Europe HVDC Cables Market Size, Share, Trends & Growth Forecast Report Segmented By Location of Deployment (Underground, Submarine, and Overhead), and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Market Size, 2025

$4.01 BnMarket Estimate, 2026

$4.21 BnMarket Forecast, 2034

$6.25 BnCAGR, 2026–2034

5.06%Executive Summary: Europe HVDC Cables Market

- Market Scope: Comprehensive regional Europe high-voltage direct current (HVDC) cables market analysis covering locations of deployment, offshore wind integration frameworks, country-level leadership, and cross-border grid interconnection metrics.

- Market Valuation: Valued at USD 4.01 billion (2025 base year), estimated at USD 4.21 billion (2026), and projected to reach USD 6.25 billion by 2034, registering a steady CAGR of 5.06% (2026–2034).

- Primary Growth Drivers: Massive expansion of offshore wind capacity, European Union grid interconnection mandates, and the integration of renewable energy grids. Key operational, regulatory, and capacity highlights include Europe’s offshore wind capacity scaling from 16 GW in 2023 to >300 GW by 2050, the EU targeting 75% electricity interconnection capacity among member states by 2030 (up from ~14% in 2020), Germany targeting 30 GW of offshore wind by 2030, the UK targeting 40 GW of offshore wind by 2030, France planning to double interconnection capacity to 18 GW by 2030, and over 30% of proposed European HVDC projects facing delays due to environmental assessments and public consultations.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Location of Deployment | Submarine HVDC Cables (dominated segment with 48.4% of total demand in 2025) | Submarine HVDC Systems (projected to register the fastest CAGR of 9.4%) |

| By Application Sector | Offshore Wind Farm Grid Interconnections & Cross-Border Power Transmission | Deep-Water Subsea & Long-Distance Terrestrial Interconnectors |

| By Cable Technology | Mass-Impregnated (MI) Cables & Conventional High-Voltage Line Formats | Advanced Extruded Direct Current (DC) Cable Systems & High-Capacity Polymer Designs |

| By Country / Region | Germany (led the European market with a 24.1% share in 2025) | Pan-European North Sea & Baltic Offshore Wind Corridors (e.g., UK & France) |

Major Market Players & Market Structure

Market Structure: Highly competitive European power transmission and cable manufacturing landscape featuring major multinational energy engineering and specialized cable enterprises competing intensely on submarine HVDC grid projects, offshore wind farm connectivity, cross-border European interconnectors, and advanced extruded DC cable engineering.

Key Companies: ABB Ltd., ACOME, Brugg Kabel AG, GE, LS Cable & System Ltd., Nexans, NKT A/S, Prysmian Group, Siemens AG, Sumitomo Electric Industries, Tele-Fonika Kable, Toshiba Corporation, Tratos, and ZTT.

Europe HVDC Cables Market Size

The Europe HVDC cables market size was valued at USD 4.01 billion in 2025. The European market size is expected to reach USD 6.25 billion by 2034 from USD 4.21 billion in 2026, growing at a CAGR of 5.06% from 2026 to 2034.

The European HVDC (High-Voltage Direct Current) cables market plays a critical role in the continent’s evolving energy infrastructure, facilitating long-distance, high-capacity power transmission with minimal losses. HVDC technology is increasingly favored over traditional alternating current (AC) systems for interconnecting national grids, integrating offshore wind farms, and enabling cross-border electricity trade. These cables are essential for transporting renewable energy generated in remote or offshore locations to urban centers where demand is highest.

Europe’s transition toward a low-carbon energy future has significantly boosted the demand for HVDC solutions. With ambitious climate targets set under the European Green Deal, countries are investing heavily in offshore wind projects, particularly in the North Sea and Baltic regions. According to the European Commission, offshore wind capacity in Europe is expected to increase from 16 GW in 2023 to over 300 GW by 2050, necessitating robust transmission infrastructure like HVDC cables to ensure grid stability and efficiency.

In addition to renewable integration, HVDC cables support grid interconnectivity between neighboring countries, enhancing energy security and market flexibility. Projects such as NordLink (connecting Norway and Germany), Viking Link (UK and Denmark), and ElecLink (France and UK) exemplify this trend.

