Europe Hay Market Size, Share, Growth, Trends And Forecasts Report, Segmented By Product, Type, And By Region (The UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Hay Market Size

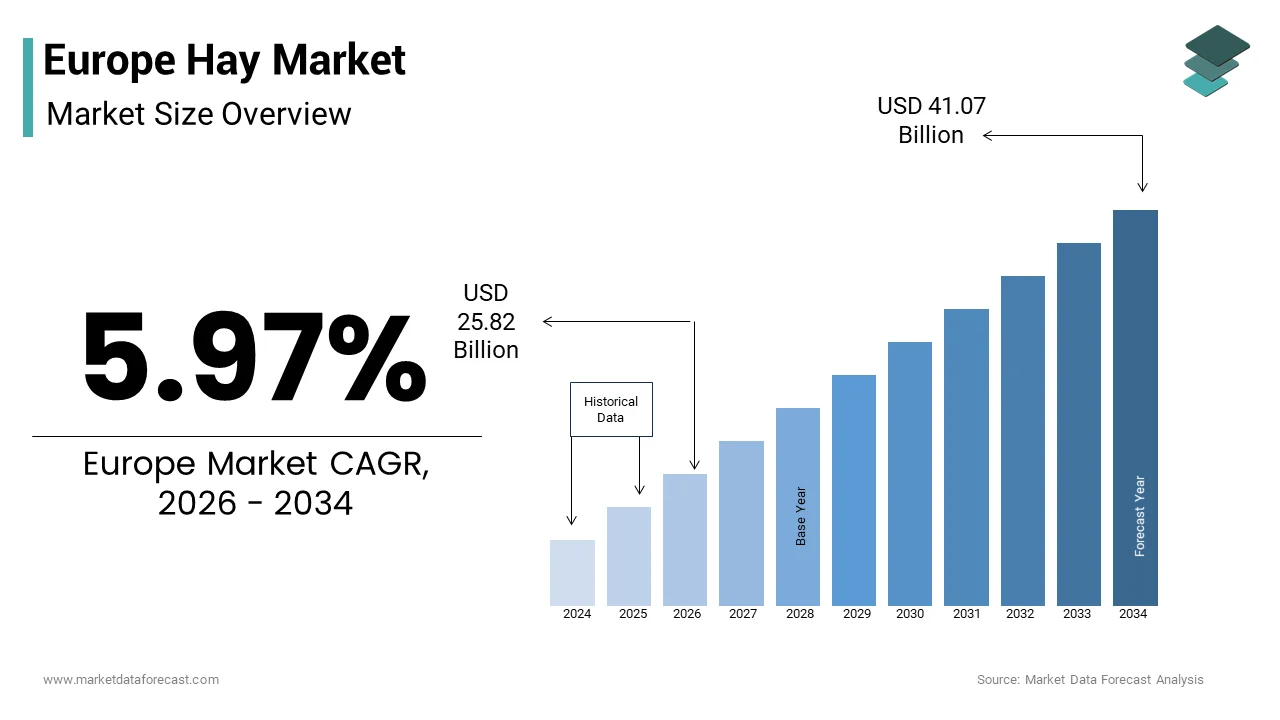

The Europe Hay Market size was valued at USD 24.37 billion in 2025 and is anticipated to reach USD 25.82 billion in 2026 to reach USD 41.07 billion by 2034, estimated to be growing at a CAGR of 5.97% during the forecast period from 2026 to 2034.

Hay plays a crucial role in supporting the livestock industry, particularly in dairy and beef cattle farming. As of 2024, Europe accounts for over 30% of global forage production, with hay forming a significant portion of this output. Countries such as Germany, France, Spain, and Poland are among the largest producers, collectively contributing to more than 55% of total EU hay output. According to Eurostat, approximately 18 million hectares of agricultural land in the EU are dedicated to grassland and forage crops, with hay being a dominant component. The demand for high-quality hay has been driven by the need for a consistent feed supply amid fluctuating pasture availability due to climate variability.

