Europe Herbicides Market Share, Size, Growth, Trends, And Forecast Report, Segmented By Type (Synthetic (Glyphosate, 2, 4-D, Diquat, Others), Bioherbicides), Crop Type (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables, Others), Mode Of Action (Non-selective, Selective), And By Country (U.K France, Germany, Spain, Italy, Sweden, Russia and Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis From (2025 to 2034)

Europe Herbicides Market Size

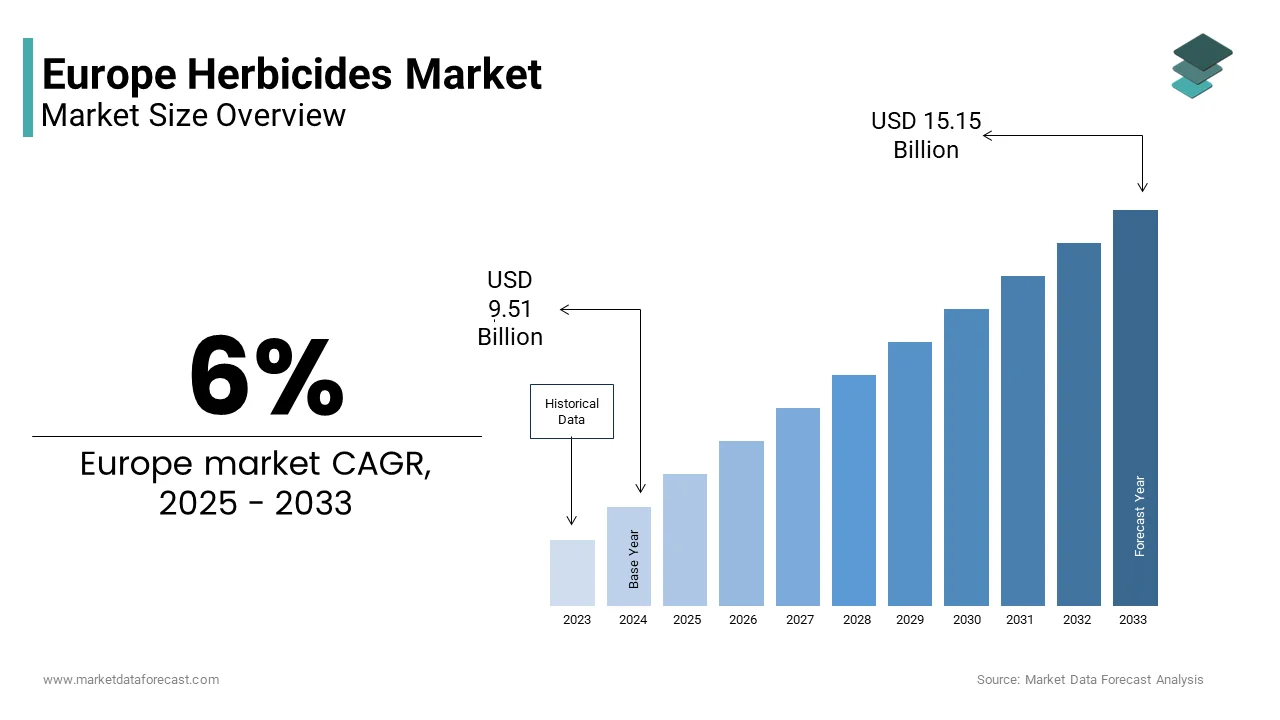

The European herbicides market was valued at USD 9.51 billion in 2025 and is projected to reach USD 10.08 billion in 2026, increasing to USD 16.07 billion by 2034, growing at a CAGR of 6% during the forecast period from 2026 to 2034.

