Europe Feed Fats And Proteins Market Size, Share, Trends & Growth Forecast Report, Segmented By Source, Livestock, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of EU), Industry Analysis Forecast From (2026 to 2034)

Europe Feed Fats & Proteins Market Size

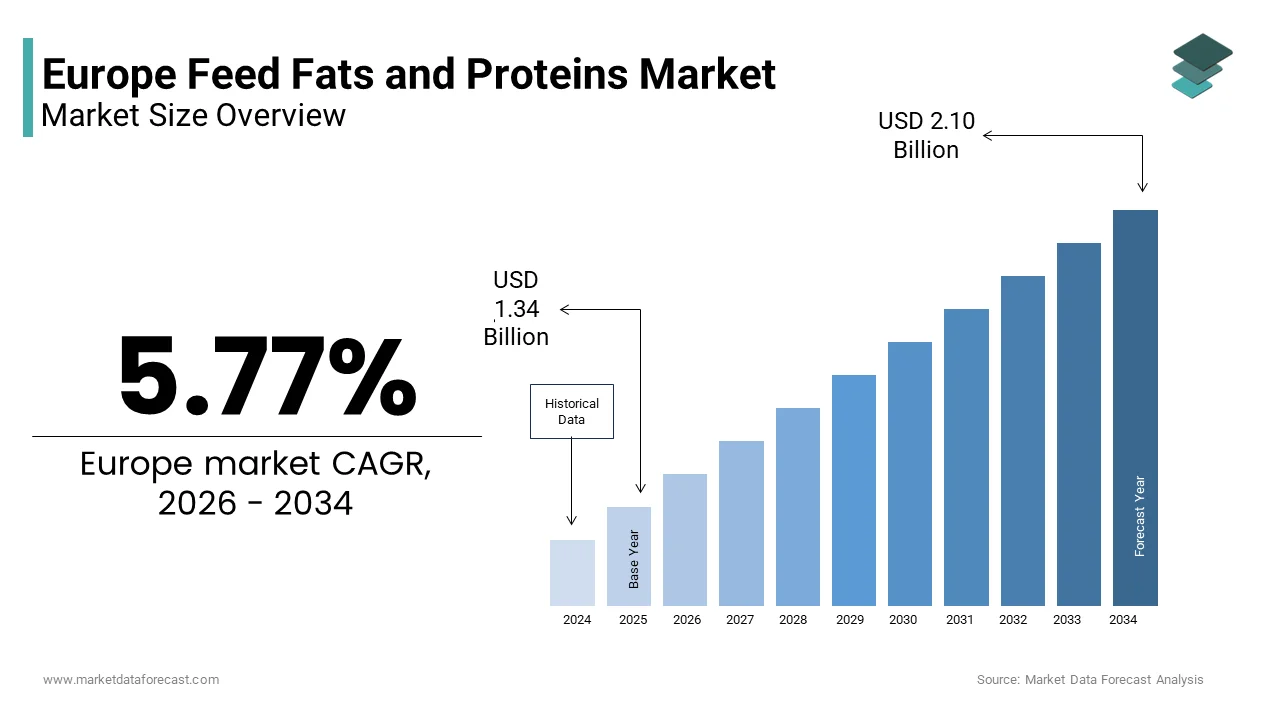

The Europe Feed Fats & Proteins market was valued at USD 1.27 billion in 2025 and is anticipated to reach USD 1.34 billion in 2026 and USD 1.99 billion by 2033, growing at a CAGR of 5.77% during the forecast period from 2026 to 2034.

Current Introduction of the Europe Feed Fats & Proteins Market Report

Feed fats and proteins refer to the essential macronutrients added to animal diets to support growth, energy, and overall health. These components are vital in the livestock industry for maximizing the productivity of animals like cattle, poultry, and fish. Fats, derived from vegetable oils, animal tallow, or recycled food waste, deliver up to 2.25 times the metabolizable energy of carbohydrates, while proteins, sourced from soybean meal, rapeseed cake, fishmeal, and emerging alternatives like insect meal, supply lysine, methionine, and other indispensable amino acids. The European feed industry’s reliance on these ingredients is shaped by stringent regulations on antibiotic use, sustainability mandates under the Green Deal, and the region’s high animal welfare standards. According to European feed industry estimates, total industrial compound feed production in the European Union continued to decline in 2023, driven largely by contraction in the pig sector, despite some recovery in poultry feed production. The European Commission’s Protein Crop Strategy aims to reduce soy dependency by expanding domestic legume cultivation, while the revised Renewable Energy Directive restricts the use of food crop-based fats in biofuels, redirecting supply toward feed applications. These policy currents, combined with evolving nutritional science, define the strategic importance of feed fats and proteins in Europe’s food security and circular agriculture agenda.