As per the European Environment Agency, changing weather patterns have led to more frequent droughts and unseasonal rainfall, reducing natural grazing capacity and increasing reliance on stored forages like hay. This shift is especially evident in southern Europe, where prolonged dry spells have reduced pasture productivity by up to 20% since 2020. Additionally, the European Commission reports that over 60% of large-scale dairy farms now rely on purchased or stored hay during winter months, reflecting structural changes in feeding strategies. With rising animal numbers and stricter environmental regulations on manure management, hay remains a vital resource in maintaining sustainable and efficient livestock operations across Europe.

MARKET DRIVERS

Rising Demand for High-Quality Animal Feed Amid Expanding Livestock Production

One of the primary drivers of the Europe hay market is the growing demand for high-quality forage to support the region’s expanding livestock sector, particularly in dairy and beef cattle farming. According to the European Milk Board, EU milk production reached 113 billion liters in 2023, requiring consistent and nutritious feed supplies throughout the year. Hay, especially alfalfa and clover varieties, plays a central role in meeting these nutritional needs. As per Eurostat, the number of dairy cows in the EU increased by 2.4% between 2020 and 2023, reaching over 24 million head, with major increases seen in the Netherlands, Germany, and Ireland. These animals require stable feed sources, especially during winter when fresh grazing is unavailable. In response, hay consumption in dairy farms rose by an estimated 18% over the same period, according to the European Grassland Federation.

Moreover, approximately 70% of beef cattle in Western Europe receive hay-based diets for at least six months of the year, ensuring protein and fiber intake necessary for weight gain and health maintenance. With organic and grass-fed meat and dairy markets expanding, particularly in Scandinavia and Alpine regions, the demand for premium hay with low contamination levels is expected to grow further, reinforcing its strategic importance in European agriculture.

Climate-Induced Pasture Shortages Increasing Reliance on Stored Forage

Climate change is increasingly influencing agricultural practices across Europe, directly impacting pasture availability and driving up the demand for alternative forage sources like hay. According to the European Environment Agency (EEA), Southern and Central Europe experienced a 15% reduction in usable grazing days in 2023, primarily due to prolonged droughts and erratic rainfall patterns. In Spain, for example, pasture yield dropped by nearly 25% in Andalusia and Castilla-La Mancha due to extreme heatwaves, pushing farmers to increase hay procurement to sustain livestock. Similarly, in France, the Ministry of Agriculture reported a 20% decline in fresh forage availability in 2023, prompting a corresponding rise in hay imports from Germany and Eastern Europe. According to the EEA, since 2018, the frequency of severe drought events in Europe has doubled, leading to greater unpredictability in pasture-based feeding systems. This instability is prompting farmers to invest in higher-quality hay reserves to ensure feed continuity, especially in dairy and beef operations. As a result, hay production and trade within the EU have seen steady growth, with total hay exports within Europe rising by 12% in 2023, according to the European Free Trade Association (EFTA). These trends underscore how climate-induced disruptions are reshaping feed sourcing strategies and boosting the overall hay market in Europe.

MARKET RESTRAINTS

Fluctuating Weather Patterns Affecting Hay Yield and Quality

One of the most significant restraints hindering the growth of the Europe hay market is the impact of unpredictable weather conditions on hay production. Excessive rainfall during harvest seasons or prolonged droughts can severely affect both yield and nutritional content, making it difficult for farmers to maintain a consistent supply of high-quality forage. According to the European Environment Agency (EEA), unpredictable spring and summer weather has led to a 12–18% annual variation in hay yields across key producing countries such as France, Germany, and Italy. In 2023, heavy rains in Northern Europe delayed harvesting, causing mold infestations in over 20% of first-cutting hay, rendering it unsuitable for high-value dairy use.

