Europe Glycobiology Market Size, Share, Trends & Growth Forecast Report By Product, Application, End User and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, From (2026 to 2034)

Europe Glycobiology Market Report Summary

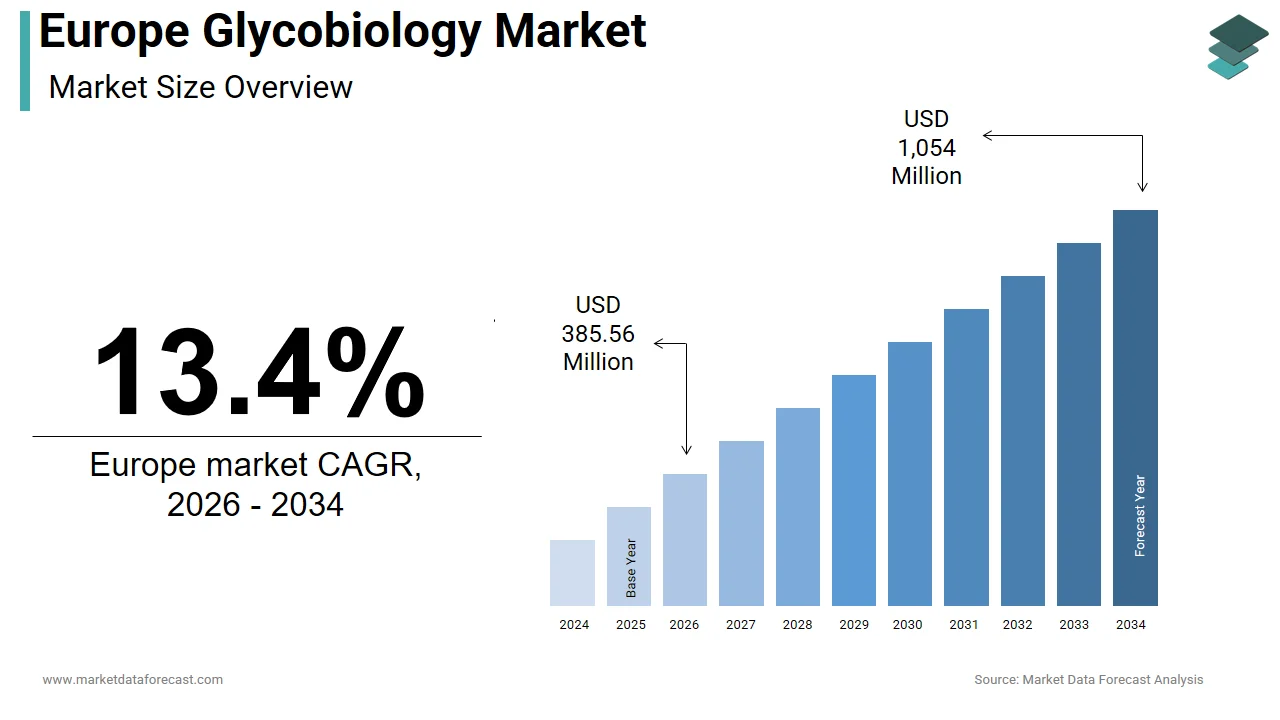

The Europe glycobiology market was valued at USD 340 million in 2025, is anticipated to reach USD 385.56 million in 2026, and is projected to reach USD 1,054 million by 2034, growing at a strong CAGR of 13.4% from 2026 to 2034. Market growth is driven by rising investments in life sciences research, increasing focus on personalized medicine, and expanding applications of glycan analysis in drug development and diagnostics. Researchers and pharmaceutical companies across Europe are leveraging glycobiology to understand disease mechanisms, improve biologics development, and enhance therapeutic efficacy. Advancements in analytical technologies, bioinformatics tools, and high-throughput screening platforms are further accelerating market expansion.

Key Market Trends

- Rising adoption of glycan profiling and biomarker discovery techniques in biomedical research.

- Increasing integration of glycobiology in biologics and biosimilar development.

- Growing demand for advanced mass spectrometry and chromatography platforms.

- Expansion of academic–industry collaborations in glycoscience research.

- Strengthening focus on precision medicine and targeted therapies.

