Europe Haemostatic Agents Market Research Report By Type, Treatment, End User and Country (United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands and Rest of Europe) – Industry Size, Share, Trends and Growth Forecast (2025 to 2033)

Europe Hemostatic Agents Market Report Summary

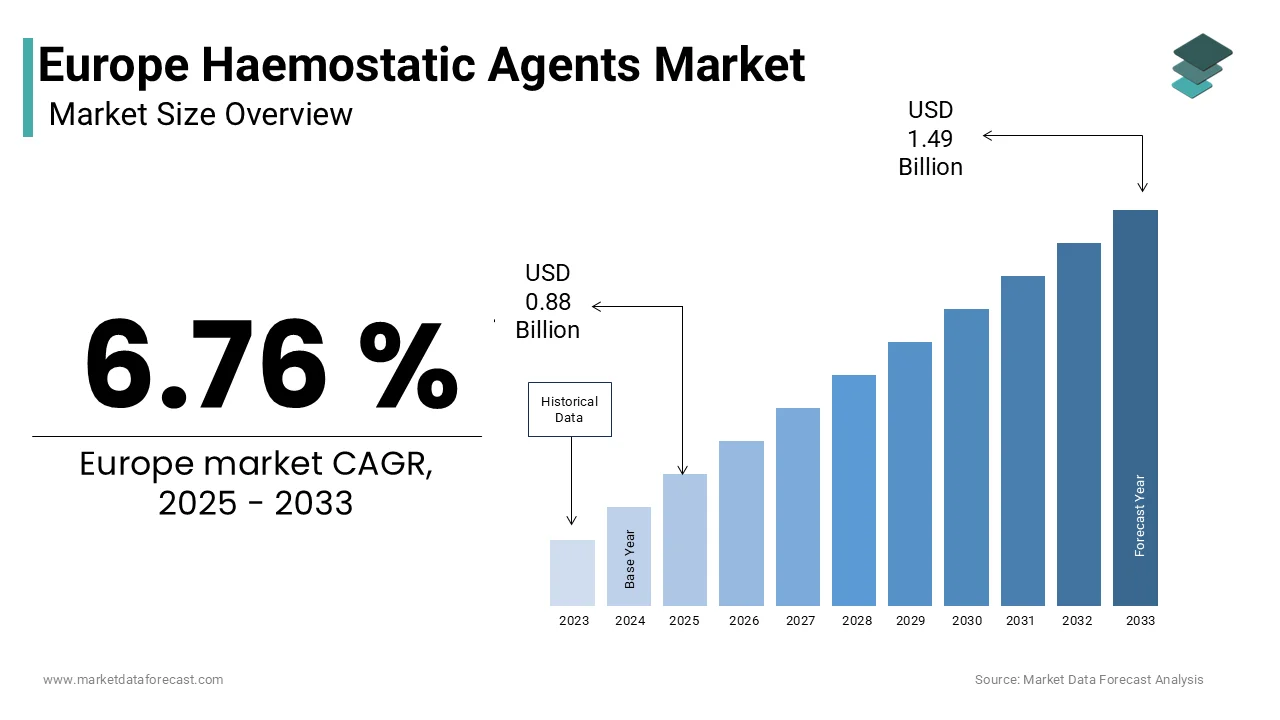

The Europe Hemostatic Agents Market was valued at USD 0.83 billion in 2024, is estimated to reach USD 0.88 billion in 2025, and is projected to reach USD 1.49 billion by 2033, growing at a CAGR of 6.76% during the forecast period (2025–2033). Market growth is driven by the rising number of surgical procedures, increasing prevalence of cardiovascular diseases and trauma cases, and technological advancements in surgical wound management products. The growing demand for minimally invasive surgeries, along with the adoption of advanced hemostatic materials such as fibrin sealants, gelatin sponges, and oxidized cellulose, is further boosting the market. Additionally, Europe’s aging population, well-established healthcare infrastructure, and strong reimbursement framework are contributing to the expansion of hemostatic product utilization across medical facilities.

