Europe Geotextiles Market Size, Share, Trends, & Growth Forecast Report By Material (Polypropylene, Polyester, Polyethylene, Other Materials), Fabric Type, Function, Application and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Geotextiles Market Report Summary

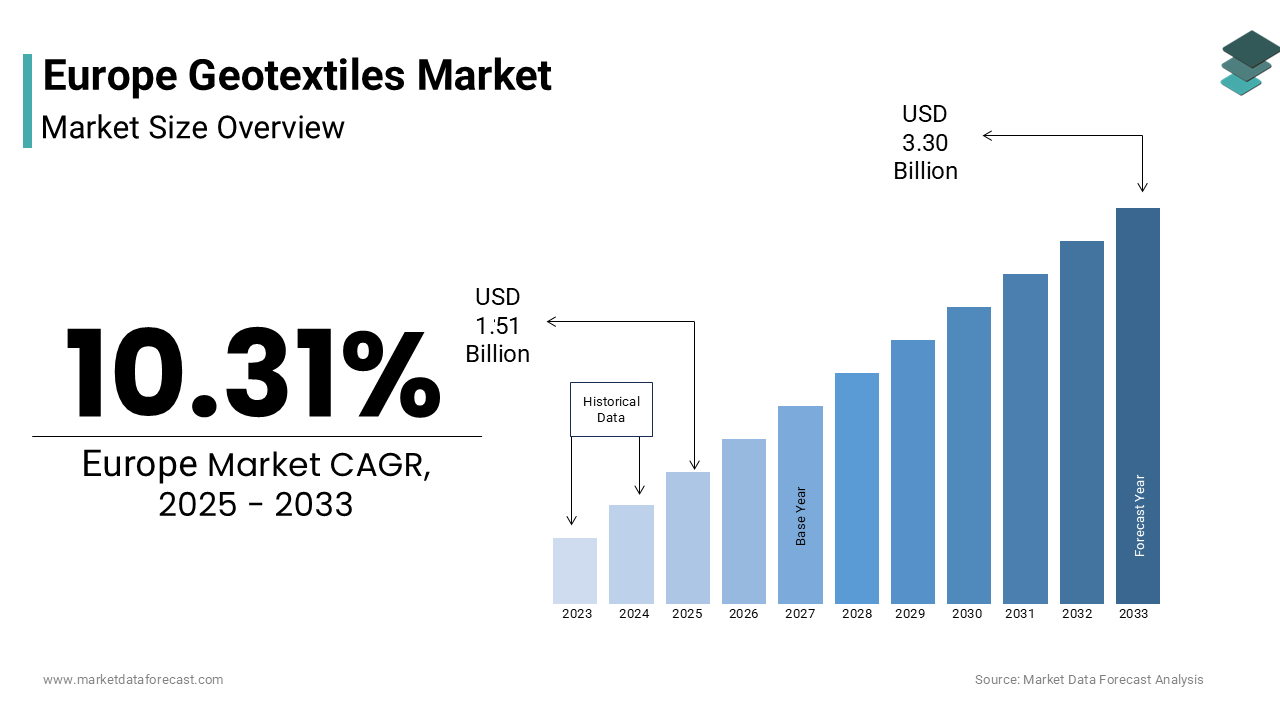

The Europe geotextiles market was valued at USD 1.37 billion in 2024, is expected to reach USD 1.51 billion in 2025, and is projected to reach USD 3.30 billion by 2033, growing at a CAGR of 10.31% during the forecast period from 2025 to 2033. The growth of the Europe geotextiles market is driven by accelerating investment in climate-resilient transport infrastructure, rising adoption of sustainable construction materials, and increasing use of geotextiles in road construction, erosion control, drainage, and environmental protection projects. Strong alignment with the European Green Deal, growing emphasis on long-term infrastructure durability, and expanding applications in urban green infrastructure and flood mitigation are further supporting market expansion across the region.

