Europe Greenhouse Irrigation Systems Market Size, Share, Trends & Growth Forecast Report, Segmented By Type, Application, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis Forecast From (2025 to 2033)

Europe Greenhouse Irrigation Systems Market Size

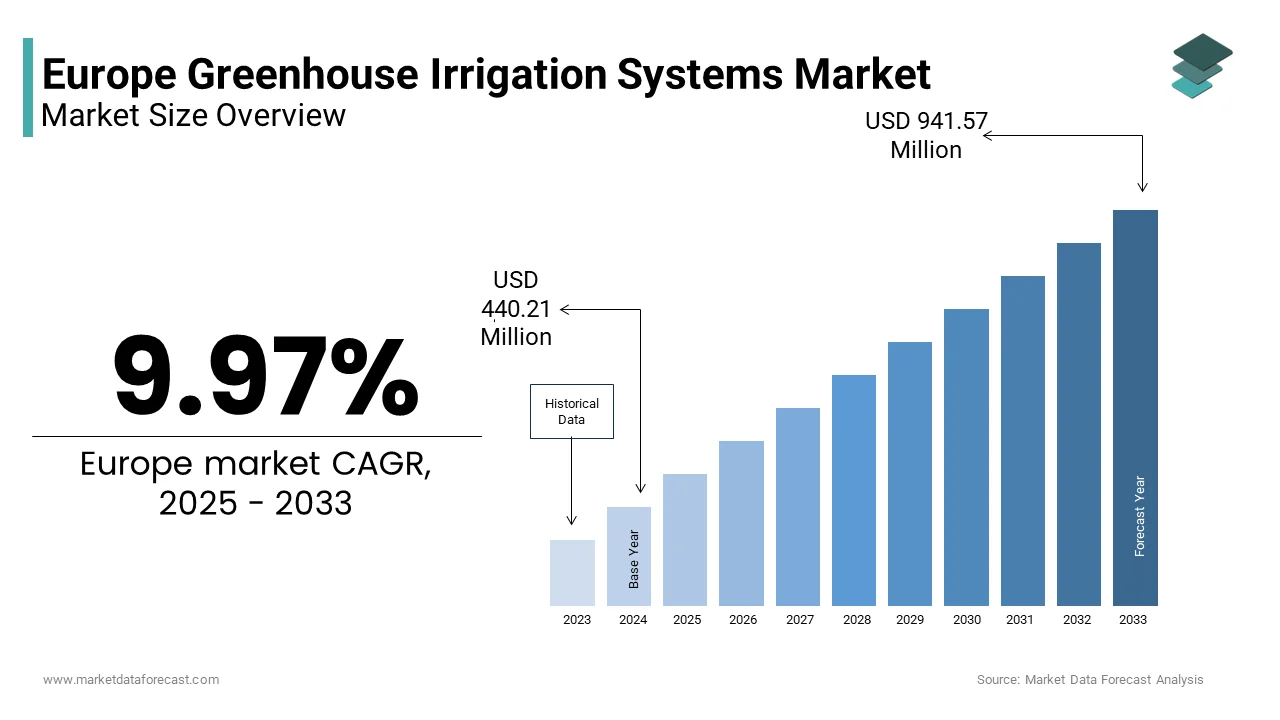

The European greenhouse irrigation systems market was valued at USD 400.30 million in 2024 and is anticipated to reach USD 440.21 million in 2025 and USD 941.57 million by 2033, growing at a CAGR of 9.97% during the forecast period from 2025 to 2033.