Key Market Trends

- Increasing Surgical Volume: The rising number of elective and emergency surgeries, particularly cardiovascular and orthopedic procedures, is driving demand for efficient hemostatic solutions.

- Advancements in Biologic Hemostats: Development of bioengineered and recombinant hemostatic agents is improving efficacy, biocompatibility, and absorption rates.

- Minimally Invasive Surgery Growth: Surgeons’ growing preference for laparoscopic and robotic-assisted surgeries is encouraging the adoption of quick-acting hemostatic materials.

- Expanding Trauma and Emergency Care: Europe’s trauma management systems are increasingly integrating topical hemostats for rapid bleeding control.

- Rising Cardiovascular Disease Burden: The Growing prevalence of cardiac disorders and the rise in bypass and valve replacement surgeries are fueling market expansion.

- Focus on Hemostatic Innovation: Manufacturers are investing in fibrin-based, collagen-based, and polymer-based hemostats to address diverse surgical needs.

- Regulatory Support for Surgical Safety: The European Medical Device Regulation (MDR) framework is reinforcing product quality, traceability, and performance standards in surgical devices and agents.

Segmental Analysis

By Type Insights

- The fibrin sealants and others segment held the largest share of 32.1% of the European hemostatic agents market in 2024.

- Its dominance is driven by high clinical efficacy, biological compatibility, and broad applications across cardiovascular, general, and orthopedic surgeries.

- Continuous innovation in plasma-derived and recombinant fibrin sealants is enhancing their adoption in both inpatient and outpatient surgical settings.

By Treatment Insights

- The cardiovascular surgery segment led the European hemostatic agents market in 2024, accounting for a 28.3% share.

- Growth is attributed to the increasing incidence of heart disease, open-heart procedures, and vascular repairs, all requiring reliable hemostatic management.

- The rising complexity of cardiac interventions and preference for low-blood-loss procedures are reinforcing the demand for advanced hemostatic technologies.

By End User Insights

- The hospitals segment dominated the European hemostatic agents market in 2024, occupying a substantial share.

- Hospitals represent the largest consumption base due to high surgical volume, multi-specialty departments, and comprehensive wound management systems.

- The growing establishment of hybrid operating rooms and trauma centers is further increasing the use of modern hemostatic solutions.

Regional Analysis

- Germany was the top performer in the European hemostatic agents market, accounting for an 18.5% share in 2024. The country’s leadership stems from its advanced healthcare system, high procedural volume in cardiovascular and orthopedic surgeries, and early adoption of bio-based hemostats.

- France was the second-largest market, holding a 14.2% share in 2024. Its growth is supported by strong national healthcare policies, expansion of trauma and emergency units, and increased funding for surgical innovation and hospital modernization.

- The United Kingdom remains a major player, driven by high surgical throughput, advanced trauma care systems, and a favorable regulatory environment that supports medical device innovation despite post-Brexit adjustments. The nation’s focus on blood management and operating room safety continues to stimulate steady market growth.

- Italy is experiencing moderate but consistent growth, supported by its aging population and high prevalence of cardiovascular disease. Increased investment in private healthcare and specialized surgical centers is fostering demand for hemostatic solutions.

- Spain is projected to grow considerably during the forecast period, driven by expanding ambulatory surgical practices, modernization of trauma systems, and increased healthcare expenditure on minimally invasive care.

Competitive Landscape

The European Hemostatic Agents Market is highly competitive, characterized by the presence of global medical device manufacturers and specialized wound management companies. Key players are focusing on developing next-generation bioactive and absorbable hemostats, expanding distribution networks, and forming strategic partnerships with hospitals and surgical centers. Mergers and acquisitions are also shaping the market, as larger companies integrate biomaterial specialists and surgical technology firms to enhance their portfolios. Some of the companies that are playing a dominating role in the global Europe Hemostatic Agents Market include Ethicon, Pfizer, Baxter International, R. Bard, The Medicines Company, Anika Therapeutics, Advanced Medical Solutions, Integra LifeSciences, B. Braun Melsungen, Gelita Medical, Equimedical, Vascular Solutions, Marine Polymer Technologies, and Z-Medica.

