Europe Gas Turbine Market Size, Share, Trends, & Growth Forecast Report Segmented By Technology (Open Cycle and Combined Cycle), Capacity, End-Use, Application, Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2024 to 2033

Europe Gas Turbine Market Size

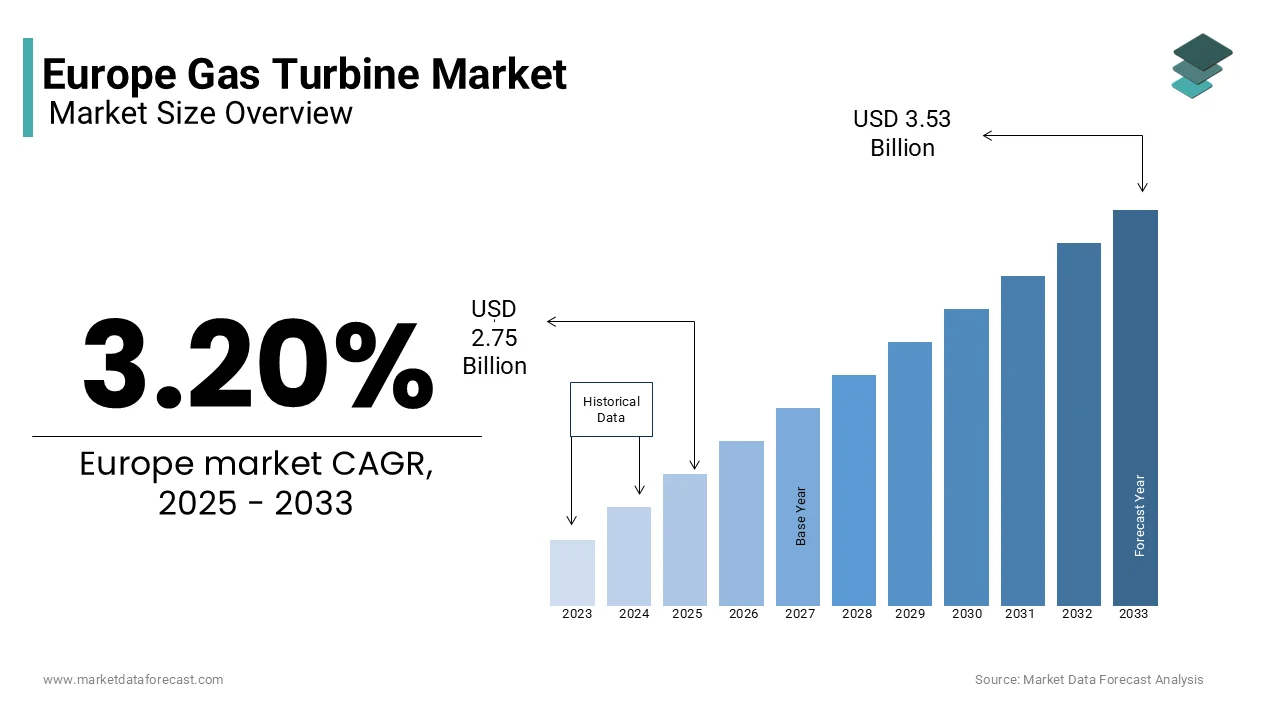

The Europe gas turbine market, valued at USD 2.66 billion in 2024, is projected to grow to USD 3.53 billion by 2033, increasing from USD 2.75 billion in 2025 at a CAGR of 3.20% between 2025 and 2033.

The Europe gas turbine market has emerged as a cornerstone of the region’s energy transition, driven by the growing demand for cleaner and more efficient power generation solutions. A significant factor shaping the market is the increasing integration of renewable energy sources. As per the International Energy Agency (IEA), renewable energy capacity in Europe grew by 15% in 2023 by necessitating flexible gas turbines to balance grid stability. Additionally, government subsidies and private investments have amplified adoption by positioning gas turbines as a key player in Europe’s clean energy infrastructure.