Greenhouse irrigation systems represent engineered solutions that deliver precise volumes of water and nutrients directly to plant root zones within controlled agricultural environments. These systems are integral to modern horticulture in Europe,e where climate volatility, ty water scarcity,ity and the demand for high-yielding specialty crops intersect. Unlike open field agriculture, greenhouse cultivation relies on closed-loop technologies such as drip emitters, micro sprinklers, and capillary mats to optimize resource use while minimizing runoff and evaporation. According to the European Environment Agency, agricultural water abstraction in Southern Europe can exceed 60% of total freshwater use during peak summer months, which is intensifying the need for efficient irrigation. Furthermore, the European Commission’s Farm to Fork Strategy targets a 50% reduction in nutrient losses by 2030, directly incentivizing precision delivery systems that prevent over‑fertilization. For instance, the Netherlands had about 10,150 hectares of greenhouse horticulture in 2023, which illustrates the high concentration of protected cultivation in a few member states and the regional importance of precision irrigation and fertigation technologies. These environmental, policy, and agronomic pressures define the operational landscape for greenhouse irrigation technologies across the continent.

MARKET DRIVERS

Stringent EU Water Efficiency Mandates Accelerate Adoption of Precision Irrigation

The European Union’s escalating regulatory focus on agricultural water stewardship is primarily driving the growth of the Europe greenhouse irrigation systems market. According to the European Environment Agency, over 20% of Europe’s river basins experience water stress during summer months, with agricultural use accounting for a large share of withdrawals in Mediterranean regions. As per the EU Water Reuse Regulation (fully enforceable in 2023), member states must implement water‑efficiency plans for high‑consumption sectors, including horticulture. Spain now requires greenhouses in Murcia and Almería to achieve a minimum irrigation efficiency of 85% as per Royal Decree 1070/2022. Similarly, the Netherlands, ds under its National Water Plan, has tied greenhouse licensing to the use of closed‑loop irrigation that recirculates at least 90% of nutrient solution. As per Statistics Netherlands, a very high share of Dutch greenhouse growers had adopted sensor‑controlled drip systems by 2023 to comply with national norms. Germany’s Federal Ministry for Food and Agriculture has integrated irrigation efficiency into its Common Agricultural Policy funding criteria, denying subsidies to operations using non‑regulated watering methods. These coordinated policy instruments transform regulatory compliance into a technological imperative, driving consistent demand for automated, moisture‑responsive, and recirculating irrigation architectures across European greenhouse farms.

Rising Cultivation of High‑Value Specialty Crops Demands Tailored Water Delivery

The growth of the European greenhouse irrigation systems market is also driven by the economic viability of greenhouse farming in Euro, whichpe, which increasingly hinges on the production of premium horticultural commodities such as berries, tomatoes, peppers, and ornamental flowers, all of which require exacting irrigation protocols. According to the European Commission, a large share of greenhouse output by value consists of tomatoes and strawberries, as these crops are highly sensitive to moisture fluctuation and salinity buildup. In the Netherlands, where greenhouse tomato yields are among the highest globally, precise drip irrigation is non‑negotiable for maintaining fruit quality and preventing blossom end rot. Similarly,y in Italy, protected strawberry cultivation in Emilia‑Romagna expanded between 2021 and 2023 according to ISTAT, requiring micro‑emitter systems that deliver water directly to the crown without wetting foliage to suppress fungal pathogens. France’s horticultural cooperative FNPP now mandates that member greenhouses growing potted ornamentals use capillary mat systems to reduce water use by 30% while improving root uniformity. These crop‑specific agronomic requirements, coupled with a narrow profit margin,s compel growers to invest in irrigation technologies that offer programmable dosing, zonal control, and integration with climate computers. This alignment between crop economics and irrigation precision sustains robust demand across Europe’s high‑intensity horticultural corridors.

