Europe Hemp Seeds Market Size, Share, Trends, & Growth Forecast Report, Segmented By Form, Application, Distribution Channels, And By Country (The UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Hemp Seeds Market Size

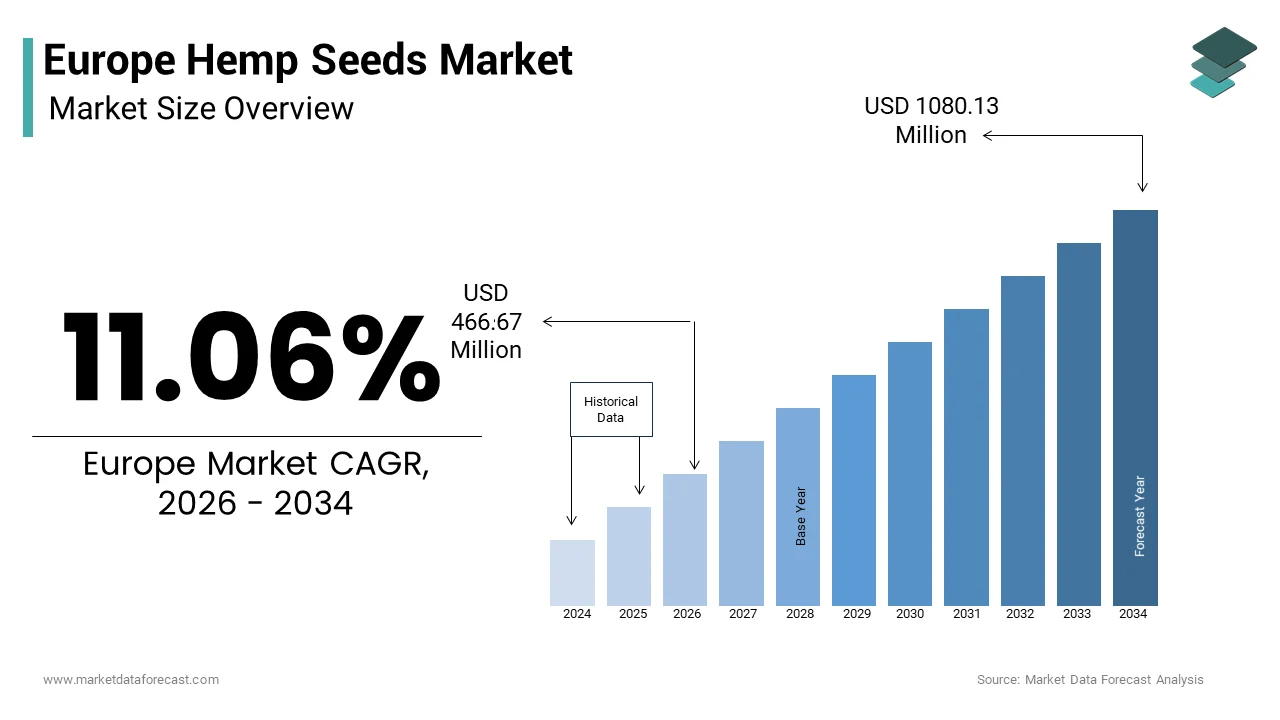

The Europe hemp seeds market was valued at USD 420.20 million in 2025 and is anticipated to reach USD 466.67 million in 2026 to reach USD 1080.13 million by 2034, growing at a CAGR of 11.06% during the forecast period from 2026 to 2034.

