the EU Green Deal. By adopting digital tools, companies can reduce energy consumption, creating a competitive edge. This strategy enables firms to cater to the growing demand for tech-driven solutions while improving profitability through streamlined operations.

Strategic Partnerships and Collaborations

Strategic partnerships and collaborations have emerged as a critical growth strategy for key players in the Europe facility management market. Companies are teaming up with technology providers, real estate developers, and government entities to expand their service offerings and geographic reach. For instance, G4S has collaborated with cybersecurity firms to enhance its security-focused facility management services, ensuring compliance with data protection regulations. Additionally, partnerships allow companies to access cutting-edge technologies and tap into new customer segments, such as smart city projects. These collaborations strengthen market positioning by fostering innovation and scalability.

Focus on Sustainability and ESG Initiatives

Sustainability has become a cornerstone strategy for key players aiming to strengthen their foothold in the Europe facility management market. Companies are aligning their operations with environmental, social, and governance (ESG) goals to meet regulatory requirements and consumer expectations. For example, Sodexo’s "Better Tomorrow 2025" initiative focuses on reducing carbon footprints and promoting workforce diversity, resonating with Europe’s commitment to carbon neutrality by 2050. By embedding sustainability into their core strategies, these players not only comply with regional mandates but also differentiate themselves in a competitive market, attracting environmentally conscious clients and enhancing brand reputation.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players in the Europe facility management market include CBRE Group, ISS A/S, Sodexo, Compass Group, Jones Lang LaSalle (JLL), Cushman & Wakefield, Atalian Servest, Mitie Group plc, Vinci Facilities, and G4S plc.

The European facility management market is characterized by intense competition, driven by the presence of global leaders and regional players striving to gain a competitive edge. The market is highly fragmented, with companies adopting diverse strategies such as technological innovation, sustainability initiatives, and strategic partnerships to differentiate themselves. According to a report by a leading consultancy firm, the top five players collectively account for approximately 40% of the market share, leaving significant room for smaller firms to compete on niche services. The increasing demand for integrated facility management solutions has intensified rivalry, with providers focusing on delivering end-to-end services tailored to client needs. Additionally, the growing emphasis on sustainability and smart technologies has pushed companies to invest heavily in digital transformation. As per insights from a trade association, nearly 70% of key players have adopted IoT-enabled systems to optimize operations. Regulatory pressures, particularly in energy efficiency and environmental compliance, further shape the competitive landscape, compelling firms to innovate while maintaining cost efficiency. This dynamic environment fosters both collaboration and competition, as companies strive to balance customization, scalability, and technological advancements.

RECENT HAPPENINGS IN THE MARKET

- In March 2023, ISS Facility Services partnered with Microsoft to integrate AI-driven analytics into its facility management platforms, enhancing predictive maintenance capabilities across Europe.

- In June 2023, Sodexo launched its "Green Buildings Initiative," investing €500 million to retrofit existing facilities with energy-efficient technologies, aligning with EU sustainability goals.

- In August 2023, G4S acquired a Netherlands-based cybersecurity firm to bolster its security-focused facility management services, ensuring compliance with GDPR and other data protection regulations.

- In November 2023, Compass Group expanded its presence in Scandinavia by acquiring a local facility management provider, strengthening its footprint in the Nordic region.

- In January 2024, Bouygues Energies collaborated with Siemens to develop smart building solutions for European commercial properties, targeting a 30% reduction in energy consumption by 2025.

DETAILED SEGMENTATION OF EUROPE FACILITY MANAGEMENT MARKET INCLUDED IN THIS REPORT

This research report on the Europe facility management market has been segmented and sub-segmented based on the mode of delivery, end-user & region.

By Mode of Delivery Insights

- Outsourced Facility Management

- In-House Facility Management

By End User Insights

- Commercial

- Industrial

- Government & Public Sector

- Healthcare

- Education

- Residential

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving growth in the European facility management market?

Key drivers include the rising demand for energy efficiency, growing outsourcing trends, smart building technologies, and increasing focus on sustainability and compliance.

2. Who are the key players in the European facility management market?

Major players include CBRE Group, ISS A/S, Sodexo, Compass Group, JLL, Cushman & Wakefield, Mitie Group, and Atalian Servest.

3. How is technology influencing facility management in Europe?

The adoption of IoT, AI, and data analytics is transforming facility management through smart maintenance, predictive analytics, and automation of routine tasks.

4. Which countries lead the facility management market in Europe?

The United Kingdom, Germany, and France are among the leading countries in terms of market share and service adoption.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com