Europe Hydronic Radiators Market Size, Share, Trends & Growth Forecast Research Report, Segmented By Product, Application, Distribution Channel, Source, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2026 to 2034)

Market Size, 2025

$7.79 BnMarket Estimate, 2026

$8.14 BnMarket Forecast, 2034

$11.63 BnCAGR, 2026–2034

4.55%Executive Summary: Europe Hydronic Radiators Market

- Market Scope: Comprehensive regional hydronic radiators market analysis covering product types, application sectors, power source categories, country-specific leadership frameworks, and key strategic developments.

- Market Valuation: Valued at USD 7.79 billion (2025), estimated at USD 8.14 billion (2026), and projected to reach USD 11.63 billion by 2034, registering a robust CAGR of 4.55% (2026–2034).

- Primary Growth Drivers: Rising demand for energy-efficient residential heating solutions, stringent environmental regulations under the European Green Deal, district heating expansion, and net-zero energy building construction. Opportunities include heat pump integration, smart thermostats, and low-temperature compatible radiators.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Product & Application | Panel radiators (held 36% market share); Residential sector (led with a 62.8% share in 2025) | Underfloor heating (projected CAGR of 7.8%); Commercial applications (fastest CAGR of 7.3%) |

| By Power Source & Region | Gas-powered systems (held largest source share in 2025); Germany (led regional market with a 23.4% share) | Electric-powered hydronic radiators (fastest-growing source segment with a CAGR of 8.6%) |

Major Market Players & Market Structure

Market Structure: Highly competitive European climate systems and heating infrastructure landscape featuring specialized manufacturers and multi-national groups competing intensely on heat pump compatibility, digital configurators, and low-temperature radiator innovations.

Key Companies: Zehnder Group, Buderus, Watts Water Technologies, Viega, DiaNorm, Vasco Group, Kermi, Caleffi, IRSAP, Uponor, Purmo Group, Arbonia, and Jaga.

Europe Hydronic Radiators Market Size

The Europe hydronic radiators market was valued at USD 7.79 billion in 2025 and is anticipated to reach a valuation of USD 8.14 billion in 2026 and USD 11.63 billion by 2034, growing at a CAGR of 4.55%, from 2026 to 2034.

The Europe hydronic radiators market is a vital component of the continent’s broader heating systems industry, serving both residential and commercial infrastructure with efficient, water-based heat distribution solutions. Unlike electric radiators that rely solely on electricity, hydronic radiators use heated water or glycol circulated through pipes and connected panels to provide consistent, energy-efficient warmth. These systems are commonly integrated with boilers, district heating networks, and renewable sources such as heat pumps and solar thermal installations.

Europe’s aging building stock, combined with stringent environmental regulations, has led to increased interest in retrofitting older properties with more sustainable heating alternatives. Moreover, the European Green Deal and national decarbonization targets are accelerating the shift away from fossil fuel-based heating systems. The growing adoption of smart thermostats and zone control systems further enhances the appeal of hydronic setups by enabling precise temperature management and reduced energy waste.

MARKET DRIVER

Rising Demand for Energy-Efficient Heating Solutions in Residential Buildings

One of the primary drivers of the Europe hydronic radiators market is the increasing demand for energy-efficient heating systems in residential buildings, particularly among homeowners seeking long-term cost savings and improved indoor comfort. Hydronic radiators offer superior thermal performance compared to traditional forced-air systems due to their ability to distribute heat evenly without drying out the air. According to the European Environment Agency, space heating accounts for two-thirds of household energy consumption in the EU, making efficiency improvements a top priority for policymakers and consumers alike. Additionally, many European countries have implemented stricter building codes that favor low-energy and passive house standards. These trends reflect a broader regional shift toward sustainable housing solutions that minimize energy waste while maintaining optimal living conditions. Furthermore, the integration of smart controls—such as programmable thermostats and zone-based heating—has enhanced the appeal of hydronic radiators by allowing users to customize temperatures room-by-room.

