Europe Heavy Construction Equipment Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By End-User, Application, Power Source, Equipment, And By Region (U.K France, Germany, Spain, Italy, Sweden, Russia and Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

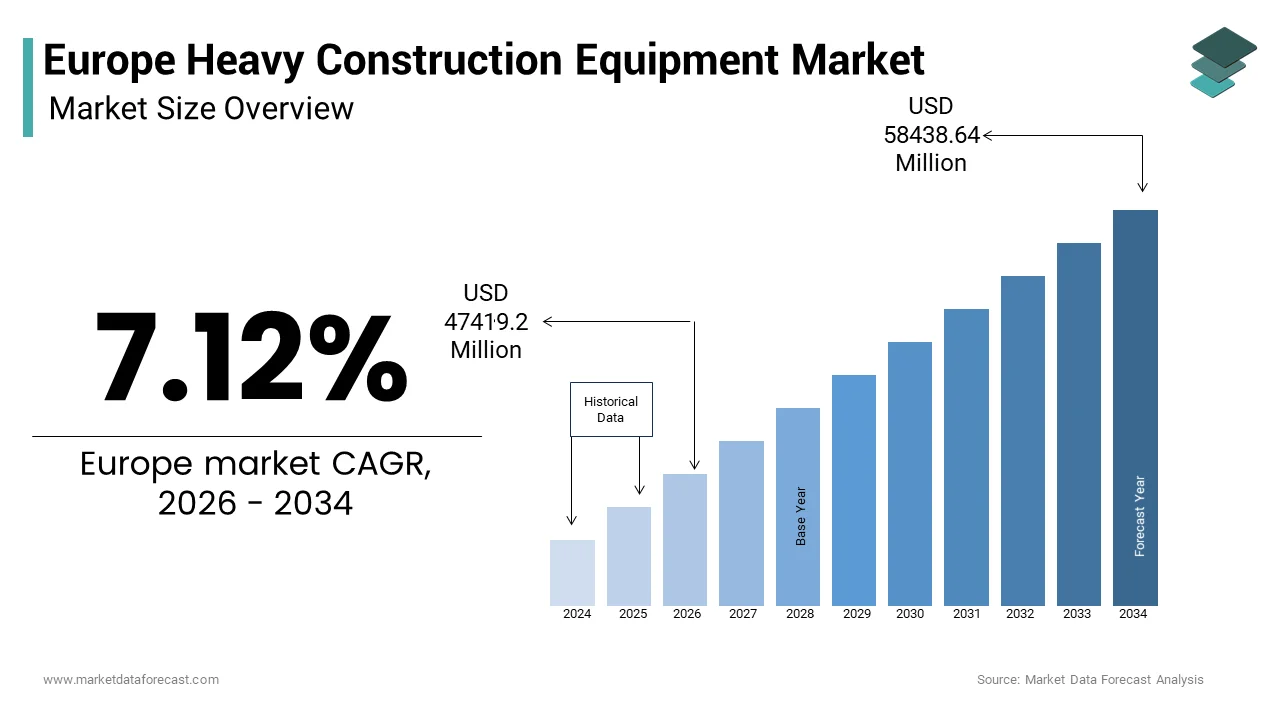

Market Size, 2025

$46024 MnMarket Estimate, 2026

$47419 MnMarket Forecast, 2034

$58438 MnCAGR, 2026–2034

7.12%Europe Heavy Construction Equipment Market Size

The European heavy construction equipment market size was valued at USD 46024.65 million in 2025 and is anticipated to reach USD 47419.2 million in 2026 and USD 58438.64 million by 2034, growing at a CAGR of 7.12% during the forecast period from 2026 to 2034.

Current Introduction of the European Heavy Construction Equipment Market

Heavy construction equipment refers to heavy-duty vehicles and large-scale machinery specifically designed to execute demanding tasks on construction sites that exceed human capacity. This market serves as a critical enabler of physical capital formation across the European Union, where infrastructure modernization intersects with stringent environmental mandates. As per sources, a significant portion of the European Union's road network requires rehabilitation or expansion to meet modern safety and mobility standards. Furthermore, many urban wastewater treatment plants across the European Union require upgrades and modernization to manage new pollutants and comply with updated, stricter environmental regulations. The European Commission’s Renovation Wave Strategy targets the retrofitting of millions of buildings by 2030, a policy directive that inherently necessitates the sustained deployment of heavy machinery. These structural imperatives position the heavy construction equipment segment not merely as a commercial domain but as an instrumental pillar in executing Europe’s decarbonization and resilience agendas.