Europe Haemostatic Agents Market Size

The europe hemostatic agents market was valued at USD 0.83 billion in 2024, is estimated to reach USD 0.88 billion in 2025, and is projected to reach USD 1.49 billion by 2033, growing at a CAGR of 6.76% from 2025 to 2033.

Haemostatic agents are vital medical substances used to accelerate or support the body’s natural blood clotting process during surgical interventions or traumatic injuries. In Europe, these agents are increasingly integrated into both hospital and pre-hospital care protocols across trauma centres and operating rooms. Their relevance spans a wide spectrum of procedures ranging from cardiovascular and neurosurgical operations to emergency battlefield medicine. The clinical urgency to minimise blood loss and reduce transfusion dependence has intensified the adoption of advanced haemostatic technologies. According to the European Society of Anaesthesiology and Intensive Care (ESAIC), surgical bleeding remains a significant cause of perioperative morbidity, leading to the development of extensive guidelines for its management. According to sources, hundreds of millions of surgical procedures are performed globally each year, with tens of millions in Europe, underlining the significant procedural volume driving haemostatic agent utilisation. Furthermore, Trauma, including road traffic injuries, is a major cause of hospital admissions and a significant driver of demand for haemostasis solutions across Europe. The continent’s ageing population also contributes indirectly, as older adults often present with coagulopathies or are on anticoagulant therapy, increasing the complexity of bleeding management during interventions. These structural, clinical, and demographic dynamics establish a foundational need for reliable and effective haemostatic agents across European healthcare systems.

MARKET DRIVERS

Rising Incidence of Trauma and Emergency Surgeries

The escalating burden of physical trauma across European nations has significantly amplified the need for immediate and effective haemostatic intervention, which propels the expansion of the European haemostatic agents market. Road traffic accidents remain a principal source of traumatic injury. The consistent influx of trauma cases places emergency departments and trauma centres under pressure to deploy fast-acting haemostatic agents that can stabilise patients before definitive surgical care. Military and disaster response frameworks within Europe have also expanded their haemostatic readiness. Civilian emergency medical services in countries like Germany and France have similarly adopted haemostatic gauzes and powders as standard equipment. This clinical imperative, backed by institutional protocols and injury epidemiology, sustains a reliable and growing demand for haemostatic agents throughout the European healthcare continuum.

Expansion of Minimally Invasive and Complex Surgical Procedures

The ongoing shift toward minimally invasive surgeries across European healthcare systems has paradoxically increased reliance on topical and absorbable haemostatic agents, which fuels the growth of the European haemostatic agents market. The reduction in incision size and tissue disruption achieved by these methods comes at the cost of limited direct visualisation and physical access, which makes precise and localised bleeding control essential. Haemostatic agents such as oxidised regenerated cellulose and fibrin sealants are routinely employed in these procedures to ensure microvascular integrity without mechanical clamping. Cardiothoracic surgery presents another critical domain. The use of haemostatic matrices and flowable agents in such contexts is not optional but essential to prevent re-exploration for bleeding. These procedural complexities, combined with rising surgical volumes driven by demographic and technological factors, create a sustained and specialised demand for advanced haemostatic solutions in Europe.

MARKET RESTRAINTS

Stringent Regulatory Pathways and Lengthy Approval Timelines

Rigorous regulatory oversight significantly slows product commercialisation and limits portfolio expansion, thereby slowing the expansion of the European haemostatic agents market. Medical devices and biologics used for haemostasis must comply with the European Union Medical Device Regulation 2017 745, which imposes comprehensive clinical evidence requirements, post-market surveillance obligations, and conformity assessments by notified bodies. As per research, the average time to achieve full CE marking for a novel haemostatic device exceeds several months, a timeline that has lengthened due to a shortage of designated notified bodies and heightened scrutiny of biocompatibility and thrombogenicity data. This regulatory bottleneck disproportionately affects small and medium-sized enterprises that lack the infrastructure to navigate complex submissions. Furthermore, the European Medicines Agency maintains strict guidelines for haemostatic agents derived from human or animal plasma, which require extensive viral inactivation validation and traceability documentation. These prolonged pathways not only increase development costs but also delay patient access to next-generation technologies. The resulting market inertia discourages innovation and allows incumbent products with grandfathered approvals to dominate, even when superior alternatives exist. Consequently, regulatory stringency, while essential for patient safety, acts as a significant restraint on market dynamism and technological refresh in the European haemostatic agents landscape.

