Europe In Vitro Colorectal Cancer Screening Tests Market Research Report – Segmented By Test ( Fecal Occult Blood Tests (FOBT),Biomarker Tests) End-Use & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of EU) - Industry Analysis From 2025 to 2033

Europe In Vitro Colorectal Cancer Screening Tests Market Size

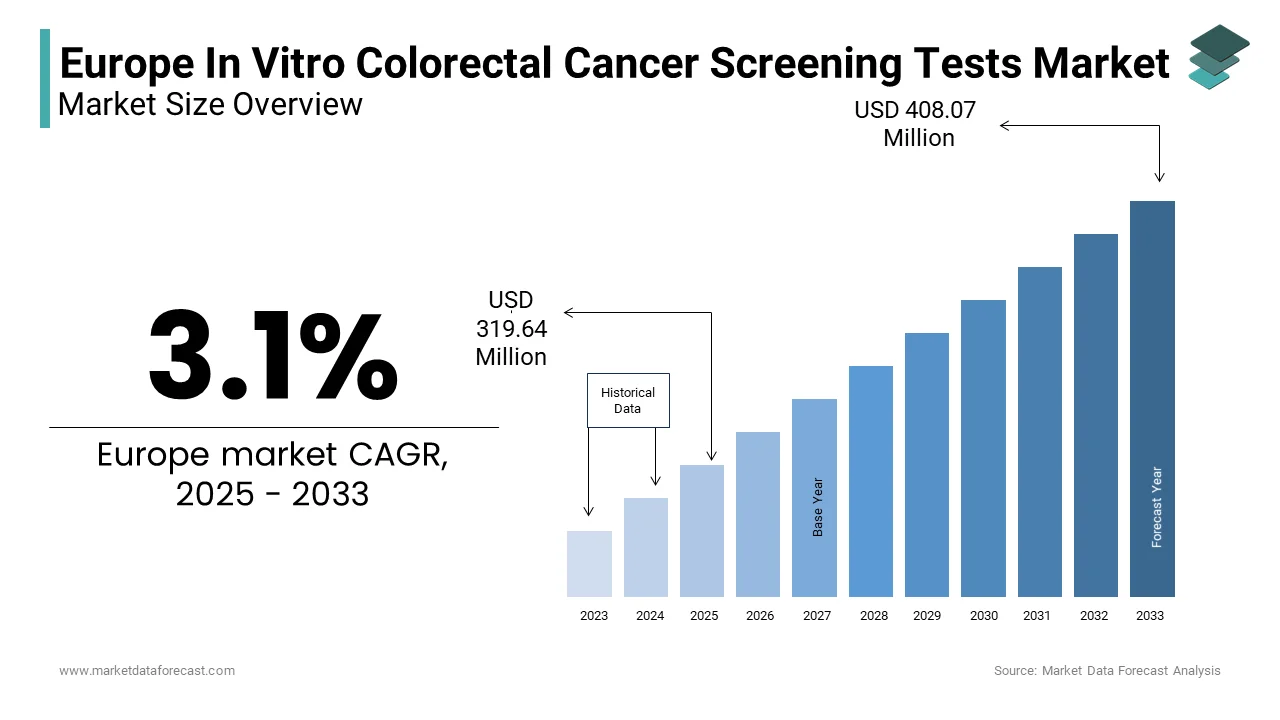

The Europe in vitro colorectal cancer screening tests market Size was valued at USD 310.03 million in 2024. The Europe in vitro colorectal cancer screening tests market size is expected to have 3.1 % CAGR from 2025 to 2033 and be worth USD 408.07 million by 2033 from USD 319.64 million in 2025.

The Europe in vitro colorectal cancer screening tests market has emerged as a critical segment within the broader healthcare diagnostics industry. This growth is driven by rising awareness about early cancer detection and the increasing prevalence of colorectal cancer.

