Europe Household Appliances Market Size, Share, Trends & Growth Forecast Report – Segmented By Product (Major Appliances, Small Appliances), Distribution Channe, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Market Size, 2025

$101 BnMarket Estimate, 2026

$106 BnMarket Forecast, 2034

$147 BnCAGR, 2026–2034

4.16%Europe Household Appliances Market Summary

The Europe household appliances market was valued at USD 101.89 billion in 2025, is estimated to reach USD 106.13 billion in 2026, and is projected to grow to USD 147.04 billion by 2034, registering a CAGR of 4.16% from 2026 to 2034. Market growth is driven by rising disposable incomes, increasing adoption of smart and energy-efficient appliances, and growing consumer demand for convenience-driven home technologies. The expansion of modern retail, advancements in IoT-enabled appliances, and strong replacement demand across major European economies further support market expansion. Sustainability-focused designs, reduced energy consumption, and integration of AI-based functionalities are shaping the long-term outlook of the regional household appliances market.

Key Market Trends

- Rising demand for smart and connected appliances driven by IoT integration and automation technologies.

- Growing focus on energy-efficient and eco-friendly appliances aligned with EU sustainability directives.

- Increasing consumer adoption of premium and multifunctional appliances for enhanced convenience.

- Expansion of omnichannel retail, with electronic stores and online platforms boosting appliance accessibility.

- High replacement demand for refrigerators, washing machines, and kitchen appliances across major EU economies.

Segmental Insights

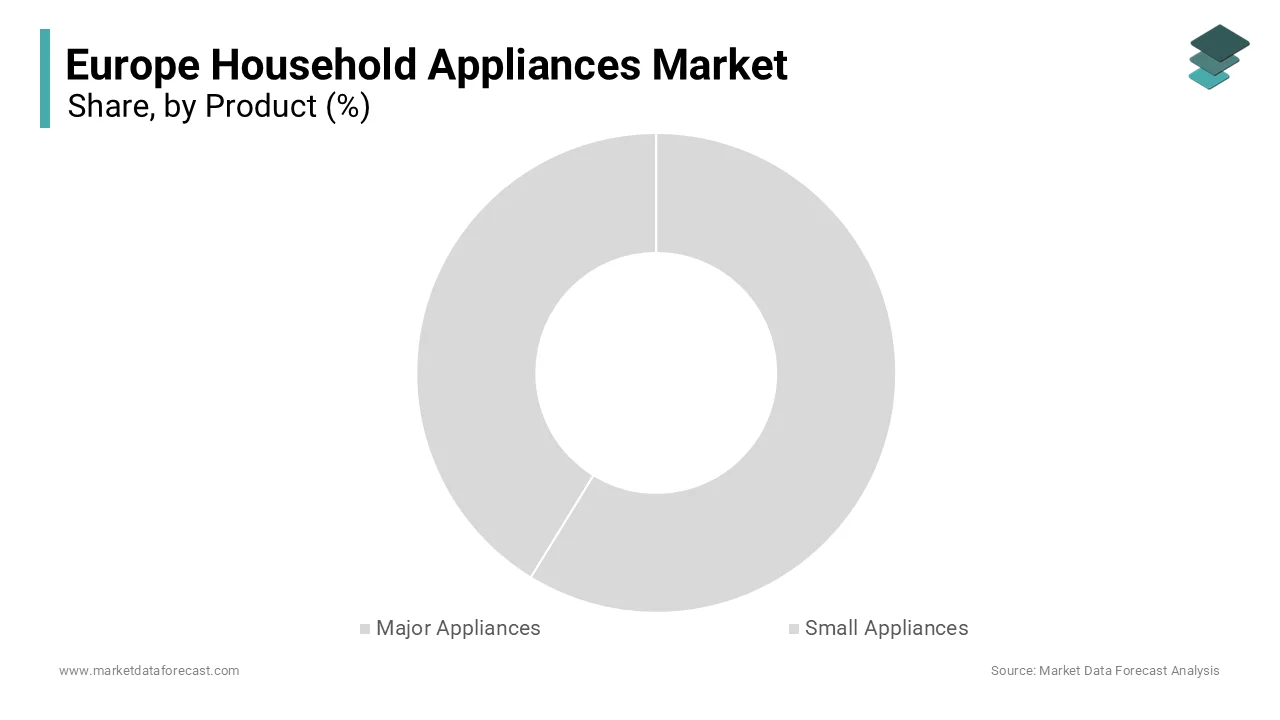

- Based on product, the major appliances segment dominated the market with 68% share in 2025, supported by strong demand for refrigerators, washing machines, and cooking appliances driven by modernization of households and replacement cycles.