MARKET DRIVERS

Accelerated Public Infrastructure Investment Under the EU Green Deal

Public sector capital expenditure driven by the European Green Deal constitutes a primary growth enabler for the European heavy construction equipment market. Large-scale European funding initiatives are prioritizing substantial investment into infrastructure projects focused on climate objectives, such as renewable energy integration and sustainable transport. A significant portion of these allocated funds is directed toward physical construction activities, which creates a high demand for heavy machinery and traditional building resources. Major European nations are aligning their national transportation plans with broader sustainability goals by focusing on the modernization of existing rail networks and the expansion of high-speed transit. Infrastructure strategies are emphasizing the development of multimodal logistical centers and the electrification of transit systems to promote lower-carbon mobility. These initiatives generate consistent procurement cycles for excavators, motor graders, and crawler cranes, particularly models compliant with Stage V emission standards. The alignment of fiscal policy with ecological transition thus ensures durable demand visibility for manufacturers and rental firms alike.

Urbanization and Housing Shortages Driving Civil Construction Activity

Persistent housing deficits, exacerbated by rapid urban concentration, are intensifying demand for earthmoving and material handling equipment across European metropolitan zones, further contributing to the expansion of the European heavy construction equipment market. The population living in urban areas within the European Union has shown an upward trend, resulting in greater demand for housing. The pace of new housing development has not kept up with the requirements stemming from demographic changes and migration. National governments are implementing initiatives designed to speed up the construction of housing. Specific national plans have been established to increase the supply of affordable residential units over the coming years. Targeted goals have been set by certain countries to increase the annual output of new homes. These programs necessitate extensive site preparation, foundation work, and utility trenching, directly stimulating demand for hydraulic excavators and wheeled loaders. Moreover, modern residential developments in Western Europe are increasingly adopting underground parking and deep geothermal heating systems, both of which require heavy construction machinery for deep excavation to meet space efficiency and sustainability goals. Urban densification policies in cities like Berlin and Vienna further mandate brownfield redevelopment, where demolition and soil remediation operations rely heavily on high-capacity dozers and material handlers. This convergence of demographic pressure and regulatory urban planning sustains robust equipment deployment cycles independent of cyclical economic fluctuations.

MARKET RESTRAINTS

Stringent Emission Regulations Increasing Operational Costs

The enforcement of Stage V emission standards under EU Regulation 2016/1628 imposes substantial compliance burdens on equipment owners and operators, which acts as a key restraint to theEuropeane heavy construction equipment market. These regulations mandate near elimination of particulate matter and nitrogen oxide emissions, requiring manufacturers to integrate complex exhaust aftertreatment systems such as diesel particulate filters and selective catalytic reduction units. The transition to updated, more stringent emissions standards for heavy construction machinery is associated with a notable increase in the initial acquisition cost for equipment. The implementation of more complex aftertreatment technologies requires more frequent and costly maintenance, which may increase the total cost of ownership. Small and medium-sized construction enterprises often encounter challenges in managing the capital requirements necessary for fleet updates. The overall impact of stricter environmental regulations is felt unevenly across the construction sector, creating pressure on firms with limited financial capacity to adopt newer machines. Consequently, equipment utilization rates have declined in price-sensitive segments, with some firms deferring purchases or shifting to older non-compliant models in secondary markets. This regulatory friction not only dampens near term demand but also fragments the used equipment ecosystem, complicating residual value forecasting and financing structures across the asset lifecycle.

Skilled Labor Shortages Limiting Equipment Utilization Efficiency

A chronic deficit in certified heavy equipment operators is constraining the effective deployment of advanced machinery across the region and the expansion of theEuropeane heavy construction equipment market. Consequently, this shortage is suppressing productivity gains despite technological advancements. The construction industry is experiencing a notable shortage of skilled personnel, particularly in roles involving specialized equipment operation. Training and certification rates for machinery operators are failing to keep pace with the ongoing demand for labor within the sector. A gap exists between the available workforce and the requirements for operating heavy machinery on construction sites. The demand for certified machine operators is consistently outpacing the number of new professionals entering the workforce. This scarcity forces contractors to either operate machines below optimal capacity or invest in costly training programs, neither of which scales efficiently. Compounding the issue, modern equipment embedded with telematics, automated grading, and hybrid powertrains demands higher cognitive and digital literacy, yet vocational curricula in several EU member states remain outdated. As reported by the Confederation of European Construction Industries, many contractors across Southern Europe struggle to adopt new, advanced machinery because they cannot find enough qualified operators, creating a significant labor barrier that persists even when financing for equipment is available. The mismatch between workforce capabilities and machine sophistication results in suboptimal return on investment, discouraging fleet renewal and reducing overall market velocity. Failure to align skills training with technology adoption will negate the productivity benefits of advanced machinery.