The European Union’s Horizon 2020 program has allocated significant funding to cancer research, including non-invasive diagnostic tools, which has spurred innovation in this sector.

MARKET DRIVERS

Rising Incidence of Colorectal Cancer

The escalating incidence of colorectal cancer serves as a primary driver for the Europe in vitro colorectal cancer screening tests market. According to the World Health Organization (WHO), colorectal cancer ranks as the second most common cancer in Europe, accounting for 13% of all cancer diagnoses. The aging population, coupled with lifestyle factors such as poor diet and sedentary habits, has contributed to an increase in cases over the past decade.

Government-led awareness campaigns, such as the UK’s Bowel Cancer Screening Programme, have significantly boosted test adoption, with participation rates surging high in targeted regions. Also, advancements in early detection technologies have improved survival rates, encouraging more individuals to undergo regular screenings.

Advancements in Diagnostic Technologies

Technological advancements in diagnostic tools are reshaping the Europe in vitro colorectal cancer screening tests market. According to Deloitte, innovations such as next-generation sequencing (NGS) and multiplex biomarker assays have enhanced the sensitivity and specificity of tests, reducing false-positive rates. Companies like Roche Diagnostics have developed non-invasive stool DNA tests that detect genetic mutations linked to colorectal cancer, achieving greater accuracy rate. These advancements have not only improved patient outcomes but also reduced healthcare costs associated with late-stage treatments. Moreover, the integration of AI-driven analytics has streamlined test interpretation, enabling faster and more accurate diagnoses.

MARKET RESTRAINTS

High Costs of Advanced Screening Tests

High costs associated with advanced in vitro colorectal cancer screening tests act as a significant barrier to market growth. This financial burden is further exacerbated by limited reimbursement policies, with only limiter share of EU countries offering full coverage for such tests. In addition, the complexity of these tests often requires specialized equipment and trained personnel, increasing operational expenses for healthcare providers.

Limited Awareness and Stigma Surrounding Screening

Limited awareness and societal stigma surrounding colorectal cancer screening pose another significant restraint. According to the European Cancer Patient Coalition, lower share of eligible adults in Southern and Eastern Europe participate in screening programs, primarily due to cultural taboos and misconceptions about the procedure. A survey revealed that 35% of respondents avoided testing In Europe due to fear of invasive procedures, despite the availability of non-invasive alternatives. This lack of awareness is compounded by insufficient educational campaigns, particularly in underserved regions. Governments and healthcare providers face challenges in dispelling myths and encouraging regular screenings, which limits market penetration and delays early diagnosis.

MARKET OPPORTUNITIES

Expansion of Telemedicine and Remote Diagnostics

The expansion of telemedicine and remote diagnostics presents a transformative opportunity for the Europe in vitro colorectal cancer screening tests market. According to McKinsey, telehealth consultations grew significantly during the pandemic, with patients increasingly opting for home-based diagnostic solutions. Non-invasive tests, such as fecal immunochemical tests (FIT), can be easily administered at home and mailed to laboratories for analysis. This trend aligns with the EU’s Digital Health Strategy, which aims to integrate digital tools into mainstream healthcare. By leveraging telemedicine platforms, companies can reach underserved populations, particularly in rural areas, while reducing operational costs.

Partnerships with Public Health Initiatives

Partnerships with public health initiatives offer a lucrative opportunity for market players to expand their reach and impact. In Europe, collaborative programs between governments and private entities have increased screening participation rates in pilot regions. These partnerships enable companies to access large-scale patient databases, enhancing research capabilities and product development. In Addition, government subsidies for screening programs reduce financial barriers, fostering widespread adoption.

MARKET CHALLENGES

Regulatory Hurdles and Approval Delays

Regulatory hurdles and approval delays pose significant challenges to the Europe in vitro colorectal cancer screening tests market. According to the European Medicines Agency (EMA), the average time required for diagnostic test approval ranges from 12 to 18 months, depending on the complexity of the technology. This lengthy process delays market entry, particularly for innovative products like liquid biopsy kits, which require extensive clinical validation. Besides, varying regulatory standards across EU member states complicate compliance, increasing operational burdens for manufacturers.

