Europe Gas Market Research Report By Sector (Upstream, Midstream, Downstream) Location of Deployment (Onshore, Offshore) & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of EU) - Industry Analysis From (2026 to 2034)

Europe Gas Market Size

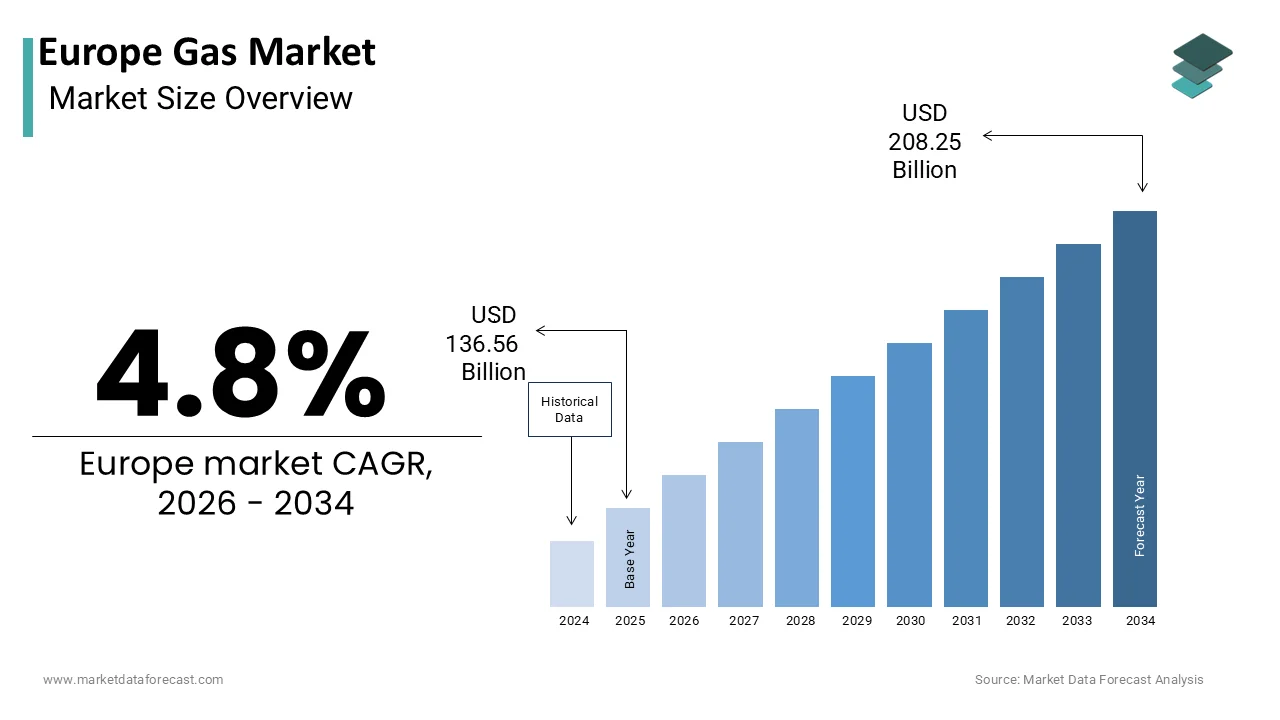

The Europe Gas Market Size was valued at USD 136.56 billion in 2025, is expected to have 4.8% CAGR from 2026 to 2034, and be worth USD 208.25 billion by 2034 from USD 143.12 billion in 2025.

TheEuropeane gas market encompasses the exploration, production, transportation, distribution, and consumption of natural gas across 44 countries, including major economies such as Germany, France, Italy, and the UK. A defining feature of the European gas market is its integration under the framework of the EU Internal Energy Market, which promotes cross-border trade, infrastructure interconnectivity, and regulatory harmonization. Moreover, technological advancements in underground storage, digital metering, and grid balancing are enhancing operational efficiency and flexibility.

