Europe Green Data Center Market Size, Share, Trends, & Growth Forecast Report By Service (Professional Services, Monitoring Services),Solution, End-user and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Green Data Center Market Report Summary

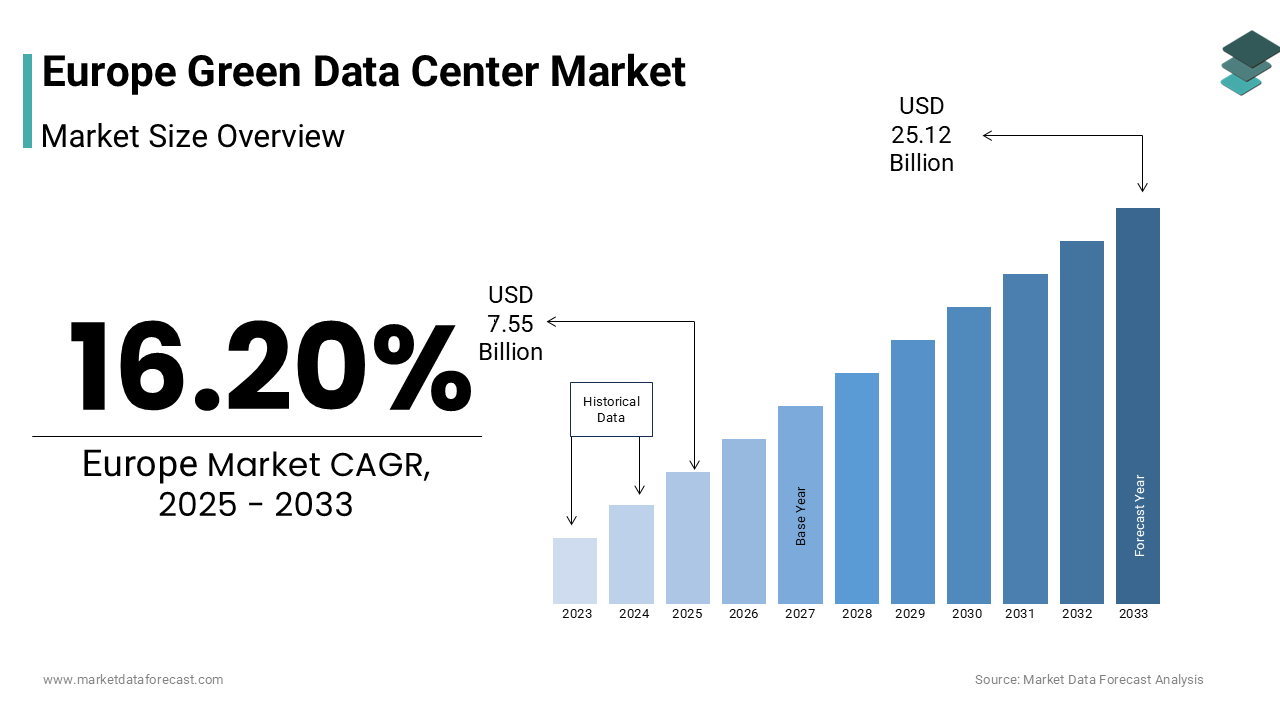

The Europe Green Data Center Market Report was valued at USD 6.50 billion in 2024, is projected to reach USD 7.55 billion in 2025, and is expected to grow substantially to USD 25.12 billion by 2033, expanding at a CAGR of 16.20% from 2025 to 2033. The market growth is driven by stringent EU climate regulations, rising enterprise demand for low-carbon digital infrastructure, and the surge in energy-intensive AI and cloud workloads. Advancements in efficient cooling technologies, broader integration of renewable power and energy storage, and policy frameworks like the Climate Neutral Data Centre Pact are accelerating green data center adoption while site selection and grid constraints continue to shape deployment strategies.

Key Market Trends

- Rapid uptake of liquid immersion and outside-air economization to reduce PUE and cooling energy consumption.

- Expansion of on-site renewables, corporate PPAs, and battery storage to support 24/7 low-carbon operations.

- Proliferation of AI-driven monitoring and energy orchestration software for real-time optimization and predictive maintenance.

- Rise of edge and micro green data centers to serve latency-sensitive applications with modular, low-impact designs.

- Increasing emphasis on water stewardship, circular materials, and lifecycle carbon accounting in site approvals and investor due diligence.

Segmental Insights

- Based on service, the professional services segment dominated in 2024, driven by demand for sustainability compliance, energy modeling, and green certification advisory.

- Based on solution, the power infrastructure segment commanded the largest share in 2024, reflecting investments in UPS, on-site PV, BESS, and advanced power conversion to meet hourly renewable matching and resilience requirements.