Competition from Alternative Screening Methods

Competition from alternative screening methods, such as colonoscopy, poses a significant challenge to the Europe in vitro colorectal cancer screening tests market. According to the European Society of Gastrointestinal Endoscopy, colonoscopy remains the gold standard for colorectal cancer detection, capturing 95% of lesions. However, its invasiveness and high costs deter many patients, creating opportunities for less invasive alternatives. Despite advancements in non-invasive tests, skepticism persists among healthcare providers, with only limited portion of general practitioners recommending FIT or biomarker tests as primary screening tools, as noted by ESMO.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 3.1 % |

| Segments Covered | By Test,End-Use and Country. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, Germany, Italy, France, Spain, Sweden, Denmark, Poland, Switzerland, Netherlands, Rest of Europe. |

| Market Leaders Profiled | Abbott Laboratories, Epigenomics AG, Beckman Coulter, Eiken Chemical Co Ltd |

SEGMENT ANALYSIS

By Test Insights

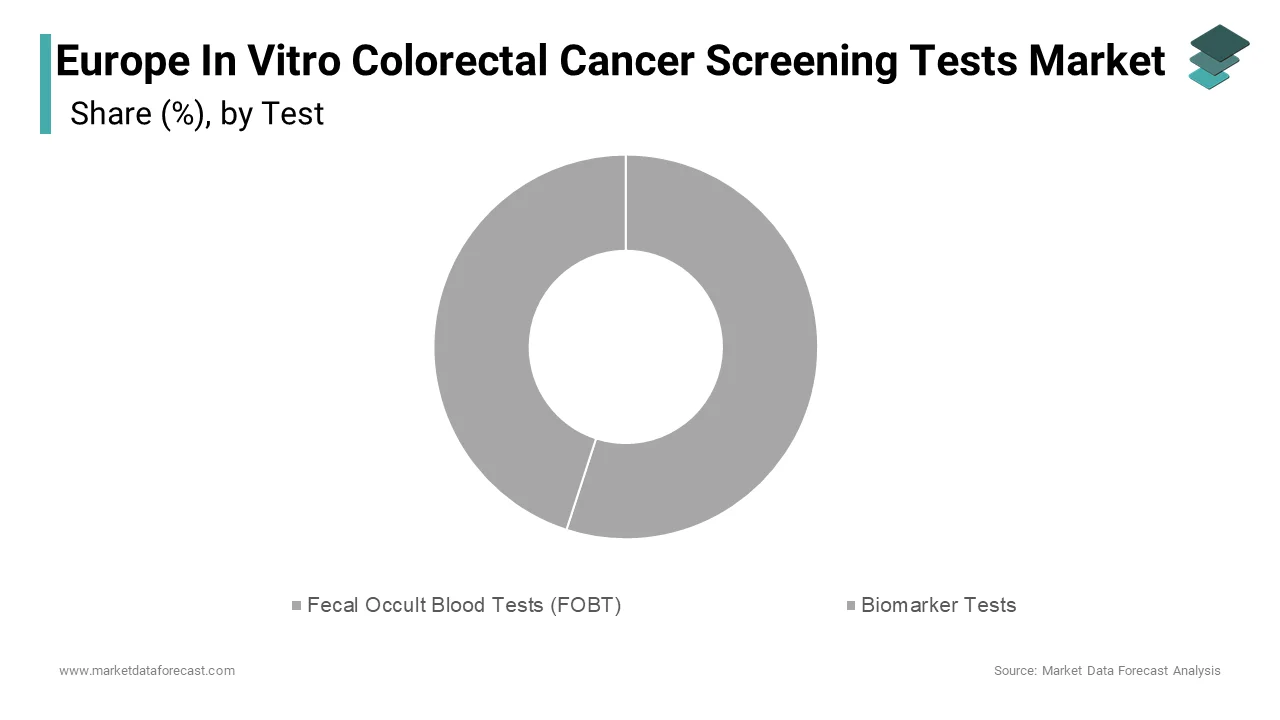

The segment of fecal occult blood tests (FOBT) managed the Europe in vitro colorectal cancer screening tests market by holding a 55.3% share of total revenue in 2024. This dominance is attributed to their affordability and ease of use, making them widely accessible across diverse demographics. The European Colorectal Cancer Screening Guidelines recommend FOBT as a first-line screening tool, driving adoption rates higher in Western Europe, as per Deloitte. Advancements in immunochemical variants, such as FIT, have further solidified their position, improving sensitivity. Moreover, government-led initiatives, such as the UK’s NHS Bowel Cancer Screening Program, have distributed millions of FOBT kits annually, enhancing public trust and compliance.

Biomarker tests are the fastest-growing segment, with a CAGR of 18% from 2025 to 2033. This progress is fueled by their superior accuracy and ability to detect early-stage cancers, with sensitivity rates greater. The rise of personalized medicine has further accelerated adoption, with biomarker tests enabling tailored treatment plans based on genetic profiles. Government investments in precision oncology, such as Germany’s €500 million Precision Medicine Initiative, have catalyzed research and development in this space. Apart from these, partnerships with biotech firms have expanded the availability of advanced biomarker panels, positioning this segment as a transformative force in the European market.

