Europe Gemstones Market Size, Share, Trends And Growth Forecasts Research Report, Segmented By Nature, Type, Product, End Use and Region - Industry Analysis (2026 to 2034)

Europe Gemstones Market Report Summary

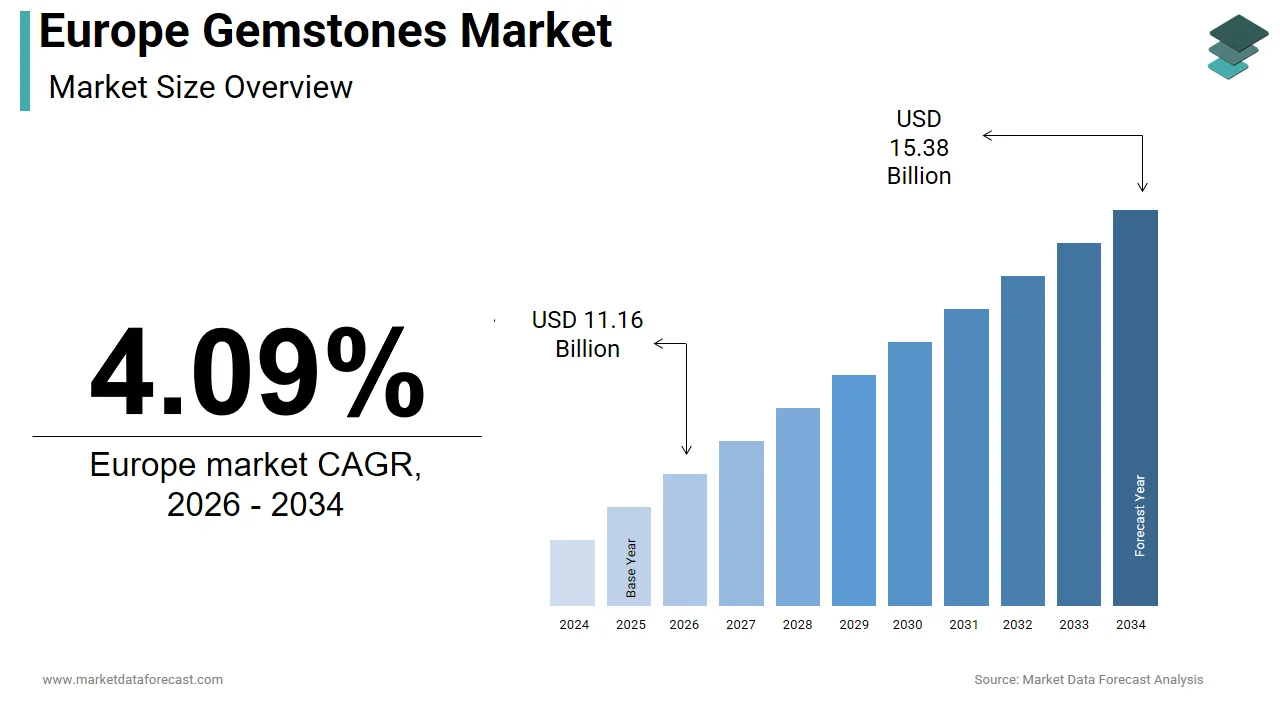

The European gemstones market was valued at USD 10.72 billion in 2025, is estimated to reach USD 11.16 billion in 2026, and is projected to reach USD 15.38 billion by 2034, growing at a CAGR of 4.09% from 2026 to 2034. The growth of the European gemstones market is driven by rising demand for fine jewelry, increasing consumer preference for luxury and customized ornaments, and growing awareness of gemstone investment value. Moreover, Europe’s established presence of leading jewelry houses and a growing inclination toward ethically sourced and certified gemstones continue to fuel the market expansion.

Key Market Trends

- The increasing popularity of lab-grown gemstones due to sustainability and affordability advantages.

- Rising use of gemstones in engagement rings, designer jewelry, and fashion accessories.

- Growing focus on traceability and ethical sourcing of gemstones driven by ESG regulations and consumer awareness.