Herbicides refer to the chemical and biological substances applied to control or eliminate unwanted vegetation in agricultural, horticultural, and non-crop settings. These products are categorised as selective or non-selective and include active ingredients such as glyphosate, glufosinate,nate pendimethalin, and emerging bio-herbicides derived from natural compounds. The market operates within a highly regulated framework shaped by the European Union’s Sustainable Use of Pesticides Directive and the Farm to Fork Strategy, which targets a reduction in chemical pesticide use by 2030. Herbicides constitute the largest segment of the global pesticide market by value, accounting for approximately 44% of total sales in recent years, according to sources. Arable land in Europe spans approximately 122 million hectares as documented by Eurostat, and significant weed pressure can reduce yields. For instance, uncontrolled weed competition can diminish wheat output by up to 30%, a figure consistent with research findings from institutions like the Julius Kühn Institute in Germany. Concurrently, the European Union has intensified scrutiny under Regulation (EC) No 1107/2009, which has led to a reduction in approved active substances over time. The total number of all approved active substances for plant protection products is around 400-500. This tension between agronomic necessity and environmental policy defines the complex operating environment for herbicide innovation and deployment across the continent.

MARKET DRIVERS

Persistent Weed Pressure Threatens Crop Yields and Food Security

Persistent weed pressure threatens crop yields and food security, which boosts the growth of the Europe herbicides market. Weeds remain the most economically damaging biotic stressor in European agriculture, with infestations reducing cereal yields depending on species and density, as per research. Climate change exacerbates the problem with warmer autumns, enabling earlier weed germination and extended growing seasons for invasive species. The EU is actively working to maintain a high level of self-sufficiency for essential crops like cereals. Farmers, therefore, continue to rely on herbicides as a core component of integrated weed management despite regulatory headwinds, ensuring consistent baseline demand across major crop systems.

Adoption of Herbicide Tolerant Crops in Limited but Strategic Crops

Herbicide-tolerant varieties of non-GM crops developed through mutagenesis or gene editing are gaining regulatory acceptance, which further contributes to the expansion of the Europe herbicides market. These systems allow precise application of specific herbicides, such as imazamox, reducing overall chemical load while improving efficacy. Moreover, herbicide-tolerant sugar beet varieties are under advanced field testing in Germany and France to combat cleavers and volunteer potatoes. This technological shift enables more efficient herbicide use, aligning with precision agriculture goals and providing a controlled pathway for chemical weed management within the EU’s sustainability framework.

MARKET RESTRAINTS

Progressive Bans on Key Active Ingredients Under EU Regulatory Policy

The EU implemented a stringent re-evaluation process under Regulation EC 1107/2009, which restricts the growth of the Europe herbicides market. This has led to the non-renewal of numerous herbicide active substances deemed to pose unacceptable risks to human health or the environment. The approval for glyphosate was extended, but only for a limited period, following considerable scientific and political discussion. In contrast, other chemical substances faced different regulatory decisions. For instance, the approvals for bromoxynil and aclonifen were not renewed. These varying outcomes indicate a trend where the European Commission is making substance-specific decisions regarding pesticide approvals, with some substances facing non-renewal while others receive only temporary extensions. Each withdrawal forces farmers to adopt alternatives that may be less effective, more expensive, or require multiple applications. These regulatory attritions fragment the herbicide toolbox and increase production risk, particularly for specialty crops with narrow weed control windows. The cumulative effect is a shrinking portfolio of reliable options constraining agronomic flexibility and elevating input uncertainty.

Stringent Buffer Zone and Application Restrictions Limit Field Usability

National authorities in the region have imposed increasingly restrictive use conditions on approved herbicides to protect biodiversity and water quality, which ultimately obstructs the expansion of the Europe herbicides market. These constraints significantly reduce practical applicability, particularly in regions with high field fragmentation, such as Southern Europe. According to studies, a portion of arable land in Belgium and Italy falls within restricted zones limiting herbicide access. Such spatial limitations force farmers toward mechanical weeding, which is costly labour labor-intensive, and less effective in wet conditions, thereby undermining the reliability of chemical weed control even when active substances remain authorised.