- Based on distribution channel, the electronic stores segment led with 65.5% market share in 2025, reflecting consumer preference for in-store product comparison, expert guidance, and availability of bundled deals.

Regional Insights

Europe continues to experience strong household appliance adoption fueled by rising urbanization, smart home expansion, and growing consumer expectations for energy-efficient products.

- Germany led the market with 22.8% share in 2025, driven by high purchasing power, rapid adoption of premium smart appliances, and a robust manufacturing ecosystem.

- The UK, France, Italy, and Spain remain major contributors due to strong demand for advanced kitchen and cleaning appliances.

- Northern and Western Europe continue to drive growth with faster adoption of eco-certified, energy-efficient appliances supported by strict EU energy standards.

Competitive Landscape

The Europe household appliances market is highly competitive, featuring global and regional brands investing in smart technologies, sustainable designs, and product innovation. Companies are expanding their digital retail presence, integrating IoT capabilities, and enhancing energy-efficiency standards to meet evolving consumer expectations.

Prominent players in the Europe household appliances market include Whirlpool Corporation, Samsung Electronics Co. Ltd., Robert Bosch GmbH, LG Electronics Inc., Electrolux AB, Haier Smart Home Co., Ltd., Panasonic Corporation, Sharp Corporation, Miele, Midea Group, Koninklijke Philips N.V., Breville Group Limited, De'Longhi S.p.A., SEB Groupe (Groupe SEB), and Dyson Limited

Europe Household Appliances Market Size

The Europe household appliances market size was valued at USD 101.89 billion in 2025 and is projected to reach USD 147.04 billion by 2034 from USD 106.13 billion in 2026, growing at a CAGR of 4.16%.

Household appliances include a diverse range of electrical and electronic devices designed for domestic use, including refrigerators, washing machines, dishwashers, ovens, cooktops and small appliances such as coffee machines, vacuum cleaners and air treatment systems. These products are integral to modern European living, which reflects evolving standards of convenience, hygiene and energy efficiency. According to Eurostat, over 95% of EU households owned a refrigerator and washing machine in 2025, while dishwasher penetration stood at around 50% in Western and Northern Europe. Urbanisation trends further influence demand as per the European Directorate-General for Regional Policy, 78% of the EU population resided in urban or suburban areas in 2025, which is driving demand for space-efficient and multifunctional appliances. Concurrently, the average age of major appliances in use has risen to 12.3 years, as documented by the European Environment Agency, signalling a growing replacement cycle. This confluence of regulatory pressure, consumer behaviour, and infrastructure maturity defines the contemporary landscape of the European household appliances market.

MARKET DRIVERS

Stringent EU Energy and Ecodesign Regulations Driving Product Innovation

The European Union’s regulatory ecosystem serves as a principal catalyst for technological advancement and consumer renewal cycles in the household appliances sector, which is majorly driving the growth of the European household appliances market. The revised Energy Labelling Regulation implemented in 2021 reset efficiency classes to a stricter A–G scale, rendering most previously top-rated appliances midtier overnight. According to the European Commission, a large majority of refrigerators sold in 2025 carried a B rating or higher, which is an increase from early adoption levels in 2021 and is demonstrating rapid industry adaptation. The Ecodesign for Sustainable Products Regulation, effective from 2025, mandates reparability scoring, minimum spare part availability for seven to ten years, and standardised interfaces for key components. According to a 2025 assessment by the European Consumer Organisation, over two-thirds of consumers now consider reparability information before purchasing large appliances. Manufacturers have responded by redesigning modular architectures. For instance, dishwasher brands now offer tool-free access to pumps and filters. These regulations not only reduce household energy consumption but also stimulate innovation in compressor technology, insulation materials, and digital diagnostics, which is transforming compliance into competitive differentiation.