MARKET DRIVERS

Transition from Coal-Fired Power Generation

One of the primary drivers behind the sustained relevance of the Europe gas market is the ongoing transition from coal-fired power generation to natural gas-based electricity production. As part of broader decarbonization efforts, several European countries have committed to phasing out coal due to its high carbon emissions and environmental impact. Natural gas emits up to 60% less carbon dioxide than coal when used for electricity generation, making it an attractive transitional fuel during the shift toward renewables. Countries such as Germany, the Netherlands, and Austria have actively replaced coal plants with gas-fired combined cycle power stations to meet interim emission reduction targets. Additionally, regulatory mechanisms such as the EU Emissions Trading System (EU ETS) have made coal less economically viable by increasing the cost of carbon allowances.

Expansion of Liquefied Natural Gas (LNG) Infrastructure

Another key driver shaping the Europe gas market is the rapid expansion of liquefied natural gas (LNG) import infrastructure, which has significantly altered the region’s gas supply dynamics. Historically reliant on Russian pipeline gas, European countries have accelerated investments in LNG terminals to enhance energy security and reduce geopolitical exposure. According to the International Energy Agency, LNG accounted for over 40% of total gas imports into Europe in late 2023, reflecting a dramatic shift in sourcing strategies. Moreover, global LNG suppliers such as Qatar, the United States, and Nigeria have ramped up deliveries to Europe, attracted by strong demand and competitive pricing. As per data from Eurogas, European LNG imports surged by 65% in 2023 compared to 2021, ensuring a more diversified and resilient gas supply chain.

MARKET RESTRAINTS

Policy Push Toward Renewable Energy and Decarbonization Targets

A significant restraint affecting the Europe gas market is the accelerating policy push toward renewable energy deployment and deep decarbonization targets set by the European Union and individual member states. Under the European Green Deal, the EU aims to achieve climate neutrality by 2050, necessitating a drastic reduction in fossil fuel consumption, including natural gas. Several national governments have introduced aggressive phase-out timelines for gas-powered heating systems and power plants. For instance, the Netherlands plans to eliminate natural gas from residential heating by 2040, which is replacing it with district heating and heat pumps. Similarly, France has announced restrictions on new gas-fired power plant construction unless they incorporate carbon capture technologies. Moreover, financial institutions are reducing lending support for new gas infrastructure projects. These evolving policy landscapes pose a fundamental challenge to the future viability of the Europe gas market, which is compelling industry players to explore low-carbon alternatives such as green hydrogen and biomethane.

Volatility in Global Gas Prices and Supply Uncertainties

Another major constraint impacting the Europe gas market is the volatility in global gas prices and persistent uncertainties surrounding supply availability. Unlike oil, which is traded globally through well-established benchmarks, natural gas markets remain fragmented, which is leading to price fluctuations influenced by geopolitical events, weather conditions, and infrastructure disruptions. This instability creates challenges for both consumers and industrial users who rely on predictable energy costs for budgeting and investment planning. In 2023, several manufacturing sectors, including chemicals, steel, and glass,s reported reduced production levels due to elevated gas prices, highlighting the economic repercussions of market volatility. Furthermore, supply uncertainty persists despite increased LNG imports and domestic production from Norway and the Netherlands. Long-term LNG contracts are often linked to oil prices or subject to geopolitical risks, complicating procurement strategies for European buyers. Additionally, aging infrastructure and limited storage capacity in some regions exacerbate seasonal supply pressures during the winter months when demand peaks.

MARKET OPPORTUNITIES

Development of Hydrogen-Ready Gas Infrastructure

A major opportunity emerging in the European gas market is the development of hydrogen-ready infrastructure, positioning natural gas networks as a crucial enabler of the continent’s clean energy transition. Recognizing the potential of hydrogen as a zero-emission energy carrier, European regulators and industry stakeholders are investing in retrofitting existing gas pipelines, storage facilities, and distribution systems to accommodate hydrogen blends and eventually pure hydrogen.

According to the European Hydrogen Backbone initiative, over 70% of the EU’s existing gas transmission network could be repurposed for hydrogen transport by 2040. Several pilot projects are already underway, including the HyPipe project in Germany and the H2SouthWest initiative in the UK, which aim to test hydrogen blending in residential and industrial applications.