Expansion of District Heating Networks Across Urban Centers

A significant factor driving the Europe hydronic radiators market is the rapid expansion of district heating networks, especially in major metropolitan areas where centralized heat distribution offers environmental and economic advantages. District heating systems deliver hot water or steam from a central plant to multiple buildings via underground piping, making them highly compatible with hydronic radiator technology. According to the International Energy Agency, district heating now supplies heat to a large population of European households, with strong growth observed in cities such as Copenhagen, Warsaw, and Stockholm.

In Denmark, for instance, district heating covers a significant share of total space heating demand, supported by extensive government investment in biomass and waste-to-energy plants. This infrastructure development has created a parallel demand for hydronic radiators capable of efficiently utilizing centrally generated heat. The scalability and carbon-reduction potential of district heating make it a key pillar of Europe’s strategy to meet climate neutrality goals by 2050.

MARKET RESTRAINT

High Installation Costs and Complex Retrofitting Requirements

One of the main restraints affecting the Europe hydronic radiators market is the relatively high installation cost compared to simpler heating alternatives such as electric panel heaters or direct gas-fired systems. Hydronic radiator systems require a comprehensive setup involving boilers, pipework, circulation pumps, and sometimes underfloor integration, which increases labor and material expenses. This financial burden is particularly challenging for homeowners in Southern and Eastern Europe, where disposable incomes remain lower than in Western counterparts. A report by the European Bank for Reconstruction and Development found that a notable portion of surveyed households in Bulgaria and Romania cited affordability as a primary barrier to adopting advanced heating technologies, despite recognizing their long-term benefits. Moreover, retrofitting existing buildings with hydronic systems often involves significant structural modifications, especially in older properties with limited space for piping and boiler placement.

Regulatory Constraints and Preference for Alternative Heating Technologies

Another key restraint impacting the Europe hydronic radiators market is the presence of regulatory policies and consumer preferences that favor alternative heating technologies such as heat pumps and electric radiators. While hydronic systems are highly efficient when paired with renewable energy sources, some national policies prioritize all-electric heating solutions as part of broader electrification strategies. In addition, in regions where natural gas is still widely available and subsidized, there is less incentive to adopt hydronic systems unless they are integrated with heat pumps or district heating. Consumer perceptions also play a role, with some users associating hydronic systems with slow warm-up times and higher maintenance needs compared to plug-and-play electric alternatives.

MARKET OPPORTUNITY

Integration with Renewable Energy Sources and Heat Pumps

A major opportunity for the Europe hydronic radiators market lies in their seamless integration with renewable energy sources such as solar thermal systems, biomass boilers, and heat pumps. As the European Union accelerates its transition toward carbon-neutral heating, hydronic radiators are emerging as ideal partners for low-temperature heating solutions that operate efficiently even with intermittent energy inputs. According to the International Renewable Energy Agency, heat pump installations in Europe grew substantially in recent years, which is driven by subsidies and policy incentives aimed at replacing fossil fuel-based heating. Hydronic radiators function optimally with heat pumps because they can maintain comfortable indoor temperatures using water at lower operating temperatures compared to traditional radiators. Similarly, in Austria, the Federal Ministry for Climate Action emphasized the importance of hydronic-compatible heating circuits in achieving national renewable heating targets. Moreover, advancements in hybrid systems that combine solar thermal collectors with hydronic setups are expanding the market’s reach beyond conventional applications.

Growth in Passive House and Net-Zero Building Construction

The increasing adoption of passive house and net-zero energy building (NZEB) standards across Europe presents a significant growth opportunity for the hydronic radiators market. These construction models prioritize ultra-low energy consumption and rely on highly efficient heating systems that align perfectly with the performance characteristics of hydronic radiators. According to the European Passive House Network, over 100,000 certified passive houses existed in Europe by the end of 2023, with Germany, Austria, and Switzerland leading the way. Passive buildings achieve minimal heat loss through superior insulation and airtight design, making hydronic radiators an ideal match due to their ability to operate effectively at lower water temperatures. Additionally, the European Commission's Renovation Wave Strategy encourages the adoption of NZEB principles in both new and renovated buildings, further reinforcing the case for hydronic heating. Manufacturers are responding by developing compact, high-efficiency radiators specifically designed for passive and ultra-low-energy homes. In the Netherlands, several real estate developers have begun standardizing hydronic radiator installations in green-certified residential complexes to enhance energy performance ratings.