- Advancements in gemstone cutting, treatment, and certification technologies are improving product value and transparency.

- Expansion of e-commerce jewelry platforms offering authenticated and customizable gemstone jewelry across Europe.

Segmental Insights

- Based on nature, the natural gemstones segment dominated the European gemstones market in 2024, accounting for a substantial share. The segment’s leadership is attributed to the continued consumer preference for naturally occurring gemstones due to their rarity, unique characteristics, and long-term value retention, particularly among luxury consumers and collectors.

- Based on type, the precious gemstones segment held the majority share of 65.2% of the European gemstones market in 2024, driven by high demand for diamonds, rubies, emeralds, and sapphires. The rising use of these gemstones in luxury jewelry collections and engagement rings has sustained their dominance.

- Based on product, the diamonds segment led the European gemstones market in 2024, capturing a 52.7% share. The enduring cultural and emotional value of diamonds, supported by strong demand from the bridal jewelry and luxury gift markets, continues to drive segment growth.

Regional Insights

The European gemstones market demonstrates steady growth across both Western and Central Europe, supported by rising disposable incomes and strong luxury retail presence.

- Switzerland was the top performer in the European gemstones market, accounting for 24.5% share in 2024, driven by its prominence as a global luxury hub with leading jewelry and watch brands such as Cartier and Gübelin.

- France and the United Kingdom hold significant shares due to their strong luxury retail sectors and the presence of iconic gemstone and jewelry brands.

- Italy continues to play a major role as a designer jewelry hub, blending traditional craftsmanship with modern gemstone settings.

- Germany and Spain are experiencing increasing consumer demand for affordable and lab-grown gemstone jewelry, driven by younger, sustainability-conscious buyers.

- Nordic countries are witnessing growth due to the rising demand for ethically sourced and sustainable gemstone products.

Competitive Landscape

The European gemstone market is moderately consolidated, featuring a blend of luxury brands, mining corporations, and independent gemstone certification institutions. Companies are increasingly investing in sustainable sourcing practices, blockchain-based traceability systems, and design innovation to enhance transparency and appeal to ethically aware consumers. Key players in the Europe gemstones market include Cartier (France), Gübelin Gem Lab (Switzerland), Pandora (Denmark), Gem Diamonds (U.K.), SWAROVSKI (Austria), Anglo American plc (U.K.), GEMFIELDS (U.K.), Petra Diamonds Limited (U.K.), Rio Tinto (U.K.), and Botswana Diamonds PLC (Ireland).

Europe Gemstones Market Size

The Europe gemstones market was valued at USD 10.72 billion in 2025, is estimated to reach USD 11.16 billion in 2026, and is projected to reach USD 15.38 billion by 2034, growing at a CAGR of 4.09% from 2026 to 2034.

Gemstones refer to the natural and laboratory grown precious and semi-precious stones, including diamonds, sapphires, emeralds, rubies, and coloured gemstones, used primarily in fine jewellery, investment, and heritage collections. Unlike commodity markets, this sector is defined by provenance, ethical sourcing, and artisanal value addition through cutting and setting. Europe’s historical role as a global jewellery hub, anchored by centres such as Antwerp for diamonds and Idar Oberstein for coloured stones, continues to shape market dynamics. According to sources, the majority of high-value gemstones entering the EU are voluntarily certified by a range of laboratories. As per Eurostat, intra-EU trade in precious stones and jewellery exceeded a substantial amount in 2023, which reflects deep integration across manufacturing and retail channels. Furthermore, the European Commission is phasing in a framework for digital traceability of diamonds, including rough diamonds, with a mandatory deadline of January 1, 2026. This confluence of legacy craftsmanship, stringent compliance, and evolving consumer ethics defines the structural identity of the Europe gemstones market.