- Based on end-user industry, financial institutions accounted for a leading share in 2024 owing to strict ESG disclosure mandates and low-latency, high-reliability needs; healthcare is poised for strong growth as digital health workloads increase.

Regional Insights

- Germany held the largest share at 22.8% in 2024, driven by a mature industrial base, strong renewables mix, and Frankfurt’s hyperscale hub status.

- The United Kingdom is a key market with strong policy alignment to net-zero goals and concentrated demand from finance and media hubs around London.

- The Netherlands benefits from high connectivity (AMS-IX), progressive sustainability covenants, and offshore wind integration, making it a strategic green data center location.

- Sweden is attractive for near-carbon-free power and free-air cooling advantages, yielding some of Europe’s lowest average PUEs.

- France leverages a low-carbon, nuclear-heavy grid and domestic digital sovereignty initiatives that favor certified green data center deployments.

Competitive Landscape

The Europe Green Data Center Market is increasingly competitive as hyperscalers, colocation providers, telecom groups, and infrastructure vendors differentiate on verified sustainability credentials, renewable access, and circular design. Market advantage hinges on securing grid connections or dedicated renewables, demonstrating water-efficient cooling strategies, and offering robust transparency through third-party certifications (ISO 14001, LEED) and continuous reporting. Strategic alliances with energy providers, municipalities, and technology partners are common to mitigate permitting, grid, and community risks while enabling scalable green deployments.Prominent players operating in the market include Schneider Electric SE, Vertiv Co., Eaton Corporation plc, ABB Ltd, Equinix, Inc., Digital Realty Trust, Inc., Green Mountain AS, IBM Corporation, Hewlett Packard Enterprise (HPE), Cisco Systems, Inc., and Siemens AG.

Europe Green Data Center Market Size

The europe green data center market size was valued at USD 6.50 billion in 2024 and is anticipated to reach USD 7.55 billion in 2025 from USD 25.12 billion by 2033, growing at a CAGR of 16.20% during the forecast period from 2025 to 2033.

Green data centers are facilities engineered to minimize environmental impact through energy efficiency, renewable power integration, advanced cooling technologies, and sustainable construction practices. These data centers prioritize reduced power usage effectiveness ratios, water conservation, and lifecycle carbon reduction. According to the International Energy Agency, digital infrastructure across Europe consumes roughly 2.5% of the region’s total electricity and this demand is increasing due to rapid cloud adoption, artificial intelligence workloads, and tightening data sovereignty regulations. The European Union’s Climate Neutral Data Centre Pact targets full climate neutrality for all data centers by 2030, which is supported by the broader objectives of the European Green Deal. According to Eurostat, about 42% of the EU’s electricity generation in 2023 came from low-carbon sources, which is creating a favorable macro energy environment for sustainable digital operations. Cooling systems in conventional data centers can account for up to 40% of total energy consumption but green technologies such as liquid immersion cooling and outside-air economization are gaining momentum as efficient alternatives. The physical footprint of digital infrastructure is also under scrutiny, with land use constraints, permitting delays, and community opposition emerging as key non-market factors shaping data center deployment strategies across EU member states.

MARKET DRIVERS

Stringent Climate Regulations Accelerate Adoption of Sustainable Infrastructure

The comprehensive climate policy framework of the European Union is propelling the growth of the green data center market growth in Europe. Legislative instruments such as the Corporate Sustainability Reporting Directive mandate extensive environmental disclosures, which is compelling operators to adopt verifiable decarbonization pathways. The EU Taxonomy for Sustainable Activities further defines technical screening criteria that classify data center investments as environmentally sustainable only if they meet specific energy efficiency and renewable energy thresholds. According to the European Environment Agency, data centers accounted for about 1% of the European Union’s total greenhouse gas emissions in 2022, which is underscoring the regulatory urgency surrounding their decarbonization. The Climate Neutral Data Centre Pact is signed by more than 50 leading industry stakeholders and this requires participants to report annually on their progress toward carbon neutrality, water stewardship, and circular economy adoption. The Energy Efficiency Directive also sets binding targets for EU member states to reduce final energy consumption by 19% by 2030 compared to 2005 levels, which is creating a compliance-driven market pull for sustainable data center designs. Facility operators are increasingly investing in on-site solar photovoltaic generation and securing renewable energy through long-term corporate power purchase agreements. According to the European Commission, more than 300 such agreements were signed across the EU in 2023, which is indicating a structural shift in energy sourcing behavior that extends beyond traditional operational efficiency measures.

