Europe Fintech Market Size, Share, Trends & Growth Forecast Report By Deployment Mode, Technology, Application, End-User, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Market Size, 2025

$98.10 BnMarket Estimate, 2026

$121.86 BnMarket Forecast, 2034

$690.86 BnCAGR, 2026–2034

24.22%Europe Fintech Market Report Summary

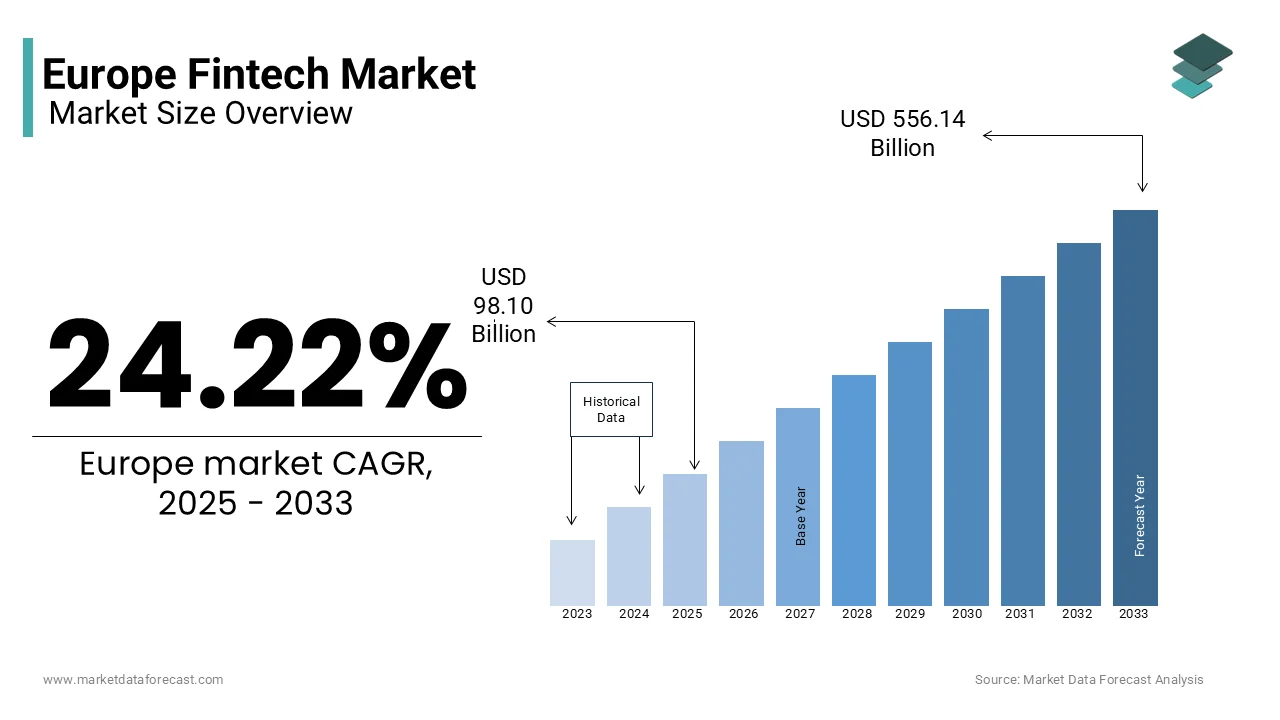

The Europe fintech market was valued at USD 98.10 billion in 2025, is estimated to reach USD 121.86 billion in 2026, and is projected to reach USD 690.86 billion by 2034, growing at a CAGR of 24.22% from 2026 to 2034. Market growth is driven by the rapid adoption of digital financial services, increasing smartphone and internet penetration, and rising investments in fintech innovation across Europe. Fintech solutions are transforming traditional financial services by enabling digital payments, online lending, wealth management, and banking services through advanced technology platforms. The expansion of open banking frameworks, increasing venture capital investments in fintech startups, and growing consumer preference for digital financial services are further accelerating market growth.

Key Market Trends

- Rapid growth of digital payment platforms and mobile financial services.

- Increasing adoption of open banking and API-based financial ecosystems.

- Rising investments in fintech startups and financial technology innovation.

- Growing demand for cloud-based financial infrastructure and scalable platforms.

- Expansion of neobanks and digital-only financial institutions.