MARKET RESTRAINTS

High Initial Capital Outlay Deters Small and Medium-Scale Growers

Despite long‑term operational benefits, the substantial upfront investment required for advanced greenhouse irrigation systems remains a critical barrier to widespread adoption, particularly among small and medium‑sized horticultural enterprises, which is hampering the growth of the Europe greenhouse irrigation systems market. According to the European Commission’s Farm Structure Survey, a majority of greenhouse operations in the EU manage less than one hectare of protected area and operate with modest annual revenues. Installing a fully automated drip and fertigation system with moisture sensors and climate integration typically costs tens of thousands of euros per hectare, as estimated by sector economic studies. In Southern and Eastern Europe, where access to agricultural credit is limited, adoption rates for precision irrigation among small greenhouse farms remain substantially lower than in Western Europe, according to national ministry audits. Even in Germany, where low‑interest green loans are available, payback periods for such systems often exceed five years, deterring risk‑averse growers. Public subsidy programs exist, st but frequently require co‑financing of 30–50%, which many smallholders cannot afford. Consequently, a significant portion of Europe’s greenhouse sector continues to rely on manual or timer‑based watering, which is leading to inefficiencies that contradict broader sustainability goals. This financial gap between technological potential and economic reality constrains market penetration despite clear agronomic advantages.

Fragmented Technical Standards Across Member States Complicate System Integration

The absence of harmonized technical and interoperability standards for irrigation control systems across European countries creates significant implementation challenges for greenhouse operators and equipment suppliers, which further hinders the growth of the Europe greenhouse irrigation systems market. As per the European Committee for Standardization, national building and agricultural codes in countries like Sweden, Poland, and Portugal impose divergent requirements for electrical safety, water pressure, and nutrient‑tank materials in greenhouse infrastructure. This fragmentation forces irrigation system vendors to maintain multiple product variants, increasing costs and delaying deployment. For instance, only a minority of irrigation controllers sold in Europe are fully compatible with all major climate‑computer brands due to proprietary communication protocols. In France, for example, national regulations require certain fertigation safety features that differ from standard German models. Furthermore, the lack of common data formats for soil‑moisture sensors impedes integration with farm‑management software, limiting the effectiveness of precision irrigation. As per AgriTech Europe, a notable share of greenhouse growers abandoned planned irrigation upgrades due to incompatibility with existing automation systems. Until the European Commission establishes unified technical frameworks under relevant digital and standards programs, these interoperability gaps will continue to hinder the seamless adoption of advanced irrigation solutions across the continent.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Adaptive Irrigation Scheduling

The fusion of artificial intelligence with real‑time environmental data is unlocking unprecedented levels of irrigation autonomy and crop responsiveness in European greenhouses, which is a prominent opportunity in the Europe greenhouse irrigation systems market. As per Wageningen University, over one hundred commercial greenhouses in the Netherlands, Belgium, and Denmark had deployed AI‑driven irrigation platforms by 2024 that analyze plant transpiration, substrate moisture, and weather forecasts to adjust watering cycles dynamically. According to trials conducted at the Dutch Greenhouse Delta, these systems reported measurable reductions in water use and improvements in tomato yield consistency. As per EIT Food, funding was allocated in 2023 to support startups developing machine‑learning models that correlate leaf temperature and stem‑diameter fluctuations with irrigation needs. According to the Institute for Sustainable Agriculture in Spain, an AI algorithm reduced water consumption in strawberry greenhouse trials by predicting evapotranspiration peaks up to 48 hours in advance. National digital agriculture strategies in Finland and Austria now include grants for AI irrigation integration, recognizing its role in achieving Farm to Fork nutrient‑efficiency targets. This convergence of data science, agronomy, and automation positions intelligent irrigation as a transformative opportunity for Europe’s precision horticulture sector.