Rising Demand for Connected and Smart Home Integration

European households are increasingly adopting internet-connected appliances that integrate with broader smart home ecosystems, driven by convenience, energy management, and security expectations, which is further boosting the regional market growth. According to the European Telecommunications Standards Institute (ETSI), tens of millions of EU households owned at least one smart appliance in 202,4 a,, nd this figure is projected to rise significantly by 2027. Refrigerators with internal cameras, washing machines with remote start via mobile apps, and ovens with recipe-guided cooking are no longer niche offerings. According to the GSMA’s 2025 Smart Home Adoption Index, a substantial share of German and Dutch consumers rank appliance connectivity as “important” when replacing old units. This shift is amplified by interoperability standards such as Matter, which ensures cross-brand compatibility across Apple, Google, and Amazon platforms. Whirlpool and Electrolux embedded Matter protocol into 2025 product lines, which is enabling seamless integration without proprietary hubs. Moreover, utility providers in France and Italy now offer dynamic electricity tariffs that sync with smart appliances to shift cycles to off-peak hours, reducing bills by up to double-digit percentages, as verified by the Florence School of Regulation. This convergence of digital infrastructure, consumer willingness, and grid responsiveness is redefining appliance functionality beyond mechanical performance.

MARKET RESTRAINTS

Prolonged Replacement Cycles Due to Economic Uncertainty

Household appliance purchases in Europe face significant headwinds from extended replacement timelines fuelled by macroeconomic volatility and shifting consumer priorities, which are hampering the regional market growth. According to the European Central Bank’s Household Expectations Survey (2026), a majority of respondents indicated they would delay major durable purchases due to inflation concerns and job market instability. The average lifespan of major appliances has consequently increased as the European Environment Agency recorded a mean usage duration of over 13 years for refrigerators in 2025, compared to around 10 years in 2018. This trend is particularly pronounced in Southern and Eastern Europe, where real disposable income growth remained below 1% in 2025, as per Eurostat. Even when repairs become uneconomical, consumers increasingly opt for secondhand or refurbished units as sales of which grew by over 20% in 2025, according to the European Circular Economy Stakeholder Platform. Manufacturers face margin compression as promotional discounts intensify to stimulate demand, yet consumer willingness to pay premium prices for new features remains constrained, which is creating a structural drag on volume growth.

Supply Chain Fragmentation and Geopolitical Disruptions

The European household appliances market contends with persistent vulnerabilities in global supply chains, particularly for critical electronic components and rare earth materials. According to the European Union Agency for Cybersecurity, over two-thirds of microcontrollers used in European appliances are sourced from East Asia, with lead times fluctuating between several months in 2025 due to export restrictions and port congestion. The conflict in Eastern Europe further disrupted the supply of neonga s causing double-digit spikes in sensor costs, as documented by the Fraunhofer Institute for Reliability and Microintegration. Additionally, the EU’s dependency on Chinese rare earths for motor magnets remains high as China supplied nearly 90% of Europe’s neodymium demand in 2025, according to the European Raw Materials Alliance. While companies like BSH and Miele are investing in nearshoring pilot projects in Poland and Romania, full supply chain resilience remains years away. These external dependencies introduce cost unpredictability and production delays, which limit agility in responding to demand surges or regulatory shifts.

MARKET OPPORTUNITIES

Expansion of Circular Economy Business Models

The transition toward circularity presents a lucrative opportunity for the European household appliances market. Leasing, subscription, and product-as-a-service models are gaining traction, particularly in urban markets where ownership is less prioritised. According to the Ellen MacArthur Foundation, over 100 appliance-related circular initiatives were launched across Europe in 2025, including Electrolux’s “Care by Electrolux” washing machine subscription in Sweden and Philips’ “Light as a Service” model adapted for kitchen ventilation systems. These models rely on design for disassembly, with a majority of new Miele dishwashers now using standardised fasteners enabling full refurbishment in under an hour, as per internal company data shared with the European Remanufacturing Network. The EU’s Right to Repair Directive mandates that spare parts remain available for up to ten years, facilitating certified second-life markets. In France, hundreds of certified repair shops now participate in the “Repar’Acteurs” network supported by ADEME, processing large volumes of appliances in 2025. This shift from transactional to relational commerce enhances customer lifetime value while aligning with EU sustainability mandates.