MARKET DRIVERS

Phasing Out of Antibiotic Growth Promoters Elevates Nutritional Precision Demand

The European Union’s comprehensive ban on antibiotic growth promoters since 2006 has fundamentally reshaped livestock nutrition, and thereby propelled the expansion of the Europe feed fats & proteins market. This shift has driven demand for high-quality fats and proteins that support gut health and immune resilience without pharmacological intervention. European veterinary antimicrobial sales for food-producing animals have dropped significantly, prompting increased adoption of alternative nutritional strategies to maintain performance. Feed fats rich in medium-chain fatty acids, such as those from palm kernel and coconut oil, demonstrate antimicrobial properties that suppress pathogenic bacteria like Salmonella and Clostridium perfringens. Research indicates that supplementing broiler diets with protected medium-chain triglycerides can enhance intestinal health and boost feed conversion efficiency. Similarly, high digestibility proteins like enzymatically hydrolyzed soy or fermented rapeseed meal enhance amino acid absorption while lowering nitrogen excretion. As per studies, implementing optimized fat and protein diets in piglet production effectively reduces post-weaning diarrhea, which aligns with and directly supports animal welfare standards. Precision fat and protein feed strategies are now indispensable for sustainable intensification, directly supporting the EU Farm to Fork Strategy's goal of reducing antimicrobial use.

Rising Intensification of European Livestock and Aquaculture Systems

The structural consolidation of the region’s livestock and aquaculture sectors has amplified demand for energy-dense and amino acid-balanced feed ingredients, which in turn contributed to the growth of the Europe feed fats & proteins market. These ingredients are essential to sustain high productivity under space and emission constraints. Dairy operations in the Netherlands and Denmark are consolidating, resulting in fewer, larger herds, while poultry facilities in Poland and Spain are increasingly adopting high-capacity, industrialized production methods. These intensified systems require rations with elevated metabolizable energy and ideal protein profiles to maximize output per animal. European aquaculture, led by Mediterranean finfish production, is focusing on adopting sustainable fishmeal replacements for carnivorous species, such as sea bass and trout, that ensure the retention of essential fatty acids. Feed fats from algal oil and proteins from single-cell sources now offer viable alternatives. Dairy farms, particularly those aiming for high productivity, are increasingly utilizing bypass fats to boost energy intake, resulting in higher daily milk production per cow during peak lactation. This performance imperative, coupled with environmental regulations like the EU’s National Emission Ceilings Directive that penalize excess nitrogen, compels producers to adopt scientifically formulated fat and protein matrices that align productivity with compliance.

MARKET RESTRAINTS

Heavy Reliance on Imported Protein Meals Creates Supply Chain Vulnerability

The region’s feed industry remains greatly dependent on imported soybean meal, primarily from Brazil and the United States, which ultimately restricts the expansion of the Europe feed fats & proteins market. This dependency exposes the industry to geopolitical disruptions and price volatility. According to the European Feed Manufacturers Federation, the European Union remains heavily reliant on external, mostly South American, sources for high-protein feed, with soybean meal dominating the total volume of imported protein materials. This dependency contradicts the European Commission’s Farm to Fork objective of increasing self-sufficiency in plant protein production. The convergence of the global fertilizer crisis and drought-related production losses in South America triggered substantial price spikes for soybean meal, causing increased costs for European livestock producers, notes reports tracking global commodity prices. Eurostat data shows that despite EU efforts to increase domestic legume cultivation for reduced import dependency, crops like faba beans and peas remain a marginal part of the overall agricultural landscape. Furthermore, alternative proteins like insect meal remain constrained by scale. The European Insect Protein Association confirms that while insect farming expands, output remains too low to meaningfully replace soybean meal in EU animal feed. European feed producers face ongoing price and supply volatility, undermining formulation stability, until import substitution gains momentum.

