Europe Garden Pesticides Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By Product Type, Application, Distribution Channels, And By Country (U.K France, Germany, Spain, Italy, Sweden, Russia and Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2026 to 2034)

Europe Garden Pesticides Market Size

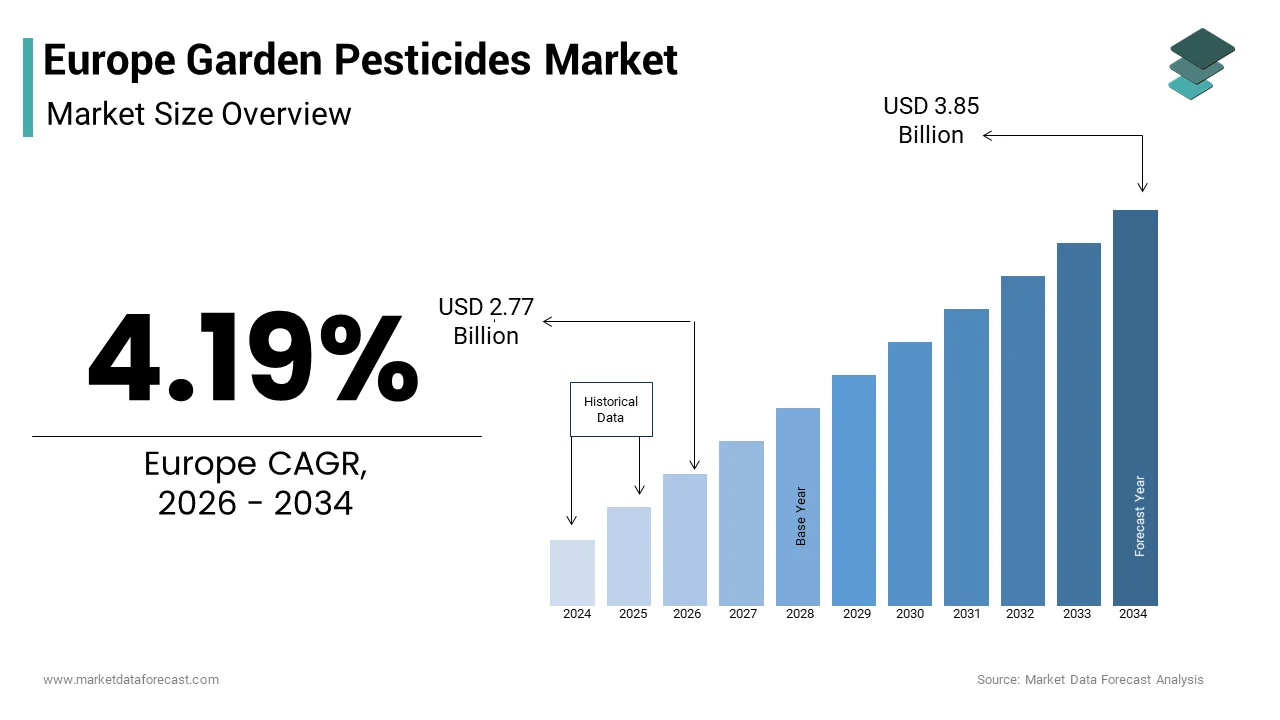

The Europe garden pesticides market size was valued at USD 2.66 billion in 2025 and is anticipated to reach USD 2.77 billion in 2026 to reach USD 3.85 billion by 2034, growing at a CAGR of 4.19% during the forecast period from 2026 to 2034.

Current Introduction of the Europe Garden Pesticides Market

Garden pesticides are chemical and biological substances used by homeowners, urban gardeners, and small-scale horticulturists to control pests, diseases, and weeds in residential lawns, ornamental gardens, and balcony or community green spaces. The European Union’s regulatory framework, particularly Regulation EC 1107 2009, governs the approval of active substances, while national authorities oversee product authorization and usage guidelines. As per Eurostat, over 82 million households in the European Union engaged in some form of gardening in 2023, with 63% maintaining ornamental plants and 41% cultivating vegetables or herbs. This widespread horticultural activity creates consistent demand for accessible pest management solutions. Additionally, climate change has extended growing seasons and enabled new pest populations to establish northward, as per the European and Mediterranean Plant Protection Organization. These ecological and behavioral trends underpin a dynamic yet highly regulated market for garden pesticides across Europe.