Growth in Urban Micro Housing Driving Demand for Compact Appliances

Europe’s intensifying urban densification is reshaping appliance design toward space optimisation and multifunctionality. According to Eurostat’s 2025 Housing in Europe report, a significant share of new residential completions in EU cities were under 50 square metres, which reflects the surge in microapartments and coliving units. This spatial constraint fuels demand for narrow-width refrigerators, slim dishwashers, and combination washer-dryers, as these are the categories that industry associations report grew at double-digit rates in 2025. Brands such as Beko and Candy have introduced built-in” series with unified facades that blend into kitchen cabinetry, while Siemens launched a countertop dishwasher with 6-litre water consumption per cycle and around 40% less than standard models. The trend is especially strong in cities such as Paris, Berlin, and Amsterdam, where municipal planning policies incentivise high-density housing. According to the OECD’s 2025 Global State of National Urban Policy report, compact appliance adoption correlates strongly with public transport access and car-free living, which indicates a lifestyle-driven market shift. Manufacturers who align industrial design with urban living realities are best positioned to capture this structural growth vector.

MARKET CHALLENGES

Intensifying Price Competition from Asian Manufacturers

The rising pressure from Asian competitors offering technologically comparable products at significantly lower price points is one of the major challenges to the European household appliances market. According to the European Commission’s 42nd Annual Report on Trade Defence Instruments (2025), imports of household appliances from China, Turkey, and South Korea rose sharply between 2022 and 2025, with landed prices substantially below those of EU-made equivalents. Brands such as Haier, TCL, and LG now dominate entry-level and mid-tier segments in Southern and Eastern Europe, which is leveraging automated factories and vertically integrated component supply. In Spain and Italy, retail tracking data from GfK confirms that a majority of new refrigerator purchases under €400 in 2025 were non-European brands. While European manufacturers retain strength in premium and built-inn categories, the erosion of midmarket share threatens economies of scale. Attempts to counter this through cost optimisation often conflict with EU sustainability mandates, which increase production complexity. Without strategic differentiation through service design, localisation, or superior durability, European players risk further margin erosion in volume-driven categories.

Inconsistent Implementation of Repair and Recycling Infrastructure

Despite progressive EU legislation, the on-the-ground execution of repair and recycling systems remains fragmented across member states, which is undermining circular economy objectives and consumer confidence. According to a 2025 audit by the European Environment Agency, fewer than half of EU countries have nationwide networks ensuring spare part delivery within 72 hours, which is a key requirement under the new Right to Repair Directive. In contrast, regions such as Bavaria and Lombardy offer same-day access, while parts of Eastern Europe lack certified repair centres entirely. Similarly, e-waste collection rates vary dramatically. According to the Eurostat’s 2025 Circular Economy Dashboard, Sweden recycles over 80% of end-of-life appliances as compared with barely one-third in Romania. This disparity discourages consumers from repairing or responsibly discarding units, perpetuating landfill use. Moreover, the absence of harmonised refurbishment standards means secondhand appliances often lack performance guarantees, limiting resale value. Until infrastructure gaps are closed through coordinated public-private investment, the market will struggle to fully realise the environmental and economic benefits of circularity and leave both regulators and manufacturers with unmet sustainability targets.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.16% |

| Segments Covered | By Product, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Whirlpool Corporation, Samsung Electronics Co. Ltd., Robert Bosch GmbH, LG Electronics Inc., Electrolux AB, Haier Smart Home Co., Ltd., Panasonic Corporation, Sharp Corporation, Miele, Midea Group, Koninklijke Philips N.V., Breville Group Limited, De'Longhi S.p.A., SEB Groupe (Groupe SEB), and Dyson Limited |

SEGMENTAL ANALYSIS

By Product Insights

The major appliances segment dominated the European household appliances market by holding 68% of the market share in 2025. The dominance of this segment in the European market is attributed to its essential role in daily domestic life and regulatory-driven replacement cycles. According to Eurostat (2025), refrigerators and washing machines remain near universal in EU households, with penetration rates exceeding 90% and 85% respectively. The EU Ecodesign Directive mandates minimum energy performance standards, accelerating the replacement of old, er inefficient units. According to the European Environment Agency (EEA, 2025), a significant share of refrigerators in use were over 12 years old and rated below class C under the new energy labelling system, which is creating a substantial installed base ripe for renewal. Manufacturers such as BSH and Electrolux have capitalised on this by integrating smart diagnostics and extended warranties, which is enhancing perceived value. Urban housing policies in Germany and the Netherlands increasingly require new builds to include dishwashers and dryers, which embeds major appliances into construction standards. This structural entrenchment cements major appliances as the market’s backbone. In the next few years, the major appliances segment is expected to sustain dominance due to regulatory compliance, replacement demand, and integration into housing standards.