MARKET OPPORTUNITIES

Development and Adoption of Bio-Based and Microbial Herbicides

The EU’s Green Deal and Horizon Europe programme are accelerating investment in biological alternatives to synthetic herbicides, which is setting up new opportunities for the growth of the Europe herbicides market. In addition, the European Commission allocated funds to projects developing bio-herbicides from natural compounds such as pelargonic acid, essential oils, and soil microbes. These products benefit from faster regulatory pathways under the EU’s Biological Plant Protection Products Directive and face fewer use restrictions. Companies have launched bio-herbicide blends for organic and integrated production systems. Furthermore, the EU Organic Regulation permits most bio-herbicides, creating a dedicated market channel. Bio-herbicides represent a high-growth frontier aligned with policy and consumer trends, driven by millions of hectares of organic farmland and increasing demand for residue-free produce.

Integration of Herbicide Application with Precision Agriculture Technologies

Advancements in digital farming enable ultra-precise herbicide delivery, which reduces volume and environmental impact and thereby provides key opportunities for the Europe herbicides market. Camera-guided spot-spraying systems from companies like Ecoation and Naïo Technologies can target individual weeds with significant accuracy, reducing herbicide use. Similarly, drone-based applications are gaining traction in vineyards and orchards in Spain and Italy, where terrain limits tractor access. The European GNSS Agency promotes such innovations through the Copernicus Earth Observation programme, which provides weed mapping data to farmers. This convergence of robotics, AI, and spatial analytics transforms herbicides from blanket treatments to surgical interventions supporting the EU’s pesticide reduction targets while maintaining agronomic efficacy.

MARKET CHALLENGES

Rising Prevalence of Herbicide-Resistant Weed Populations

Continuous reliance on limited modes of action has accelerated the evolution of resistant weed biotypes in the region, which hinders the growth of the Europe herbicides market. Many different types of weeds across Europe have developed the ability to resist common chemicals designed to kill them. A significant number of these resistant species are specifically unaffected by a particular group of chemicals known as ALS inhibitors. Weeds that are no longer killed by glyphosate have been found in more than a dozen countries across the continent. This resistance renders standard herbicide programmes ineffective, forcing farmers to resort to tank mixes, increased application frequency, or mechanical control. The slow pace of new modes of action discovery exacerbates the crisis. Resistant weeds threaten to undermine the entire foundation of chemical weed management in European agriculture unless rapid innovation in chemistry or non-chemical alternatives occurs.

Fragmented National Implementation of EU Pesticide Regulations

The inconsistent interpretation and enforcement of rules by member states creates a complex compliance landscape for herbicides, even though the EU is establishing a common regulatory framework, which further hampers the expansion of the Europe herbicides market. This fragmentation forces manufacturers to maintain multiple product formulations and registration dossiers, increasing time to market by several months. Small and medium agrochemical firms struggle to navigate this patchwork, limiting their ability to innovate or compete. The lack of true harmonisation contradicts the single market principle and impedes the efficient deployment of sustainable weed control solutions across borders despite shared ecological and agronomic challenges.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6% |

| Segments Covered | By Type, Crop Type, Mode of Action, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden |

| Market Leaders Profiled | BASF SE, The Dow Chemical Company, E.I. du Pont de Nemours & Company, Monsanto Company, Syngenta AG, FMC Corporation, Platform Specialty Products Corporation, Nufarm Ltd., Nissan Chemical Industries Ltd., Drexel Chemical Co. |

SEGMENT ANALYSIS

By Type Insights

The synthetic herbicides segment held a substantial share of the Europe herbicides market in 2024, which was driven by their efficacy, cost efficiency, and deep integration into established agronomic practices. Synthetic herbicides remain the only viable solution for controlling aggressive weed complexes such as blackgrass in cereals or cleavers in oilseed rape. Despite regulatory pressure, these chemistries offer unmatched reliability in high-pressure scenarios where yield loss from uncontrolled weeds can exceed. Hence, reliance on synthetic modes of action remains agronomically indispensable, particularly in large-scale arable systems that underpin EU food security. Moreover, synthetic herbicides deliver high performance at low application rates, with glyphosate costing less per hectare compared to that for emerging bio alternatives. They are also fully compatible with standard sprayers, GPS guidance systems, and tank mix protocols that European farmers have refined over decades. This operational synergy reduces fuel, labour, and equipment wear.