MARKET DRIVERS

Expansion of Offshore Wind Energy Capacity Across Europe

One of the primary drivers of the European HVDC cables market is the rapid expansion of offshore wind energy installations, which require efficient and reliable transmission infrastructure to deliver power from remote sea-based turbines to onshore grids. HVDC cables are uniquely suited for transmitting large volumes of electricity over long distances with minimal energy loss, making them the preferred choice for connecting offshore wind farms to mainland grids. For example, the Dogger Bank Wind Farm in the UK, one of the world’s largest offshore wind projects, relies on HVDC transmission systems to transport power back to shore efficiently. Additionally, regulatory frameworks such as the EU Renewable Energy Directive and national subsidies for offshore wind development have accelerated project approvals and investments. In Germany, the Federal Ministry for Economic Affairs and Climate Action outlined plans to install at least 30 GW of offshore wind capacity by 2030 , all of which will depend on advanced HVDC cabling for effective power evacuation.

Increasing Cross-Border Grid Interconnections and Regional Energy Integration

Increasing Cross-Border Grid Interconnections and Regional Energy Integration

A significant driver fueling the Europe HVDC cables market is the growing emphasis on cross-border grid interconnections and regional energy integration aimed at enhancing energy security, optimizing resource utilization, and stabilizing electricity markets. As per the European Network of Transmission System Operators for Electricity (ENTSO-E), the EU aims to increase interconnection capacity among member states to at least 75% of installed electricity production by 2030 , up from around 14% in 2020 , requiring extensive deployment of HVDC transmission infrastructure. HVDC cables enable stable and controllable power exchange between different AC systems, making them ideal for linking national grids that operate at varying frequencies or phases. This capability supports the balancing of intermittent renewable energy sources across borders. Projects such as NordLink (Norway-Germany), ElecLink (France-UK), and the upcoming Greenlink Interconnector (Ireland-Wales) highlight how HVDC technology is being leveraged to enhance regional energy cooperation.

Moreover, the European Commission's TEN-E (Trans-European Networks for Energy) regulation prioritizes interconnector projects that improve market integration and reduce dependency on fossil fuels. Several EU member states have signed bilateral agreements to develop new interconnections using HVDC cables, reinforcing the strategic importance of these systems in achieving a unified and resilient European power network.

MARKET RESTRAINTS

High Capital Investment and Long Project Development Timelines

One of the main restraints affecting the Europe HVDC cables market is the substantial capital investment required for project development, coupled with lengthy approval and construction timelines. HVDC transmission projects involve complex engineering, specialized materials, and extensive permitting processes, leading to high upfront costs. These financial demands often deter private investors and delay project implementation, especially in regions where regulatory clarity and funding mechanisms are still evolving. In Southern and Eastern Europe, where grid modernization efforts are less advanced than in Northern and Western Europe, securing financing for HVDC projects remains a challenge. Furthermore, environmental impact assessments, land acquisition, and public opposition can extend project timelines by several years.

Technical Complexity and Limited Local Expertise in HVDC Systems

Another key restraint impacting the Europe HVDC cables market is the technical complexity involved in designing, installing, and maintaining HVDC systems, along with a shortage of skilled professionals and local manufacturing capabilities in certain regions. Unlike conventional AC transmission lines, HVDC systems require advanced converter stations, control algorithms, and insulation technologies that demand specialized expertise. According to the European Centre for Renewable Energy, there is a noticeable skills gap in HVDC engineering and maintenance, particularly in Central and Eastern Europe, where most grid operators traditionally rely on AC-based infrastructure. This lack of technical know-how increases reliance on foreign consultants and global contractors, raising overall project costs and reducing operational autonomy. Moreover, the limited availability of domestic manufacturing facilities for high-voltage cable components—such as extruded polymer insulation and conductive materials—creates supply chain vulnerabilities. In Italy and Spain, industry reports indicate that procurement delays for critical HVDC cable parts have led to extended commissioning periods for major offshore wind and interconnector projects.

