Europe Glyphosate Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By Crop Type, Application, And By Region (The UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034.

Europe Glyphosate Market Size

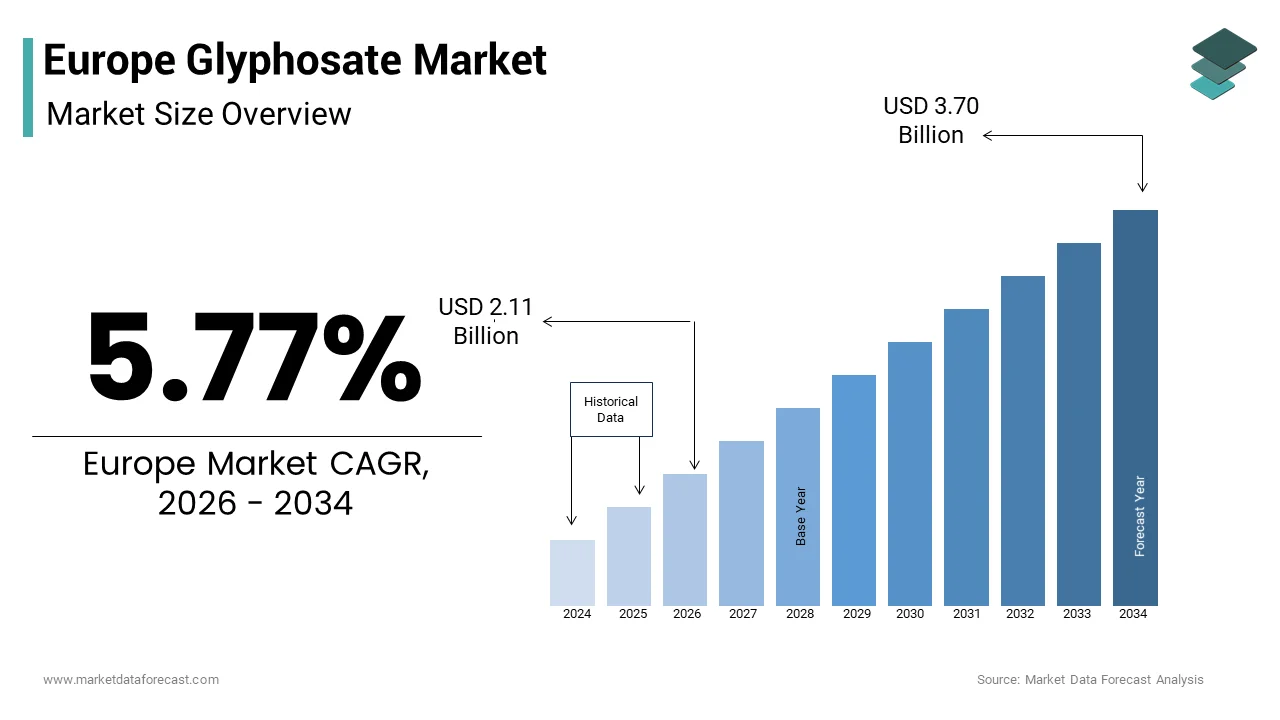

The Europe glyphosate market size was valued at USD 1.97 billion 2025 and is anticipated to reach USD 2.11 billion in 2026 to reach USD 3.70 billion by 2034, estimated to grow at a CAGR of 5.77% during the forecast period from 2026 to 2034.