MARKET CHALLENGE

Limited Awareness and Misconceptions About Hydronic Radiator Benefits

A pressing challenge facing the Europe hydronic radiators market is the limited consumer awareness and prevailing misconceptions regarding the technology’s functionality and benefits. Many potential buyers remain unfamiliar with the advantages of hydronic systems compared to conventional heating methods such as forced-air furnaces or electric radiators. These misconceptions are particularly prevalent in markets like Italy and Spain, where electric heating remains dominant due to historical reliance on simple plug-in solutions. Also, misinformation about maintenance requirements and energy efficiency contributes to hesitation among homeowners considering system upgrades.

Supply Chain Disruptions and Component Shortages

Another significant challenge impacting the Europe hydronic radiators market is the ongoing supply chain disruptions and shortages of critical components used in manufacturing. The production of hydronic radiators relies on materials such as steel, aluminum, copper, and specialized valves, many of which have experienced procurement delays due to global logistics bottlenecks and geopolitical uncertainties. According to the European Industrial Gases Association, delays in raw material deliveries increased in 2023, affecting manufacturers’ ability to scale production in line with rising demand. These supply issues have been exacerbated by fluctuating energy prices and labor shortages within the manufacturing sector. This scarcity has led to extended lead times and increased costs, ultimately delaying project completions in both residential and commercial sectors. Furthermore, the reliance on imported components from Asia and North America has made European manufacturers vulnerable to trade restrictions and customs delays.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.55% |

| Segments Covered | By Product, Application, Distribution Channel, Source, and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Zehnder Group, Buderus, Watts Water Technologies, Viega, DiaNorm, Vasco Group, Kermi, Caleffi, IRSAP, Uponor, Purmo Group, Arbonia, Jaga |