Segmental Insights

- Based on product, the kits and reagents segment dominated the market in 2025 by holding 45.4% market share, driven by high demand for standardized assay kits, labeling reagents, and analytical consumables in routine glycan analysis.

- Based on application, the drug discovery segment commanded 40.8% share in 2025, supported by the growing use of glycobiology in target identification, lead optimization, and biologics characterization.

- Based on end user, the academic research institutions segment led the market by holding 50.9% share in 2025, driven by strong government funding, active research programs, and expanding university-based life sciences laboratories.

Regional Insights

The Europe glycobiology market is witnessing strong growth across major economies, supported by advanced research infrastructure, pharmaceutical innovation, and expanding biotechnology ecosystems.

- Germany led the regional market in 2025 with 26.5% share, driven by strong life sciences research capabilities and high investments in biopharmaceutical development.

- The United Kingdom accounted for 16.9% share in 2025, supported by leading academic institutions and a vibrant biotech startup environment.

- Switzerland is expected to register a prominent CAGR over the forecast period, driven by its precision science focus and global pharmaceutical leadership.

Competitive Landscape

The Europe glycobiology market is characterized by strong competition among analytical instrument manufacturers, life science reagent suppliers, and biotechnology solution providers. Market players are focusing on developing high-sensitivity detection systems, expanding reagent portfolios, and enhancing data analysis platforms. Strategic collaborations with academic institutions, pharmaceutical companies, and research consortia are strengthening competitive positioning across the region.

Prominent companies operating in the Europe glycobiology market include Bruker Corporation, Takara Bio, Inc., Thermo Fisher Scientific, Waters Corporation, Danaher Corporation, New England Biolabs, ProZyme, Inc., Shimadzu Corporation, Merck KGaA, and Agilent Technologies.

Europe Glycobiology Market Size

The size of the Europe glycobiology market was valued at USD 340 million in 2025. This market is expected to grow at a CAGR of 13.4% from 2026 to 2034 and be worth USD 1,054 million by 2034 from USD 385.56 million in 2026.

Glycobiology includes scientific research tools, reagents, instrumentation, and services dedicated to the study of glycoconjugates, including glycoproteins, glycolipids, and proteoglycans, which play critical roles in cellular communication, immune response, and disease pathogenesis. Unlike genomics or proteomics, glycobiology investigates the structurally complex and heterogeneous sugar moieties attached to biomolecules, which is a field long considered technically challenging but now gaining momentum due to advances in mass spectrometry and bioinformatics.

As per the European Molecular Biology Organization, numerous academic and clinical laboratories across Europe actively conduct glycomics research with significant clusters in Germany, the United Kingdom, Sweden, and Switzerland. The European Union has allocated more than 85 million euros since 2021 under Horizon Europe to projects investigating glycosylation in cancer, neurodegeneration, and infectious diseases. According to the European Medicines Agency, several biologics approved in the EU between 2020 and 2024 require precise glycosylation profiling for batch consistency, underscoring regulatory recognition of glycobiology’s therapeutic relevance.

MARKET DRIVERS

Rising Integration of Glycosylation Analysis in Biopharmaceutical Development

Biopharmaceuticals, particularly monoclonal antibodies, represent a cornerstone of modern therapy in Europe, and their efficacy, safety, and stability are profoundly influenced by glycosylation patterns, which are one of the major factors propelling the growth of the European glycobiology market. According to the European Medicines Agency, a majority of approved therapeutic proteins are glycosylated, and minor alterations in sugar structures can trigger immunogenicity or reduce half-life. In 2024, the European Commission mandated enhanced glycan characterization for all new biosimilar submissions under its updated Guideline on Similar Biological Medicinal Products. This regulatory shift has intensified demand for high-resolution analytical platforms such as liquid chromatography, mass spectrometry, and capillary electrophoresis across contract development organizations. Germany hosts numerous biopharma firms with in-house glycoanalytical capabilities as per the German Association of Research-Based Pharmaceutical Companies. Furthermore, the rise of antibody-drug conjugates and fusion proteins, many of which are in late-stage trials in Europe as per the European Society for Medical Oncology, requires rigorous glycan monitoring to ensure target specificity and payload delivery. This convergence of regulatory science and therapeutic innovation solidifies glycobiology as an indispensable pillar in Europe’s advanced therapy ecosystem.