In contrast, Southern Europe faced extended dry spells, resulting in lower leaf retention and reduced protein content in hay, which negatively impacts livestock performance. As per the Italian National Institute for Agricultural Economics, alfalfa hay crude protein levels fell below 14% in parts of Sicily and Sardinia, down from an average of 18%, affecting marketability. These fluctuations not only disrupt local production but also create price volatility. According to the European Commission, hay prices in the EU varied by up to 30% between 2022 and 2023, depending on regional availability and quality concerns.

Rising Cost of Production and Input Prices

The increasing cost of production, which includes expenses related to land use, machinery, fertilizers, and labor, is further impeding the growth of the European hay market. As input costs rise, many small and mid-sized hay producers are finding it harder to maintain profitability, limiting their ability to scale or meet growing demand. As per the European Fertilizer Manufacturers Association (EFMA) reports that fertilizer prices surged by over 40% in 2022, significantly affecting hay crop fertility and yield potential.

Labor costs have also risen sharply, particularly in Western Europe, where minimum wage increases and labor shortages have pushed operational costs up by 15%, as noted by the German Farmers’ Union in 2023. This economic pressure has led some farmers to reduce hay acreage or switch to alternative crops with better returns, thereby tightening the overall hay supply. According to the estimations of the European Commission, hay production declined slightly in several Western European countries in 2023, despite strong demand, highlighting the impact of rising costs on market dynamics. Without policy support or technological advancements to offset these pressures, the rising cost of production will continue to constrain the growth of the European hay market.

MARKET OPPORTUNITIES

Expansion of Organic Livestock Farming Driving Demand for Chemical-Free Hay

A growing shift toward organic livestock farming across Europe is creating new opportunities for the hay market, particularly for chemical-free and sustainably produced forage. As consumer demand for organic meat and dairy products rises, so does the requirement for certified organic feed inputs, including hay. According to the Research Institute of Organic Agriculture (FiBL), the number of organic livestock farms in Europe increased by 9% in 2023, with countries like Austria, Sweden, and Denmark leading the transition. These farms must adhere to strict guidelines that prohibit synthetic pesticides and fertilizers, making organic hay a critical input.

As per the European Commission, organic hay production in the EU expanded by 14% between 2021 and 2023, with Germany, France, and Hungary emerging as key suppliers. Premium pricing for organic hay is up to 30% higher than conventional alternatives, which is incentivizing more farmers to convert part of their land to organic hay cultivation. Additionally, the EU Organic Regulation (EU 2018/848) mandates that organic ruminants must obtain a minimum of 60% of their feed from forage, further strengthening the demand for high-quality hay. With the European Green Deal promoting agroecological transitions, the organic hay segment is poised for sustained growth, offering a lucrative niche within the broader European hay market.

Integration of Hay in Carbon Sequestration and Sustainable Farming Programs

An emerging opportunity for the European hay market lies in its integration into carbon sequestration initiatives and sustainable farming programs supported by the Common Agricultural Policy (CAP). Permanent grasslands, including those used for hay production, play a key role in soil carbon storage and biodiversity preservation, aligning with the EU’s climate goals. According to the European Environment Agency, permanent grasslands in the EU store approximately 10% of total agricultural soil carbon, with well-managed hay fields contributing significantly to this figure. Hay meadows cover over 12 million hectares of farmland, serving as carbon sinks while also supporting pollinators and other wildlife.

Under CAP's Eco-schemes, farmers who maintain permanent grasslands and avoid conversion to arable land are eligible for subsidies. In 2023, France introduced a national incentive program offering €180 per hectare for hay meadow conservation, encouraging farmers to retain traditional hay systems rather than shifting to more intensive cropping. Similarly, in the UK, the Environmental Land Management Scheme (ELMS) supports farmers practicing low-input hay production, promoting ecological balance and long-term sustainability. By linking hay production to environmental benefits, policymakers and agricultural stakeholders are opening new revenue streams and reinforcing the value of hay beyond livestock feed, enhancing its market outlook in Europe.