Stringent Regulations on Animal By-Product Use Limit Fat Sourcing Options

The European Union’s Regulation EC No 1069/2009 maintains rigorous controls on animal by-products that hinder the growth of the Europe feed fats & proteins market. Consequently, the use of rendered fats from Category 3 materials, including restaurant waste and fish processing residues, is significantly restricted in livestock feed. While these rules ensure food safety and prevent disease transmission, they reduce the availability of cost-effective, circular fat sources. According to research, a significant portion of Europe's high-quality rendered animal fats is increasingly being diverted away from feed and industrial uses to satisfy the growing demand for biodiesel, a trend driven by EU transport fuel policies. This is due to regulatory barriers, despite their high energy value and fatty acid profiles suitable for monogastric species. The Renewable Energy Directive’s phase out of food and feed competing feedstocks for biofuels was intended to redirect these streams to feed, but cross-contamination risks and documentation burdens deter compounders. Only a small minority of Dutch feed producers utilize rendered animal fats due to stringent traceability audits and restrictions imposed by retailers, highlighting a trend where market requirements outweigh the technical availability of these materials. This regulatory caution, while justified from a public health standpoint, curtails the circular economy potential of the feed fat sector and inflates reliance on virgin vegetable oils, which face their own sustainability scrutiny under EU deforestation regulations.

MARKET OPPORTUNITIES

Expansion of Insect and Single-Cell Protein Production Under Circular Economy Mandates

The European Union is pushing toward circular bioeconomy models, which provide new opportunities for the Europe feed fats & proteins market. This initiative is enabling investment in novel protein sources that convert organic waste into high-quality feed ingredients. Insect farming, using black soldier fly and mealworm larvae fed on pre-consumer food waste, is gaining regulatory and commercial traction. The European Commission expanded the use of insect protein in livestock feed, specifically for pigs and poultry, to advance sustainable circular food systems. Major European insect protein manufacturers are producing high-grade insect meal that provides a significant protein content, competing with traditional sources. The European insect production sector has experienced rapid, multi-fold growth in installed production capacity, expanding from a niche market into a large-scale industrial sector in a few years. Similarly, single-cell proteins from microbial fermentation of methane or ethanol, such as those by Unibio in Denmark and Solar Foods in Finland, offer landless protein alternatives. Projections indicate that the adoption of novel, locally produced proteins will drastically reduce the European Union's dependency on imported soy for animal feed within the coming years. The EU's Green Procurement criteria validating insect meal as sustainable opens up this burgeoning sector as a key to localized and resilient protein.

Integration of Precision Nutrition and Digital Feed Formulation Platforms

Digital transformation in the regional agriculture is enabling hyper-targeted inclusion of fats and proteins based on real-time animal performance and environmental data. This integration is expected to fuel the growth of the Europe feed fats & proteins market. Advanced feed formulation software now integrates with farm management systems to adjust nutrient profiles dynamically in response to lactation stage, ambient temperature, or disease challenge. A substantial proportion of intensive dairy and pig farming operations across major Northern European agricultural producers (Germany, the Netherlands, Denmark) have adopted algorithmic, digital, and precision-driven nutritional balancing. These platforms optimize the use of specialty fats like calcium soaps of palm fatty acids and protected amino acids such as methionine hydroxy analogs to minimize waste and maximize efficiency. Wageningen University research indicates that employing precision fat-protein balancing in dairy cattle significantly lowers nitrogen excretion rates while concurrently decreasing enteric methane emissions per liter of milk produced. Furthermore, blockchain-enabled traceability, piloted by Cargill and Agrifirm, allows integrators to verify the sustainability credentials of fat and protein sources, which meet retailer sustainability demands. This data-driven approach transforms fats and proteins from bulk commodities into precision tools for performance and environmental stewardship.

MARKET CHALLENGES

Price Volatility of Vegetable Oils Linked to Biofuel and Food Competition

Feed fats in the region face persistent price instability, which slows down the expansion of the Europe feed fats & proteins market. This is due to competing demands from the food and bioenergy sectors, particularly for palm rapeseed and sunflower oils. The European Renewable Energy Directive’s mandates for renewable transport fuels have historically diverted significant oilseed crushing output toward biodiesel, tightening feed fat availability. Rapeseed oil prices have shown significant fluctuation, influenced by evolving biofuel mandates and interruptions in supply associated with international conflicts. Policy adjustments intended to reduce biofuels derived from food crops have been made, yet existing agreements and infrastructure perpetuate inter-sector competition. A considerable amount of domestic rapeseed oil output is regularly directed towards energy applications, which impacts its availability for alternative uses. This volatility forces compounders to frequently reformulate ratios, often substituting with less optimal or more expensive alternatives like fish oil or synthetic amino acids. European feed producers remain exposed to destabilizing economic and geopolitical shocks due to the lack of a long-term policy separating food-feed-fuel streams.