MARKET OPPORTUNITIES

Growth in Submarine HVDC Cable Deployment for Offshore Wind Farms

A major opportunity emerging in the Europe HVDC cables market is the increasing deployment of submarine HVDC cables to connect large-scale offshore wind farms to the mainland grid. With Europe spearheading global offshore wind development, particularly in the North Sea and Baltic regions, the need for high-capacity, long-distance underwater transmission infrastructure is growing rapidly. According to WindEurope, the region plans to install over 100 GW of new offshore wind capacity by 2040, much of which will be located far from shorelines, necessitating submarine HVDC solutions. Submarine HVDC cables offer distinct advantages over traditional HVAC (High-Voltage Alternating Current) systems, including lower transmission losses over long distances and greater grid stability. In Germany, the Federal Network Agency (Bundesnetzagentur) mandates the use of HVDC technology for offshore wind projects located more than 80 kilometers from the coast, ensuring optimal power delivery. Moreover, advancements in extruded DC cable technology and voltage source converter (VSC) systems are enabling higher transmission capacities and improved reliability. Companies like Siemens Energy and ABB are actively developing next-generation submarine HVDC systems capable of handling multi-gigawatt loads, positioning Europe at the forefront of this technological shift.

Electrification of Remote and Island Communities via HVDC Links

Another promising opportunity for the Europe HVDC cables market lies in the electrification and grid reinforcement of remote and island communities through dedicated HVDC connections. Many islands and isolated regions across Europe, such as Crete in Greece, Sardinia in Italy, and the Faroe Islands in Denmark, currently rely on expensive and polluting diesel generators for power generation. Also, these areas emit disproportionately high levels of CO₂ due to outdated energy infrastructure and limited access to centralized grids. HVDC cables offer a viable solution by enabling long-distance, high-efficiency power transmission from mainland grids or nearby renewable sources. Projects such as the Crete–Mainland Greece Interconnection and the Norðurál Connection in Iceland demonstrate how HVDC links can integrate remote regions into cleaner, more stable electricity networks. In Iceland, Landsvirkjun reported that HVDC transmission enabled the island to export surplus hydroelectric power while improving domestic grid resilience. Furthermore, the European Union’s Clean Energy Package encourages the interconnection of isolated systems as part of its broader decarbonization strategy.

MARKET CHALLENGES

Environmental and Permitting Hurdles for Onshore and Submarine Cable Routes

A pressing challenge facing the Europe HVDC cables market is the difficulty in securing permits and navigating environmental regulations for both onshore and submarine cable routes. HVDC transmission projects often traverse ecologically sensitive areas, protected landscapes, and densely populated zones, triggering opposition from local communities and regulatory bodies. According to the European Environment Agency, over 30% of proposed HVDC projects in Europe have experienced significant delays due to environmental impact assessments and public consultations. Onshore cable installations frequently encounter resistance due to land-use conflicts, visual impact concerns, and electromagnetic field (EMF) perception risks. In Germany, the SuedOstLink project—an HVDC line designed to transport wind power from northern to southern Germany—faced prolonged opposition from residents and conservation groups, forcing route modifications and delaying commissioning by several years. Similarly, submarine cable projects must undergo rigorous marine environmental studies to assess potential impacts on ecosystems, fisheries, and seabed integrity. In the UK, the East Anglia ONE North offshore wind connection faced scrutiny from marine biologists and fishing associations before final approval was granted.

Grid Code Compliance and System Stability Concerns in Multi-Terminal HVDC Networks

Another significant challenge impacting the Europe HVDC cables market is the complexity of ensuring grid code compliance and maintaining system stability in multi-terminal HVDC networks. As HVDC systems evolve beyond point-to-point configurations to meshed, multi-node architectures, managing dynamic load flows, fault responses, and synchronization becomes increasingly intricate. According to the European Network of Transmission System Operators for Electricity (ENTSO-E), existing grid codes were primarily designed for AC systems, leaving gaps in regulatory requirements for HVDC operations, particularly regarding frequency response, inertia emulation, and reactive power management. This inconsistency complicates the integration of HVDC-connected renewable sources into the broader grid framework. Moreover, unlike AC systems that inherently provide synchronized voltage waveforms, HVDC systems require sophisticated control mechanisms to maintain grid stability, especially during disturbances or blackouts. Standardization efforts are underway through organizations such as CIGRE and IEC, but progress remains slow.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.06% |

| Segments Covered | By Location of Deployment, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | ABB Ltd., ACOME, Brugg Kabel AG, GE, LS Cable & System Ltd., Nexans, NKT A/S, Prysmian Group, Siemens AG, Sumitomo Electric Industries, Ltd., Tele-Fonika Kable S.A., TOSHIBA CORPORATION, Tratos, and ZTT, and others. |