MARKET DRIVERS

Expansion of Urban Gardening and Edible Landscaping Initiatives

The resurgence of urban gardening for accessible and safe pest control solutions for home use is majorly boosting the growth of Europe garden pesticides market. As per Eurostat, 41% of European households grew vegetables, fruit,s or herbs in 2023, a 9% increase from 2019, driven by food security concerns and sustainability awareness. Cities like Berlin, Paris, and Copenhagen have institutionalized urban agriculture through municipal allotment programs. Berlin alone manages over 90,000 garden plots, as reported by its Urban Greening Office. These edible gardens are highly vulnerable to aphids, caterpillars,,s and fungal pathogens that can decimate yields without intervention. In response, consumers increasingly seek ready-to-use sprays and granules that are effective yet compliant with residential safety standards. France’s Ministry of Ecological Transition noted a 28% rise in registered home garden pesticide sales between 2021 and 2023, directly linked to the proliferation of community and balcony gardening. This grassroots greening movement transforms private green spaces into active cultivation zones, sustaining steady demand for targeted pest management products.

Prolonged Growing Seasons and Northward Spread of Invasive Species Due to Climate Change

Climate change is fundamentally altering pest ecology, extending infestation windows, and introducing non-native species into previously unaffected regions. The prolonged growing seasons and the northward spread of invasive species due to climate change are additionally propelling the growth of Europe garden pesticides market. Warmer average temperatures have enabled pests like the box tree moth and spotted wing drosophila to survive winters, as far north as Sweden and Denmark, where they were previously absent. The European Environment Agency confirms that the growing season in Western and Central Europe has lengthened by 12 to 15 days since 2000, giving pests additional reproductive cycles. For instance, aphid populations now produce up to five generations per year in Germany compared to three in the 1990s, as per the Julius Kühn Institute. Home gardeners face unprecedented pressure to protect ornamental and edible plants without agricultural-grade tools. National plant health services in the Netherlands and Italy have issued public advisories urging proactive garden monitoring and approved pesticide use. This shifting bio-threat landscape compels residential users to adopt timely and effective pest control measures, reinforcing reliance on registered garden pesticides as a first line of defense.

MARKET RESTRAINTS

Strict EU and National Regulations Limiting Active Ingredient Approvals and Usage

The European Union enforces some of the world’s most rigorous regulations on pesticide use, significantly constraining the formulation and availability of garden products, which is one of the restraining factors for the growth of Europe-garden pesticides market. Regulation EC 1107 2009 mandates that active substances undergo comprehensive risk assessments for human health and environmental impact before approval. As per the European Commission, over 70 active substances commonly used in garden pesticides were withdrawn between 2015 and 2023 due to concerns over ecotoxicity or endocrine disruption. Neonicotinoids, for instance,e were banned for all outdoor uses in 2018 following European Food Safety Authority findings linking them to pollinator decline. National authorities further restrict usa.ge. France’s Labbe Law prohibits non-professional use of synthetic pesticides entirely, allowing only biocontrol products in home gardens. Germany’s Plant Protection Act requires garden pesticides to carry explicit warnings and usage instructions, limiting consumer appeal. These regulatory barriers reduce the number of effective solutions available to home users, forcing reliance on less potent biological alternatives that often require repeated applications. The compliance burden also increases development costs and time to market for manufacturers, stifling innovation in the residential segment.

Growing Consumer Preference for Chemical-Free and Organic Gardening Practices

A significant and expanding segment is actively avoiding synthetic pesticides in favor of organic or non-chemical alternatives. According to the European Consumer Organisation, 54% of respondents in a 2023 survey expressed a strong preference for “chemical-free” gardening, citing concerns about children's pet safety and environmental impact. This shift is particularly pronounced in Northern Europe. Sweden’s National Board of Housing reports that 68% of urban gardeners use only physical barriers, rs companion planting, ing or homemade remedies. Retailers reflect this trend; the United Kingdom’s largest garden center chain reported that certified organic pest control products grew by 33% in 2023 while synthetic spray sales declined. Social media and gardening influencers further amplify natural methods, promoting neem, oil, diatomaceous earth, and beneficial insects as ethical alternatives. The European Commission’s Farm to Fork Strategy indirectly reinforces this mindset by advocating reduced chemical use across all land uses, including domestic spaces. As public awareness grows, the social acceptability of synthetic pesticides in residential settings diminishes, pressuring manufacturers to reformulate or risk brand reputation erosion.