Limited Availability of Sustainable Marine Oils Constrains Aquaculture Feed Innovation

The region’s growing aquaculture sector faces acute constraints in sourcing marine-derived fats rich in omega-3 fatty acids, which inhibits the growth of the Europe feed fats & proteins market. Meanwhile, wild fish stocks used for fish oil production remain under severe pressure. Global production levels for fish oil have reached a consistent ceiling. A specific portion of this supply is designated for the European aquaculture industry. Permissible catch limits for certain fish species used as raw materials for oil production have been reduced following observations suggesting current stock levels are harvested beyond sustainable parameters. This creates a potential constraint on the regional supply of fish oil available for feed manufacturing. This scarcity drives prices upward. The European Market Observatory for Fisheries and Aquaculture Products observed a significant spike in the cost of imported fish oil during the period spanning two years ago. Algal and genetically modified camelina oils show potential, but scaled-up commercial use is limited. Europe's salmon farming industry faces significant challenges in sourcing sufficient omega-3s sustainably, leading the Scottish Aquaculture Innovation Centre (SAIC) and other groups to develop algal-based solutions to reduce reliance on finite marine resources, though meeting total European demand remains a complex, ongoing innovation effort. Hence, Europe’s aquaculture expansion is limited by fat availability until sustainable marine oil alternatives become affordable and plentiful, which directly affects feed quality and environmental impact.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.77% |

| Segments Covered | By Source, Livestock, And By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, & Rest of Europe |

| Market Leaders Profiled | Eurofins Scientific SE (Luxembourg), Agilent Technologies Inc. (U.S.), Thermo Fisher Scientific Inc. (U.S.), LGS Limited. (U.K.), Illumina Inc. (U.S.), ZZoetisInc. (U.S.), Neogen Corporation (U.S.), Galseq Srl Via Italia (Italy), AgAgrigenomicsnc. (U.S.), Biogenetic Services Inc. (U.S.) |

SEGMENTAL ANALYSIS

By Source Insights

The tallow and soybean segment held the largest share of 42.1% of the Europe Feed Fats & Proteins Market in 2024. The dominance of the tallow and soybean segment is driven by the complementary nutritional profiles and established supply chains of both ingredients. Soybean meal remains the primary protein source in European livestock rations due to its high lysine content and digestibility, despite import dependency. The European Union relies heavily on imported soy products to satisfy the high demand from its livestock sectors, with Brazil and South America serving as the dominant suppliers to meet these nutritional needs. Simultaneously, rendered animal fat, known as tallow, serves as a cost-efficient, high-energy ingredient in livestock nutrition, offering significant metabolic energy to support animal growth. The integration of these two ingredients allows compounders to balance amino acid profiles while delivering concentrated energy, particularly in high-performance ratios. Regulatory clarity under EU feed legislation also supports their use. Both are listed in the Catalogue of Feed Materials with well-defined specifications, ensuring consistent quality and traceability across member states.

The poultry meal segment is predicted to witness the highest CAGR of 8.7% from 2025 to 2033 due to tightening regulations on meat and bone meal and the rise of integrated poultry production that generates consistent byproduct streams. Following the BSE crisis, the European Union implemented strict regulations against using animal-derived proteins in ruminant feed, though recent regulations have eased restrictions to allow the use of poultry-derived proteins in non-ruminant feed. This regulatory distinction has enabled poultry integrators to recycle processing residues into high-protein meals containing a notable percentage of crude protein. Large-scale poultry processors in France, particularly in the western regions, are actively recovering poultry meal to improve sustainability and lower waste disposal expenses. Furthermore, poultry meal’s low ash content and high phosphorus bioavailability make it superior to some plant proteins in swine and aquaculture formulations. Following the regulatory change permitting processed animal proteins, poultry meal inclusion in piglet starter feeds in the Netherlands has seen an upward trend. Poultry meal is gaining traction as a sustainable, localized protein source, reducing reliance on imports due to better circular economy practices and improved rendering technology.

