Europe Gymnastics Equipment Market Size, Share, Trends & Growth Forecast Report – Segmented By Age Group, Equipment Type, Material, Usage Type, End User, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Gymnastics Equipment Market Report Summary

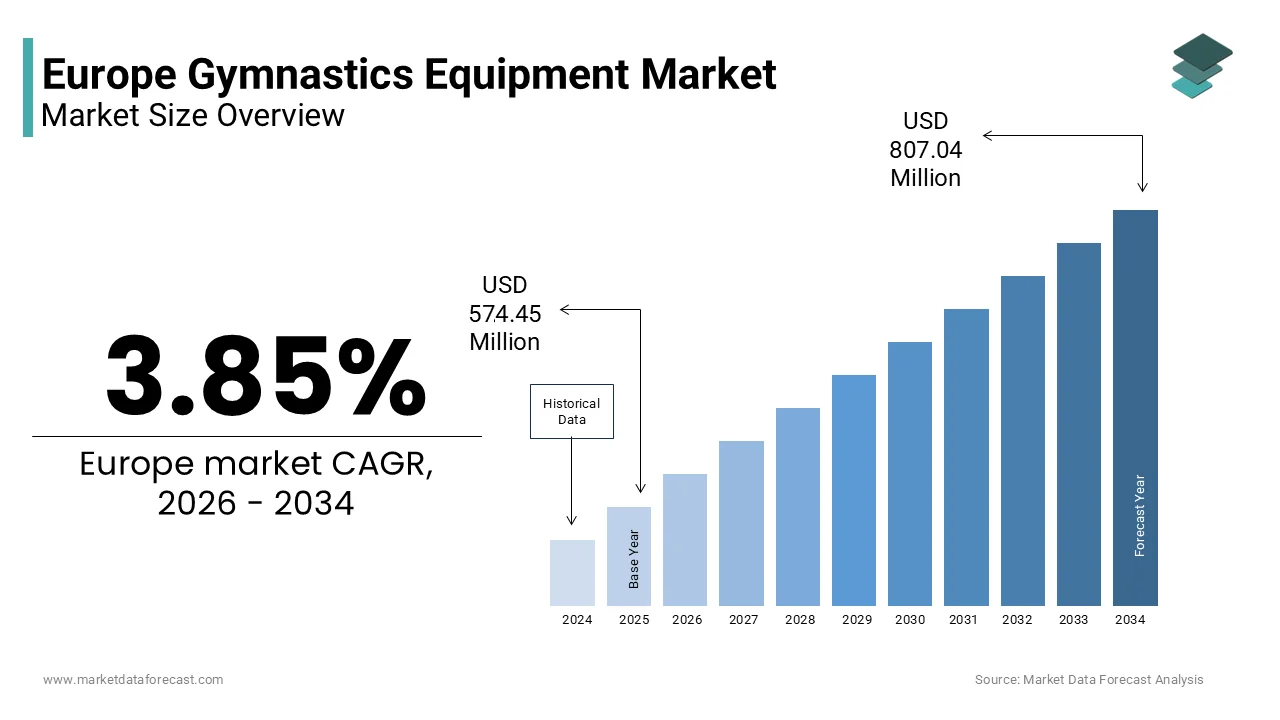

The Europe gymnastics equipment market was valued at USD 574.45 million in 2025, is estimated to reach USD 596.58 million in 2026, and is projected to reach USD 807.04 million by 2034, growing at a CAGR of 3.85% during the forecast period from 2026 to 2034. The growth of the Europe gymnastics equipment market is driven by increasing participation in gymnastics and physical fitness activities, rising emphasis on youth sports development, and growing investments in sports infrastructure across schools and training centers. Governments and educational institutions across Europe are promoting gymnastics as part of physical education programs, which is increasing the demand for professional and recreational gymnastics equipment. In addition, the expansion of sports clubs, rising interest in competitive gymnastics, and increasing awareness of fitness among children and young athletes are supporting market growth.

Key Market Trends

- Increasing participation of children and young athletes in gymnastics programs supported by school sports initiatives and youth training academies.

- Growing investments in sports infrastructure across educational institutions, training centers, and recreational facilities.

- Rising demand for safety focused equipment such as mats and protective flooring systems to reduce the risk of injuries during training.

- Expansion of recreational gymnastics activities that encourage physical fitness, flexibility, and coordination among children and beginners.

- Increasing adoption of high quality and durable gymnastics equipment by sports clubs and professional training facilities.

Segmental Insights

- Based on age group, the children segment dominated the Europe gymnastics equipment market in 2025. The growth of this segment is driven by increasing participation of children in school sports programs and gymnastics training academies across Europe.

- Based on equipment type, the mats and flooring segment held the dominant position in the Europe gymnastics equipment market in 2025. The widespread use of safety mats and protective flooring in training and competition environments is supporting the strong demand for this equipment category.