By End-Use Insights

The hospitals and clinics segment ruled the Europe in vitro colorectal cancer screening tests market with 65.7% of total demand in 2024. This prominence is driven by their role as primary healthcare providers, offering comprehensive diagnostic services to a wide patient base. The integration of AI-driven analytics has further enhanced diagnostic capabilities, reducing turnaround times. Additionally, government subsidies for hospital-based screening programs have increased accessibility, particularly in underserved regions.

Diagnostic laboratories are the highest expanding area, with a CAGR of 15%. This rise is caused by the increasing outsourcing of diagnostic services, particularly in urban areas. Advancements in automation and robotics have streamlined operations, reducing costs while enhancing throughput. In addition, collaborations with telemedicine platforms have expanded their reach, enabling remote sample collection and analysis.

COUNTRY LEVEL ANALYSIS

Germany stood as a leader in the Europe in vitro colorectal cancer screening tests market by commanding a 22.3% share of regional demand in 2024. This dominance is driven by a robust healthcare system and proactive government initiatives, such as the nationwide screening program launched in 2019. Additionally, investments in precision medicine have accelerated adoption of advanced biomarker tests, with usage growing annually.

The United Kingdom possessed a significant share of the market, bolstered by its NHS-led screening programs and strong emphasis on preventive healthcare. London and Manchester are key contributors. Government funding for cancer research has further propelled innovation, with non-invasive tests gaining traction.

France continued to be the important player in 2024 and is supported by its proactive public health policies and high healthcare spending. Paris and Lyon are major hubs, contributing to a notable share of the country’s total screenings. The French National Cancer Institute (INCa) highlights that screening participation rates high, driven by extensive awareness campaigns and subsidies. Advancements in telemedicine have further accelerated adoption, with remote diagnostics gaining popularity.

Italy commands a key position in the market which is driven by its aging population and high cancer incidence rates, according to Accenture. Milan and Rome are key contributors. Government-led initiatives have increased participation rates by 25%, as noted by the Italian Ministry of Health. The adoption of advanced biomarker tests has gained momentum, with usage growing.