By Livestock Insights

The poultry segment led the Europe Feed Fats & Proteins Market in 2024. The leading position of the poultry segment is attributed to Europe’s massive broiler and layer production, which supplies millions of metric tons of poultry meat annually. Poultry’s rapid growth cycle and high feed conversion efficiency necessitate energy-dense and amino acid-balanced rations, driving consistent demand for soybean meal, tallow, and specialty fats like protected lipids. The European Commission’s Poultry Meat Strategy emphasizes productivity under antibiotic-free conditions, prompting nutritionists to optimize fat-protein matrices for gut health and immune support. Poland, leading the European Union in poultry production, maintains high annual compound feed consumption for its intensive farming operations. Also, poultry feed formulations in Poland incorporate consistent percentages of fats and proteins to ensure optimal nutrition. Additionally, rising consumer demand for white meat as a lean protein source has expanded production in Spain, France, and the Netherlands. New European Food Safety Authority guidance regarding mycotoxin risks has prompted the industry to adopt stricter safety measures to protect animal health. The updated safety assessments have driven an increased use of specialized binders, adsorbent-coated components, and broken-down protein sources in feed to mitigate contaminants. This confluence of scale, nutritional precision, and market demand solidifies poultry as the primary driver of feed fat and protein utilization in Europe.

The aquaculture segment is estimated to register the fastest CAGR of 9.3% during the forecast period, owing to the EU’s strategic push to enhance seafood self-sufficiency and reduce pressure on wild fish stocks. Europe produced significant metric tons of farmed fish, with salmon,n sea bass, ss and trout dominating high-value output. These carnivorous species require rations rich in omega-3 fatty acids and highly digestible proteins, traditionally sourced from fishmeal and fish oil. However, supply constraints have accelerated the adoption of alternative fats like algal oil and proteins from insect meal and microbial biomass. Research indicates that a significant portion of marine-based ingredients in salmon feed can be replaced with alternatives while maintaining fish growth and fillet quality. The influence of Nordic aquaculture standards on European regulations is driving interest in specialized lipids designed to replicate natural marine fat profiles. European funding initiatives are actively supporting the development of innovative, sustainable feed sources, including the establishment of pilot facilities for insect-based protein production. The shift toward intensive, controlled aquatic farming is accelerating, ensuring that aquaculture remains at the forefront of feed technology and adoption beyond traditional livestock.

COUNTRY ANALYSIS

Germany Feed Fats & Proteins Market Analysis

Germany dominated the Europe Feed Fats & Proteins Market by capturing a share of 19.4% in 2024. The supremacy of the German market is propelled by Europe’s largest livestock population, advanced rendering infrastructure, and a stringent feed safety culture. The German agricultural sector supports a large livestock population, requiring a substantial volume of compound feed for production needs. Significant quantities of compound feed are utilized annually within the country to sustain the broiler and pig populations. Tallow production in the country is a robust industry that provides a consistent supply of fats. This produced tallow is utilized to supply both internal demand and international markets. The tallow produced for feed fats is recognized for its quality. German compounders adhere to DIN and GMP+ standards that exceed EU minimums, ensuring traceability from slaughterhouse to feed mill. The German Society for Animal Nutrition regularly updates nutrient requirement tables, guiding precise fat and protein inclusion. Additionally, Germany is a pioneer in circular feed systems. This blend of scale, regulation, and sustainability infrastructure makes Germany the benchmark for feed ingredient quality and innovation in Europe.

France Feed Fats & Proteins Market Analysis

France was the second-largest in the Europe Feed Fats & Proteins Market by accounting for a 16.8% share in 2024. The growth of the French market is driven by its vertically integrated poultry sector—particularly in regions like Brittany, which produces 60 percent of national output—and its extensive network of rendering plants. France's rendering industry acts as a major, high-volume circular bioeconomy driver, processing substantial amounts of animal by-products into tallow and meat meals annually. The sector contributes significantly to sustainability by transforming, in large part, chicken-based materials into high-value processed proteins and fats for pet food and agricultural feed, consistently managing a significant share of the national slaughterhouse output. Soybean meal imports, primarily from South America, complement domestic rapeseed cake to meet protein needs across swine and poultry operations. The French Ministry of Agriculture’s Ecophyto Plan encourages reduced antibiotic use, driving adoption of medium-chain fatty acid-enriched fats and fermented proteins for gut health. Furthermore, France’s leadership in the EU Protein Plan has spurred trials on faba bean and lupin inclusion, though soy remains dominant. The convergence of large-scale production, circular waste valorization, and policy-driven nutritional innovation establishes France as a resilient and adaptive feed ingredient market.