MARKET DRIVERS

Transition to Cleaner Energy Sources

The transition to cleaner energy sources is a cornerstone driving the Europe gas turbine market. According to the European Commission, natural gas-powered turbines produce 50% less carbon dioxide compared to coal-fired plants by making them an attractive interim solution during the energy transition. These systems enable utilities to reduce emissions while maintaining grid reliability in countries like Germany and France. A pivotal factor amplifying this growth is the emphasis on combined-cycle gas turbines (CCGT). As per a report by Statista, CCGT systems achieved an efficiency rate of 60% in 2023 by surpassing traditional open-cycle designs. For instance, Siemens Energy installed over 10 GW of CCGT capacity across Europe, reducing carbon emissions by 30 million tons annually. These innovations not only enhance sustainability but also align with EU decarbonization goals.

Integration with Renewable Energy Grids

The integration of gas turbines with renewable energy grids is significantly bolstering market growth. According to Frost & Sullivan, investments in hybrid energy systems grew by 25% in 2023 with the partnerships between governments and private sector players. Gas turbines play a vital role in managing variable energy flows from wind and solar sources by ensuring grid stability and energy security. For example, a study by Accenture, gas turbines reduced curtailment losses by 40% in 2023 by enabling efficient energy utilization. Additionally, collaborations with renewable energy developers have expanded functionality, enabling seamless integration with wind farms and solar parks. These factors collectively drive the adoption of gas turbines by positioning them as essential components of Europe’s sustainable energy ecosystem.

MARKET RESTRAINTS

High Initial Costs and Maintenance Expenses

One of the primary barriers impeding the growth of the Europe gas turbine market is the high initial cost and ongoing maintenance expenses associated with advanced systems. According to Deloitte, setting up a combined-cycle gas turbine system can cost up to €1 million per megawatt by deterring smaller utilities and industrial players from adopting cutting-edge technologies.

Additionally, maintenance costs remain a concern, particularly for aging fleets. According to a report by PwC, 40% of European operators cited budget constraints as a barrier to upgrading their turbine infrastructure in 2023. While larger corporations can absorb these expenses, smaller operators often struggle to justify the investment by creating a fragmented market landscape. This issue undermines the pace of technological adoption and limits overall market growth.

Competition from Alternative Technologies

Intense competition from alternative technologies poses another significant restraint for the Europe gas turbine market. According to Capgemini, emerging solutions such as hydrogen fuel cells and solid oxide fuel cells are gaining traction in research and pilot projects. These alternatives offer advantages like higher efficiency and lower environmental impact by threatening the dominance of traditional gas turbines. For instance, a study by KPMG reveals that hydrogen-based systems captured 10% of the power generation market share in 2023 owing to their superior performance in low-carbon applications. The rapid pace of technological disruption underscores the need for continuous adaptation and differentiation while innovation in materials and designs can mitigate this challenge.

MARKET OPPORTUNITIES

Growth of Industrial Applications

The rapid growth of industrial applications presents a transformative opportunity for the Europe gas turbine market. These systems enable efficient power generation by reducing reliance on grid electricity and lowering operational costs. According to a report by McKinsey, gas turbines reduced energy costs by 25% in 2023 by making them an attractive choice for large-scale operations. Additionally, government incentives promoting industrial electrification have amplified adoption, solidifying gas turbines’ role in modernizing operations. These innovations not only improve sustainability but also align with EU Green Deal objectives.

Expansion into Hydrogen-Powered Turbines

The expansion into hydrogen-powered turbines offers another promising avenue for growth in the Europe gas turbine market. Gas turbines designed for hydrogen combustion ensure safe and efficient energy transfer by reducing carbon emissions by 90%. The hydrogen-powered turbines gained significant traction in 2023 owing to their ability to handle variable loads and integrate with renewable energy sources. These systems are indispensable for urban mobility initiatives, such as those in Paris and Berlin, where space constraints necessitate compact designs. These advancements not only drive revenue but also position gas turbines as a cornerstone of Europe’s sustainable transportation ecosystem.