MARKET OPPORTUNITIES

Rise of Biopesticides and Microbial Solutions Aligned with Regulatory and Consumer Trends

The accelerating approval and adoption of biopesticides is creating new opportunities for the growth of Europe garden pesticides market. Unlike synthetic chemicals, biopesticides derived from bacteria, fungi, i or plant extracts face faster regulatory pathways under EU Regulation 1107 2009’low-risksk criteria. As per the European Biopesticides Association, over 120 microbial and botanical active substances received national authorization for home garden use between 2020 and 2023. Products containing Bacillus thuringiensis for caterpillar control and Trichoderma harzianum for root rot prevention are now widely available in France, Germany, and the Netherlands. The European Commission’s 2022 guidance explicitly encourages biocontrol adoption in urban settings as part of its biodiversity strategy. Retail partnerships are expanding Aldi and Lidl, which now stock certified biopesticides in their garden sections across 15 EU countries. Moreover, consumer trust is growing, with a 2024 survey by the German Federal Ministry of Food showing that 61% of gardeners perceive biopesticides as equally or more effective than synthetics for common pests. This emergence of regulatory support, retail access, ss and shifting perception positions biopesticides as the cornerstone of next-generation residential pest management in Europe.

Integration of Digital Tools and Smart Gardening Ecosystems for Precision Application

The emergence of smart gardening technologies offers a novel avenue for targeted and efficient pesticide use in residential settings, which is also a significant factor escalating the growth of Europe garden pesticides market. Connected devices, such as soil sensors, weather stations, ns aAI-poweredred pest identification apps, enable gardeners to apply treatments only when necessary, minimizing overuse. As per the European Smart Gardening Alliance, over 2.1 million smart irrigation and monitoring systems were sold in Europe in 2023, many featuring integrated pest alert functions. Companies like Bosch and Gardena now offer app-linked sprayers that calculate precise dosage based on plant type and infestation level, reducing chemical runoff. In the Netherlands, a pilot program by Wageningen University validated an AI model that identifies aphid hotspots from smartphone photos with 89% accuracy, guiding spot treatment instead of blanket spraying. The European Commission’s Digital Europe Programme has allocated funding to scale such precision horticulture tools for urban users. These innovations align with the EU’s sustainable use directive by promoting “as little as possible but as much as necessary” application.

MARKET CHALLENGES

Inconsistent National Implementation of EU Pesticide Regulations Creating Market Fragmentation

Despite a unified EU regulatory framework, significant disparities in national authorization and enforcement create operational complexity for manufacturers and confusion for consumers. The inconsistent national implementation of EU pesticide regulations is expected to decline the growth of Europe garden pesticides market. As per the European Commission’s 2023 Pesticide Residue Monitoring Report, the same active substance may be approved for garden use in Germany but prohibited in France or Belgium under national derogations. For example, copper-based fungicides are widely available in Spain for home vine protection but face severe restrictions in Denmark due to soil accumulation concerns. This patchwork forces companies to maintain multiple product formulations and labeling versions, increasing costs and logistics burdens. Furthermore, cross-border e-commerce complicates compliance. Consumers in restricted countries often purchase unapproved products online from neighboring states, as noted by the European Consumer Safety Network in 2024. National plant protection agencies lack harmonized inspection protocols for retail and online sales, leading to uneven enforcement. This regulatory dissonance not only hampers market efficiency but also undermines public trust in pesticide safety oversight, posing a systemic barrier to coherent market development across the European Union.