Expansion of Urban and Vertical Farming Drives Demand for Compact Modular Systems

Europe’s accelerating shift toward urban agriculture is creating a new market segment for space‑efficient modular irrigation technologies tailored to vertical and rooftop greenhouses, which is another prominent opportunity in the Europe greenhouse irrigation systems market. As per Eurostat, a majority of the EU population now resides in urban areas, and municipal governments in cities such as Berlin, Paris, and Copenhagen are actively promoting urban food production through zoning incentives and infrastructure grants. According to the European Urban Agriculture Network, several hundred vertical farms were operational in Europe by early 2024, with many relying on closed‑loop drip or aeroponic systems due to space and water constraints. As per Gothenburg’s 2023 urban farming subsidy program, recipient projects were required to use recirculating irrigation to achieve very high water‑reuse rates. Similarly, Paris’s Parisculteurs initiative mandates modular emitter grids compatible with building load limits and rainwater harvesting. These urban contexts demand irrigation solutions that are lightweight, scalable, and easily maintained by non‑agronomic staff. Companies are responding with plug‑and‑play kits featuring low‑pressure emitters, gravity‑fed reservoirs, and IoT‑enabled leak detection. As cities intensify efforts to localize food supply and reduce transport emissions, this niche but high‑growth segment offers commercial potential for specialized irrigation providers.

MARKET CHALLENGES

Aging Agricultural Workforce Limits Technical Adoption and Maintenance Capacity

The demographic decline in Europe’s farming community directly undermines the operational sustainability of sophisticated greenhouse irrigation systems that require digital literacy and routine technical upkeep, which is majorly challenging the expansion of the Europe greenhouse irrigation systems market. As per Eurostat, the average age of European farm managers exceeded 55 years in 2023, with only a small share under the age of 40. According to national agricultural census data, in some counties,ries a high proportion of greenhouse operators are over 55 and report limited proficiency with smartphone apps or automated control interfaces. As per a 2023 study by the European Society for Agricultural Engineers, a notable share of advanced irrigation systems in Southern Europe operate below design efficiency due to incorrect programming or neglected sensor calibration. According to Cedefop and sector workforce analyses, a substantial shortfall of skilled horticultural technicians is projected in the coming years. In rural regions,gions some growers revert to manual watering despite owning automated systems because they lack troubleshooting support. This human capital gap limits system effectiveness across large portions of Europe’s greenhouse sector.

Energy Intensity of Pressurized Irrigation Systems Conflicts with Decarbonization Goals

The operational energy demands of high‑pressure drip and misting systems present a growing contradiction with Europe’s agricultural decarbonization agenda, which is further challenging the expansion of the Europe greenhouse irrigation systems market. As per the European Commission’s Joint Research Centre, irrigation pumps can account for a significant share of electricity consumption in intensive greenhouse operations, particularly in year‑round production zones. According to the Netherlands Environmental Assessment Agency, average Dutch greenhouse energy use is on the order of tens of kilowatt‑hours per square meter annually, with irrigation contributing a meaningful portion of that total. As per the EU Renewable Energy Directive, member states are required to increase the share of renewables in final energy consumption, with a 2030 target that raises carbon‑compliance pressures for growers. In Germany, the phase‑out of natural gas for heating has shifted energy loads to electric pumps, amplifying grid dependency. For instance, only a minority of European greenhouses had integrated photovoltaic systems by 2023. This energy intensity forces a strategic dilemma between water efficiency and carbon footprint, compelling growers to seek low‑pressure or gravity‑fed alternatives that may compromise irrigation uniformity. Until renewable microgrids and energy‑recovery technologies become standard, this tension will remain a critical sustainability challenge for the sector.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2024 to 2033 |

| CAGR | 9.97% |

| Segments Covered | By Type, By Application, and Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Republic, ic & Rest of Europe |

| Market Leaders Profiled | Netafim Ltd., Jain Irrigation Systems Ltd., Nelson Irrigation Corporation, Valmont Industries Inc., Rivulis Irrigation Ltd., The Toro Company, EPC Industries Limited, Lindsay Corporation, Rain Bird Corporation, Irritec S.P.A. |