Expansion of Glycomics in Precision Diagnostics for Cancer and Rare Diseases

Glycosylation aberrations serve as sensitive biomarkers for early disease detection, with altered glycan signatures now validated in cancers, neurodegenerative conditions, and congenital disorders of glycosylation, which is further boosting the expansion of the European glycobiology market. According to the European Reference Network for Rare Diseases, over 130 distinct CDG subtypes have been identified, many diagnosable only through specialized glycomics workflows such as MALDI-TOF mass spectrometry of serum transferrin. In oncology, the CA19-9 antigen used in pancreatic cancer monitoring is a sialylated Lewis antigen whose interpretation requires glycoform context. A multicenter study coordinated by the Karolinska Institute in Sweden demonstrated that combining core fucosylation profiles with standard imaging improved hepatocellular carcinoma detection sensitivity. National health systems are responding accordingly, with France’s Plan France Médecine Génomique 2025 now incorporating glycomics into its multi-omics diagnostic pipeline. Similarly, the UK Biobank has begun glycan profiling of hundreds of thousands of participant samples to correlate glycosylation traits with long-term health outcomes. These initiatives transform glycobiology from a niche research domain into a clinically actionable discipline, driving sustained investment in diagnostic infrastructure and trained personnel across Europe.

MARKET RESTRAINTS

Technical Complexity and Lack of Standardized Analytical Protocols

Glycobiology remains hindered by the absence of universal methodologies for glycan release, labeling, separation, and data interpretation, unlike the standardized pipelines available in genomics, which is a key restraint to the European glycobiology market growth. According to the European Glycosciences Forum, fewer than one-third of European laboratories use identical protocols for N-linked glycan analysis, leading to inter-lab variability that compromises data reproducibility. The structural diversity of glycans, including branching, linkage isomerism, and modifications like sulfation, demands orthogonal techniques such as exoglycosidase sequencing and ion mobility spectrometry, which are costly and require expert operation. A survey by the Max Planck Society revealed that many glycomics researchers in Germany spend a significant portion of project time optimizing sample preparation rather than biological interpretation. Moreover, public databases like UniCarbKB and GlyTouCan remain fragmented with inconsistent annotation standards, limiting machine learning applications. This methodological fragmentation not only slows discovery but also deters pharmaceutical sponsors seeking robust quality control frameworks, thereby constraining translational potential despite strong biological rationale.

Acute Shortage of Specialized Glycoscience Expertise

Europe faces a critical deficit in scientists trained at the intersection of carbohydrate chemistry, bioinformatics, and cell biology, which are essential for advancing glycobiology and further impeding the glycobiology market growth in Europe. According to the European Federation of Biotechnology, fewer than 200 PhD-level glycoscientists graduate annually across the EU, with concentrations limited to elite institutions in Oxford, Utrecht, and Copenhagen. The European Training Network for Glycoscience reported that a majority of advertised postdoctoral positions in glycomics remained unfilled due to narrow candidate pools. This scarcity impedes both academic progress and industrial adoption, as biopharma companies struggle to staff analytical development teams capable of interpreting complex glycan datasets. In France, national research agencies have flagged glycoscience as a strategic skills gap in their workforce assessment. Meanwhile, educational curricula in life sciences rarely include dedicated glycomics modules, perpetuating a cycle of underexposure. Without urgent investment in cross-disciplinary training programs and career incentives, Europe risks ceding leadership in this high-value field to regions with more coordinated talent development strategies, such as the United States and Japan.

MARKET OPPORTUNITIES

Therapeutic Glycoengineering of Next Generation Biologics

Europe is emerging as a hub for rational glycoengineering to enhance the efficacy and safety of protein therapeutics through controlled manipulation of glycosylation pathways, which is a prominent opportunity in the European glycobiology market. According to the Paul Ehrlich Institute, German regulatory authorities approved several glycoengineered antibodies between 2022 and 2024, including obinutuzumab, which features reduced fucose content to amplify antibody-dependent cellular cytotoxicity against B-cell malignancies. Academic spin-outs such as Glycotope GmbH in Berlin and Lectiva Therapeutics in Leiden are pioneering platform technologies that enable site-specific glycan remodeling using enzymatic or cell line engineering approaches. The European Investment Bank committed 60 million euros in 2023 to support the scale-up of these platforms under its Innovation Finance Initiative. Furthermore, the inclusion of glycooptimized vaccines, such as those targeting HIV envelope glycans, in the European Vaccine Initiative’s portfolio signals expanding applications beyond oncology. With dozens of glycoengineered candidates in preclinical development across EU institutions, this frontier merges synthetic biology with clinical need, offering a pathway to superior biologics that leverage sugar code precision for targeted immune modulation.