- Based on usage type, the recreational usage segment led the Europe gymnastics equipment market in 2025. The growing popularity of gymnastics as a recreational fitness activity among children and beginners is contributing to the segment’s growth.

- Based on end user, the schools segment dominated the Europe gymnastics equipment market in 2025. Educational institutions are increasingly incorporating gymnastics into physical education programs, which is driving the demand for training equipment in schools.

Regional Insights

- The Europe gymnastics equipment market is witnessing stable growth across several countries due to increasing sports participation, government support for youth sports programs, and expanding training infrastructure.

- Germany was the largest contributor, accounting for 20.9% of the Europe gymnastics equipment market share in 2025. The country’s strong sports culture, well established gymnastics clubs, and increasing participation in youth sports programs are supporting market growth.

Competitive Landscape

The Europe gymnastics equipment market is characterized by the presence of specialized sports equipment manufacturers focusing on product quality, safety standards, and innovation in training equipment. Companies are developing durable and safety focused equipment designed for both professional competitions and recreational training environments. Strategic collaborations with sports organizations, schools, and gymnastics clubs are helping manufacturers expand their market presence. Prominent players in the Europe gymnastics equipment market include Gymnova, Spieth Gymnastics, Janssen Fritsen, ABEO SA, American Athletic Inc (AAI), Norbert's Athletic Products, Tumbl Trak, Taishan Sports Industry Group, Continental Sports Ltd, and Decathlon SA.

Europe Gymnastics Equipment Market Size

The Europe gymnastics equipment market size was valued at USD 574.45 million in 2025 and is projected to reach USD 807.04 million by 2034 from USD 596.58 million in 2026, growing at a CAGR of 3.85%.

Gymnastics equipment encompasses a specialized sector dedicated to the manufacturing, distribution, and installation of apparatus designed for artistic, rhythmic, and trampoline gymnastics across the continent. This industry supplies essential infrastructure ranging from competition standard vaulting tables and uneven bars to safety flooring and training aids for clubs, schools, and professional arenas. The definition extends beyond mere hardware to include certified safety systems that adhere to strict European Norms ensuring athlete protection during high impact manoeuvres. According to Eurostat, physical activity participation rates vary across member states, yet gymnastics remains a cornerstone of school physical education curricula in nations like France and Germany, which is creating a foundational demand for durable and compliant equipment. Furthermore, the European Union emphasizes the importance of sport in social inclusion and health, with the European Commission noting that citizens widely engage in club-based sports annually. Unlike general fitness gear, this market is heavily regulated by the International Gymnastics Federation and European standardization bodies which mandate rigorous testing for load bearing and shock absorption. The landscape is currently shifting towards modular and technologically integrated solutions that allow facilities to adapt spaces for multiple disciplines while maintaining the highest safety standards for athletes of all ages.

MARKET DRIVERS

Government Initiatives Promoting Youth Sports and Physical Education

The robust support from national governments and educational institutions aimed at fostering youth development through structured physical activity is primarily driving the growth of the Europe gymnastics equipment market. Many European countries have integrated gymnastics deeply into their school systems, viewing it as fundamental for developing motor skills, discipline, and physical literacy among children. According to the European Commission, the Erasmus+ sport program allocates funding to projects that encourage grassroots participation and improve sports infrastructure across the union. This financial backing enables schools and local clubs to upgrade aging facilities with modern, safety-compliant apparatus that meet current regulatory standards. In nations such as France, the Ministry of National Education mandates regular gymnastics sessions, creating a consistent replacement cycle for mats, beams, and bars due to wear and tear. As per the European Gymnastics Union, registered clubs rely on public subsidies to maintain their training environments, ensuring a steady demand for high-quality equipment. The emphasis on early specialization in competitive sports further drives clubs to invest in professional-grade apparatus to nurture talent from a young age. This institutional commitment transforms gymnastics equipment from a discretionary purchase into a necessary public investment, sustaining market growth regardless of broader economic fluctuations.

Rising Health Consciousness and Popularity of Recreational Gymnastics

The surging awareness regarding physical health and the growing popularity of gymnastics as a recreational activity for adults and children alike serve as a powerful driver for market expansion. Post-pandemic trends have seen a shift towards activities that improve flexibility, core strength, and mental well-being, with gymnastics emerging as a preferred choice for holistic fitness. According to the World Health Organization European Region, insufficient physical activity remains a leading risk factor for non-communicable diseases, prompting public health campaigns that promote diverse sports participation including gymnastics. This cultural shift has led to the proliferation of private gymnastics academies and recreational centers catering to non-competitive participants who require safe and inviting training environments. As per national fitness associations, the rise of adult gymnastics classes has opened a new revenue stream for facility operators, necessitating the purchase of durable equipment capable of withstanding higher usage frequencies. The influence of social media showcasing gymnastic feats has also inspired younger generations to enroll in classes, increasing membership numbers in local clubs. Consequently, facility owners are compelled to expand their inventory with varied apparatus such as foam pits, tumble tracks, and rhythmic gear to accommodate this broadening demographic base.