Hemp seeds refer to the Cannabis sativa L seeds containing less than 0.3% tetrahydrocannabinol (THC), the psychoactive compound regulated under European narcotics legislation. These seeds are prized for their dense nutritional composition, particularly their high content of complete plant protein, omega-3 and omega-6 fatty acids in an ideal 1:3 ratio, dietary fiber, and essential minerals such as magnesium and zinc. Unlike cannabis grown for medicinal or recreational use, industrial hemp is cultivated under the European Union’s Common Agricultural Policy framework, which maintains a list of approved low-THC varieties. According to the European Commission, the land dedicated to hemp cultivation in the EU expanded by 75% from 19,970 hectares in 2015 to 34,960 hectares in 2019, which shows a significant upward trend over that period. According to data from GFI Europe and the Smart Protein project, the sales volume of plant-based foods in Europe grew significantly from 2018 to 2020, with continued growth in many categories and countries into 2024, especially for private-label and specific items like plant-based cheese and barista milk..

MARKET DRIVERS

Rising Consumer Preference for Plant-Based Nutrition

European dietary behavior has increasingly pivoted toward plant-forward and functional foods, which propels the growth of the Europe hemp seeds market. This is driven by health consciousness, environmental concerns, and ethical consumption. Hemp seeds uniquely fulfill multiple nutritional criteria: they provide all nine essential amino acids, offer anti-inflammatory omega fatty acids, and are naturally gluten-free and allergen-friendly. The European Union's scientific bodies are increasingly acknowledging the health benefits of functional food ingredients, such as alpha-linolenic acid found in hemp seeds, which is likely to promote consumer confidence and product development in this area. The market for hemp seed-based food products in Western Europe is experiencing substantial and accelerating commercial growth. This confluence of nutritional science, consumer demand, and retail innovation establishes a durable and expanding demand base across mainstream grocery, sports nutrition, and premium health food channels.

Expansion of Regulatory Approval for Novel Food Applications

Regulatory evolution has been instrumental in unlocking hemp seeds’ commercial potential. This further contributes to the expansion of the Europe hemp seeds market. There is a shift towards the standardization and harmonization of hemp-derived foods within the European Union's regulatory framework, which transitions from fragmented national rules to a unified market approach. As per sources, regulatory changes are significantly streamlining market access and reducing compliance costs for hemp-based products, particularly benefiting small and medium enterprises (SMEs). This harmonization reduced compliance complexity and market entry costs for small and medium enterprises. These coordinated regulatory and scientific advancements have transformed hemp seeds from a niche supplement into a mainstream agri-food ingredient.

MARKET RESTRAINTS

Stringent and Fragmented THC Threshold Regulations

National THC limits for industrial hemp remain inconsistent, which creates legal and logistical barriers and obstructs the growth of the Europe hemp seeds market. There are significant differences in the maximum permissible THC levels for hemp across various European countries. Environmental stressors like heat or delayed harvest can cause THC levels to inadvertently exceed legal limits. The divergence in national THC regulations substantially increases compliance costs for hemp processors operating in multiple countries. Also, a notable percentage of hemp crops occasionally exceed the established THC threshold in some regions, leading to their mandatory destruction or downgrading. These uncertainties discourage long-term investment in breeding and deter farmers from scaling production, which creates a structural supply bottleneck that impedes market growth.

Lack of Standardized Cultivation Infrastructure

Its value chain in the region suffers from underdeveloped agronomic support systems that restrict the expansion of the Europe hemp seeds market. Unlike major cereals, industrial hemp lacks standardized planting protocols, certified seed distribution networks, and region-specific technical advisories. According to research, Hemp seed yields vary significantly across EU member states, indicating diverse growing conditions and agricultural practices. Also, hemp farmers predominantly rely on informal information networks rather than formal agricultural extension services.. Specialized harvesting machinery is scarce. This infrastructural deficit undermines supply reliability, discouraging food manufacturers from entering long-term sourcing agreements and constraining market scalability.

MARKET OPPORTUNITIES

Integration into Functional Food and Beverage Innovation

These seeds are increasingly leveraged in the region’s expanding functional food and beverage sector due to their multi-functional nutritional benefits, which createnew opportunities for the growth of the Europe hemp seeds market. They support cardiovascular health through arginine, promote brain function via omega-3s, and aid muscle recovery with high-quality protein. According to sources, there is a significant and growing consumer demand in Europe for plant-based protein beverages, with hemp emerging as a popular ingredient in new product development. Brands have capitalized on this trend by launching hemp-based meal replacements and protein bars targeting urban wellness consumers. These high-value, anience-backed uses illustrate a clear pathway for premiumization and category diversification.