Key Market Trends

- Rising use of geotextiles in climate-resilient road and rail infrastructure

- Increasing adoption of bio-based and biodegradable geotextiles in ecological engineering

- Integration of geotextiles into urban green infrastructure and stormwater management systems

- Growing demand for high-performance non-woven fabrics in filtration and drainage applications

- Expanding role of geotextiles in landfill containment and environmental protection projects

Segmental Insights

- Based on material, the polypropylene segment held the largest share of the Europe geotextiles market in 2024. This dominance is attributed to its favorable balance of tensile strength, chemical resistance, cost efficiency, and widespread acceptance in public infrastructure projects such as road construction and pavement repair.

- Based on fabric type, the non-woven segment accounted for the leading share of the Europe geotextiles market in 2024. The segment’s growth is driven by its superior permeability, filtration efficiency, and versatility across drainage, separation, and erosion control applications, particularly in green infrastructure and urban stormwater systems.

- Based on application, road construction and pavement repair represented the largest segment of the Europe geotextiles market in 2024. The dominance of this segment is supported by Europe’s aging road network, continuous rehabilitation programs, and institutionalized use of geotextiles to extend pavement lifespan and reduce maintenance costs.

Regional Insights

The Europe geotextiles market shows strong growth across major economies, supported by infrastructure modernization, climate adaptation mandates, and environmental regulations.

- Germany led the Europe geotextiles market by accounting for 18.5% of the regional market share in 2024, driven by large-scale transport rehabilitation projects, stringent engineering standards, and strong domestic manufacturing capabilities.

- France ranked second, supported by aggressive integration of geotextiles in ecological restoration, riverbank stabilization, and climate adaptation projects aligned with national biodiversity and water management strategies.

- The United Kingdom is projected to witness the fastest CAGR during the forecast period, fueled by increasing investments in flood protection, shoreline stabilization, and climate-resilient infrastructure despite post-Brexit regulatory changes.

- Italy and Spain are experiencing steady growth due to geographic vulnerability to erosion, landslides, desertification, and increasing deployment of geotextiles in agriculture, renewable energy, and slope stabilization projects.

Competitive Landscape

The Europe geotextiles market is moderately consolidated and characterized by strong competition based on technical performance, regulatory compliance, and sustainability credentials rather than price alone. Leading players focus on innovation in bio-based materials, recycled content integration, and customized solutions tailored to public infrastructure and environmental projects. Compliance with EU circular economy regulations and environmental standards has become a key competitive differentiator, favoring manufacturers with strong R&D and certification capabilities. Major players operating in the Europe geotextiles market include TenCate Geosynthetics, Solmax, Officine Maccaferri, HUESKER, NAUE GmbH & Co. KG, BontexGeo, Fibertex Nonwovens, AGRU America (AGRULINE), GSE Environmental, and Low & Bonar.

Europe Geotextiles Market Size

The europe geotextiles market size was valued at USD 1.37 billion in 2024 and is anticipated to reach USD 1.51 billion in 2025 from USD 3.30 billion by 2033, growing at a CAGR of 10.31% during the forecast period from 2025 to 2033.

Geotextiles are permeable textiles engineered to enhance the performance of civil infrastructure through functions such as filtration, separation, reinforcement, drainage, and erosion control. In Europe, their deployment has become integral to sustainable construction practices across transportation, water management, and environmental protection projects. Additionally, Eurostat data indicates that in 2023 Union’s total land surface was dedicated to agriculture, amplifying the need for soil stabilization solutions. These textiles are increasingly specified in public works aligned with the European Green Deal, which mandates climate resilient development across member states.

MARKET DRIVERS

Accelerated Investment in Climate Resilient Transport Infrastructure

The public expenditure on climate resilient transportation networks is a major factor propelling the growth of Europe geotextiles market. National governments and supranational bodies are prioritizing infrastructure capable of withstanding extreme weather events, which have increased in frequency and intensity. In response, the transport resilience projects, including road and rail corridors vulnerable to flooding and slope instability. Geotextiles plays an important role in these initiatives by reinforcing subgrades, improving load distribution, and preventing subsoil washout. This strategic alignment between climate adaptation funding and geosynthetic application not only ensures long term asset durability but also reduces lifecycle maintenance costs, where a key consideration for financially constrained public agencies. The integration of these materials thus reflects a systemic shift from reactive repair to proactive resilience in Europe’s transport planning ethos.