MARKET CHALLENGES

Competition from Alternative Forage Sources and Feed Substitutes

The rising competition from alternative forage sources and feed substitutes, which are often more convenient or cost-effective for certain types of livestock operations, is one of the prominent challenges to the growth of the European hay market. Silage, straw, and processed feed pellets are becoming more widely adopted, particularly in large-scale commercial farms where storage and handling efficiency are prioritized. According to the European Dairy Association, silage usage in EU dairy farms increased by 16% between 2020 and 2023, driven by improvements in fermentation technology and easier mechanized feeding systems. Unlike hay, silage retains higher moisture content and energy density, making it more suitable for high-yield dairy herds.

In addition, the European Feed Manufacturers' Association reports that the use of compound feed for ruminants grew by 8% in 2023, particularly in urban and peri-urban livestock systems where land constraints make hay cultivation impractical. Furthermore, innovations in feed formulation, such as protein-rich legume blends and hydroponic fodder systems, are gaining traction in niche markets, especially in countries like the Netherlands and Denmark, where precision livestock farming is widespread. These alternative feed options, combined with evolving farm management practices, present a notable challenge to the dominance of hay in the European livestock diet, necessitating differentiation through quality, consistency, and targeted marketing to maintain market relevance.

Seasonal Availability and Storage Constraints Limiting Market Stability

Seasonal availability and storage limitations remain a persistent challenge for the Europe hay market, affecting both supply consistency and product quality throughout the year. Unlike grain-based feeds or silage, hay is highly dependent on favorable weather during the short harvesting window, and improper storage can lead to spoilage and nutrient loss. According to the European Grassland Federation, hay harvested outside optimal conditions can lose up to 25% of its nutritional value, particularly in terms of protein and digestibility. This variability affects livestock performance and reduces buyer confidence in off-season purchases.

Storage issues are equally pressing. The German Farmers’ Union reports that improperly stored hay results in losses of up to 15% annually, primarily due to mold development and spontaneous combustion risks if moisture content exceeds recommended levels. Additionally, as per the European Commission, only 40% of EU farms have dedicated, climate-controlled hay storage facilities, forcing many smallholders to sell quickly after harvest at lower prices or risk degradation. This seasonality-driven supply chain creates price volatility and limits the ability of producers to offer year-round reliability, posing a structural challenge to market expansion and stakeholder investment in the European hay industry.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.97% |

| Segments Covered | By Product, Type, and Region. |

| Various Analyses Covered | Global, Regional and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Anderson Hay & Grain, Border Valley, Knight Ag Sourcing, Hay USA, Bailey Farms, Hayday Farm, Barr-Ag, Standlee, Legal Alfalfa Products Ltd, M&C Hay. |

SEGMENTAL ANALYSIS

By Product Insights

Largest Segment: Hay Bales

The hay bales segment dominated the European hay market by holding 77.4% of the European market share in 2025. The domination of the hay bales segment in the European market is primarily due to their widespread use across traditional and large-scale livestock operations. This segment remains the backbone of forage feeding systems, especially in dairy and beef cattle farming. According to Eurostat, over 90% of EU farms that rear ruminants rely on hay bales as a primary feed source during winter months when fresh pasture is unavailable. Their dominance stems from ease of storage, compatibility with existing farm equipment, and minimal processing requirements compared to pellets or cubes. As per the European Grassland Federation, hay bales account for more than 65% of all harvested forage traded within the EU, with Germany, France, and Poland being the largest producers and consumers. The demand is particularly strong in rural and semi-mechanized farms where infrastructure limitations make processed forms of hay less practical. Additionally, according to the European Commission, over 70% of organic livestock farms exclusively use hay bales, citing better traceability, lower processing impact, and compliance with organic certification standards. These factors collectively reinforce hay bales as the most dominant product type, maintaining their stronghold despite emerging alternatives like pelleted and cubed hay products.