SEGMENTAL ANALYSIS

By Product Type Insights

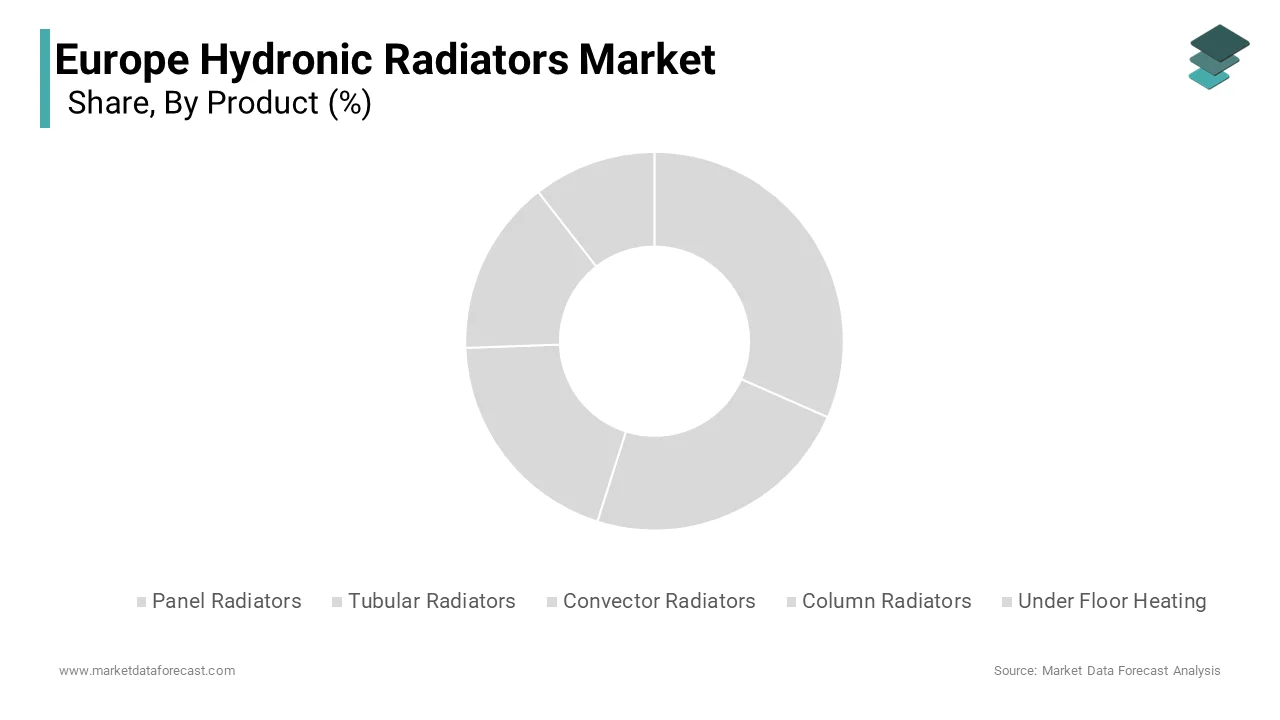

The Panel Radiators had the largest market share, i.e, 36% of total demand in 2025. This segment's control is mainly due to their widespread use in residential and commercial buildings across Europe, where they are favored for their efficiency, sleek design, and ease of installation. One key driver behind this segment’s leadership is the growing adoption of panel radiators in new housing developments and retrofit projects. These units offer superior heat output at lower water temperatures, making them highly compatible with energy-efficient boilers and heat pumps. Another contributing factor is the increasing integration of panel radiators into smart home ecosystems. Manufacturers such as Stelrad and Zehnder Group have introduced models equipped with programmable thermostatic valves and digital controls, allowing users to optimize energy consumption.

The Underfloor Heating segment is projected to grow at the fastest CAGR of 7.8% and is driven by its rising popularity in residential and commercial construction due to superior thermal comfort and space-saving advantages. Unlike traditional radiators, underfloor heating distributes warmth evenly across the floor surface, enhancing indoor climate control while freeing up wall space. A major factor fueling this growth is the increasing incorporation of underfloor heating in passive house and net-zero energy building designs. According to the European Passive House Network, over 90,000 certified passive houses existed in Europe by the end of 2023, many of which utilized underfloor heating systems integrated with low-temperature heat sources such as heat pumps and solar thermal collectors. The Swedish Energy Agency noted that a significant percentage of newly constructed eco-homes in Sweden in 2023 featured underfloor heating, noting its alignment with national sustainability goals. Apart from these, advancements in modular piping systems and compatibility with smart thermostats have made underfloor heating more accessible and efficient.

By Application Insights

The Residential segment dominated with a market share of 62.8% in 2025. This strong position is basically attributed to the extensive use of hydronic radiators in single-family homes, apartments, and multi-unit residential buildings across the continent. One of the main drivers of this segment’s leadership is the ongoing renovation wave targeting older housing stock, particularly in Western and Central Europe. In response, governments across France, Germany, and Austria have launched incentive programs promoting the replacement of outdated heating systems with modern hydronic setups. Another critical factor is the rising adoption of hydronic radiators in new residential developments, especially those designed to meet passive house or nearly zero-energy building (NZEB) standards.