Rising Energy Costs Reinforce Investment in Energy Efficient Technologies

Persistently elevated electricity prices across Europe have intensified the economic rationale for energy-optimized data infrastructure is further contributing to the expansion of the green data center market in Europe. According to Eurostat, the average industrial electricity price in the European Union was approximately €0.18 per kilowatt hour (or €180 per megawatt hour) in mid-2024, which is remaining well above pre-2021 levels as energy markets continue to stabilize after the crisis. This sustained cost pressure is prompting operators to minimize grid dependency through advanced efficiency strategies. Modern green data centers commonly achieve power usage effectiveness (PUE) ratios close to 1.2 while older facilities often operate above 1.7. According to the Lawrence Berkeley National Laboratory, direct liquid cooling can reduce cooling-related energy consumption by up to 80% compared with traditional air-based systems. The adoption of dynamic load management and AI-based power optimization allows real-time adjustment of server utilization and cooling output. In Germany, where industrial electricity tariffs averaged about €0.22 per kilowatt hour in 2023, hyperscale operators have increasingly migrated compute loads to Nordic countries offering lower-cost, renewable hydropower. According to the Nordic Data Centre Association, data center electricity demand in Sweden and Finland continued double-digit growth through 2023, which is reflecting strong inflows of such relocations. These dynamics illustrate how evolving energy economics are shaping both site selection and technology adoption in European green data center market.

MARKET RESTRAINTS

High Capital Expenditure for Sustainable Infrastructure Deters Widespread Adoption

The upfront investment required to implement green data center technologies remains a significant barrier, particularly for mid-tier operators and colocation providers, which is majorly impeding the growth of the green data center market in Europe. According to the European Data Centre Association, constructing a new facility that complies with the EU Code of Conduct for Data Centre Energy Efficiency typically involves higher capital expenditure than conventional builds due to the inclusion of specialized cooling systems and renewable energy integration through on-site generation or battery storage, and advanced building management technologies. Retrofitting existing infrastructure presents even greater challenges because of limited structural flexibility and the risk of operational downtime. According to the Fraunhofer Institute for Systems and Innovation Research, payback periods for energy efficiency retrofits in Western Europe can extend over several years, which many firms view as financially difficult under current economic conditions. The shortage of skilled labor with expertise in sustainable design and energy optimization also increases project costs and timelines. In Southern Europe, where investment access remains more constrained, only a minority of data centers have completed comprehensive energy efficiency upgrades, according to national-level assessments such as those by the Italian Data Center Observatory. These combined financial and technical barriers continue to slow the pace of data center decarbonization across the region despite supportive regulatory frameworks.

Geographic and Grid Capacity Constraints Limit Green Data Center Expansion

The availability of suitable locations with robust renewable energy access and grid capacity is increasingly scarce across densely populated European regions, which is also hampering the expansion of the European green data center market. According to EirGrid, Ireland’s transmission system operator, data centers are projected to account for roughly 30% of the country’s electricity demand by 2027, which has prompted a temporary pause on new grid connections in the Dublin region. Similarly, in the Netherlands, national grid operator TenneT has suspended new large-scale data center connections in parts of the Randstad area due to grid congestion expected to persist until at least 2026. According to the European Network of Transmission System Operators for Electricity (ENTSO-E), around 60 gigawatts of renewable energy and industrial projects across Europe are currently delayed because of limited grid capacity. Moreover, community resistance to data center development has grown in regions facing water scarcity or visual impact concerns, particularly in rural areas with high renewable potential. In Sweden, municipal authorities in Norrbotten have introduced stricter zoning rules following local protests over land-use changes. These combined constraints are forcing operators to postpone projects, consider less optimal sites, or invest in off-grid solutions such as dedicated wind farms or green hydrogen backup systems, which is further complicating deployment economics and timelines.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence Drives Demand for Energy Optimized Compute Facilities

The rapid deployment of generative artificial intelligence workloads across Europe is creating unprecedented demand for high-performance computing infrastructure that simultaneously adheres to strict sustainability mandates, which is one of the promising opportunities in the European green data center market. According to the International Energy Agency, global data center electricity consumption is projected to double by 2026, which is reaching more than 1,000 terawatt-hours annually, roughly matching Japan’s total power use. This growing energy intensity has prompted major cloud providers to prioritize green data centers equipped with liquid cooling and powered by low-carbon or renewable sources. Microsoft’s European expansion includes a €2 billion investment in Sweden, designed to leverage the nation’s predominantly nuclear and hydropower-based grid. Similarly, Google has pledged that all its data centers worldwide will run on 24/7 carbon-free energy by 2030, a commitment exceeding standard annual renewable energy matching. According to the European High Performance Computing Joint Undertaking, more than half of new EU supercomputing capacity commissioned since 2022 supports AI and is hosted in facilities adhering to the EU Code of Conduct for Data Centre Energy Efficiency. In parallel, the European Chips Act earmarks €43 billion for domestic semiconductor and data infrastructure development, favoring energy-efficient and resilient architectures. These converging efforts position green data centers not merely as compliance tools but as strategic assets underpinning Europe’s AI and digital sovereignty.