Integration of AI-Driven Glycoinformatics Platforms

The application of artificial intelligence to decode the glycome offers a transformative opportunity for the European glycobiology market. According to the European Bioinformatics Institute, its GlyConnect platform uses deep learning algorithms to predict glycosylation sites and glycan structures from genomic and proteomic inputs with high accuracy in benchmark tests against experimental data. Startups like Glycanostics in Sweden and SugarX in Switzerland are commercializing cloud-based tools that automate spectral interpretation and integrate glycomics with multi-omics datasets. In 2024, the European High Performance Computing Joint Undertaking allocated 12 million euros to develop exascale computing workflows for large-scale glycan simulation, enabling virtual screening of glycan-protein interactions. These digital advances address historical bottlenecks in data analysis while democratizing access for non-specialist labs. As per the European Open Science Cloud, the volume of glycomics data is projected to grow significantly by 2027, making AI-driven platforms essential infrastructure for accelerating biomarker discovery and therapeutic design across the continent.

MARKET CHALLENGES

High Instrumentation and Reagent Costs Limit Broad Accessibility

Advanced glycobiology research demands capital-intensive instrumentation such as high-resolution mass spectrometers with ion mobility capabilities and specialized HPLC systems equipped with fluorescent or electrochemical detectors, which is challenging the European glycobiology market growth. According to the German Research Foundation, the average cost of establishing a fully functional glycomics core facility exceeds 1.2 million euros, excluding recurring expenses for isotopically labeled standards and enzymatic kits. In Southern and Eastern Europe, where research budgets are constrained, only a limited share of universities maintain dedicated glycan analysis platforms, as per a survey by the Central European Institute of Technology. Even in wealthier nations, shared equipment often suffers from backlogs with long wait times, delaying project timelines. Commercial reagents for glycan release, such as PNGase F variants or procainamide labeling kits, remain expensive and restrict experimental scope. These financial barriers create a two-tier research landscape where only well-funded institutions can pursue cutting-edge questions, thereby stifling innovation and equitable participation across the European Research Area.

Regulatory Ambiguity in Clinical Translation of Glycan-Based Biomarkers

Despite promising diagnostic potential, most glycan-based biomarkers lack clear regulatory pathways for clinical validation and commercialization in Europe, which is further challenging the expansion of the European glycobiology market. According to the European Society of Clinical Microbiology and Infectious Diseases, no glycomics-derived test has yet received CE IVD certification as a standalone diagnostic despite years of peer-reviewed evidence linking specific glycoforms to disease states. Regulatory bodies, including the European Medicines Agency and notified bodies under IVDR, provide limited guidance on analytical validation requirements for heterogeneous glycan signatures, which do not conform to traditional binary biomarker models. A review by the French National Agency for Medicines and Health Products Safety noted that glycan assays often fail to meet repeatability thresholds due to biological variability and technical noise, leading to high attrition in clinical trial contexts. This uncertainty discourages diagnostic companies from investing in assay development even when academic proof of concept exists. Until harmonized regulatory frameworks acknowledge the probabilistic nature of glycomic signatures, Europe will struggle to convert its strong basic science output into tangible patient-facing innovations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, End User, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Bruker Corporation, Takara Bio, Inc., Thermo Fisher Scientific and Waters Corporation, Danaher Corporation, New England Biolabs, ProZyme, Inc., Shimadzu Corporation, Merck KGaA (Germany), Agilent Technologies. |