Segmental Insights

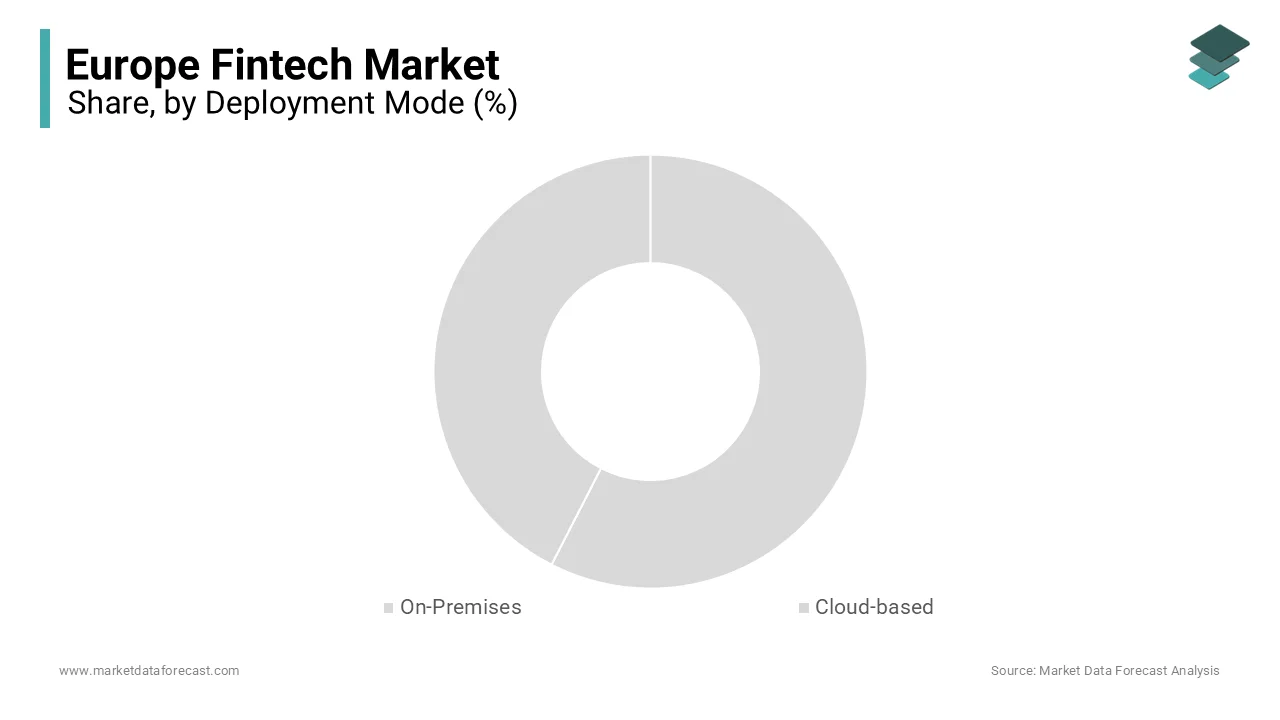

- Based on deployment mode, the cloud-based segment dominated the Europe fintech market in 2025, driven by the need for scalable, flexible, and cost-efficient infrastructure that supports agile fintech startups and digital banking platforms.

- Based on technology, the application programming interface (API) segment accounted for 32.3% share in 2025, supported by the widespread adoption of open banking frameworks and integration of financial services across multiple platforms.

- Based on end user, the banking segment held the largest share of 55.3% in 2025, driven by the transformation of traditional banking services through digital payments, mobile banking, and automated financial solutions.

Regional Insights

The Europe fintech market is witnessing rapid growth across major financial hubs due to strong regulatory frameworks, fintech innovation ecosystems, and growing consumer adoption of digital financial services.

- The United Kingdom led the regional market in 2025 with 28.3% share, supported by London’s position as a global fintech hub and strong venture capital investments.

- Germany ranked second with 19.3% share in 2025, driven by increasing adoption of B2B fintech solutions and strong industrial financial services integration.

- France is expected to experience significant growth due to government support for fintech innovation through initiatives such as the Paris FinTech Forum and favorable policies for financial technology startups.

Competitive Landscape

The Europe fintech market is highly competitive and characterized by a mix of established financial institutions, fintech startups, and technology providers driving digital innovation. Market participants are focusing on developing advanced financial platforms, expanding digital payment ecosystems, and integrating AI-driven financial services. Strategic partnerships, venture capital funding, and regulatory innovation are shaping competitive dynamics across the region.

Prominent companies operating in the Europe fintech market include Adyen, Revolut, PayPal, Starling Bank, Klarna, N26, OakNorth, Trade Republic, Solarisbank, and Cavalry Ventures.

Europe Fintech Market Size

The fintech market size was worth USD 98.10 billion in 2025. The Europe market is expected to be worth USD 690.86 billion by 2034 from USD 121.86 billion in 2026, growing at a CAGR of 24.22% during the forecast period.