MARKET RESTRAINTS

Stringent Safety Regulations and High Compliance Costs

The rigorous enforcement of safety standards and certification requirements acts as a significant restraint on the Europe gymnastics equipment market by elevating manufacturing costs and extending time to market for new products. Equipment must comply with specific European Norms such as EN 12198 for apparatus safety, which demands extensive testing for structural integrity, stability, and shock absorption capabilities. According to the European Committee for Standardization, adherence to these norms requires manufacturers to invest heavily in research, development, and third-party certification processes, which can be prohibitively expensive for smaller enterprises. These costs are often passed down to consumers, resulting in higher retail prices that may deter budget-constrained schools and community clubs from upgrading their facilities. As per the European Gymnastics Union, the complexity of navigating varying national implementations of EU directives can create barriers to cross-border trade, limiting market access for innovative but smaller brands. Furthermore, the liability risks associated with potential accidents force insurers to demand proof of strict compliance, adding another layer of administrative and financial burden. This regulatory environment, while essential for athlete safety, inadvertently slows down the adoption of new technologies and limits the diversity of suppliers available to buyers, thereby constraining overall market dynamism.

High Initial Capital Investment and Maintenance Expenses

The substantial upfront capital required to procure professional-grade gymnastics equipment coupled with ongoing maintenance costs presents a major barrier to market growth, particularly for small clubs and startups. High-quality apparatus such as electronic vaulting tables, sprung floors, and competition-standard bars represent significant financial outlays that many organizations struggle to afford without external funding. According to the European Small Business Alliance, access to finance remains a critical challenge for sports clubs, which often operate on thin margins and rely on membership fees alone. The total cost of ownership extends beyond the initial purchase to include regular inspections, part replacements, and specialized cleaning services needed to maintain safety certifications. As per national gymnastics federations, the lifespan of certain equipment components is limited by intense usage, necessitating frequent reinvestment that strains operational budgets. Economic uncertainties and inflationary pressures on raw materials further exacerbate these costs, forcing some facilities to delay upgrades or continue using outdated and potentially less safe equipment. This financial constraint limits the total addressable market and hinders the modernization of training centers, especially in regions with lower disposable incomes or reduced government support for sports infrastructure.

MARKET OPPORTUNITIES

Integration of Smart Technology and Data Analytics in Training

The incorporation of smart technology and data analytics into gymnastics equipment presents a promising opportunity for the Europe market by enhancing training efficiency and athlete performance monitoring. Modern apparatus equipped with sensors can track metrics such as impact force, rotation speed, and landing precision, providing coaches and athletes with immediate actionable feedback. According to the Fraunhofer Institute, the integration of Internet of Things devices in sports equipment is revolutionizing how performance data is collected and analyzed, allowing for personalized training regimens that reduce injury risks. This technological evolution appeals to elite training centers and national federations seeking a competitive edge through scientific coaching methods. As per the European Institute of Sport Science, there is growing demand for digital solutions that bridge the gap between physical practice and virtual analysis, enabling remote coaching and talent identification. Manufacturers who develop connected apparatus capable of syncing with cloud-based platforms can differentiate themselves in a crowded market and command premium pricing. The opportunity extends to creating subscription-based software services that offer advanced analytics, creating recurring revenue streams beyond hardware sales. This shift towards digitization aligns with the broader Industry 4.0 movement in Europe, positioning gymnastics equipment as a high-tech asset rather than a static tool.

Expansion of Home-Based Fitness and Compact Equipment Solutions

The enduring trend of home-based fitness offers a lucrative avenue for the Europe gymnastics equipment market through the development of compact, versatile, and safe apparatus designed for residential use. The pandemic accelerated the adoption of home workouts, and many families now seek space-efficient solutions that allow children and adults to practice basic gymnastic skills safely within limited living areas. According to Eurostat, the proportion of individuals engaging in physical activity at home has remained elevated compared to pre-pandemic levels, indicating a sustained shift in consumer behavior. This demand drives innovation in foldable beams, portable bars, and modular matting systems that offer professional quality without the footprint of commercial gear. As per European retail associations, there has been a notable increase in online sales of junior gymnastics kits, suggesting strong appetite for accessible entry-level equipment. Manufacturers can capitalize on this by designing aesthetically pleasing and easy-to-store products that appeal to urban households. Furthermore, partnering with online fitness platforms to offer bundled equipment and virtual classes can create a comprehensive home ecosystem. This segment allows companies to tap into the vast consumer market directly, bypassing traditional institutional sales channels and diversifying their revenue sources.