Expansion of Edge Computing Creates Decentralized Demand for Micro Green Data Centers

The proliferation of latency-sensitive applications such as autonomous vehicles, industrial IoT, and smart city infrastructure is driving the deployment of edge data centers across European urban and industrial zones, which is further providing prominent opportunities for the European green data center market. Unlike hyperscale facilities, these micro data centers must operate within strict spatial, energy, and noise constraints often in repurposed commercial buildings. This environment necessitates inherently green designs that minimize resource use and integrate seamlessly with local infrastructure. According to the European Telecommunications Standards Institute, a growing share of new edge computing deployments in Europe integrates modular liquid cooling and direct current (DC) power architectures to improve overall energy efficiency. The European Union’s Digital Europe Programme has allocated about €1.5 billion to strengthen edge infrastructure for public services such as healthcare and transportation, with sustainability criteria embedded in procurement requirements. In Germany, Deutsche Telekom has introduced a network of containerized edge facilities powered entirely by on-site solar photovoltaic panels and second-life electric vehicle batteries. According to the European Environment Agency, the number of urban data processing nodes across Europe is expected to increase significantly by 2027, which will require innovative thermal management systems and greater use of circular materials. These distributed computing nodes represent a fundamental shift toward localized, sustainable digital infrastructure, where green attributes are designed in from the outset rather than added retrospectively.

MARKET CHALLENGES

Shortage of Skilled Workforce Impedes Implementation of Advanced Green Technologies

The successful deployment and operation of green data centers require specialized expertise in areas such as thermal fluid dynamics, renewable energy integration, and AI-enabled facility management, which is primarily challenging the growth of the European green data center market. However, Europe faces a pronounced talent gap in these interdisciplinary domains. According to the European Commission’s 2024 Digital Skills and Jobs Coalition report, Europe’s data center sector is expected to require around 150,000 additional skilled professionals by 2027, with green technology expertise identified as the fastest-growing competency gap. This shortage is already delaying project timelines, inflating labor costs, and increasing the risk of suboptimal system performance. For example, improper calibration of liquid cooling systems can offset expected energy savings, while poorly structured power purchase agreements may result in stranded renewable assets. According to a survey by the Green Data Center Academy, only about 23% of EU member states currently offer certified training programs in sustainable data infrastructure, which is underscoring significant gaps in workforce readiness. Competition for skilled labor from adjacent industries such as electric vehicle manufacturing and renewable energy development further exacerbates the shortage. Without a coordinated, EU-wide upskilling strategy, the adoption of advanced green technologies will likely remain uneven across member states and is undermining the data center sector’s collective decarbonization progress.

Water Scarcity Conflicts with Evaporative Cooling Requirements

Despite advances in dry cooling and liquid immersion, many green data centers in Europe still rely partially on evaporative or adiabatic cooling systems, which consume significant volumes of water and further challenging the expansion of the European market. This poses a growing conflict in regions experiencing prolonged droughts and declining freshwater availability. According to the European Drought Observatory, more than 30% of the European Union’s land area experienced severe or extreme drought conditions during the summer of 2023, which is marking one of the most widespread drought events since records began in 2011. According to the European Environment Agency, Spain faces chronic water stress, with several river basins experiencing demand that far exceeds sustainable renewable water supply levels. A typical large-scale (100-megawatt) data center using evaporative cooling can consume millions of liters of water each year, roughly equivalent to the annual usage of thousands of residents, which indicates the scale of potential local impact. In response, the French government introduced mandatory water impact assessments for new digital infrastructure projects in 2024 to ensure more sustainable water use. Operators across Europe are increasingly deploying closed-loop cooling systems and rainwater harvesting solutions, although these approaches add both technical complexity and capital cost. As climate models project increasing aridity across Southern and Central Europe through 2050, the intersection of digital expansion and water scarcity is emerging as a major operational and reputational risk for the data center market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Service, Solution, End User Industry and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, and the Czech Republic. |

| Market Leader Profiled | Schneider Electric SE, Vertiv Co., Eaton Corporation plc, ABB Ltd, Equinix, Inc., Digital Realty Trust, Inc., Green Mountain AS, IBM Corporation, Hewlett Packard Enterprise (HPE), Cisco Systems, Inc., Siemens AG |