High Cost of Advanced Haemostatic Products and Reimbursement Limitations

Many advanced haemostatic agents remain financially inaccessible across broad segments of the European healthcare system because of high acquisition costs and inconsistent reimbursement policies, which hamper the growth of the European haemostatic agents market. Fibrin sealants and synthetic haemostatic matrices can cost significantly, which places them beyond routine use in cost-constrained settings. National health technology assessment bodies often restrict reimbursement to specific high-risk procedures by limiting adoption in general surgery or emergency departments. This financial gatekeeping not only compromises clinical outcomes but also fragments market access, as manufacturers must navigate a patchwork of national pricing and reimbursement decisions. Such disparities undermine equitable access to life-saving haemostasis technologies. Inconsistent adoption of innovative haemostatic agents across Europe is hindering market growth, a problem that will continue until pricing models are aligned with healthcare budgets and reimbursement policies are broadened.

MARKET OPPORTUNITIES

Integration of Haemostatic Agents in Point of Care and Pre-Hospital Settings

The systematic deployment of haemostatic agents beyond hospital operating rooms into community-based and pre-hospital emergency care environments creates new opportunities for the European haemostatic agents market. Ambulance services, fire brigades, and first responder units across Europe are increasingly being equipped with haemostatic dressings to manage life-threatening bleeding before hospital arrival. Leading medical bodies are increasingly recommending advanced haemostatic dressings as standard practice for managing severe external bleeding. The integration of haemostatic gauze into emergency medical service protocols is a key factor in improving patient survival rates from severe blood loss in pre-hospital settings. Military adoption further validates this trend. This expanding operational footprint transforms haemostatic agents from niche surgical tools into essential components of public health emergency preparedness, which opens new procurement channels and scaling usage beyond traditional hospital silos.

Advancements in Bioresorbable and Synthetic Haemostatic Technologies

The evolution of next-generation haemostatic agents that are fully bioresorbable, non-immunogenic, and derived from non-animal sources provides a major opportunity for the expansion of the European haemostatic agents market. Traditional agents relying on bovine or human plasma face persistent safety and ethical concerns, which drive demand for synthetic alternatives. Polysaccharide-based matrices and recombinant human thrombin formulations now offer comparable efficacy without zoonotic or supply chain risks. These technologies align with the European Green Deal’s emphasis on sustainable and ethically sourced medical products, enhancing their regulatory and institutional appeal. Hospitals aiming for reduced transfusion reliance and consistent product performance can benefit from these engineered solutions' supply stability and predictable outcomes. Their compatibility with robotic and laparoscopic delivery systems further positions them as indispensable tools in the future of precision surgery across Europe.

MARKET CHALLENGES

Risk of Adverse Reactions and Immunogenicity with Biological Agents

The immunological risks associated with biologically derived products, particularly those sourced from human or bovine plasma, challenge the growth of the European haemostatic agents market. Fibrin sealants and gelatin-based matrices can trigger hypersensitivity reactions, foreign body responses, or even anaphylaxis in susceptible patients. These immune-mediated complications not only endanger patient safety but also expose healthcare providers to litigation and regulatory scrutiny. Furthermore, religious and cultural objections to animal-derived ingredients, particularly among Muslim and Jewish communities, limit acceptance in diverse urban centres like London, Paris, and Berlin. Also, the clinical caution constrains product selection and forces institutions to maintain multiple agent types, increasing inventory complexity and costs. The risk of immunogenicity continues to limit the widespread acceptance of biological haemostatic agents across Europe, a situation that will persist until fully synthetic or recombinant alternatives can match their performance in all clinical scenarios.