The bioherbicides segment is predicted to witness the highest CAGR of 11.3% from 2025 to 2033 due to policy support and organic sector expansion. The European Commission has prioritised biological plant protection under the Farm to Fork Strategy, allocating funds through Horizon Europe to develop bio-herbicides from natural sources such as fatty acid microorganisms and plant extracts. This funding has enabled firms like Belchim and Futureco Bioscience to commercialise pelargonic acid and Phoma macrostoma-based products approved in many EU member states. These formulations benefit from streamlined authorisation under Regulation EU 2022 1, which reduces review timelines compared to synthetic actives. Furthermore, the EU Organic Regulation permits all reregistered bio-herbicidescreating immediate market access in a sector that grows annually. This policy-driven pipeline ensures sustained innovation and commercialisation. Major European food retailers, including Carrefour and Edeka, mandate reduced pesticide residues in private label supply chains, with bio-herbicides exempt from maximum residue level testing. This market complements the regulatory push, creating dual incentives for adoption. The expansion of traceability systems will accelerate the commercial advantage of bio-herbicides, thus further speeding up their integration.

By Crop Insights

The cereals and grains segment led the Europe herbicides market and captured a 48.1% share in 2024. The expansion of the cereals and grains segment is propelled by their vast acreage and high weed sensitivity. Cereals occupy millions of hectares of EU arable land, with wheat, barley, and oats forming the backbone of European food and feed systems. Weed competition during early growth stages can reduce wheat yields. Given that EU wheat production totals significant millions of metric tons annually, even minor yield losses translate into significant economic and food security impacts. Consequently, farmers invest heavily in pre-emergence residual herbicides like pendimethalin and post-emergence actives such as mesosulfuron to protect this high-value crop. National authorities grant more flexible herbicide authorisations for cereals due to their strategic importance. Similarly, glyphosate remains provisionally permitted for pre-sowing weed burndown in cereal rotations across most member states. This pragmatic regulatory approach recognises that mechanical alternatives are often impractical on large fields, particularly in wet autumns. The EU Pesticide Residue Monitoring Programme also sets higher maximum residue levels for cereals compared to fruits and vegetables, acknowledging the necessity of chemical control. This policy accommodation ensures cereals remain the primary herbicide application domain.

The fruits and vegetables segment is estimated to register the fastest CAGR of 9.7% over the forecast period, owing to labour shortages and high-value crop protection needs. The European horticultural sector faces a critical deficit of seasonal workers. Hand weeding costs in strawberry fields exceed a notable amount per hectare annually, which makes chemical alternatives essential for competitiveness. Precision herbicides applied via shielded sprayers now enable selective weed control in transplanted crops such as tomatoes and lettuce without crop damage. This operational pragmatism in high-value systems sustains herbicide demand despite stricter residue limits. The area under protected cultivation in Europe has grown annually. Greenhouses and high tunnels create microclimates that accelerate weed germination while limiting mechanical access. Additionally, the shift toward perennial fruit orchards in Southern Europe, such as blueberries and raspberries, requires long-term weed control solutions that synthetic residuals provide. These structural trends in high-value horticulture create sustained and growing herbicide demand even as field crop usage declines.

By Mode of Action Insights

The selective herbicides segment dominated the Europe herbicides market and held a significant share in 2024. The dominance of the selective herbicides segment is fuelled by their ability to target weeds without damaging crops, a critical requirement in diverse European rotations. European farms commonly rotate cereals, oilseeds, and pulses within three-to-four-year cycles, necessitating herbicides that control specific weed spectra without carryover damage. Sulfonylureas, for instance, selectively inhibit ALS enzyme in broadleaf weeds while leaving cereals unharmed. Similarly, propyzamide provides grass control in oilseed rape without affecting subsequent barley crops. National extension services provide detailed herbicide rotation charts to prevent residual injury, which supports selective product use. Selective herbicides reduce chemical load by acting only on target species, allowing beneficial plants and soil microbes to persist. The ecological advantage aligns with the EU Sustainable Use Directive, which mandates risk mitigation through product choice. Besides, selective systems enable conservation tillage by controlling specific volunteers without total vegetation kill, supporting soil health goals under the Common Agricultural Policy. These environmental co-benefits enhance their regulatory and social acceptability, making them the preferred tool in integrated weed management across the continent.