SEGMENTAL ANALYSIS

By Product Insights

The kits and reagents segment dominated the market by holding 45.4% of the European glycobiology market share in 2025. The dominance of kits and reagents segment in the European market is attributed to their essential role as consumables in routine glycan analysis workflows across academic and industrial laboratories. Researchers rely on standardized kits for enzymatic deglycosylation, fluorescent labeling, and glycan release, which ensure reproducibility and reduce method development time. In Germany, a majority of university core facilities reported using commercial glycan labeling kits from vendors such as ProZyme and Takara Bio as per the German Society for Biochemistry and Molecular Biology. The European Union’s Horizon Europe program has funded more than 35 collaborative projects since 2021 that mandate the use of CE-marked reagents to comply with data quality standards. Additionally, the rise of high-throughput screening in biopharma necessitates bulk procurement of consistent reagent batches, enabling scale economies for suppliers and reinforcing recurring demand. This operational indispensability cements kits and reagents as the backbone of glycobiology infrastructure.

The instruments are projected to expand at a CAGR of 11.4% over the forecast period, owing to the adoption of next-generation analytical platforms capable of resolving glycan structural complexity with high precision. High-resolution mass spectrometers equipped with ion mobility separation, such as those from Waters and Thermo Fisher Scientific, are increasingly deployed in national reference laboratories to support regulatory submissions for glycosylated biologics. In Sweden, the SciLifeLab national infrastructure invested 28 million euros in 2024 to upgrade its glycomics instrumentation suite, enabling real-time glycan mapping of therapeutic antibodies. Similarly, France’s CNRS established a pan-institutional consortium to share access to cryo-electron microscopy coupled with glycoproteomics workflows. These capital investments reflect a strategic shift from descriptive glycomics toward functional and spatial glycosylation analysis. As AI-driven data interpretation tools mature, instrument vendors are integrating software ecosystems that automate spectral annotation, further lowering the expertise barrier and expanding the user base beyond traditional glycoscience hubs.

By Application Insights

The drug discovery segment commanded for 40.8% of the regional market share in 2025. The leading position of the drug discovery segment in the European market is attributed to the critical role of glycosylation in the pharmacokinetics, immunogenicity, and target engagement of biotherapeutics. A large proportion of monoclonal antibodies in clinical development within the EU require detailed glycan profiling during cell line selection and process optimization as mandated by the European Medicines Agency’s Guideline on Development of Monoclonal Antibodies. Major pharmaceutical companies, including Roche, Novartis, and AstraZeneca, maintain dedicated glycoanalytical teams in their Basel, Gothenburg, and Cambridge R&D centers, respectively. In 2024, the Innovative Medicines Initiative launched the GlycoDelete II consortium with 65 million euros in public-private funding to engineer simplified glycosylation pathways for improved drug consistency. Furthermore, the rise of antibody-drug conjugates and bispecifics, many of which are in Phase II trials across Europe, demands rigorous control over Fc glycan composition to modulate effector functions. This deep integration into biologics innovation ensures sustained demand for glycobiology tools throughout the drug development continuum.

The oncology segment is a promising segment and is predicted to register a CAGR of 14.1% over the forecast period. Factors such as the validation of tumor-associated carbohydrate antigens as both diagnostic biomarkers and immunotherapeutic targets are propelling the growth of the oncology segment in the regional market. Aberrant sialylation, fucosylation, and truncated O-glycans are now recognized hallmarks of malignancy with clinical utility in cancers such as pancreatic, ovarian, and triple-negative breast cancer. A multicenter trial coordinated by the Netherlands Cancer Institute demonstrated that serum levels of sialyl Lewis X predicted metastatic relapse in colorectal cancer patients with high sensitivity. Consequently, diagnostic developers like Fujirebio Europe are advancing CE-marked assays that quantify specific glycoforms in liquid biopsies. Moreover, glycoengineered cancer vaccines, such as those targeting Globo H and TF antigens, are entering late-stage trials in Germany and Switzerland. The European Commission’s Cancer Mission has prioritized glycomics as a cross-cutting technology, accelerating funding and collaboration. This convergence of biomarker validation, therapeutic targeting, and policy support positions oncology as the most dynamic frontier in European glycobiology.