SEGMENTAL ANALYSIS

By Service Insights

The professional services segment dominated the market by holding 37.5% of the European market share in 2024. The growth of the professional services segment in the European market is driven primarily by the complexity of sustainability compliance and infrastructure transformation. Enterprises increasingly rely on expert consultancy for energy modeling carbon footprint auditing and green certification processes such as LEED or ISO 50001. According to the European Commission, the implementation of the EU Taxonomy and the Corporate Sustainability Reporting Directive (CSRD) has significantly increased demand for professional advisory services across the data center industry as operators seek compliance with new sustainability disclosure and performance requirements. Many new projects in Western Europe now routinely engage external sustainability consultants to conduct lifecycle assessments and integrate circular economy principles, both of which are encouraged under the European Green Deal. According to a 2024 Deloitte insights report on digital infrastructure, most European data center operators identify complex regulatory compliance as a leading factor driving outsourcing of environmental and ESG advisory services. The Green Data Center Academy further notes that only a minority of mid-sized European firms currently employ in-house sustainability engineers, which is intensifying reliance on external expertise. This convergence of stringent environmental legislation and technical complexity has positioned professional services as a central pillar of green data center development across the region and propelling the growth of the professional services segment in the European market.

The monitoring services segment is expected to exhibit the fastest CAGR during the forecast period in the European green data center market due to real time energy and thermal performance tracking becoming critical for operational decarbonization. Advanced monitoring platforms now integrate AI driven anomaly detection and predictive maintenance reducing unplanned outages and energy waste. According to the International Energy Agency, continuous digital energy monitoring in industrial and commercial facilities can reduce energy consumption by 10–20% compared with reliance on periodic manual audits, illustrating its growing importance for efficiency optimization. The European Union’s Energy Efficiency Directive requires large energy consumers, including data centers with installed power above 500 kilowatts, to implement granular sub-metering and regular energy performance reporting, which is driving widespread adoption of monitoring technologies. According to Siemens, its data center monitoring solutions have seen strong year-on-year growth across Europe, particularly in Germany and the Nordic countries, as operators pursue real-time optimization. Major cloud providers such as AWS and Google Cloud now require continuous sustainability telemetry from their colocation partners as part of their 24/7 carbon-free energy strategies. According to Gartner’s 2024 analysis, more than 80% of new European green data centers integrate third-party monitoring APIs to enable automated sustainability reporting for regulators and investors. This convergence of regulatory, operational, and reputational drivers are boosting the growth of the monitoring services segment in the European market.

By Solution Insights

The power infrastructure segment commanded for 41.8% of the European market share in 2024 and emerged as the leading performer. The leading position of the power infrastructure segment in the European market is attributed to its foundational role in energy sourcing and efficiency. Key components include uninterruptible power supplies renewable energy integration systems and high efficiency transformers. The transition to low carbon grids and the EU’s requirement for hourly matching of electricity consumption with renewable generation have intensified investments in on site photovoltaics battery energy storage and green hydrogen backup systems. According to the European Commission, a growing majority of newly permitted data centers in Europe now integrate renewable power procurement mechanisms, such as corporate power purchase agreements (PPAs) and co-located solar or wind farms to meet tightening sustainability targets under EU climate policy. The revised EU Code of Conduct for Data Centre Energy Efficiency establishes stricter technical standards, including limiting power distribution losses to below 5%, which is accelerating the deployment of advanced power conversion and energy management technologies. According to BloombergNEF, Europe added over 14 gigawatts of new battery storage capacity in 2023, with data centers representing a notable share of non-grid storage installations as operators seek on-site resilience and renewable integration. This regulatory and technological convergence around grid stability and carbon performance ensures that power infrastructure segment remains a cornerstone of green data center design across the continent.

The management software segment is anticipated to experience most rapid growth due to its indispensable role in optimizing energy use across dynamic computing environments. These platforms unify power cooling workload and carbon data into a single dashboard enabling real time sustainability governance. According to the International Energy Agency, the rapid rise of AI workloads has significantly increased power variability in data centers, with short-term spikes reaching several times baseline consumption, which is making adaptive software control essential for grid and operational stability. According to Schneider Electric, adoption of AI-enabled data center infrastructure management (DCIM) platforms has expanded rapidly across Europe as operators seek to optimize cooling, power distribution, and workload scheduling in real time. The European High-Performance Computing Joint Undertaking requires all publicly funded supercomputing facilities to implement certified energy orchestration software that complies with EN 50600-4-3 efficiency standards. In France, the government’s Green IT initiative mandates quarterly energy performance reporting for public-sector data centers, verified through management software analytics, which is accelerating adoption nationwide. According to IDC Europe, advanced DCIM systems typically improve power usage effectiveness (PUE) by around 0.2 to 0.3 points, translating to multi-million-euro annual energy savings for large-scale facilities. This combination of regulatory enforcement, operational necessity, and financial benefit firmly establishes the management software segment as one of the fastest-growing solution segments in Europe’s data center ecosystem.