MARKET DRIVERS

Rising Demand for Ethically Sourced and Traceable Gemstones

Regional consumers increasingly prioritise transparency and sustainability in luxury purchases, which directly drives the growth of the Europe gemstones market. As per studies, a portion of respondents in Europe stated they would avoid jewellery containing stones of uncertain origin. This ethical shift aligns with the EU’s Corporate Sustainability Due Diligence Directive, which requires companies to map supply chains for human rights and environmental risks, which impacts gemstone importers and retailers. In response, major European jewellers like Cartier and Chopard have adopted blockchain-enabled traceability systems. Apart from these, the Responsible Jewellery Council certified over 1900 European entities in 2023, facilitating credible claims. Certification bodies offer origin reports with geographic DNA profiling, which further satisfies consumer demand for verifiable provenance. This convergence of regulation, technology, and values is reshaping procurement strategies across the European gemstone value chain.

Growth in High Net Worth Population and Luxury Investment Demand

The expanding affluent demographic in the region is fuelling the expansion of the Europe gemstones market. As per the Global Wealth Report 2023, Europe is home to millions of high-net-worth individuals, which represents a portion of the global total. This cohort increasingly views rare coloured gemstones as inflation-resistant stores of value. According to research, a portion of European collectors acquired gemstones for portfolio diversification. Auction results reflect this trend. Furthermore, some private banks offer gemstone valuation and custody services by integrating physical stones into wealth management portfolios. This financialisation of gemstones, supported by institutional infrastructure, elevates their role beyond aesthetics to tangible investment instruments in Europe’s luxury economy.

MARKET RESTRAINTS

Stringent Regulatory Compliance and Documentation Burdens

The region’s rigorous legal framework for gemstone trade imposes administrative and financial barriers on, gemstone market. As per sources, all rough diamond shipments must include tamper-proof containers, government-validated certificates, and digital entry records through the EU’s TRACES NT system. For coloured gemstones, while not covered by Kimberley, the EU Conflict Minerals Regulation requires due diligence for tin, tantalum, tungsten, and gold, and increasingly influences expectations for other minerals. These overlapping requirements increase compliance costs, which discourages market entry and fragments supply chains despite strong end demand.

Limited Domestic Gemstone Production and Import Dependency

Lack of significant primary gemstone deposits; consequently, its heavy dependence on imports from Africa, Asia, and South America impedes the expansion of the Europe gemstone market. As per studies, the majority of colored gemstone mining occurs in countries in the global south, such as Myanmar, Mozambique, and Zambia, with only minor, specialized gem production in Europe. Political and military conflict, such as the civil unrest that has impacted Myanmar's Mogok region, has caused significant disruptions and declines in the global supply of high-quality rubies. These supply chain disruptions directly affect international gem dealers and European ateliers who rely on these stones. Simultaneously, customs issues, including challenges with Harmonized System (HS) code classification, can create delays for gemstone shipments. Volatile pricing and supply insecurity plague European businesses that lack domestic mining or strategic stockpiles. This instability impedes long-term planning and inventory management, as stone's unique nature prevents standardization.

MARKET OPPORTUNITIES

Integration of Laboratory-Grown Gemstones into Mainstream Luxury Retail

Laboratory-grown gemstones are setting up a high growth opportunity for the growth of Europe gemstones market. This development is driven by technological parity with natural stones and alignment with sustainability mandates. Synthetic gemstones produced through advanced crystal growth techniques are now achieving optical and structural qualities comparable to natural stones, according to studies. In the United Kingdom, jewelry brands are increasingly introducing lab-grown alternatives as part of a larger shift toward sustainable sourcing, as per sources. Public procurement policies across Europe are beginning to prioritize low-impact materials, creating new institutional opportunities for synthetic gemstones, according to studies. Regulatory frameworks within the European Union emphasize transparency in labeling while continuing to support innovation and high-end product positioning, as per sources. Production costs for lab-created gems continue to decline each year, reinforcing the broader trend toward accessible luxury and circular material usage, according to studies. Hence, lab-grown gemstones offer scalable, ethical, and price-stable alternatives that resonate with younger European consumers seeking luxury without ecological compromise.