Spain Feed Fats & Proteins Market Analysis

Spain is another key player in the Europe Feed Fats & Proteins Market due to the rapid intensification of poultry and swine production in response to rising meat exports and domestic consumption. Spain is now the EU’s second-largest pork producer and third-largest poultry producer, with compound feed output of millions of metric tons. Arid conditions in key regions like Catalonia and Castilla y León necessitate energy-dense rations to offset heat stress induced feed intake decline. The use of tallow in warm-weather product formulations has shown a notable upward trend in recent years. Spain represents a major market for aquaculture feed, with a high volume of farmed sea bass and bream production. Research indicates that blended vegetable and marine oils designed as structured lipids can improve growth outcomes in juvenile fish during varying salinity conditions. Spain's market expansion is exceeding the EU average, supported by a high export orientation and climate-adaptive feeding practices.

Netherlands Feed Fats & Proteins Market Analysis

The Netherlands grew steadily in the Europe Feed Fats & Proteins Market. Despite its modest land area, the country is Europe’s largest agricultural exporter by value, driven by ultra-efficient dairy, pig, and poultry systems that demand high precision feed formulations. Dutch compounders utilize real-time nutrient balancing software that adjusts fat and protein inclusion based on lactation stage or ambient temperature. The Netherlands imports a substantial volume of soybean meal to meet its agricultural demands, yet it mitigates this reliance by utilizing advanced rendering processes. Rendering operations contribute to the local supply chain by producing significant quantities of tallow and poultry meal. Governmental strategies in the region emphasize circularity, resulting in a high percentage of food processing waste being repurposed into feed ingredients. Additionally, Dutch feed mills supply neighboring Germany and Belgium, making the country a critical logistics node. This combination of technological sophistication, circular infrastructure, and export orientation ensures the Netherlands remains a high-value, high-influence player in the European feed ingredient landscape.

Poland Feed Fats & Proteins Market Analysis

Poland is likely to expand in the Europe Feed Fats & Proteins Market from 2025 to 2033, owing to massive growth in poultry and swine production, supported by EU structural funds and competitive labor costs. Poland has become a major producer of poultry within the EU and holds a notable position in pig production. This scale of livestock output requires a substantial amount of compound feed. The country's feed production depends on both imported protein sources and domestic animal fats. The production of domestic tallow has risen with the growth of local slaughter capacity. Poland also benefits from proximity to Ukrainian corn and sunflower meal, offering alternative protein and fat sources amid global volatility. Poland is emerging as a crucial growth channel for feed fats and proteins in Central and Eastern Europe, propelled by investments in automated feed mill technology and expanding Middle Eastern and Baltic markets.

COMPETITIVE LANDSCAPE

Competition in the Europe Feed Fats & Proteins Market is shaped by a mix of multinational agribusinesses,s regional compounds, rs and specialized ingredient suppliers. Large players leverage global supply chains and R and D capabilities to offer integrated solutions,ons while smaller firms differentiate through niche products like protected fats or hydrolyzed proteins. The market is highly regulated with strict requirements on traceability, safety,y and sustainability, ty which raise entry barriers and favor established participants. Price volatility in vegetable oils and imported meals intensifies cost competition yet creates opportunities for innovators in alternative ingredients. Geographical clusters in the Netherlands,nds Germany, and France serve as hubs for feed technology and circular economy initiatives. Competition increasingly centers on nutritional efficacy,y environmental impact,ct and digital service integration rather than commodity pricing alone. As the EU advances its Green Deal and Farm to Fork objectives,ves companies that align feed solutions with emission reduction and protein autonomy goals ga ain strategic advantage in this evolving landscape.

KEY MARKET PLAYERS

Some of the major companies dominating the market, by their products and services, include

- Archer Daniels Midland Company (ADM)

- Cargill Incorporated

- Glanbia Nutritionals

- ADM Animal Nutrition

- The Scoular Company, Darling International Inc.

- Roquette Freres

- Omega Protein Corporation

- Aarhuskarlshamn AB (AAK)

- Euroduna Rohstoffe GmbH

- Bunge Ltd.

- Agrana Beteiligungs-AG (Agrana)

- Lansing Trade Group LLC.