SEGMENTAL ANALYSIS

By Type Insights

The drip irrigation system dominated the Europe greenhouse irrigation systems market by holding 60.5% of the European market share in 2024. The dominance of the drip irrigation systems segment in the European market is attributed to its unmatched precision in water and nutrient delivery, which aligns directly with Europe’s regulatory and agronomic priorities. As per Wageningen University in 2023, drip systems achieve water use efficiencies of up to 95% in controlled environments compared to 60% to 70% for traditional overhead methods. The primary driver is the European Union’s Farm to Fork Strategy,y which mandates a 50% reduction in nutrient losses and pesticide use by 2030. Drip irrigation minimizes leaching of fertilizers into groundwater and prevents foliar wetness that encourages fungal pathogens, which is critical for high‑value crops like tomatoes and cucumbers. According to the Dutch Ministry of Agriculture, in the Netherlands, ds over ninety‑three% of greenhouse vegetable growers use pressure‑compensated drip lines integrated with climate computers to match irrigation to real‑time plant transpiration. Similarly, Spain’s Andalusian regional government requires all new greenhouse projects in Almería to install closed‑loop drip systems that recirculate at least 80% of drainage water under Decree 127/2022. These policy and performance synergies solidify drip irrigation as the foundational technology in Europe’s precision horticulture landscape.

The boom irrigation system segment is the fastest growing segment in the Europe greenhouse irrigation market and is anticipated to witness a CAGR of 11.5% over the forecast period,iod owing to the rising demand for labour‑saving solutions in large‑scale ornamental and young plant production where uniform overhead watering remains essential. Unlike fixed sprinklers, boom systems traverse greenhouse bays on rails, delivering consistent water distribution while reducing manual labor. According to the European Ornamental Growers Association, over 70% of nursery operations producing potted plants and cuttings in Germany and the Netherlands have replaced hand watering with automated boom systems since 2021 due to chronic labor shortages. According to the German Federal Employment Agency, a deficit of over 25000 seasonal horticultural workers in 2023promptedg growers to invest in mechanization. Furthermore, boom systems now incorporate variable‑rate nozzles and substrate moisture feedback, allowing zone‑specific application that conserves water without compromising crop uniformity. As per Denmark’s Green Growth initiative, subsidies covered 40% of boom system costs for nurseries adopting ISO 14046 water footprint certification. As urban pressures shrink available labor and precision agriculture standards evolve, this segment bridges automation and agronomic consistency in Europe’s high‑value plant propagation sector.

By Application Insights

The vegetables segment dominated the market by holding 50.6% of the regional market share in 2024. The leading position of the vegetables segment in this regional market is attributed to the continent’s strategic emphasis on food security, high consumer demand for fresh produce, and the economic efficiency of protected vegetable cultivation. According to Eurostat, in 2023, European greenhouses produced over twelve point five million metric tons of tomatoes, cucumbers, and peppers, with the Netherlands alone exporting €6.2 billion worth of greenhouse vegetables. These crops require exacting irrigation protocols to maintain fruit quality, shelf life, and yield consistency. The European Commission’s Common Agricultural Policy now ties direct payments to water efficiency metrics, with vegetable growers in water‑stressed regions like Murcia required to demonstrate at least 80% irrigation efficiency to qualify for subsidies as per Regulation (EU) 2023/1082. Additionally, the rise of year‑round tomato production in Nordic countries using geothermal‑heated greenhouses has intensified reliance on sensor‑driven irrigation to compensate for low natural light and high transpiration variability. According to the Swedish Board of Agriculture, Sweden, a 40% increase in the drip‑irrigated greenhouse vegetable area between 2021 and 2023. These intertwined policies, crop economics, and climate adaptation factors anchor vegetables as the leading application for advanced irrigation in Europe.