Revival of Heritage Craftsmanship through EU Cultural Funding Programmes

Region’s rich tradition of gemstone cutting and jewellery making is being revitalised through targeted cultural and regional development funding, which provides fresh prospects for the expansion of the Europe gemstones market. As per research, notable amounts were allocated to preserve intangible craft heritage, including gem engraving in Idar Oberstein, Germany, and cameo carving in Torre del Greco, Italy. These initiatives support master artisans in training apprentices and modernising workshops with digital design tools while retaining hand finishing techniques. This fusion of heritage preservation and innovation not only safeguards Europe’s competitive edge in high-end craftsmanship but also differentiates its offerings in a global market increasingly dominated by mass production.

MARKET CHALLENGES

Proliferation of Misrepresentation and Synthetic Substitution Without Disclosure

The increasing sophistication of synthetic and treated gemstones has intensified risks of undisclosed substitution by eroding consumer trust and brand reputation, which constrains the growth of the Europe gemstones market. Advanced simulants like hydrothermal emeralds or flux-grown rubies exhibit near identical spectroscopic signatures to natural stones, requiring specialised equipment for detection. The challenge is exacerbated by inconsistent testing access; only a few EU countries host ISO accredited gem labs, according to studies. The integrity of Europe's high-value gemstone market is threatened by the risk of mislabeling, even among top retailers, due to a lack of mandatory disclosure and affordable verification.

Volatility in Global Gemstone Pricing Due to Speculative Trading

Gemstone valuations in the region are increasingly influenced by speculative investment flows rather than intrinsic rarity or craftsmanship, and this creates price instability, thereby slowing down the expansion of the Europe gemstones market. This financialisation disconnects retail pricing from artisanal input costs, squeezing independent jewellers who cannot absorb sudden input cost swings. Furthermore, auction house guarantees, where houses underwrite minimum sale prices, distort market signals by inflating perceived value. Such speculation affects long-term pricing transparency and complicates inventory planning for European retailers who rely on consistent valuation models to maintain margins and customer trust in a traditionally relationship-based trade.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Nature, Type, Product, End-use, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Cartier (France), Gübelin Gem Lab (Switzerland), Pandora (Denmark), Gem Diamonds (U.K.), SWAROVSKI (Austria), Anglo American plc (U.K.), GEMFIELDS (U.K.), Petra Diamonds Limited (U.K.), Rio Tinto (U.K.), and Botswana Diamonds PLC (Ireland). |

SEGMENTAL ANALYSIS

By Nature Insights

The natural gemstones segment continued to dominate the Europe gemstones market by accounting for a substantial share in 2025. The dominance of the natural gemstones segment is attributed to their historical prestige, perceived rarity, and enduring role in high-value jewellery and heirloom collections. This dominance is further supported by cultural narratives, European aristocracy, and museums have long curated natural gemstones as symbols of legacy, with institutions like the Victoria and Albert Museum housing collections that elevate their cultural capital. Apart from these, auction performance validates their investment appeal. Regulatory frameworks also support natural stones. EU consumer protection laws mandate clear labelling of synthetics, implicitly positioning natural gems as the default premium category. Collectors and connoisseurs, particularly in Switzerland and France, continue to drive demand for untreated stones with verifiable provenance, ensuring natural gemstones retain their central position despite rising synthetic competition.

The synthetic gemstones segment is predicted to witness the highest CAGR of 14.2% from 2025 to 2033 due to technological parity, sustainability imperatives, and shifting generational preferences. In addition, according to the UK’s National Association of Jewellers, a portion of millennial consumers prioritised ethical sourcing over natural origin, creating fertile ground for lab-grown alternatives. Major retailers have responded decisively. Furthermore, European sustainability frameworks are increasingly promoting the use of low-impact materials, which creates new market opportunities for synthetic products in sectors such as corporate gifting and institutional procurement, according to studies. The use of renewable energy sources by synthetic gemstone manufacturers in Germany and Sweden aligns the industry with Europe's decarbonization objectives, according to sources, which also note stable pricing and reliable availability.