The non-selective herbicides segment is anticipated to witness the fastest CAGR of 8.9% during the forecast period. The expansion of the non-selective herbicides segment is driven by pre-sowing applications and no tillage expansion. Non-selective herbicides, particularly glyphosate, are indispensable for no-till and reduced till systems, which now cover a portion of EU arable land. These systems suppress weeds before planting without soil disturbance, preserving organic matter and moisture. The EU’s Soil Mission under Horizon Europe actively promotes such practices to combat erosion, making non-selective herbicides a de facto enabler of climate-smart agriculture. Despite political controversy, their agronomic function in soil conservation ensures continued use under controlled application windows. Imazamox, a non-selective ALS inhibitor, can be applied over the top of tolerant crops, eliminating both grasses and broadleaves in a single pass. This technological shift transforms non-selective activities from burndown tools to in-crop solutions, aligning with precision agriculture goals. The expansion of this segment beyond traditional pre-planting use will accelerate as more mutagenesis-derived tolerant crops gain approval.

COUNTRY ANALYSIS

France Herbicides Market Analysis

France was the top performer in the Europe herbicides market and accounted for a 24.6% share in 2024. The supremacy of France in the regional market is primarily driven by its vast arable base and intensive cropping systems. The country cultivates millions of hectares of cereals and oilseeds, which makes weed control economically critical. France is maintaining access to important chemical weed killers, such as glyphosate, for initial planting, even though it has a goal to significantly cut down on pesticide use. The country is rapidly increasing its use of smart, camera-guided technology for targeting weeds, with over 15,000 farms already using these precise systems. Strong research infrastructure at institutions ensures continuous herbicide efficacy monitoring, further anchoring France as the region’s agronomic and volume leader.

Germany Herbicides Market Analysis

Germany followed closely in the Europe herbicides market by capturing an 18.8% share in 2024. The growth of the German market is fuelled by its high-yielding cereal and sugar beet production. The country faces severe blackgrass and cleavers pressure with infestations affecting millions of hectares. Germany restricts the non-agricultural use of herbicides, yet it still provides emergency authorizations for critical active ingredients when used in food crops. The nation also mandates integrated weed management under the National Action Plan, which paradoxically increases herbicide use through multi-mode of action strategies to delay resistance. Germany’s dual commitment to environmental protection and agronomic realism creates a complex but stable herbicide market where innovation and regulation coexist.

Spain Herbicides Market Analysis

Spain continues to be a key player in the Europe herbicides market, with its diverse cropping zones and climate-driven weed pressure. The country leads in herbicide use for horticulture, with large hectares of fruits and vegetables requiring year-round weed control. Drought conditions make mechanical weeding impractical in autumn sowings, driving reliance on pre-emergence residuals like pendimethalin. Spain also pioneers the adoption of herbicide-tolerant sunflower varieties. Water scarcity further incentivises no till systems, which depend on glyphosate burndown across millions of hectares of arable land. This confluence of climate agronomy and innovation sustains Spain’s strategic importance in Southern Europe.

Italy Herbicides Market Analysis

Italy experienced consistent growth in the Europe herbicides market, with demand concentrated in cereal, rice, and specialty horticulture. A significant amount of Europe's rice is grown in the Po Valley region, where managing weeds requires the use of herbicides because the fields are kept underwater, making it impossible to remove weeds with machinery. Italy also cultivates hectares of durum wheat highly sensitive to weed competition. Recent approvals of imidazolinone-tolerant crops have further modernised weed control in sunflower and maize systems. Italy’s blend of traditional and high-tech farming ensures consistent herbicide demand across both conventional and evolving production models.