The small appliances segment is expected to register the fastest CAGR of 6.85% over the forecast period in the European market. The balance of rising disposable income, flexible living arrangements, and convenience-driven lifestyles is propelling the growth of small appliances in this European household appliances market. According to the European Commission’s Household Budget Survey (2025), expenditure on small kitchen and personal care appliances increased significantly year-on-year, with air fryers, coffee machines, and robotic vacuum cleaners leading purchases. Kantar consumer insights (2026) highlight that urban millennials are the most engaged, with more than half of consumers aged 25–39 owning multiple small appliances compared to lower adoption among older cohorts. E-commerce platforms have further fuelled trial, which is offering bundled deals and subscription models. For instance, Philips’ “Daily Collection” coffee capsules aare linkedto machine purchases. As per the European Test Organisation for Domestic Appliances, innovations in energy efficiency have reduced usage barriers, with modern hand blenders consuming minimal electricity per use. This blend of affordability, portability, and tech integration positions small appliances as the most dynamic growth vector in the European household appliances market. Over the next few years, small appliances are expected to expand rapidly, driven by affordability, lifestyle shifts, and digital retail adoption.

By Distribution Channel Insights

The electronic stores segment dominated the European household appliances market by accounting for 65.5% of the European market share in 2025, owing to its role as the preferred channel for high-involvement purchases requiring demonstration and expert advice. Chains such as MediaMarkt, Saturn, and Fnac offer immersive showrooms where consumers can test dishwasher noise levels, compare refrigerator compartments, and experience smart connectivity features firsthand. According to the European Retail Association for Electronics and Appliances (2025), a majority of major appliance buyers visited a physical electronics retailer before purchasing, citing trust in product authenticity and post-sale support. These stores also provide bundled services that enhance convenience and reduce purchase friction. In Germany and Italy, premium brand sales, including Miele and Sme, occur predominantly through authorised electronics dealers. Furthermore, store staff trained in EU energy labels and repairability scores guide consumers toward compliant choices, aligning retail practice with regulatory intent. This consultative model remains unmatched by other channels for complex durable goods. In the next few years, electronic stores are expected to retain dominance for major appliances, supported by experiential retail and bundled services.

The online segment is expected to register the fastest CAGR of 9.2% over the forecast period in the European household appliances market. The balance of enhanced logistics, seamless financing, and AI-powered recommendation engines is propelling the growth of online distribution in this European market. According to Eurostat (2025), cross-border ecommerce of electrical goods within the EU rose sharply, with appliances among the top categories by value. Platforms such as Amazon and Cdiscount now offer white-glove delivery, including unpacking, installation, and packaging removal, closing the service gap with physical stores. For instance, more than half of small appliance purchases occurred online, underscoring the channel’s strength in convenience categories. Retailers leverage dynamic pricing algorithms that adjust to energy label tiers, which promotes Arated models during off-peak electricity tariff campaigns. Augmented reality apps such as Bosch’s “Home Appliances AR” enable consumers to visualise appliance dimensions in their kitchens, which is reducing return rates. This fusion of digital convenience with physical reassurance is rapidly reshaping appliance retail. Over the next few years, the online distribution segment is expected to expand rapidly, driven by digital innovation, logistics improvements, and consumer preference for convenience.

REGIONAL ANALYSIS

Germany Market Analysis

Germany dominated the market in Europe in 2025 by capturing 22.8% of the regional market share. The dominating position of Germany in the European market is driven by its engineering quality, energy efficiency, and durability. The demand for household appliances in Germany is growing exponentially, with premium brands such as Bosch, Siemens, and Miele leading sales. According to Statista, 96% of households owned a washing machine and 89% a dishwasher in 2025, among the highest penetration rates globally. Regulatory measures accelerate replacement cycles, with the German Energy Agency mandating rated appliances in new rentals. Berlin’s 2023 housing code requires built-in kitchen appliances in all new residential units. Germany also hosts over 1,200 certified appliance service centres, ensuring compliance with the EU’s Right to Repair Directive. With refrigerators averaging a lifespan of 14 years yet frequent replacement for efficiency gains, Germany is expected to sustain a stable and high-value market.