Supply Chain Vulnerabilities for Plasma-Derived and Raw Material Inputs

Supply chain fragility due to its dependence on specialised biological raw materials, particularly human plasma and bovine collagen, further constrains the expansion of the European haemostatic agents market. Europe is heavily dependent on the United States for a significant majority of its plasma-derived pharmaceutical ingredients. Shortfalls in the US plasma collection system can directly lead to product allocation delays in European countries. Similarly, bovine-sourced materials are subject to stringent animal health regulations. Non-compliance with traceability standards by major international suppliers can disrupt the manufacturing processes of leading producers in Europe. Moreover, the concentration of manufacturing in a limited number of certified facilities. These systemic vulnerabilities challenge inventory reliability and force clinicians to substitute less optimal agents, potentially compromising surgical outcomes and patient safety across the region.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Type, Treatment, End User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Ethicon, Pfizer, Baxter International, R. Bard, The Medicines Company, Anika Therapeutics, Advanced Medical Solutions, Integra LifeSciences, B. Braun Melsungen, Gelita Medical, Equimedical, Vascular Solutions, Marine Polymer Technologies, Z-Medica. |

SEGMENTAL ANALYSIS

By Type Insights

The fibrin sealants and others segment held the largest market share of 32.1% of the European haemostatic agents market in 2024. The dominance of the fibrin sealants and others segment is driven by their dual functionality as surgical sealants and haemostats, enabling effective tissue adhesion and bleeding control in high-risk procedures. A further driver of this segment is their widespread adoption in cardiovascular and transplant surgeries, where precision and biocompatibility are paramount. Their autologous or recombinant origin also aligns with European regulatory preferences for non-bovine alternatives, which reduces immunogenicity concerns. The availability of CE-marked products further institutionalises their use in tertiary care centres.

The combination haemostats segment is on the rise and is expected to be the fastest-growing segment in the regional market by witnessing a CAGR of 9.4 from 2025 to 2033. The rapid growth of the combination haemostats segment is fueled by the rising demand for multifunctional products that integrate mechanical scaffolding with biochemical clotting activation. Combination agents, typically blending gelatin or cellulose matrices with thrombin or fibrinogen, offer synergistic haemostasis in diffuse or hard-to-access bleeding sites. A different growth accelerator of this segment is their efficacy in oncological and spinal surgeries, where conventional monotherapy often fails. Furthermore, regulatory endorsements are expanding access. The shift towards greater operative efficiency and patient safety in European hospitals highlights the role of combination haemostats as the leading edge in advanced bleeding control solutions.

By Treatment Insights

In 2024, the cardiovascular surgery segment led the European haemostatic agents market and accounted for a 28.3% share. The prominence of the cardiovascular surgery segment is driven by the inherently high bleeding risk associated with cardiopulmonary bypass, anticoagulant use, and manipulation of fragile cardiac tissues. Nearly all these procedures necessitate advanced haemostatic support due to systemic heparinization and platelet dysfunction induced by extracorporeal circuits. Fibrin sealants and oxidised regenerated cellulose are routinely deployed to achieve haemostasis on suture lines and raw myocardial surfaces. Moreover, the ageing population intensifies demand. National clinical guidelines mandate the intraoperative availability of topical haemostats in all cardiac theatres, which institutionalises their use and cements cardiovascular surgery as the dominant treatment segment.

The neurosurgery and others segment is expected to exhibit a noteworthy CAGR of 8.7% from 2025 to 2033 due to the zero tolerance for intracranial bleeding and the rising volume of minimally invasive neuro procedures across Europe. Moreover, neurosurgeons prioritise ultra-precise adhesives and bioresorbable haemostats like oxidised regenerated cellulose and flowable gelatin thrombin formulations. Furthermore, national investments in neurosurgical infrastructure are accelerating adoption. Regulatory bodies in the Netherlands and Switzerland have also fast-tracked approvals for neuro-compatible haemostats due to unmet clinical need. The escalating challenge posed by neurological conditions in Europe is driving a demand for specialised haemostatic tools that will exceed the growth rate seen in other surgical fields.