The Commercial Applications segment is expected to register the highest CAGR of 7.3% from 2025 to 2033. It is outpacing other application segments due to increasing investment in sustainable office spaces, retail centers, and hospitality infrastructure. As businesses prioritize energy efficiency and occupant well-being, hydronic radiators are becoming a preferred heating solution in modern commercial buildings. One of the key drivers behind this growth is the expansion of green building certification schemes such as BREEAM, LEED, and DGNB, which encourage the use of efficient and environmentally friendly heating technologies. Also, a notable share of new commercial developments in Northern Europe pursued some form of sustainability certification in 2023, often requiring hydronic radiator systems integrated with heat pumps or district heating networks. Besides, the post-pandemic shift toward flexible workspaces and hybrid office models has led to increased demand for adaptable heating solutions that support zone-based temperature control. Moreover, government-backed initiatives promoting decarbonization of public and private sector buildings are accelerating adoption. These trends show the growing importance of the commercial applications segment in shaping the future of the hydronic radiators market in Europe.

By Distribution Channel Insights

The Offline segment captured the biggest market share of total sales in 2025. This influence is primarily due to the reliance of contractors, plumbers, and HVAC professionals on traditional distribution networks fothe r procurement of heating components and equipment. One of the key factors supporting this segment’s leadership is the complexity involved in selecting and installing hydronic radiator systems, which often requires technical consultation and expert guidance available through physical dealerships and trade suppliers. A large majority of professional buyers in the HVAC industry prefer purchasing radiators through offline channels due to the need for product demonstrations, compatibility checks, and immediate availability. Additionally, established relationships between manufacturers and local distributors ensure steady supply chains and after-sales service, reinforcing customer confidence. Furthermore, large-scale construction and renovation projects often involve bulk procurement through regional distributor networks, further strengthening the offline channel’s market position in Europe.

The Online Distribution Channel is anticipated to grow at the fastest CAGR of 9.1% and is driven by increasing digitalization, the convenience of e-commerce platforms, and expanding direct-to-consumer strategies by manufacturers. With the proliferation of online marketplaces and dedicated HVAC e-retailers, consumers and small contractors are increasingly turning to digital platforms for competitive pricing and doorstep delivery. One of the primary drivers of this trend is the growing number of DIY enthusiasts and smaller renovation firms seeking cost-effective and easily accessible heating solutions. Another significant factor is the strategic shift by leading manufacturers toward omnichannel distribution models. Companies like Jaga Climate Systems and Stelrad have expanded their e-commerce presence, offering configurators, virtual consultations, and nationwide delivery options to enhance customer experience.

By Source Insights

The Gas-powered segment spearheaded the market in 2025. This development is due to the extensive gas infrastructure across Western and Central Europe, where natural gas remains a widely used energy source for central heating systems. One of the key drivers of this segment’s leadership is the continued reliance on gas-fired boilers in both existing and newly constructed residential and commercial buildings. Countries such as Italy, Germany, and the Netherlands have historically favored gas-based heating due to its affordability and reliability compared to alternative fuels. Another contributing factor is the compatibility of gas boilers with hydronic radiator technology, ensuring stable performance and consistent heat output even in colder climates. Despite growing policy incentives for electrification and renewable heating, gas-powered hydronic radiators continue to play a dominant role in Europe’s heating landscape, particularly in regions where gas supply remains abundant and economically viable.

The Electric-Powered Hydronic Radiators segment is projected to grow at the highest CAGR of 8.6%. This is fueled by increasing electrification efforts, renewable energy adoption, and the push to phase out fossil fuel-based heating systems. Unlike conventional hydronic setups that rely on gas boilers, electric-powered variants use immersion heaters or heat pumps to circulate warm water through radiator panels, offering a cleaner and more flexible alternative. One of the primary drivers behind this growth is the European Union’s regulatory push to reduce carbon emissions from the building sector. Initiatives such as the REPowerEU Plan and national bans on gas connections in new constructions are accelerating the shift toward electric heating solutions. Additionally, advancements in thermal storage and smart control technologies are making electric-powered hydronic systems more attractive to homeowners and developers.