Circular Economy Applications in Agri-Food Byproduct Valorization

The residual biomass from hemp seed processing offers potential within Europe’s circular bioeconomy that drives the expansion of the Europe hemp seeds market. Post-oil extraction meal contains protein and can replace imported soy in animal feed. Apart from these, seed hulls, rich in antioxidants and lignin, are being developed into biodegradable food packaging. Companies such as HempFlax and Bcomp are already producing food service trays and takeaway containers from seed byproducts. This dual-revenue model enhances farm economics, supports corporate ESG goals, and aligns with the EU’s Circular Economy Action Plan by creating a sustainable growth vector beyond human consumption.

MARKET CHALLENGES

Climate Vulnerability and Agronomic Instability

Industrial hemp’s sensitivity to climatic shifts poses a threat to yield stability and regulatory compliance, which challenges the growth of the Europe hemp seeds market. As a photoperiod-sensitive crop, hemp requires specific temperature and daylight conditions during flowering to maintain THC below legal limits. Higher temperatures during the flowering stage were generally associated with increased THC concentrations in hemp cultivars. Unlike major crops, hemp lacks publicly funded breeding programs for climate resilience. Drought conditions led to a general reduction in hemp seed yields, particularly in Southern European regions. Failure to quickly develop heat-tolerant or fast-maturing crop varieties will escalate production risks, restrict the areas where these crops can be grown, and discourage investment.

Limited Consumer Awareness Beyond Niche Health Circles

These seeds remain poorly understood by the broader European public, which holds back the expansion of the Europe hemp seeds market. There is a trend of widespread consumer confusion between hemp seeds and marijuana, with many consumers expressing concern about potential psychoactive effects. Misconceptions are especially prevalent in Eastern and Southern Europe. Many consumers incorrectly believe that consuming hemp seeds could result in a positive drug test. Hemp seed products generally have a lower repeat purchase rate compared to other seeds like chia or flax. Mainstream retailers often place hemp products in specialty aisles, reducing visibility. Mass consumer penetration and price competitiveness will remain out of reach if the market does not implement coordinated public education, clear labeling, and inclusion in national nutrition policies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 11.06% |

| Segments Covered | By Form, Application, Distribution Channel, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, RussSwedenden |

| Market Leaders Profiled | Navitas NaturalEuropeannpen Hemp and Grain co., Harvest Hemp Foods, Hemp Oil Canada, Green source organics, CHII Naturally Pure Hemp, Kenny delights, Man,itoba and GFR Ingredients Inc. |

SEGMENT ANALYSIS

By Form Insights

The shelled hemp seeds segment dominated the Europe hemp seeds market and accounted for a 42.5% share in 2024. Factors such as their palatable texture,, improved digestibilit,,y and immediate usability in everyday cooking without additional processing have mainly contributed to the growth of the shelled hemp seeds segment. Unlike whole seeds,, which pass through the digestive tract largely intact,, shelled seeds offer near complete nutrient absorption. According to sources, a share of European consumers prefer ready-to-eat plant protein formats that require no preparation. Shelled seeds are increasingly incorporated into breakfast bowls,, smoothi,es and baked goods. This nutritional advant,age combined with neutral taste and visual ap,peal has made shelled hemp seeds the default format for food manufacturers and health-conscious households ,alike accelerating their market entrenchment. Shelled hemp seeds resonate deeply with Europe’s clean label movement as they require no add,itives preser,vatives or chemical processing. The preference is amplified in premium retail channels. Moreover, major food brands have standardized shelled hemp seeds iplant-basednt based snack and breakfast lines, further embedding the format in mainstream consumption. This synergy between regulatory suppor,t retail strate,gy and consumer behavior solidifies shelled hemp seeds as the cornerstone of the European market.