Limited Efficacy Awareness and Misuse of Approved Products Leading to Resistance and Environmental Harm

Even when gardeners use legally approved pesticides, widespread lack of technical knowledge results in incorrect application timing, dosage, or target selection, reducing effectiveness and increasing ecological risk. According to a 2024 study by the Julius Kühn Institute in Germany, over 60% of home users applied fungicides preventively without confirming disease presence, while 45% used insecticides during flowering periods harmful to pollinators. The European Food Safety Authority has documented rising resistance in common pests like spider mites and whiteflies due to repetitive use of the same mode of action products in residential zones. In Italy, regional plant health services reported that amateur misuse contributed to localized contamination of urban water runoff with pyrethroids exceeding environmental quality standards. National campaigns like the UK’s “Dispose of Pesticides Responsibly” initiative highlight persistent gaps in safe handling and disposal practices. Without standardized education or mandatory training, as exists for professional applicators, home users operate with fragmented knowledge, inadvertently driving resistance development and environmental contamination. This behavioral challenge undermines the sustainability goals of the EU’s pesticide reduction strategy and demands innovative outreach beyond labeling alone.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.19% |

| Segments Covered | By Product Type, Application, And By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic,& Rest of Europe |

| Market Leaders Profiled | Betterbee Inc. (U.S.), Miller’s Honey Company (U.S.), Dabur India Limited (India), Shangdong Bokang Apiculture Co. Ltd. (China), Beehive Botanicals Inc. (U.S.). |

SEGMENTAL ANALYSIS

By Product Insights

The insecticides segment accounted in holding 42.3% of the Europe garden pesticides market share in 2025, with the high visibility and immediate damage caused by insect pests in ornamental and edible home gardens, prompting rapid consumer response. According to the European and Mediterranean Plant Protection Organization, over 200 invasive insect species are now established in European urban green spaces, with pests like aphids, whiteflies,, es and box tree moths causing widespread concern among amateur gardeners. The Royal Horticultural Society in the United Kingdom reported that insect-related queries constituted 68% of all plant health inquiries in 2023, underscoring public anxiety over infestations. In Germany, the Federal Office of Consumer Protection noted that pyrethroid and neem-based insecticide sales for home use rose between 2021 and 2023, particularly in regions affected by the oak processionary moth. Additionally, the expansion of balcony and container gardening practiced by over 35 million urban householdscreates micro ecosystems highly susceptible to rapid pest colonization. The immediacy of insect damage, combined with ready-to-use spray formats and strong retail presence, sustains insecticides as the most frequently purchased garden pesticide categoryacross Europe.

The fungicides segment is projected to expand at a CAGR of 6.9% from 2025 to 2033 from rising incidence of fungal diseases linked to changing climate patterns and intensive urban horticulture. As per the Julius Kuhn Institute in Germany, outbreaks of powdery mildew d,,owny mildew, and botrytis in home gardens increased by 31% between 2019 and 2023 due to higher humidity and erratic rainfall. The cultivation of disease-prone ornamentals such as roses, hydrangeas, and tomatoes grown in over 55% of European home gardens fuels demand for preventive and curative treatments. Regulatory shifts also favor bio-based fungicides, where copper and sulfur formulations, along with microbial products containing Bacillus subtilis, are increasingly authorized under low-risk criteria. Retailers in the Netherlands and Sweden now dedicate prominent shelf space to organic fungicides, reflecting consumer preference for sustainable solutions. As climate volatility intensifies and edible gardening expands, fungicides are transitioning from occasional to essential inputs in residential plant care routines.

By Application Insights

The private gardens segment held a dominant share of the Europe garden pesticides market in 2024, with the cultural and recreational significance of home gardening across the continent, where over 82 million households maintain private green spaces for aesthetics food production, or leisure. As per Eurostat, 63% of European households engage in ornamental gardening,g while 41% cultivate vegetables or herbs, creating consistent demand for pest and disease control. National policies further reinforce this trend;d, Germany’s Federal Ministry for the Environment supports over 1.4 million allotment gardens through municipal programs, each requiring individual pest management. In the United Kingdom, the Royal Horticultural Society estimates that private gardeners account for 90% of all non-professional pesticide use, driven by high plant density and aesthetic expectations. Unlike public or institutional settings, private users prioritize convenience and immediate results, favoring ready-to-use sprays and granules available at garden centers and supermarkets. The emotional and personal investment in home gardens ensures sustained product engagement, making this segment the cornerstone of the residential pesticide market.