By End User Insights

The hospitals segment dominated the European haemostatic agents market and occupied a substantial share in 2024. The growth of the hospitals segment is attributed to their role as the primary site for complex, high-acuity surgeries requiring advanced bleeding control. European hospitals perform the vast majority of cardiovascular, oncological, and trauma procedures where haemostatic agents are indispensable. Tertiary referral centres, in particular, maintain extensive formularies that include fibrin sealants, collagen matrices, and combination products. National procurement frameworks further consolidate hospital dominance. Apart from these, the integration of haemostatic protocols into hospital accreditation standards mandates their availability in operating theatres and emergency departments. The high concentration of surgical specialists and the presence of blood banks also make hospitals the natural epicentre for haemostatic agent deployment, which supports their market leadership across all European subregions.

The surgery centres segment is predicted to witness the highest CAGR of 10.1% over the forecast period. The swift expansion of the surgery centres segment is driven by the continent-wide shift toward outpatient and ambulatory surgical models, particularly in orthopaedic, ophthalmic, and dermatological procedures. Many of these procedures, despite being traditionally lower risk, are increasingly using topical hemostats to minimise postoperative complications and facilitate faster discharge. Regulatory evolution has also enabled broader adoption. Apart from these, cost efficiency initiatives incentivise surgery centres to adopt single-use haemostats that reduce operating room turnaround time. The prioritisation of dehospitalization in European healthcare, a strategy to manage bed shortages and costs, is fostering the continued rise of surgery centres as a vital and expanding pathway for haemostatic agent supply.

COUNTRY LEVEL ANALYSIS

Germany Haemostatic Agents Market Analysis

Germany was the top performer in the European haemostatic agents market and accounted for an 18.5% share in 2024. Its high volume of complex surgical interventions, robust healthcare infrastructure, and early adoption of advanced medical technologies are propelling the demand for haemostatic agents in the German market. Germany performs millions of inpatient surgeries annually, with a significant proportion involving cardiovascular and oncological procedures that demand sophisticated haemostasis. The nation hosts Europe’s highest density of university hospitals and trauma centres, all of which maintain comprehensive haemostatic protocols. Regulatory alignment with EU MDR and strong reimbursement frameworks through statutory health insurance ensure consistent product access. Furthermore, Germany’s medical device manufacturing base drives domestic innovation and clinical validation of next-generation haemostats. Hence, Germany remains the undisputed anchor of the European haemostatic agents market.

France Haemostatic Agents Market Analysis

France was the second-largest player in the European haemostatic agents market and occupied a 14.2% share in 2024. The growth of the French market is driven by its centralised healthcare system and high procedural volumes in trauma and transplant surgery. The French public hospital network conducts millions of surgical procedures annually. France is a European leader in organ transplantation. These procedures heavily rely on fibrin sealants and combination haemostats to manage parenchymal bleeding. National clinical guidelines recommend topical haemostats for liver and lung resections, institutionalising their use. The country’s strong biomedical research ecosystem, including institutes like INSERM, further accelerates clinical adoption of novel haemostatic formulations, solidifying France’s position as a key growth engine in the region.

United Kingdom Haemostatic Agents Market Analysis

The United Kingdom is a major player in the European market, with its high surgical throughput and trauma care demands despite post-Brexit regulatory adjustments. It oversees a large number of inpatient operations yearly, with a notable concentration in cardiovascular and gastrointestinal surgeries. The UK is also a hub for trauma research and protocol development. The UK has adopted a domestic legal framework to enable conformity assessment bodies to continue operating, which allows for the continued placing of products on the Great Britain market. Hence, the UK sustains robust demand for reliable and CE or UKCA-marked haemostatic technologies.