The hay pellets segment is predicted to witness the highest CAGR of 9.3% over the forecast period, owing to the evolving feeding practices and increasing adoption in niche livestock sectors. One of the key drivers behind this growth is the rising use of pelleted hay in equine nutrition, particularly among urban horse owners and performance stables where dust reduction and controlled nutrient intake are critical. According to the European Equestrian Federation, pellet-based feeding systems have gained traction among 35% of professional stables in Western Europe, up from just 12% in 2018. The integration of hay pellets into precision livestock farming models, especially in robotic feeding systems used in high-tech dairy barns, is also contributing to the expansion of the hay pellets segment in the European market. According to the German Agricultural Machinery Association, automated feeding units in smart dairy farms increasingly utilize pelleted forages due to their uniformity and ease of dispensing. Furthermore, hay pellet exports grew by 22% in 2023, driven by demand from smallholder farmers in Eastern Europe and North Africa seeking compact, transportable feed solutions. With these trends aligning toward convenience, consistency, and specialized applications, hay pellets are gaining momentum as a preferred alternative in modern agricultural systems.

By Type Insights

The dairy cow feed segment led the market by commanding 57.5% of the European market share in 2025. The growth of the dairy cow feed segment is majorly driven by the growing reliance of the dairy cow feed sector on consistent and high-quality forage inputs. This dominance is directly linked to the scale and nutritional demands of the European dairy industry. For instance, according to the European Milk Board, EU milk production reached 113 billion liters in 2023, supported by over 24 million dairy cows, each requiring substantial daily forage intake. Hay, especially alfalfa, clover, and timothy varieties and plays a central role in maintaining rumen health and milk yield consistency.

As per the European Grassland Federation, dairy farms across Germany, the Netherlands, and Ireland use an average of 1.2 tons of hay per cow annually, with higher usage in regions practicing seasonal housing due to climatic constraints. For instance, over 70% of dairy farms in Western Europe incorporate hay as a core component of Total Mixed Ration (TMR) feeding systems, ensuring balanced fiber and protein intake necessary for high-yield performance. Moreover, the growing emphasis on organic dairy production, which mandates a minimum of 60% forage-based diet, has further solidified hay’s importance in this segment. In Austria and Denmark, organic dairy farms report using up to 1.5 tons of certified hay per cow annually, reinforcing the segment's dominance in both volume and value terms.

The beef cattle and sheep feed segment is experiencing the fastest growth in the Europe hay market and is likely to expand at a CAGR of 8.4% over the forecast period due to the shifting livestock management strategies and rising consumer preference for grass-fed meat. For instance, countries like Spain, Italy, and Romania are witnessing notable growth in pasture-restricted environments where hay becomes essential for year-round feeding. Sheep farming has also seen renewed interest, particularly in mountainous and marginal lands where grazing is limited. As per the European Association of Animal Production, sheep numbers in Greece, Portugal, and Bulgaria rose by 6–8% in 2023, with hay playing a crucial role in winter feeding programs. According to the European Environment Agency, climate-induced pasture shortages in Southern Europe have led to a 14% increase in hay procurement for beef and sheep operations since 2021, especially in drought-prone areas such as Andalusia and Sardinia. Additionally, the rise of grass-fed and pasture-finished beef markets in Scandinavia and Alpine regions has increased demand for premium hay that supports flavor development and marbling in meat, creating new revenue streams for hay producers. With these dynamics in play, the beef cattle and sheep feed segment is rapidly gaining traction, positioning itself as one of the most dynamic avenues for growth in the European hay market.