MARKET CHALLENGES

Shortage of Skilled Installers and Certified Maintenance Personnel

A critical challenge facing the Europe gymnastics equipment market is the acute shortage of skilled professionals capable of correctly installing and maintaining complex apparatus to meet stringent safety standards. Proper installation of equipment such as sprung floors and high bars requires specialized knowledge and certification to ensure structural integrity and athlete safety, yet the pool of qualified technicians is shrinking. According to the European Centre for the Development of Vocational Training, there is a growing mismatch between the skills required in specialized sectors like sports infrastructure and the available workforce, leading to delays in facility openings and upgrades. Incorrect installation can lead to catastrophic failures and legal liabilities, making clubs hesitant to purchase advanced equipment without guaranteed professional support. As per national gymnastics federations, the aging workforce of installers is not being replaced at a sufficient rate, creating a bottleneck for market expansion. This scarcity drives up labor costs and extends project timelines, frustrating customers and potentially stifling demand. Manufacturers must invest in training programs to cultivate a new generation of technicians, but the lack of standardized vocational courses across different countries complicates these efforts. Until this skills gap is addressed, the market risks being constrained by logistical limitations rather than product demand.

Volatility in Raw Material Prices and Supply Chain Disruptions

The Europe gymnastics equipment market faces persistent challenges from the volatility of raw material prices and ongoing supply chain disruptions that affect production costs and delivery schedules. Key materials such as high-grade steel, specialized foams, and synthetic leathers are subject to global price fluctuations driven by energy costs and geopolitical tensions. According to the European Steel Association, energy price spikes have significantly increased production costs for metal components used in frames and supports, squeezing manufacturer margins. Additionally, reliance on global supply chains for specific polymers and electronics makes the industry vulnerable to logistical bottlenecks and shipping delays. As per the European Central Bank, supply chain constraints have led to extended lead times for manufactured goods, forcing clubs to postpone facility upgrades and competitions. The unpredictability of material availability hampers the ability of manufacturers to honor contracts promptly, damaging customer relationships and market reputation. Furthermore, the push for sustainable sourcing adds another layer of complexity, as eco-friendly materials often come at a premium and with limited availability. Companies must navigate these uncertainties by diversifying suppliers and optimizing inventory management, yet the inherent instability remains a formidable obstacle to consistent growth and profitability in the sector.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.85% |

| Segments Covered | By Age Group, Equipment Type, Material, Usage Type, End User, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Gymnova, Spieth Gymnastics, Janssen Fritsen, ABEO SA, American Athletic Inc (AAI), Norbert's Athletic Products, Tumbl Trak, Taishan Sports Industry Group, Continental Sports Ltd, and Decathlon SA |

SEGMENTAL ANALYSIS

By Age Group Insights

The children segment dominated the market by capturing the highest share of the Europe gymnastics equipment market in 2025. The dominance of children segment in the European market is attributed to the foundational role gymnastics plays in early childhood physical education and motor skill development across the continent and the mandatory inclusion of gymnastics in national school curricula for primary education in many European nations. According to the European Commission, physical education is compulsory in all EU member states, with gymnastics often serving as a core component for developing balance, coordination, and strength in young learners. This institutional requirement ensures that schools and local clubs regularly purchase mats, low beams, and mini vaults to accommodate large cohorts of students. As per Eurostat, children between the ages of five and twelve participate widely in organized sports activities, with gymnastics ranking among the top choices for parents seeking structured physical activity. The emphasis on early talent identification by national federations further fuels investment in specialized training centers equipped with junior-level apparatus. Furthermore, the safety standards for this age group are exceptionally rigorous, necessitating frequent replacement of worn equipment to prevent injuries, thereby driving a steady replacement cycle. The combination of educational mandates, parental preference for holistic development, and the sheer volume of participants solidifies the children segment as the market leader.

The adults segment is a promising segment and is estimated to record a CAGR of 9.5% over the forecast period due to a cultural shift towards functional fitness and the rising popularity of adult gymnastics classes as a comprehensive workout solution for strength, flexibility, and mental well-being. The post-pandemic health consciousness that has led many adults to seek diverse and engaging forms of exercise beyond traditional gym routines is also boosting the expansion of the adults segment in the European market. According to the World Health Organization European Region, there is a concerted effort to increase physical activity levels among the working-age population to combat sedentary lifestyle diseases, with gymnastics gaining traction as an effective method. The proliferation of dedicated adult gymnastics studios and the integration of gymnastic elements into cross-fit and calisthenics programs have created a new demand stream for robust equipment capable of withstanding heavier body weights and higher intensity usage. As per national fitness associations, membership in adult gymnastics programs has surged in major urban centers, prompting facilities to invest in professional-grade bars, rings, and foam pits. Additionally, the influence of social media showcasing adult gymnasts has inspired individuals to pursue the sport recreationally, further expanding the consumer base. This demographic shift transforms gymnastics from a youth-only activity into a lifelong pursuit, driving unprecedented growth in equipment sales tailored for mature athletes.