MARKET OPPORTUNITIES

Retrofitting and Electrification of Existing Fleets

The growing viability of retrofitting internal combustion engine-based heavy equipment with electric or hybrid powertrains paves the way for market participants to extend asset lifecycles while meeting sustainability mandates, which is expected to boost the growth rate of theEuropeane heavy construction equipment market. Compared to purchasing new equipment, retrofitting existing machinery and industrial infrastructure offers a cost-effective path to sustainability, significantly reducing capital expenditure while achieving similar environmental benefits and extending the operational life of assets. Companies such as Bosch Rexroth and Siemens have developed modular electrification kits compatible with major brands,s including Volvo and Caterpillar, enabling contractors to convert existing excavators and wheel loaders into zero-emission assets. European financial institutions, including the EIB, are increasingly directing funding toward decarbonization projects, supporting industrial, building, and transportation retrofits to align with net-zero targets. The Swedish government's Climate Leap initiative provides substantial subsidies for retrofitting and upgrading high-emission machinery, resulting in growing demand for green conversion technologies among industrial and construction firms. This approach not only mitigates the financial barrier of Stage V compliance but also aligns with circular economy principles promoted by the EU Circular Economy Action Plan. Retrofitting heavy machinery serves as a viable, temporary step toward decarbonization, bridging the gap while charging networks grow and battery technologies advance, avoiding the high costs and disruptions of immediate full electrification.

Expansion of Cross-Border Infrastructure Corridors Under TEN-T

The Trans European Transport Network’s revised framework was adopted in 2024, which opens new prospects for theEuropeane heavy construction equipment market. This is achieved through the mandated completion of core network corridors by 2030. The European Union is undergoing a massive infrastructure overhaul, integrating high-speed rail, inland waterways, and multimodal terminals across all member states, necessitating extensive, specialized heavy civil engineering and tunneling. The European Commission is driving a multi-hundred billion Euro initiative, heavily reliant on private and public funding, which keeps demand high for construction machinery, specifically for earthworks, tunneling, and terminal infrastructure. Notably, the Scandinavian-Mediterranean Corridor is undergoing a major transformation through mountainous regions, requiring advanced tunneling machinery and heavy-duty, articulated equipment to overcome challenging terrain and create new, high-performance rail alignments. Similarly, the North Sea Baltic Corridor’s electrification and double-tracking program demands continuous operation of piling rigs and track-laying cranes across Poland, Lithuania, and Estonia. Multiple high-priority projects within the TEN-T network are currently active across Europe, maintaining high demand for heavy machinery fleets for large-scale, cross-border construction projects simultaneously. This coordinated supranational infrastructure push creates predictable, multiyear equipment deployment windows that transcend national economic cycles, offering manufacturers and lessors stable revenue horizons and encouraging localized service hub development along corridor routes.

MARKET CHALLENGES

Supply Chain Volatility for Critical Components

Persistent disruptions in the procurement of semiconductors and specialty steel alloys are affecting production stability and delivery timelines for heavy-duty vehicles and large-scale machinery manufacturers in the region, which challenges the growth of the European heavy construction equipment market. Extended procurement times for specialized electronic components, particularly those used in industrial control systems, have shifted, often exceeding typical industry benchmarks. The cost of specific raw materials required for structural machinery components has risen significantly, driven by constraints in manufacturing energy and supply chain restrictions. Manufacturers are adjusting their distribution strategies to manage the scarcity of critical components and raw materials. The availability of machinery has been impacted, resulting in longer wait times for fulfilling customer orders. Shortages in electronic components are causing longer repair durations for equipment in the field. Unlike consumer electronics, heavy machinery cannot easily substitute components due to safety certification and load-bearing requirements, leaving little room for design flexibility. This fragility in upstream supply chains not only inflates inventory carrying costs but also erodes customer confidence in delivery reliability, potentially accelerating shifts toward local or regional equipment sourcing even at higher price points.