By End User Insights

The academic research institutions segment led the market by holding 50.9% of the regional market share in 2025. The growth of the academic research institutions segment in the European market can be credited to Europe’s long-standing strength in fundamental life sciences, with hundreds of universities hosting active glycoscience laboratories as documented by the European Glycosciences Forum. National research councils in Germany, France, and the UK consistently fund glycomics under thematic priorities such as host-pathogen interactions and stem cell biology. For instance, the German Research Foundation allocated 18 million euros in 2024 to collaborative research centers focused on glycan-mediated signaling. Doctoral training networks like GlyCoCan and GLYCOPHARM have graduated more than 120 PhD students since 2020, creating a pipeline of specialized talent. Core facilities at institutions such as the University of Copenhagen and Imperial College London provide open access to advanced instrumentation, fostering interdisciplinary collaboration. While commercial applications are growing, academic labs remain the primary incubators of novel methodologies and biological insights that later translate into diagnostics and therapeutics.

The contract research organizations (CRO) segment is the fastest-growing end-user segment and is anticipated to grow at a CAGR of 15.5% over the forecast period. This rapid ascent is propelled by biopharmaceutical companies outsourcing complex glycan characterization to specialized CROs possessing regulatory-compliant platforms and expert staff. Firms such as Charles River Laboratories, Eurofins, and Evotec have established dedicated glycoanalytical service lines offering end-to-end support from cell line screening to lot release testing. In 2024, Evotec inaugurated a GMP-certified glycomics lab in Hamburg capable of supporting IND-enabling studies for biosimilars and novel biologics. The implementation of the EU’s revised Guideline on Similar Biological Medicinal Products has intensified demand for comparative glycan fingerprinting, driving CROs to invest in orthogonal methods like LC-MS and CE-LIF. Additionally, the rise of glycoengineered cell and gene therapies requires CROs to develop new assays for viral vector glycosylation, a niche but high-value service area. As regulatory expectations grow, so does reliance on third-party expertise, making CROs indispensable accelerators in Europe’s advanced therapy ecosystem.

COUNTRY-LEVEL ANALYSIS

Germany Glycobiology Market Analysis

Germany held the leading share of 26.5% of the European glycobiology market in 2025. The country’s dominance is anchored in its dense network of world-class research institutions, including the Max Planck Institutes, Helmholtz Centers, and Technical Universities that collectively publish a large number of peer-reviewed glycomics papers annually. Germany hosts major biopharma R&D hubs in Munich, Berlin, and Mainz, where companies like BioNTech and Merck KGaA integrate glycan analysis into mRNA vaccine and monoclonal antibody development. The Federal Ministry of Education and Research has committed 45 million euros since 2022 to the Glyco3 initiative promoting glycoscience infrastructure and industry collaboration. National reference laboratories routinely use glycomics for biosimilar comparability studies under Paul Ehrlich Institute oversight. This synergy of academic excellence, regulatory rigor, and industrial adoption establishes Germany as a central engine of glycobiology innovation in Europe.

United Kingdom Glycobiology Market Analysis

The United Kingdom accounted for 16.9% of the regional market share in 2025. The growth of the UK in the European market is driven by its concentration of elite universities and biotech clusters. According to the UK Research and Innovation body, more than 40 academic groups at institutions such as Oxford, Imperial College, and the University of York actively investigate glycan roles in immunity, infection, and neurodegeneration. The Francis Crick Institute operates one of Europe’s most advanced integrated glycoproteomics platforms supporting both basic and translational projects. Post-Brexit, the UK increased its investment in life sciences through the Life Sciences Vision, allocating 12 million pounds in 2023 specifically for glycoengineering of next-generation therapeutics. Companies like GlycoThera and Lectiva Therapeutics have emerged from this ecosystem, securing venture funding for glycan-targeted platforms. The Medicines and Healthcare products Regulatory Agency maintains close alignment with EMA on glycosylation requirements, ensuring continued access to European markets. This blend of scientific depth, agile regulation, and entrepreneurial energy sustains the UK’s influential role despite geopolitical shifts.