Regulatory Alignment with Sustainable Infrastructure Mandates

European policy increasingly mandates the use of performance enhancing materials that support long term environmental and economic efficiency. The regulatory alignment with sustainable infrastructure mandates is additionally fuelling the growth of the Europe geotextiles market. The European Commission’s Green Public Procurement criteria now recommend geotextiles for erosion control in all publicly funded civil works. As per the European Construction Institute, EU funded earthworks projects, included geotextile specifications increase from 2020. These performance metrics align with the EU’s objective of maximizing infrastructure longevity under constrained fiscal envelopes, thus institutionalizing geotextiles as a non-discretionary component in modern civil engineering practice.

MARKET RESTRAINTS

Stringent Regulatory Emphasis on Circular Economy Principles

The European Union’s binding waste and resource efficiency mandates structural barrier to conventional geotextile adoption is restraining the growth of Europe geotextiles market. Under the Circular Economy Action Plan adopted in 2020, the European Commission requires that all construction products demonstrate end of life recyclability and reduced virgin material dependence by 2030. However, as per the European Geosynthetics Society, fewer installed polypropylene based geotextiles meet these forthcoming recyclability thresholds due to composite layering and polymer cross contamination. Furthermore, the European Chemicals Agency classified certain legacy stabilizers used in geotextile manufacturing as Substances of Very High Concern in 2023, restricting their use without extensive authorization. Similarly, Sweden’s Environmental Protection Agency now mandates full life cycle assessments for all geotextiles used in state funded projects, a requirement that has delayed procurement timelines by an average of five months, according to the Swedish Transport Administration. These regulatory shifts, while environmentally justified, impose substantial reformulation expenses, certification delays, and supply chain recalibrations that disproportionately affect small and medium manufacturers lacking R and D capacity.

Limited End of Life Infrastructure for Synthetic Geotextiles

Europe lacks dedicated collection and recycling systems for post construction geosynthetics, which is additionally declining the growth of Europe geotextiles market. According to the European Waste Catalogue, geotextiles are classified under mixed plastic waste streams, rendering them ineligible for standard polymer recycling due to contamination with soil, adhesives, and other construction debris. The European Environment Agency estimates that very less geotextiles are recovered at project decommissioning, with the remainder landfilled or incinerated. This gap contradicts the EU’s landfill diversion targets under the Waste Framework Directive, which aim to restrict municipal and construction waste landfilling by 2035.

MARKET OPPORTUNITIES

Expansion of Nature Based Solutions in Flood and Erosion Control

The growing institutional endorsement of nature-based solutions are attributed in showcasing new opportunities for the growth of Europe geotextiles market. Unlike conventional synthetics, these materials integrate with natural systems by offering temporary stabilization, while enabling vegetation establishment. According to the International Union for Conservation of Nature, over European riverbanks were rehabilitated using bioengineering techniques between 2020 and 2023, with geotextiles serving as foundational erosion control layers. Spain’s Ministry for Ecological Transition reported that bio based geotextiles reduced post fire hillslope erosion in pilot watersheds during 2023, outperforming synthetic alternatives in ecological recovery metrics. This paradigm shift aligns with the EU Biodiversity Strategy for 2030, which calls for restoring free flowing rivers and degraded ecosystems. As public agencies prioritize ecological functionality alongside engineering performance, bio geotextiles are positioned to capture an expanding niche, particularly in sensitive habitats where synthetic persistence poses long term environmental risks.

Integration of Geotextiles in Urban Green Infrastructure Development

The proliferation of urban green infrastructure initiatives offers a high growth vector for specialized geotextile applications in densely populated European cities, which is additionally to enhance the growth of the Europe geotextiles market. As per Eurostat, many European cities exceeded World Health Organization air quality limits in 2023, accelerating demand for green stormwater management. In Copenhagen, the Cloudburst Management Plan allocated many Euros through 2025 for decentralized drainage systems incorporating nonwoven geotextiles in urban blocks. Likewise, Paris integrated geotextile lined bioswales into its 2024 Olympic site redevelopment to meet the city’s mandate of managing rainfall on site. As per recent study, green infrastructure could reduce urban runoff by up to 55%, thereby diminishing pressure on aging sewer networks. These projects necessitate geotextiles with tailored pore structures, chemical resistance, and UV stability, creating opportunities for high performance variants.