The hemp seed protein segment is likely to experience the fastest CAGR of 18.7% between 2025 and 2033 due to its adoption in sports recovery and medical nutrit,ion whallergen-freefree and sustainable protein sources are increasingly mandated. Unlike whey or soy, hemp protein is naturally free from dairy, gluten, and common allergen,s making it compliant with EU allergen labeling regulations. Hospitals have begun trialing hemp protein in malnutrition protocols for elderly patients. This expansion intevidence-baseded health applications provides a high-margin growth vector distinct from commodity seed formats. Recent advances in dry and wet fractionation have significantly improved the solubility and emulsification properties of hemp protein isolates, addressing previous formulation challenges. The innovations have attracted formulation interest from multinational food corporations. The segment's integration into mass market and therapeutic applications will accelerate as its functional performance reaches parity with conventional proteins.

By Application Insights

The hemp segment led the Europe hemp seeds market and held a substantial share in 2024. The prominence of the hemp segment is attributed to its broad interpretation as a standalone ingredient category. Hemp refers to direct culinary and supplemental use of seeds or derivatives in raw for,m such as sprinkling on sala,ds blending into smooth,ies or consuming as snacks. This segment also dominates because it encompasses both home use and food service applications without requiring complex processing. Many consumers perceive whole or shelled seeds as more “natural” than juices or ,,teas which are viewed as processed. This perception aligns with the EU’s Farm to Fork Strategy emphasis on minimal processing. The simplicity ,of use l,ow cost and immediate nutritional payoff make “hemp” the default entry point for new c,onsumers establishing its enduring market leadership. The normalization of hemp seeds in daily diets has been accelerated by widespread culinary promotion across media and retail. Major supermarket chains have in-store in store cooking demonstrations featuring hemp seeds. Apart from these, culinary schools have incorporated hemp into plant-based curriculum modules. This grassroots culinary integration transforms hemp from a specialty item into a pantry staple, reducing reliance on beverage formats that require cold chain logistics and preservatives. The result is aself-sustainingg cycle of trial repetition and habitual use that cements the “hemp” application as the market’s backbone.

The hemp seed-based juice segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 22.3% from 2025 to 2033, owing to the urban shift towardon-the-goo functional beverages that deliver nutrition without preparation. Hemp seed juice typically blends cold-pressed oil or protein with fruits and greens, offering a complete amino acid and omega profile in a single serve format. The convenience health premium trifecta aligns perfectly with the consumption rhythms ofhigh-incomee urban professionals, driving disproportionate growth relative to traditional applications. Advancements inlow-temperaturee juicing and aseptic bottling have resolved earlier challenges of oxidation and rancidity in hemp-based beverages. The technological progress has enabled major players like Innocent and Alpro to enter the segment with stable,clean-labell products. The fresh hemp juice market, particularly in Scandinavia, is experiencing a high-velocity growth channel as e-commerce platforms leverage both reliable technology and innovative logistics to offer subscription-based delivery models.

SEGMENTAL ANALYSIS

By Distribution Channel Insights

The retailers segment held the largest share of 25.5% of the Europe hemp seeds market in 2024. The growth of the retailers segment because to the dominance of hypermarkets and organic supermarkets in mainstreaming hemp. Traditional and organic retailers serve as the primary gateway for consumer trial and repeat purchase. These channels benefit from high foot traffic, trusted brand association,s anin-storere nutrition labeling that demystifies hemp for average shoppers. The scale of these retailers enables volume purchasing, which lowers consumer prices compared to online or specialty outlets. Moreover, EU shelf space regulations favor locally sourced plant proteins. This regulatory and logistical advantage ensures that retailers remain the central artery of market distribution despite digital disruption. Retailers have aggressively leveraged private label development to capture margin and control supply. Chains offer store brand shelled seeds ata lower cost than national brands, stimulating trial amongprice-sensitivee segments. Seasonal promotions during health awareness months, such as January and Septembe,r further spike sales. Additionally, retailers collaborate with national nutrition bodies tco-brandnd educational campaigns. This blend of affordability, accessibilit,y and trust makes physical retail the enduring foundation of market penetration.