France Market Analysis

France represents a promising regional segment in the European household appliances market. According to INSEE, 55% of households replaced at least one major appliance in 2025, supported by the government’s “Prime Énergie” subsidy covering up to €200 for efficient upgrades. Circular retail models are strong, with Darty’s “Recommerce” program refurbishing and reselling 185,000 appliances in 2025. Lifestyle preferences amplify demand for built-in ovens and wine coolers, with 41% of new kitchens featuring integrated designs. Online appliance sales grew by 17% in 2025, driven by Cdiscount and Fnac. France is expected to remain a high-growth hub, sustained by public incentives, private innovation, and lifestyle alignment.

United Kingdom Market Analysis

The United Kingdom plays a key role in Europe’s household appliances market. According to the Office for National Statistics, 21% of households are private renters, replacing appliances every 5–7 years compared to the national average of 11 years. Built-to-rent developments institutionalise procurement, with Greystar installing 12,000 smart appliance suites in 2025. E-commerce penetration is among Europe’s highest, with 49% of appliance purchases online in 2025. Smart integration is advancing, with 38% of new washing machines featuring WiFi connectivity. The UK is expected to remain resilient, driven by rental demand, digital maturity, and smart home adoption.

Italy Market Analysis

Italy represents a high-value segment in Europe’s household appliances market. According to Istat, dishwasher ownership reached 68% in 2025, up from 52% in 2020. Italy’s “Superbonus 110” tax incentive accelerated appliance upgrades, with 1.2 million units installed between 2021 and 2023. Espresso machine sales grew by 22% in 2025 and reflecting cultural attachment to coffee rituals. With 63% of kitchens featuring coordinated appliance suites, Italy is expected to sustain demand through design heritage, policy support, and lifestyle integration.

Spain Market Analysis

Spain is emerging as a structurally resilient market in Europe’s household appliances sector. According to Spain’s National Statistics Institute, new residential construction rose by 14% in 2025, with all new builds required to include energy class A appliances. AEMET recorded 120+ days above 30°C in 2025, boosting demand for advanced cooling and heating pump washing machines. The “Plan Renove Electrodomésticos” provided €150 rebates, stimulating 850,000-unit sales in 2025. Online sales grew by 2year-on-yearear, led by MediaMarkt and PC Components. Spain is expected to strengthen its role as a Southern European growth corridor.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the notable key players in the European household appliances market are

- Whirlpool Corporation

- Samsung Electronics Co. Ltd.

- Robert Bosch GmbH

- LG Electronics Inc.

- Electrolux AB

- Haier Smart Home Co., Ltd.

- Panasonic Corporation

- Sharp Corporation

- Miele

- Midea Group

- Koninklijke Philips N.V.

- Breville Group Limited

- De'Longhi S.p.A.

- SEB Groupe (Groupe SEB)

- Dyson Limited

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the European household appliances market are prioritising regulatory compliance through energy-efficient and repairable product designs. They invest heavily in smart home integration, leveraging platforms like Matter to ensure cross-brand compatibility. Companies are expanding circular economy initiatives, including take-back leasing and remanufacturing programs. Strategic partnerships with retailers, housing developers, and utility companies enhance ecosystem reach. Innovation in materials, such as bio-based plastics and low-GWP refrigerants, addresses environmental mandates. Digitalisation of after-sales services through AI diagnostics and remote support improves customer retention. These strategies collectively reinforce competitiveness amid tightening sustainability regulations and evolving consumer expectations.

COMPETITION OVERVIEW

The European household appliances market features intense competition among established European manufacturers, Asian entrants, and niche premium brands. European players like BSH Electrolux and Miele lead in premium and built-in segments through engineering excellence and sustainability credentials. Meanwhile, Asian competitors, including Hai,er LG and Samsung, dominate mid-tier and entry-level categories with aggressive pricing and rapid technology adoption. Competition is increasingly defined by compliance with EU ecodesign and energy labelling rules, reparability score, and carbon footprint transparency. Digital capabilities such as smart connectivity ty predictive maintenance, and integration with energy management systems have become key differentiators. Private label growth in retail channels adds further pressure on margins. The market also sees rising competition from circular models where refurbished and leased appliances challenge traditional ownership. Innovation speed, regulatory agility, and service depth now determine competitive advantage more than scale alone.