Growth of Biogas and Renewable Gas Production

An expanding opportunity within the Europe gas market is the rapid growth of biogas and renewable gas production by offering a sustainable alternative to conventional fossil-based natural gas. Biogas, primarily derived from organic waste, agricultural residues, and wastewater treatment, is being upgraded to biomethane and injected into the existing gas grid by enabling seamless integration with current infrastructure. Government incentives and regulatory support have been instrumental in driving this trend. The Renewable Energy Directive II (RED II) mandates that at least 42.5% of energy consumed in transport must come from renewable sources by 2030, by encouraging the adoption of biomethane in road and maritime transport. Moreover, corporate demand for carbon-neutral energy solutions is rising. Major industrial players, including Unilever, Nestlé, and BMW, have signed long-term contracts to procure renewable gas for their European operations by aligning with sustainability commitments.

MARKET CHALLENGES

Geopolitical Risks and Energy Security Concerns

A critical challenge facing the Europe gas market is the heightened geopolitical risk and lingering concerns over energy security in light of recent disruptions to traditional supply routes. Historically dependent on Russian pipeline gas, Europe has had to rapidly reconfigure its gas sourcing strategy following the reduction of flows via Nord Stream and other major conduits. According to the European Commission, before 2022, which is approximately 40% of the EU’s gas imports originated from Russia by leaving many countries exposed to supply shocks and political leverage. In response, European nations have sought alternative suppliers, including Qatar, the United States, and African exporters such as Nigeria and Algeria. However, securing long-term contracts and infrastructure remains a complex task. Additionally, regional tensions continue to influence market stability. Conflicts in Eastern Europe, coupled with sanctions and countermeasures, have led to unpredictable shifts in pricing and availability.

Aging Infrastructure and Need for Modernization

Another pressing challenge confronting the Europe gas market is the aging infrastructure that underpins gas transportation, storage, and distribution across the continent. Many of the region's gas pipelines were constructed decades ago and require substantial investment to ensure reliability, safety, and compatibility with emerging energy vectors such as hydrogen and biomethane. The need for modernization extends beyond pipelines to include underground storage facilities, compressor stations, and digital monitoring systems. In 2023, the European Commission highlighted that gas storage utilization rates dropped below historical averages due to technical constraints and insufficient investment in facility upgrades. Moreover, the integration of hydrogen-ready components into existing networks requires extensive retrofitting, posing both technical and financial hurdles. While pilot projects are underway in Germany, the Netherlands, and France, widespread implementation will take years and depend on regulatory clarity and investor confidence.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Sector, Location of Deployment, and Country. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, Germany, Italy, France, Spain, Sweden, Denmark, Poland, Switzerland, the Netherlands, and the rest of Europe. |

| Market Leaders Profiled | Shell, BP, TotalEnergies, Equinor, Eni, OMV, Gazprom, Uniper |

SEGMENT ANALYSIS

By Sector Insights

The downstream segment was the largest and held 46.3% of the Europe gas market share in 2025. One of the primary drivers behind its dominance is the extensive use of natural gas for heating and electricity production, particularly in countries with colder climates such as Germany, France, and the UK. According to Eurostat, nearly 40% of European households rely on gas for space heating, ensuring consistent demand throughout the year. Additionally, the industrial sector remains a major consumer of natural gas, especially in energy-intensive industries like chemicals, glass, and steel manufacturing.

The midstream segment is likely to grow with a CAGR of 7.8% during the forecast period. This rapid expansion reflects the urgent need for enhanced transportation and storage infrastructure following the disruption of traditional Russian supply routes. The significant investment in liquefied natural gas (LNG) import terminals and regasification facilities is also to fuel the growth of the segment. Countries such as Germany, Poland, and Spain have accelerated the development of LNG infrastructure to diversify their gas sourcing strategies. Furthermore, cross-border interconnector projects are being fast-tracked to enhance regional gas flow resilience. Storage infrastructure is also undergoing modernization. According to Gas Infrastructure Europe, underground gas storage utilization increased by 18% in 2023 compared to previous years, driven by policy mandates requiring higher reserve levels.