MARKET CHALLENGES

Technological Limitations and Efficiency Concerns

Technological limitations and efficiency concerns represent a significant challenge for the Europe gas turbine market. This limitation is particularly evident in open-cycle designs, which require expensive upgrades to match the performance of combined-cycle systems. For example, a report by ABB reveals that efficiency-related issues delayed the deployment of large-scale turbine projects by 12 months in 2023 in high-pressure applications.

Regulatory Uncertainty and Policy Shifts

The regulatory uncertainty and policy shifts pose another pressing challenge for the Europe gas turbine market. According to PwC, over 70% of manufacturers face challenges in adapting to evolving EU regulations, particularly those mandating the use of eco-friendly materials and designs. These regulations complicate product development by raising production costs and slowing market progress.

For instance, a study by KPMG has revealed that the compliance-related delays reduced turbine production by 15% in 2023 for systems using natural gas. Addressing these concerns requires significant investments in research and development, which may not be feasible for all stakeholders, slowing market progress.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

3.20% |

|

Segments Covered |

By Technology, Capacity, End-Use, Application, and Country |

|

Various Analyses Covered |

Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and Rest of Europe |

|

Market Leaders Profiled |

Ansaldo Energia, GE Aerospace, Kawasaki Heavy Industries Ltd, ManpowerGroup Inc, Mitsubishi Corp, Opera Ltd ADR, Siemens AG, and Caterpillar Inc. |

SEGMENTAL ANALYSIS

By Technology Insights

The Combined cycle segment dominated the Europe gas turbine market by capturing 65.6% of the total share in 2024 owing to its superior efficiency and ability to integrate with renewable energy sources by making it indispensable for power utilities.

A key factor fueling this dominance is the emphasis on reducing carbon emissions. According to the IEA, combined-cycle systems reduced CO2 emissions by 30% in 2023 by ensuring compliance with stringent EU regulations. Additionally, advancements in modular designs have improved scalability and cost-effectiveness that further solidifies the segment’s prominence.

The open cycle segment is likely to gain huge traction with a projected CAGR of 7.2% during the forecast period. This growth is fueled by the increasing demand for flexible and cost-effective solutions in industrial applications. The open-cycle systems gained significant traction in 2023 with their ease of installation and maintenance. These systems are particularly valuable for remote locations byenabling rapid deployment without significant upfront costs.

By End-Use Insights

The Power & utility was the largest in the Europe gas turbine market and held 43.2% of the share in 2024. The rising demand for the grid stability is driving the growth of the segment. According to the European Network of Transmission System Operators for Electricity (ENTSO-E), gas turbines reduced grid instability by 25% in 2023 by ensuring consistent energy supply.

The industrial segment is lucratively growing with a CAGR of 8.5% during the forecast period. This growth is fueled by the increasing adoption of gas turbines for on-site power generation by reducing reliance on grid electricity. These systems are particularly valuable for sectors like oil and gas, enabling efficient energy management.

By Application Insights

The power generation segment was accounted in holding a significant share of the Europe gas turbine market in 2024. The growth of the segment is driven by growing demand for reliable and efficient electricity production in urbanized regions like Germany, France, and the UK. A key factor fueling this dominance is the integration of gas turbines with renewable energy grids. According to the European Commission, gas turbines reduced curtailment losses from wind and solar sources by 40% in 2023 by ensuring grid stability and energy security. Additionally, government subsidies promoting cleaner energy solutions have amplified adoption with the segment’s prominence. A report by PwC, combined-cycle systems accounted for 70% of power generation installations in 2023.

The oil & gas segment is emerging with an estimated CAGR of 9.2% from 2025 to 2033. This growth is fueled by the increasing adoption of gas turbines for upstream and midstream operations in remote locations. The investments in gas turbines for oil & gas applications grew by 35% in 2023 is driven by their ability to provide on-site power generation. These systems are particularly valuable for offshore platforms by enabling efficient energy management while reducing operational costs. Additionally, collaborations with oil majors have expanded functionality that is by enabling seamless integration with existing infrastructure.