The fruit plants and flowers segment is the fastest growing application category in the Europe greenhouse irrigation systems market and is expected to witness a CAGR of 9.55% over the forecast period, owing to the rising consumer preference for locally grown berries, cut flowers, and potted ornaments, ls coupled with innovations in substrate‑based cultivation that demand tailored watering. According to the European Association of Flower Bulb Producers, cut flower production in greenhouses expanded by 21% in 2023, with the Netherlands exporting over two billion stems of roses and chrysanthemums under protected conditions. Strawberries represent a particularly dynamic subsegment, with Spain’s Huelva region reporting a 33% increase in protected berry area between 2022 and 2024, as per the Spanish Ministry of Agriculture. These crops are highly sensitive to moisture on petals and fruit surfaces, requiring subsurface drip or micro‑sprinkler systems that avoid foliar contact. As per the Horticulture Cluster of Brittany, France, a 2023 initiativemandatesg that all subsidized flower greenhouse projects integrate irrigation systems with evapotranspiration compensation to reduce water use by 25%. Additionally, the EU’s Green Public Procurement criteria now prioritize locally grown flowers for institutional events, further stimulating protected cultivation. These consumer, market, and regulatory dynamics position fruit plants and flowers as Europe’s most rapidly expanding irrigation application.

COUNTRY ANALYSIS

Netherlands Greenhouse Irrigation Systems Market Analysis

The Netherlands held the foremost position in the Europe greenhouse irrigation systems market with an 26.1% share of the regional market in 2024. The dominance of the Netherlands in the European market is driven by its globally integrated horticultural cluster, advanced water‑recycling infrastructure, and policy‑led innovation ecosystem. Dutch growers operate extensive closed‑loop irrigation systems with more than 95% of facilities using sensor‑controlled drip networks. The government’s Greenhouse 2030 vision mandates zero discharge of nutrients and water from commercial facilities, accelerating the adoption of recirculating irrigation and fertigation. Wageningen University collaborates with hundreds of irrigation technology firms to develop real‑time root‑zone monitoring tools that adjust flow based on plant stress indicators, while the Netherlands Enterprise Agency offers low‑interest loans covering up to 50% of automation costs for farms achieving ISO 14046 certification. These research, policy, and commercial synergies make the Netherlands both the largest market and the innovation benchmark for greenhouse irrigation across Europe.

Spain Greenhouse Irrigation Systems Market Analysis

Spain ranked second in the European greenhouse irrigation market. The growth of Spain in the European market can be credited to the vast greenhouse complexes in Andalusia that form Europe’s primary winter vegetable production zone under acute water constraints. The province of Almería alone hosts tens of thousands of hectares of protected cultivation where drip irrigation and high reuse rates are legally required, prompting growers to integrate solar‑powered pumps, soil‑moisture telemetry, and low‑pressure drip tape that reduces energy use while maintaining uniformity on sandy soils. Regional water authorities report declining agricultural abstraction despite expanding cultivation, reflecting enforced efficiency measures. These adaptations to aridity, regulatory pressure, and export competitiveness cement Spain’s critical role in the European irrigation landscape.

Italy Greenhouse Irrigation Systems Market Analysis

Italy had a prominent share of the European greenhouse irrigation systems market in 2024. The strong horticultural traditions in Emilia‑Romagna and Puglia, and growing alignment with EU sustainability mandates, are propelling the Italian market growth. New greenhouse installations increasingly specify drip and precision fertigation systems, and national recovery funds have subsidized modernization of water infrastructure and precision irrigation in drought‑declared regions. Regional authorities now require metered fertigation with remote data transmission for operators drawing surface water, and research centers have developed biodegradable drip lines that reduce plastic waste while maintaining flow consistency. Policy incentives, technological adaptation, and export‑oriented production models sustain Italy’s robust position in the greenhouse irrigation market.

France Greenhouse Irrigation Systems Market Analysis

France represents a dynamic, policy‑responsive market for advanced greenhouse irrigation technologies. The growth of France in the European market is driven by strategic investments in high‑tech horticulture and stringent national water governance. Precision irrigation adoption is growing across key regions, and national plans mandate closed‑loop systems with real‑time leak detection for new projects in water‑stressed departments. French research institutes have piloted AI‑based irrigation schedulers that cut water use substantially while improving uniformity, and incentive programs favor systems that minimize pesticide runoff through targeted root‑zone delivery. These integrations of regulation, agronomic science, and digital innovation position France as a leading adopter of advanced irrigation solutions.