The fintech are financial services converge with advanced technology to redefine how capital is managed, transferred, and invested across the continent. The region has emerged as a global leader in financial innovation driven by a supportive regulatory environment and a highly digitized population. As per Eurostat, data from 2023, approximately 91% of individuals in the European Union aged 16 to 74 used the internet regularly, creating a fertile ground for digital financial adoption. The European Central Bank indicates that the volume of non-cash payment transactions surpassed 105 billion in 2022, reflecting a decisive shift away from physical currency. Furthermore, the implementation of the General Data Protection Regulation has established rigorous standards for data privacy that shape the operational frameworks of fintech firms globally. The market is characterized by a symbiotic relationship between agile startups and incumbent banks, who increasingly collaborate through open banking initiatives. Consumer expectations have evolved to demand seamless, instant, and personalized financial experiences that only technology-driven solutions can provide.

MARKET DRIVERS

Widespread Implementation of Open Banking Regulatory Frameworks

The comprehensive enforcement of open banking regulations, specifically the Revised Payment Services Directive, mandates data sharing between banks and third-party providers. This widespread implementation of open banking regulatory frameworks is a primary factor bolstering the growth of Europe fintech market. This legislative framework dismantles data silos and allows fintech companies to access customer financial information with explicit consent, thereby enabling the creation of aggregated financial management tools and personalized products. According to the European Commission, the number of registered third-party providers has exceeded 5000 entities across the European Economic Area since the full implementation of the directive in 2019. This regulatory push has stimulated a surge in innovation where startups leverage application programming interfaces to build services that compete directly with traditional bank offerings. The directive has led to a 45% increase in the usage of account information services, allowing consumers to view multiple bank accounts in a single dashboard. Such capabilities enhance user experience and drive higher engagement rates with digital financial platforms. Furthermore, the regulatory clarity provided by the European Banking Authority regarding strong customer authentication has increased consumer trust in digital transactions. Banks are now compelled to collaborate with fintech firms rather than viewing them solely as threats, leading to a hybrid ecosystem of innovation. This regulatory-induced openness accelerates the pace of product development and ensures that fintech solutions remain aligned with evolving consumer expectations for customization and control.

Surging Adoption of Mobile First Financial Behaviors Among Younger Demographics

The entrenched mobile-first behavior is observed predominantly among millennials and Generation Z consumers, who view smartphones as their primary interface for managing finances. The adoption of mobile-first financial behaviours among younger people is attributed to prompting the growth of Europe fintech market. These demographics demand instant access to financial services and prefer using mobile applications for everything from account opening to investment management rather than visiting physical branches. This shift forces traditional financial institutions to partner with fintech firms or develop their own sophisticated mobile ecosystems to retain relevance. Data from Statista indicates that mobile banking users in Western Europe are projected to reach 270 million by 2025, demonstrating a compound annual growth rate that outpaces general internet usage. The demand extends beyond basic transactions to complex financial products such as mortgages and wealth management, which are increasingly digitized. Neobanks and fintech apps have capitalized on this trend by offering features such as real-time spending analytics and instant peer-to-peer payments, which resonate deeply with younger users who value transparency and speed. The psychological comfort these generations have with digital interfaces reduces the friction associated with adopting new financial technologies. The institutions that fail to optimize their mobile offerings face significant customer churn as users seamlessly switch to competitors providing superior digital engagement.

MARKET RESTRAINTS

Escalating Cybersecurity Threats and Data Privacy Concerns

The escalating sophistication of cyberattacks and the pervasive fear of data breaches among consumers and institutions alike is attributed to hampering the growth of Europe fintech market. As digital financial volumes grow, so does the attractiveness of these platforms to criminal organizations seeking to exploit vulnerabilities in software or human behavior. According to Europol, the European Union Agency for Law Enforcement Cooperation, reported a 40% increase in cybercrime incidents targeting financial institutions in 2023 compared to the previous year. These attacks range from phishing schemes to advanced persistent threats that compromise sensitive customer data and undermine trust in digital channels. The cost of remediation and regulatory fines following a breach can be astronomical, with some incidents resulting in penalties exceeding 20 million euros, under GDPR provisions. This financial risk forces fintech firms to allocate substantial portions of their budgets to cybersecurity measures rather than innovation or customer acquisition. This hesitation slows down the adoption curve for advanced services, such as biometric authentication or AI-driven financial advice. Moreover, the complexity of maintaining compliance with varying national cybersecurity standards across different European countries adds operational burdens.