By Type Insights

The precious gemstones segment held the majority share of 65.2% of the Europe gemstones market in 2024. Factors such as their entrenched status in luxury jewellery, investment portfolios, and ceremonial traditions have significantly contributed to the growth of the precious gemstones segment. As per research, diamond transactions alone accounted for a substantial amount in intra-EU trade, emphasizing the segment’s economic weight. Cultural rituals further cement demand. Besides, precious stones benefit from robust certification ecosystems. Auction performance reinforces premium positioning. Sotheby’s London recorded an increase in precious gemstone lot sales in 2023, led by Kashmir sapphires and Colombian emeralds. The combination of emotional symbolism, financial recognition, and institutional validation ensures precious gemstones remain the cornerstone of Europe’s high-value gem trade.

The semi-precious gemstones segment is estimated to register the fastest CAGR of 9.7% during the forecast period, owing to creative design innovation and demand for unique, expressive jewellery. As per sources, semi-precious stones featured in a portion of fine jewellery collections presented at Milan Fashion Week, as designers seek alternatives to saturated diamond aesthetics. Their broader colour palette enables personalisation. Furthermore, semi-precious stones offer greater affordability without compromising beauty. A high-quality 5-carat amethyst costs less compared to tens of thousands for a comparable sapphire, which enables accessible luxury. The rise of independent ateliers in Barcelona and Copenhagen, which specialise in one-of-a-kind pieces using locally sourced or ethically traded semi-precious stones, further fuels this trend. Social media is fuelling a rise in visual diversity and self-expression, which in turn is allowing semi-precious gemstones to redefine modern European jewellery outside of old-fashioned hierarchies.

By Product Insights

In 2024, the diamonds segment led the Europe gemstones market and captured a 52.7% share 2024. The growth of the diamonds segment is fuelled by their irreplaceable role in engagement rings, status jewellery, and investment vehicles. As per studies, a large number of diamond engagement rings were sold across the EU in 2023, with France, Germany, and the UK accounting for a portion of volumes. The diamond’s dominance is also supported by institutional infrastructure. Regulatory alignment also supports continuity. Furthermore, diamonds benefit from unparalleled liquidity. Even amid lab-grown competition, natural diamonds retain emotional and financial gravitas, particularly in Southern Europe, where multi-generational gifting traditions persist. This blend of cultural ritual, regulatory trust, and market depth secures the diamond’s leading position.

The alexandrite segment is anticipated to witness the fastest CAGR of 16.8% from 2025 to 2033. The rapid expansion of the alexandrite segment can be attributed to its extreme rarity, dramatic colour change properties, and rising collector interest. Pricing for alexandrite varies widely depending on the stone's origin, the quality of its color change, clarity, and carat weight. An exceptional, large alexandrite can fetch very high prices at auction. The scarcity has intensified demand among high-net-worth collectors. Contemporary sources from Brazil and Tanzania are being ethically developed, with some gem labs introducing geographic fingerprinting to authenticate origin. Apart from these, alexandrite’s June birthstone status and association with transformation resonate with wellness-oriented luxury consumers. Designers have begun featuring alexandrite in limited edition pieces by leveraging its mystique for storytelling. So, its exclusivity and optical uniqueness position it for exceptional growth among connoisseurs and investors alike.

COUNTRY LEVEL ANALYSIS

Switzerland Gemstones Market Analysis

Switzerland was the top performer in the Europe gemstones market and occupied a 24.5% share in 2024. The prominence of Switzerland is primarily driven by its neutrality, political stability, and robust wealth management sector, which makes it a preferred destination for gemstone investment and storage. It is functioning as the continent’s premier hub for high-value trading, private banking integration, and precision craftsmanship. Swiss private banks such as Pictet and Lombard Odier offer gemstone custody and valuation services, which embed physical stones into asset portfolios. Besides, Geneva hosts major auctions. The Swiss Gemmological Institute provides world-leading certification, reinforcing trust in provenance and quality. This ecosystem of finance, discretion, and expertise cements Switzerland’s unrivalled position in Europe’s luxury gemstone landscape.