COUNTRY-LEVEL ANALYSIS

Germany Hydronic Radiators Market Analysis

Leading Market Share with Strong Policy Support and Infrastructure Modernization

Germany was the largest share of the Europe hydronic radiators market with 23.4% in 2025 and is driven by robust government incentives, extensive district heating networks, and a strong focus on energy-efficient building upgrades. As one of Europe’s largest economies with a dense housing stock, Germany has prioritized heating system modernization through financial support programs such as the KfW funding initiative. Also, Germany’s commitment to reducing greenhouse gas emissions under its National Climate Protection Plan has reinforced the shift away from fossil-fuel-based heating toward cleaner alternatives. The country’s extensive network of district heating, covering over 14% of households, further supports the widespread deployment of hydronic radiators in both urban and suburban settings. With continuous investment in green infrastructure and a strong manufacturing base for heating components, Germany remains the dominant force in the European hydronic radiators market.

France Hydronic Radiators Market Analysis

France is positioning itself as a key player due to its aggressive residential retrofitting initiatives and national energy transition policies. The French government has implemented substantial subsidies and tax incentives to promote the replacement of outdated heating systems with modern, energy-efficient alternatives. According to the French Environment and Energy Management Agency (ADEME), approximately 1.2 million households benefited from these subsidies, significantly boosting demand for hydronic heating solutions. Also, France’s growing reliance on district heating—particularly in cities like Paris and Lyon—has created a favorable environment for hydronic radiator adoption in both public and private housing sectors.

United Kingdom Hydronic Radiators Market Analysis

Rising Demand for Low-Carbon Heating Solutions in Urban Areas

The United Kingdom captures a notable market share and is supported by increasing demand for low-carbon heating systems in urban centers and new residential developments. The UK government’s Heat and Buildings Strategy aims to phase out high-carbon heating technologies, encouraging the adoption of hydronic systems powered by heat pumps and district heating networks. According to the Department for Business, Energy & Industrial Strategy (BEIS), over 220,000 electric and hybrid heating units, including hydronic radiators, were installed in UK homes in 2023 under the Boiler Upgrade Scheme. Additionally, London and Manchester have seen a surge in large-scale regeneration projects incorporating hydronic radiator systems to meet stringent environmental regulations.

Italy Hydronic Radiators Market Analysis

Expansion of District Heating Networks Drives Market Growth

Italy is experiencing steady growth due to the expansion of district heating networks and government-led energy efficiency programs. The Italian government’s National Integrated Energy and Climate Plan (PNIEC) emphasizes the transition toward centralized heating solutions, particularly in densely populated urban areas. According to the Italian Association for Energy Economics (IAEE), district heating now serves over 6 million households, any of which utilize hydronic radiator systems for efficient heat distribution. In Milan and Turin, municipal authorities have invested heavily in upgrading district heating infrastructure to integrate renewable energy sources such as biomass and waste heat recovery.

Sweden Hydronic Radiators Market Analysis

Sweden is distinguished by its early adoption of renewable energy-driven heating solutions and high penetration of passive house construction. The country has been a global leader in district heating, with a large portion of households connected to district heating networks, many of which are supplied by biomass, waste-to-energy, and geothermal sources. According to the Swedish Energy Agency, hydronic radiator systems are standard in a significant portion of new residential builds,e specially those designed to meet passive house standards. The rapid expansion of heat pump installations—growing annually —has further strengthened the demand for compatible hydronic radiator setups. Additionally, the Swedish government’s “Buildings of the Future” initiative has encouraged the development of smart, energy-efficient buildings that incorporate advanced hydronic heating technologies.

COMPETITIVE LANDSCAPE

The competition in the Europe hydronic radiators market is characterized by a dynamic mix of established global brands, regional specialists, and emerging players striving to capture market share through technological advancement and strategic positioning. As demand for energy-efficient and sustainable heating solutions rises, companies are increasingly focusing on product differentiation through design, performance, and smart functionality. The market remains highly fragmented, with several dominant firms leveraging strong brand recognition, extensive distribution channels, and R&D capabilities to maintain their leadership positions. However, smaller manufacturers are gaining traction by offering cost-effective alternatives tailored to niche segments such as retrofit projects and modular housing developments. Regulatory shifts toward low-carbon heating, coupled with growing consumer awareness about indoor air quality and comfort, are further influencing competitive dynamics. Companies are also investing in digital platforms and direct-to-consumer engagement to enhance visibility and streamline procurement.