COUNTRY ANALYSIS

Germany dominated the hay market in Europe and accounted for 18.8% of the regional market share in 2025. The dominating position of Germany in the European market is attributed to its strong agricultural infrastructure and significant dairy and beef cattle sectors. The country’s emphasis on high-quality forage is closely linked to its advanced livestock farming systems, particularly in regions like Bavaria and Lower Saxony. According to the Federal Statistical Office of Germany (Destatis), over 4.2 million hectares of farmland are dedicated to grassland and forage crops, with hay playing a critical role in winter feeding strategies. In 2023, hay production reached 9.8 million metric tons, supporting both domestic consumption and regional exports.

For instance, over 65% of dairy farms use high-protein hay as part of their Total Mixed Ration (TMR) systems, ensuring optimal milk yield and animal health. Additionally, rising organic dairy production has increased demand for certified organic hay, with premiums of up to 30% incentivizing more farmers to shift toward sustainable hay cultivation. With climate-induced pasture shortages becoming more frequent, especially in southern states, Germany is increasingly relying on stored forages. This trend, combined with policy support under the Common Agricultural Policy (CAP), positions Germany as a key player in shaping the future dynamics of the European hay market.

France is a promising player in the European hay market. The growth of France in the regional market is driven by its expansive livestock industry and strategic position in intra-European hay trade. As one of the continent's largest agricultural producers, France plays a dual role as both a major consumer and exporter of high-quality hay, particularly to neighboring countries like Belgium and Switzerland. As per data from Agreste, the French Ministry of Agriculture, approximately 3.7 million hectares are allocated to permanent grasslands, with annual hay production exceeding 8 million metric tons in 2023. Regions such as Auvergne-Rhône-Alpes and Brittany are especially prominent in hay production due to concentrated dairy operations.

Spain is anticipated to witness a notable CAGR in the European market over the forecast period due to the growing reliance on stored forages due to increasing climate pressures and reduced natural grazing capacity. As temperatures rise and droughts become more frequent, Spanish livestock farmers are turning to hay as a reliable alternative to sustain dairy, beef, and sheep operations. According to the Spanish Ministry of Agriculture, Fisheries, and Food, pasture productivity declined by nearly 25% in Andalusia and Castilla-La Mancha in 2023, directly boosting hay procurement. In response, hay imports from France and Germany rose by 18%, while domestic production also saw an uptick, reaching over 3.2 million metric tons annually.

COMPETITIVE LANDSCAPE

The Europe hay market is characterized by a fragmented competitive landscape, with a mix of large agricultural machinery manufacturers, regional hay producers, and independent feed suppliers vying for market share. Unlike consolidated agrochemical or seed markets, the hay industry remains largely decentralized, with competition emerging at multiple levels—from production and processing to distribution and end-user engagement.

At the machinery level, companies like DeLaval, Kverneland, and AGCO compete by introducing high-efficiency haymaking equipment that improves drying times, reduces leaf loss, and ensures optimal baling. These firms often collaborate with agricultural cooperatives and research institutions to tailor equipment for diverse climatic zones across Europe.

On the product side, hay producers face competition based on quality, consistency, and traceability, particularly in the organic and specialty livestock feed markets. Countries like Germany, France, and the Netherlands are seeing increasing differentiation through certifications, moisture control technologies, and nutrient profiling, which appeal to discerning dairy and equine consumers.

Additionally, climate-induced supply volatility and fluctuating input costs are intensifying pressure on smaller producers, prompting strategic mergers, vertical integration, and digital inventory tracking systems among larger players. As the demand for sustainable, high-nutrient forages rises, competition is expected to evolve beyond price and volume, focusing increasingly on value addition, carbon footprint reduction, and targeted marketing to niche livestock sectors.

KEY MARKET PLAYERS

These are the market players that are dominating the European hay market.