United Kingdom Gemstones Market Analysis

The United Kingdom was the second largest in the Europe gemstones market by capturing 19.3% share in 2024. The growth of the United Kingdom is due to its historic jewellery district, Hatton Garden, strong auction presence, and dynamic retail innovation. The UK’s post-Brexit regulatory autonomy has enabled faster adoption of labelling standards for synthetic stones, fostering transparency. Furthermore, London’s role as a global art and luxury capital attracts high-net-worth collectors. This blend of heritage infrastructure and adaptive regulation sustains the UK’s influential market role.

France Gemstones Market Analysis

France is another key region in the Europe gemstones market, with Paris’s legacy as a global fashion and haute joaillerie capital. The country is home to iconic houses like Cartier, Van Cleef and Boucheron, which drive demand for exceptional natural gemstones through haute couture collaborations. French consumers exhibit a strong preference for certified stones. Furthermore, the Ministry of Culture supports artisanal gem setting through the Entreprise du Patrimoine Vivant label by preserving craftsmanship. Paris Fashion Week continues to showcase gemstone-centric collections, which influence European trends. This fusion of artistic prestige, regulatory rigour, and cultural heritage ensures France’s enduring relevance in the high-end segment.

Italy Gemstones Market Analysis

Italy is moving ahead steadfastly in the Europe gemstones market, and is renowned for its artisanal goldsmithing and integration of coloured stones into wearable art. Centres combine centuries-old techniques with modern design, which produces a percentage of Europe’s fine jewellery according to Confindustria Moda. Italian designers increasingly source traceable stones. The Vicenzaoro trade fair, Europe’s largest jewellery exhibition, reported a rise in exhibitors featuring ethically sourced coloured gemstones. Moreover, Italy’s strong domestic luxury consumption, fuelled by tourism and family wealth, supports consistent demand. This synergy of craftsmanship, design innovation, and ethical sourcing positions Italy as a vital creative engine in the European gemstone ecosystem.

Germany Gemstones Market Analysis

Germany is likely to grow in the Europe gemstones market from 2025 to 2033 owing to technical precision, strong consumer protection laws, and a growing collector base. German consumers prioritise transparency. The country hosts leading laboratories like DGK and is a key market for investment-grade stones, with private banks in Frankfurt offering gemstone appraisal services. Apart from these, Germany’s robust vocational training system sustains a pipeline of skilled gem setters and polishers, particularly in Pforzheim, the historic jewellery town. This emphasis on authenticity, education, and regulatory clarity ensures Germany’s steady and discerning participation in the European gemstone market.

COMPETITIVE LANDSCAPE

The Europe gemstones market features a bifurcated competitive landscape where heritage luxury houses and agile ethical disruptors coexist. Traditional players like Cartier and Van Cleef compete on rarity, provenance, and artisanal mastery while newer entrants such as Pandora gain ground through sustainability and accessibility. Competition is not primarily price-based but revolves around authenticity certification and narrative depth. Independent ateliers in Italy and Germany differentiate through bespoke craftsmanship, whereas Swiss institutions dominate technical validation. The threat of undisclosed synthetics intensifies reliance on accredited laboratories like SSEF and Gübeli,n creating a trust economy. Regulatory burden from the EU Conflict Minerals Regulation and Corporate Sustainability Due Diligence Directive raises entry barriers, favouring established players with robust compliance systems. Meanwhile, auction houses like Christie’s influence pricing and desirability through curated sales. Overall, rivalry is sophisticated, nuanced, and increasingly defined by transparency rather than volume.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe gemstones market include

- Cartier (France)

- Gübelin Gem Lab (Switzerland)

- Pandora (Denmark)

- Gem Diamonds (U.K.)

- SWAROVSKI (Austria)

- Anglo American plc (U.K.)

- GEMFIELDS (U.K.)

- Petra Diamonds Limited (U.K.)

- Rio Tinto (U.K.)

- Botswana Diamonds PLC (Ireland)

TOP PLAYERS IN THE EUROPE GEMSTONES MARKET

- Cartier is a cornerstone of the Europe gemstones market with a legacy of sourcing exceptional natural diamonds and coloured stones for its haute joaillerie collections. The company contributes globally by setting benchmarks in ethical procurement and gemstone curation, often acquiring record-breaking stones for iconic pieces. These initiatives enhance transparency and align with EU sustainability directives while strengthening emotional engagement with high-net-worth clientele across Europe and beyond.