TOP PLAYERS IN THE MARKET

- BSH Hausgeräte GmbH is a leading European manufacturer operating globally under brands such as Bosch, Siemens, Gaggenau and Neff. The company plays a pivotal role in advancing smart and sustainable home appliances across Europe with a strong emphasis on energy efficiency and connectivity. In 2025, BSH launched its Home Connect ecosystem across 30 European countries, enabling seamless integration of appliances with major smart home platforms. It also inaugurated a carbon-neutral dishwasher production line in Germany aligned with its net-zero 2030 target. These initiatives reinforce its technological leadership and commitment to circular design while expanding its influence in premium and built-in segments worldwide.

- Electrolux Group is a major global player headquartered in Sweden with deep roots in the European household appliances market through its Electrolux AEG and Frigidaire brands. The company focuses on sustainable innovation, including the development of refrigerants with near-zero global warming potential and fabrics made from recycled ocean plastic for vacuum cleaner components. In early 2026, Electrolux introduced its “Circular Care” program across Western Europe, offering repair leasing and take-back services. It also partnered with IKEA to co-develop energy-efficient kitchen appliances featuring a modular design for easy disassembly. These actions solidify its position as a sustainability-driven innovator in both European and global markets.

- Whirlpool Corporation maintains a significant presence in Europe through its Whirlpool, KitchenAid, and Hotpoint brands, serving diverse consumer segments from mass market to premium. The company has intensified its focus on digital services and energy optimisation in response to EU regulatory shifts. In 202,4, Whirlpool rolled out AI-powered load-sensing technology across its European washing machine range, reducing water and energy use by up to 25%. It also expanded its remanufacturing facility in Poland to refurbish 200000 units annually, supporting the EU’s circular economy agenda. These strategic investments enhance product differentiation and align Whirlpool with Europe’s decarbonisation and consumer durability expectations.

MARKET SEGMENTATION

This research report on the European household appliances market has been segmented and sub-segmented based on categories.

By Product

- Major Appliances

- Small Appliances

By Distribution Channel

- Hypermarkets & Supermarkets

- Electronic Stores

- Online

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the Europe household appliances market?

The Europe household appliances market includes major and small appliances used for cooking, cleaning, laundry, refrigeration, and home comfort across residential households.

2. What factors are driving the growth of the household appliances market in Europe?

Key growth drivers include rising urbanization, increased disposable incomes, smart home adoption, energy-efficient technologies, and strong demand for premium and connected appliances.

3. Which household appliance category is most popular in Europe?

Major appliances such as refrigerators, washing machines, and air conditioners remain the most widely purchased due to their necessity and long replacement cycles.

4. Which countries dominate the Europe household appliances market?

Germany, the United Kingdom, France, Italy, and Spain lead the market due to strong manufacturing bases and high consumer spending.

5. What are the major distribution channels for household appliances in Europe?

Household appliances are primarily sold through hypermarkets & supermarkets, electronic stores, and online retail platforms.

6. How is the shift toward smart homes impacting the market?

The rise of smart homes is accelerating demand for connected appliances with IoT features such as remote control, energy monitoring, and automation.

7. What role does energy efficiency play in appliance purchases?

Energy efficiency is a major buying consideration, driven by EU energy labeling regulations and increased consumer awareness of electricity costs and sustainability.

8. What is the future outlook for the Europe household appliances market?

The market is expected to grow steadily due to rising adoption of smart appliances, sustainability-driven innovations, and continued expansion of online retail.

9. What challenges does the Europe household appliances market face?

Key challenges include fluctuating raw material costs, supply chain disruptions, environmental regulations, and increasing competition from low-cost manufacturers.

10. Who are the leading players in the Europe household appliances market?

Top companies include Whirlpool Corporation, Samsung Electronics, Bosch, LG Electronics, Electrolux, Haier, Panasonic, Midea Group, Philips, Breville, De’Longhi, SEB Groupe, Sharp, Miele, and Dyson.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com