Glyphosate is a broad-spectrum systemic herbicide widely used across Europe for pre-sowing weed control, crop desiccation, and maintenance of non-agricultural areas such as railways and industrial zones. Chemically classified as an organophosphorus compound, it functions by inhibiting the EPSP synthase enzyme essential for plant amino acid synthesis. Despite its efficacy, glyphosate remains one of the most scrutinized agrochemicals in the European Union due to ongoing debates over its potential health and environmental impacts. Scientific evaluations suggest a low likelihood of a carcinogenic hazard to humans from glyphosate use under common conditions; however, its regulatory position is still debated. A significant amount of cultivated land in the relevant region relies on chemical methods for weed control, with glyphosate historically being prominent in certain soil management practices. A temporary market approval for glyphosate was permitted, including provisions that allow individual areas to set their own limits on its use. Countries like Germany and France have enacted phase-out timelines, while others, including Spain and Poland, continue permitting their use under strict application protocols. This fragmented regulatory landscape defines the Europe glyphosate market not as a unified commercial space but as a patchwork of national risk assessment, policy preferences, and agronomic necessities.

MARKET DRIVERS

Adoption of Conservation Agriculture Practices Sustains Glyphosate Dependency

Conservation agriculture, which emphasizes minimal soil disturbance, permanent soil cover, and crop rotation, relies heavily on chemical weed control to maintain field productivity without ploughing, and it drives the growth of the Europe glyphosate market. Across Europe, a significant area of farmland is managed using conservation agriculture principles. Glyphosate is a primary tool utilized in these systems for managing cover crops and controlling perennial weeds. The use of no-till systems has expanded considerably in several countries, including Spain, France, and Italy. No-till methods offer benefits such as reducing soil erosion and enhancing carbon sequestration. Farms employing no-till practices may experience reduced diesel consumption and lower soil CO2 emissions compared to conventional tillage methods. National agronomic advisory services in Romania and Bulgaria actively promote glyphosate-based termination protocols to support soil health targets under the Common Agricultural Policy. The lack of a similar, cost-effective alternative for pre-sowing weed management means conservation farming's viability continues to rely on glyphosate, even with political challenges.

Infrastructure and Non-Crop Area Management Require Reliable Vegetation Control

Glyphosate remains indispensable for managing vegetation in public infrastructure and industrial zones where mechanical alternatives are impractical or unsafe, which boosts the expansion of the Europe glyphosate market. Many national rail operators within the region utilize chemical methods for managing trackside vegetation. Shifting to manual weed removal along railway corridors is associated with higher maintenance costs and presents potential worker safety hazards. Similarly, airports, highways, and utility rights of way depend on targeted glyphosate applications to ensure operational safety. Restricted use of certain substances in non-agricultural settings is permitted under specific regulations. Alternative vegetation control methods may require more frequent applications to achieve similar results along rail lines. This operational necessity in critical infrastructure ensures continued, if limited, glyphosate usage even in countries that have banned it in farming.

MARKET RESTRAINTS

National Bans and Phased Withdrawals Severely Limit Agricultural Use

A growing number of European Union member states have enacted outright bans or accelerated phase-out plans for glyphosate in agricultural settings, directly constricting market access, which in turn degrades the growth of the Europe glyphosate market. Several European nations are progressing toward significant restrictions or full prohibitions on the agricultural use of glyphosate. Germany is set to end all agricultural use of glyphosate. France is implementing a roadmap for the progressive reduction of glyphosate use, targeting a near-total ban with only limited exceptions for certain farming systems. Austria and Luxembourg have already established full bans on the substance. The actions taken by these nations are substantially reducing the available market for products containing glyphosate within the European region. Even in countries where it remains legal, such as Italy and Poland, farmers face increasing social and retailer pressure to avoid glyphosate, with major supermarket chains requiring residue-free certification for fresh produce. These regulatory and commercial fragmentation forces manufacturers to maintain separate product portfolios and compliance strategies for each jurisdiction, increasing operational complexity and diminishing economies of scale.