REGIONAL ANALYSIS

Germany was the largest contributor for the Europe gas turbine market with a share of 22.3% in 2024. The country’s growth is driven by its robust industrial base and commitment to renewable energy integration owing to the initiatives like the Energiewende policy. A pivotal factor fueling this dominance is the growing emphasis on grid stability. According to the German Energy Agency (DENA), gas turbines reduced grid instability by 30% in 2023 by creating a surge in demand for advanced systems.

The UK gas turbine market is likely to gain huge traction with projected CAGR of 11.6% during the forecast period. London and Manchester have emerged as critical hubs owing to a robust investment in renewable energy and urban electrification. The transition to net-zero emissions has significantly bolstered demand. As per the UK Climate Change Committee, renewable energy capacity grew by 20% in 2023 owing to the advanced gas turbine systems to manage variable energy flows. Additionally, government funding for EV charging infrastructure has expanded adoption by reinforcing the UK’s prominence in sustainable energy solutions.

France is likely to grow with a dominant growth opportunity in the next coming years. Paris has emerged as a key player by hosting major renewable energy projects and innovation centers.

A major driver of this growth is the increasing adoption of nuclear and renewable energy sources. According to the French Ministry of Energy, over 40% of the country’s electricity is generated from nuclear power that is by requiring reliable gas turbine systems to ensure seamless energy distribution. Additionally, urbanization initiatives have amplified demand for low-voltage solutions in commercial and residential sectors.

Italy gas turbine market is likely to have steady pace in the next coming years. Milan and Rome are rapidly emerging as key hubs owing to growing emphasis on renewable energy integration.

A key factor driving Italy’s growth is the increasing adoption of solar energy. According to the Italian National Agency for New Technologies, solar capacity grew by 25% in 2023 is creating demand for efficient gas turbine solutions. Additionally, government subsidies supporting industrial electrification have expanded adoption by ensuring scalability and safety.

Spain gas turbine market is anticipated to have steady growth pace in the next coming years. Barcelona and Madrid lead the charge by hosting major renewable energy projects and innovation centers. A pivotal driver of Spain’s growth is the rapid expansion of wind energy infrastructure. According to the Spanish Wind Energy Association, wind farms accounted for 25% of the country’s electricity generation in 2023 owing to the robust gas turbine systems to manage high loads. Additionally, collaborations with private sector players have expanded functionality by enabling seamless integration with national grids.

KEY MARKET PLAYERS

The major players in the Europe gas turbine market include Ansaldo Energia, GE Aerospace, Kawasaki Heavy Industries Ltd, ManpowerGroup Inc, Mitsubishi Corp, Opera Ltd ADR, Siemens AG, and Caterpillar Inc.

TOP 3 PLAYERS IN THE MARKET

Siemens Energy

Siemens Energy is a global leader in the gas turbine market by playing a pivotal role in shaping the Europe segment. The company offers a comprehensive portfolio of open-cycle and combined-cycle systems tailored to diverse applications. Its focus on sustainability and innovation has positioned it as a trusted partner for utilities and industrial operators. Siemens ensures widespread adoption while maintaining compliance with stringent EU regulations by leveraging partnerships with governments and renewable energy developers.

General Electric (GE)

General Electric specializes in advanced gas turbine technologies, emphasizing efficiency and scalability. The company’s HA-series turbines are widely adopted in power generation and industrial applications, enabling efficient energy management. GE’s commitment to sustainability aligns with EU Green Deal objectives, earning it a loyal customer base. Collaborations with tech startups have expanded functionality.

Mitsubishi Heavy Industries (MHI)

Mitsubishi Heavy Industries is renowned for its cutting-edge gas turbine systems in high-pressure and high-temperature applications. The company’s focus on modular designs and eco-friendly materials has made it a leader in power utilities. MHI delivers superior performance while reducing environmental impact by integrating AI-driven analytics.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Emphasis on Sustainability

Leading players in the Europe gas turbine market have embraced sustainability as a core strategy to enhance their competitive edge. For instance, the development of hydrogen-compatible turbines has resonated with environmentally conscious consumers. These initiatives not only align with EU regulations but also foster brand loyalty among stakeholders prioritizing green solutions.