The lawn and garden application segment is projected to grow at a CAGR of 7.3% during the forecast period, with the professionalization of residential landscaping and rising investment in garden aesthetics as extensions of living space. According to the European Landscape Contractors Association, spending on garden design and maintenance by European households increased by 18% in 2023, with premium lawns and structured planting schemes becoming status symbols in suburban areas. These curated landscapes are highly vulnerable to pests and disease,s requiring coordinated treatment strategies. Additionally, the rise of “garden wellness” trends promoting outdoor relaxation and mental health has elevated expectations for pristine green spaces. Retailers respond with bundled products targeting lawn insects, ts fungal pathogens, nd weed competition in unified systems. As European homeowners increasingly view gardens as functional living environments rather than passive plots, demand for comprehensive lawn and garden pest solutions intensifies across both DIY and contractor channels.

COUNTRY ANALYSIS

Germany Garden Pesticides Market Analysis

Germany was the top performer of the Europe garden pesticides market by holding 21.3% of the share in 2024, with a deeply rooted gardening culture, strong regulatory oversight, and extensive allotment infrastructure. The country hosts over 1.4 million registered Kleingarten or allotment gardens managed under federal law, as documented by the German Federal Ministry for the Environment. These plots, used by more than 5 million citizens, require individual pest management and drive consistent product demand. Germany maintains a rigorous approval process through the Federal Office of Consumer Protection and Food Safety, which evaluates all garden pesticides for ecotoxicity and user safety. Despite restrictions on neonicotinoids and synthetic herbicides, biopesticide authorizations have risen;n 28 new microbial products were approved in 2023 alone. Retail channels are highly developed with specialized garden centers like Dehner and Hornbach offering extensive pesticide sections alongside expert advice. Public awareness is amplified by institutions such as the Julius Kühn Institute, which publishes seasonal pest alerts and best practice guides.

France Garden Pesticides Market Analysis

France's garden pesticide market was positioned second by capturing 18.2% of the share in 2024, with its pioneering ban on synthetic pesticides for non-professional use under the 2014 Labbe Law. This legislation has a rapid shift toward biocontrol products by making France the largest contributor toorganic garden pesticides in Europe. According to France’s Ministry of Ecological Transition, sales of approved biopesticides for home gardens grew by 37% between 2021 and 2023, while synthetic insecticide sales declined by 29%. The country’s 17 million home gardeners now rely on neem oil, pyrethrin,s and beneficial insects sourced from certified organic retailers. National campaigns like “Jardiner Autrement” promote alternative pest management through public workshops and digital resources. The French Agency for Fo, od Environmental, and Occupational Health actively monitors product safety and enforces labeling standards. France’s regulatory stance not only shapes domestic consumption but also influences policy debates across Southern Europe, establishing it as a trendsetter in sustainable residential pest control.

United Kingdom Garden Pesticides Market Analysis

The United Kingdom garden pesticides market growth is expected to have the fastest CAGR throughout the forecast period, with the passionate gardening participation and dynamic retail ecosystems. As per the Royal Horticultural Society, 72% of UK adults engage in gardening, with over 27 million maintaining private plots or container gardens. This enthusiasm drives consistent demand for accessible and effective pest control solutions. Major retailers like B and Q and Wyevale offer extensive pesticide ranges, including organic options certified by the Soil Association. The UK stands out for its robust extension service; RHS plant clinics handled over 120 000 pest identification requests in 2023, guiding appropriate product use. Unlike some EU nations, the UK permits a broader range of synthetic actives for home use under strict labeling, balancing efficacy with safety. Post Brexit, the Health and Safety Executive continues to align with EU risk assessments while enabling faster authorization of low-risk biopesticides. Urban gardening initiatives in London and Manchester further expand the user base. The combination of cultural priority, retail accessibility, and expert support ensures the UK remains a high-volume and innovation-responsive market for garden pesticides.