By End User Industry Insights

The financial institutions segment accounted for 30.8% of the European market share in 2024. The dominance of the financial institutions segment is attributed to the stringent ESG disclosure mandates and reputational sensitivity. Banks asset managers and insurers are subject to the EU Sustainable Finance Disclosure Regulation which requires detailed reporting on the environmental footprint of their digital operations. According to the European Banking Authority, an increasing share of major European banks now include data center–related carbon intensity metrics in their annual sustainability disclosures, which is reflecting growing regulatory and stakeholder scrutiny. Financial institutions rely on low-latency, high-reliability digital infrastructure to process large transaction volumes, which has accelerated partnerships with green hyperscale providers such as Equinix and Digital Realty that operate certified sustainable campuses. UBS has transitioned its European cloud workloads to AWS regions powered by carbon-free energy, while HSBC has invested in a large-scale green data center lease in Frankfurt aligned with the Climate Neutral Data Centre Pact. According to PwC’s 2024 financial services sustainability report, most European banks now treat green data center certification as a mandatory vendor requirement rather than a differentiator. This alignment of regulatory reporting, client expectations, and digital transformation priorities positions the financial services segment as a key driver of green data center demand across Europe.

The healthcare segment is predicted to showcase a promising CAGR in the European green data center market during the forecast period owing to the digital health expansion and the energy intensity of medical data processing. Genomic sequencing AI diagnostics and telemedicine generate massive datasets requiring secure high-performance computing often hosted in green facilities to meet public sector sustainability mandates. According to the European Commission, the European Health Data Space initiative requires all EU member states to transition their health data infrastructure to compliant, energy-efficient data centers by 2027 to ensure both digital interoperability and environmental performance. In Sweden, institutions such as the Karolinska Institute have begun deploying research data centers powered entirely by renewable energy and supported by closed-loop cooling systems to reduce environmental impact. The European Commission’s Digital Europe Programme has earmarked more than €800 million to develop sustainable health data infrastructure, prioritizing projects achieving power usage effectiveness (PUE) ratios below 1.3. According to the Organisation for Economic Co-operation and Development (OECD), the healthcare sector’s digital storage requirements have surged across Europe due to the expansion of electronic health records and high-resolution medical imaging archives. The European Environment Agency estimates that healthcare contributes roughly 7% of the EU’s total carbon emissions, which is underscoring the sector’s need to decarbonize. Together, these developments position green data centers as critical infrastructure for Europe’s healthcare digitalization and climate accountability objectives.

REGIONAL ANALYSIS

Germany held the largest share of 22.8% of the regional market in 2024. The promising position of Germany in the European green data center market is attributed to its advanced industrial base robust renewable energy infrastructure and stringent regulatory environment. According to the Fraunhofer Institute for Solar Energy Systems, Germany generated approximately 52% of its electricity from renewable sources in 2023, creating a favorable environment for green data operations. Frankfurt remains Europe’s largest data center hub, hosting more than 80 facilities with a combined capacity exceeding 1 gigawatt, according to the German Data Centre Association. The Federal Government’s Data Centre Strategy 2030 mandates that all public sector data centers achieve a power usage effectiveness (PUE) below 1.4 and use 100% renewable electricity. Major new investments include Google’s €2 billion data center in St. Ghislain, Belgium and Microsoft’s renewable-powered AI campus in Berlin. According to Eurostat, Germany’s average industrial electricity price was among the highest in Europe in 2023, which has driven operators to invest in on-site solar power generation and large-scale battery storage. Additionally, growing community resistance to water-intensive cooling methods has accelerated the shift toward innovative dry and hybrid cooling systems, positioning Germany as a testbed for next-generation green data center design.

The United Kingdom is a prominent market for green data centers in Europe. London’s status as a global financial and digital hub and strong policy alignment with net zero goals are propelling the growth of the green data centers market in the UK. According to National Grid ESO, renewable sources supplied around 48% of the United Kingdom’s electricity generation in 2023, with wind power contributing roughly 29%, underscoring strong alignment between the country’s energy mix and green data infrastructure goals. The UK’s Climate Change Committee has set a target for all critical digital infrastructure to achieve net-zero emissions by 2040, with interim milestones beginning in 2025. The Slough and Croydon corridors together host more than 60 green-certified data centers serving major financial and media clients. Under the UK’s Digital Infrastructure Plan, new data centers must demonstrate both water efficiency and grid responsiveness to secure planning approval. Amazon Web Services has expanded its London region with a facility achieving a 1.15 power usage effectiveness (PUE) ratio, powered entirely by UK onshore and offshore wind farms. According to a 2024 TechUK report, nearly three-quarters of UK data center operators now deploy AI-driven load shifting to synchronize computing activity with renewable energy availability. Despite regulatory divergence following Brexit, the UK continues to maintain close technical alignment with EU sustainability frameworks, ensuring ongoing investor confidence in its green data infrastructure sector.