Switzerland Glycobiology Market Analysis

Switzerland is estimated to register a prominent CAGR in the European glycobiology market during the forecast period, owing to its precision science and global pharmaceutical leadership. As per the Swiss National Science Foundation, glycoscience features prominently in national research programs, with ETH Zurich and the University of Geneva pioneering methods in glycan synthesis and imaging. The presence of Novartis and Roche in Basel creates direct demand for high-fidelity glycan analytics to support biologics such as ocrelizumab and trastuzumab emtansine. In 2024, the Swiss government launched the GlycoInnovate initiative, providing tax incentives for companies developing glycan-based diagnostics. Swissmedic, the national regulator, participates in EMA working groups on biosimilars, ensuring harmonized glycosylation standards. Moreover, Switzerland’s neutrality facilitates international collaboration with both EU and non-EU partners, enhancing data sharing and technology transfer. This unique confluence of academic rigor, industrial scale, and regulatory sophistication enables Switzerland to contribute significantly to glycobiology despite its smaller population.

France Glycobiology Market Analysis

France is projected to account for a notable share of the European glycobiology market during the forecast period, owing to the centralized research planning and strong public investment. According to the French National Centre for Scientific Research (CNRS), more than 25 laboratories across Paris, Lyon, and Toulouse focus on glycan-mediated mechanisms in microbiology and oncology. The Pasteur Institute maintains a WHO reference center for glycoconjugate vaccine development, particularly against bacterial meningitis. France’s Plan France 2030 allocated 30 million euros in 2023 to establish a national glycomics platform offering open access to advanced instrumentation. Public health agencies increasingly recognize glycan biomarkers in early cancer detection, with pilot programs for prostate and liver cancer underway in Marseille and Strasbourg. Collaborative frameworks like the French Glycoscience Network foster knowledge exchange between academia and SMEs. This top-down support, combined with clinical integration, ensures France remains a pivotal contributor to Europe’s glycoscience advancement.

Sweden Glycobiology Market Analysis

Sweden is anticipated to grow at a healthy CAGR in the European glycobiology market over the forecast period, owing to innovations in glycoimmunology and digital integration. According to the Swedish Research Council, glycobiology is a strategic priority within the national life science strategy, with Karolinska Institutet and Lund University leading studies on glycan checkpoints in autoimmune diseases and cancer immunotherapy. The SciLifeLab national infrastructure provides cloud-based glycoinformatics tools used by numerous research groups across Scandinavia. In 2024, the Swedish Innovation Agency Vinnova granted 9 million euros to Glycanostics, a Stockholm-based startup developing AI-powered glycan diagnostic algorithms for inflammatory bowel disease. Sweden’s participation in the Nordic Glycomics Consortium enables shared biobank resources and standardized protocols across borders. Moreover, Swedish biotechs like Affibody and Alligator Bioscience incorporate glycoengineering into their therapeutic pipelines, enhancing half-life and tissue targeting. This fusion of computational biology, clinical insight, and entrepreneurial agility positions Sweden as a forward-looking force in the evolving European glycobiology landscape.

COMPETITIVE LANDSCAPE

The Europe glycobiology market features a competitive landscape dominated by multinational life science technology providers alongside specialized reagent developers and emerging bioinformatics startups. Competition centers not on price but on analytical depth, workflow integration, and regulatory compliance, particularly in biopharmaceutical applications where glycosylation directly impacts product approval. Established players like Thermo Fisher, Merck, and Agilent leverage their broad portfolios to offer end-to-end solutions, while niche firms differentiate through enzyme specificity or AI-driven data tools. Academic excellence in countries like Germany, Sweden, and the UK fuels demand for cutting-edge instrumentation, yet also creates pressure for continuous innovation. Regulatory alignment with EMA guidelines serves as both a barrier and a differentiator, as only vendors with validated methods gain traction in GMP environments. Despite technical complexity, the market is gradually democratizing through user-friendly platforms and shared infrastructure initiatives, fostering broader participation beyond traditional glycoscience hubs.

KEY MARKET PLAYERS

Key players dominating the Europe glycobiology market profiled in this report are

- Bruker Corporation

- Takara Bio, Inc.

- Thermo Fisher Scientific

- Waters Corporation

- Danaher Corporation

- New England Biolabs

- ProZyme, Inc.