KEY MARKET PLAYERS

Are the market players that are dominating the Europe hydronic radiators market incincludedhnder Group

- Buderus

- Watts Water Technologies

- Viega

- DiaNorm

- Vasco Group

- Kermi

- Caleffi

- IRSAP

- Uponor

- Purmo Group

- Arbonia

- Jaga

Top Players in the Market

- Among the leading players shaping the Europe hydronic radiators market, Stelrad Radiators stands out as a major manufacturer known for its innovative and energy-efficient radiator solutions. The company offers a diverse product portfolio that includes panel radiators, designer models, and high-performance units tailored for both residential and commercial applications. Stelrad plays a crucial role in setting industry standards through continuous product development and sustainability initiatives across European markets.

- Another key player is Zehnder Group,r ecognized globally for its premium hydronic radiator systems that combine aesthetic design with superior thermal efficiency. Zehnder specializes in creating holistic indoor climate solutions, particularly in passive houses and low-energy buildings. The company's commitment to sustainability and integration with renewable energy sources has positioned it as a leader in the high-end segment of the European hydronic radiators market.

- Lastly, Jaga Climate Systems plays an instrumental role in advancing hydronic radiator technology by introducing low-mass, rapid-response heating systems that align with modern energy-saving goals. Jaga’s focus on compact, eco-friendly designs and smart control integration has made it a preferred choice for architects and developers across Europe, reinforcing its influence in shaping future trends in the sector.

Top Strategies Used by Key Market Participants

One of the primary strategies employed by key players in the Europe hydronic radiators market is product innovation and design differentiation. Companies are continuously developing advanced radiator models that offer improved thermal performance, sleek aesthetics, and compatibility with smart home systems to meet evolving consumer preferences and building regulations.

Another crucial approach is expanding distribution networks and strengthening partnerships with HVAC professionals . Leading manufacturers are collaborating with plumbers, contractors, and distributors to ensure wider market reach and reliable after-sales support, enhancing customer trust and brand loyalty across different regions.

A third major strategy involves investing in sustainability and promoting green heating solutions .Markett participants are emphasizing eco-friendly manufacturing processes, recyclable materials, and integration with renewable energy systems such as heat pumps and solar thermal setups to align with European decarbonization goals and attract environmentally conscious consumers.

RECENT MARKET NEWS

- In February 2025, Stelrad launched a new line of ultra-slim, high-efficiency panel radiators designed for modern residential and commercial buildings, aiming to enhance thermal performance while offering a minimalist aesthetic appealing to contemporary architectural styles.

- In May 2025, Zehnder Group expanded its production facility in Belgium to increase capacity and improve supply chain responsiveness, supporting growing demand for hydronic radiators in Western and Central Europe amid rising interest in low-energy housing projects.

- In July 2025, Jaga Climate Systems introduced a new range of radiators compatible with low-temperature heat pump systems, reinforcing its commitment to sustainable heating and expanding its appeal among eco-conscious builders and homeowners across Scandinavia and Germany.

- In September 2025, Reznor, a prominent HVAC equipment manufacturer, acquired a European distributor specializing in hydronic components, aiming to strengthen its regional presence and streamline access to professional installer networks in key growth markets.

- In November 2025, Purmo, part of the Uponor Group, unveiled a digital configurator tool for architects and engineers, enabling real-time customization of hydronic radiator layouts and specifications to improve project planning efficiency and client engagement across major construction hubs in Europe.

MARKET SEGMENTATION

This research report on the Europe hydronic radiators market is segmented and sub-segmented into the following categories.

By Product Type

- Panel Radiators

- Tubular Radiators

- Convector Radiators

- Column Radiators

- Under Floor Heating

- Others

By Application

- Residential

- Commercial

- Industrial

- Institutional

By Distribution Channel

- Online

- Offline

By Power Source

- Electric

- Gas

By Material

- Steel

- Aluminium

- Copper

- Iron

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

Why is the hydronic radiator market contracting in Western Europe despite rising heating demand?