Intensified Public Opposition and Retailer Restrictions Suppress Demand

Persistent public skepticism about glyphosate’s safety, amplified by media coverage and non-governmental organization campaigns, has translated into consumer pressure and retail policies that indirectly suppress usage, and thereby hinder the expansion of the Europe glyphosate market. A majority of European citizens express support for an EU-wide ban on glyphosate, regardless of recent scientific reassessments by safety authorities. This sentiment influences purchasing behavior. Major retailers, including Carrefour,r Ede, ka and T, Tesco now enforce private standards prohibiting glyphosate residues above detection limits in fresh fruits and vegetables. In response, contract farmers supplying these chains have abandoned glyphosate, regardless of national legality, opting for more expensive and less effective alternatives. This de facto market exclusion,n driven by consumer perception rather than regulatory mandate, significantly erodes dem, particularly in high-value horticultural sectors across Western and Northern Europe.

MARKET OPPORTUNITIES

Development of Precision Application Technologies Enhances Stewardship and Acceptability

Innovations in precision agriculture offer a pathway to sustain glyphosate use through targeted application that minimizes environmental dispersion and human exposure. This ultimately provides new opportunities for the growth of the Europe glyphosate market. AI-powered weed recognition technology has been demonstrated to reduce the use of certain chemicals in agriculture. The use of AI technology can maintain effective weed control while minimizing chemical application. There is a move in some regions toward mandating the inclusion of advanced technology on professional sprayers, such as drift reduction nozzles and real-time dosage controls. Regulatory frameworks at a broader regional level encourage the use of precision agriculture methods as a way to cut the overall risk associated with pesticide use. By transforming glyphosate from a broadcast tool into a surgical intervention, manufacturers can reposition it as a responsible component of integrated weed management rather than a blanket solution.

Integration into Integrated Weed Management Frameworks Extends Functional Relevance

Forward-looking agronomists are embedding glyphosate within integrated weed management systems to offer fresh prospects for the expansion of the Europe glyphosate market. This approach combines cultural, mechanical, and chemical tactics to delay resistance and reduce the overall load. Multiple agricultural extension services are currently encouraging practices that minimize the application of glyphosate. These practices often focus on applying the herbicide only during specific, crucial stages of crop growth, such as before planting or harvesting. In certain regions, farmers involved in integrated weed management programs have successfully decreased their overall use of herbicide active ingredients. These reductions in herbicide use were achieved without negatively impacting crop yields. These frameworks treat glyphosate as a strategic reserve rather than a routine input, enhancing its longevity and social license. Agrochemical companies are responding by co-developing decision support tools that recommend optimal timing and dosage based on field scouting and weather data. This shift from volume-based to strategy-based usage allows glyphosate to retain relevance in a sustainability-constrained agricultural future.

MARKET CHALLENGES

Emergence of Glyphosate-Resistant Weed Populations Undermines Efficacy

The repeated and often exclusive reliance on glyphosate in certain cropping systems has accelerated the evolution of resistant weed biotypes across the region, which threatens its long-term utility, and negatively impacts the growth of the Europe glyphosate market. Multiple instances of weed species that are resistant to glyphosate have been identified across various regions. In one specific area, a significant portion of winter wheat fields showed reduced effectiveness of glyphosate against a common weed. This resistance forces farmers to resort to more toxic older herbicides or costly mechanical interventions, negating the economic and environmental advantages that once justified glyphosate use. The use of integrated approaches to manage resistance is inconsistent, with many farmers not following the suggested practice of rotating different herbicide types. The effectiveness of glyphosate is decreasing because regions aren't coordinating, allowing resistance to build even where its use is legal.

Legal and Insurance Liabilities Create Commercial Uncertainty

Ongoing litigation and shifting liability frameworks are among the major barriers to the Europe glyphosate market. This poses significant non-regulatory risks to glyphosate manufacturers and distributors in Europe. EU-level court decisions regarding product approvals do not preclude ongoing national legal actions. National courts continue to be a venue for civil claims related to product use. A recent preliminary national court decision allowed for collective action regarding environmental concerns linked to a specific product. That particular case is proceeding through the national court system for further review. Simultaneously, major European insurers, including Allianz and AXA, have revised product liability policies to exclude coverage of glyphosate-related claims unless manufacturers demonstrate enhanced stewardship protocols. The legal ambiguity discourages investment in formulation innovation and distribution partnerships, particularly among smaller national distributors wary of downstream liability. The commercial environment for glyphosate will continue to face unpredictable risks, unrelated to science or agriculture, until judicial and insurance frameworks are stabilized.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.77% |