Fragmented Regulatory Landscapes Across Member States

Divergent national interpretations of EU-wide directives on noise limits, operator licensing, and machine homologation create operational inefficiencies that hinder cross-border equipment deployment, fleet standardization, and the expansion of theEuropeane heavy construction equipment market. The overarching European machinery regulation establishes fundamental safety requirements, yet individual nations often introduce their own supplementary mandates. Localized regulations can vary significantly, with some countries requiring specific environmental noise controls in residential areas. Certain regions may also mandate more frequent, specialized safety inspections for heavy equipment compared to others. These varied national requirements can lead to increased compliance and operational costs for companies managing projects across multiple European locations. The differences in regional standards mean that a uniform approach to machine safety and maintenance is not always sufficient for compliance throughout Europe. Moreover, operator certification reciprocity remains incomplete. AGerman-issuedd license for crane operation is not automatically recognized in Greece, necessitating redundant training and administrative processing. The European Commission’s Single Market assessments identify the construction machinery sector as heavily impacted by regulatory fragmentation, with a substantial portion of firms experiencing project delays linked to inconsistent permitting processes across member states. Such asymmetries discourage economies of scale in fleet procurement and complicate resale strategies, as residual values fluctuate significantly based on jurisdiction-specific compliance status. Fragmented regulations, pending the Single Market Enforcement Action Plan, will continue to create hidden costs that distort markets and restrict equipment mobility.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.12% |

| Segments Covered | By End-User, Application, Power Source, Equipment, and By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Caterpillar (US), Komatsu (JP), Hitachi Construction Machinery (JP), Volvo Construction Equipment (SE), JCB (GB), Doosan Infracore (KR), Liebherr (DE), CASE Construction Equipment (US), Terex Corporation (US) |

SEGMENTAL ANALYSIS

By Types Insights

The earthmoving equipment segment held the majority share of 42.1% of theEuropeane heavy construction equipment market in 2025. The supremacy of the earthmoving equipment segment is driven by the continent’s extensive civil infrastructure renewal agenda and persistent urban land development pressures. The European Commission’s Renovation Wave Strategy alone necessitates large-scale excavation, grading, and site preparation across millions of square meters of urban and peri-urban zones. Urban revitalization efforts in Germany are driving a substantial need for heavy earthmoving equipment, particularly hydraulic excavators and motor graders. The expansion of subway infrastructure in France requires a significant deployment of specialized tunnel-boring machines and associated earthmoving machinery. Agricultural modernization funding is stimulating demand for smaller and mid-sized dozer equipment, particularly within the Eastern European region. Increased public investment in infrastructure projects across Europe is directly leading to higher procurement levels for tracked and wheeled loader machinery. The versatility of earthmoving machinery across residential, commercial, and utility applications ensures its sustained leadership, particularly as municipalities prioritize brownfield remediation and flood resilience earthworks in response to climate adaptation mandates.

The material handling equipment segment is predicted to witness the highest CAGR of 5.8% between 2026 and 2034 due to the convergence of logistics infrastructure expansion and automation readiness in port and intermodal terminal operations. Increased container volume passing through European ports is encouraging terminal operators to upgrade to equipment designed for higher capacity and more efficient empty container management. The expansion of battery manufacturing facilities across the European Union is driving a need for specialized heavy-duty material handling equipment and automated vehicles to manage large components. Furthermore, the commissioning of large-scale logistics parks in Poland is generating demand for modern, high-capacity lifting equipment compliant with updated emissions regulations, while contractors are increasingly opting to lease material handling equipment to support flexible project requirements. The integration of telematics and load-sensing technologies also enhances operational efficiency, making this segment increasingly attractive for both private and public sector users seeking productivity gains without full capital commitment.

By Applications Insights

In 2025, the earthmoving segment was the largest segment in theEuropeane heavy construction equipment market by capturing a 38.1% share. The prominence of the earthmoving segment is attributed to the structural necessity of ground preparation for nearly all major construction undertakings, from highway widening to renewable energy installations. The expansion of renewable energy infrastructure involves significant land alteration, including the grading and stabilization of large areas for solar and wind installations. Urban development initiatives are increasingly incorporating substantial underground infrastructure work, requiring extensive excavation for utilities and water management systems. Landscape restoration efforts following wildfire events necessitate widespread mechanical land clearing, which drives demand for specialized earthmoving machinery. Infrastructure maintenance and safety efforts, particularly regarding slope stabilization, heavily utilize articulated earthmoving equipment to manage landslide risks. The universality of earthmoving tasks across sectors, coupled with regulatory emphasis on erosion control and topsoil preservation, ensures this application remains the backbone of equipment deployment across the region.