The online distribution segment is expected to exhibit a noteworthy CAGR of 26.4% from 2025 to 2033. The rapid expansion of the online distribution segment is fuelled by the proliferation osubscription-baseded DTC platforms that specialize in organic and functional foods. Companies offer monthly deliveries of hemp seed protein oil and blends with customization based on dietary goals. These platforms integrate nutrition tracking apps and personalized wellness plans, creating sticky customer relationships. The absence of retailer margin pressure allows for higher product quality and traceability messagin,g which appeals to health literate consumers. This model bypasses traditional gatekeepers and enables niche players to achieve national reach without physical shelf space. The EU’s Digital Single Market strategy has significantly reducecross-borderer friction for specialty food e-commerce. Platforms offer pan-European hemp seed delivery with unified logistics and VAT handling. Additionally, real-time inventory and dynamic pricing algorithms optimize stock turnover, reducing waste and enabling competitive pricing. These structural digital enablers transform online from a supplementary channel into a primary growth engin,e particularly fovalue-addeded and specialized formats.

COUNTRY LEVEL ANALYSIS

France Hemp Seeds Market Analysis

France outperformed other regions in the Europe hemp seeds market and accounted for a 24.6% share in 2024. The domination of the French market is driven by its long-standing position as the continent’s top industrial hemp producer. The country cultivated over substantial hectares of hemp, making it responsible for nearly half of the EU’s total acreage. This agricultural dominance ensures a stable andcost-effectivee raw material supply that supports both domestic processing and export. French regulations have been uniquely supportive. Consumer adoption is further accelerated by the “Programme National Nutrition Santé”. Retail penetration is extensive, with over 90 percent of Carrefour and Monoprix stores carrying multiple hemp seed formats. The convergence of policy agronomy and industrial infrastructure solidifies France’s leadership and creates aself-reinforcingg ecosystem that attracts R and D investment and value chain consolidation.

Germany Hemp Seeds Market Analysis

Germany followed closely in the Europe hemp seeds market by capturing a 19.4% share in 2024, with its robust health food culture and advanced processing capabilities. The country is a significant manufacturing and innovation hub within Europe for products derived from the crop. German facilities are major producers, accounting for a majority share of Europe's hemp seed protein isolates. Consumer demand for plant-based protein sources is high, with a significant percentage of households making purchases. Furthermore, Germany’s strong e-commerce logistics network facilitates efficient DTC distribution, particularly for premium organic products. The integration of hemp into national nutrition discours,e supported by university research from institutions like the University of Hohenhe,im ensures continued demand growth across both retail and clinical applications.

United Kingdom Hemp Seeds Market Analysis

The United Kingdom maintains a notable share of the Europe hemp seeds market due to its progressive regulatory stance and vibrant health and wellness sector. The rise of premium grocery chains has creathigh-visibilityity channels. Additionally, the UK’s strong sports nutrition industry has embraced hemp protein, with brands like Form Nutrition and Vivo Life achieving significant export success. Urban centers like London and Manchester show particularly high per capita consumption fueled by fitness culture and sustainability values. This combination of regulatory clarit,y retail sophisticati,on and consumer literacy sustains the UK’s position ashigh-valuelue market despite modest domestic cultivation.

Italy Hemp Seeds Market Analysis

Italy expanded steadily in the Europe hemp seeds market, with growth fueled by culinary tradition and agricultural diversification. Historically, a major cereal and olive oil produce,r Italian farmers have increasingly turned to hemp as a rotational crop to combat soil depletion and meet EU green subsidy criteria. Hemp cultivation in Italy is expanding significantly. Italian consumers show a strong preference for domestically sourced hemp products and are willing to pay a premium for them. Hemp ingredients are increasingly well-integrated into mainstream Italian cuisine and products, achieving national distribution. The synergy between agrarian poli,cy gastronomic herit,age and beauty innovation creates a uniquely Italian adoption model that emphasizes terroir and craftsman,ship driving sustained market expansion.