Fragmented Regulatory Landscapes Across Member States

The immense difficulty fintech firms face when attempting to navigate fragmented regulatory landscapes that persist despite efforts toward harmonization under the European Union. The fragmented regulatory landscapes across member states are limiting the growth of Europe fintech market. While directives like PSD2 provide a common framework, individual member states often implement additional national requirements regarding consumer protection anti-money laundering protocols, and licensing procedures. According to analysis by Deloitte, fintech companies operating in more than five European countries must comply with over 30 distinct sets of regulatory guidelines, which increases compliance costs by an estimated 30% compared to domestic operations. This fragmentation creates barriers to entry for smaller startups that lack the resources to manage multi-jurisdictional legal complexities. It also slows down the rollout of unified products as firms must customize their offerings to meet specific national mandates. The lack of a single fintech license valid across all member states means that expansion strategies require meticulous planning and significant legal overhead. Furthermore, differing interpretations of regulations by national supervisors can lead to uncertainty and inconsistent enforcement actions. This regulatory patchwork hinders the creation of a truly seamless single market for digital financial services.

MARKET OPPORTUNITIES

Expansion of Embedded Finance Across Non-Financial Sectors

The rapid expansion of embedded finance, where financial services are integrated directly into non-financial platforms and customer journeys, is setting up new opportunities for the growth of Europe fintech market. This trend allows retailers, travel agencies, and automotive companies to offer banking products, such as loans insurance and payment processing at the point of sale without redirecting customers to a separate bank interface. This integration enhances customer convenience and opens new revenue streams for fintech firms that provide the underlying infrastructure via API connections. For instance, e-commerce platforms can now offer instant buy now pay later options powered by fintech partners, increasing conversion rates and average order values. The automotive industry is also leveraging this by embedding car financing and insurance directly into online vehicle configurators. This shift transforms fintech companies from destination brands into invisible enablers of commerce, allowing them to reach customers in contexts where they are already engaged in purchasing decisions. The data generated from these embedded interactions provides rich insights into consumer behavior, enabling more accurate risk assessment and personalized product offerings. Fintech firms that position themselves as flexible infrastructure providers stand to capture significant market share by powering the financial ecosystems of diverse sectors.

Utilization of Artificial Intelligence for Hyper Personalization

The deployment of advanced artificial intelligence and machine learning algorithms to deliver hyper-personalized financial experiences that anticipate customer needs before they arise is expected to leverage the growth of Europe fintech market. Unlike generic marketing campaigns, AI enables fintech firms to analyze vast amounts of transactional data in real time to offer tailored advice, product recommendations, and automated savings strategies. As per a study by Accenture, 75% of European financial services customers express a willingness to share their data if it results in highly personalized services and better financial outcomes. This willingness creates a fertile ground for fintech companies to differentiate themselves through intelligent features, such as predictive cash flow analysis or automated investment rebalancing. AI-driven chatbots and virtual assistants are becoming sophisticated enough to handle complex queries and provide financial coaching, reducing operational costs while enhancing user satisfaction. The ability to detect fraudulent patterns instantly also improves security and builds trust. Furthermore, machine learning models can optimize credit scoring by incorporating alternative data sources, allowing firms to serve underbanked populations who lack traditional credit histories. This inclusivity expands the total addressable market and fosters social and economic growth. As computational power increases and algorithms become more refined, the scope for personalization will widen, enabling fintech firms to act as proactive financial partners rather than passive service providers. Institutions that master this capability will likely achieve higher customer loyalty and lifetime value in an increasingly crowded marketplace.

MARKET CHALLENGES

Intensifying Margin Compression Due to Aggressive Pricing Wars

The intensifying margin compression resulting from aggressive pricing wars among fintech startups and neobanks striving to acquire share in a saturated environment is likely to impede the growth of Europe fintech market. Many new entrants offer fee-free accounts zero interest loans and high yield savings rates which erodes profitability and sustainability in the long term. As per financial disclosures analyzed by Bloomberg, several prominent European fintech firms reported net losses exceeding 150 million euros in 2023, primarily due to heavy spending on customer acquisition incentives and below-cost pricing strategies. This race to the bottom forces even established institutions to lower their fees to remain competitive, thereby shrinking overall industry margins. The reliance on interchange fees from card transactions as a primary revenue source becomes risky when transaction volumes fluctuate or when regulators cap these fees to protect consumers. Additionally, the cost of capital has risen in the recent economic climate, making it harder for loss-making fintech firms to secure funding for continued expansion. Investors are increasingly demanding clear paths to profitability, which pressures companies to cut costs often at the expense of service quality or innovation. The inability to diversify revenue streams beyond basic transactional fees leaves many players vulnerable to economic downturns. Sustainable growth requires a shift towards value-added services, but the prevailing competitive dynamics make it difficult to introduce premium pricing without losing customers to cheaper alternatives.