The lifting segment is estimated to register the fastest CAGR of 6.2% during the forecast period, due to the vertical densification of urban centers and the proliferation of modular construction techniques. Cities like Vienna and Copenhagen now mandate that all new residential buildings above eight stories incorporate prefabricated structural elements, requiring mobile and tower cranes with precision lifting capabilities. The increasing adoption of off-site building methods across Europe has driven substantial growth in the modular sector, resulting in longer on-site crane rental durations to accommodate the assembly of prefabricated components. Additionally, offshore wind farm installation has emerged as a critical driver. The development of offshore wind infrastructure requires specialized marine equipment capable of installing substantial turbine foundations. Moreover, the expansion of onshore electrical infrastructure necessitates the use of heavy-lift, high-capacity cranes to position critical components. The installation of large-scale infrastructure projects, both offshore and onshore, relies on specialized heavy-lifting technology and rigging systems. The placement of substantial transformers for grid substations involves the utilization of high-capacity all-terrain cranes. Safety regulations under the EU Machinery Directive also favor newer lifting equipment with anti-swing and load moment indicators, accelerating fleet turnover and technology adoption across the segment.

By End Users' Insights

The construction segment led theEuropeane heavy construction equipment market by occupying a substantial share in 2025 because of the sector’s role as the primary consumer of capital-intensive machinery for both public and private development. European initiatives are directing substantial funding toward member states to support widespread construction-related reforms, which include initiatives for educational facilities, healthcare upgrades, and digital infrastructure expansion. Regional development funds in the UK are supporting a variety of local projects that necessitate significant earthmoving and infrastructure work, such as road improvements and drainage systems. National strategic plans in Spain are focusing on enhancing social housing and rail connectivity, which contributes to continued demand for specialized equipment. A pattern is emerging where, across different European regions, large-scale funding is being channeled into infrastructure, renovation, and development projects. The sector’s cyclical yet policy-buffered nature, bolstered by long-term EU cohesion funds, ensures steady machine utilization. Moreover, the rise of design-build contracts across Western Europe has shifted risk to contractors, incentivizing ownership of versatile fleets rather than reliance on third-party rentals. This financial and operational dynamic cements the construction industry’s position as the central pillar of equipment consumption across the continent.

The mining end-user segment is anticipated to witness the fastest CAGR of 7.1% from 2026 to 2034. The rapid growth of the mining-end-user segment is propelled by the EU’s Critical Raw Materials Act, which identifies numerous minerals essential for clean tech and defense, and mandates domestic extraction of a portion of annual consumption by 2030. Mining operations are increasing nickel output through the adoption of electric haul trucks and automated drilling equipment. Significant, long-term investments are driving a transition toward fossil-free processes in iron ore production, necessitating a shift in heavy machinery fleets. European nations are reopening and supporting established sites to boost rare earth extraction capabilities. Substantial growth in projected lithium demand is driving increased exploration activities, which are accelerating the deployment of specialized, compact, and high-torque machinery to improve extraction efficiency. Unlike traditional construction, mining operations demand rugged, high-duty-cycle machines with extended service intervals, creating premium opportunities for OEMs specializing in durability and remote diagnostics. This strategic reorientation toward resource sovereignty is transforming mining from a marginal to a high-growth equipment user segment.

COMPETITIVE LANDSCAPE

The European heavy construction equipment market features intense competition among global manufacturers and regional specialists vying for technological leadership and customer loyalty. Established players differentiate through emissions-compliant product innovation, digital service ecosystems, and robust after-sales support networks. The competitive landscape is further shaped by rising demand for electric and hybrid machines, prompting accelerated R&D investments. Local content requirements and national infrastructure priorities influence procurement decisions, creating opportunities for agile suppliers. Price sensitivity among small contractors fosters growth in rental andsecond-handd equipment segments, intensifying pressure on residual value management. Regulatory harmonization efforts under the EU Machinery Regulation aim to level the playing field,d yet national implementation variances persist. New entrants from Asia face barriers related to certification service infrastructure and brand trust, st limiting near term disruption. Over, competition remainnovation-driveniven with sustainability and total cost of ownership as decisive factors.