SEGMENT ANALYSIS

By Location of Deployment Insights

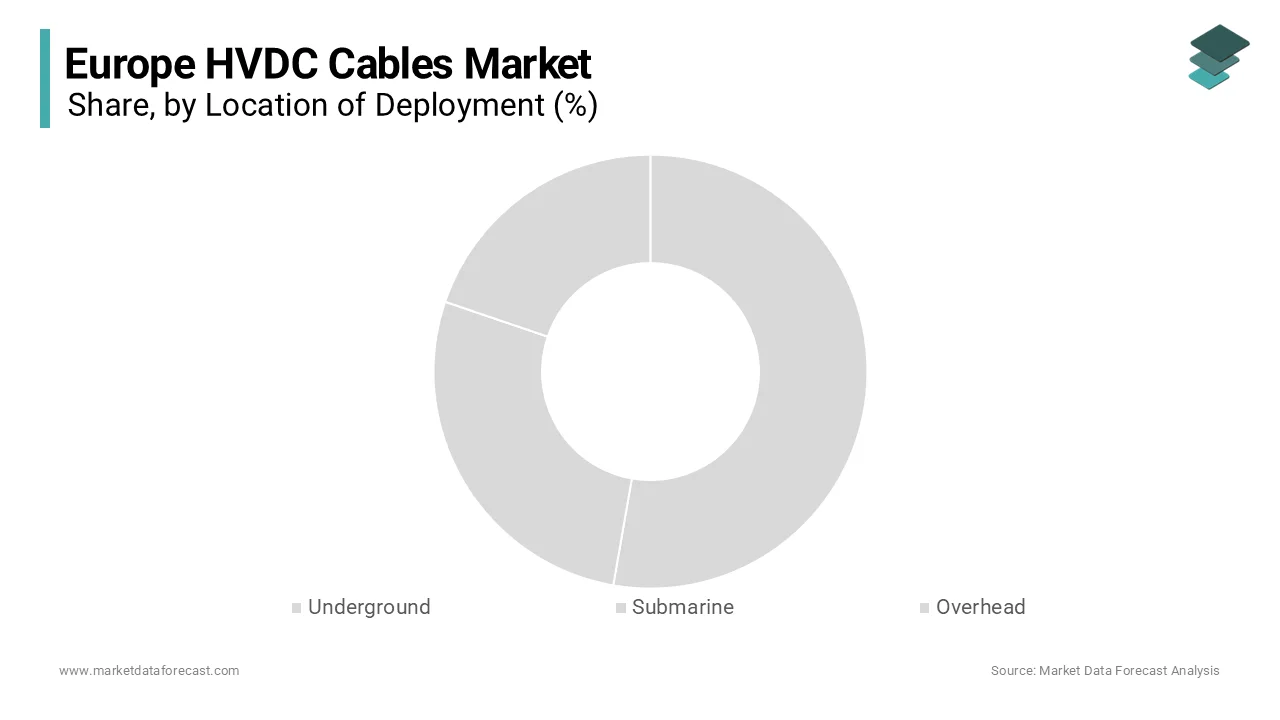

The Submarine holds the largest market share by accounting for 48.4 % of total demand in 2025. This segment’s dominance is primarily attributed to the rapid expansion of offshore wind energy projects and the increasing need for cross-border interconnections beneath seas and oceans. One key driver behind this segment’s leadership is the aggressive development of large-scale offshore wind farms in the North Sea, Baltic Sea, and Irish Sea. Projects such as Dogger Bank (UK), NordLink (Norway–Germany), and DolWin and BorWin clusters (Germany) have already demonstrated the critical role of submarine HVDC cables in transporting renewable energy from sea-based turbines to onshore grids. Another significant factor is the growing number of transnational grid interconnectors deployed under water bodies to enhance regional energy security and market integration. As per ENTSO-E, the EU aims to increase interconnection capacity to at notable portion of installed generation capacity by 2030, further reinforcing the importance of submarine HVDC cables in achieving this objective.