Shortage of Specialized Technical Talent and Expertise

The acute shortage of specialized technical talent capable of developing and maintaining complex fintech solutions in areas such as blockchain, artificial intelligence and cybersecurity is additionally to inhibit the growth of Europe fintech market. The rapid pace of innovation in the financial sector has created a demand-supply gap where the number of available skilled professionals falls far short of industry needs. According to a report by the European Centre for the Development of Vocational Training, the European Union faces a deficit of over 1 million digital specialists, including those with expertise in financial technologies. This scarcity drives up salary costs and makes it difficult for smaller fintech startups to compete with large tech giants and banks for top talent. The lack of experienced personnel delays product development cycles and increases the risk of technical failures or security vulnerabilities. Furthermore, the interdisciplinary nature of fintech requires professionals who possess both deep technical knowledge and understanding of financial regulations, which is a rare combination. Educational institutions struggle to update curricula fast enough to keep pace with emerging technologies, exacerbating the skills gap. Companies are forced to invest heavily in training programs and relocation packages to attract international experts, which strains limited resources. The inability to scale teams quickly limits the ability of fintech firms to seize market opportunities and innovate at the required speed.

SEGMENTAL ANALYSIS

By Deployment Mode Insights

The cloud-based segment was the largest by accounting for a dominant share of the Europe Fintech Market share in 2025, owing to the inherent need for scalability and cost efficiency which traditional on-premises infrastructure cannot match for agile financial startups and evolving neobanks. The first major factor is the ability of cloud platforms to handle massive fluctuations in transaction volumes without requiring significant capital expenditure on physical hardware. According to a report by Flexera, 92% of European financial services firms have adopted a multi-cloud strategy in 2023 to leverage best-of-breed services and ensure business continuity. This approach allows fintech companies to deploy updates and new features rapidly, which is crucial in a competitive environment where speed determines survival. The enhanced security and compliance capabilities offered by major cloud providers, who invest billions in cybersecurity measures that individual fintech firms could not afford independently, are another attribute propelling the growth of the segment. Data from the European Union Agency for Cybersecurity indicates that cloud providers often maintain higher security standards than many on-premises data centers, reducing the risk of breaches. Furthermore, the cloud facilitates seamless integration with third-party APIs, which is essential for open banking ecosystems. The shift toward remote work models has also accelerated cloud adoption as it enables secure access to financial systems from anywhere. These combined advantages ensure that the cloud-based model remains the default choice for the vast majority of fintech innovations across the continent.

The on-premises segment is likely to witness the fastest CAGR of 4.2% throughout the forecast period, with the specific regulatory and security requirements. The growth of the segment is driven by the persistent hesitation of large legacy banks and government-affiliated financial institutions to migrate sensitive core banking data to public cloud environments due to strict data sovereignty laws. The stringent interpretation of data residency regulations in countries like Germany and France where national supervisors mandate that certain financial data must remain within physical borders under direct control of the institution. As per guidelines from the European Banking Authority, several systemic banks maintain that core ledger functions must reside on local servers to ensure immediate regulatory oversight and mitigate third-party dependency risks. The concern over vendor lock-in, where institutions fear losing control over their technology stack if they rely entirely on a single cloud provider, is also elevating the growth of the segment. A study by McKinsey and Company reveals that 45% of European banks cite vendor concentration risk as a primary barrier to full cloud migration. Consequently, these institutions are investing in modernizing their existing on-premises data centers with hybrid capabilities that offer some agility while retaining physical control. This cautious approach ensures a sustained demand for advanced on-premises solutions, particularly for high-security applications where absolute data control is non-negotiable.

By Technology Insights

The application programming interface segment was accounted in holding 32.3% of the European fintech market share in 2025, owing to the mandatory nature of open banking regulations which require banks to expose customer data to third-party providers through secure APIs. The Revised Payment Services Directive, which legally obliges financial institutions to provide API access, thereby creating a massive installed base and continuous demand for API management solutions. This regulatory mandate has transformed APIs from a technical tool into a strategic asset that drives the entire fintech ecosystem. The rise of embedded finance, where non-financial companies integrate banking services directly into their platforms using APIs to offer seamless customer experiences is greatly influencing the growth of segment. Data from Bain and Company suggests that API-driven embedded finance transactions in Europe are growing at twice the rate of traditional banking channels. APIs enable real-time data exchange, which is critical for services like instant payments account aggregation and identity verification. The ability to connect disparate systems efficiently allows fintech firms to scale rapidly without building entire infrastructures from scratch.