KEY MARKET PLAYERS

A few of the market players that are in the European heavy construction equipment market

- Caterpillar (US)

- Komatsu (JP)

- Hitachi Construction Machinery (JP)

- Volvo Construction Equipment (SE)

- JCB (GB)

- Doosan Infracore (KR)

- Liebherr (DE)

- CASE Construction Equipment (US)

- Terex Corporation (US)

Top Players In The Market

- Volvo Construction Equipment maintains a strong presence in the European heavy construction equipment market through its focus on sustainable innovation and advanced electromobility solutions. The company has accelerated the deployment of its electric compact excavators and wheel loaders across urban construction sites in Germany, France, and the Netherlands. Recently, Volvo CE inaugurated a dedicated electric machine assembly line at its facility in Eskilstuna, Sweden, enhancing localized production capacity. The firm also expanded its dealer network with certified technicians trained in high voltage systems to support StageV-compliant and zero-emission fleets. Its partnership with major European rental companies ensures rapid adoption of new models aligned with EU decarbonization mandates.

- Caterpillar Inc plays a pivotal role in the European heavy construction equipment market by supplying high-tonnage machinery for mining infrastructure and energy projects. The company has reinforced its service ecosystem through digital integration, offering remote diagnostics and predictive maintenance via its Cat Connect platform. In recent years, ars Caterpillar upgraded its distribution centers in Belgium and Poland to streamline parts logistics across Central and Eastern Europe. It also launched tailored financing programs for contractors transitioning to lower-emission fleets. Collaborations with European engineering firms on large-scale rail and tunneling projects have further solidified its operational footprint and technical influence in the region.

- Liebherr Group is a key contributor to the European heavy construction equipment market, renowned for its tower cranes, mobile ccranes and earthmoving machinery engineered for precision and durability. Headquartered in Germany, the company leverages its integrated manufacturing model to ensure component quality and supply chain resilience. Liebherr recently enhanced its product portfolio with hybrid hydraulic excavators featuring intelligent power management systems. It also invested in digital training simulators deployed across vocational institutes in Austria, a Switzerlan,d and France to address operator shortages. Strategic participationin EU-funded infrastructure tenders, particularly in Alpine and coastal regions,s underscores its commitment to long term regional engagement.

Top Strategies Used By The Key Market Participants

Key players in theEuropeane heavy construction equipment market prioritize electrification of product portfolios to align with stringent EU emission norms and climate objectives. They invest heavily in digitalization, integrating telematics, predictive maintenance, and fleet management software to enhance customer productivity. Strategic localization of manufacturing and service hubs reduces delivery lead times and supports circular economy initiatives. Companies actively collaborate with public authorities and contractors on pilot projects for zero-emission construction sites. Additionally, they expand rental and subscription-based business models to offer flexible asset access, especially for small and medium enterprises facing capital constraints. Workforce development through operator training programs addresses skill gaps and ensures safe, efficient machine utilization. These strategies collectively strengthen market positioning while advancing sustainability and operational resilience across the European landscape.

MARKET SEGMENTATION

This research report on theEuropeane heavy construction equipment market is segmented into the following categories.

By End-User

- Construction

- Mining

- Infrastructure

- Oil and Gas

- Utilities

By Application

- Excavation

- Material Handling

- Demolition

- Road Construction

- Site Development

By Power Source

- Internal Combustion Engine

- Electric

- Hybrid

- Hydraulic

- Pneumatic

By Equipment Type

- Excavators

- Bulldozers

- Cranes

- Loaders

- Dump Trucks

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is heavy construction equipment?

Heavy construction equipment includes large machinery such as excavators, loaders, bulldozers, and cranes used in infrastructure and building projects.

What drives the Europe heavy construction equipment market?

Growth in infrastructure development, public construction spending, and urbanization are key drivers of market expansion.

Which equipment types are most widely used in Europe?

Excavators, wheel loaders, backhoe loaders, and cranes are among the most used heavy construction machines.

How does infrastructure development impact equipment demand?

Increased road, tunnel, rail, and urban development projects boost demand for advanced construction equipment.

Are electric and hybrid construction machines gaining traction?

Yes, demand for electric and hybrid heavy equipment is rising due to emission regulations and sustainability goals.

What role does technology play in the equipment market?

Telematics, automation, GPS guidance, and remote monitoring improve machine productivity and fleet management.

Which countries lead the Europe heavy construction equipment market?

Germany, France, Italy, the UK, and Spain are among the largest markets due to high construction investment.

How do strict emissions standards affect the market?

EU emissions regulations are accelerating the shift toward cleaner, low-emission engines and electrified machinery.

What challenges does the market face?

High equipment costs, supply chain disruptions, and skilled operator shortages are key market challenges.

Are used construction machines significant in Europe?

Yes, the used equipment segment supports cost-conscious buyers and fleet upgrades.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com