| Segments Covered | By Crop Type, Application, Non-Crop, And & Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe |

| Market Leaders Profiled | Monsanto company (U.S.), Syngenta AG (Switzerland), Bayer AG (Germany), E.I. Du Pont De Nemours & Company (U.S.), The Dow Chemical Company (U.S.), Nufarm limited (Australia), Nantong Jiangshan Agrochemical & Chemical, Inc. (China), Adama Agricultural Solutions Ltd (Israel), UPL Limited (India), and Zhejiang Xinan Chemical Industrial Group Co., Ltd. (China). |

SEGMENTAL ANALYSIS

By Crop Insights

The conventional crops segment was the prominent segment in the Europe glyphosate market and accounted for a substantial share in 2024. The European Union’snear-totall prohibition of genetically modified herbicide-tolerant crops in commercial agriculture has mainly contributed to the prominence of the conventional crops segment. A minimal amount of available land in the EU is used for cultivating GM crops, primarily limited to specific regions where insect-resistant maize is permitted. Consequently, glyphosate is used almost exclusively in conventional systems for pre-sowing burndown pre pre-harvest desiccation, and fallow weed control. In some agricultural areas, the use of glyphosate for managing weeds before planting non-GM crops like sunflower and barley is a common practice. Similarly, in Eastern Europe, glyphosate remains critical for managing perennial weeds in conventional wheat and rapeseed rotations. National agronomic guidelines in Poland and Romania continue to recommend glyphosate as the most cost-effective tool for establishing clean seedbeds in no-till systems. This regulatory and agronomic reality ensures that conventional cropping, not biotechnology, defines glyphosate usage patterns across Europe.

The conventional crops segment also remains the fastest-growing segment, with a CAGR of 2.1% from 2025 to 2033 due to the expansion of conservation agriculture in regions where glyphosate is still legally permitted. The implementation of no-till and reduced tillage systems in the EU is expanding. In Spain and Italy, where glyphosate remains authorized for agricultural use, farmers are increasingly adopting pre-sowing glyphosate applications to terminate cover crops without tillage, thereby complying with soil health mandates. Conventional wheat farms utilizing certain management practices in no-till systems can achieve notable reductions in fuel use and increases in soil organic carbon over time. Even as Western European nations phase out glyphosate, its strategic role in sustainable soil management in Southern and Eastern Europe ensures continued, albeit geographically constrained, growth within the conventional crop segment.

By Crop-Based Application Insights

The grains and cereals segment led the Europe glyphosate market in 2024 and captured a 63.6% share in 2024. The leading position of the grains and cereals segment is driven by the extensive use of glyphosate for pre-sowing weed control and pre-harvest desiccation in wheat, barley, and oats across key producing regions. In some regions, an established practice for managing field residue involves using a particular herbicide on significant areas of winter wheat. In Spain, glyphosate is routinely applied as a pre-harvest desiccant in barley destined for malting to ensure uniform ripening and harvest timing. National agronomic advisory services in Romania and Bulgaria continue to promote glyphosate-based burndown protocols as the most economical method to control problematic grasses like blackgrass in cereal rotations. The large scope of cereal production in Europe means that these crops represent a major application area for this herbicide, primarily used for its effectiveness in weed control.

The oil seeds segment is likely to experience the fastest CAGR of 3.4% during the forecast period, owing to the expansion of on-till rapeseed and sunflower cultivation in Southern and Eastern Europe, where glyphosate remains permitted. Sunflower production area has shown an upward trend in a key agricultural region of Europe. Farmers in this area commonly use glyphosate to manage difficult broadleaf weeds before planting crops. Reduced tillage methods are increasingly used in another European region for managing rapeseed cultivation. This approach generally incorporates the use of glyphosate for preparing the seedbed. The European Commission’s Protein Plan further incentivizes oilseed expansion to reduce import dependency, with glyphosate serving as a key enabler of sustainable establishment. This agronomic synergy ensures oil seeds will drive the next phase of glyphosate adoption in permissible regions.