United Kingdom Herbicides Market Analysis

The UK is predicted to expand in the Europe herbicides market between 2025 and 2033 due to its high-intensity arable sector and post-Brexit regulatory autonomy. Large hectares of cereals face severe blackgrass pressure with a notable share of populations resistant to multiple herbicide groups. This crisis has intensified reliance on pre-emergence actives and tank mixes despite pesticide reduction targets. The UK’s departure from the EU allows faster emergency authorisations, which provide greater agronomic flexibility than many EU states. Hence, the UK remains a sophisticated and resilient herbicide market, balancing sustainability and productivity.

COMPETITIVE LANDSCAPE

The Europe herbicides Market features concentrated competition among three to four multinational agrochemical leaders, with limited room for small players due to high regulatory and R and D barriers. Bayer, Syngenta, and BASF dominate through extensive patent-protected portfolios, strong regulatory capabilities, and deep agronomic support networks. Competition is not price-based but revolves around efficacy, resistance management, environmental profile, and digital integration. The regulatory landscape under Regulation EC 1107 2009 acts as both a filter and a catalyst, favouring firms with global registration expertise and local policy engagement. While synthetic herbicides remain dominant, bio herbicides are emerging as a contested frontier with both multinationals and biotech startups vying for early mover advantage. Fragmented national implementation of EU rules creates uneven playing fields but also opportunities for country-specific strategies. Overall, the market is defined by a delicate balance between agronomic necessity, environmental responsibility, and regulatory compliance, with innovation increasingly measured in sustainability metrics rather than just weed kill performance.

KEY MARKET PLAYERS

A few of the market players in the Europe herbicides market include

- BASF SE

- The Dow Chemical Company

- Bayer AG

- E.I. du Pont de Nemours & Company

- Monsanto Company

- Syngenta AG

- FMC Corporation

- Platform Specialty Products Corporation

- Nufarm Ltd.

- Nissan Chemical Industries Ltd.

- Drexel Chemical Co.

Top Players in the Market

- Bayer AG is a pivotal player in the herbicide market through an extensive portfolio anchored by glyphosate-based solutions and selective herbicides for cereals and oilseeds. The company leverages deep agronomic expertise and a robust regulatory affairs network to navigate Europe’s complex pesticide approval landscape. It also expanded its digital farming platform Climate FieldView to integrate herbicide application recommendations based on real-time weed pressure data from satellite imagery. Furthermore, Bayer intensified collaboration with the European Crop Protection Association to advocate science-based authorization processes. These actions reinforce its commitment to integrated weed management, sustainability, and farmer support in a tightening regulatory environment.

- Syngenta Group maintains a strong presence in the herbicides market with innovative selective herbicides such as mesosulfuron and pyroxsulam tailored for resistant weed control in cereals. The company integrates chemical and biological solutions under its Good Growth Plan, promoting reduced environmental impact. It also enhanced its Operation Pollinator initiative to support biodiversity on treated fields, aligning with EU Green Deal objectives. Additionally, Syngenta partnered with agricultural cooperatives in Spain and Italy to deliver precision spraying training, reducing target drift. By combining product innovation, ecological stewa,rdshon-farmon farm educa Syngenta strengthens its relevance across conventional and sustainable farming systems.

- BASF SE plays a strategic role in the Euherbicidescides Market through its differentiated cproductsincluding imazamoherbicide-tolerant crops and residual actives like pendimethalipre-emergence control. The company invests heavily in resistance management strategies and regulatory science to sustain product availability. It also launched a digital herbicide stewardship toolkit providing farmers with resistance tracking and application best practices compliant with national action plans. Furthermore, BASF expanded its biologicals pipeline with a microbial herbicide candidate now in field trials across the Netherlands and Denmark. These initiatives position BASF at the intersection of innovation ion compliance, and sustainability in Europe’s evolving weed control landscape.