The Netherlands is anticipated to account for a notable share of the European market during the forecast period owing to its central European location high connectivity and progressive sustainability policies. Amsterdam is among the top three internet exchange points globally with AMS IX facilitating over 8 terabits per second of peak traffic. According to Statistics Netherlands, renewable sources accounted for about 47% of the country’s total electricity generation in 2023, driven largely by rapid offshore wind expansion in the North Sea. The Dutch government’s Data Centre Sustainability Covenant requires that all new facilities achieve a maximum power usage effectiveness (PUE) of 1.3 and use zero potable water for cooling by 2027. Despite a temporary 2022 moratorium on new grid connections in the congested Randstad region, national grid operator TenneT has since expedited over 2 gigawatts of dedicated green data center connections linked directly to offshore wind projects. Microsoft’s Amsterdam data center campus operates entirely on Dutch wind and geothermal energy, while Equinix employs aquifer thermal energy storage (ATES) systems to provide efficient, year-round cooling. Additionally, the Netherlands’ flat terrain and stable geology enable cost-effective underground data center construction, further enhancing its attractiveness as a hub for sustainable digital infrastructure.

Sweden is predicted to command for a prominent share of the European market during the forecast period due to its near carbon free electricity mix and cold climate enabling free air cooling. According to the Swedish Energy Agency, about 96% of Sweden’s electricity generation in 2023 came from renewable and nuclear sources, giving the country one of the cleanest power grids in Europe. The Stockholm, Uppsala, and Gothenburg corridors have become prime locations for hyperscalers aiming to meet 24/7 carbon-free energy targets. Following Google’s success with its Hamina facility in neighboring Finland, Sweden has attracted major investments such as Meta’s €800 million data center in Boden, which operates entirely on hydropower. The Swedish Environmental Protection Agency requires all data centers with a capacity above 1 megawatt to submit annual assessments covering water use and biodiversity impact, which is promoting responsible site selection and operations. According to the Nordic Data Centre Association, Swedish data centers achieve an average power usage effectiveness (PUE) of around 1.08, which is the lowest in Europe due to the extensive use of free-air cooling for most of the year. Additionally, Sweden’s abundant boreal forests are enabling circular construction practices, with wood-based modular data centers gaining popularity among sustainability-focused operators.

France is anticipated to account for a noteworthy share of the European market during the forecast period owing to the led digital sovereignty initiatives and a nuclear powered low carbon grid. In 2023 nuclear energy supplied 65% of France’s electricity while total low carbon sources exceeded 92% according to RTE the national grid operator. The French government’s France Relance plan allocates €1.2 billion to green data infrastructure with strict criteria on energy reuse and circular design. Paris Lyon and Marseille have emerged as key hubs with initiatives like the Green Datacenter Campus in Massy achieving ISO 14001 certification. The 2023 Digital Sovereignty Act requires all public entities to store sensitive data in French certified green data centers by 2026 accelerating domestic demand. Orange and Atos have partnered to deploy liquid cooled AI clusters powered by local hydroelectric plants in the Alps. According to Syntec Numérique the French professional services body over 60% of new private sector data center contracts in 2023 included mandatory third party green audits. France’s unique blend of state direction energy abundance and regulatory rigor positions it as a cornerstone of continental green digital infrastructure.

COMPETITIVE LANDSCAPE

The competition in the Europe green data center market is intensifying as global hyperscalers regional specialists and telecom backed providers vie for dominance in a highly regulated and sustainability driven environment. Players differentiate through energy efficiency innovation renewable energy access and compliance with evolving EU environmental mandates. The market features a mix of large scale hyperscale campuses and agile edge facilities catering to diverse client needs. Competitive advantage increasingly hinges on verified carbon neutrality water stewardship and circular design rather than just capacity or connectivity. New entrants face high barriers including grid access constraints permitting delays and community opposition particularly in water stressed regions. Incumbents respond by forming strategic alliances with energy providers local authorities and technology partners to secure resources and social license. Transparency in environmental reporting has become a key battleground with third party certifications such as ISO 14001 and LEED serving as trust signals. As artificial intelligence and sovereign cloud demands grow competition is shifting toward intelligent sustainable infrastructure capable of delivering both performance and planetary responsibility.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Green Data Center Market include

- Schneider Electric SE

- Vertiv Co.

- Eaton Corporation plc

- ABB Ltd

- Equinix, Inc.

- Digital Realty Trust, Inc.

- Green Mountain AS

- IBM Corporation

- Hewlett Packard Enterprise (HPE)

- Cisco Systems, Inc.