Italy Haemostatic Agents Market Analysis

Italy is moderately growing in the European haemostatic agents market due to its ageing population and high prevalence of cardiovascular disease. A share of Italians are aged 65 or older, the second highest proportion in the EU after Portugal. This demographic reality fuels demand for cardiac surgeries. Italian university hospitals in Milan, Rome, and Turin are early adopters of bioresorbable haemostats, particularly in neurosurgical and hepatic applications. The Italian Medicines Agency maintains a positive reimbursement stance for CE-marked haemostatic agents used in high-risk surgeries, facilitating broad hospital access. Apart from these, Italy’s strong tradition in minimally invasive surgery promotes the use of injectable and flowable haemostats compatible with laparoscopic tools. Regional healthcare autonomy does create procurement variability, but national clinical societies like the Italian Society of Surgery have issued consensus guidelines that standardise haemostatic agent use across major centres, supporting consistent market growth.

Spain Haemostatic Agents Market Analysis

Spain is likely to grow in the European haemostatic agents market between 2025 to 2033 due to expanding ambulatory surgery and trauma system modernisation. Spain performs millions of hospital surgeries annually, as per the Ministry of Health, with a rising shift toward day surgery in private and public outpatient centres. The country’s trauma burden is significant. Spanish hospitals have integrated combination haemostats into colorectal and liver resection pathways following positive outcomes from the Spanish Surgical Infection Study Group trials. The country's role as a top-five European market for haemostatic agents will strengthen as it upgrades rural emergency care and expands robotic surgery networks.

COMPETITIVE LANDSCAPE

The European haemostatic agents market exhibits intense competition characterised by a mix of multinational corporations and specialised European medical device firms. Established players leverage brand recognition, clinical evidence and extensive distribution networks to maintain dominance,ce while emerging companies focus on niche innovations such as plant-derived or microbial-fermented haemostats. The regulatory environment under EU MDR has raised entry barriers, intensifying the advantage for incumbents with robust quality systems. Product differentiation through formulation delivery mechanisms and biocompatibility profiles is a key competitive lever. Pricing pressures from national reimbursement bodies further complicate market dynamics, pushing companies to demonstrate clear health economic benefits. Simultaneously, hospitals increasingly demand integrated solutions that combine haemostasis with adhesion prevention or antimicrobial properties. This evolving landscape fosters continuous innovation but also consolidates market power among firms capable of navigating clinical, regulatory, and commercial complexities across diverse European healthcare systems.

KEY MARKET PLAYERS

Companies playing an influential role inEuropeanurope haemostatic agents market profiled in this report are

- Ethicon

- Pfizer

- Baxter International

- R. Bard, The Medicines Company

- Anika Therapeutics

- Advanced Medical Solutions

- Integra LifeSciences

- B Braun Melsungen

- Gelita Medical

- Equimedical

- Vascular Solutions

- Marine Polymer Technologies

- Z-Medica.

TOP LEADING PLAYERS IN THE MARKET

- Ethicon, a subsidiary of Johnson andJohnsonon is a prominent contributor to the European haemostatic agents market with a comprehensive portfolio that includes Surgiflo and Floseal. The company focuses on advanced haemostatic technologies tailored for complex surgical environments. Ethicon has strengthened its position through strategic regulatory submissions and clinical collaborations with European surgical societies. In recent years, the company has invested in educational initiatives to train surgeons on the optimal use of its haemostatic products across cardiovascular and neurosurgical procedures. These efforts reinforce its reputation for clinical excellence and support broader adoption across EU hospitals and surgical centres.

- Baxter International maintains a strong footprint in the European market through its Tisseel and Evicel fibrin sealant platforms. The company emphasises biocompatibility and reliability in high-risk surgical settings. Baxter has enhanced its market influence by expanding manufacturing capacity in Europe to ensure supply chain resilience. It also partners with national health authorities to align product indications with local clinical guidelines. Recent R&D investments have focused on recombinant thrombin formulations to address plasma-derived safety concerns. These initiatives underscore Baxter’s commitment to innovation and regulatory compliance across the European haemostatic agents landscape.