While space heating needs persist, the market is shifting from replacement volume to value-driven upgrades: aging cast-iron and steel-panel radiators are being swapped not 1:1, but with fewer, higher-output units (e.g., low-H₂O radiators) or displaced entirely by underfloor heating (UFH) and heat pump-compatible systems—especially in retrofits where system temperatures must drop below 55°C.

What segment is now driving innovation—and premium pricing?

Low-temperature, high-efficiency radiators (e.g., Stelrad Elite, Zehnder Charleston, Vogel & Noot Natura)—optimized for 45–55°C flow temps (vs. traditional 70–80°C)—are growing fastest. Paired with heat pumps or condensing boilers, they reduce energy use by 15–25% and qualify for EU Ecodesign (Lot 20) and national subsidies (e.g., Germany’s BEG grants), commanding 20–35% price premiums.

Which country leads in smart radiator adoption—and why?

Germany—driven by stringent EnEV/ GEG energy regulations and high heat pump penetration (>50% of new heating installs in 2024). Over 30% of new radiator sales now include integrated thermostatic heads with Bluetooth/Zigbee (e.g., Danfoss Eco™, Honeywell Evohome) for room-by-room optimization, feeding data into building energy management systems (BEMS).

How are sustainability mandates reshaping material choices?

The EU’s Ecodesign for Sustainable Products Regulation (ESPR) and CBAM are accelerating use of recycled steel (up to 90% in Stelrad’s RadLine) and aluminum (lighter, faster response)—while Zehnder and Rettig now offer carbon-neutral certified radiators via verified offsets and green electricity in production.

Who are the dominant players—and how is competition evolving?

Stelrad (Netherlands), Rettig Group (Finland), Zehnder Group (Switzerland), Vogel & Noot (Austria) lead in design, efficiency, and digital integration. Eastern European OEMs (Galmet, Roca Romania) compete on cost for social housing, while Chinese imports (e.g., Sunricher) target budget DIY segments though face scrutiny over CE marking and thermal performance claims.

What’s the biggest barrier to heat pump–radiator compatibility?

Delta-T mismatch: Most legacy radiators need >60°C to deliver design output, but heat pumps operate most efficiently at ≤55°C. Solutions include oversizing radiators (not always feasible in retrofits), fan-assisted models (e.g., Myson Turbo Fan), and hybrid systems (radiator + UFH)—but installer training gaps slow adoption.

How is the “renovation wave” influencing product specs?

EU Renovation Wave targets (3% public building upgrades/year) prioritize dry-install radiators (no wet plastering), modular designs for tight spaces (e.g., Zehnder’s Flat Curve), and quick-connect fittings—cutting installation time by 40% and enabling weekend retrofits in occupied buildings.

Why is cast iron seeing a niche resurgence—despite inefficiency?

In heritage renovations (UK, France, Italy), cast iron radiators (e.g., Pimlico, The Radiator Company) are rebounding for aesthetic authenticity and thermal inertia—pairing well with biomass boilers or solar thermal. Modern versions now include internal convector fins and powder-coated finishes to meet modern efficiency expectations.

What regulatory shift is most impactful for 2025+?

The EU Energy Labelling Regulation (EU 2023/1610) now requires seasonal space heating energy efficiency (ηₛₕ) class (A–G) for radiators—calculated via EN 16443. This exposes legacy products as “Class D–F,” pushing distributors to stock only Class A–B units and accelerating phase-out of non-compliant inventory.

What’s the market outlook for 2025–2030?

The Europe hydronic radiator market will stabilize post-2025—growing at ~1.2% CAGR—but with strong value growth: smart, low-temperature, circular-design radiators will dominate new builds and deep retrofits. The future isn’t just heating—it’s intelligent thermal comfort, seamlessly integrated into net-zero building ecosystems.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com