MARKET CHALLENGES

Volatility in Raw Material Pricing and Supply Chain Fragmentation

The acute exposure to petrochemical price fluctuations and fragmented polymer sourcing networks is one of the major challenges for the growth of Europe geotextiles market. Polypropylene and polyester, which constitute geotextile feedstock, are subject to global oil market dynamics and regional refining capacity constraints. According to the International Energy Agency, European polymer prices increased by 22% between January and October 2023 due to refinery outages and heightened export competition from the Middle East. This volatility directly impacts manufacturing margins, as most European producers operate under fixed price public contracts that prohibit mid-term cost adjustments. Compounding this issue is the fragmented nature of the polymer supply chain, as highlighted by Plastics Europe, which reported that only few European refineries possess dedicated polypropylene lines meeting geotextile grade specifications. Consequently, manufacturers often rely on intermediaries, increasing lead times by up to 6 weeks and procurement costs by 12 to 15%. The situation worsened in 2024, when a major North Sea polymer plant in the Netherlands underwent unscheduled maintenance, disrupting supply to over forty geotextile converters.

Inconsistent Technical Standards Across Member States

The absence of harmonized testing and performance standards is another attribute to limit the growth of the Europe geotextiles market. While the European Committee for Standardization has issued EN ISO 10319 and EN ISO 12958 for tensile and filtration properties, national authorities frequently impose supplementary criteria that conflict with pan European norms. As per the European Construction Industry Federation, EU member states maintain distinct geotextile approval protocols, creating compliance redundancies that inflate certification costs. In Poland, for example, road authorities require frost heave resistance tests not recognized under EN standards, delaying project approvals by an average of 4 months. Similarly, Austria mandates additional UV degradation thresholds for alpine applications that necessitate separate product batches. This regulatory fragmentation discourages cross border tenders and deters innovation, as manufacturers avoid investing in R and D for niche national requirements. The European Commission acknowledged this issue in its 2023 Single Market Scoreboard, noting that construction product divergence costs the sector an estimated one point two billion euros annually in duplicated testing and delayed deployments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Analysed | By Material, Fabric Type, Function, Application and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Analysed | United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, and the Czech Republic. |

| Market Leaders Profiled | TenCate Geosynthetics, Solmax, Officine Maccaferri, HUESKER, NAUE GmbH & Co. KG, BontexGeo, Fibertex Nonwovens, Agru America (AGRULINE), GSE Environmental, and Low & Bonar |

SEGMENTAL ANALYSIS

By Material Insights

The polypropylene segment was the largest by holding a significant share of the Europe geotextiles market in 2024 with its optimal balance of tensile strength chemical inertness and cost efficiency in civil engineering contexts. According to the European Road Federation, some national road agencies in the EU include polypropylene geotextiles in pavement design manuals due to their proven ability to extend road lifespan. The availability and manufacturing maturity is also to surge the growth of the segment. Europe hosts more than forty dedicated polypropylene polymerization units capable of producing geotextile grade resin with consistent melt flow indices. This scale enables competitive pricing typically 15 to 20% lower than polyester equivalents making polypropylene the default choice for budget constrained public infrastructure programs especially in Southern and Eastern Europe where lifecycle cost thresholds are tightly enforced.

The bio based geotextile materials segment is projected to grow at a CAGR of 20.1% from 2025 to 2033 with the two converging imperatives. The European Commission’s mandate under the Green Deal requires that all publicly funded erosion control projects in Natura 2000 zones utilize biodegradable materials by 2027. This policy directly stimulates demand for geotextiles made from polylactic acid flax or jute fibers, which decompose within 12 to 24 months after vegetation establishment. The national soil conservation programs are increasingly prioritizing ecological compatibility over pure mechanical performance. Germany’s Federal Agency for Nature Conservation has since integrated these findings into its riverbank restoration guidelines further institutionalizing bio-based adoption.