By Equipment Type Insights

The mats and flooring segment held the dominant position in the Europe gymnastics equipment market by holding the highest share of the Europe gymnastics equipment market in 2025 due to their critical role in ensuring athlete safety and their ubiquitous presence across all types of gymnastics facilities. Every gymnastics discipline, from artistic to rhythmic and trampoline, requires extensive coverage of specialized shock-absorbing surfaces to prevent injuries during falls and landings. The primary driver for this dominance is the stringent enforcement of safety regulations by European standardization bodies, which mandate specific thickness, density, and fire-resistance properties for gymnastics flooring. According to the European Committee for Standardization, compliance with norms such as EN 12503 is mandatory for all competition and training venues, forcing facilities to invest in high-quality certified products. Furthermore, mats and flooring experience higher wear and tear compared to rigid apparatus, necessitating more frequent replacement cycles to maintain safety standards. As per the European Gymnastics Union, clubs and schools undergo regular safety inspections that often result in mandates to upgrade aging floor systems. The versatility of modern matting systems, which can be used for multiple sports and activities, also enhances their appeal to multi-purpose recreation centers. The sheer surface area required for even a small training hall means that flooring projects represent significant capital expenditures, consistently driving this segment to the top of the market hierarchy.

The balance beams segment is anticipated to grow at the fastest CAGR of 8.2% over the forecast period owing to the rising focus on technical precision and the expansion of rhythmic and artistic gymnastics programs for girls. The growing number of competitive events, the increasing emphasis on skill acquisition at younger ages that requires access to high-quality beams for daily practice and the innovation in beam design with manufacturers introducing adjustable height models and enhanced surface textures that mimic competition standards while offering greater safety for learners are further propelling the expansion of the balance beams segment in this regional market. According to the International Gymnastics Federation, the complexity of routines has increased, demanding equipment that provides superior stability and consistent rebound characteristics to support advanced skills. As per national coaching associations, the shortage of adequate training beams in local clubs has become a bottleneck for talent development, prompting a wave of procurement to bridge the gap. Additionally, the trend towards home-based training has spurred demand for compact, foldable beams that allow young athletes to practice balance elements safely in residential settings. The combination of competitive pressure, technological advancements, and the democratization of training equipment through home solutions fuels the rapid expansion of this specific segment.

By Usage Type Insights

The recreational usage segment led the market by accounting for the largest share of the Europe gymnastics equipment market in 2025. The dominance of recreational usage segment in the European market is attributed to the vast number of participants who engage in gymnastics for fun, fitness, and general physical development rather than elite competition. This segment encompasses school physical education classes, community center programs, and casual club activities, which collectively represent the largest volume of equipment consumption. The primary driver is the widespread integration of gymnastics into general education systems, where the focus is on inclusivity and fundamental movement skills rather than high-performance outcomes. According to the European Commission, millions of children participate in school-based sports activities weekly, with gymnastics being a staple due to its ability to develop comprehensive physical literacy. This mass participation model requires durable, versatile, and cost-effective equipment that can withstand high-frequency use by varying skill levels. As per Eurostat, the number of registered recreational sports clubs far exceeds those dedicated solely to competitive training, creating a broader customer base for manufacturers. Furthermore, the rise of "gymnastics for all" initiatives promotes participation across all ages and abilities, further expanding the demand for non-competitive apparatus. The lower barrier to entry for recreational equipment compared to professional-grade gear also facilitates higher sales volumes, solidifying this segment's leadership position in the market landscape.

The professional usage segment is poised to witness the fastest CAGR of 10.6% over the forecast period owing to the increased investment in elite training infrastructure and the hosting of major international competitions. Governments and private investors are pouring resources into state-of-the-art facilities to nurture Olympic hopefuls and attract prestigious events, driving demand for top-tier, regulation-compliant apparatus. A key factor is the legacy effect of hosting events like the European Championships and World Cups, which often leaves behind upgraded venues equipped with the latest technology. According to the European Olympic Committees, several nations have launched strategic plans to improve their medal prospects, resulting in the construction of national high-performance centers. These facilities require the most advanced equipment available, including smart beams and electronic scoring integration, to simulate competition conditions accurately. As per industry analysis, the push for professionalization extends to club levels, where ambitious organizations are upgrading their setups to retain top talent and coaches. The willingness of professional entities to pay a premium for quality, durability, and brand reputation accelerates revenue growth in this segment faster than any other usage type, despite its smaller overall volume compared to recreational users.