The Submarine segment is also anticipated to grow at the fastest CAGR of 9.4% which is driven by the accelerating deployment of offshore wind farms and the expansion of undersea grid interconnections across Europe. A major factor fueling this growth is the increasing reliance on HVDC submarine cables to transport bulk renewable energy from remote offshore wind farms to mainland grids. According to the German Wind Energy Association, offshore wind capacity in the country is expected to reach over 30 GW by 2030 , requiring substantial investments in submarine HVDC infrastructure. Besides, the European Union's Clean Energy Package emphasizes the importance of strengthening transnational electricity links, many of which are best executed via submarine routes. Moreover, technological advancements in extruded DC cable systems and voltage source converter (VSC) stations have improved reliability and scalability, making submarine HVDC an increasingly viable solution for large-scale clean energy transportation.

REGIONAL ANALYSIS

Germany spearheaded the Europe HVDC cables market with a 24.1% in 2025. It is driven by its ambitious offshore wind expansion and grid modernization efforts. As one of Europe’s largest economies and a leader in renewable energy adoption, Germany has prioritized HVDC infrastructure to connect North Sea wind farms to high-demand regions in the south. Projects such as SylWin, DolWin, and BorWin have already established a strong foundation for HVDC-based offshore transmission. Besides, Germany is investing heavily in interconnectors with neighboring countries to enhance energy security and market flexibility.

The United Kingdom is positioning itself as a key player due to its rapidly expanding offshore wind sector and growing cross-border interconnection initiatives. The UK government’s Ten Point Plan for a Green Industrial Revolution includes a target of 40 GW of offshore wind capacity by 2030 , much of which will be connected via HVDC submarine cables. According to the Crown Estate, over 8 GW of new offshore wind capacity received seabed rights in 2023 alone, reinforcing the need for advanced transmission infrastructure. Moreover, the UK is investing in interconnectors to strengthen energy security and reduce reliance on fossil fuels.

France is making strategic investments in cross-border grid interconnections. The market in nation is driven by its focus on strengthening grid interconnections with neighboring countries and integrating renewable energy sources. As part of its national energy transition strategy, France has prioritized the development of HVDC transmission corridors to facilitate cross-border electricity trade and enhance system stability. According to Réseau de Transport d'Électricité (RTE), France plans to double its interconnection capacity to 18 GW by 2030 , with several projects relying on HVDC technology for efficient power exchange. The ElecLink interconnector, connecting France and the UK through the Channel Tunnel, and the planned Aquind Interconnector both utilize HVDC systems to optimize cross-border transmission. Besides, France is exploring the potential of offshore wind in the English Channel and Bay of Biscay, which would require submarine HVDC cables for power evacuation.

The Netherlands is experiencing steady growth due to its strategic role in offshore wind development and regional electricity trading. The Dutch government has positioned the country as a key enabler of North Sea offshore wind energy transport, with plans to develop large-scale offshore grid hubs that will interconnect multiple wind farms and export electricity to neighboring countries. According to TenneT, the Dutch transmission system operator, the North Sea Wind Power Hub initiative aims to create artificial islands that serve as central points for collecting and distributing wind-generated electricity using HVDC technology. Additionally, the Netherlands is investing in interconnectors with Germany, the UK, and Belgium to enhance grid resilience and support the European electricity market.

Denmark is distinguished by its early adoption of offshore wind and commitment to regional energy integration. As a global leader in wind energy, Denmark has leveraged HVDC technology to interconnect its domestic grid with neighboring countries and facilitate cross-border electricity flows. The Viking Link interconnector, linking Denmark and the UK, and the upcoming Greenlink project connecting Ireland and Wales are prime examples of Denmark’s role in advancing HVDC-based transmission. According to Energinet, Denmark’s national transmission system operator, the country plans to expand offshore wind capacity to 12 GW by 2030, including the development of artificial energy islands in the North Sea that will rely on HVDC cables for power distribution. Apart from these, Denmark is participating in the North Sea Link and COBRAcable projects, reinforcing its position as a hub for HVDC interconnectivity in Northern Europe.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

ABB Ltd., ACOME, Brugg Kabel AG, GE, LS Cable & System Ltd., Nexans, NKT A/S, Prysmian Group, Siemens AG, Sumitomo Electric Industries, Ltd., Tele-Fonika Kable S.A., TOSHIBA CORPORATION, Tratos, and ZTT are the key market players in the Europe HVDC cables market.