By Fabric Type Insights

The non-woven segment led the European geotextiles market by capturing 28.1% of share in 2024 owing to their multifunctional utility across filtration separation and drainage applications, where isotropic pore structure and high permeability are critical. Their indispensable role in green infrastructure systems, such as rain gardens and permeable pavements, which are now mandated in over 70 European cities under urban stormwater regulations. As per the German Federal Environment Agency, non-woven geotextiles installed beneath permeable surfaces reduce clogging by retaining fine particles while allowing water infiltration at rates exceeding one hundred millimeters per hour. Europe’s non woven production capacity expanded by 12% in 2023 reaching 3.2 million metric tons annually enabling rapid customization for project specific hydraulic requirements. Moreover, the material’s compatibility with needle punching and thermal bonding processes allows integration of recycled content currently across EU producers, as verified by the European Recycling Platform. This aligns with public procurement rules in countries like the Netherlands and Sweden that award bonus points for recycled content.

The Knitted segment is ascribed to witness a fastest CAGR of 18.7% throughout the forecast period. This surge is not driven by volume but by specialized high value applications demanding precise dimensional stability and elongation control. The primary growth vector is in reinforced soil structures such as modular block retaining walls used in urban landscaping and railway embankments. Companies in Switzerland, and Denmark have pioneered computer controlled knitting machines that produce geotextiles with spatially variable tensile properties tailored to finite element model outputs. This capability was leveraged in the 2024 Oslo Urban Slope Stabilization Project, where knitted units reduced material usage, while maintaining safety factors above 1.5.

By Application Insights

The Road construction and pavement repair segment was the largest by holding 49.2% of Europe’s geotextiles market share in 2024. The continent’s aging road network necessitates continuous intervention. As per recent study, 57% of EU motorways and 72% of regional roads were constructed before 1990 and now require rehabilitation. Geotextiles are routinely deployed as interlayers to prevent reflective cracking and moisture ingress functions validated by the Swedish National Road and Transport Research Institute, which found that geotextile interlayers reduce pothole formation. EU cohesion funding prioritizes cost effective longevity. Countries like Poland and Romania have institutionalized their use in national road standards following field trials that demonstrated a 25 year service life extension at a marginal upfront cost increase. This institutional embedding ensures consistent demand irrespective of economic cycles as road maintenance remains a non-discretionary public obligation across all member states.

The landfill and waste containment application segment is projected to register 15.8% from 2025 to 2033 owing to the tightening regulatory frameworks and the urgent need to retrofit obsolete disposal sites. As per the EU Landfill Directive, all member states must reduce biodegradable municipal waste landfilled to 35% of 1995 levels by 2025, a target that has triggered the construction of over 120 engineered containment cells since 2022. Each requires multilayer geotextile systems for leachate collection separation and protection of geomembranes. The French Ministry of Ecological Transition identified unlined historical sites requiring capping with geotextile reinforced soil barriers to prevent groundwater contamination. These projects demand geotextiles with exceptional puncture resistance and chemical stability performance thresholds that command premium pricing and stimulate innovation in composite fabric design.

REGIONAL ANALYSIS

Germany Geotextiles Market Analysis

Germany was the top performer of the Europe geotextiles market by holding 18.5% of share in 2024 with its dual role as both a high volume infrastructure maintainer and an innovation hub for advanced geosynthetic systems. The Federal Ministry for Digital and Transport’s 2024 budget allocated some billion euros to autobahn rehabilitation with geotextile specifications embedded in all major tenders exceeding five million euros. Moreover, Germany hosts Europe’s most stringent technical approval process through the Deutsches Institut für Bautechnik, which has certified for specific engineering functions more than any other EU nation. This regulatory rigor fosters trust in performance claims and accelerates public adoption. These innovations are increasingly deployed in critical infrastructure like the Rhine River dikes, where early failure detection is paramount.