By End User Insights

The schools segment dominated the market in Europe in 2025 and held the leading share of the regional market. The mandatory nature of physical education in national curricula, the extensive network of educational institutions across the continent and the legal requirement for schools to provide safe and adequate facilities for gymnastics instruction are contributing to the dominance of schools segment in the European market. According to the Eurydice network, physical education is compulsory in all countries, with gymnastics frequently cited as a core activity for developing motor skills in primary and secondary education. This regulatory framework ensures that public funding is regularly allocated for the purchase and maintenance of gymnastics equipment. As per national ministries of education, thousands of schools undergo periodic facility audits that often trigger procurement cycles to replace outdated or unsafe gear. The sheer number of schools, combined with the need to equip large gymnasiums to accommodate entire classes, results in high-volume orders that dwarf other end-user segments. Furthermore, government initiatives aimed at improving student health and reducing obesity rates have led to increased budgets for sports infrastructure, further reinforcing the leading position of the schools segment in the market.

The fitness centers segment is expected to exhibit ta promising CAGR of 9.5% over the forecast period owing to the integration of gymnastic-style training into mainstream fitness offerings. The rise of functional training, calisthenics, and obstacle course workouts has prompted traditional gyms to incorporate gymnastics apparatus such as rings, parallel bars, and plyometric boxes into their floors. A major factor is the shifting consumer preference towards dynamic and engaging workout routines that challenge balance, strength, and coordination, moving away from monotonous cardio machines. According to the European Health and Fitness Association, the number of health club members has rebounded strongly post-pandemic, with a notable increase in demand for group classes that utilize gymnastic elements. This trend has forced fitness operators to diversify their equipment portfolios to remain competitive and attract younger demographics. As per industry insights, the adoption of "hybrid" training zones that blend weightlifting with gymnastics skills is becoming a standard feature in modern facilities. The scalability of this trend, applicable to both large chains and boutique studios, drives rapid equipment adoption. The ability of gymnastics gear to enhance the perceived value of a gym membership further accelerates investment in this segment, making it the fastest expanding frontier for market growth.

REGIONAL ANALYSIS

Germany Gymnastics Equipment Market Analysis

Germany stood as the leading nation in the Europe gymnastics equipment market by holding 20.9% of the regional market share in 2025. The dominance of Germany in the European market is driven by its robust club system, strong tradition in artistic gymnastics, and high standards for sports infrastructure. The country's market status is defined by a dense network of over 15,000 registered gymnastics clubs that serve millions of members, creating a perpetual demand for high-quality training apparatus. The primary driver for this dominance is the "Turnverein" culture, where gymnastics is deeply embedded in community life and supported by substantial public and private funding. According to the German Olympic Sports Confederation, gymnastics remains one of the most popular organized sports in the nation, ensuring consistent equipment turnover and upgrades. Furthermore, Germany hosts numerous international competitions, necessitating world-class facilities that adhere to the strictest safety and performance standards. As per the Federal Institute for Sports Science, significant investments are made annually in modernizing sports halls and training centers to foster elite talent and promote grassroots participation. The presence of leading domestic manufacturers also strengthens the supply chain, offering cutting-edge solutions tailored to local needs. This combination of cultural depth, institutional support, and industrial capability secures Germany's position as the most influential market for gymnastics equipment in Europe.

France Gymnastics Equipment Market Analysis

France captured a promising share of the Europe gymnastics equipment market in 2025 due to its comprehensive school sports program and a highly successful national competitive gymnastics framework. The strong government backing for sports development, particularly through the Ministry of Sports that prioritizes gymnastics as a key discipline for youth engagement and elite success and the mandatory inclusion of gymnastics in the school curriculum are further propelling the French market growth. According to the French Ministry of National Education, millions of students participate in gymnastics activities annually, driving steady demand for safe and durable apparatus. Additionally, France's consistent performance in international competitions has spurred investment in regional training centers equipped with professional-grade gear to nurture future champions. As per the French Gymnastics Federation, the number of licensed gymnasts has grown steadily, prompting clubs to expand their facilities and update their equipment to meet rising standards. The organization of major events like the World Artistic Gymnastics Championships further stimulates market activity by showcasing the need for advanced technology and safety features. This synergy between education, competitive success, and event hosting sustains France's prominent standing in the regional market.

United Kingdom Gymnastics Equipment Market Analysis

The United Kingdom is predicted to account for a prominent share of the Europe gymnastics equipment market during the forecast period. Factors such as the revitalized focus on grassroots sports development, the legacy of hosting major global sporting events, a fragmented but active landscape of private clubs, school programs, and community leisure centers that are increasingly investing in modern gymnastics facilities are driving the UK market growth. The primary driver for growth is the strategic initiative by UK Sport and local authorities to increase participation rates following the inspiration generated by Olympic successes. According to Sport England, funding allocations for grassroots gymnastics have increased to improve facility quality and accessibility, directly boosting equipment procurement. The rise of recreational gymnastics and ninja warrior-style training in commercial leisure centers has also diversified the demand base beyond traditional clubs. As per British Gymnastics, membership numbers have shown resilience, with a particular surge in preschool and adult categories, necessitating a wider range of apparatus sizes and types. The emphasis on safeguarding and safety standards has further accelerated the replacement of older equipment with compliant, modern alternatives. This combination of strategic funding, diverse participation trends, and safety compliance propels the UK as a key growth market in the region.