By Location of Deployment Insights

The onshore segment was the largest by occupying 60.1% of the Europe gas market share in 2025. One of the key factors driving the onshore segment is the continued reliance on domestic production from conventional sources. Countries such as the Netherlands, Germany, and the UK have historically been major onshore gas producers, with the Groningen field in the Netherlands serving as one of Europe’s largest reserves until its phased shutdown in 2023. Moreover, smaller-scale onshore gas developments, including unconventional sources such as coal bed methane and tight gas, are gaining traction in Eastern Europe. In Poland, exploration for shale gas has intensified despite technical and regulatory challenges, as noted by the Polish Geological Institute. In addition, onshore gas infrastructure offers greater accessibility for maintenance and upgrades, making it more adaptable to evolving energy policies.

The offshore segment is likely to experience a CAGR of 9.3% in the coming years. This acceleration is driven by increasing exploration and production activities in the North Sea, Norwegian Continental Shelf, and emerging deepwater basins in the Mediterranean and Black Sea. A primary factor behind this surge is Norway’s expanding offshore gas production, which continues to serve as a cornerstone for European energy security. Additionally, advancements in subsea technology and floating production systems have made previously uneconomical reserves viable. Companies like Equinor, Shell, and TotalEnergies have deployed digital monitoring tools and autonomous drilling solutions to improve efficiency and reduce operational risks. Another key driver is the growing interest in carbon capture and storage (CCS) projects linked to offshore platforms. Initiatives such as the Northern Lights project in the North Sea are repurposing depleted gas fields for CO₂ sequestration, aligning offshore operations with climate neutrality goals.

COUNTRY LEVEL ANALYSIS

Germany was the top performer in the European gas market by accounting for 18.3% of share in 2025. A key driver of Germany’s dominant position is its high industrial gas consumption, particularly in chemical, automotive, and steel manufacturing sectors. To mitigate risks associated with past reliance on Russian pipeline gas, Germany has rapidly expanded its LNG import infrastructure. In 2023, the country commissioned three floating LNG terminals, enhancing its ability to secure diversified supply sources. Additionally, Germany is investing heavily in hydrogen-ready gas infrastructure, positioning itself as a leader in the transition to low-carbon gases. National hydrogen strategy initiatives include retrofitting pipelines and developing large-scale electrolyzer facilities by ensuring the long-term relevance of the gas sector in a decarbonized energy system.

The United Kingdom was positioned second with 13.2% of the Europe gas market share in 2025. A major factor influencing the UK gas market is its heavy reliance on gas-fired power generation. As per National Grid ESO, natural gas provided nearly 40% of electricity generation in 2023 by ensuring continued demand despite rising renewable penetration. Seasonal variations in wind availability further reinforce the necessity of a flexible gas supply to maintain grid stability. Despite government commitments to net-zero emissions by 2050, gas remains integral to heating and industrial applications. Ongoing investments in hydrogen blending trials and carbon capture technologies indicate a strategic effort to sustain the gas sector while aligning with long-term decarbonization objectives.

The Italian gas market is likely to grow with a major transit hub and importer. According to the Italian Ministry of Ecological Transition, natural gas fulfills nearly 40% of Italy’s total energy needs by underpinning its significance in both power generation and residential heating.

A key driver of Italy’s gas market is its extensive pipeline connectivity with North Africa and Eastern Europe. The Trans Adriatic Pipeline (TAP), part of the Southern Gas Corridor initiative, delivers Azerbaijani gas directly to Italy, enhancing diversification beyond traditional Russian supplies. Italy is also advancing plans for hydrogen and biomethane integration. The National Hydrogen Strategy outlines ambitions to convert portions of the existing gas grid for hydrogen transport and storage, supporting the broader transition toward cleaner energy vectors and reinforcing Italy’s influence in shaping the future of the European gas market.