France Geotextiles Market Analysis

France geotextiles market was positioned second by holding 17.2% of share in 2024 with the aggressive policy integration of geotextiles in ecological engineering rather than conventional civil works. The French Biodiversity Strategy mandates that all river restoration projects employ bioengineering techniques with geotextiles, as foundational components. According to the French Water Agency, waterways underwent, such rehabilitation between 2021 and 2024 consuming more coir and polypropylene geotextiles. Field data from the National Research Institute for Agriculture Food and Environment shows these interventions reduced sediment runoff by 71% in Mediterranean regions. Unlike Germany France’s growth is less tied to transport infrastructure and more to climate adaptation mandates that prioritize ecological functionality by making its market uniquely responsive to environmental legislation rather than pure construction cycles.

The United Kingdom Geotextiles Market Analysis

The United Kingdom geotextiles market is anticipated to witness a fastest CAGR from 2025 to 2033. Despite Brexit, the UK remains deeply integrated into European engineering practices with geotextile usage driven by climate resilience imperatives rather than new construction. The National Infrastructure Commission’s 2023 report emphasized that the country’s strategic road network is at high risk of flooding or slope failure due to intensifying rainfall. The Environment Agency’s 2024 Shoreline Management Review identified coastline requiring immediate protection with geotextile sand containers and revetments, now standard in East Anglia and Yorkshire. Additionally, the UK’s Building Safety Regulator introduced stringent ground stability requirements for residential developments on reclaimed land historically common in cities like Manchester and Liverpoo that further embedding geotextiles in foundation design.

Italy Geotextiles Market Analysis

Italy geotextiles market growth is likely to grow from geographic vulnerability and subsequent regulatory codification. This has led to mandatory geotextile inclusion in slope stabilization works under the 2023 Civil Protection Directive which requires all at risk municipalities to implement structural mitigation by 2026. As per the Ministry of Agricultural Policies, arable land suffers from severe erosion exacerbated by intensive olive and vine cultivation on hilly terrain.

Spain Geotextiles Market Analysis

Spain geotextiles market growth is uniquely shaped by arid climate challenges and the rapid deployment of utility scale renewable energy projects. Persistent drought and desertification affect Spanish territory, as per the State Meteorological Agency necessitating geotextile based dust suppression and soil retention measures in road and rail corridors across Andalusia and Castilla La Mancha. The 2023 National Desertification Action Plan allocated for such interventions with non-woven geotextiles specified for their water retention and seed bed formation capabilities. The Spanish Association of Renewable Energy Companies notes that every megawatt of solar capacity installed consumes approximately eight hundred square meters of geotextiles for base stabilization.

COMPETITIVE LANDSCAPE

The Europe geotextiles market features intense but structured competition characterized by a blend of established engineering specialists and agile regional innovators. Dominant players differentiate themselves through technical validation environmental compliance and integration with public infrastructure planning rather than price competition. The regulatory environment notably the EU Green Deal and national circular economy mandates elevates barriers to entry favoring firms with robust R and D capabilities and certified sustainable product lines. Competition is further shaped by project specific performance requirements which necessitate customized solutions and close collaboration with civil engineers and environmental agencies. While global players maintain strong footholds through standardized high performance systems local manufacturers gain traction in niche applications such as bio-based erosion control or alpine slope stabilization. Overall, the competitive landscape rewards technical credibility regulatory agility and strategic alignment with Europe’s climate resilient infrastructure agenda rather than broad market coverage alone.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Geotextiles Market include

- TenCate Geosynthetics

- Solmax

- Officine Maccaferri

- HUESKER

- NAUE GmbH & Co. KG

- BontexGeo

- Fibertex Nonwovens

- Agru America (AGRULINE)

- GSE Environmental

- Low & Bonar

Top Players in the Europe Geotextiles Market

NAUE GmbH and Co KG

NAUE GmbH and Co KG is a leading German manufacturer of geosynthetics with a robust global footprint spanning over one hundred countries. The company specializes in high performance geotextiles geogrids and drainage systems tailored for infrastructure and environmental applications. In recent years NAUE has intensified its focus on digital engineering solutions launching its REACH approved geosynthetic design software NAUE Select in 2023 to enhance project accuracy and client collaboration. The company also expanded its production capacity at its Espelkamp facility in 2024 to meet rising demand for reinforced soil systems across Southern Europe. Its commitment to sustainability is evident through its ISO 14021 certified recycled product line which aligns with EU circular economy mandates. NAUE’s integration of R and D with practical field validation continues to reinforce its reputation as a technical leader in the global geosynthetics sector.