- Shimadzu Corporation

- Merck KGaA

- Agilent Technologies

TOP PLAYERS IN THE MARKET

- Thermo Fisher Scientific is a pivotal contributor to the Europe glycobiology market through its comprehensive portfolio of mass spectrometry systems, chromatography platforms, and glycan labeling kits. The company supplies advanced instrumentation such as the Orbitrap Astral MS, which enables high-sensitivity glycomics profiling to leading academic centers and biopharmaceutical firms across Germany, France, and the UK. Globally, Thermo Fisher supports regulatory-compliant workflows for glycosylated biologics development, aligning with EMA and FDA guidelines. Recently, the company launched an integrated glycoproteomics software module for its BioPharma Finder platform, enhancing automated glycan identification and quantification. This innovation strengthens its position by reducing data analysis time and improving reproducibility for researchers navigating complex glycosylation patterns in therapeutic proteins.

- Merck KGaA plays a central role in the Europe glycobiology ecosystem by providing specialized enzymes, reagents, and sample preparation kits under its Sigma Aldrich and Millipore brands. Its offerings include endoglycosidases, fluorescent tags, and HILIC columns tailored for N and O-linked glycan analysis, widely adopted in European core facilities. The company contributes to global standards development through collaboration with organizations like the Consortium for Functional Glycomics. In recent years, Merck expanded its glycoengineering capabilities by launching cell culture media formulations that modulate glycosylation profiles during monoclonal antibody production. It also enhanced its online technical support portal with glycan workflow templates, accelerating method adoption among non-specialist users and reinforcing its reputation as a solutions-oriented partner in precision glycoscience.

- Agilent Technologies significantly advances the Europe glycobiology market through its high-performance liquid chromatography and mass spectrometry solutions optimized for glycan separation and structural characterization. Its 1290 Infinity III LC system, coupled with the 6545XT AdvanceBio Q TOF MS, which is routinely used in EU biopharma quality control labs for batch consistency testing of glycosylated therapeutics. Agilent’s global impact includes co-developing reference methods with the National Institute of Standards and Technology to improve inter-laboratory comparability. To strengthen its European footprint, the company recently introduced a cloud-based glycan library integrated with its MassHunter software, enabling real-time spectral matching against curated databases. This digital enhancement empowers researchers to achieve faster and more confident glycan annotation, supporting both discovery and regulated applications.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe glycobiology market focus on integrating hardware, software, and consumables into seamless analytical workflows to enhance user productivity and data reliability. They invest heavily in application-specific solution development, such as glycoprofiling for biosimilars or glycoform monitoring in vaccine production. Strategic collaborations with academic institutions and regulatory bodies help establish methodological standards and drive technology adoption. Companies also prioritize digitalization by embedding artificial intelligence and cloud-based libraries into their platforms to simplify complex data interpretation. Additionally, they expand localized technical support and training programs to address the shortage of glycoscience expertise and lower barriers to entry for new users across diverse research settings.

MARKET SEGMENTATION

This Europe glycobiology market research report is segmented and sub-segmented into the following categories.

By Product

- Enzymes

- Instruments

- Kits & Reagents

By Application

- Diagnostic

- Drug Discovery

- Oncology

By End User

- Academic Research Institutions

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe glycobiology market?

The Europe glycobiology market involves research on glycans for diagnostics and therapies across biotech firms and institutions.

Why is the Europe glycobiology market growing?

The Europe glycobiology market grows due to demand for glycan biomarkers and chronic disease research in pharmaceuticals.

What applications exist in the Europe glycobiology market?

In the Europe glycobiology market, applications include biomarker discovery and glycan-based therapeutics development.

Who leads the Europe glycobiology market?

Leading players in the Europe glycobiology market are biotech and pharma companies focusing on glycoengineering innovations.

What trends shape the Europe glycobiology market?

Trends in the Europe glycobiology market feature AI integration for glycan analysis and personalized medicine advances.

How does glycobiology impact healthcare in the Europe glycobiology market?

Glycobiology drives diagnostics for cancer in the Europe glycobiology market via altered glycan pattern studies.

What role do glycans play in the Europe glycobiology market?

Glycans act as biomarkers and therapy targets in the Europe glycobiology market for various diseases.

Which countries dominate the Europe glycobiology market?

Germany, UK, and France lead the Europe glycobiology market with advanced research infrastructures.

What challenges face the Europe glycobiology market?

Challenges in the Europe glycobiology market include complex glycan analysis and regulatory frameworks.

How does the Europe glycobiology market support drug development?

The Europe glycobiology market aids drug development through glycan engineering for biologics efficacy.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com