Spain is supported by its expanding healthcare infrastructure and rising awareness about early cancer detection . Barcelona and Madrid are key contributors, accounting for major share of the country’s total screenings. Government investments in precision oncology have further accelerated adoption of advanced tests, positioning Spain as a resilient player in the European market.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the Europe in vitro colorectal cancer screening tests market are Abbott Laboratories, Epigenomics AG, Beckman Coulter, Eiken Chemical Co Ltd, Sysmex Corp, Siemens Healthineers AG ADR, Quest Diagnostics Inc, OncoCyte Corp, Merck KGaA, Kyowa Kirin Co Ltd, R-Biopharm, Immunostics, Randox

The Europe in vitro colorectal cancer screening tests market is characterized by intense competition, with established players vying for dominance amid rapid technological advancements. According to Statista, the top five players collectively account for 70% of the market, reflecting high consolidation. However, the rise of niche players specializing in precision diagnostics is disrupting traditional models.

Regulatory pressures, particularly around accuracy and compliance, are reshaping competitive dynamics. Companies that fail to innovate risk losing market share to agile competitors. Additionally, the proliferation of AI-driven solutions and telemedicine platforms is leveling the playing field, enabling smaller firms to compete effectively. These factors highlight the complexity of the competitive landscape.

Top Players in the Market

Roche Diagnostics

Roche Diagnostics is a global leader in the in vitro colorectal cancer screening tests market, renowned for its innovative diagnostic solutions. The company’s Cobas platform offers highly sensitive biomarker tests, enabling early detection of colorectal cancer with high accuracy. Roche’s focus on precision medicine has led to the development of personalized screening tools, aligning with EU healthcare goals.

Abbott Laboratories

Abbott Laboratories plays a pivotal role in the market, offering affordable and reliable screening solutions. Its Alinity platform integrates advanced automation, reducing turnaround times. Abbott’s strategic partnerships with healthcare providers have strengthened its presence across Europe, ensuring widespread accessibility.

Sysmex Corporation

Sysmex Corporation is a prominent player in the market, known for its cutting-edge diagnostic technologies. The company’s XN-Series analyzers provide rapid and accurate results, enhancing operational efficiency. Sysmex’s collaboration with public health initiatives has expanded its reach, contributing to regional screening goals.

RECENT HAPPENINGS IN THE MARKET

In March 2023, Roche Diagnostics launched its new biomarker panel in Munich, Germany. This initiative aimed to improve early detection rates by integrating genetic profiling into routine screenings.

In June 2023, Abbott Laboratories partnered with a Spanish telemedicine startup, MedScreen. This collaboration sought to expand remote diagnostic capabilities for rural populations.

In September 2023, Sysmex Corporation introduced its AI-driven analytics platform in Paris, France. This move aimed to streamline test interpretation and enhance accuracy.

In November 2023, Siemens Healthineers acquired a German biotech firm specializing in liquid biopsy kits. This acquisition aimed to strengthen its portfolio of non-invasive screening solutions.

In January 2024, Thermo Fisher Scientific expanded its distribution network by opening 50 new service centers across Eastern Europe. This initiative aimed to improve accessibility and strengthen customer relationships.

MARKET SEGMENTATION

This research report on the europe in vitro colorectal cancer screening tests market has been segmented and sub-segmented into the following categories.

By Test

- Fecal Occult Blood Tests (FOBT)

- Biomarker Tests

By End-Use

- Hospitals & Clinics

- Diagnostic Laboratories

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe.

Frequently Asked Questions

What is driving the growth of the in vitro colorectal cancer screening market in Europe?

Key drivers include: Rising incidence of colorectal cancer Government initiatives for early detection Technological advancements in non-invasive testing

Which countries in Europe are leading in the adoption of these tests?

Countries with robust healthcare systems and national screening programs, such as Germany, the UK, France, Italy, and the Netherlands, are leading in adoption.

Who are the key players in the European in vitro colorectal cancer screening market?

Major companies include: Exact Sciences Corporation Epigenomics AG Abbott Laboratories QuidelOrtho Corporation Sysmex Corporation

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com