Netherlands Hemp Seeds Market Analysis

The Netherlands is likely to grow in the Europe hemp seeds market from 2025 to, 2033 owing to its role as a logistics and innovation nexus rather tlarge-scale scale producer. The country’s influence is also due to its port infrastructure, food technology cluster,s and progressive food policies. Rotterdam serves as Europe’s primary entry point for organic raw materials. The Netherlands is also home to Wageningen Universi,ty which leaEU-fundedded research on hemp protein functionality and lipid stability. Consumer adoption is advanced. Retailers have pioneered in-store hemp seed grinding stations and recipe integration. This ecosystem of trade,, science poli,cy and consumer readiness positions the Netherlands as a strategic amplifier for the broader European market despite its modest domestic acreage.

COMPETITIVE LANDSCAPE

The Europe hemp seeds market features a moderately fragmented competitive landscape with a mix of specialized agri process,,ors multinational wellness b,rands and regional cooperatives. Competition centers on product differentiation through nutritional ef,ficacy sustainability story,telling and supply chain transparency rather than price alone. Leading players distinguish themselves via vertically integrated op,erations certified organ,ic status and compliance with evolving Novel Food and THC regulations across diverse national jurisdictions. Innovation in application formats such as protei,n isolates beverag,e emulsions and functional snacks drives category expansion beyond bulk seeds. Barriers to entry remain moderate due to agronomic complexity and regulato,ry ambiguity but scale advantages in processing and distribution favor established actors. Collaboration with research institutions and participation in EU policy dialogues further consolidate competitive positioning as the market transitions from niche to mainstream.

KEY MARKET PLAYERS

A few of the market players in the European hemp seed market include

- Navitas Naturals

- Canah International

- Manitoba Harvest Europe

- Europen Hemp

- Hempro International

- Grain Co.

- Harvest Hemp Foods

- Hemp Oil Canada

- Green source organics

- CHII Naturally Pure Hemp

- Kenny delights

- Manitoba

- GFR Ingredients Inc.

Top Players In The Market

- Canah International is a leading European hemp processor specializing in certified organic hecold-pressed cold pressed oils headquartered in Germany. The company operates one of the largest vertically integrated supply chains in the region, sourcing raw material from numerous contracted farms across Central Europe. The company actively participates inEU-fundedd research consortia focused on sustainable protein diversification and supplies ingredients to major plant-based dairy and sports nutrition brands across many countries. Its commitment to traceability, blockchain documentatio,n anallergen-freeee manufacturing has positioned it as a preferred B2B partner in premium food applications.

- Manitoba Harvest Europe, a subsidiary of the North American pioneer in hemp food,s has established a strong foothold in Western Europe through strategic distribution partnerships and localized product development. Operating a dedicateEU-compliantnt processing hub in the Netherlands ensures full adherence to Novel Food regulations and THC limits. Manitoba Harvest Europe collaborates with retailers like Carrefour and Edeka on private label initiatives and funds consumer education campaigns on plant protein benefits through partnerships with national nutrition councils. Its parent company’s global scale enables cost-efficient logistics, while its European arm drives regional relevance through culinary innovation and sustainability storytelling.

- Hempro Internationa,l based in the Czech Republ,ic is a key innovator in hemp seed byproduct valorization and circular economy integration. The company processes over 5000 metric tons of hemp seeds annua,lly converting hulls into biodegradable food packaging and meal into animal feed supplements. It also partners with Scandinavian functional beverage brands to supply stabilized hemp seed emulsions ready-to-drinkrink formats. Its dual focus on human nutrition and agri-circularity strengthens its influence across multiple value chains in the European bioeconomy.