By Non-Crop Application Insights

The turf and ornamental grass segment held the leading share of the Europe glyphosate market in 2024. The dominance of the turf and ornamental grass segment is attributed to the herbicide’s irreplaceable role in maintaining high-quality amenity spaces, including golf courses, sports fields, public parks, and roadside verges, where manual or mechanical weed control is impractical. Most professional football stadiums incorporate specific methods for managing weeds around their pitches. National railway operators in Sweden and the Netherlands continue to apply glyphosate along track ballast to prevent vegetation from compromising drainage and signaling systems. Although residential use is banned in many countries, professional turf managers retain legal access under strict licensing. Alternative weed control methods often necessitate significantly more applications to manage resilient perennial weeds effectively. This operational necessity highly-visibility managed landscapes, sustains glyphosate demand in non-agricultural settings despite public scrutiny.

The turf and ornamental segment is also on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 1.8% from 2025 to 2033. The rapid expansion of the turf and ornamental segment is fuelled by the increasing stringency of mechanical alternatives and the adoption of precision application technologies that enhance stewardship. Integrated vegetation management plans are being adopted for professional sports grounds, prioritizing glyphosate as a measure of last resort. The strategic use of glyphosate has increased in some areas because approved alternatives have proven less effective. Protocols for public green spaces now allow the use of glyphosate with specific application methods that help eliminate drift, such as wick applicators or shielded sprayers. The use of technology like GPS-guided spot spraying can significantly reduce the overall volume of glyphosate needed while maintaining the quality of turf in managed parks. Regulatory changes are prompting a move from complete bans to a system that manages risk for professional use, leading to more defensible, targeted, and efficient turf and ornamental applications. This ensures that the reliance on glyphosate in Europe’s managed landscapes persists, albeit in a refined capacity.

COUNTRY ANALYSIS

Spain Glyphosate Market Analysis

Spain was the top performer in the Europe glyphosate market and accounted for a 29.6% share in 2024. The domination of the German market is primarily driven by its continued legal authorization of glyphosate in agriculture, combined with vast arable lands under extensive cropping systems. Certain cereal and oilseed crops are managed with a particular herbicide for application during specific stages of growth. There is no immediate national timeline for discontinuing the use of this herbicide. One agricultural management approach acknowledges the role of this herbicide in systems designed to minimize soil disturbance. This approach is used across a considerable portion of the area dedicated to growing cereals. Additionally, Spain hosts the EU’s only significant GM maize cultivation, though minimal, further anchoring herbicide infrastructure. Public opposition remains lower than in Northern Europe,e, with farmer cooperatives like ASAJA actively defending its use. This regulatory permissiveness, agronomic necessity, ty and political support make Spain the de facto stronghold of glyphosate in European agriculture.

France Glyphosate Market Analysis

France was the second-largest country in the Europe glyphosate market and captured an 18.8% share in 2024. Residual usage persists in limited exemptions for perennial crops like vines and orchards, where mechanical alternatives risk root damage. Vineyard management practices currently include the use of certain herbicides in specific regions. Additionally, non-crop applications along railways and industrial zones remain legal under Decree 2023-- 412. Government programs are providing funding this year to help farmers shift to different methods for managing weeds. This transitional reality, where policy ambition outpaces practical alternatives, ensures France retains significant though declining glyphosate activity as Europe’s former largest market navigates its exit strategy.