- Anderson Hay & Grain

- Kverneland Group (Norway)

- AGCO Corporation (U.S., with strong presence in Europe)

- DeLaval (Sweden)

- Border Valley

- Knight Ag Sourcing

- Hay USA

- Bailey Farms

- Hayday Farm

- Barr-Ag

- Standlee

- Legal Alfalfa Products Ltd

- M&C Hay

Top Players In The Market

- DeLaval plays a significant role in the European hay market through its extensive range of harvesting and feeding equipment that supports efficient hay production and utilization. While primarily known as an agricultural machinery provider, DeLaval contributes to the hay value chain by enabling high-quality forage harvesting and automated feeding systems used in modern dairy farms across Scandinavia and Western Europe. The company's innovations in robotic feeding solutions have improved how hay is integrated into precision livestock management, enhancing feed efficiency and animal health outcomes.

- Kverneland is a leading manufacturer of agricultural implements, including specialized haymaking equipment such as tedders, rakes, and balers. Its contribution to the European hay market lies in offering advanced machinery that improves drying efficiency, bale density, and overall forage quality. By providing durable and adaptable equipment tailored for small to large-scale hay producers, Kverneland supports both traditional and organic farming practices across countries like Germany, France, and Poland. Their integration with precision farming tools further enhances hay production efficiency, making them a key enabler in the sector.

- AGCO, through its European brands such as Fendt and Massey Ferguson, supplies critical haymaking machinery that powers commercial hay production across Europe. The company’s contribution includes developing high-performance balers, mowers, and conditioners suited for varying climatic conditions and farm sizes. AGCO also collaborates with local cooperatives and agritech firms to enhance hay storage and handling logistics, ensuring consistent supply chains. With a focus on sustainability and smart farming technologies, AGCO strengthens the competitiveness of European hay producers in global markets.

Top Strategies Used By Key Market Participants

Technological Innovation in Hay Processing and Handling

Key players are investing heavily in technological advancements to improve hay harvesting efficiency, product quality, and ease of use. Companies like DeLaval and Kverneland are integrating smart sensors, GPS-guided machinery, and automated feeding systems to streamline hay production and usage. These innovations help reduce labor costs, optimize forage preservation, and ensure uniformity in feed delivery, particularly crucial for large-scale dairy operations. As per the European Agricultural Machinery Industry Association (CEMA), adoption of precision haymaking equipment has risen by 20% since 2021, reflecting industry-wide efforts to modernize the hay value chain.

Expansion of Organic and Premium-Quality Hay Offerings

With rising demand from organic dairy and grass-fed beef sectors, leading hay producers and suppliers are shifting toward certified organic hay production and premium-grade forage products. This strategy caters to niche markets in countries like Denmark, Austria, and Switzerland, where consumers prioritize natural and sustainable food sources. According to the Research Institute of Organic Agriculture (FiBL), organic hay production in Europe grew by 14% between 2021 and 2023, driven by policy incentives and premium pricing. By aligning with EU organic regulations, companies are strengthening their foothold in high-value segments of the hay market.

Strategic Partnerships and Distribution Network Expansion

To enhance market reach and logistical efficiency, major players are forming strategic alliances with local cooperatives, feed mills, and livestock associations. Companies like AGCO and regional hay exporters are expanding their distribution networks to ensure reliable year-round hay availability, especially in regions prone to seasonal shortages. For instance, France-based hay exporters have partnered with logistics providers to increase exports to North Africa and Eastern Europe, capitalizing on growing international demand. As noted by Eurostat, hay trade within the EU increased by 12% in 2023, highlighting the importance of robust distribution strategies in sustaining competitive advantage.

RECENT MARKET NEWS

- In April 2024, DeLaval launched a new line of AI-powered hay harvesting attachments designed for integration with autonomous tractors across European farms. This innovation enables real-time moisture monitoring and optimal baling conditions, improving forage quality and reducing post-harvest losses by up to 15%, according to internal field trials.

- In March 2024, Kverneland Group partnered with Lely Astronaut, a leading milking robot manufacturer, to develop synchronized feeding systems that integrate high-quality hay into automated dairy barn operations. This collaboration enhances precision feeding in robotic dairy setups, particularly in the Netherlands and Germany, where adoption of smart farming is widespread.