France commands approximately 10% of the Europe gas market, maintaining a significant but relatively smaller role compared to other major economies due to its strong nuclear-based electricity generation mix. However, gas remains essential for industrial and residential applications. Nearly 12 million French households rely on gas for heating, particularly in northern and eastern regions where winters are harsher. France is also strengthening its LNG import capabilities to enhance supply security. Furthermore, France is prioritizing biomethane and green hydrogen as transitional fuels. Investments in biogas upgrading facilities and pilot hydrogen injection projects reflect a forward-looking approach that integrates gas into a sustainable energy framework.

The Netherlands gas market growth is likely to grow in the coming years. However, production from this field was officially halted in 2023 due to seismic activity concerns, marking a significant shift in the country’s gas dynamics. The country hosts major gas trading hubs such as Title Transfer Facility (TTF), which has become the continent’s primary gas pricing benchmark. Additionally, the Netherlands is leading in hydrogen readiness. Projects such as HyStock and NortH2 are focused on converting depleted gas fields into hydrogen storage sites, leveraging existing underground assets for clean energy applications.

Spain's gas market growth is likely to grow with prominent growth during the forecast period. A primary growth driver is Spain’s geographic advantage in accessing Algerian and Nigerian gas supplies via pipeline and sea routes. The Medgaz and Galsi pipelines facilitate direct connections to North Africa, offering a reliable alternative to Eastern European supply constraints.

COMPETITIVE LANDSCAPE

The competition in the European gas market is intensifying as traditional energy firms, national utilities, and emerging clean energy players vie for influence in a rapidly transforming sector. While historically dominated by state-backed producers and integrated oil majors, the landscape is now being reshaped by regulatory pressures, geopolitical shifts, and the push for decarbonization. Established players such as Shell, TotalEnergies, and Equinor are adapting by modernizing infrastructure, securing alternative LNG supplies, and incorporating hydrogen and biomethane into their portfolios. At the same time, national gas operators and regional suppliers are strengthening their positions through strategic alliances, digitalization, and investment in smart grid technologies.

New entrants specializing in renewable gas and hydrogen are also gaining traction, challenging incumbents with innovative business models and lower-emission offerings. Governments and regulators further influence the competitive environment through policy incentives, infrastructure mandates, and cross-border market integration efforts. In this evolving context, only those companies that can balance reliability, sustainability, and adaptability will be able to maintain long-term relevance and prominence in the European gas market.

KEY MARKET PLAYERS

Companies playing a prominent role in the European Gas Market are

- Shell,

- BP,

- TotalEnergies,

- Equinor,

- Eni,

- OMV,

- Gazprom,

- Uniper,

- Engie,

- RWE,

- VNG,

- Naturgy,

- Repsol,

- PGNiG,

- Wintershall Dea,

- Enagas,

- Fluxys,

- Gascade,

- Snam.

Top Players in the Market

Royal Dutch Shell is a leading player in the Europe gas market, leveraging its extensive upstream, midstream, and downstream capabilities to maintain a dominant presence. The company plays a crucial role in LNG supply chain development, operating major import terminals and trading platforms that support Europe’s energy security. Shell’s strategic focus on decarbonization includes investments in carbon capture, hydrogen blending, and biomethane projects, positioning it at the forefront of the gas industry’s transition toward sustainability. Its global reach and technological expertise make it a key influencer in shaping future gas markets beyond Europe.

TotalEnergies

TotalEnergies has established itself as a major force in the Europe gas market by combining traditional gas operations with forward-looking clean energy strategies. The company is actively involved in securing long-term LNG supply contracts, developing underground storage solutions, and integrating renewable gases into existing infrastructure. TotalEnergies is also investing heavily in hydrogen and biomethane production, aiming to align its gas portfolio with European climate goals. Through partnerships and digital innovations, it enhances operational efficiency and strengthens its position across the entire gas value chain, reinforcing its influence both regionally and globally.