Top Strategies Used By The Key Market Participants

Key players in the Europe herbicides market pursue multifaceted strategies centred on regulatory resilience, product diversification, and digital integration. Companies invest in robust scientific dossiers to secure reauthorizations and emergency approvals for critical active substances amidst tightening EU scrutiny. They accelerate the development of bio-based low-risk herbicides to align with Farm to Fork reduction targets and access organic markets. Strategic partnerships with cooperative,,ives research institutes, and digital agronomy platforms enhance farm adoption and stewardship. Precision application technologies, including dose mapping and drift reduction zones, are promoted to minimise environmental impact and comply with national buffer zone rules. Additionally, firms advocate collectively through industry associations for harmonised regulatory interpretation across member states. These coordinated efforts ensure continued agronomic relevance while navigating the region’s complex sustainability and policy mandates.

MARKET SEGMENTATION

This research report on the Europe herbicides market is segmented and sub-segmented into the following categories.

By Type

- Synthetic

- Bioherbicides

- Glyphosate

- 2, 4-D

- Diquat

- Others

By Crop Type

- Cereals & grains

- Oilseeds & pulses

- Fruits & Vegetables

By Mode Of Action

- Non-Selectie

- Selective

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is driving change in the Europe Herbicides Market?

The Europe Herbicides Market is being reshaped by the EU’s Sustainable Use of Pesticides Regulation (SUR), national bans on glyphosate (e.g., Germany, France), and rising adoption of integrated weed management (IWM) in response to resistant biotypes.

How is the EU’s Farm to Fork Strategy impacting the Europe Herbicides Market?

With the 50% pesticide risk reduction target by 2030, the Europe Herbicides Market is shifting toward low-risk active substances (e.g., pelargonic acid, acetic acid), bioherbicides, and precision application—accelerating decline in high-risk synthetics.

Which herbicide modes of action are under regulatory pressure?

Glyphosate (renewal pending 2027), sulfonylureas (resistance + drift concerns), and chloroacetamides (e.g., S-metolachlor—under re-evaluation for groundwater risks) face heightened scrutiny in the Europe Herbicides Market.

Are bioherbicides commercially viable yet in Europe?

Still niche—but growing fast. Products based on Phoma macrostoma, mustard seed meal, or vinegar derivatives are gaining in organic horticulture and urban settings, supported by CAP eco-scheme subsidies in the Europe Herbicides Market.

How is herbicide resistance affecting farmer choices?

Over 60 resistant weed species (e.g., Alopecurus myosuroides, Papaver rhoeas) are documented—pushing growers toward tank mixes, crop rotation, and non-chemical tools (e.g., robotic weeding), reducing reliance on single-actives in the Europe Herbicides Market.

Which crops drive the most herbicide use in Europe?

Cereals (wheat, barley) dominate volume, but high-value vegetables and vineyards show the highest spend per hectare—especially where manual weeding costs are prohibitive in the Europe Herbicides Market.

Is precision spraying technology gaining traction?

Yes—AI-powered sprayers (e.g., ecoRobotix, Naïo Technologies) that target weeds at the plant level cut herbicide use by 70–90%, making them increasingly cost-effective for large farms in the Europe Herbicides Market.

How do national bans differ across the EU?

Patchwork regulation persists: Austria and Luxembourg ban glyphosate outright; Germany permits professional use only until 2024; France restricts home/garden sales—creating compliance complexity for distributors in the Europe Herbicides Market.

What role do adjuvants play in modern herbicide programs?

Critical—advanced drift-reduction and deposition-enhancing adjuvants help maintain efficacy at lower doses, supporting SUR compliance and reducing off-target movement in the Europe Herbicides Market.

What’s the outlook for the Europe Herbicides Market through 2030?

Volume will decline (~2–3% CAGR), but value will stabilize due to premium pricing for low-risk and precision-enabled solutions—making the Europe Herbicides Market increasingly innovation- and service-driven rather than volume-driven.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com