Investment in R&D

Investments in research and development are a cornerstone strategy for staying ahead in the market. Companies focus on developing advanced turbine systems with higher efficiency and lower costs to address evolving customer needs. This approach allows them to tackle challenges such as grid modernization while maintaining its dominance in technological advancements.

Geographic Expansion

Expanding into emerging markets within Europe, such as Eastern Europe and Scandinavia, has become a priority for key players. By establishing localized services and partnerships, companies can better serve regional demands while capitalizing on favorable regulatory frameworks. This strategy ensures sustained growth amid intensifying competition.

COMPETITIVE LANDSCAPE

The Europe gas turbine market is characterized by intense competition owing to the presence of global giants and regional innovators vying for market share. Major players like Siemens Energy, General Electric, and Mitsubishi Heavy Industries dominate the landscape by leveraging their extensive expertise in energy infrastructure solutions. However, the market also features niche players specializing in renewable energy integration and hybrid systems is creating a fragmented yet dynamic ecosystem.

Technological innovation is a key battleground, with companies investing heavily in IoT, AI, and blockchain to differentiate themselves. According to McKinsey, over 60% of European enterprises prioritize secure and scalable gas turbine solutions, intensifying competition among providers to offer cutting-edge technologies. Additionally, stringent EU regulations mandating sustainability have forced companies to innovate responsibly.

Mergers and acquisitions are another hallmark of the competitive landscape. Larger firms acquire smaller innovators to expand their product portfolios and geographic reach. Meanwhile, price wars and aggressive marketing strategies are common, particularly in saturated markets like Germany and the UK. Despite these challenges, the market remains ripe for growth, with opportunities in emerging segments such as hydrogen-powered turbines driving future competition.

RECENT HAPPENINGS IN THE MARKET

- In March 2024, Siemens Energy partnered with the German government to develop hydrogen-compatible gas turbines, enhancing its position in low-carbon energy solutions. This initiative aims to reduce carbon emissions while improving grid reliability.

- In June 2023, General Electric launched its next-generation HA-series turbine in France, designed to achieve 64% efficiency. This move underscores the company’s commitment to technological innovation.

- In September 2023, Mitsubishi Heavy Industries acquired a Swedish startup specializing in modular turbine designs, expanding its portfolio of advanced technologies. This acquisition strengthens Mitsubishi’s prominence in high-pressure applications.

- In January 2024, Ansaldo Energia introduced a compact gas turbine system in Italy, targeting industrial applications. This launch positions Ansaldo as a leader in scalable energy solutions.

- In November 2023, MAN Energy Solutions unveiled its hybrid energy platform in Spain, integrating gas turbines with renewable energy sources. This initiative enhances mobility applications while addressing space constraints in urban areas.

MARKET SEGMENTATION

This research report on the European gas turbine market is segmented and sub-segmented into the following categories.

By Technology

- Open Cycle

- Combined Cycle

By Capacity

- Greater than equal to 200 MW

- >200 MW

By End-Use

- Power & Utility

- Industrial

By Application

- Oil & Gas

- Power Generation

- Marine

- Aerospace

- Process Plants

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What are the key factors driving the Europe gas turbine market?

The market is driven by increasing power demand, a shift towards cleaner energy sources, advancements in gas turbine technology, and government regulations supporting low-carbon power generation.

What types of gas turbines are most commonly used in Europe?

Heavy-duty gas turbines and aeroderivative gas turbines are the most common, with heavy-duty models being preferred for power plants and aeroderivative ones used for industrial and mobile applications.

What are the latest technological advancements in the Europe gas turbine market?

Advancements include higher efficiency models, hydrogen-ready turbines, digital monitoring systems, and lower-emission combustion technologies.

What is the future outlook for the gas turbine market in Europe?

The market is expected to evolve with a focus on efficiency, hydrogen integration, and hybrid power solutions, ensuring gas turbines remain relevant in the energy transition.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]