Germany Glyphosate Market Analysis

Germany is also a major country in the Europe glyphosate market as it implements its full agricultural ban by the end of the year. However, non-agricultural use remains permitted for critical infrastructure, including railways, airports, and military zones. An amendment allows for exceptions to certain plant protection rules regarding public infrastructure maintenance. The use of the specific application has significantly decreased on conventional farms over the last few years. This bifurcated landscape, total exclusion in farming versus strategic retention in infrastructure, captures Germany’s risk-managed approach to glyphosate in its final phase of agricultural use.

Italy Glyphosate Market Analysis

Italy expanded steadily in the Europe glyphosate market. While Northern regions like Lombardy enforce strict local bans, Southern regions, including Puglia and Sicily, continue widespread use in olive groves, vineyards, and cereal systems. A significant amount of durum wheat cultivation in the South utilizes glyphosate for weed control before sowing in no-till systems. National policy allows regional autonomy, creating a patchwork where usage persists where agronomic need is highest, nd alternatives are least viable. Restricting the use of glyphosate in the South could raise production costs and impact the capacity for soil carbon sequestration. This regional pragmatism ensures Italy remains a significant though declining market as national cohesion on agrochemical policy remains elusive.

Poland Glyphosate Market Analysis

Poland is emerging as a key growth region in the Europe glyphosate market due to its embrace of conservation agriculture and absence of national restrictions. A government program discusses the use of a particular herbicide for managing cover crops as a way to address climate concerns. Farmer representatives indicate a widely held view among their members that the use of the herbicide is important for maintaining the viability of grain exports. Unlike Western Europe, public opposition remains minimal, with trust in agronomic institutions high. This alignment of policy agronomy and social acceptance positions Poland as the new frontier of glyphosate use in a rapidly restricting European landscape.

COMPETITIVE LANDSCAPE

The Europe glyphosate market is defined not by aggressive commercial rivalry but by strategic retreat, adaptation, and stewardship amid escalating regulatory and social pressure. Competition among remaining players centers on technical differentiation, precision delivery systems, EM, S, and compliance infrastructure rather than pricing or volume. Incumbents like Ayeryer Synea and Nufarm operate in a shrinking but fragmented landscape where national bans coexist with infrastructure exemptions and agronomic necessity in Southern and Eastern Europe. The market is increasingly bifurcated between agricultural use—rapidly declining in the West—and professional non-crop applications—retained for safety and practicality in transport and utilities. New entrants are virtually absent due to reputational risk and regulatory complexity. Success hinges on demonstrating responsible use through training digital tools and integration into conservation agriculture frameworks. As the EU moves toward a pesticide risk reduction target of fifty percent by 2030, glyphosate’s future depends not on market dominance but on its defensible role as a last resort tool in specific high need contexts.

KEY MARKET PLAYERS

The key players that are present in the glyphosate industry include

- Monsanto Company (U.S.)

- Syngenta AG (Switzerland)

- Bayer AG (Germany)

- E.I. Du Pont De Nemours & Company (U.S.)

- The Dow Chemical Company (U.S.)

- Nufarm Limited (Australia)

- Nantong Jiangshan Agrochemical & Chemical, Inc. (China)

- Adama Agricultural Solutions Ltd (Israel)

- UPL Limited (India)

- Zhejiang Xinan Chemical Industrial Group Co., Ltd. (China).

Top Players In The Market

- Bayer AG remains a central figure in the Europe glyphosate market as the original developer and global marketer of glyphosate under the Roundup brand. Despite legal and regulatory headwind,,s the company continues to supply glyphosate formulations to professional users in countries where it remains authorized for agricultural and non-crop use. The firm also invested in closed transfer systems to minimize handler exposure and environmental drift. Collaborations with farmer cooperatives in Spain and Poland focus on integrating glyphosate into conservation agriculture protocols, reinforcing its role as a soil health enabler rather than a standalone herbicide. These science-based engagement strategies aim to preserve glyphosate’s functional relevance amid increasing scrutiny.