Equinor

Equinor, formerly Statoil, is a key player in the Europe gas market in offshore production from the North Sea. As Norway’s largest energy company, Equinor supplies a significant portion of Europe’s natural gas through secure pipeline networks and flexible LNG exports. The company is pioneering the integration of carbon capture and storage (CCS) with gas production, setting new benchmarks for low-carbon gas operations. By repurposing depleted fields for hydrogen storage and blue gas production, Equinor is redefining the role of gas in a net-zero future, which is making it a model for sustainable gas.

Top strategies used by the key market participants

Expansion of LNG Infrastructure and Supply Chain Integration

Major players in the Europe gas market are aggressively expanding liquefied natural gas (LNG) infrastructure to diversify supply sources and reduce dependence on traditional pipeline imports. This includes investments in floating storage and regasification units, terminal expansions, and long-term procurement agreements with global suppliers to ensure flexibility and resilience in gas supply.

Development of Hydrogen-Ready Gas Assets

Leading companies are retrofitting existing gas pipelines, storage facilities, and distribution networks to accommodate hydrogen blends and prepare for full hydrogen conversion. This strategy enables them to align with EU decarbonization targets while preserving the value of their existing infrastructure in a post-fossil fuel era.

Strategic Partnerships for Carbon Capture and Renewable Gas Integration

To enhance sustainability credentials and comply with tightening emissions regulations, key players are forming strategic alliances focused on carbon capture and storage (CCS), biomethane production, and synthetic gas development. These collaborations aim to decarbonize gas operations and integrate cleaner alternatives into mainstream energy systems.

RECENT HAPPENINGS IN THE MARKET

- In March 2025, Shell announced a strategic partnership with a German utility to develop a hydrogen-ready gas transmission network across northern Europe. This initiative was designed to facilitate the gradual replacement of fossil-based gas with low-carbon alternatives while ensuring continuity of supply and grid stability.

- In July 2025, TotalEnergies secured exclusive rights to develop an underground hydrogen storage facility in France, utilizing depleted gas fields to store large volumes of clean hydrogen. This move was intended to support the country's hydrogen mobility and industrial decarbonization strategies, reinforcing TotalEnergies’ dominance in the emerging hydrogen economy.

- In October 2025, Equinor launched a pilot project in collaboration with Danish and German partners to transport captured CO₂ from industrial hubs to offshore storage sites beneath the North Sea. This initiative supports the broader deployment of carbon capture and blue hydrogen initiatives across Europe, enhancing Equinor’s role in sustainable gas solutions.

- In January 2025, Eni finalized an agreement to acquire a biogas production company based in Italy, expanding its renewable gas portfolio and enabling direct injection of biomethane into the national grid. This acquisition was aimed at strengthening Eni’s position in the green gas segment and meeting rising demand from environmentally conscious consumers.

- In March 2025, Wintershall Dea initiated a joint venture with a Polish energy firm to explore unconventional gas reserves in Eastern Europe, focusing on enhanced recovery techniques and environmental safeguards. This move was intended to bolster regional gas self-sufficiency and provide an alternative to imported supplies, reinforcing Wintershall Dea’s strategic footprint in the evolving Europe gas market.

MARKET SEGMENTATION

This research report on the europe gas market has been segmented and sub-segmented into the following categories.

By Sector

- Upstream

- Midstream

- Downstream

By Location of Deployment

- Onshore

- Offshore

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe.

Frequently Asked Questions

What role does LNG play in Europe’s gas supply?

LNG (Liquefied Natural Gas) now plays a critical role, making up over 30% of Europe’s gas imports. It allows diversification of suppliers, especially since Russian pipeline gas volumes have drastically reduced.

How does Europe store natural gas for winter?

Europe uses underground gas storage facilities, typically filling them during summer when demand is low. The EU mandates a minimum storage fill level (e.g., 90% by November) to ensure winter security.

Is Europe still importing gas from Russia?

Yes, but at much lower levels. Russian pipeline flows via Ukraine and Turkey continue in smaller volumes, while some Russian LNG still reaches Europe. The EU is working to phase this out further.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com