Germany Greenhouse Irrigation Systems Market Analysis

Germany is anticipated to showcase a healthy CAGR in the European greenhouse irrigation market during the forecast period, due to the energy‑efficient greenhouse designs, high labor costs that favor automation, and public support for sustainable agriculture. Automated drip and boom systems are widely used across protected cultivation, and subsidy programs encourage irrigation systems powered by on‑site photovoltaics to address energy intensity. Industry standards and certification schemes require precise water metering and nutrient monitoring, and regional initiatives provide technical assistance for integrating rainwater harvesting with drip irrigation. These systemic efforts to align irrigation with decarbonization, labor efficiency, and circular water principles sustain Germany’s significant and evolving presence in the market.

COMPETITIVE LANDSCAPE

The Europe greenhouse irrigation systems market features robust competition among global technology leaders and specialized European vendors,ors all navigating a landscape defined by environmental regulation, labor scarcity, and precision agriculture demands. Companies differentiate through water efficiency, accuracy integration with greenhouse automation, and support for circular nutrient systems. The enforcement of the EU Farm to Fork Strategy and WaterReuse Regulation has elevated technical and compliance barriers, favoring firms with proven track records in closed-loop system design and data-driven agronomy. At the same time, the diversity of crops—from tomatoes to ornamentals—requires adaptable solutions that balance automation with agronomic nuance. Competition extends beyond hardware to include digital service, training, and sustainability validation as growers seek holistic partnerships rather than mere equipment suppliers. This environment encourages continuous innovation, low-energy delivery, smart control, and biodegradable components while intensifying collaboration with policymakers and research bodies to shape future standards.

KEY MARKET PLAYERS

Some of the major companies dominating the market, by their products and services, include

- Netafim Ltd.

- Jain Irrigation Systems Ltd

- Nelson Irrigation Corporation

- Valmont Industries Inc

- Rivulis Irrigation Ltd.

- The Toro Company

- EPC Industries Limited

- Lindsay Corporation

- Rain Bird Corporation

- Irritec S.P.A.

Top Players In The Market

- Netafim is a globally recognized pioneer in precision irrigation with deep integration into Europe’s greenhouse sector. The company supplies advanced drip and micro irrigation solutions tailored for protected cultivation across tomatoes, berries, and ornamentals. Netafim contributes significantly to global water conservation efforts through its closed-loop systems that minimize nutrient runoff and optimize water use. In recent years, the company has expanded its digital agronomy platform in Europe, integrating real-time soil moisture data with automated fertigation control. It also established a dedicated greenhouse innovation center in the Netherlands, collaborating with Wageningen University to develop climate-responsive irrigation protocols. These initiatives reinforce its leadership in sustainable horticulture and strengthen its technological footprint across European high-tech greenhouse clusters.

- Rivulis is a major international provider of irrigation technologies with a strong presence in European greenhouse markets, particularly in Southern and Western Europe. The company offers a comprehensive portfolio, including pressure-compensated driplines, micro sprinklers,s and smart irrigation controllers designed for substrate-based cultivation. Rivulis supports global food security by enabling consistent yields undewater-constraineded conditions through precision delivery. To enhance its European position, Rivulis recently launched its ITC irrigation management software across France, Italy, and Spain, allowing growers to monitor and adjust irrigation remotely via mobile applications. The company also partnered with agricultural cooperatives in Almería to retrofit legacy greenhouses with water-efficient systems aligned with EU regulatory standards. These actions demonstrate its commitment to digital transformation and sustainability in European horticulture.