The artificial intelligence segment is anticipated to witness a fastest CAGR of 24.5% from 2026 to 2034 with the urgent need for advanced data processing capabilities to manage fraud detection personalized marketing and automated customer service. The increasing sophistication of financial crimes, which necessitates AI-driven real-time monitoring systems that can identify anomalies faster than human analysts, is solely to leverage the growth of segment. The consumer demand for hyper-personalized financial advice, which AI algorithms deliver by analyzing vast datasets to tailor product recommendations and investment strategies. Machine learning models allow fintech companies to automate complex processes, such as credit scoring and loan underwriting, reducing turnaround times from days to minutes. Furthermore, the deployment of natural language processing in chatbots has significantly lowered customer support costs while improving satisfaction scores.

By End-User Insights

The banking segment held 55.3% of the Europe Fintech Market share in 2025, as banking services constitute the core of financial interactions and are the primary target for digital disruption and innovation. Also, the massive volume of retail and corporate transactions that require efficient digital processing solutions ranging from mobile payments to cross-border transfers is also expected to amplify the growth of the segment. As per Eurostat, data, the value of non-cash payment transactions in the European Union exceeded 105 billion in 2022, with the vast majority processed through fintech-enhanced banking channels. The intense competition among traditional banks and neobanks, which forces continuous investment in fintech solutions to improve user experience and reduce operational costs. The European Banking Federation notes that digital transformation spending by European banks reached record levels in 2023 as institutions race to retain customers who expect seamless mobile-first experiences. Banks are increasingly partnering with fintech firms to offer value-added services such as robo-advisory and instant lending, which expands the addressable market for fintech technologies. The regulatory push for open banking has further cemented the role of fintech in the banking sector by mandating collaboration between incumbents and startups. This structural reliance on technology for core banking operations ensures that the banking segment remains the primary engine of market growth.

The insurance segment is expected to register the fastest CAGR of 19.8% from 2026 to 2033 with the emergence of Insurtech solutions that leverage big data and IoT to revolutionize underwriting claims processing and customer engagement. The shift toward usage-based insurance models, where telematics and connected devices provide real-time data to calculate premiums more accurately, is significantly bolstering the growth of the segment. According to Deloitte, the adoption of usage-based insurance policies in Europe is expected to double by 2026, driven by consumer demand for fairer pricing and personalized coverage. The automation of claims processing through AI and computer vision, which significantly reduces settlement times and fraud rates. Data from Swiss Re indicates that automated claims handling can reduce processing costs by up to 40%, making it a highly attractive proposition for insurers facing margin pressures. Furthermore, the rise of on-demand insurance products for the gig economy and short-term rentals requires agile digital platforms that traditional systems cannot support. Fintech companies are filling this gap by providing white-label solutions that enable rapid product launches.

COUNTRY-LEVEL ANALYSIS

United Kingdom Fintech Market Analysis

The United Kingdom was the largest contributor to the Europe Fintech Market by accounting for 28.3% of the market share in 2025. The nation has cultivated a unique ecosystem supported by proactive regulatory sandboxes and a deep pool of venture capital that attracts startups from around the world. The status of the UK as a global fintech hub is reinforced by its early adoption of open banking standards, which mandated data sharing and spurred intense competition. As per reports from UK Finance, the country is home to over 2500 active fintech firms, making it the largest cluster in Europe and second only to New York globally. The presence of successful unicorns like Revolut and Wise has forced traditional incumbents to accelerate their digital transformation agendas to retain customers. London serves as the epicenter for this activity, attracting talent and investment to develop cutting-edge financial solutions in areas like blockchain and regtech. The government's commitment to maintaining a competitive edge post-Brexit has led to further deregulation and incentives for tech innovation. High internet penetration rates and a culturally progressive attitude toward digital finance create a perfect storm for fintech growth.

Germany Fintech Market Analysis

Germany Fintech Market held 19.3% of the share in 2025 with a strong focus on B2B fintech and industrial applications. The robust manufacturing sector that demands efficient digital supply chain finance and payment solutions is driving the growth of the market in this country. According to the German Federal Bank, the volume of digital B2B transactions grew by 15% in 2023, signaling a shift toward automated financial workflows in the industrial sector. The presence of major automotive and engineering companies that are integrating fintech solutions to optimize cash flow and manage complex international payments will also bolster the growth of the market. German consumers are increasingly embracing digital wallets and mobile banking apps, particularly among the younger demographic who find traditional branch hours inconvenient. The regulatory environment under BaFin ensures high security standards, which builds trust in digital channels despite initial skepticism. Major institutions like Deutsche Bank are investing billions in modernizing their IT landscapes to compete with agile fintech entrants.