Italy Gymnastics Equipment Market Analysis

Italy is projected to witness a healthy CAGR in the Europe gymnastics equipment market during the forecast period owing to the strong tradition in rhythmic gymnastics and a growing emphasis on artistic disciplines within its extensive club network. The pivotal role of local sports associations, the significant influence of successful national athletes who inspire participation at the grassroots level and the integration of gymnastics into the "Avviamento allo Sport" initiative are propelling the Italian market growth. According to the Italian National Olympic Committee, gymnastics remains a popular choice for young girls, particularly in rhythmic disciplines, driving specific demand for carpets, ribbons, and hoops alongside traditional apparatus. The renovation of municipal sports centers, often funded by regional governments, provides another avenue for equipment sales as facilities upgrade to meet modern safety norms. As per the Italian Gymnastics Federation, the number of affiliated clubs continues to grow, fostering a competitive environment that necessitates regular equipment updates. The cultural appreciation for aesthetic sports and the commitment to nurturing talent ensure that Italy remains a vital and dynamic market for gymnastics equipment manufacturers.

Russia Gymnastics Equipment Market Analysis

Russia is anticipated to account for a notable share of the Europe gymnastics equipment market over the forecast period. The historical dominance of Russia in the sport and a state-driven approach to maintaining elite training infrastructure are propelling the Russian market growth. Despite geopolitical challenges, the internal market remains robust due to the deep-rooted culture of gymnastics as a national priority and the continuous operation of specialized sports schools. The primary driver for equipment demand is the government's commitment to preserving its status as a global powerhouse in artistic and rhythmic gymnastics, which requires constant investment in high-performance facilities. According to the Russian Ministry of Sport, significant resources are allocated to regional sports schools and reserve centers to identify and train young talent, ensuring a steady procurement of professional-grade apparatus. The vast geography of the country necessitates a widespread distribution network to supply equipment to remote training centers, creating a unique logistical dynamic. As per the Russian Gymnastics Federation, the focus on self-sufficiency has encouraged the development of domestic manufacturing capabilities, although high-end imported equipment remains in demand for elite levels. The enduring popularity of gymnastics among the youth and the state's unwavering support for competitive success sustain Russia's position as a significant market participant within the European context.

COMPETITIVE LANDSCAPE

The competition in the Europe gymnastics equipment market is characterized by a mix of established global manufacturers and specialized regional players who compete on quality, safety compliance, and technological innovation. Major companies differentiate themselves by obtaining rigorous certifications from international bodies and offering customized solutions tailored to specific client needs ranging from schools to Olympic venues. The market sees frequent product launches featuring enhanced ergonomic designs and integrated digital tools that provide performance analytics for athletes and coaches. Price competition is moderate as buyers prioritize safety and durability over cost savings given the high liability risks associated with equipment failure. Regional specialists often compete by providing superior local service support and faster response times for maintenance requests. The barrier to entry remains high due to the need for extensive testing and certification processes which require significant capital investment. Collaboration between manufacturers and software developers is increasing to create connected ecosystems that link physical apparatus with cloud-based training platforms. Overall, the landscape is dynamic with companies vying to establish themselves as leaders in safety and innovation while adapting to stringent regulatory requirements and shifting consumer preferences towards sustainable and smart equipment solutions across the continent.

KEY MARKET PLAYERS

Some of the notable key players in the Europe gymnastics equipment market are

- Gymnova

- Spieth Gymnastics

- Janssen Fritsen

- ABEO SA

- American Athletic Inc (AAI)

- Norbert's Athletic Products

- Tumbl Trak

- Taishan Sports Industry Group

- Continental Sports Ltd

- Decathlon SA

Top Players in the Market

- Spieth America stands as a premier manufacturer in the Europe gymnastics equipment market, renowned for producing high precision apparatus that meet the strictest international safety and performance standards. The company significantly contributes to the global landscape by supplying equipment for major Olympic Games and World Championships, setting the benchmark for quality worldwide. Spieth recently strengthened its European position by launching a new line of eco-friendly flooring systems designed to reduce environmental impact while enhancing athlete safety. The firm actively collaborates with national federations to develop custom training solutions that integrate advanced shock absorption technologies. By expanding its distribution network across key European nations, Spieth ensures rapid delivery and professional installation services for clubs and arenas. Their commitment to innovation drives the development of adjustable apparatus that cater to both junior and elite athletes, ensuring versatility for diverse training environments. This strategic focus on sustainability and technological advancement solidifies their reputation as a leader in the global gymnastics industry.