The competition in the Europe HVDC cables market is marked by a blend of innovation-driven leadership and strategic positioning by global and regional players. As demand surges due to offshore wind expansion and transnational grid interconnection initiatives, key manufacturers are intensifying efforts to differentiate themselves through technological advancements and operational excellence. The market is dominated by a few established firms with deep technical expertise, including Nexans, Prysmian Group, and ABB, which hold significant influence over project execution and supply chain dynamics. However, niche players and emerging suppliers are increasingly challenging these leaders by offering cost-competitive or specialized HVDC solutions tailored to specific regional requirements. Competitive differentiation is largely based on product reliability, installation capabilities, and the ability to deliver customized solutions for complex offshore and subsea environments. Additionally, companies are strengthening their market position through strategic acquisitions, local partnerships, and proactive engagement in policy discussions around energy infrastructure.

TOP PLAYERS IN THIS MARKET

Nexans

Among the leading players shaping the Europe HVDC cables market, Nexans stands out as a global leader in advanced cable solutions, with a strong presence in high-voltage transmission projects. The company plays a pivotal role in delivering submarine and underground HVDC systems that support offshore wind integration and cross-border interconnections across Europe.

Prysmian Group

Another key player is Prysmian Group, recognized for its cutting-edge HVDC cable technologies and extensive R&D capabilities. Prysmian contributes significantly to the global market by supplying high-performance cables for large-scale renewable energy transmission, particularly in deep-sea and long-distance land applications.

ABB Ltd

Lastly, ABB remains a major force in the HVDC sector, offering end-to-end solutions that include not only cables but also converter stations and grid integration technology. ABB’s expertise in power systems enables seamless integration of HVDC infrastructure into national grids, reinforcing grid stability and enhancing Europe’s renewable energy connectivity strategy.

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

One of the primary strategies employed by key players in the Europe HVDC cables market is investing heavily in R&D to develop next-generation HVDC cable technologies . Companies are focusing on improving insulation materials, increasing voltage capacities, and enhancing system efficiency to meet the evolving needs of offshore wind and cross-border transmission projects.

Another crucial approach is expanding manufacturing and production facilities within Europe to ensure faster delivery times, reduce logistical complexities, and comply with regional standards. This localization strategy helps companies maintain a competitive edge by aligning with EU regulations and supporting large-scale infrastructure development plans.

A third major strategy involves forming strategic partnerships and joint ventures with transmission system operators and offshore wind developers .

RECENT HAPPENINGS IN THE MARKET

- In March 2025, Nexans announced the expansion of its HVDC cable production facility in France, aiming to increase capacity for submarine cable manufacturing and better serve the growing offshore wind and interconnector markets across Northern Europe.

- In May 2025, Prysmian Group secured a strategic partnership with a leading offshore wind developer to provide turnkey HVDC cabling solutions for a multi-gigawatt wind farm project in the North Sea, reinforcing its leadership in renewable energy transmission infrastructure.

- In July 2025, ABB launched a new generation of compact HVDC converter stations designed specifically for offshore platforms, enabling more efficient integration of distant wind farms into mainland grids and strengthening its portfolio for future European energy projects.

- In September 2025, NKT acquired a specialized HVDC cable installation vessel, enhancing its deployment capabilities and allowing the company to offer integrated design, supply, and installation services for submarine cable projects across the Baltic and North Seas.

- In November 2025, Siemens Energy formed a joint venture with a German engineering firm specializing in subsea cable laying operations, aiming to improve project execution timelines and expand its presence in the expanding European HVDC interconnector market.

MARKET SEGMENTATION

This research report on the Europe HVDC cables market is segmented and sub-segmented into the following categories.

By Location of Deployment

- Underground

- Submarine

- Overhead

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the compound annual growth rate (CAGR) of the Europe HVDC cables market?

The Europe HVDC cables market is expected to grow at a CAGR of 5.06% from 2025 to 2033.

2. What factors are driving the growth of the HVDC cables market in Europe?

Growth drivers include the rise in cross-border electricity trade, expansion of renewable energy projects, and the need for reliable long-distance transmission infrastructure.

3. Which sectors are major users of HVDC cables in Europe?

Key sectors include power utilities, offshore wind energy, and interconnection projects between countries.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com