- Siemens AG

Top Players in the Market

Equinix

Equinix is a global digital infrastructure leader with significant footprint across Europe’s green data center landscape. The company operates over 40 sustainability certified facilities in the region including flagship campuses in London Frankfurt and Paris. Equinix has committed to achieving climate neutrality across its global portfolio by 2030 and actively participates in the EU Climate Neutral Data Centre Pact. In recent years it has deployed advanced liquid cooling systems and expanded its use of renewable energy through long term power purchase agreements with European wind and solar developers. Its emphasis on energy reuse such as capturing waste heat for district heating in the Netherlands demonstrates its integrated approach to sustainability.

Digital Realty

Digital Realty supports Europe’s digital transformation through a robust network of green data centers in key markets including Amsterdam Madrid and Dublin. The company prioritizes energy efficiency and renewable energy integration aligning with Science Based Targets initiative validation. It recently launched its PlatformDIGITAL sustainability framework to help clients measure and reduce their digital carbon footprint. Digital Realty has also pioneered water stewardship programs in water stressed regions and implemented AI driven cooling optimization across its European portfolio to lower power usage effectiveness ratios significantly enhancing its environmental performance and client appeal.

Vantage Data Centers

Vantage Data Centers has rapidly expanded its European presence with large scale sustainable campuses in Germany Netherlands and Italy. The company emphasizes modular design and low impact construction using recycled materials and energy efficient mechanical systems. Vantage recently secured long term renewable energy contracts with Iberdrola and Ørsted to power its facilities entirely with wind and solar energy. It also introduced its proprietary ECO program focusing on circular economy principles including server lifecycle management and heat reuse partnerships with local municipalities. These initiatives reflect its strategic commitment to embedding sustainability into core operations across the European market.

Top Strategies Used by the Key Market Participants

Key players in the Europe green data center market employ a range of strategic initiatives to reinforce their sustainability leadership and operational resilience. They prioritize long term renewable energy procurement through corporate power purchase agreements to ensure grid decarbonization alignment. Investment in advanced cooling technologies such as liquid immersion and indirect adiabatic systems reduces energy and water consumption significantly. Companies actively collaborate with local governments and utility providers to co develop dedicated renewable microgrids and grid stability solutions. Circular economy integration including waste heat recovery and sustainable material sourcing is increasingly embedded in new builds. Participation in industry pacts like the Climate Neutral Data Centre Pact provides credibility and collective accountability. Additionally firms leverage artificial intelligence for real time energy optimization and predictive maintenance to enhance efficiency. Strategic site selection in Nordic and Alpine regions capitalizes on natural cooling advantages. Partnerships with technology vendors enable deployment of next generation high density computing infrastructure compatible with green standards.

MARKET SEGMENTATION

The research report on the europe green data center market has been segmented and sub-segmented based on categories.

By Service

- Professional Services

- Monitoring Services

By Solution

- Power Infrastructure

- Management Software

By End User Industry

- Financial Institutions

- Healthcare

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe Green Data Center Market?

The Europe Green Data Center Market focuses on data centers designed for high energy efficiency, low carbon footprint, and sustainable operations using renewable energy sources and advanced cooling technologies.

What drives the growth of the Europe Green Data Center Market?

The market growth is driven by rising energy costs, strict European Union environmental regulations, and increased demand for sustainable IT infrastructure.

Which countries are leading the Europe Green Data Center Market?

Leading countries include Germany, the United Kingdom, the Netherlands, France, and the Nordic nations, particularly Norway and Sweden.

What are the major components of a green data center?

Key components include efficient power distribution units, renewable energy systems, advanced cooling technologies, and energy management software.

Which technologies are used to make data centers greener?

Technologies such as liquid cooling, AI-based energy management, DCIM (Data Center Infrastructure Management), and renewable energy integration are commonly used.

What is the current market size of the Europe Green Data Center Market?

The market is experiencing rapid growth and is expected to reach several billion USD by 2033, supported by digital transformation and sustainability initiatives.

Who are the key players in the Europe Green Data Center Market?

Major players include Schneider Electric SE, Vertiv Co., ABB Ltd, Eaton Corporation plc, Equinix, Digital Realty, and Green Mountain AS.

What challenges are faced by the Europe Green Data Center Market?

Challenges include high initial investment costs, limited renewable energy availability in some regions, and complex regulatory compliance.

How do green data centers impact IT companies in Europe?

They help IT companies reduce carbon emissions, align with ESG goals, and attract environmentally conscious clients and investors.

What future trends are expected in the Europe Green Data Center Market?

Trends include increasing adoption of AI-driven automation, modular data centers, hydrogen-powered facilities, and carbon-neutral operations.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com