- Janssen Fritsen leverages decades of expertise to maintain a dominant presence in the Europe gymnastics equipment market through its comprehensive range of artistic and rhythmic gymnastics products. As a subsidiary of a larger sports group, the company integrates cutting edge materials science to create durable and safe apparatus for users of all ages. Janssen Fritsen recently expanded its European footprint by introducing smart training tools equipped with sensors that provide real time feedback on technique and force distribution. The firm focuses on modular designs that allow facilities to reconfigure spaces easily for different disciplines or events. Through strategic partnerships with local gyms and schools, Janssen Fritsen offers tailored leasing programs that make high quality equipment accessible to organizations with limited budgets. Their dedication to research and development results in innovative safety features such as enhanced grip surfaces and improved landing zones. This customer centric approach combined with continuous product evolution ensures the company remains a trusted partner for gymnastics communities across the continent and globally.

- Gymnova is a leading innovator in the Europe gymnastics equipment market, distinguished by its French heritage and unwavering commitment to excellence in design and manufacturing. The company plays a pivotal role globally by equipping numerous international competitions and training centers with its state-of-the-art apparatus. Gymnova recently strengthened its market position by unveiling a next generation vaulting table that offers superior stability and adjustable resistance settings for varied skill levels. The firm actively invests in sustainable production methods, utilizing recycled materials and energy efficient processes to minimize its carbon footprint. By collaborating with top coaches and athletes, Gymnova incorporates practical insights into its product development cycle to ensure optimal performance and safety. Their expansion into digital services includes virtual reality training modules that complement physical equipment usage. This holistic approach to combining hardware excellence with digital innovation allows Gymnova to meet the evolving needs of modern gymnastics facilities. Their strong brand recognition and focus on quality continue to drive growth and influence in the European and global markets.

Top Strategies Used by Key Market Participants

Key players in the Europe gymnastics equipment market primarily focus on product innovation and technological integration to differentiate their offerings and meet evolving safety standards. Companies heavily invest in research and development to create apparatus using advanced composite materials that offer superior durability and shock absorption. Strategic partnerships with national federations and elite training centers enable manufacturers to test new products in real world scenarios and gain valuable feedback for improvement. Expanding distribution networks through local dealers and online platforms ensures broader market reach and faster delivery times for customers across diverse regions. Firms increasingly adopt sustainable manufacturing practices to align with European environmental regulations and appeal to eco conscious buyers. Offering comprehensive after sales services including installation, maintenance, and certification helps build long term relationships with clients and ensures equipment longevity. Acquisitions of smaller specialized brands allow major players to diversify their product portfolios and enter niche segments such as rhythmic gymnastics or adaptive sports. Continuous engagement with coaching communities through workshops and sponsorships strengthens brand loyalty and drives adoption of new technologies.

MARKET SEGMENTATION

This research report on the European gymnastics equipment market has been segmented and sub-segmented based on categories.

By End User

- Gymnastics Clubs

- Schools

- Fitness Centers

- Recreation Centers

- Individuals

By Material

- Wood

- Metal

- Foam

- Nylon

- Polyurethane

- Glass Fiber

By Age Group

- Children (5-12 years)

- Teenagers (13-19 years)

- Adults (20-59 years)

- Seniors (60 years and above)

By Usage Type

- Recreational

- Competitive

- Professional

By Equipment Type

- Mats Flooring

- Balance Beams

- Vaults

- Uneven Bars

- Parallel Bars

- Pommel Horse

- Rings

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1.What is the Europe gymnastics equipment market?

The Europe gymnastics equipment market refers to the industry involved in manufacturing and supplying equipment used for gymnastics training and competitions.

2.What factors are driving the growth of the Europe gymnastics equipment market?

Growth is driven by increasing participation in gymnastics, rising sports infrastructure investments, and growing interest in fitness activities.

3.What types of gymnastics equipment are commonly used?

Common equipment includes balance beams, uneven bars, rings, vaults, mats, and pommel horses.

4.Who are the major end users in the Europe gymnastics equipment market?

Key end users include schools, sports clubs, training centers, gyms, and professional sports organizations.

5.Which countries are major markets for gymnastics equipment in Europe?

Germany, the United Kingdom, France, Italy, and Spain are key contributors to the market.

6.How do sports programs influence the gymnastics equipment market?

Government and school sports programs increase participation and demand for training equipment.

7.What role do gymnastics clubs play in market growth?

Gymnastics clubs drive equipment demand by providing training facilities and organizing competitions.

8.What materials are commonly used to manufacture gymnastics equipment?

Manufacturers commonly use steel, aluminum, wood, foam, and durable synthetic materials.

9.What is the future outlook for the Europe gymnastics equipment market?

The market is expected to grow steadily due to rising sports participation and increasing investments in athletic infrastructure.

10.What challenges affect the Europe gymnastics equipment market?

Challenges include high equipment costs, strict safety regulations, and limited space for installation.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com