- Gübelin Gem Lab is a globally respected Swiss institution pivotal to the Europe gemstones market through its advanced gemmological analysis and origin certification services. The company supports the entire value chain, from miners to retailers, by providing scientific validation of authenticity, treatment, and geographic provenance. It also expanded its laboratory network to reduce certification turnaround time. By merging centuries-old expertise with cutting-edge technology, Gübelin reinforces trust in natural gemstones and combats misrepresentation across European luxury markets.

- Pandora has significantly reshaped the Europe gemstones market by championing laboratory-grown stones as accessible luxury. The company transitioned its entire fine jewellery line to lab-created diamonds and gemstones in 2023, sourcing exclusively from carbon-neutral facilities in Europe. This strategic pivot aligns with EU Green Deal principles and appeals to younger, values-driven consumers. Its vertically integrated supply chain ensures consistent quality and pricing, democratizing gemstone jewellery while maintaining premium aesthetics. Through this innovation, Pandora bridges mass market reach with sustainable luxury, influencing global industry standards.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe gemstones market prioritise traceability through blockchain and nano tagging to meet stringent EU due diligence requirements. They invest heavily in gemmological certification and origin verification to combat misrepresentation and build consumer trust. Luxury houses focus on storytelling by linking stones to geographic heritage and artisanal craftsmanship, enhancing emotional value. Mass market brands leverage laboratory-grown gemstones to offer ethical, affordable alternatives aligned with sustainability mandates. Companies also collaborate with mine cooperatives and certification bodies to secure transparent supply chains. Digital platforms, including virtual try-ons and provenance portals, improve engagement while vocational training partnerships preserve cutting and setting expertise. These strategies collectively address regulatory compliance, consumer ethics, and market differentiation in a high-scrutiny environment.

MARKET SEGMENTATION

This research report on the Europe gemstones market has been segmented and sub-segmented into the following categories.

By Nature

- Natural

- Synthetic

By Type

- Precious

- Semi-Precious

By Product

- Diamond

- Emerald

- Ruby

- Sapphire

- Alexandrite

- Topaz

- Others

By End Use

- Astrology

- Jewelry and Ornaments

- Luxury Arts

- Others

By Region

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

1. What is the Europe gemstones market and what drives its growth?

The Europe gemstones market involves diamonds, rubies, sapphires, and emeralds. Growth is driven by luxury jewelry demand, investment interest, and rising consumer affluence

2. Which gemstone type dominates the Europe gemstones market?

Diamonds represent the largest revenue segment. Rubies are forecast to be the fastest growing gemstone type by 2034

3. Why are colored gemstones gaining popularity in the Europe gemstones market?

Colored gemstones like rubies, emeralds, and sapphires attract buyers seeking uniqueness, investment value, and fashion appeal.

4. Which country leads Europe gemstones market growth?

Germany is expected to register the highest CAGR from 2025 to 2033, driving innovation and luxury consumption

5. How do luxury jewelry trends influence Europe gemstones market?

Customized designs, rare stones, and sustainability trends are shaping consumer preferences and boosting high-value sales

6. What role does gemstone certification play in the Europe gemstones market?

Certification ensures origin and authenticity, with institutions like GIA supporting buyer confidence in quality gems

7. What challenges affect the Europe gemstones market?

Supply chain constraints, authenticity concerns, and regulatory demands for ethical sourcing remain top industry challenges

Supply chain constraints, authenticity concerns, and regulatory demands for ethical sourcing remain top industry challenges

Consumers increasingly seek responsibly sourced gems to limit environmental impact and promote ethical practices

9. How important are auctions for the Europe gemstones market?

Auction houses play a key role, especially for rare stones, driving high-value sales and global visibility for unique gems

10. How do fashion trends impact Europe gemstones market demand?

Designer endorsements and seasonal collections boost colored gemstone sales and shape consumer preferences

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com