HUESKER Synthetic GmbH and Co KG

HUESKER Synthetic GmbH and Co KG headquartered in Germany is a globally recognized innovator in geosynthetic solutions with a strong emphasis on soil reinforcement erosion control and sustainable infrastructure. The company has significantly advanced its product portfolio through the development of its Secugrid and Combigrid systems which are now specified in critical transport and mining projects worldwide. HUESKER launched its GreenLine range of bio based geotextiles incorporating polylactic acid fibers to address ecological restoration requirements in sensitive European habitats. The company also established a dedicated testing laboratory in Lennestadt in early 2024 to accelerate certification under evolving EU environmental standards. Through strategic partnerships with research institutions such as RWTH Aachen University HUESKER continues to pioneer performance verified solutions that bridge civil engineering needs with environmental stewardship on a global scale.

TenCate Geosynthetics Europe BV

TenCate Geosynthetics Europe BV based in the Netherlands is a key contributor to global geotextile innovation with extensive operations across Asia North America and Latin America. The company is renowned for its advanced polypropylene and polyester non woven solutions used in road construction coastal protection and waste containment. TenCate integrated artificial intelligence into its quality control systems at its Nijverdal plant reducing production defects by twenty two%. The company also co led a Horizon Europe funded consortium in late 2023 to develop smart geotextiles with embedded fiber optic sensors for real time infrastructure monitoring. Its collaboration with the Dutch Ministry of Infrastructure on the Delta Program II further demonstrates its role in national climate resilience planning.

Top Strategies Used by the Key Market Participants

Key players in the Europe geotextiles market primarily employ product innovation through sustainable material development strategic capacity expansion in high demand regions and digital integration for engineering support and quality assurance. They actively pursue public private partnerships to align with EU climate and infrastructure policies while investing in certifications that meet evolving environmental regulations. Additionally, these companies prioritize technical collaboration with academic and governmental bodies to validate performance claims and accelerate adoption in public tenders.

MARKET SEGMENTATION

This research report on the europe geotextiles market has been segmented and sub–segmented into the following categories.

By Material

- Polypropylene

- Polyester

- Polyethylene

- Other Materials

By Fabric Type

- Woven

- Non-woven

- Knitted

By Function

- Separation

- Drainage

- Filtration

- Reinforcement

- Protection

By Application

- Road Construction and Pavement Repair

- Erosion

- Drainage

- Railworks

- Agriculture

- Other Applications

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What are geotextiles?

Geotextiles are permeable synthetic fabrics used in civil engineering projects to improve soil stability, drainage, filtration, and reinforcement.

What is driving the growth of the Europe geotextiles market?

Growth is driven by increasing infrastructure development, road construction, railway expansion, and environmental protection projects across Europe.

Which materials are commonly used in geotextiles?

Polypropylene and polyester are the most commonly used materials due to their durability, chemical resistance, and cost-effectiveness.

What are the major applications of geotextiles in Europe?

Major applications include roadways, railways, erosion control, drainage systems, landfills, and coastal protection.

Which countries dominate the Europe geotextiles market?

Germany, France, the UK, Italy, and Spain are key contributors due to strong infrastructure and construction activities.

What types of geotextiles are widely used?

Woven, non-woven, and knitted geotextiles are widely used, with non-woven geotextiles holding a significant market share.

What challenges does the Europe geotextiles market face?

Challenges include fluctuating raw material prices and high initial installation costs in some applications.

How is technology influencing the geotextiles market?

Advances in polymer technology and manufacturing processes are improving strength, durability, and performance of geotextiles.

How do sustainability regulations impact the market?

Strict EU environmental regulations are encouraging the use of eco-friendly and recyclable geotextiles, boosting demand for sustainable products.

What is the future outlook for the Europe geotextiles market?

The market is expected to grow steadily due to continued investments in transportation infrastructure, flood control, and sustainable construction projects.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com