- In February 2024, AGCO Corporation expanded its hay equipment service network in Eastern Europe, opening three new regional support centers in Poland, Romania, and Hungary. This move supports the growing demand for durable and climate-adapted haymaking machinery amid increasing pasture shortages in the region.

- In January 2024, Claas (Germany) introduced the LEXION Bio 610 forage harvester, optimized for high-capacity hay processing in large-scale livestock operations. The machine improves fiber preservation and reduces dust content, addressing the rising demand for premium hay in organic dairy farms across Scandinavia and Austria.

- In December 2023, Raven Industries (acquired by CNH Industrial) launched a digital hay inventory management platform under its Precision Agriculture division. This tool allows farmers and cooperatives to track hay stock levels, moisture content, and nutrient profiles in real time, enhancing supply chain efficiency across Western and Central Europe.

MARKET SEGMENTATION

This research report on the Europe hay market is segmented and sub-segmented into the following categories.

By Product

- Hay Bales

- Hay Pellets

- Hay Cubes

By Type

- Dairy Cow Feed

- Beef Cattle & Sheep Feed

- Pig Feed and Poultry Feed

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the projected CAGR of the Europe Hay Market from 2024 to 2033?

The Europe hay market is expected to grow at a CAGR of 5.97% from 2024 to 2033, driven by increasing reliance on stored forages due to climate-induced pasture shortages, rising organic livestock production, and demand for high-quality equine feed across Western and Central Europe

Which country leads in hay production and consumption in Europe?

Germany accounts for over 18% of total EU hay output, making it the largest producer and consumer. As per the Federal Statistical Office of Germany (Destatis), hay production reached 9.8 million metric tons in 2023, supporting its robust dairy and beef cattle sectors.

How many hectares of farmland in Europe are dedicated to hay cultivation?

As of 2024, approximately 18 million hectares across the EU are used for grassland and forage crops, with hay being a dominant component. In countries like France and Poland, hay fields cover over 2.5 million hectares combined, according to Eurostat.

What is the average price of hay per ton in major European markets?

Hay prices vary across Europe but averaged between €150–€220 per ton in 2024, depending on quality, moisture content, and regional availability. According to the European Commission’s Agricultural Market Information System, premium alfalfa hay commands up to €270 per ton in organic dairy regions.

How has climate change impacted hay yields and quality in Europe?

According to the European Environment Agency, unpredictable spring and summer weather has caused an annual variation of 12–18% in hay yields across key producing countries. Mold contamination increased by over 20% in Northern Europe in 2023, affecting marketability and pricing.

What percentage of dairy farms in Europe use hay as a primary feed source?

Over 70% of EU dairy farms rely on hay during winter months , especially in Germany, France, and the Netherlands. The European Milk Board reports that hay forms up to 60% of Total Mixed Ration (TMR) diets for high-yield dairy cows.

Which type of hay is most preferred for sheep and beef cattle in Southern Europe?

In Spain, Italy, and Greece, alfalfa hay dominates usage , particularly in beef and dairy sheep operations. As per the Spanish Ministry of Agriculture, alfalfa-based hay accounts for over 55% of forage imports and domestic use in these regions due to its high protein and fiber content.

How much has the equine hay market grown in Europe since 2021?

The equine hay segment grew by over 14% since 2021 , with premium dust-extracted and vacuum-packed hay sales rising sharply in Germany, Sweden, and the UK , catering to performance stables and equestrian centers. According to the European Equestrian Federation , this trend is expected to continue due to improved awareness of respiratory health in horses.

How much hay is traded within Europe annually?

As reported by Eurostat, intra-EU hay trade reached nearly 4.2 million metric tons in 2023, with Germany, France, and Poland leading both exports and imports. Trade volumes have increased due to regional imbalances in supply and demand, especially in areas affected by droughts or land-use changes

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com