Italy Garden Pesticides Market Analysis

Italy's garden pesticides market growth is likely to grow with the favorable year-round pest activity and a strong tradition of ornamental horticulture. The country’s warm, humid summers create ideal conditions for fungal diseases and insect outbreaks. Italy’s National Research Council reported a 40% increase in olive peacock spot and rose black spot in home gardens between 2020 and 2023. Over 22 million Italian households maintain gardens, with a pronounced focus on decorative plants, vines, and citrus trees that require intensive protection. The Ministry of Agricultural Policies actively promotes integrated pest management through regional agricultural offices, which distribute guidelines to amateur growers. Copper-based fungicides remain widely used despite EU restrictions due to their efficacy against downy mildew in vineyard-inspired home plots. Retail chains like Leroy Merlin have expanded organic pesticide sections in response to consumer demand, particularly in northern regions. Additionally, Italy’s aging rural population increasingly manages home gardens as leisure activities, sustaining product usage. These ecological and cultural factors ensure Italy remains a high-pressure and high-engagement market for both conventional and bio-based garden pesticides.

Netherlands Garden Pesticides Market Analysis

The NeNetherlands'arden pesticide market growth is propelled by the hub for green innovation and sustainable urban gardening practices. Known globally for its horticultural expertise, the country applies this knowledge to residential settings through advanced biocontrol solutions and precision application tools. The Dutch government’s Green Deal for Urban Horticulture promotes chemical-free pest management through subsidies for beneficial insects and pheromone traps. The Netherlands Food and Consumer Product Safety Authority maintains one of Europe’s strictest approval systems, yet fast-tracks microbial pesticides; 42 biopesticides received authorization in 2023. Companies like Koppert Biological Systems supply home garden versions of professional biocontrol agents, bridging commercial and residential markets. Educational campaigns by Wageningen University empower citizens to identify pests and choose targeted treatments.

COMPETITIVE LANDSCAPE

The Europe garden pesticides market features a competitive mix of multinational agrochemical companies, es specialized horticultural brands,nds and emerging biocontrol innovators. Competition is primarily driven by regulatory compliance, ance product safety, safety,afety and alignment with organic or chemical-free gardening trends rather than price alone. Established players like BASF Syngenta and UPL leverage their R and D capabilities to reformulate legacy actives into eco-friendly formats while simultaneously expanding their biopesticide pipelines. Regional brands in countries like France and the Netherlands focus on niche organic segments with locally sourced ingredients and strong retail partnerships. The market is highly fragmented due to divergent national regulations. France’s ban on synthetic home pesticides contrasts with more permissive regimes in Eastern Europe, requiring tailored product portfolios. Innovation is increasingly centered on integrated solutions that combine pest control with plant nutrition and digital diagnostics. Barriers to entry remain moderate but are rising due to complex EU authorization processes and consumer interest in synthetic chemistry. As sustainability becomes non-negotiable, the competitive edge lies in scientific credibility, ecological safety,,y and seamless integration into the modern European gardener’s routine.

KEY MARKET PLAYERS

Key players in the Europe Garden Pesticides Market are

- Scotts Miracle-Gro

- Syngenta AG

- Spectrum Brands

- Bayer AG

- UPL Limited

- SC Johnson & Son

- BASF SE

- Sumitomo Chemical

- Andersons

- DuPont

- Monsanto.

Top Players In The Market

- BASF SE is a global leader in agricultural and home garden protection solutions with a strong footprint across Europe. The company offers a diversified portfolio of insecticides, es fungicides, and herbicides tailored for non-professional users under trusted brands such as Lizetan and Celaflor. BASF emphasizes sustainable innovation by developing bio-based formulations and low-dose delivery systems that align with EU regulatory standards. In recent years, the company has expanded its garden care segment through strategic partnerships with European retail chains and garden centers to enhance product visibility and consumer education. BASF launched a new line of ready-to-use biofungicides containing naturally derived active ingredients for home rose and vegetable gardens in Germany, France,e and the Netherlands. These initiatives reinforce its commitment to accessible, effective, and environmentally responsible pest management for European gardeners.

- Syngenta Group maintains significant influence in the Europe garden pesticides market through its consumer horticulture division, which delivers science-backed solutions for home use. The company markets products under well-recognized brands like Solabiol and Patch Magic that combine pest control with soil enhancement and seed technology. Syngenta actively supports urban greening initiatives and collaborates with national horticultural societies to promote integrated pest management practices among amateur gardeners. The company introduced a digital plant care assistant in partnership with a Swiss agritech startup, enabling users to identify pests and receive tailored treatment recommendations. Syngenta also accelerated regulatory submissions for microbial actives across Southern Europe to meet rising demand for organic alternatives. These efforts position Syngenta as a holistic garden wellness provider rather than a conventional pesticide supplier.