Top Players In The Market

- Cargill Incorporated maintains a strong presence in the Europe Feed Fats & Proteins Market through its integrated supply chain spanning oilseed crushing, rendering, and compound feed manufacturing. The company supplies specialty fats such as calcium soaps and protected amino acids alongside soybean and rapeseed meals to livestock and aquaculture producers across Western and Central Europe. It also expanded its circular sourcing initiative by partnering with food processors to convert Category 3 animal byproducts into certified feed fats. These actions reinforce Cargill’s role as a global nutrition solutions provider while enhancing its sustainability credentials in the European market.

- ADM Animal Nutrition operates extensively in Europe, offering a diversified portfolio of feed fats, proteins,s and value-added amino acids tailored to poultry, swine, and aquaculture needs. The company leverages its global oilseed processing network to ensure a consistent supply of soybean and sunflower meals while investing in alternative proteins like fermented rapeseed and insect meal. It also collaborated with Wageningen University on a research program evaluating the impact of structured triglycerides on gut health in weaned piglets. These initiatives demonstrate ADM’s commitment to scientific innovation and localized nutritional solutions across European livestock systems.

- Glanbia Nutritionals is a key participant in the Europe Feed Fats & Proteins Market with a focus on high-digestibility protein ingredients derived from dairy co-products and plant sources. The company supplies functional proteins such as hydrolyzed whey and fermented pea concentrates that support gut development and immune function in young animals. It also strengthened traceability by implementing blockchain-enabled batch tracking across its Irish and German production sites. Glanbia addresses European demand for antibiotic-free and welfare-aligned feed by prioritizing digestibility, safety, and transparency, while simultaneously contributing to global feed standards.

Top Strategies Used By The Key Market Participants

Key players in the Europe Feed Fats & Proteins Market focus on vertical integration to secure raw material supply from oilseed crushers and rendering facilities. They invest in precision nutrition technologies, including digital formulation tools and real-time nutrient monitoring systems, to optimize feed efficiency. Companies actively develop alternative protein sources such as insect mea,l single-cell proteins, and fermented plant ingredients to reduce soy dependency. Strategic collaborations with research institutions and universities enable validation of novel fat and protein efficacy in gut health and immunity. Additionally, firms enhance sustainability credentials through circular sourcing certification and blockchain-based traceability to meet retailer and regulatory demands.

MARKET SEGMENTATION

This research report on the Europe feed fats & proteins market is segmented and sub-segmented into the following categories.

By Source

- Poultry Meal

- Meat & Bone Meal

- Tallow and Soybean

- Corn

- Cotton Seeds

By Livestock

- Poultry

- Ruminants

- Aqua

- Equine

- Swine

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe feed fats and proteins market?

The Europe feed fats and proteins market includes fat and protein-rich feed ingredients used in animal nutrition to improve energy density, growth performance, and feed efficiency for livestock, poultry, and aquaculture.

Why are fats and proteins important in animal feed?

Fats provide high energy, while proteins supply essential amino acids, both of which are critical for growth, reproduction, immune function, and production performance in animals.

What products are included in this market?

Key products include animal fats, vegetable oils, fish oils, protein meals (soybean, rapeseed, sunflower), and protein concentrates used in compound feeds and ration formulations.

What drives growth in the Europe feed fats and proteins market?

Growth is driven by rising animal protein consumption, intensification of livestock production, focus on feed efficiency, and demand for high-performance nutrition.

Which animals benefit most from feed fats and proteins?

Feed fats and proteins are widely used for poultry, swine, cattle (dairy and beef), sheep, goats, and aquaculture species to support growth and production goals.

How do fats improve animal diets?

Fats boost dietary energy, enhance palatability, aid in fat-soluble vitamin absorption, and reduce overall feed intake while maintaining growth.

How do proteins support animal performance?

Proteins supply essential amino acids necessary for muscle development, milk and egg production, immune response, and tissue repair.

What trends are shaping the Europe feed fats and proteins market?

Key trends include sustainable and alternative proteins, precision nutrition, feed additive integration, and optimized fat sources for energy efficiency.

Are alternative protein sources growing in Europe?

Yes. Demand is rising for insect proteins, algae, fermented proteins, and other novel sources to improve sustainability and reduce reliance on traditional protein meals.

How do regulations affect the market?

EU feed regulations govern ingredient safety, labeling, contaminant limits, and allowable inclusion levels to ensure animal health and food chain safety.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com