- B Braun plays a critical role through its Aesculap division, offering a range of absorbable haemostats, including gelatin and cellulose-based products. The company leverages its German engineering heritage to deliver precision haemostatic solutions for minimally invasive and open surgeries. B Braun has recently intensified its engagement with European surgical training academies to demonstrate product efficacy in robotic and laparoscopic applications. It has also modernised its production facilities in Melsungen to meet EU MDR requirements ahead of schedule. These proactive measures solidify B Braun’s position as a trusted partner in European surgical care.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European haemostatic agents market employ several strategic approaches to maintain competitiveness and drive growth. Product innovation remains central with companies investing heavily in R&D to develop bioresorbable synthetic and recombinant haemostats that address safety and ethical concerns. Regulatory compliance is another critical strategy as firms align with EU MDR 2017 745 to secure timely CE certifications. Strategic collaborations with academic hospitals and surgical societies enhance clinical validation and surgeon adoption. Companies also pursue regional manufacturing to strengthen supply chain resilience and mitigate import dependencies. Additionally, they engage in educational outreach and training programs to demonstrate proper use and build trust among healthcare professionals. These multifaceted strategies collectively reinforce market presence and support long-term sustainability in Europe’s evolving haemostatic landscape.

MARKET SEGMENTATION

This research report on the europe haemostatic agents market has been segmented and sub-segmented into the following categories.

By Type

- Thrombin-Based Haemostats

- Gelatin-Based Haemostats

- Collagen-Based Haemostats

- Oxidised Regenerated Cellulose-Based Haemostats

- Combination Haemostats

- Fibrin Sealants and Others

By Treatment

- Cardiovascular

- General Surgery

- Digestive Surgery

- Neurosurgery and Others

By End User

- Hospitals

- Surgery Centres

- Nursing Homes and Others

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands, and the Rest of Europe

Frequently Asked Questions

1. Which product types dominate the Europe Haemostatic Agents Market?

Topical hemostats and adhesive & tissue sealants are the primary product categories dominating the Europe Haemostatic Agents Market, with topical hemostats holding the largest revenue share due to their widespread surgical use.

2. How does the aging population impact the Europe Haemostatic Agents Market?

The aging population in Europe is prone to chronic diseases and injuries that require surgical interventions. This demographic trend increases the demand for haemostatic agents to manage bleeding and improve surgical outcomes.

3. What are the key challenges facing the Europe Haemostatic Agents Market?

High costs of surgical treatments, strict regulatory approvals, and limited awareness of advanced hemostatic technologies are key challenges restraining the growth of the Europe Haemostatic Agents Market.

4. Which countries contribute the most to the Europe Haemostatic Agents Market?

Germany, France, and the UK are major contributors to the Europe Haemostatic Agents Market, driven by their advanced healthcare systems and investment in surgical technology.

5. How is technology influencing the Europe Haemostatic Agents Market growth?

Emerging technologies like robot-assisted surgeries and advanced synthetic sealants foster growth in the Europe Haemostatic Agents Market by improving surgical precision and reducing post-operative complications

6. What role do minimally invasive surgeries play in the Europe Haemostatic Agents Market?

Minimally invasive surgeries reduce patient recovery time and complications and drive demand for specialized haemostatic agents tailored to these techniques in the Europe market.

7. How is the Europe Haemostatic Agents Market segmented by end user?

The Europe Haemostatic Agents Market primarily serves hospitals, surgical centers, and trauma care units, with hospitals accounting for the majority of market consumption.

8. What are some leading companies in the Europe Haemostatic Agents Market?

Key players include Ethicon, Pfizer, Baxter International, R. Bard, and Advanced Medical Solutions, who have a strong presence and product portfolios in the Europe Haemostatic Agents Market.

9. How do chronic diseases affect the Europe Haemostatic Agents Market?

Increased prevalence of chronic diseases such as diabetes and cardiovascular disorders necessitate more surgical procedures, thereby boosting demand for haemostatic agents in Europe

10. What types of haemostatic agents are gaining popularity in Europe?

Combination hemostats, thrombin-based, and oxidized regenerated cellulose-based hemostats are gaining traction due to their efficacy in complex surgeries in Europe.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com