- Valmont Industries is a leading global manufacturer of agricultural solutions with a strategic focus on advanced irrigation for protected cultivation in Europe. Through its subsidiary Valmont Hydro and collaborations with European greenhouse builders, the company delivers integrated overhead and drip systems for vegetable and nursery applications. Valmont contributes to global resource efficiency by engineering low-pressure boom irrigation units that reduce both water and energy consumption. In 2024, the company introduced its next-generation AgSense Smart Control system across Germany and the Netherlands, featuringAI-drivenn irrigation scheduling based on evapotranspiration forecasts and substrate conditions. It also expanded its service network in Eastern Europe to provide technical support for irrigation automation. These moves reflect Valmont’s emphasis on localized innovation and operational reliability in Europe’s evolving greenhouse landscape.

Top Strategies Used by the Key Market Participants

Key players in the Europe greenhouse irrigation systems market emphasize compliance with stringent EU water and nutrient regulations by developing closed-loop recirculating technologies that minimize environmental impact. They invest in digital integration, offering cloud-based platforms that connect irrigation controllers with climate computers and soil sensors for real-time adaptive watering. Strategic collaborations with research institutions such as Wageningen University and national agricultural agencies facilitate the development of crop-specific irrigation protocols. Companies also localize manufacturing and service hubs across the Netherlands, Spain, and Germany to ensure rapid deployment and technical support. Furthermore, they pursue sustainability certifications and participate in public subsidy programs to align with national decarbonization and circular economy agendas, enhancing both market access and grower trust.

MARKET SEGMENTATION

The Europe greenhouse irrigation systems market is segmented and sub-segmented into the following categories.

By Type

- Drip Irrigation System

- boom irriBoomon system

- and a micro-sprinkler irrigation system

By Application

- Vegetables

- Nursery crops

- Fruit plants and flowers

- Ornaments

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe greenhouse irrigation systems market?

The Europe greenhouse irrigation systems market covers technologies and equipment—including drip systems, sprinklers, micro-irrigation, and fertigation solutions—used to efficiently deliver water and nutrients to crops in controlled greenhouse environments.

Why are greenhouse irrigation systems important?

Greenhouse irrigation systems ensure uniform water application, optimal plant growth, resource efficiency, reduced labor, and precise water-nutrient delivery needed for high-value horticultural and protected crops.

What drives growth in the Europe greenhouse irrigation systems market?

Growth is driven by rising demand for year-round crop production, water scarcity challenges, expansion of protected agriculture, government sustainability policies, and precision farming adoption.

What types of irrigation systems are used in European greenhouses?

Common systems include drip irrigation, micro-sprinklers, overhead sprinklers, ebb and flow systems, and automated fertigation units that integrate with nutrient delivery and climate control systems.

How do greenhouse irrigation systems benefit growers?

They improve crop yields, reduce water use, minimize nutrient waste, automate irrigation scheduling, and enhance plant health, enabling higher quality and consistent production.

Which crops benefit most from greenhouse irrigation systems?

Greenhouse irrigation is widely used for vegetables (tomatoes, cucumbers, peppers), herbs, ornamentals, seedlings, berries, and specialty high-value crops.

What role does automation play in greenhouse irrigation?

Automation with sensors, timers, and climate controllers enables precise irrigation timing, soil moisture monitoring, and reduced manual intervention, optimizing water and nutrient use.

How does fertigation enhance irrigation systems?

Fertigation integrates nutrient delivery with irrigation, allowing plants to receive water and soluble fertilizer simultaneously, improving efficiency and reducing fertilizer waste.

Which regions lead the greenhouse irrigation systems market in Europe?

Major markets include the Netherlands, Germany, Spain, Italy, and France, supported by advanced greenhouse infrastructure, horticultural innovation, and export-oriented production.

What trends are shaping the Europe greenhouse irrigation systems market?

Key trends include smart irrigation with IoT connectivity, sensor-based precision irrigation, automated fertigation, water-saving technologies, and climate-controlled irrigation management.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com