Top Strategies Used By The Key Market Participants

Key players in the Europe hemp seeds market prioritize vertical integration to secure raw material quality and ensure regulatory compliance across fragmented national THC frameworks. They invest heavily in novel food-compliant product innovation, focusing on protein isolates andready-to-consumee formats aligned with clean label trends. Strategic partnerships with major retailers and private label manufacturers accelerate mainstream distribution while reducing reliance on niche health channels. Companies also engage in EU-funded research initiatives to validate nutritional claims and develop climate-resilient cultivars. Sustainability credentials are leveraged through carbon-neutral certifications, lifecycle assessment,s and circular byproduct utilizati,on enhancing brand equity among environmentally conscious consumers and B2B clients.

MARKET SEGMENTATION

This research report on the European hemp seed market has been segmented and sub-segmented into the following categories.

By Form

- Whole hemp seed

- Shelled hemp seed

- Hemp seed protein

- Hemp seed oil

By Application

- Tea

- Hemp

- Juice

By Distribution Channel

- Retailers

- Online

- Convenience stores

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

Frequently Asked Questions

What is driving growth in the Europe Hemp Seeds Market?

The Europe Hemp Seeds Market is expanding due to rising demand for plant-based protein, EU approval of hemp seeds as a novel food (2023), and strong uptake in health foods, pet nutrition, and sustainable cosmetics.

Are hemp seeds legal across all EU countries?

Yes—whole and hulled (Cannabis sativa L., <0.3% THC) seeds are permitted for food use under EU Novel Food Regulation (EU) 2023/1667—but national nuances (e.g., labeling, import checks) still create compliance complexity in the Europe Hemp Seeds Market.

Which applications dominate the Europe Hemp Seeds Market?

Human food (protein powders, snacks, bakery inclusions) leads, followed by pet food (omega-3 enrichment) and cosmetics (cold-pressed oil in skincare)—with emerging interest in aquaculture and poultry feed in the Europe Hemp Seeds Market.

How is the Common Agricultural Policy (CAP) supporting hemp cultivation?

CAP eco-schemes now include industrial hemp as a soil-regenerative break crop—encouraging farmers in France, Romania, and the Baltics to diversify, directly boosting raw material supply in the Europe Hemp Seeds Market.

Are organic hemp seeds gaining premium positioning?

Yes—certified organic hemp seeds command 25–40% price premiums, especially in DACH and Nordics, where consumers link “hemp” with natural wellness and sustainability in the Europe Hemp Seeds Market.

What are the main processing challenges in the Europe Hemp Seeds Market?

Dehulling without rancidity (due to high PUFA content), THC cross-contamination risk during harvest/transport, and lack of large-scale EU processing capacity remain key bottlenecks in the Europe Hemp Seeds Market.

Which countries lead production and innovation?

France is the largest grower (≈50% of EU acreage), while the Netherlands, Germany, and Italy lead in value-added processing (protein isolation, encapsulated oils) and branded B2B ingredient supply in the Europe Hemp Seeds Market.

How are food safety authorities regulating THC limits?

EFSA mandates strict batch testing: total THC (THC + THCA) must be ≤1 mg/kg in finished foods—pushing processors toward certified low-THC cultivars (e.g., Fedora 17, Santhica 27) in the Europe Hemp Seeds Market.

Is there competition from non-EU hemp seed imports?

Yes—Canadian and Ukrainian seeds still dominate high-volume B2B supply due to scale and lower cost, but “EU-grown” claims are gaining traction with retailers prioritizing traceability and carbon footprint in the Europe Hemp Seeds Market.

What’s the outlook for the Europe Hemp Seeds Market through 2030?

Strong growth (CAGR ~12–15%) is expected, driven by protein diversification trends, pet food reformulation, and circular bioeconomy initiatives—though success hinges on harmonizing national rules and scaling processing infrastructure in the Europe Hemp Seeds Market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com