- Syngenta Group contributes significantly to the Europe glyphosate market through its generic glyphosate formulations tailored for professional turf infrastructure and permitted agricultural uses. The company leverages its extensive distribution network across Southern and Eastern Europe to serve markets where glyphosate remains legally accessible. The firm also co-developed decision support software with agricultural universities in Italy and Romania to optimize glyphosate timing in no-till systems. By aligning its offerings with national integrated weed management guidelines, Syngenta positions itself as a responsible supplier focused on risk mitigation and agronomic efficiency rather than volume sales.

- Nufarm Limited plays a strategic role in the Europe glyphosate market by supplying high-purity glyphosate formulations to professional users in permissible geographies, including Spain,n Pola, nd and the Czech Republic. The company’s European manufacturing facility in the Netherlands ensures regulatory compliance with EU biocidal and plant protection standards. The firm also partnered with railway maintenance contractors in Germany and Sweden to provide certified training on targeted application methods that comply with national infrastructure exemptions. These initiatives reinforce Nufarm’s focus on technical differentiation and professional user support in a shrinking but still critical European market.

Top Strategies Used By The Key Market Participants

Key players in the Europe glyphosate market prioritize regulatory compliance by aligning formulations and labeling with national authorizations and EU Sustainable Use Regulation requirements. They invest in stewardship programs that promote precision application and buffer zone adherence to minimize environmental impact. Companies develop closed transfer systemslow-driftdrift nozzles to reduce handler exposure and off-target movement. Strategic partnerships with farmer cooperatives, ilway operators, and municipal authorities ensure continued access in permitted non-crop and agricultural segments. Firms also provide digital decision support tools that integrate weather, soil, and weed data to optimize timing and dosage. They focus on professional user training and certification to reinforce responsible use narratives. FinaFinallyyhey reposition glyphosate as a strategic component within integrated weed management rather than a standalone solution to extend its functional relevance in a sustainability-driven policy environment.

MARKET SEGMENTATION

This research report on the European glyphosate market is segmented and sub-segmented into the following categories.

By Crop Type

- GM Crops

- Conventional Crops

By Application

- Crop-based which includes

- Grains & Cereals

- Oil Seeds

- Fruits & Vegetables

By Non-Crop

- Turf & Ornamental Grass

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is glyphosate used for in Europe?

Glyphosate is a broad-spectrum herbicide used to control weeds in crops, orchards, vineyards, grasslands, and non-crop areas like railways and industrial sites.

Why is glyphosate important for European agriculture?

It helps farmers manage weeds efficiently, reduces labor and fuel use, and supports no-till or reduced-till farming systems that protect soil health.

Which crops rely most on glyphosate in Europe?

Cereals, oilseeds, corn, sugar beets, orchards, and vineyards often use glyphosate for pre-plant weed control or between-row management.

Why is glyphosate a topic of debate in Europe?

Concerns about environmental impact, biodiversity, and long-term health effects have led to strict regulations and ongoing discussions about restricted use or alternatives.

What trends are shaping glyphosate use in Europe?

A shift toward controlled application, precision spraying, integrated weed management, and a greater interest in organic or mechanical weed control.

Which countries use glyphosate the most?

Major agricultural producers such as France, Germany, Spain, Poland, and the UK have seen historically high demand due to large crop acreage.

Are farmers looking for alternatives to glyphosate?

Yes, due to regulatory pressure and public concern, some farmers are testing mechanical weeding tools, cover crops, crop rotation strategies, and non-glyphosate herbicides.

What challenges does the glyphosate market face in Europe?

Regulatory restrictions, rising compliance costs, evolving safety guidelines, and the need for more sustainable weed-control practices.

Why is glyphosate still widely used despite restrictions?

Because it remains one of the most effective and affordable weed-control tools, especially for large-scale farming, where alternatives may be costlier or less efficient.

What is the outlook for glyphosate use in Europe?

Use is expected to remain under strict regulation, with gradual movement toward safer formulations, reduced application rates, and integration with more sustainable weed-management systems.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com