France Fintech Market Analysis

France fintech market is deemed to grow with the influenced by strong government support for fintech through initiatives like the Paris FinTech Forum and favorable tax regimes for startups. The driving factors include a high level of smartphone penetration and a population that is increasingly comfortable with managing finances digitally. As per data from the French Banking Federation, the number of active users of fintech applications exceeded 20 million in 2023, reflecting a widespread acceptance of digital financial tools. French banks are leveraging artificial intelligence to personalize customer interactions and streamline loan approval processes, which enhances user satisfaction. The presence of major European players like BNP Paribas and Société Générale drives significant investment in digital platforms that serve both domestic and international markets. The regulatory framework encourages innovation while maintaining strict consumer protection, which fosters a balanced growth environment. The rise of green finance and sustainable investing options within fintech platforms appeals to the environmentally conscious French consumer base. Furthermore, the integration of banking services with e-commerce platforms is gaining traction, creating new avenues for growth.

Netherlands Fintech Market Analysis

The Netherlands Fintech Market growth is likely to grow with its advanced progression toward a cashless society. The growth of the market in this country is likely to grow with the exceptionally high adoption rates of digital payments and open banking, driven by a culturally ingrained preference for efficiency. Dutch consumers are early adopters of new technologies such as instant payment systems and peer-to-peer lending platforms, which enhance financial inclusion. The strong presence of ING and other forward-thinking institutions has set high standards for digital user experiences that competitors must match. The government actively supports digital innovation through policies that encourage electronic transactions and reduce reliance on physical cash. The high level of English proficiency and digital literacy among the populace facilitates the rapid rollout of international fintech solutions.

Sweden Fintech Market Analysis

Sweden fintech market growth is propelled by being the birthplace of several global fintech giants including Klarna and Spotify, which has created a vibrant startup culture. According to Statistics Sweden, the usage of mobile payment solutions surged by 25% in 2023 as merchants and consumers alike adapted to digital norms. The primary driver is the near-total elimination of cash in the economy, which has forced all participants to adopt digital financial tools for daily transactions. Swedish banks are aggressively launching mobile-first products to capture the attention of users who rarely visit physical branches. The tech-savvy population and strong government support for digitalization create an ideal testing ground for new fintech innovations. Government programs aimed at promoting digital literacy have further accelerated adoption rates among all age groups.

COMPETITIVE LANDSCAPE

The competition within the Europe Fintech Market is characterized by an intense rivalry between agile neobanks, specialized payment processors, and traditional financial institutions undergoing digital transformation. Incumbent banks leverage their vast capital reserves and established trust relationships to fund massive technology upgrades, while fintech startups compete on superior user experience, lower fees, and niche specialization. This dynamic creates a fragmented yet vibrant landscape where no single entity holds absolute control, forcing all participants to innovate continuously. The entry of big tech companies into financial services adds further pressure as they utilize their enormous user data and seamless ecosystems to capture market share. Regulatory frameworks like open banking have lowered barriers to entry, enabling smaller firms to challenge incumbents with specialized offerings. Price wars are common as institutions sacrifice short-term margins to acquire users through attractive sign-up bonuses and zero-fee structures. Differentiation now relies heavily on the ability to provide integrated lifestyle features and proactive financial advice rather than basic transactional capabilities.

KEY MARKET PLAYERS

The leading companies operating in the Europe fintech market include:

- Adyen

- Revolut

- PayPal

- Starling Bank

- Klarna

- N26

- OakNorth

- Trade Republic

- Solarisbank

- Cavalry Ventures

TOP PLAYERS IN THE MARKET

- Revolut operates as a leading digital banking platform originating from the United Kingdom with a massive global footprint serving millions of customers. The company provides a comprehensive suite of financial services, including currency exchange, stock trading, and cryptocurrency management through a single mobile application. Its contribution to the global market involves democratizing access to complex financial instruments for retail users and setting new standards for user experience in digital finance. Recently, Revolut has intensified its expansion by securing full banking licenses in multiple European jurisdictions to offer deposit protection and lending products. The firm continuously launches innovative features such as junior accounts and business tools to capture diverse demographic segments. These strategic moves solidify its reputation as a versatile financial super app that challenges traditional banking models worldwide through continuous product diversification and aggressive international scaling.