- UPL Limited has strategically expanded its presence in the Europe garden pesticides market by leveraging its global biocontrol expertise and sustainable chemistry platforms. The company offers a range of garden protection products under the Doff and BioProtection brand,s which are widely distributed in the United Kingdom and Benelux regions. UPL focuses on reformulating traditional actives intuser-friendlyly formats such as spray gels and granules that minimize environmental runoff. In 2024, the company inaugurated a dedicated garden care innovation lab in the Netherlands to developnext-generationn biopesticides derived from plant extracts and beneficial microbes. It also partnered with major European retailers to launch educational in-store displays on responsible pesticide use. Through these localized and sustainability-oriented actions, UPL strengthens its reputation as an agile and eco-conscious player in the residential horticulture space.

Top Strategies Used by the Key Market Participants

Key players in the Europe garden pesticides market prioritize the development of bio-based and low-risk formulations to comply with stringent EU regulations and meet consumer demand for sustainable solutions. They invest in user-friendly delivery formats such as ready-to-use sprays, granules, and gel applications that enhance safety and ease of use for non-professional gardeners. Companies actively collaborate with retail chains and garden centers to providein-storee education and product demonstrations that build consumer trust. Strategic partnerships with horticultural societies and digital agritech firms enable accurate pest identification and personalized treatment guidance. Additionally, they pursue accelerated regulatory pathways for microbial and botanical actives to expand their organic portfolios. These strategies collectively address regulatory compliance, consumer preference,s, and competitive differentiation in a rapidly evolving residential pest control sector.

MARKET SEGMENTATION

This research report on the European garden pesticides market size is segmented and sub-segmented into the following categories.

By Product Type

- Herbicide

- Insecticide

- Fungicide

- Other Pesticides

By Application

- Insect Control

- Insect Repellents

- Lawn and garden

- Public

- Private

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe garden pesticides market?

The Europe garden pesticides market includes chemical and biological products designed to control pests (insects, weeds, fungi, rodents) in domestic gardens, landscaping, recreational areas, and small-scale horticultural settings across European countries.

Why are garden pesticides used?

Garden pesticides help protect ornamental plants, lawns, flowers, and edible gardens from damage by pests and diseases, improve plant health, preserve aesthetic value, and maintain outdoor living spaces.

What drives growth in the Europe garden pesticides market?

Growth is driven by increasing urban gardening and landscaping activities, rising disposable incomes, greater consumer interest in outdoor living spaces, and the expansion of home gardening trends.

What types of pesticides are used in gardens?

Common garden pesticides include insecticides (for insect control), herbicides (weed killers), fungicides (disease control), rodenticides (rodent control), and biological/organic alternatives safe for home use.

How do garden pesticides benefit homeowners?

They help homeowners reduce pest damage, prevent weed overgrowth, manage fungal diseases, improve plant growth, and enjoy healthy lawns and gardens with minimal pest interference.

Are biological pesticides used in European gardens?

Yes. Biological and organic pesticides (microbial agents, botanical extracts, and eco-friendly formulations) are increasingly used due to environmental concerns, safety preferences, and organic gardening adoption.

How do regulations impact the garden pesticides market in Europe?

EU and national regulations restrict hazardous active ingredients, enforce safety labeling, govern allowable pesticide use, and promote reduced-risk and organic alternatives to protect human health and ecosystems.

Which pests are commonly controlled in gardens?

Garden pesticides are used against aphids, caterpillars, slugs/snails, ants, mites, broadleaf weeds, fungal diseases (mildew/rot), and rodents that damage plants and turf.

What safety precautions should gardeners take?

Home gardeners should follow label directions, wear protective gear, avoid application near water sources, restrict access by children/pets, and store products safely to reduce health and environmental risks.

What trends are shaping the Europe garden pesticides market?

Key trends include eco-friendly and organic pesticides, low-toxicity products, integrated pest management (IPM) for gardens, increased retail availability, and digital guidance for safe use.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com