- Adyen stands as a Dutch payment technology giant that provides a unified commerce platform enabling businesses to accept payments across online, mobile, and in-store channels globally. The company serves major multinational corporations by offering seamless integration of payment methods and sophisticated fraud protection mechanisms. Its global contribution lies in simplifying the complexity of cross-border transactions and providing real-time data analytics to optimize acceptance rates for merchants. Recent actions include the launch of embedded financial products that allow platforms to offer banking services directly to their users without leaving the ecosystem. Adyen actively invests in expanding its acquiring network to support local payment methods in emerging markets, thereby increasing reach for its clients. The firm also focuses on sustainability by helping merchants track and reduce the carbon footprint of their transactions. These initiatives demonstrate how Adyen strengthens its market position by becoming an indispensable infrastructure partner for the global digital economy.

- Klarna is a Swedish fintech pioneer that revolutionized the buy now, pay later sector by offering flexible payment solutions at the point of sale for online and offline retailers. The company has expanded its services to include direct consumer banking products such as savings accounts and shopping rewards programs globally. Its contribution to the international market involves reshaping consumer credit habits and enabling merchants to increase conversion rates through frictionless checkout experiences. Recently, Klarna has focused on achieving profitability by streamlining operations and introducing AI-driven shopping assistants that personalize the consumer journey. The firm partners with major global brands to integrate its payment options deeply into their e-commerce platforms, enhancing customer loyalty. Klarna also emphasizes responsible lending practices by implementing strict credit checks and educational tools for users. These efforts ensure its continued leadership in the alternative credit space while adapting to changing regulatory landscapes and economic conditions worldwide.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe Fintech Market primarily employ aggressive expansion strategies through obtaining full banking licenses to broaden their product offerings beyond payments into lending and deposits. Companies frequently pursue strategic partnerships with established traditional banks to leverage existing infrastructure while injecting technological innovation into legacy systems. Another dominant strategy involves heavy investment in artificial intelligence and machine learning to enhance fraud detection capabilities and deliver hyper-personalized customer experiences. Firms are increasingly focusing on building super apps that consolidate multiple financial services into a single interface to increase user retention and lifetime value. Geographic diversification serves as a critical approach where participants enter emerging markets to capture growth opportunities outside saturated Western European regions. Furthermore, companies prioritize regulatory compliance by engaging proactively with supervisors to shape favorable policies and maintain operational legitimacy. These collective strategies aim to foster ecosystem dominance improve operational efficiency and secure a competitive advantage in the rapidly evolving digital financial landscape.

MARKET SEGMENTATION

This research report on the Europe fintech market has been segmented and sub-segmented based on the following categories.

By Deployment Mode

- On-Premises

- Cloud-based

By Technology

- Application Programming Interface (API)

- Artificial Intelligence

- Blockchain

- Data Analytics

- Robotic Automation Process

By Application

- Payment

- Fund Transfer

- Loans

- Insurance

- Personal Finance

- Wealth Management

- Others

By End-User

- Banking

- Insurance

- Securities

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe fintech market?

The Europe fintech market provides digital payments, lending, and insurance through mobile platforms. UK dominates innovation while PSD2 accelerates open banking adoption.

How does the Europe fintech market function?

The Europe fintech market functions through APIs connecting banks with innovative services. Regulated providers deliver seamless digital financial experiences.

What drives growth in the Europe fintech market?

PSD2 regulations drive the Europe fintech market enabling open banking competition. Consumer smartphone adoption accelerates digital payment solutions.

Which countries lead the Europe fintech market?

UK leads the Europe fintech market as Europe's fintech capital. Germany and Netherlands follow with strong regulatory frameworks supporting innovation.

What segments define the Europe fintech market?

Digital payments dominate the Europe fintech market alongside lending platforms. Insurtech grows rapidly through personalized policy offerings.

How does regulation shape the Europe fintech market?

PSD2 governs the Europe fintech market mandating API access for third parties. Strong customer authentication enhances transaction security.

What role does open banking play in the Europe fintech market?

Open banking transforms the Europe fintech market enabling data-driven services. Account aggregation powers personalized financial recommendations.

What trends influence the Europe fintech market?

Embedded finance shapes the Europe fintech market integrating banking into e-commerce. Buy-now-pay-later solutions gain widespread merchant adoption.

What challenges face the Europe fintech market?

Regulatory compliance challenges the Europe fintech market though sandbox programs help. Legacy bank integration slows innovation deployment.

How have neobanks impacted the Europe fintech market?

Neobanks revolutionized the Europe fintech market offering fee-free digital banking. Real-time spending insights improve consumer financial management.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com